© 2012 deloitte llp. private and confidential. fatca update for individuals alex jones november...

TRANSCRIPT

© 2012 Deloitte LLP. Private and confidential.

FATCA Update for Individuals

Alex Jones November 2013

© 2012 Deloitte LLP. Private and confidential.2

FATCA, Form 8938 and Medicare Practical Issues

© 2012 Deloitte LLP. Private and confidential.3

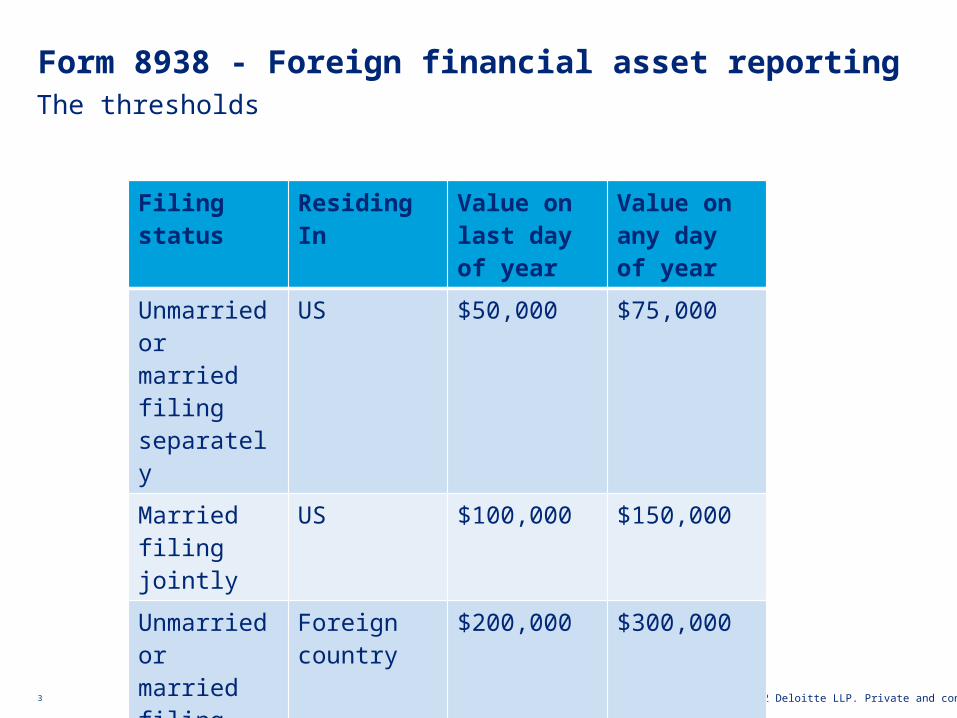

Form 8938 - Foreign financial asset reportingThe thresholds

Filing status

Residing In Value on last day of year

Value on any day of year

Unmarried or married filing separately

US $50,000 $75,000

Married filing jointly

US $100,000 $150,000

Unmarried or married filing separately

Foreign country

$200,000 $300,000

Married filing jointly

Foreign country

$400,000 $600,000

© 2012 Deloitte LLP. Private and confidential.4

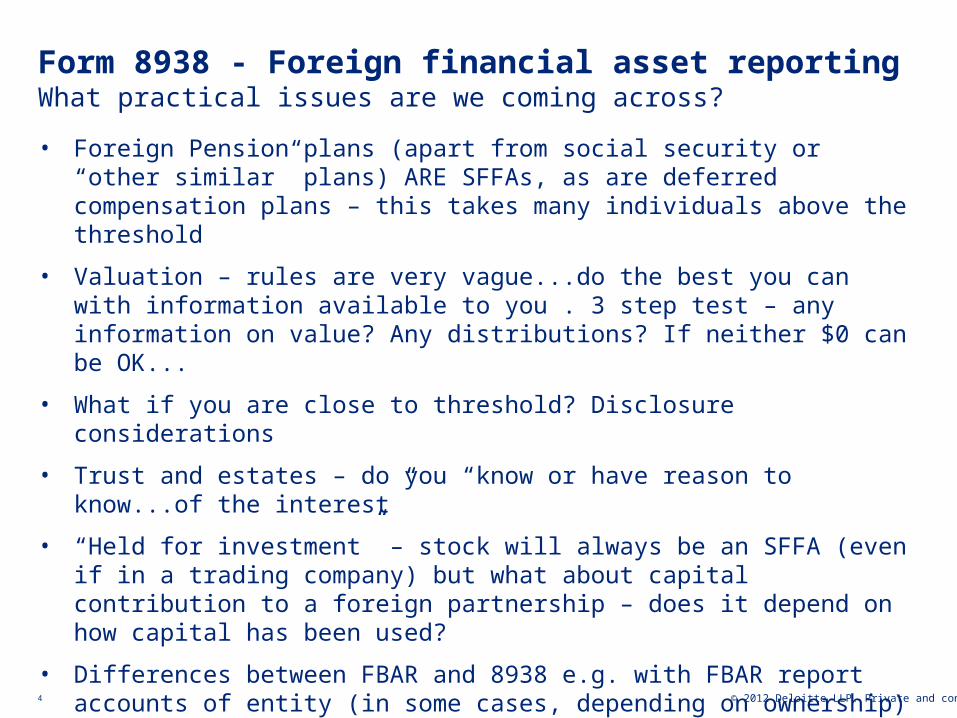

Form 8938 - Foreign financial asset reportingWhat practical issues are we coming across?

• Foreign Pension plans (apart from social security or “other similar” plans) ARE SFFAs, as are deferred compensation plans – this takes many individuals above the threshold

• Valuation – rules are very vague...do the best you can with information available to you . 3 step test – any information on value? Any distributions? If neither $0 can be OK...

• What if you are close to threshold? Disclosure considerations

• Trust and estates – do you “know or have reason to know...of the interest”

• “Held for investment” – stock will always be an SFFA (even if in a trading company) but what about capital contribution to a foreign partnership – does it depend on how capital has been used?

• Differences between FBAR and 8938 e.g. with FBAR report accounts of entity (in some cases, depending on ownership) with 8938, report entity

• If in doubt - report??

• Penalties – we have seen some recently for FBARs

© 2012 Deloitte LLP. Private and confidential.5

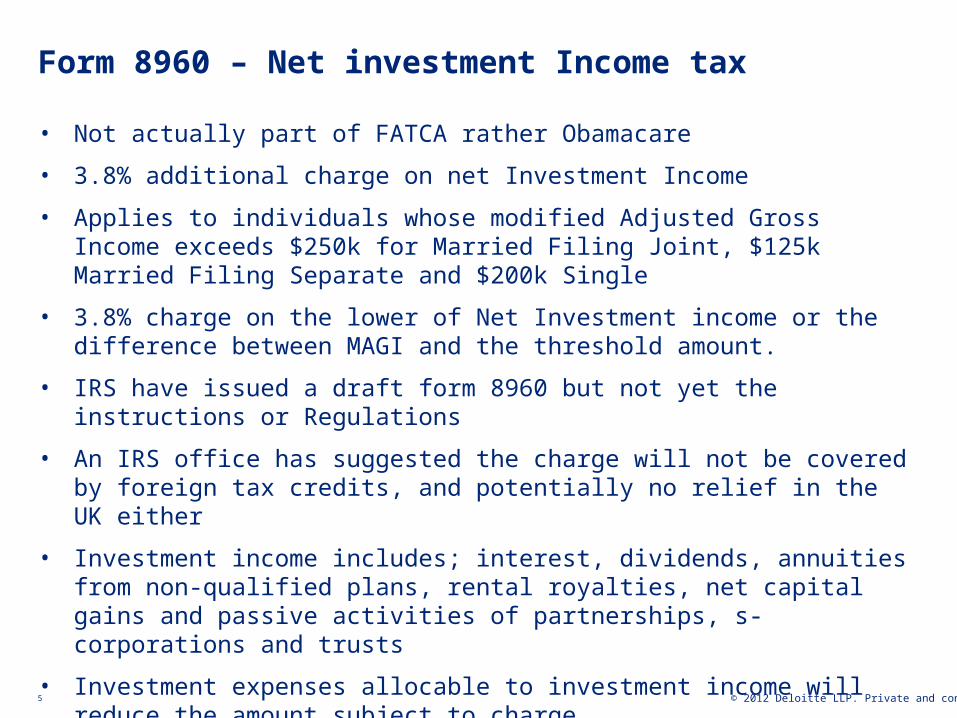

Form 8960 – Net investment Income tax

• Not actually part of FATCA rather Obamacare

• 3.8% additional charge on net Investment Income

• Applies to individuals whose modified Adjusted Gross Income exceeds $250k for Married Filing Joint, $125k Married Filing Separate and $200k Single

• 3.8% charge on the lower of Net Investment income or the difference between MAGI and the threshold amount.

• IRS have issued a draft form 8960 but not yet the instructions or Regulations

• An IRS office has suggested the charge will not be covered by foreign tax credits, and potentially no relief in the UK either

• Investment income includes; interest, dividends, annuities from non-qualified plans, rental royalties, net capital gains and passive activities of partnerships, s-corporations and trusts

• Investment expenses allocable to investment income will reduce the amount subject to charge.

• Question whether the charge applies to the growth in UK pension plans.

© 2012 Deloitte LLP. Private and confidential.6

Questions?

© 2012 Deloitte LLP. Private and confidential.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.co.uk/about for a detailed description of the legal structure of DTTL and its member firms.

Deloitte LLP is the United Kingdom member firm of DTTL.

This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will depend upon the particular circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of the contents of this publication. Deloitte LLP would be pleased to advise readers on how to apply the principles set out in this publication to their specific circumstances. Deloitte LLP accepts no duty of care or liability for any loss occasioned to any person acting or refraining from action as a result of any material in this publication.

Deloitte LLP is a limited liability partnership registered in England and Wales with registered number OC303675 and its registered office at 2 New Street Square, London EC4A 3BZ, United Kingdom. Tel: +44 (0) 20 7936 3000 Fax: +44 (0) 20 7583 1198.

© 2013 Deloitte LLP. All rights reserved.

Member of Deloitte Touche Tohmatsu Limited7