1 aaa annual meeting 2015 economic consequences of ifrs adoption in korea : a review of literature...

TRANSCRIPT

/ 1

AAA Annual Meeting AAA Annual Meeting 20152015

Economic Consequences of IFRS Adoption in Economic Consequences of IFRS Adoption in KoreaKorea: A Review of Literature: A Review of Literature

August, 2015 Jee In Jang

Korean Accounting Standard Board

/ 2

ContentContentss

I. IntroductionI. Introduction

ⅡⅡ. Background. Background

ⅢⅢ. A Review of Literature. A Review of Literature

ⅣⅣ. Concluding Remarks. Concluding Remarks

/ 3

I. IntroductionI. Introduction

/ 4

Motivation of this researchMotivation of this research

In 2007, Korean government announced its Roadmap for IFRS adoption and decided to fully adopt IFRS beginning from 2011, allowing voluntary early-adoption from 2009

1. To improve the accounting transparency of Korean entities; 2. To demonstrate Korea’s strong will to take part in the international movement towards a single set of high-quality global accounting standards

/ 5

ⅡⅡ. Background. Background

01. The IFRS Adoption Process in Korea01. The IFRS Adoption Process in Korea

02. Difference Between IFRS and K-GAAP02. Difference Between IFRS and K-GAAP

03. Distinctive Features of IFRS Adoption in 03. Distinctive Features of IFRS Adoption in KoreaKorea

/ 6

01. The IFRS Adoption Process in 01. The IFRS Adoption Process in KoreaKorea

Early Adoption Period Full Adoption Period

2009 2010 2011 2014

Mandatory Adoption - - 1,709 1,824

Voluntary Adoption 33 152 1,142 2,054

Total 33 152 2,851 3,878*

* 17.2% of externally audited entities by law(as of December, 2014)

/ 7

K-GAAP IFRS Expected Changes

• Rule-based accounting standards

• Principle-based accounting standards

• Increased discretion by management

• Separate financial statements as primary financial statements

• Consolidated financial statements as primary financial statements

• Enhanced comparability and value relevance

• Book value accounting with acquisition cost basis

• Expansion of the scope of fair value accounting

• Increased use of fair value measurement

• Relatively less detailed disclosures in notes

• Detailed disclosures in notes

• Improvement in quality and quantity of disclosures in notes

02. Difference Between IFRS and K-02. Difference Between IFRS and K-GAAPGAAP

/ 8

03. Distinctive Features of IFRS Adoption in 03. Distinctive Features of IFRS Adoption in KoreaKorea

11• Big difference between K-GAAP and IFRS• The effects of IFRS adoption would be more clearly observed (Bae. Et al. 2008)

22

33

Korean accounting culture is different from member countries of the Commonwealth.

Korea fully adopted IFRS with a Big-Bang approach and no ‘carve-outs’

‘Rule-based’ Korean accounting standards (K-GAAP) → ‘Principle-based’ IFRS.

• The ‘Big-Bang’ approach was employed instead of the ‘phase-in’ or ‘convergence’ approach.

• It may take a significant amount of time for IFRS adoption to have economic effects in Korea.

• Hofstede(1980); one of the most uncertainty avoiding countries in the world.• Legal system; code law country.

• ‘Mandatory adoption of IFRS ‘(for all listed companies and financial institutions)

• K-IFRS: translated version of IFRS without ‘carve-outs’.

/ 9

ⅢⅢ. A Review of Literature. A Review of Literature

01. Earnings Quality01. Earnings Quality

02. Comparability of Financial Statements02. Comparability of Financial Statements

03. Value Relevance03. Value Relevance

04. Analysts Behavior04. Analysts Behavior

05. Information Asymmetry05. Information Asymmetry

06. Cost of Equity Capital and Firm Value06. Cost of Equity Capital and Firm Value

/ 10

* We focus on accounting literature published in leading accounting journals in Korea: - Korean Accounting Review - Korean Accounting Journal - Accounting, Tax & Auditing Research - Selected Korean Accounting Association conference papers

(1) Earnings quality

(2) Comparability

of financial statements

(3)Value

relevance

(4)Analysts’ behavior

(5)Information asymmetry

(6)Cost of

capital firm value

• 18 empirical studies on the economic consequences of IFRS adoption in Korea

Six areas

/ 11

01. Earnings Quality01. Earnings Quality

Empirical findings Implications & Future researchImprovements in earnings quality:Improvements in earnings quality:

