® international accounting standards board financial accounting standards board updating iasb –...

TRANSCRIPT

®

International Accounting Standards

Board

FinancialAccounting Standards

Board

Updating IASB – FASB Updating IASB – FASB Memorandum of UnderstandingMemorandum of Understanding

Wayne Upton – IASB Director, International ActivitiesWayne Upton – IASB Director, International ActivitiesSue Bielstein – FASB DirectorSue Bielstein – FASB Director

The views expressed in this presentation are those of the The views expressed in this presentation are those of the presenter, not those of the IASB or FASBpresenter, not those of the IASB or FASB

®

2

First, Who are these people?First, Who are these people? IASC was founded circa 1972, about the same IASC was founded circa 1972, about the same

time as the FASBtime as the FASB A part-time board with limited staff resourcesA part-time board with limited staff resources Reorganized in 2001Reorganized in 2001 A full-time board ( two part-time members) and a A full-time board ( two part-time members) and a

greatly expanded professional staffgreatly expanded professional staff Members chosen based on criteria similar to Members chosen based on criteria similar to

those used by the FASBthose used by the FASB Board members are not “representatives” of Board members are not “representatives” of

geographical or “background” constituenciesgeographical or “background” constituencies

®

3

Evolution of the IASB – FASB Evolution of the IASB – FASB Convergence ProgramConvergence Program

First step, The Norwalk AgreementFirst step, The Norwalk Agreement Shared goal: high-quality, compatible standards that can be Shared goal: high-quality, compatible standards that can be

used for domestic and cross-border financial reportingused for domestic and cross-border financial reporting Means: converge by eliminating differences in existing Means: converge by eliminating differences in existing

standardsstandards Result: a slow process that produced improved standards but Result: a slow process that produced improved standards but

often failed to eliminate all differencesoften failed to eliminate all differences The SEC 2005 road map to eliminating the 20-F The SEC 2005 road map to eliminating the 20-F

reconciliation requirement reconciliation requirement The 2006 Memorandum of UnderstandingThe 2006 Memorandum of Understanding

Shift in goal: common, high-quality standards Shift in goal: common, high-quality standards Shift in means: improve and converge -- serving investor Shift in means: improve and converge -- serving investor

needs means the boards converging by replacing weaker needs means the boards converging by replacing weaker standards with stronger, common standards.standards with stronger, common standards.

®

4

The MoU – setting 2008 goals for The MoU – setting 2008 goals for 11 major projects11 major projects

Business combinations, Business combinations, complete convert standardcomplete convert standard

Consolidations, work Consolidations, work aimed at development of aimed at development of converged standardsconverged standards

Fair value measurement Fair value measurement guidance, to have issued guidance, to have issued converged guidanceconverged guidance

Liabilities and equity Liabilities and equity distinctions, one or more distinctions, one or more due process documentsdue process documents

IFRS 3 and SFAS 141R IFRS 3 and SFAS 141R issuedissued

Work continuesWork continues

FASB standard issued; FASB standard issued; Discussion paper issued Discussion paper issued by IASBby IASB

IASB and FASB have both IASB and FASB have both issued initial documentsissued initial documents

®

5

The MoU – setting 2008 goals for The MoU – setting 2008 goals for 11 major projects11 major projects

Financial statement Financial statement presentation, one or more presentation, one or more due process documentsdue process documents

Postretirement benefits, Postretirement benefits, one or more due process one or more due process documentsdocuments

Revenue recognition, one Revenue recognition, one or more to process or more to process documentsdocuments

Derecognition, one or Derecognition, one or more due process more due process documentsdocuments

Joint initial document Joint initial document expected by summerexpected by summer20082008

FASB issued new FASB issued new standard, IASB issued standard, IASB issued discussion documentdiscussion document

Joint initial document Joint initial document expected by summerexpected by summer20082008

