© 2017 kpmg lower gulf limited and kpmg llp, operating … report... · companies to comply when...

TRANSCRIPT

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

1

ContentsCompany name: ABC

IFRS report: IFRS 9 diagnostic report

Month: December 2017

Glossary of abbreviations 3

Background about the entire exercise and how to read the report 4

Disclaimers 5

IFRS 9 potential impact areas - Summary 6

IFRS 9 potential impact areas - Detail 7

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

2

Background about the exercise and how toread the reportBackground about the exercise

The International Accounting Standards Board has issued a new accounting standard on financial instruments (‘IFRS 9 Financial Instruments’) which is mandatory for thecompanies to comply when they prepare financial statements for annual periods beginning on or after 01 January 2018 (early application permitted).

The new financial instruments standard:

– Replaces IAS 39 Financial Instruments: Recognition and Measurement

– Introduces a generational change in the way in which companies account for all financial instruments

– Includes new guidance on the classification and measurement of financial instruments, impairment and hedge accounting

In order to assess the potential impact areas under IFRS 9, the company has used the KPMG IFRS Health Check, a simple online self-diagnostic tool and received this diagnosticreport based on the responses provided to the online assessment.

How to read the report

a) IFRS 9 potential impact areas – Summary

b) IFRS 9 potential impact areas – Detail

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

4

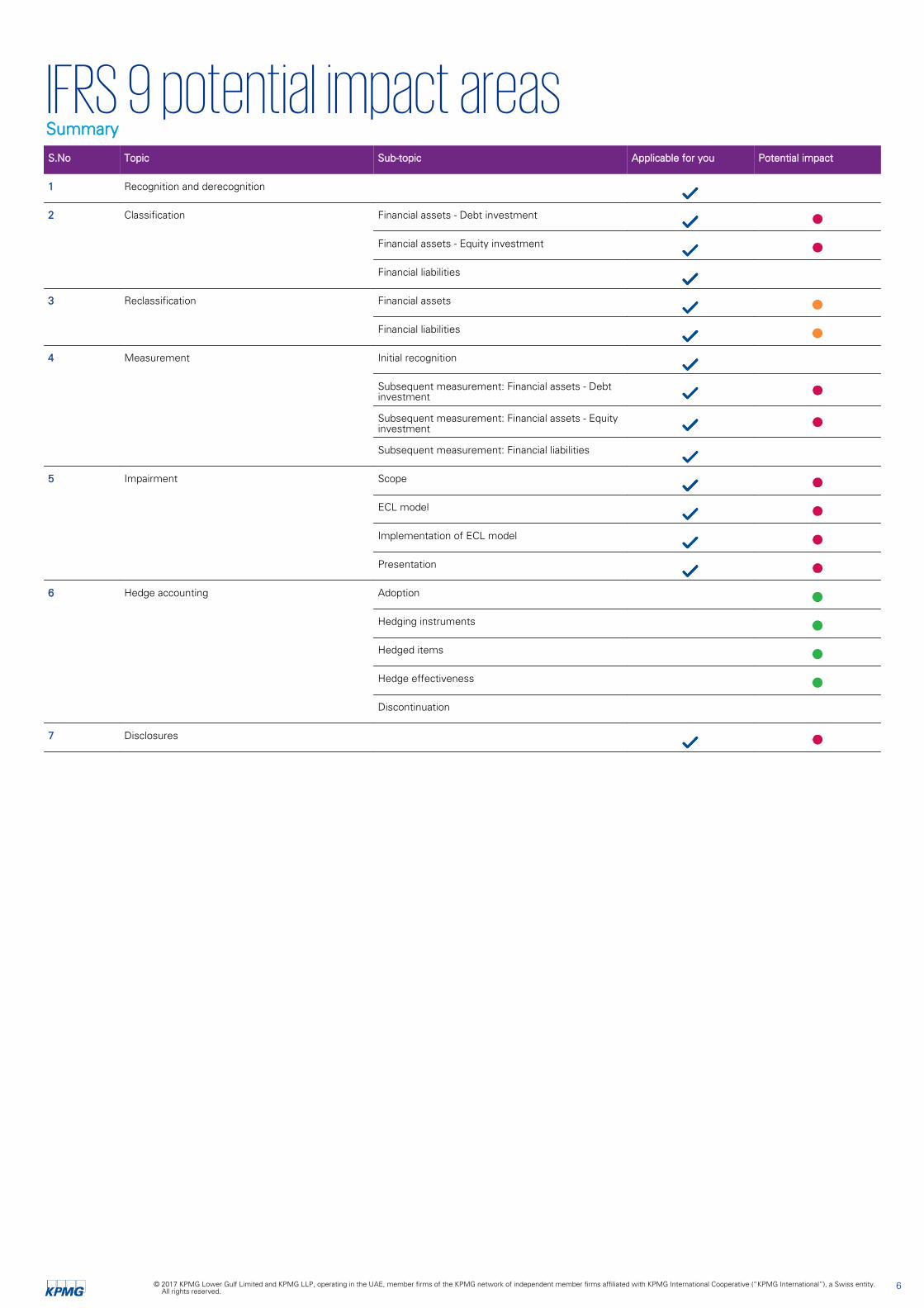

IFRS 9 potential impact areasSummary

S.No Topic Sub-topic Applicable for you Potential impact

1 Recognition and derecognition

2 Classification Financial assets - Debt investment

Financial assets - Equity investment

Financial liabilities

3 Reclassification Financial assets

Financial liabilities

4 Measurement Initial recognition

Subsequent measurement: Financial assets - Debtinvestment

Subsequent measurement: Financial assets - Equityinvestment

Subsequent measurement: Financial liabilities

5 Impairment Scope

ECL model

Implementation of ECL model

Presentation

6 Hedge accounting Adoption

Hedging instruments

Hedged items

Hedge effectiveness

Discontinuation

7 Disclosures

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

6

IFRS 9 potential impact areasDetail

Type of financial instruments in the financial statements:

a) Financial assets:- Bonds, debentures, sukuks or any other similar debt investments- Equity investments

b) Financial liabilities:- Loans and borrowings

S.No Topic Sub-topic Key changes under IFRS 9 Applicable foryou

Potentialimpact

Key reasons

1 Recognition andderecognition

IFRS 9 carries forward from IAS 39 therequirements for recognition andderecognition of financial instruments, withonly minor amendments.

2 Classification Financial assets -Debt investment

IFRS 9 contains three principal classificationcategories for debt investments:

Amortised cost - A financial asset isclassified as being subsequently measuredat amortised cost if the asset is held withina business model whose objective is tocollect contractual cash flows, and thecontractual terms of the financial asset giverise to cash flows that are solely paymentsof principal and interest (the ‘SPPIcriterion’).

FVOCI - A financial asset is classified asbeing subsequently measured at FVOCI if itmeets the SPPI criterion and is held in abusiness model whose objective isachieved by both collecting contractual cashflows and selling financial assets.

FVTPL - All other financial assets areclassified as being subsequently measuredat FVTPL. In addition, an entity may, atinitial recognition, irrevocably designate afinancial asset as at FVTPL, if doing soeliminates or significantly reduces anaccounting mismatch that would otherwisearise.

The existing IAS 39 categories of held-to-maturity, loans and receivables, andavailable-for-sale are removed.

Possible failure of 'SPPI criterion' due to theexistence of the below features in debtinvestments:

- Some feature introduces exposure to riskor volatility to the contractual cash flowsunrelated to a basic lending arrangement

- Prepayment option- Extension option- Embedded derivatives

Financial assets -Equity investment

IFRS 9 contains two principal classificationcategories for equity investments:

FVOCI - At initial recognition of an equityinvestment that is not held for trading, anentity may irrevocably elect to present inother comprehensive income (OCI)subsequent changes in its fair value.

FVTPL - All equity investments that are heldfor trading and equity investments that arenot held for trading and not designated asFVOCI.

The existing IAS 39 category of available-for-sale is removed.

Existence of some equity investments in thenature of debt (or vice-versa) may pose achallenge in their classification in the financialstatements as the classification categoriesare different for equity investments (FVOCIand FVTPL) and debt investments (amortisedcost, FVOCI and FVTPL).

Financial liabilities IFRS 9 retains the existing requirements inIAS 39 for the classification of financialliabilities.

3 Reclassification Financial assets Reclassification of financial assets isrequired if the objective of the businessmodel in which they are held changes afterinitial recognition of the assets, and if thechange is significant to the entity’soperations. Such changes are expected tobe very infrequent. No otherreclassifications are permitted.

Financial liabilities No reclassification of financial liabilities ispermitted.

4 Measurement Initial recognition IFRS 9 generally retains IAS 39'srequirements on measurement at initialrecognition.

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

7

Thank you

www.kpmg.com/aewww.kpmg.com/om

Follow us on: kpmg-mesa

@kpmg_lowergulf

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity.Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it isreceived or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after athorough examination of the particular situation. © 2017 KPMG Lower Gulf Limited, operating in the UAE and Oman, member firm of the KPMGnetwork of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name and logo are registered trademarks or trademarks of KPMG International. Designed by Creative UAE

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

10