) in a nutshellswiss tax reform; swiss tax reform and ahv financing; traf; nutshell; peter...

TRANSCRIPT

The Swiss Tax Reform (TRAF)in a nutshell

July 2019

1© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

Overview of measures

— Abolishment of privileged tax regimes (e.g. holdings, mixed companies, etc.)

— Introduction of transitional measures

Abolishment of tax regimes

Additional R&D deductions

Overall limitation mechanism

Patent box

Notional interest deduction

Reduction of cantonal tax rates

— Additional deduction of R&D expenses (up to 50%)

— Promoting R&D in CH

— The benefits from certain measures (patent box, R&D deduction and current law step up) are limited at 70%.

— Reduced cantonal taxation of profits from patents

— At least 10% of those profits are taxable

— Notional interest deductionon equity

— Only applicable for cantons with high tax rates (e.g. Zurich)

— General reduction of cantonal income tax rates announced

— Ensuring attractiveness of individual locations

NID

2© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

Abolishment of regimes as per 1 January 2020

1 2 3Holding company regime: 7.83%

Dominant player in the professional services space confident in ability to generate sustainable long term growth

Strong and seamless presence in our clients over the long term

12 3 4Mixed / Auxiliary Company regime: 8.3 – 12%

Principal Company practice: 5 – 9%

Finance branch practice: 1 – 2%

Which Swiss tax privileges and practices are being abolished with TRAF?

What is the impact for affected companies?

− Businesses will be subject to ordinary taxation unless new privileges are available (e.g. patent box)

− Taxpayers can choose a transitional measure that “cushions” this impact for a number of years

− Tax rate reductions in the majority of the cantons also to be taken into account (2/3 of the Cantons will be at 12% – 14.5% in the future)

3© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

Transitional measures

Current law step up Special rate regime

‒ Effective (tax neutral) disclosure (in tax balance sheet) of hidden reserves and goodwill created under the tax privilege

‒ Revaluated assets may be depreciated by reducing taxable income

‒ Depending on the implementation of the canton, depreciation period is 5-10 years (subject to overall limitation mechanism)

‒ The increase of the tax rate change shall be cushioned over a period of 5 years (not subject to overall limitation)

‒ During the transitional period a special reduced tax rate is applied for part of the taxable income (related to the amount of hidden reserves and goodwill created under the tax privilege)

‒ Such special tax rate varies between the cantons

‒ After the transitional period: new ordinary tax rates are applied on the whole profit

Transitional measures

Ensure that hidden reserves are taxed under the tax regime in which such reserves have been created Only relevant for cantonal and communal taxes

Special rate taxation

Ordinarytaxation

4© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

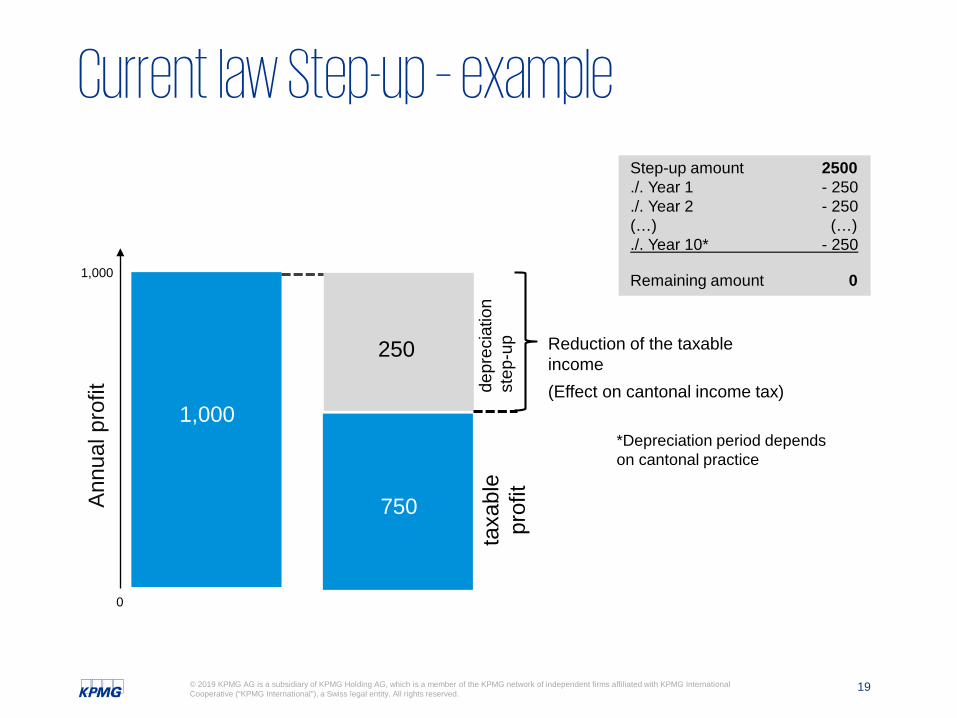

Step-up amount 2,500./. Year 1 - 250./. Year 2 - 250(…) (…)./. Year 10* - 250

Remaining amount 0

Reduction of the taxable income(Effect on cantonal income tax)

