any profit or gain arising from the transfer of capital asset is chargeable to tax under the head...

TRANSCRIPT

CAPITAL GAIN Sec 45,48,49,50,54 & 54EC

&Sec 2(14) & 2(47)

CAPITAL GAINS U/S 45 ANY PROFIT OR GAIN ARISING FROM THE

TRANSFER OF CAPITAL ASSET IS CHARGEABLE TO TAX UNDER THE HEAD CAPITAL GAINS.

*TRANSFER WHEN COMPLETE & EFFECTIVE

. Generally capital gain is taxable in the year in which capital asset is transferred.

. Different rules are applicable in case of movable/immovable asset to find out when a capital asset is “TRANSFERRED”

DEFINITION

CAPITAL ASSET IS DEFINED TO INCLUDE PROPERTY OF ANY KIND WHETHER FIXED OR CIRCULATING ,MOVABLE OR IMMOVABLE , TANGIBLE OR INTANGIBLE.

CAPITAL ASSET MEANS PROPERTY OF ANY KIND HELD BY AN ASSESSEE WHETHER OR NOT CONNECTED OR HELD BY AN ASSESSEE WITH HIS BUSINESS/PROFESSION

CAPITAL ASSET ……….. EXCEPT FOLLOWING.,

1. Any stock in trade consumable stores or raw materials held for the purpose of business and profession.

2. “Personal effect” i.e Any asset used for personal purpose. But Jewellery, archeological collections, grings, painitings, sculptures of any work of art personal use is treated as a capital asset

3. Agricultural Land in India.4. 6 ½ % Gold Bonds, 1977 or 7 % Gold

Bonds 1980, or National Defence Gold bonds 1980

5. Special Bearer Bonds, 19916. Gold Deposit Bonds issue under Gold

deposit Scheme 1999

SHORT TERM CAPITAL ASSET [SECTION 2(42A)]

SHORT TERM CAPITAL ASSET MEANS A CAPITAL ASSET HELD BY AN ASSESSEE FOR NOT MORE THAN 36 MONTHS IMMEDIATELY PRIOR TO ITS DATE OF TRANSFER

Capital Assets being shares in a company listed securities or Units in UTI or Zero Coupon bondsSuch assets is held for a period of

not more than 12 months it shall be treated as short –Term Capital Asset

LONG TERM CAPITAL ASSET [SECTION 2 (29A)]

LONG TERM CAPITAL ASSET MEANS A CAPITAL ASSET HELD BY AN ASSESSEE FOR MORE THAN 36 MONTHS.

SHARES AND DEBENTURES ARE ALSO LONG TERM CAPITAL ASSET ,BUT THE PERIOD OF HOLDING SHOULD BE MORE THAN 12 MONTHS.

TRANSFER OF

CAPITAL ASSET

According to Section 2(47)TRANSFER INCLUDES

SALE OF CAPITAL ASSET EXCHANGE OF CAPITAL ASSET RELINQUISHMENT OF CAPITAL ASSET EXTINGUISHMENT OF RIGHTS IN A

CAPITAL ASSET COMPULSORY ACQUISITION BY

GOVERNMENT CONVERSION OF CAPITAL ASSET

INTO STOCK IN TRADE

TRANSACTION NOT TREATED AS TRANSFER

DISTRIBUTION OF CAPITAL ASSET BY COMPANY TO THE SHAREHOLDER AT THE TIME OF LIQUIDATION

DISTRIBUTION OF CAPITAL ASSET BY H.U.F TO ITS MEMBERS AT THE TIME OF PARTITION.

CAPITAL ASSET DISTRIBUTED OR ACQUIRED BY WAY OF GIFT,UNDER WILL OR UNDER LAW OF INHERITANCE.

TRANSACTION NOT TREATED AS TRANSFER

TRANSFER OF CAPITAL ASSET BEING ART COLLECTION DRAWINGS PAINTINGS OR ANY ANTICS etc TO NATIONAL MUSEUM , NATIONAL ART GALLERY PULIC MUSEUM

DEBENTURES CONVERTED INTO SHARES OF THE SAME COMPANY OR DEPOSITS CERTIFICATES CONVERTED INTO DEBENTURES OF SAME COMPANY

Calculation of Short-term Capital Gain

Full Value of consideration XX Less Transfer Expenses XX Less Cost of acquisition XX Less Cost of Improvement XX