• Decrease in discretionary accruals (DA)• This effect is enhanced in firms - with additional abnormal audit hours (Park et al. 2012) - with Non-Big4 auditors (Kim 2014)• Decrease in DA in separate F/S while increase in DA in consolidated F/S (Jeong 2013)

• Due to the relatively large difference between K-GAAP and IFRS, earnings quality tends to be enhanced after IFRS adoption

• Future research: Why does increase in DA in consolidated F/S? - Use different proxy for earnings quality (eg: real activities manipulation, book and tax income difference)

Choe and Son (2012); Park et al. (2012); Jeong (2013); Kim (2014); Yu and Cha (2014)

Does the adoption of IFRS affect earnings quality?

/ 12

02. Comparability of Financial 02. Comparability of Financial StatementsStatements

Empirical findings Implications & Future researchMixed results:Mixed results:

• Reduced comparability due to the lack of standards on disclosure of operating income; while improved comparability after the KASB requirement of operating income (Cheon and Ha 2011; Lee et al. 2012)• Improved comparability in post-IFRS adoption period (Choi et al. 2013)

• No definition and requirement for disclosure of ‘operating profit or loss’ in IFRS

• The amendments to K-IFRS 1001 (equivalent to IAS1 ) in 2012 - Mandatory disclosure of ‘operating profit or loss’ and define as an amount of sales minus cost of sales and selling and administrative expenses

• Future research - Use different model suggested by Cascino and Gassen (2015) to control for the endogeneity problem

Cheon and Ha (2011); Lee at al. (2012); Choi et al. (2013)

Does the adoption of IFRS affect financial statement comparability?

/ 13

03. Value Relevance03. Value Relevance

Empirical findings Implications & Future researchMixed results:Mixed results:

• No significant difference in value relevance of both book value of equity and net income under K-GAAP and IFRS (Choi 2013)

• Value relevance of NI: IFRS > K-GAAP Value relevance of BVE: IFRS < K-GAAP (Choi et al. 2013)

• Future research Why the improvement in earnings quality does not result in the increase in value relevance?

- short test periods (1 year: 2010, 2011) and the omitted variables problem - need to use longer periods (5-10 years) in the analysis

Choi (2013); Choi et al (2013); Kim et al. (2014)

Does the adoption of IFRS affect value relevance of accounting information?

/ 14

04. Analysts Behavior04. Analysts Behavior

Empirical findings Implications & Future researchEnhanced information environment Enhanced information environment for analysts:for analysts:

• Decrease in both analysts’ forecasts error and their variance (Yu and Cha 2014)

• Analysts provide more accurate earnings forecasts for the firms with asset revaluation under IFRS (Choe and Son 2011)

• The results suggest that financial analysts

cope effectively with the transition to IFRS

• Future research - Investigate the differences in forecast accuracy between domestic and foreign analysts after IFRS adoption

Choe and Son (2011); Yu and Cha (2014)

Does the adoption of IFRS affect financial analysts’ forecast accuracy?

/ 15

05. Information Asymmetry05. Information Asymmetry

Empirical findings Implications & Future researchDecrease in information Decrease in information asymmetry: asymmetry:

• Decrease in the standard deviation of daily stock returns (Kim and Cho 2014)

• Decrease in stock price synchronicity (Shin and Choi 2014)

• Report consistent empirical evidence that information asymmetry decreases following IFRS adoption

• Future research - Use longer test periods - analyze information asymmetry issue using different model(eg. ACCRSQ model) by Frankel et al. (2006)

Shin and Choi (2014); Kim and Cho (2014)

Does the adoption of IFRS affect information asymmetry?

