2011 johns hopkins bloomberg school of public health best practices in tobacco taxation frank j....

TRANSCRIPT

2011 Johns Hopkins Bloomberg School of Public Health

Best Practices in Tobacco TaxationBest Practices in Tobacco Taxation

Frank J. Chaloupka, PhDUniversity of Illinois at ChicagoInternational Tobacco Evidence Network

2011 Johns Hopkins Bloomberg School of Public Health

Overview

Tobacco tax structure

Tobacco tax levels and tax increases

Tobacco tax administration

Economic impact of tax increases—myths and facts

2

Image source: World Health Organization. (2010).

2011 Johns Hopkins Bloomberg School of Public Health

Best Practices: Why Tax Tobacco?

Use tobacco excise tax increases to achieve the public health goal of reducing the death and disease caused by tobacco use As called for

in Article 6 of the FCTC

Additional benefitof generating significant increases intobacco tax revenues in short- to medium-term

3

Source: Jha, P. (2009).

2011 Johns Hopkins Bloomberg School of Public Health

Best Practices: What Type of Tax Structure?

Simpler tax structure is better Complex tax

structures are more difficult to administer

Complex tax structures create more opportunities for tax evasion and tax avoidance

Where existing tax structure is more complex, aim to simplify over time with goal of achieving a single uniform tax

4

Differential/tiered excise taxes on cigarettes

Number of countries

Total covered 156

With tiers 32

Base of tiers Retail price Producer price Sales volume Production volume Type—filter/non-filter Type—hand-/machine-made Type—kretek/white cigarette Packaging—soft/hard Cigarette length Trade—domestic/imported Weight (tobacco content in cigarette) Leaf content—domestic/imported

11211

122134113

Of the 155 countries with available data in TMA, 10 countries have no excise. Some countries differentiate based on more than one criterion. Eight countries differentiate their excises by more than one criterion.

2011 Johns Hopkins Bloomberg School of Public Health

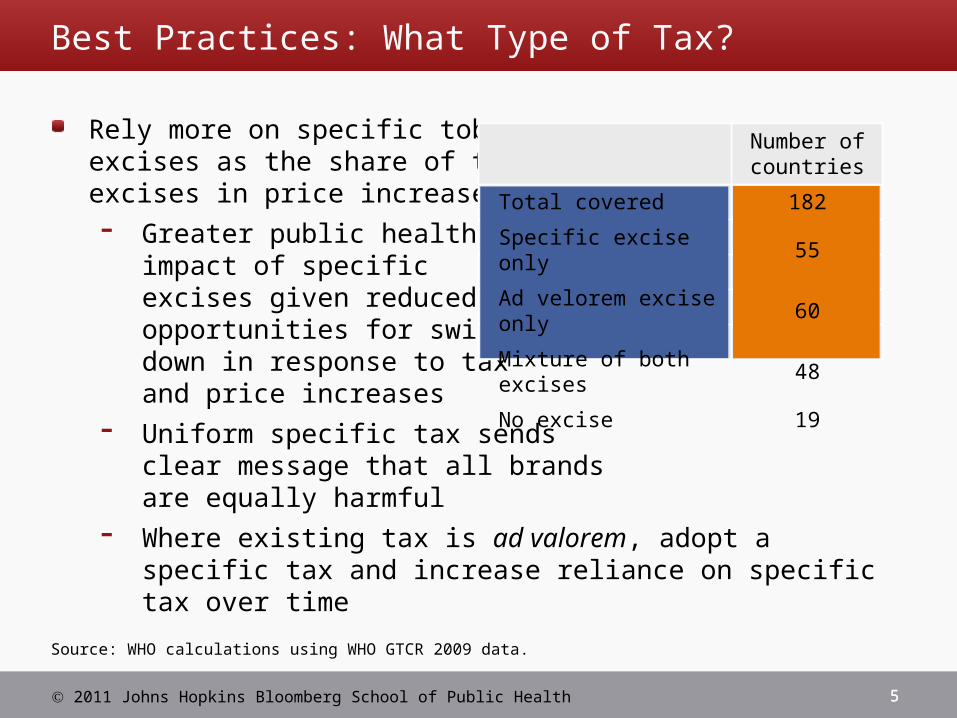

Best Practices: What Type of Tax?

Rely more on specific tobacco excises as the share of total excises in price increases Greater public health

impact of specific excises given reduced opportunities for switching down in response to tax and price increases

Uniform specific tax sends clear message that all brands are equally harmful

Where existing tax is ad valorem, adopt a specific tax and increase reliance on specific tax over time

55

Source: WHO calculations using WHO GTCR 2009 data.