______Short-term Capital Gain XX

Full Value of Consideration Section - 48

Consideration means the value received for the transfer. The value may be money or money’s worth. Consideration received or receivable is taken into account. Capital Gain are taxed on accrual basis and not on cash basis

Full Value means the whole or entire or complete value

The gross value i.e what the transferor receives in lieu of the asset he gives up

Expenditure on Transfer

Expenditure incurred by the transferor wholly and exclusively in connection with such transfer . Means the expenditure which is necessary to effect the transfer. eg., Brokerage, commission, stamp duty, registration fees, travelling expenses incurred in connection with such trasfer

Cost Of Acquisition

INTRODUCTION

Cost of acquisition of an asset is the value for which it was acquired by the assessee. Expenses of capital nature for completing or acquiring the title to the property are

includible in the cost of acquisition

No Type of Capital Asset Cost of Acquisition

1 Goodwill of a business, trademark on brand name associated with a business, right to manufacture or produce or process any article or thing or tenancy rights or state carriage permits or loom hours purchased from previous owner.

Amount of purchase price (FMV on 1-4-1981 not allowed even if acquired before 1-4-1981)

2 Same assets as above but self generated.

Nil (FMV on 1-4-1981 not allowed)

3 (a) Bonus shares(b) Right Shares

Nil (But if acquired before 1-4-1981 FMV as on 1-4-1981 allowed)Amount actually paid

4 Any other asset becoming the property of assessee.

Cost of acquisition to the assessee or its FMV as on 1-4-1981 at the option of the assessee

5 Capital asset becoming the property of the assessee in any of the modes specified in section 49(1) which became the property of the previous owner before 1-4-1981.

Cost of acquisition to the previous owner or its FMV as on 1-4-1981 at the option of the assessee.

COST OF ACQUISITON (SEC 48)

No Type of Capital Asset Cost of Acquisition

1 (a) Distribution of assets on partition of HUF.(b) Gift or will.© Succession, inheritance or devaluation.(d) Distribution of assets on liquidation of the

company(e) Transfer to a trust.(f) Transfer by holding co. to wholly owned

subsidiary co. or vice versa.(g) Transfer in a scheme of amalgamation of Two Indian companies &Two Foreign

companies(h) Conversion of self acquires individual

property with HUF property

Cost of acquisition to the previous owner. [Sec 49 (1)]

2 Share of debentures acquired on conversion of debentures, stock or deposit certificate.

Cost of corresponding debentures or the debenture stock or deposit certificate.

3 Acquisition of shares in the resulting co. due to demerger.

Cost of shares * Book value of assets tfd. / Net worth of co. before demerger.

4 Acquisition of original shares of demerged co. Original cost of acquisition less the value arrived at point no. 3 above.

DEEMED COST OF ACQUISITON (SEC 48)

MODE OF COMPUTATION (SEC 48)

The income chargeable under the head “Capital Gain” shall be computed, by deducting from the full value of the consideration received or accruing as the result of the transfer of the capital asset. The following are the amount namelyExpenditure incurred wholly or exclusively in connection with the transfer.The cost of acquisition of the asset and the cost of any improvement thereto.

Provided that long term capital gain arises from the transfer of a long term capital asset. While computing long term Capital Gain “Indexed cost of acquisition” & “Indexed cost of improvement” is to be considered.

“INDEXED COST”

meaning : index cost refers to

computing of long term capital gains.

index cost helps to tax only real gains earned by the assessee on the sale of goods.

“COST OF INFLATION INDEX”.

The index cost is computed with the help of cost of inflation index.Indexing is applied to both cost of acquisition as well as cost of improvement.

75% of the average rise in the consumer price of central government.

COST OF INFLATION INDEX FOR PREVIOUS YEARS.

FINANCIAL YEAR.

COST OF INFLATION INDEX

1981 –1982 100

1983 -1984 116

1985 –1986 133

1987-1988 150

1989 –1990 172

1991 –1992 199

2006 -2007 519NOTE: THE BENEFIT OF INDEXATION WILL NOT APPLY TO THE LONG TERM CAPITAL GAINS ARISING FROM TRANSFER OF BONDS.