/ 16

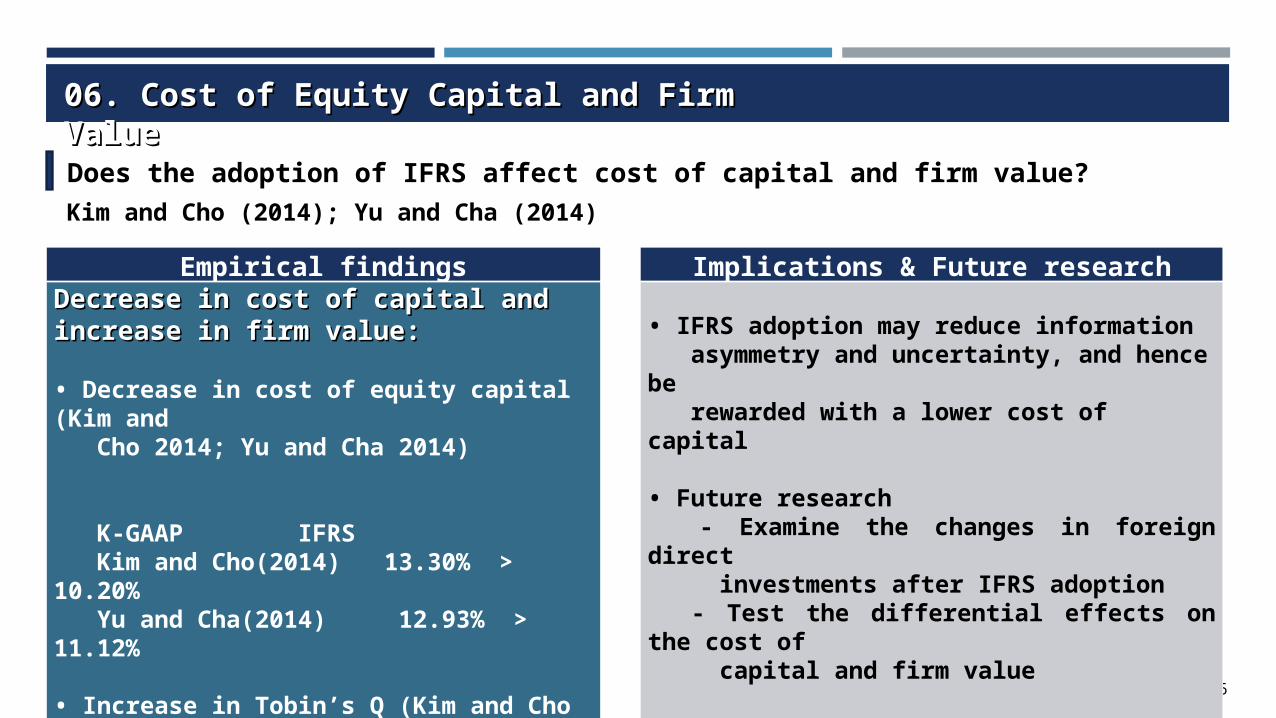

06. Cost of Equity Capital and Firm 06. Cost of Equity Capital and Firm ValueValue

Empirical findings Implications & Future researchDecrease in cost of capital and Decrease in cost of capital and increase in firm value:increase in firm value:

• Decrease in cost of equity capital (Kim and Cho 2014; Yu and Cha 2014)

K-GAAP IFRS Kim and Cho(2014) 13.30% > 10.20% Yu and Cha(2014) 12.93% > 11.12%

• Increase in Tobin’s Q (Kim and Cho 2014)

• IFRS adoption may reduce information asymmetry and uncertainty, and hence be rewarded with a lower cost of capital

• Future research - Examine the changes in foreign direct investments after IFRS adoption - Test the differential effects on the cost of capital and firm value

Kim and Cho (2014); Yu and Cha (2014)

Does the adoption of IFRS affect cost of capital and firm value?

/ 17

ⅣⅣ. Concluding Remarks. Concluding Remarks

/ 18

Summary & Suggestions for future researchSummary & Suggestions for future research

Overall, Korean studies provide evidence that IFRS adoption has led to improvements in financial reporting and accounting environment and plays a positive role in Korean capital market.

• Research results on economic consequences of IFRS adoption in Korea would provide useful insights to countries considering or in the process of adopting IFRS, especially countries with similar institutional environment to Korea.• Future research - to address national characteristics and the different effects of IFRS adoption (eg: legal tradition, accounting quality in pre IFRS, legal enforcement, importance of capital markets, difference between GAAP and IFRS) - to investigate changes in home bias after IFRS adoption - to investigate effects of translation risk

/ 19

Thank youThank you