500

taxa

ble

prof

itde

prec

iatio

nst

ep-u

p

0

Current law Step-up – exampleAn

nual

pro

fit

250

250

500

*Depreciation period dependson cantonal practice

5© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

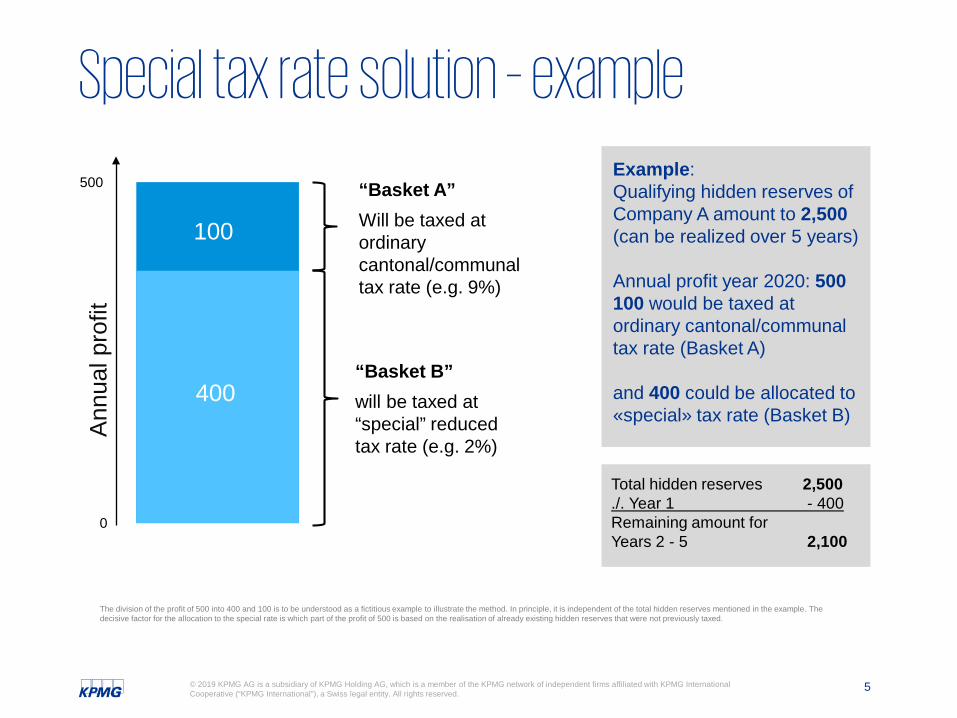

Special tax rate solution – example

“Basket B”will be taxed at “special” reduced tax rate (e.g. 2%)

Annu

al p

rofit

0

Example:Qualifying hidden reserves of Company A amount to 2,500(can be realized over 5 years)

Annual profit year 2020: 500100 would be taxed at ordinary cantonal/communal tax rate (Basket A)

and 400 could be allocated to «special» tax rate (Basket B)

100

400

500

The division of the profit of 500 into 400 and 100 is to be understood as a fictitious example to illustrate the method. In principle, it is independent of the total hidden reserves mentioned in the example. The decisive factor for the allocation to the special rate is which part of the profit of 500 is based on the realisation of already existing hidden reserves that were not previously taxed.

Total hidden reserves 2,500./. Year 1 - 400Remaining amount forYears 2 - 5 2,100

“Basket A”Will be taxed at ordinary cantonal/communal tax rate (e.g. 9%)

6© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

Implementation process of TRAF

Implementation

Abolishment of tax regimes

Additional R&D deductions

Overall limitation

Patent box

Notional interest deduction

Reduction of cantonal tax rates

Amendment ofregulations in the Federal Tax HarmonizationAct

Amendment of regulations and implementation of measuresin the Cantonal Tax Laws

Implementation

TRAF Not in TRAFAccepted by public vote on 19 May 2019

Federal level Cantonal level

How is TRAF being implemented in the Swiss tax law?*

‒ The implementation of the specific measures takes place at cantonal level

‒ All Swiss cantons plan to enforce the tax reform on 1 January 2020 in their cantonal tax laws – however the implementations vary significantly