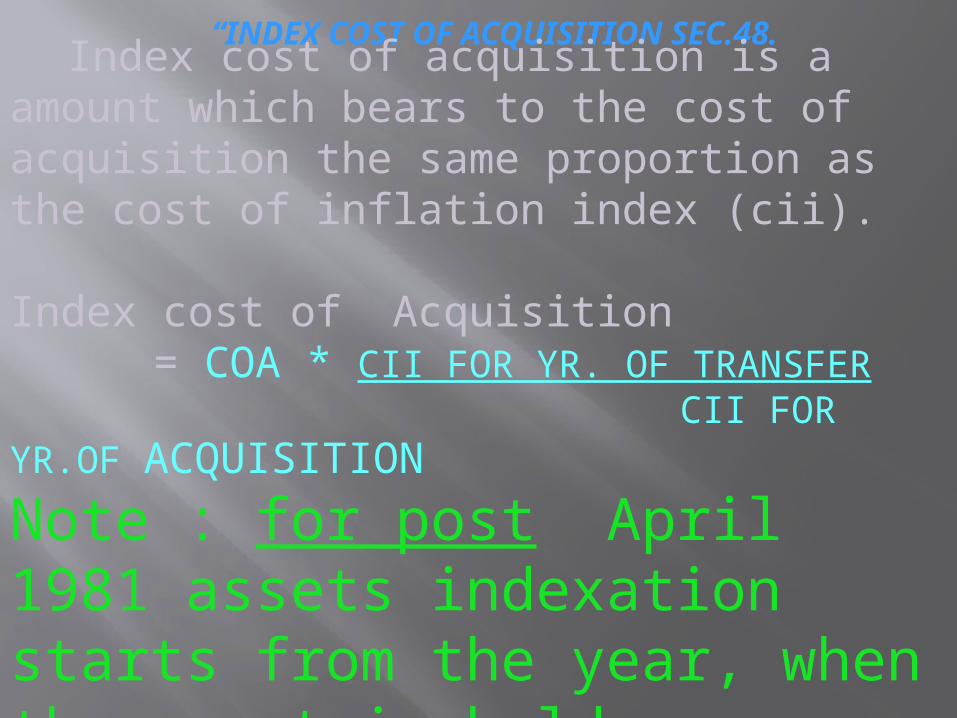

“INDEX COST OF ACQUISITION SEC.48. Index cost of acquisition is a amount which bears to the cost of acquisition the same proportion as the cost of inflation index (cii). Index cost of Acquisition

= COA * CII FOR YR. OF TRANSFER CII FOR YR.OF ACQUISITION

Note : for post April 1981 assets indexation starts from the year, when the asset is held.For pre = April 1981 assets cii for the yr of acquisition is taken as 100.

COST OF IMPROVEMENT”.

It is defined as an amount which bears the cost of improvement the same propotion as the cost of inflation index for the year which the asset is transferred.

INDEX COST OF IMPROVEMENT = CII FOR YR.OF TRANSFER.

CII FOR YR.OF IMPROVEMENT.

“INDEXED COST OF IMPROVEMENT”

Computation of Capital Gains

Particulars Amount (Rs)

Full Value of Consideration

Less: Cost of Acquisition Cost of Improvement Expenditure of Transfer

Capital gains

Less: Exemption u/s 54 Taxable Capital Gains

xxx

xxx xxx xxx

xxx

xxx

XXX

Exemptions of Capital Gains

Exemption is nothing but a reduction from the capital gain which is

taxable, on which tax will not be levied and paid.The exemptions of capital gains are provided in the following

casesUnder sec 10, 54, 54B, 54D, 54EC, 54ED, 54EF, 54F & 54G asfollows:-

Exemption of capital gains on compulsory acquisition of agricultural land

Exemption of LTCG arising from sale of shares and units Exemption of capital gain on transfer of an asset of an

undertaking engaged in the business of generation, transmission, distribution of power

If house property that is transferred is used for residential purpose

House property was a long term capital asset If agricultural land used by an assessee to purchase another

agricultural land within a period of 2 years after the date of transfer

Any LTCG shall be exempt to the extent such capital gain is invested within a period of 6 months after the date of transfer in the specified long term asset

Capital gain arising from the transfer of LTCA being listed securities or Unit of a mutual fund or the UTI shall be exempt to the extent such capital gain is invested in equity shares forming part of an eligible capital within a period of 6 months after the date of such transfer

The Capital gain that arises to an individual/HUF from the transfer of any capital asset other than residential house property shall be exempt in full if the entire net sales consideration is invested in purchase of one residential house 1 year before or two years after the date of transfer.

Any capital gain arising to an individual undertaking from the compulsory acquisition under any law, shall be exempt to the extent such capital gain is invested in the purchase of another land/building within a period of 2 years after the date of transfer

THANK YOU

SPECIAL PROVISIONS.U/S 55.

1.EXPENDITURE INCURRED 1ST APRIL 1981.NOT CONSIDERED.

2.DOUBLE DEDUCTION NOT PERMITTED.

EXEMPTION UNDER SECTION 10 (38) LONG TERM CAPITAL GAINS ON TRANSFER OF EQUITY SHARES UNITS IN CASE COVERED BY

SECURITIES TRANSACTION TAX :-

Long term capital gains arising on transfer of equity shares or units of equity oriented mutual fund is not chargeable to tax from the assessment year 2005-2006 if such a transaction is covered by securities transaction tax.

TRANSFER OF CAPITAL ASSET

TYPES OF CAPITAL ASSET?

SHORT TERM CAPITAL ASSET.

Capital asset held by the assesse for not more than 36 months except the following(12 months)

Equity & preference shares. Units of U.T.I Units of MUTUAL FUNDS Listed securities (deb. or govt. sec)

ANY ASSET OTHER THAN A SHORT TERM CAPITAL ASSET IS

REGARDED AS LONG TERM CAPITAL ASSET. THUS SHARES/SEC./UNITS

HELD FOR 12M.(OR MORE) OR ANY OTHER ASSET HELD FOR 36M. (OR MORE) ARE LONG TERM CAPITAL

ASSET.

LONG TERM CAPITAL ASSET

WHAT IS TRANSFER OF CAPITAL ASSET?

TRANSFER, IN RELATION TO CAPITAL, INCLUDES SALE, EXCHANGE OR RELINQUISHMENT OF THE ASSET OR THE EXTINGUISHMENT OF ANY RIGHTS THERE IN OR THE COMPULSORY ACQUISITION THEREOF UNDER AN LAW(SEC.2(47))

CERTAIN TRANSACTION NOT TREATED AS TRANSFER.

1. Distribution of asset in kind by a co. to its share holder at the time of liquidation .(46(1))

2. Distribution of capital asset on total or partial partition of H.U.F(47(i))

3. Transfer of capital asset under gift or will or an irrevocable trust.(47(iii))

4. Transfer of capital asset by a co. to its 100% subsidiary co.(47(v))

5. Transfer of capital asset in a scheme of amalgamation.(47(vi))

6. Transfer of capital asset by the demerged co. to resulting co.(47(vib))

7. Transfer involved in a scheme of lending securities.(47(xv))

8. Transfer by way of conversion of bonds or debentures into shares.

9. And some more of such transaction included in sec.45,46,47 & its sub sec.

Income From Other Sources

Meaning: It is a residuary head of

income which must satisfy the following criteria :- 1. There must be an income; 2. Which is NOT exempt under the IT Act 1961;

3. It is not chargeable to tax under the other heads of income

viz."Salary","Houseproperty","Business or Profession" and

'Capital Gains'.

Some Examples of this Source

1. Interest on bank deposits, loans or company deposits,

2. Family pension (received by legal heirs of an employee),

3. Income from sub-letting of house

property by a tenant,

4. Agricultural income from agricultural land situated outside India,

5. Interest received from IT Dept. On delayed refunds,

6. Remuneration received by Members of Parliament,

7. Insurance commission,

8. Examiner-ship fees received by a teacher (not from employer), 9. Income from royalty, 10. Director's commission for standing as guarantor to bankers, 11. Winnings from Lotteries,Crossword

Puzzles,Horse Races and Card Games, 12. Interest on securities, 13. Income from letting out of machinery, plant or furniture,etc.

DIVIDENT INCOME

E X E M P TU N D E R S E C 1 0 (3 4 )

R E C IV E D F R O M IN D IA N C O M P A N Y

E X E M P TU N D E R S E C 1 0 (3 5 )

R E C IV E D F R O M U N ITS O F U TI&

M U TU A L F U N D S

TA X A B L E U N D E RO TH E R S O U R C E

R E C IV E D F R O M F O R E IG N C O M P A N Y

D IV ID E N T IN C O M E

AGRICULTURAL INCOME

E X E M P T U N D E R S E C 1 0 (1 )

R E C IV E D F R O M A G R IC U L TU R A L L A N D S ITU TE D IN IN D IA N

TA X A B L E U N D E R O TH E R S O U R C E

R E C IV E D F R O M A G R IC U L TU R A L L A N D S ITU A TE D O U TS ID E IN D IA N

A G R IC U L TU R A L IN C O M E

INCOME FROM SUB-LETTING OF HOUSE PROPERTY

Income received by tenant by sub-letting the house property to a sub tenant is taxable under the head income from other source.