Work proceedingWork proceeding

®

6

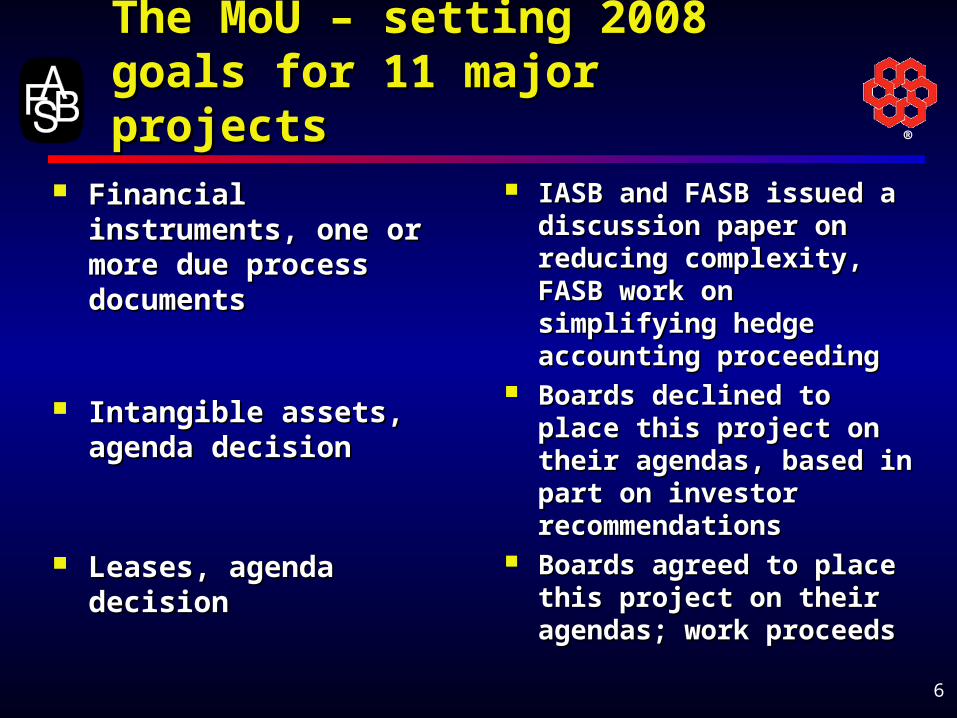

The MoU – setting 2008 goals for The MoU – setting 2008 goals for 11 major projects11 major projects

Financial instruments, one Financial instruments, one or more due process or more due process documentsdocuments

Intangible assets, agenda Intangible assets, agenda decisiondecision

Leases, agenda decisionLeases, agenda decision

IASB and FASB issued a IASB and FASB issued a discussion paper on discussion paper on reducing complexity, FASB reducing complexity, FASB work on simplifying hedge work on simplifying hedge accounting proceedingaccounting proceeding

Boards declined to place Boards declined to place this project on their this project on their agendas, based in part on agendas, based in part on investor recommendationsinvestor recommendations

Boards agreed to place Boards agreed to place this project on their this project on their agendas; work proceedsagendas; work proceeds

®

7

It’s now 2008 and time to update It’s now 2008 and time to update the MoUthe MoU

The April 2008 joint Board meetingThe April 2008 joint Board meeting Agreement on a June 2011 target for completion Agreement on a June 2011 target for completion

of major projectsof major projects Building “improved” IFRS as a platform for Building “improved” IFRS as a platform for

jurisdictions moving down IFRS in the next few jurisdictions moving down IFRS in the next few yearsyears

®

8

Why June 2011?Why June 2011? Widespread frustration among constituents about Widespread frustration among constituents about

the slow pace of board projectsthe slow pace of board projects Sharpening our focus – what improvements in Sharpening our focus – what improvements in

financial reporting are important to investorsfinancial reporting are important to investors Imposing discipline on ourselvesImposing discipline on ourselves Avoiding potential for doubling up on changes in Avoiding potential for doubling up on changes in

those jurisdictions adopting IFRSthose jurisdictions adopting IFRS

®

9

MoU: Plans for Completion by MoU: Plans for Completion by 20112011

Revenue recognitionRevenue recognition Two possible models, both based on an asset – liability Two possible models, both based on an asset – liability

approachapproach Key issuesKey issues

Identifying performance obligations and how they are satisfied When should the measurement of a performance obligation

change for reasons other than performance Accounting for conditional obligations such as rights of return Disclosure Testing

®

10

MoU: Plans for Completion by MoU: Plans for Completion by 20112011

Fair value measurement guidanceFair value measurement guidance Key issues for the IASBKey issues for the IASB

SFAS 157 exit value, or is there a complementary entry value? Fair value is more common in IFRS than in US GAAP, several

standards will need to be amended

Consolidation policyConsolidation policy Heightened attention brought on by the current banking Heightened attention brought on by the current banking

environmentenvironment Key issuesKey issues

Effective control Applicability to special-purpose entities and others. Is there a

better way to capture the principles inherent in FIN 46R?

