© 2014 fair isaac corporation. confidential. this presentation is provided for the recipient only...

TRANSCRIPT

© 2014 Fair Isaac Corporation. Confidential. This presentation is provided for the recipient only and cannot be reproduced or shared without Fair Isaac Corporation’s express consent.

Compete and Win with Technology Driven Loan Lifecycle Management

Todd ClassenVice President Strategic Accounts,WebEquity Solutions

David SmithConsultingFICO

Agenda

© 2014 Fair Isaac Corporation. Confidential.

►Introductions

►Two Primary Themes►Loan Lifecycle Management►Technology—Helps Community And Midsized

Banks Compete

►Along the Journey: Bust a few Myths

2

© 2014 Fair Isaac Corporation. Confidential.

Why Is This So Important Now?

3

© 2014 Fair Isaac Corporation. Confidential.4

How does Loan Lifecycle Management technology assist with customer growth and retention?

►Helps streamline loan processes► More efficiencies for new loans, renewals, and reviews► Reduce bottlenecks so priority decisions/customers can be treated as such► Can provide better management of covenants, ticklers, and communications

►Provides better analysis and data► More effective decisions, often in a much quicker timeline► Data can lead to better understanding of the customer and cross-sell opportunities

►Allows Relationship Managers more time to focus on relationships

Loan Lifecycle Management

© 2014 Fair Isaac Corporation. Confidential.

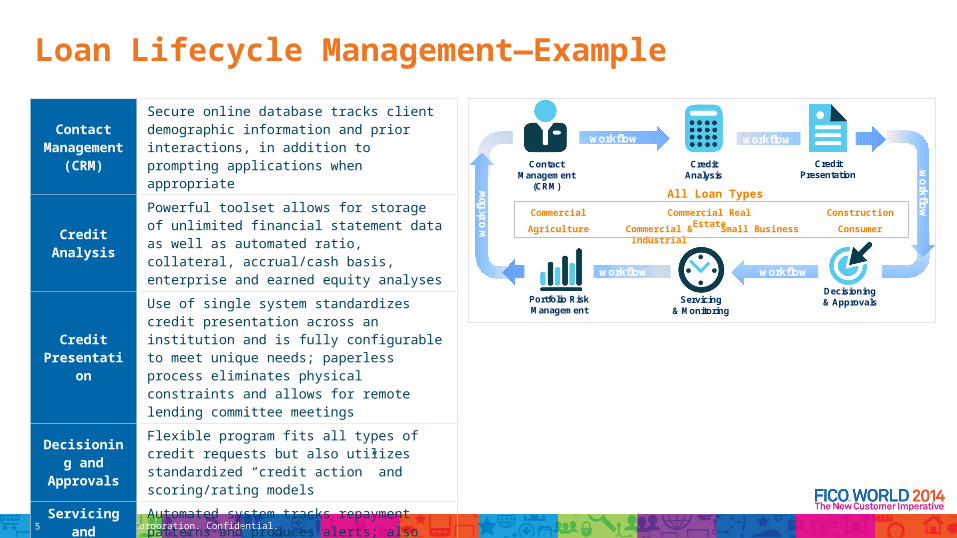

Loan Lifecycle Management—Example

workflow

wo

rkflo

w

workflowworkflow

wo

rkfl

ow

workflow

Servicing& Monitoring

CreditAnalysis

Decisioning& ApprovalsPortfolio Risk

Management

Contact Management

(CRM)

CreditPresentation

Contact Management

(CRM)

Secure online database tracks client demographic information and prior interactions, in addition to prompting applications when appropriate

Credit Analysis

Powerful toolset allows for storage of unlimited financial statement data as well as automated ratio, collateral, accrual/cash basis, enterprise and earned equity analyses

Credit Presentation

Use of single system standardizes credit presentation across an institution and is fully configurable to meet unique needs; paperless process eliminates physical constraints and allows for remote lending committee meetings

Decisioning and

Approvals

Flexible program fits all types of credit requests but also utilizes standardized “credit action” and scoring/rating models

Servicing and

Monitoring

Automated system tracks repayment patterns and produces alerts; also checks insurance and UCC filings

Portfolio Risk Management

Intuitive risk management toolset allows user to shock/stress test a single loan, a pool of loans, or an entire portfolio, as well as identify weaknesses and generate ad hoc reports

All Loan Types

Commercial Commercial Real Estate Construction

Commercial & IndustrialAgriculture Small Business Consumer

5

© 2014 Fair Isaac Corporation. Confidential.6

Scoring and Analytics

►The Myth: Use of scores and auto-decisioning doesn’t work in a relationship banking environment

© 2014 Fair Isaac Corporation. Confidential.7

►The Myth: Use of scores and auto-decisioning doesn’t work in a relationship banking environment► Business Development leaders fear reducing long-term relationships to a score

► Loan Underwriters fear becoming obsolete

► Risk Officers fear becoming reliant on a score

Scoring and Analytics

© 2014 Fair Isaac Corporation. Confidential.8

►In reality, the use of models will enhance relationships► Creates a more transparent and consistent relationship

► Treatment doesn’t change with change in personnel

► Enables Business Development groups to be proactive with high-scoring customers► Can say YES more quickly by auto-decisioning the A+ relationships► Possibly bypass application paperwork with A+ customers

► Provides performance improving strategies for low-performing customers► Reason codes point to areas of improvement► Allows the institution to educate marginal customers

Scoring and Analytics: Relationship Banking and Scoring

© 2014 Fair Isaac Corporation. Confidential.9

►The loan strategy that is automated is the intellectual property of the institution’s underwriters

►Policies and strategies have to be followed regardless

►Removes work from an underwriter’s desk—eliminates the easy decisions and leaves the difficult to decision

Scoring and Analytics: Supports Underwriting

High

Segment Applicant Population

LowMedium

AutomatedDecline

AutomatedAccept

© 2014 Fair Isaac Corporation. Confidential.10

►The score should never be the ONLY factor in a decision, automated or not► Bank policy and strategies should always be evaluated

►Overrides should include a valid business reason► Underwriters should point to data points to support the request

►Overrides should be tracked and reported► Reason codes should be defined

►Overrides should support business goals

Scoring and Analytics: Overrides and Score Reliance

© 2014 Fair Isaac Corporation. Confidential.11

►Customer #1:► $14B loan portfolio/mostly scored► The score is not the only factor: “Don’t check your brain at the door.”► However, remember the value of the score…

►Customer #2:► Original solution need/focus was to better service large C&I and CRE deals

Loan Lifecycle Management—Customer Stories

“74% of the bad accounts in our scored portfolio are where the underwriter overrode the suggested decision of the scorecard.”

“Serving small business borrowers requires speed and objectivity. Using WebEquity with the FICO SBSS scoring enabled us to cut our underwriting time from 2 days to 2 hours, and we significantly decreased early delinquencies. We’re winning more business, much more efficiently.”

© 2014 Fair Isaac Corporation. Confidential.12

Technology—Modernization Drivers for Banks

Technology Drivers

Revenue Growth Efficiency Improvement

RegulationsWorkforce

OptimizationArchitectural

Simplicity

Drivers for Modernization

Modularity SMEs Retiring Monitoring

Product Innovation

M&AGlobalization

Operating Cost

Time To Market

Customer Centricity

Business Drivers

Regulatory Drivers

Enterprise Leverage

Asset Rationalization Shared Services

SOA

Compliance

Auditing ReportingFading Skills

© 2014 Fair Isaac Corporation. Confidential.13

Technology

►The Myth: Community Banks don’t have access to powerful and affordable technology

© 2014 Fair Isaac Corporation. Confidential.14

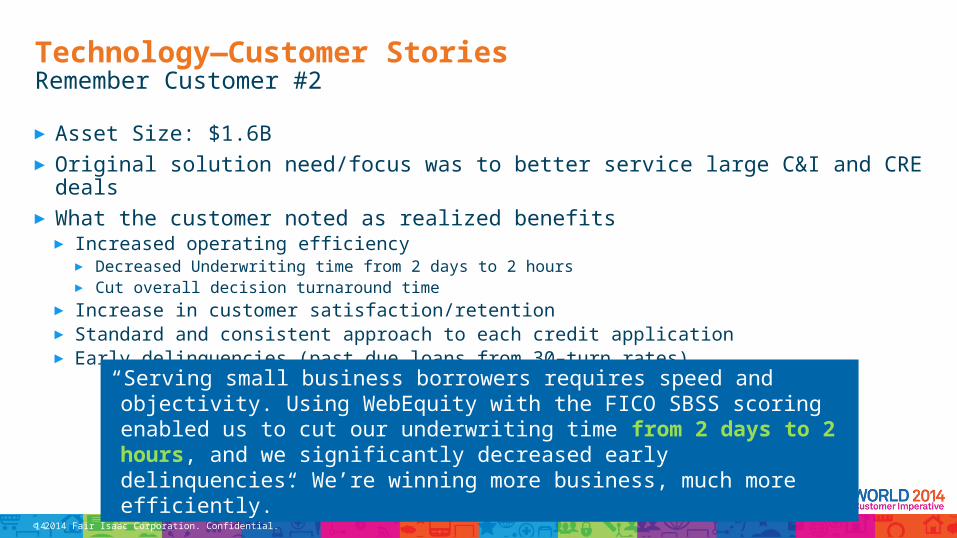

Remember Customer #2

► Asset Size: $1.6B► Original solution need/focus was to better service large C&I and CRE deals► What the customer noted as realized benefits

► Increased operating efficiency ► Decreased Underwriting time from 2 days to 2 hours► Cut overall decision turnaround time

► Increase in customer satisfaction/retention► Standard and consistent approach to each credit application► Early delinquencies (past due loans from 30–turn rates)

Technology—Customer Stories

“Serving small business borrowers requires speed and objectivity. Using WebEquity with the FICO SBSS scoring enabled us to cut our underwriting time from 2 days to 2 hours, and we significantly decreased early delinquencies. We’re winning more business, much more efficiently.”

© 2014 Fair Isaac Corporation. Confidential.

What are yourthoughts on using

the Cloud?

15

© 2014 Fair Isaac Corporation. Confidential.

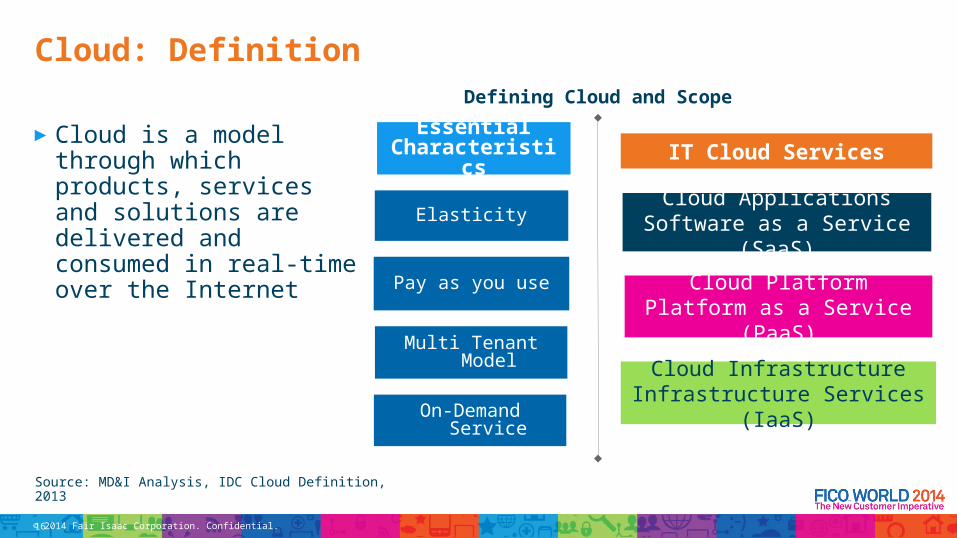

Cloud: Definition

►Cloud is a model through which products, services and solutions are delivered and consumed in real-time over the Internet

Essential Characteristics

Elasticity

Pay as you use

Multi Tenant Model

On-Demand Service

Cloud ApplicationsSoftware as a Service (SaaS)

Cloud PlatformPlatform as a Service (PaaS)

Cloud InfrastructureInfrastructure Services (IaaS)

IT Cloud Services

Defining Cloud and Scope

Source: MD&I Analysis, IDC Cloud Definition, 2013

16

© 2014 Fair Isaac Corporation. Confidential.

Cloud: SaaS

17

© 2014 Fair Isaac Corporation. Confidential.

►Banking is the leading vertical in adoption based on dollars spend in 2014

►Overall growth in these verticals is 22% (’12–’17 CAGR)► Banking is 22%► Highest is 27% (Retail)► Lowest is 17% (Central Gov.)

Cloud: Adoption

18

BankingTelecommunications

Media & EntertainmentIndustrial Products

RetailWholesale & CPG

ElectronicsLocal Government

InsuranceCentral Government

Health ProviderTransportation

CSIEnergy & Utilities

Financial MarketsAutomotive

Health PayorLife Sciences

PetroleumAerospace & Defense

TravelChemical

Higher EducationEducation(K-12)

3,200 2,527

2,308 2,284

1,957 1,840

1,626 1,386

1,287 1,269

1,138 1,018

903 902

776 733

467 406

360 313 310

232 138

102

Total = $27,481 M

Ranked by 2014 Size Values in US$ M

Source: Cloud 2H13 Pivot_20131125_ACCC

© 2014 Fair Isaac Corporation. Confidential.

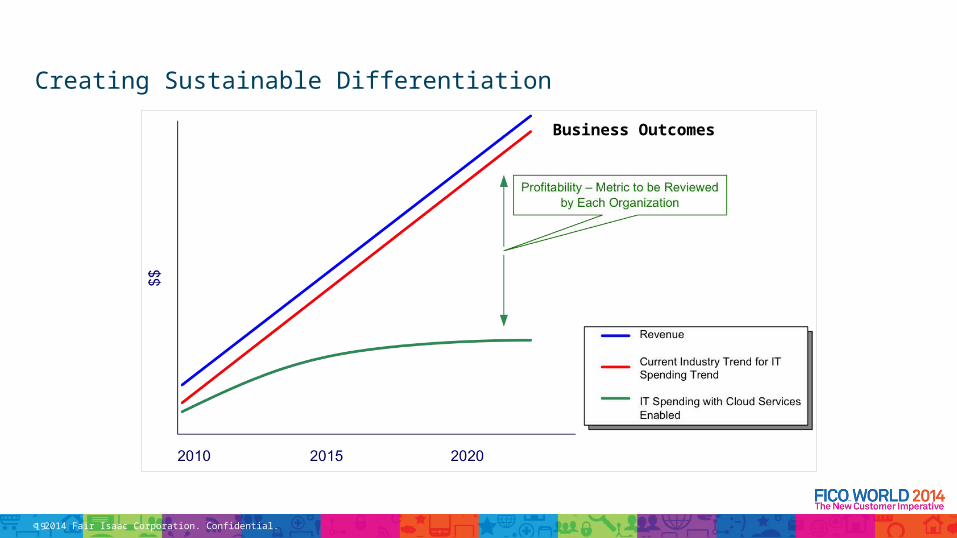

Creating Sustainable DifferentiationCloud: Value Proposition

19

Business Outcomes

© 2014 Fair Isaac Corporation. Confidential.

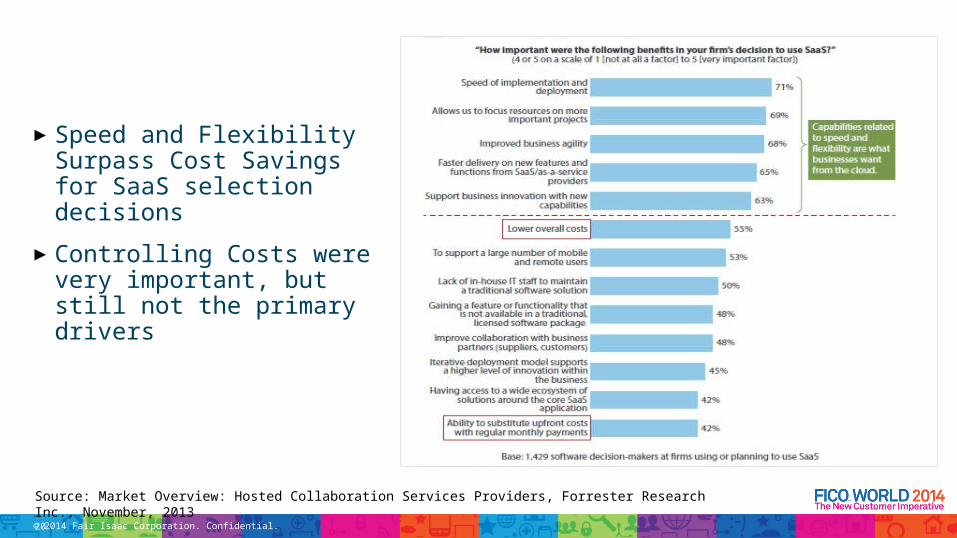

►Speed and FlexibilitySurpass Cost Savings for SaaS selection decisions

►Controlling Costs were very important, but still not the primary drivers

Cloud:Selection Reasons

20

Source: Market Overview: Hosted Collaboration Services Providers, Forrester Research Inc., November, 2013

© 2014 Fair Isaac Corporation. Confidential.21

The Cloud

► The Myth: The Cloud is less secure than on-premise installations

© 2014 Fair Isaac Corporation. Confidential.

The Cloud Is Less Secure than On-premise Solutions

As an example:

►Many community banks have only a couple layers of security

vs.

►Many SaaS Cloud solutions have multiple layers of security

Myth

22

Also note: Cloud solution providers depend on that security…so they focus dedicated resources to it

© 2014 Fair Isaac Corporation. Confidential.

Compete and Win with Technology Driven Loan Lifecycle Management

►Two Primary Themes► Loan Lifecycle Management► Technology—helps community and midsized banks compete

►Myths Busted► Use of scores and auto-decisioning doesn’t work in a relationship banking environment► Community Banks don’t have access to powerful and affordable technology► The Cloud is less secure than on-premise installations

Final Thoughts…

23

© 2014 Fair Isaac Corporation. Confidential.

Questions?

24

© 2014 Fair Isaac Corporation. Confidential. This presentation is provided for the recipient only and cannot be reproduced or shared without Fair Isaac Corporation’s express consent.

Thank You!

25

Todd ClassenVice President Strategic Accounts,WebEquity Solutions

David SmithConsultingFICO

© 2014 Fair Isaac Corporation. Confidential.

Learn More at FICO World

Related Sessions► Fuelling Growth with Centralized, Analytics-Based Credit Decisions►Why a Hosted Credit Decisions System Makes Sense►A Strategic Risk Infrastructure: Making Better Lending Decisions and Improving Customer Experience►One World, One System: Global Originations Deployment►Optimize Originations for Profit and Success

Experts at FICO World►Mark Ryan►David Lightfoot►Alan Pass

Blogs►www.fico.com/blog

26

© 2014 Fair Isaac Corporation. Confidential.

Please rate this session online!

27

Todd ClassenVice President Strategic Accounts,WebEquity Solutions

David SmithConsultingFICO

28