‒ The 6 cantons Basel-City, Glarus, St. Gallen, Neuchatel, Geneva and Fribourg have finalized the legal implementation process (in force as from 1 January 2020 – Basel-City partly already as from 1 January 2019)

‒ 10 cantons plan the public vote in calendar year 2019 (e.g. Zurich, Zug, Lucerne, Schwyz, Schaffhausen)

‒ 8 cantons plan a public vote in 2020 (e.g. Berne, Aargau, Ticino, Grisons)

‒ For the applicability of a specific measure, the cantonal law needs to be consulted!

* Status per 11 July 2019

7© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

What makes the new Swiss tax system attractive?

Low ordinary tax rates (prior to benefitting from any incentives)

Two thirds of the cantons plan to have an ordinary combined effective corporate income tax rate between 12-14.5%.

Topic: Measures:

1Incentives for innovation Output and input incentives are introduced on cantonal level:

‒ Patent box regime (according to OECD standards)

Residual income tax burden as low as approx. 9% in specific cantons (implementation at cantonal level varies significantly)

‒ R&D super deduction (optional)

Additional deduction of up to 50% of R&D expenses

2Implementation of a business migration step-up (relevant for current principal company structures)

Upon relocation to Switzerland, a foreign company/branch can disclose hidden reserves including goodwill in a tax-free manner. Hence, in the first few (up to 10) years the company may benefit from additional depreciations on such disclosed hidden reserves and goodwill (not subject to overall limitation mechanism).

3

8© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

Patent box regimeApplication of the patent box− Applicable at cantonal level only (mandatory for all cantons), up to 90% relief, resulting in an ETR as low

as approx. 9%

− Consideration of OECD modified nexus approach based on R&D expenses incurred patent box is particularly of interest, if the patent was developed in Switzerland

− Application of patent box is possible from the date of the granting of the patent until the date of its expiration

Qualifying IP− Patents (Swiss and – if comparable – foreign patents/including patented software)

− IP similar to patents, i.e.:

Supplementary protection certificates Topographies Protected varieties of plants Protected documents according to the Therapeutic Products Act Reports protected by the Ordinance on Plant Protection Products Comparable foreign rights

9© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

Additional R&D DeductionBroad Definition of R&D: − Basic research main goal is to gain knowledge− Applied research main goal is to contribute solutions to practical problems− Science-based Innovation development of new products, methods, processes

and services in industry and society

Own domestic R&D Additional deduction of 50% of R&D expenses (domestic personnel expenses plus markup of 35%)Domestic contract R&DAdditional deduction of 50% of 80% of invoiced R&D expenses

107.5

R&Dpersonnelexpenses

35%35*

100 (domestic) Contract R&D

80%

20% 20

100

Basis

50%

AdditionalR&D deduction

215

135 80

Own R&D Contract R&D

*Assumption: there are at least other R&D expenses in the amount of 35 (in addition to personnel expenses); hence overall R&D expenses in the example amount to (at least) 235.

10© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

Ordinary combined (including federal) effective corporate income tax ratesStatus as of June 2019 (undergoing possible changes)

Planned corporate income tax rates (1/2)

Year 2019

Implementation TRAF

12%

?

11© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

Planned corporate income tax rates (2/2)Minimum combined (including federal) effective corporate income tax ratesStatus as of June 2019 (undergoing possible changes)

Min. tax rate with overall limitations

12%

12© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

Checklist for existing structures− If no tax privilege is in place

Most relevant measure: tax rate reduction in majority of the cantons

Calculation of effect of tax rate reduction

Consider possible relocation in other canton

− Existence of a privileged status? e.g. mixed, domicile or principal company

First assessment concerning relevancy/applicability of the transitional measures

Determination of the existing hidden reserves/goodwill in accordance with an accepted valuation method

Detailed calculation/simulation in order to evaluate the preferred transitional measure

Communication with the responsible tax authority, including tax ruling

No general rule, individual case needs to be considered!

13© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

Checklist for future structures− If patents are in place – assessment of patent box

Identification of qualifying IP

Consideration of modified nexus approach based on R&D expenses incurred

Calculation/simulation of expected effect (cost-benefit analysis) including considering the costs of theentry taxation

Definition of the boxes and potential adjustment of accounting system for easier application

Define process to prepare required documentation tracking and tracing

Communication with the responsible tax authority, including tax ruling

− In case of domestic R&D expenses – assessment of additional R&D deductions

Identification of qualifying research and development expenses

− In case of group financing activities – assessment of NID

Assessment and calculation/simulation of expected effect of notional interest deduction (likely only available in the canton of Zurich) – expected minimum tax rate of finance companies in Zurich will be approx. 11-12% vs. lowest ordinary tax rates of approx. 12% in specific cantons

14© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

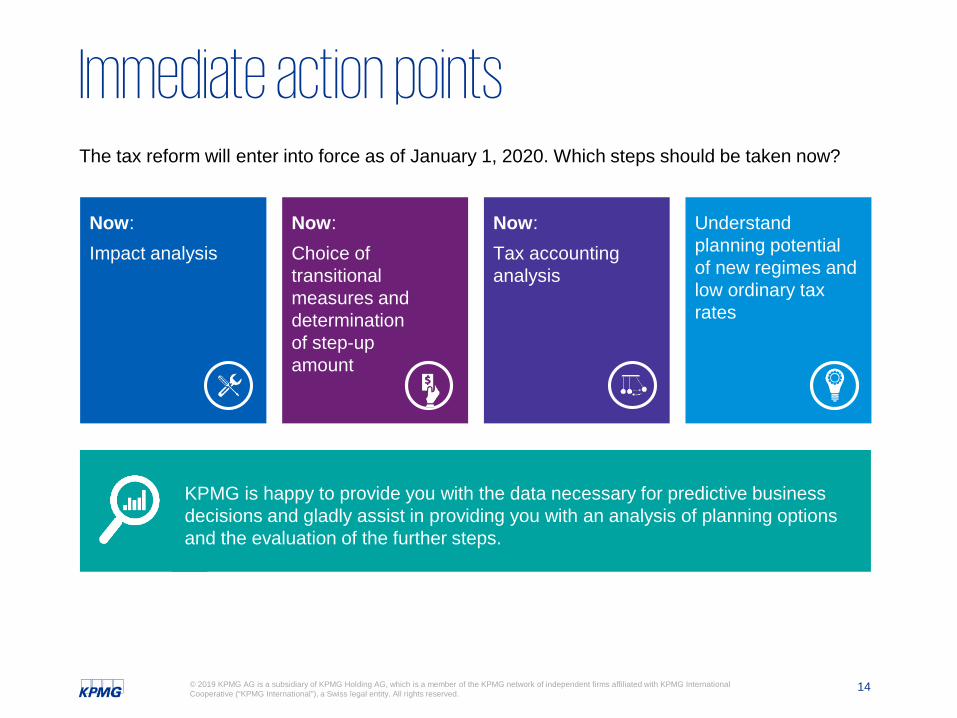

Immediate action points

Now: Impact analysis

Now: Tax accounting analysis

Now: Choice of transitional measures and determination of step-up amount

Understand planning potential of new regimes and low ordinary tax rates

KPMG is happy to provide you with the data necessary for predictive business decisions and gladly assist in providing you with an analysis of planning options and the evaluation of the further steps.

The tax reform will enter into force as of January 1, 2020. Which steps should be taken now?

15© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

ContactsPeter Uebelhart

Partner

Tax

+41 58 249 42 24

Olivier Eichenberger

Director

Corporate Tax

+41 58 249 41 67

Annex

Transitional measures (change from privileged to ordinary tax status)

18© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

Special tax rate solution – example

“Basket B”will be taxed at “special” reduced tax rate (e.g. 2%)

Annu

al p

rofit

0

“Basket A”Will be taxed at ordinary cantonal/communal tax rate (e.g. 9%)

Example:Hidden reserves of Company A amount to 500(can be allocated over 5 years)

Annual profit year 2020: 250100 will be taxed at ordinary cantonal/communal tax rate (Basket A)

And 150 could be allocated to «special» tax rate (Basket B)

150

100

250

The division of the profit of 250 into 100 and 150 is to be understood as a fictitious example to illustrate the method. In principle, it is independent of the total hidden reserves mentioned in the example. The decisive factor for the allocation to the special rate is which part of the profit of 250 is based on the realisation of already existing hidden reserves that were not previously taxed.

19© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

Reduction of the taxable income(Effect on cantonal income tax)

1,000

taxa

ble

prof

itde

prec

iatio

nst

ep-u

p

0

Step-up amount 2500./. Year 1 - 250./. Year 2 - 250(…) (…)./. Year 10* - 250

Remaining amount 0

Current law Step-up – exampleAn

nual

pro

fit

250

750

1,000

*Depreciation period dependson cantonal practice

Overall limitation of measures

21© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

Overall limitation of measures

R&

D s

uper

ded

uctio

n

Cur

rent

law

ste

p-up

dep

r.