®

11

MoU: Plans for Completion by MoU: Plans for Completion by 20112011

DerecognitionDerecognition Again, heightened attention brought on by the current Again, heightened attention brought on by the current

environmentenvironment Neither IASB nor FASB has the best standard in this area, Neither IASB nor FASB has the best standard in this area,

work proceeds to developing a better approach for the work proceeds to developing a better approach for the October 2008 joint Board meetingOctober 2008 joint Board meeting

®

12

MoU: Plans for Completion by MoU: Plans for Completion by 20112011

Financial statement presentationFinancial statement presentation Key issuesKey issues

Presentation, not recognition and measurement The cohesiveness principle and a new format or all three

statements The role of net income, comprehensive income, and recycling Initial testing already performed and it will continue during the

comment period on the upcoming discussion document

®

13

MoU: Plans for Completion by MoU: Plans for Completion by 20112011

Postretirement benefitsPostretirement benefits The IASB discussion paperThe IASB discussion paper

Places the full obligation on the balance sheet, but Argues for including changes in the obligation in net income

and/or comprehensive income and examines different approaches to doing so

The “leap frog” phenomenon – IASB project may create new The “leap frog” phenomenon – IASB project may create new differencesdifferences

Measurement of so-called cash balance plans Income statement presentation

No broadly scoped, joint phase 2 project for nowNo broadly scoped, joint phase 2 project for now

®

14

MoU: Plans for Completion by MoU: Plans for Completion by 20112011

Lease accounting, a focus on lessee accounting Lease accounting, a focus on lessee accounting for now. Lessor accounting to wait for revenue for now. Lessor accounting to wait for revenue recognition.recognition. Key issuesKey issues

Getting lease obligations on the balance sheet -- operating leases would be reported as an intangible asset and the lease obligation as a liability

Can we focus on the substantive lease term as the unit of account?

Can we address lessee accounting without debating changes to amortization and depreciation accounting?

Can we avoid reconsidering areas in which current lease accounting provides answers, even if those answers are imperfect?

®

15

MoU: Plans for Completion by MoU: Plans for Completion by 20112011

Financial InstrumentsFinancial Instruments FASB work on hedge accountingFASB work on hedge accounting IASB Discussion Paper on reducing complexityIASB Discussion Paper on reducing complexity

Approaches to classification of financial instruments Approaches to hedge accounting Is fair value to only way to eliminate complexity?

®

16

Thinking about the fair value and Thinking about the fair value and financial instrumentsfinancial instruments

Criteria to distinguish between types of financial instruments (‘classification’)

Identification and quantification of impairment

Transfers between measurement categories of financial instruments

Would not be required

Would not be required

Would not be required

®

17

Thinking about the fair value and Thinking about the fair value and financial instrumentsfinancial instruments

Hedge accounting Fair value hedge accounting—no measurement mismatches between financial instruments. There may be other recognition and measurement mismatches (eg those relating to non-financial instruments); in such circumstances, there will be demand for fair value hedge accounting.

Cash flow hedge accounting—there will be demand for hedge accounting for exposures to changes in expected future cash flows.

®

18

Thinking about fair value and Thinking about fair value and financial instrumentsfinancial instruments

Identification and separation of embedded derivatives

Not applicable for financial instruments. May still be required for other items (eg non-financial instruments with embedded derivatives).

®

19

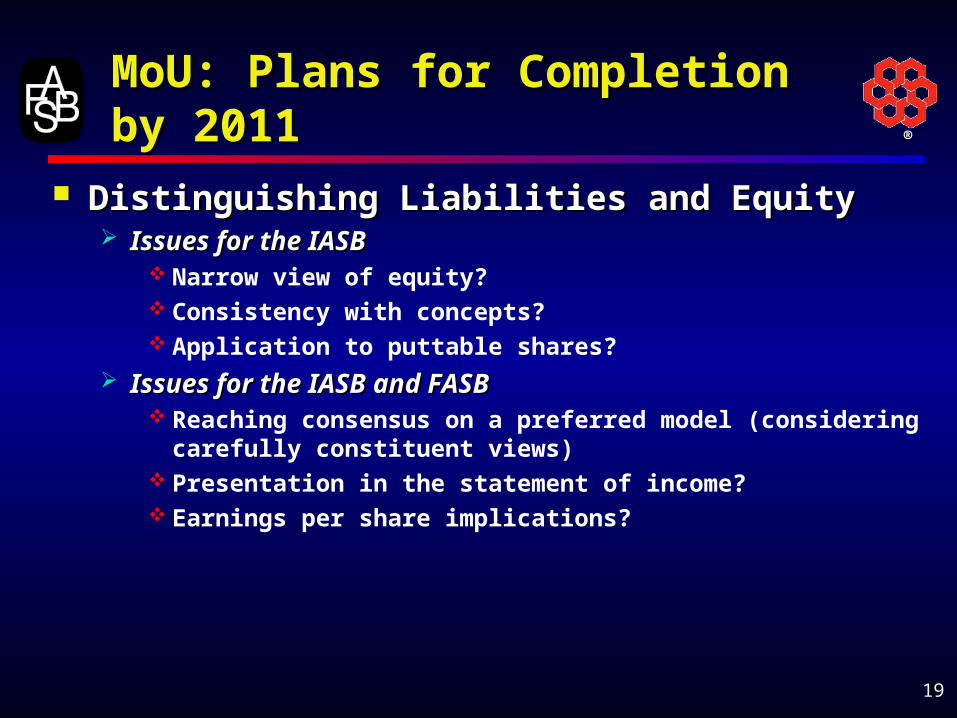

MoU: Plans for Completion by MoU: Plans for Completion by 20112011

Distinguishing Liabilities and EquityDistinguishing Liabilities and Equity Issues for the IASBIssues for the IASB

Narrow view of equity? Consistency with concepts? Application to puttable shares?

Issues for the IASB and FASBIssues for the IASB and FASB Reaching consensus on a preferred model (considering carefully

constituent views) Presentation in the statement of income? Earnings per share implications?

®

20

MoU: What about short-term MoU: What about short-term convergence?convergence?

Differences are narrow but the possible changes are often Differences are narrow but the possible changes are often significant and contentious significant and contentious

Some question whether the benefits justify the resources Some question whether the benefits justify the resources Projects often took many years to completeProjects often took many years to complete The scopes were often narrow, addressing some but not all The scopes were often narrow, addressing some but not all

differencesdifferences Two scope recommendationsTwo scope recommendations

Complete projects in process (earnings per share, joint ventures, Complete projects in process (earnings per share, joint ventures, income taxes)income taxes)

Defer work on all others (investment property, impairment of long-Defer work on all others (investment property, impairment of long-lived assets, research and development)lived assets, research and development)

Allocate Board time and staff resources to other, higher priority Allocate Board time and staff resources to other, higher priority improvementsimprovements

Income taxes – a possible change in approachIncome taxes – a possible change in approach FASB would propose to replace FAS 109 with the revised IAS 12FASB would propose to replace FAS 109 with the revised IAS 12

®

21

A U.S. PerspectiveA U.S. PerspectiveWhat Exactly is the End Goal?What Exactly is the End Goal?

““Common,” “high-quality” financial reportingCommon,” “high-quality” financial reporting by by listed listed companiescompanies (perhaps others) around the world (perhaps others) around the world

That system requires several elementsThat system requires several elements Single set of high-quality accounting standards established by a Single set of high-quality accounting standards established by a

single, independent standard settersingle, independent standard setter Mechanisms for consistent application and interpretation Mechanisms for consistent application and interpretation

internationallyinternationally Common, high-quality disclosures outside of financial Common, high-quality disclosures outside of financial

statements and a common delivery systemstatements and a common delivery system High-quality auditing standards and practiceHigh-quality auditing standards and practice Common approach to regulation and enforcementCommon approach to regulation and enforcement

Accounting standards have been leading the wayAccounting standards have been leading the way

®

22

Accounting standards internationallyAccounting standards internationally Over 100 counties have or will adopt IFRS, butOver 100 counties have or will adopt IFRS, but

“As adopted” versions of IFRS National flavors due to application differences

Accounting standards in the U.S.Accounting standards in the U.S. Active convergence program with IASBActive convergence program with IASB Active dialog with other standard setters around the worldActive dialog with other standard setters around the world FASB actively improving/maintaining other US GAAPFASB actively improving/maintaining other US GAAP

Addressing weaknesses (e.g., derecognition, consolidation) On-going interpretative function

Less focus (but some progress) on common auditing Less focus (but some progress) on common auditing standards and practices and cooperative efforts standards and practices and cooperative efforts between securities regulators and PCAOB and between securities regulators and PCAOB and international counterpartsinternational counterparts

A U.S. PerspectiveA U.S. PerspectiveWhere are we now?Where are we now?

®

23

A U.S. PerspectiveA U.S. PerspectiveWhere should we be going?Where should we be going?

Internationally? Internationally? In U.S.?In U.S.?

®

24

A U.S. PerspectiveA U.S. PerspectiveWhat’s needed internationallyWhat’s needed internationally

Address national/regional endorsement mechanisms Address national/regional endorsement mechanisms that produce “as adopted” versions of IFRSthat produce “as adopted” versions of IFRS

More consistent application of IFRS to avoid More consistent application of IFRS to avoid “national flavors”“national flavors”

Further strengthen IFRSFurther strengthen IFRS IASB to fill in major gaps (e.g., insurance, extractive industries, rate IASB to fill in major gaps (e.g., insurance, extractive industries, rate

regulation?)regulation?) Improve major areas (e.g., per FASB – IASB MOU)Improve major areas (e.g., per FASB – IASB MOU)

Strengthening IASB as a global standard setterStrengthening IASB as a global standard setter Funding — ongoing efforts by IASC Foundation TrusteesFunding — ongoing efforts by IASC Foundation Trustees StaffingStaffing Governance/Oversight — proposed regulatory “monitoring body”Governance/Oversight — proposed regulatory “monitoring body” Structure? (e.g., having multiple locations?)Structure? (e.g., having multiple locations?)

Improve coordination of global regulatory review and Improve coordination of global regulatory review and enforcementenforcement

®

25

A U.S. PerspectiveA U.S. PerspectiveWhat’s needed in the US?What’s needed in the US?

Decide on an end game:Decide on an end game: ““Mutual recognition” for foreign filers onlyMutual recognition” for foreign filers only

With continued convergence over many years Without convergence (perhaps competition between standards)

Two-GAAP System for U.S. RegistrantsTwo-GAAP System for U.S. Registrants With continued convergence over many years Without convergence (perhaps competition between standards)

A single set of hiqh-quality international standardsA single set of hiqh-quality international standards

Each path has very different implications:Each path has very different implications: Standard setters, preparers, auditors, investors, regulators, educators Standard setters, preparers, auditors, investors, regulators, educators Overall system costs and complexityOverall system costs and complexity

®

26

FASB and FAF View of End GameFASB and FAF View of End Game Single Set of Quality International Single Set of Quality International StandardsStandards

Preferred by investors — enhances Preferred by investors — enhances comparability, reduces analytical complexitycomparability, reduces analytical complexity

Consistent with globalization of capital marketsConsistent with globalization of capital markets Would bring U.S. into alignment with most other Would bring U.S. into alignment with most other

international capital markets (Europe, Australia, international capital markets (Europe, Australia, China, Russia, Japan, Korea, Canada, India, etc.)China, Russia, Japan, Korea, Canada, India, etc.)

Avoids added costs and complexity of a two – Avoids added costs and complexity of a two – GAAP system for an extended periodGAAP system for an extended period

We advocate a well planned “improve and adopt” We advocate a well planned “improve and adopt” approach to transitioning U.S. to IFRSapproach to transitioning U.S. to IFRS

– Improvement through continued joint projects between IASB and FASB in major areas

– Directly adopt other parts of IFRS

®

27

27

U.S. Adoption of IFRS?U.S. Adoption of IFRS?A complex, multi-year effortA complex, multi-year effort

Requires consideration of many issuesRequires consideration of many issues Private company reporting (IFRS, IFRS-SME, US GAAP?)Private company reporting (IFRS, IFRS-SME, US GAAP?) Role of FASBRole of FASB Implications for company systems, internal controls, data Implications for company systems, internal controls, data

gatheringgathering Education, training, CPA exams, etc.Education, training, CPA exams, etc. Possible changes to contracts, regulatory requirements, state Possible changes to contracts, regulatory requirements, state

lawslaws Evaluating SEC accounting and disclosure requirements Evaluating SEC accounting and disclosure requirements

(both within and without the financial statements(both within and without the financial statements First time adoption issuesFirst time adoption issues XBRLXBRL

FAF/FASB Forum to consider those and other issuesFAF/FASB Forum to consider those and other issues

®

28

A US PerspectiveA US PerspectiveSummary ThoughtsSummary Thoughts

FASB Remains Committed to ConvergenceFASB Remains Committed to Convergence Single set of high-quality common standardsSingle set of high-quality common standards Goal is improved reporting, not convergence for the sake of Goal is improved reporting, not convergence for the sake of

convergenceconvergence Significant Resources Devoted to this EffortSignificant Resources Devoted to this Effort Convergence Considerations Embedded in our ProcessConvergence Considerations Embedded in our Process

Uncertainty about the path forward in the USUncertainty about the path forward in the US Which end state scenario?Which end state scenario? When and how will it be decided?When and how will it be decided? When might it be implemented?When might it be implemented? Who will be impacted (public companies, private companies, Who will be impacted (public companies, private companies,

NFPs)?NFPs)? One thing is certain – there will be changeOne thing is certain – there will be change

®

29

Expressions of individual views by members of the IASB, FASB and their staff are encouraged. The views expressed in this presentation are those of the presenters. Official positions of the IASB or the FASB on accounting matters are determined only after extensive due process and deliberation.

Questions and commentsQuestions and comments