Number of countries

Total covered 182

Specific excise only 55

Ad velorem excise only

60

Mixture of both excises

48

No excise 19

2011 Johns Hopkins Bloomberg School of Public Health

Best Practices: Taxes on Different Products

Adopt comparable taxes and tax increases on all tobacco products Maximizes the public health

impact of tobacco taxes and tax increases by minimizing opportunities for substitution between tobacco products in response to changes in relative prices

Challenging where diverse products available

6

2011 Johns Hopkins Bloomberg School of Public Health

Best Practices: Adjust Taxes for Inflation

Automatically adjust specific taxes for inflation Unless adjusted

regularly, real value of tax fallsover time, as do the revenues generated by the tax

Ensures that the publichealth impact of the tax is maintained

Currently done in Australia, New Zealand

7

2011 Johns Hopkins Bloomberg School of Public Health

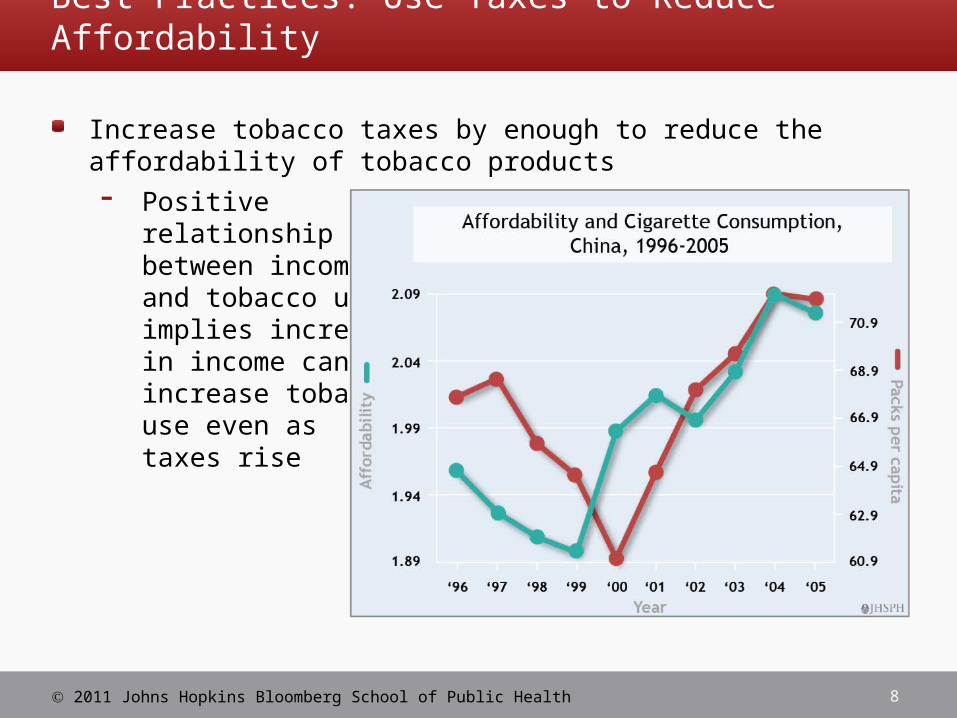

Best Practices: Use Taxes to Reduce Affordability

Increase tobacco taxes by enough to reduce the affordability of tobacco products Positive

relationship between income and tobacco use implies increases in income can increase tobaccouse even as taxes rise

8

2011 Johns Hopkins Bloomberg School of Public Health

Best Practices: Increase taxes

Set tobacco excise tax levels so that they account for at least 70% of the retail prices of tobacco products Update of the

World Bank’s 2/3-4/5 yardstick

Well above where most countries are currently

Further increase in countries that have reached target

9

2011 Johns Hopkins Bloomberg School of Public Health

Best Practices: Tax Administration

Eliminate tax or duty-free sales of tobacco products As called for in Article 6 of FCTC Reduces opportunities for

individual tax avoidance Maximizes the public health

and revenue impact of taxes

Adopt new technologies to strengthen tobacco tax administration and minimize tax avoidance and evasion Apply new, sophisticated tax stamps (banderoles) Adopt tracking and tracing technology Adopt production monitoring technologies

10

2011 Johns Hopkins Bloomberg School of Public Health

Best Practices: Tax Administration

Strengthen tax administrators’ capacity by licensing all involved in tobacco product manufacturing, distribution, and sales Facilitates identification of those engaged in illicit trade Enhances ability to penalize those engaged in illicit

trade through suspension or revocation of license

Ensure certain, swift, and severe penalties for those caught engaging in illicit trade in tobacco products Increases the expected costs of engaging in illicit trade Strong, administrative sanctions coupled with licensing

and tracking/tracing systems

11

2011 Johns Hopkins Bloomberg School of Public Health

Best Practices: Tax Administration

Strengthen tax administrators’ capacity to monitor tobacco product markets and evaluate the impact of tobacco tax increases “Trust but verify” Monitoring of tobacco production and distribution Physical controls over tobacco products Periodic audits Capacity to estimate the impact of tobacco tax changes

on tobacco product consumption and revenues

12

2011 Johns Hopkins Bloomberg School of Public Health

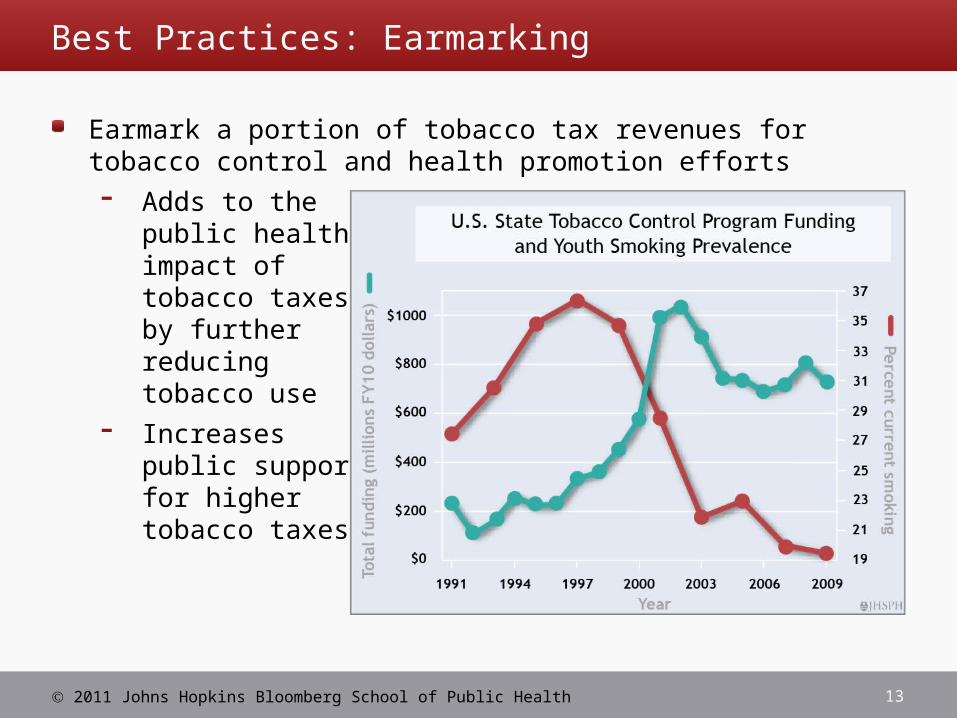

Best Practices: Earmarking

Earmark a portion of tobacco tax revenues for tobacco control and health promotion efforts Adds to the

public healthimpact of tobacco taxes by further reducing tobacco use

Increases public support for higher tobacco taxes

13

2011 Johns Hopkins Bloomberg School of Public Health

Best Practices: Economic Impact—Myths and Facts

Do not allow concerns about job losses to prevent tobacco tax increases Tobacco employment often declining even where

tobacco product consumption is rising Tax-induced reductions in tobacco-dependent

employment are offset by increases in other sectors Where concerns are significant, use tax revenues to

support the transition from tobacco farming and manufacturing to alternative livelihoods

14

2011 Johns Hopkins Bloomberg School of Public Health

Best Practices: Economic Impact—Myths and Facts

Do not allow concerns about the inflation impact of higher tobacco taxes to deter tax increase Tobacco tax increases have minimal impact on inflation

in most countries If concerns about inflationary impact on pension and

other payments tied to consumer price index, use a price index that excludes tobacco products

15

2011 Johns Hopkins Bloomberg School of Public Health

Best Practices: Economic Impact—Myths and Facts

Do not view low taxes and prices for some tobacco products as a “Pro Poor” policy High tobacco taxes on all tobacco products will result in

greater reductions in tobacco use among the poor Resulting reductions in use lead to a progressive

distribution of the health and economic benefits that result from tax increase—truly a “Pro Poor” policy

16

2011 Johns Hopkins Bloomberg School of Public Health

Best Practices: Economic Impact—Myths and Facts

Do not allow concerns about the regressivity of higher tobacco taxes to prevent tax increases Regressive impact often overstated In many countries, tax increase can reduce regressivity

given greater reductions in use among the poor Concerns about the impact on the poor can be offset by

using some of the new revenues to support efforts to help poor users quit, health promotion efforts targeting the poor, and/or poverty alleviation programs

17

2011 Johns Hopkins Bloomberg School of Public Health

Best Practices in Tobacco Taxation

A simpler tobacco tax structure that taxes all tobacco products equivalently and relies more on specific taxes will have a greater impact in reducing tobacco use and its consequences

Effective tobacco tax administration includes regularly increasing taxes with inflation and income growth so as to reduce the affordability of tobacco products

18

2011 Johns Hopkins Bloomberg School of Public Health

Best Practices in Tobacco Taxation

Strong tobacco tax administration is effective in reducing tax avoidance and tax evasion

Governments should not be deterred from raising tobacco taxes by the misleading arguments used in opposition to tax increases

Raise tobacco excise taxes so that they account for 70% of the retail prices of tobacco products

19