CASUAL INCOME

Casual income are those income which are non-recurring in nature and which is received by person unexpectedly or by chance.

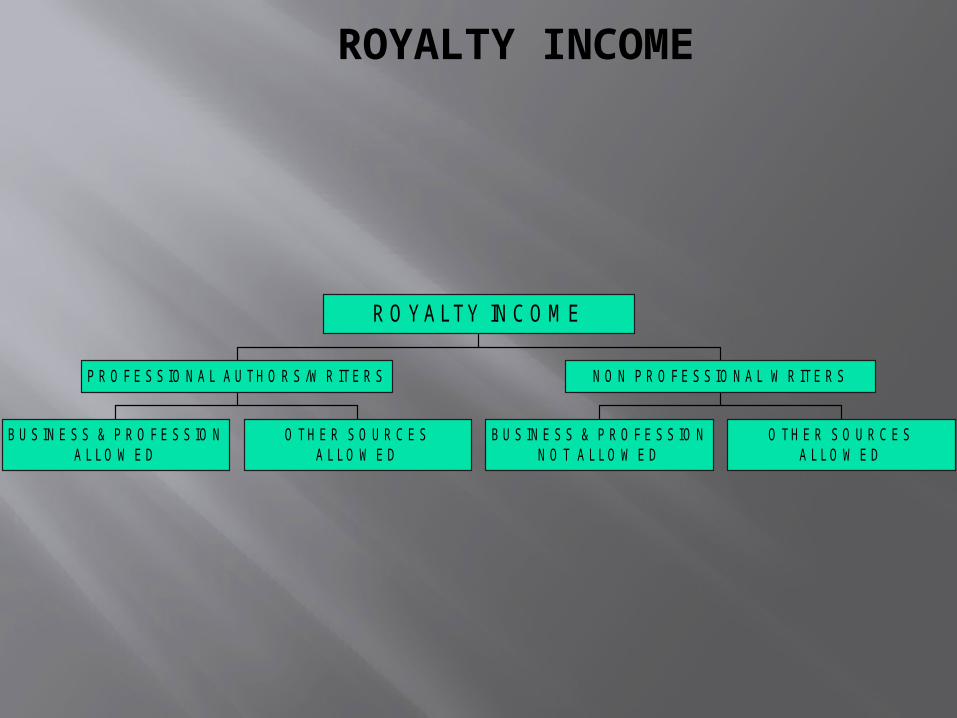

ROYALTY INCOME

B U S IN E S S & P R O F E S S IO NA L L O W E D

O TH E R S O U R C E SA L L O W E D

P R O F E S S IO N A L A U TH O R S /W R ITE R S

B U S IN E S S & P R O F E S S IO NN O T A L L O W E D

O TH E R S O U R C E SA L L O W E D

N O N P R O F E S S IO N A L W R ITE R S

ROYALTY INCOME

AWARDS / REWARDS

E X E M P TU N D E R 1 0 (1 7 A )

R E C E IV E D F R O M G O V E R M E N T

TA X A B L E U N D E R S A L A R Y TA X A B L E U N D E R O TH E R S O U R C E[N O T R E L A TE D TO JO B ]

R E C E IV E D F R O M C O M P A N Y TO A N E M P L O Y E E

TA X A B L E U N D E R B U S IN E S S & P R O F E S S IO N

R E C E IV E D F R O M M A N U F A C TU R E /S U P P L IE R

A W A R D S / R E W A R D S

FAMILY PENSION

Family pension received by family member is taxable under the head income from other source after claiming standard deduction u/s 57 which is as follows

1/3 of family pension received or Rs 15000 Which ever is less

ALLOWANCES & SALARIES RECEIVED BY MP’s & MLA’s

E X E M P TU N D E R S E C 1 0 (1 7 )

D a ily a llow C on s tit ien c y a llow o r an y o th e r a llow (u p to R s 2 0 0 0 p m )

Taxab leu n d er o th e r s ou rc e

S a la ry from g ove rm en t

Taxab leu n d er o th e r s ou rc e

O th e r A llow an c e (M ore th en R s 2 0 0 0 p m )

A L L O W A N C E & S A L A R IE S R E C E IV E D B Y M P s & M L A s

EXAMINERSHIP FEES / PAPER CHEKING / OR

PAPER SETTING FEES

U N D E RIN C O M E F R O M S A L A R Y

TA X A B L E

R E C E IV E D B Y TE A C H E RF R O M S A M E C O L L E G E / S C H O O L

U N D E RIN C O M E F R O M O TH E R S O U R C E

TA X A B L E

R E C E IV E D F R O M M U M B A I U N IV E R C ITY

B U S IN E S S & P R O F E S S IO N O TH E R S O U R C E

TA X A B L E

R E C E IV E D F R O M C O A C H IN G C L A S S E S

E X A M IN E R S H IP F E E S / P A P E R C H E K IN G /O R

P A P E R S E TTIN G F E E S

GIFTS / PRESENTS

N O T TA X A B L E

P E R S O N A L G IF TS

R E C E IV E D F R O MR E L A TIV E S / F R IE N TS

N O T TA X A B L E

P E R S O N A LG IF T

B IR TH D A Y

U N D E RIN C O M E F R O M

S A L A R Y

TA X A B L E

D IW A L I

R E C E IV E D F R O MC O M P A N Y / E M P L O Y E E

U N D E RB U S IN E S S

&P R O F E S S IO N

TA X A B L E

R E C E IV E D F R O MC L IE N T

U P TO 2 5 0 0 0 N O T TA X A B L E

U N D E RO TH E R S O U R C E

A B O V E 2 5 0 0 0 TA X A B L E

O TH E R F R IE N D S

G IF TS / P R E S E N TS

INCOME OF MINOR CHILDREN

Minor children earning income without using his talent and skill is club with parent under the head income from other source after claiming exemption of Rs 1500 under sec 10(32).

INCOME TAX

D IS A L L O W E D E X P

IN C O M E TA X P A ID

N O T TA X A B L E

N O T IN C O M E

IN C O M E TA X R E F U N D

O TH E R S O U R C E

TA X A B L E

IN TE R E S T O N IN C O M ETA X R E F U N D

IN C O M E TA X

INCOME FROM LETTING OUT VARIOUS ASSETS

Hire charge or rent received by letting out various assets like plant / mach, furniture , motor vehicle computer etc. is taxable under the head income from other source . If it is not taxed under the head business & profession .

Any related expenses incurred to earn above income will be allowed as deduction u/s 57.

INCOME ON VARIOUS SECURITIES

Any income received in the form of interest or dividend on various securities are fully taxable under the head income from other source . Provided such income are not exempt and not taxable under four main head of income .

DONATIONS

THIS DEDUCTIONS IS AVAILABLE TON ALL THE ASSESSE In this sections (80g) where an assesse pays any sum as donations to eligible funds or institutions to eligible funds or institutions, he is entitled to a deductions subject to certain limitations

from the gross total income.The following table gives the details of the institutions and funds to which donations and funds can be made for the purpose of claiming deductions u\s80g the qualifying amount and the deductions

allowable.

Limited 50%Approved charitable trustAuthority safe guarding \ promoting the interest of minorityApproved temple, mosque, church,gurudwara etc

Unlimited 50%Jawaharlal Nehru memorial fundPrime minister drought relief fundIndira Gandhi memorial fundRajeev Gandhi foundations

limited 100%Government or state governmt or local authority approved trust for promoting “family planning”

Unlimited 100%National defence fundPrime minister national relief fund Africa public contribution India fund etc

conditions The following conditions must be fulfilled to consider

the conditions eligible for deductions u\s80g The maximum amount which can be considered

eligible for deductions under this section is restricted to 10%of gross total income as reduced by the amount of deductions allowable as per chapter VIA u\s 80cca and 80u excluding section 80g.

The donation must be in the form of money and not in kind. Donation in kind will not qualify for deductions

For applying qualifying limit all donations made to the funds\institutions covered under (A) & (D).above shall be aggregated and the aggregated amount shall be limited to10% of adjusted gross total income.

DEDUCTION ON DONATION [SECTION 80G]

Donation by cash or cheque can further be divided into 2 parts:

a. Specified Institutions.b. Non-specified institution.

The donation made in kind and donation made by non specified institution are not allowed as deduction u/s 80G.

The donation under specified institution are divided into 4 categories:

Limited 50%Limited 100%Unlimited 50%Unlimited 100%