Pate

nt b

oxMinimum profit of 20% of taxable profits

before set off losses carried forwardMinimum income of 30% of taxable income before loss carry forwards (approach per entity)

Maximum deduction of70% of taxable income before loss carryforwards and excluding participation income

Not

iona

l int

eres

t ded

uctio

n

Snapshot of theproposed cantonalimplementation

23© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

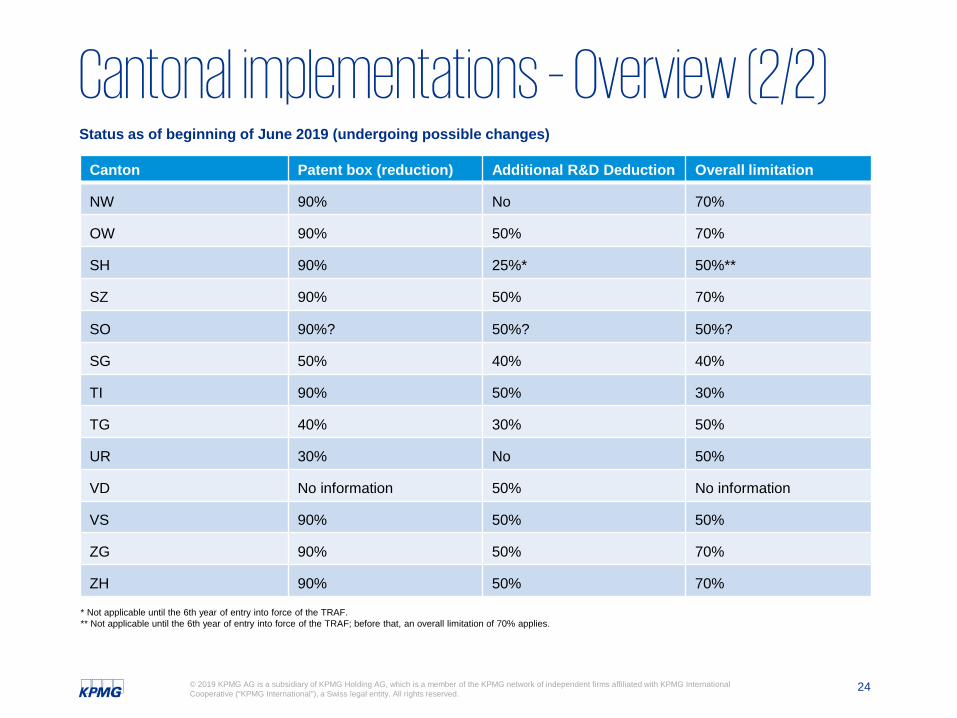

Cantonal implementations – Overview (1/2)Status as of beginning of June 2019 (undergoing possible changes)

Canton Patent box (reduction) Additional R&D Deduction Overall limitation

AG 90% 50% 70%

AR 50% 50% 50%

AI 10% No 50%

BL 90% 20% 50%

BS 90% No 40%

BE 90% 50% 70%

FR 90% 50% 20%

GE 10% 50% 9%

GL 10% No 10%

GR 70% No 70%

JU 90% 50% 70%

LU 10% No 70%

NE 20% 50% 40%

24© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.

Cantonal implementations – Overview (2/2)Canton Patent box (reduction) Additional R&D Deduction Overall limitation

NW 90% No 70%

OW 90% 50% 70%

SH 90% 25%* 50%**

SZ 90% 50% 70%

SO 90%? 50%? 50%?

SG 50% 40% 40%

TI 90% 50% 30%

TG 40% 30% 50%

UR 30% No 50%

VD No information 50% No information

VS 90% 50% 50%

ZG 90% 50% 70%

ZH 90% 50% 70%

Status as of beginning of June 2019 (undergoing possible changes)

* Not applicable until the 6th year of entry into force of the TRAF.** Not applicable until the 6th year of entry into force of the TRAF; before that, an overall limitation of 70% applies.

kpmg.ch/socialmedia

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received, or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation. The scope of any potential collaboration with audit clients is defined by regulatory requirements governing auditor independence. If you would like to know more about how KPMG AG processes personal data, please read our Privacy Policy, which you can find on our homepage at www.kpmg.ch.

© 2019 KPMG AG is a subsidiary of KPMG Holding AG, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved.