© paul atherton 2006 commercialising nanotechnology

TRANSCRIPT

© Paul Atherton 2006

Commercialising Nanotechnology

© Paul Atherton 2006

Nanotechnology

• not a useful description of technology – many different nanotechnologies

• not a useful description of markets or applications

• principal use is for Funding agencies– UK, US, EU and VC– Beware re-labelling of existing activities

© Paul Atherton 2006

Types of Nanotechnology

• Top down - Engineering Nanotechnology– miniaturisation of macroscopic devices– Micro Systems Technology (MST) – ink jet printers, disk drive

heads, air bag sensors, Pentium chips– Tools: wafer steppers, SPM, SEM, Nanomanipulators

• Bottom Up – Molecular Nanotechnology– atom by atom, molecule by molecule

• Drexler’s Molecular machines– Chemistry – nanoparticles, fullerenes– Physics – quantum dots – Biology – was always nanotechnology– Quantum effects become important at the nanoscale

• Top Down is probably nearer market than Bottom Up

© Paul Atherton 2006

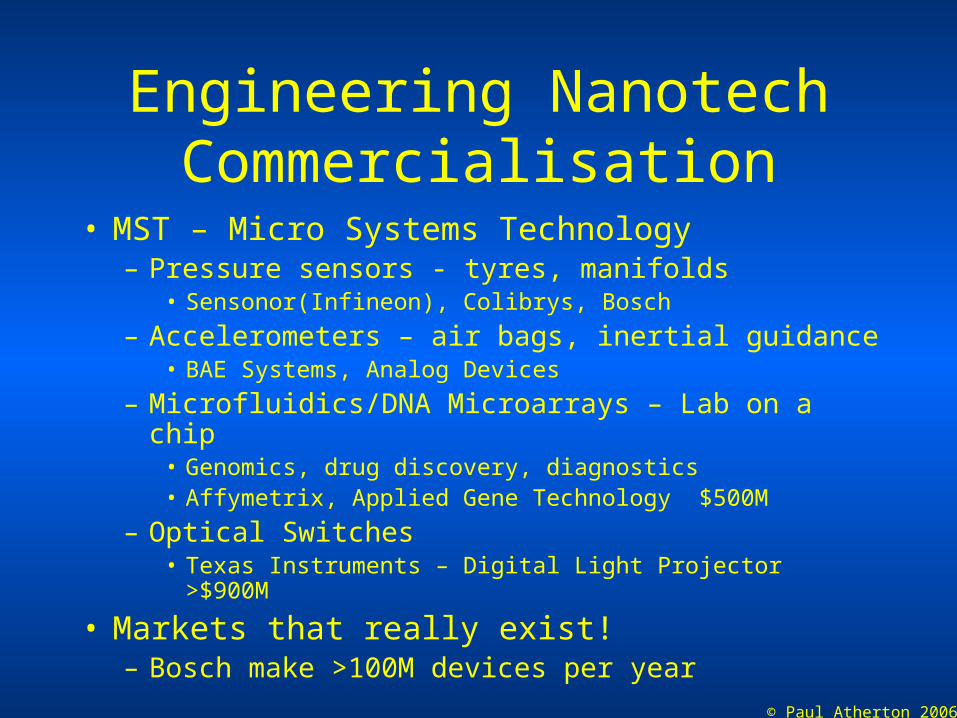

Engineering Nanotech Commercialisation

• MST – Micro Systems Technology– Pressure sensors - tyres, manifolds

• Sensonor(Infineon), Colibrys, Bosch

– Accelerometers – air bags, inertial guidance• BAE Systems, Analog Devices

– Microfluidics/DNA Microarrays – Lab on a chip• Genomics, drug discovery, diagnostics• Affymetrix, Applied Gene Technology $500M

– Optical Switches• Texas Instruments – Digital Light Projector >$900M

• Markets that really exist!– Bosch make >100M devices per year

© Paul Atherton 2006

Nano Tools

• Microscopes– SPM – Veeco, NanoInk, Infinitesima– SEM – FEI, JEOL, Hitachi etc

• Steppers – ASML, Canon, Nikon

• Coatings – EVG, Unaxis

• DRIE – STS, Suss Microtech

• Nano Manipulators – Zyvex, Klocke,

© Paul Atherton 2006

Nanotech Commercialisation

• >500 companies globally

• 1/3 in Nanoparticles

• >55 companies in Carbon Nanotubes– Of which >20 in large scale production

© Paul Atherton 2006

Nanotech Commercialisation Activity

• Fullerenes– Carbon buckyballs – Carbon nanotubes

• Single wall

• Multi wall

• Nanoparticles– 5nm TiO2, AlNi, metal shells, caged atoms

© Paul Atherton 2006

Fullerenes Carbon Buckyballs and Nanotubes

• Physical Strength

• Electrical conductivity

• Thermal conductivity

• Scaffolds - bio-pharma

• Caged atoms – quantum effects

• Nanowires

© Paul Atherton 2006

Fullerenes – Start ups 1Volume production

• Nanoledge – (France)– Large scale production (4 ounce per day) tennis

racquets, fibers.

• Mitsui CNRI (Akashima, Tokyo)– (new nanotube plant– 120 tons per year at 10% present

cost)

• Frontier Carbon (Kitakyusyu City) – Mitsubishi– large scale M/F 400kg per year– 1500 tons by 2007

© Paul Atherton 2006

Fullerenes Start Ups 2‘Functionalised’

• Carbon Nanotechnologies – Richard Smalley ($15M - angels)– Single walled and functionalised tubes

• Nantero (>$20M – DFJ and others)– NRAM™, a high-density

nonvolatile random access memory chip • Molecular Nanosystems

– Stanford ($2M – band of angels)– Nanotube sensors

• C Sixty – ($4M – CNI-angels)– Protease inhibitor – anti HIV– Dec 2004 – merged with CNI

© Paul Atherton 2006

Fullerenes Commercialisation

• Very broad applications• Entry of large manufacturing companies

– Already second movers appearing

• Price dropping rapidly• Clear specialisations developing

– market focus– Co-development deals– No IPOs yet……– NEC and Samsung

© Paul Atherton 2006

Nanoparticles

• Catalysts

• Functional materials and coatings

• Ceramics

• Drug Delivery

© Paul Atherton 2006

Nanoparticles• NanoPhase Technologies (Nasdaq)• Ntera ($30M)

– was Li-ion batteries – now nanochromic displays• Nanogram ($6.7M) – nanomaterials• Aveka (buy out from 3M) – particle processing• Oxonica ($4M) sunscreens, bio tags, catalysts.

– Floated on Aim 2005 • Quantum Dot Corp ($37M) – bio-assays

– Acquired by Invitrogen oct 2005• Nanosphere ($10 million)

– Gold nanoparticle DNA probes for bio-threat detection ( anthrax) • Qinetiq nanomaterials• Nanomagnetics – was data storage – now water

purification - Apaclara

© Paul Atherton 2006

Nanoparticles

• Capacity and cost

• Scale up issues

• Production technology– Plasma vs precipitation

• New start ups vs existing players :

• Degussa, Cabot Corp, Johnson Matthey

• BASF, Altana

© Paul Atherton 2006

Nanophase Nanosys and Oxonica

• Nanophase – first Nanotech IPO– Over valued

• Nanosys – the hyped Nanotech IPO– Over sold

• Oxonica – an unexpected IPO– Over diluted

© Paul Atherton 2006

NanoPhase Technologies

• Patents licensed from Argonne – 1990

• Zinc oxide nanoparticles – sunscreens

• Catalysts

• Floated on Nasdaq – 1998

• Early Nanotech IPO

• Rode technology wave

• Look at recent history……

© Paul Atherton 2006

Nanophase • 1998 Over hyped IPO

– paid compensation of $4.8M (Jan 2002)

• Nov 2001 Layoffs – insufficient demand• Growth, but quite volatile

– Customer delays– major customer - sunscreen

• 03Q1 revenues $1.66M 03Q2 $1.3M• Losing about $1.3M per quarter

© Paul Atherton 2006

NanoPhase update

• 25/03/2004• Altana Chemie AG – acquires 7% for $10M

– Speciality chemicals business– 2 year lock up– 8 year strategic agreement– c.f. BASF investment in Oxonica….

• $1.7M Revenues for quarter ended Sept 30 2005• Net loss for quarter - $1.53M• Q1 2006 – Revenue rises to $2M – net loss $1.5M

© Paul Atherton 2006

Market Cap $120M

© Paul Atherton 2006

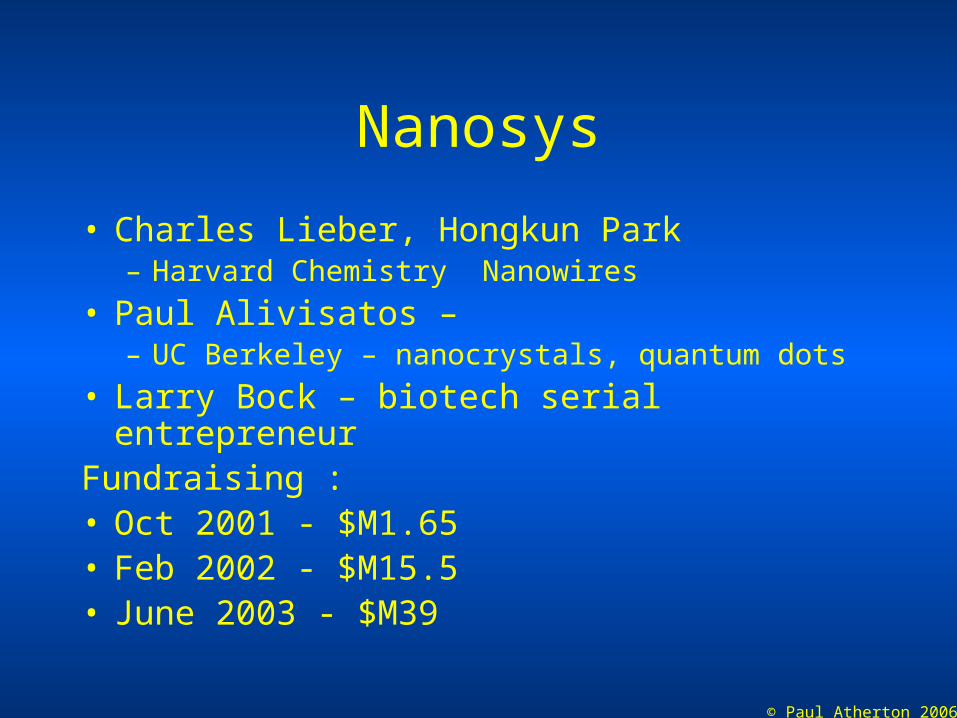

Nanosys

• Charles Lieber, Hongkun Park– Harvard Chemistry Nanowires

• Paul Alivisatos – – UC Berkeley – nanocrystals, quantum dots

• Larry Bock – biotech serial entrepreneurFundraising :• Oct 2001 - $M1.65• Feb 2002 - $M15.5• June 2003 - $M39

© Paul Atherton 2006

Nanosys

• Bio-sensors – functionalised inorganic semiconductor nanowires– 1D electron flow highly sensitive and selective

• Photovoltaics – nanocrystals in host matrix– Solar cells as roof tiles (Matsushita contract)

• Macroelectronics – flexible low cost substrate• Nanostructured surfaces

– Hydrophobic and anti-microbial surfaces

© Paul Atherton 2006

Nanosys• Land Grab IP strategy

– > 120 patents owned or licensed• Licensed portfolios from world class scientists and

institutions– Lawrence Berkeley - Alivisatos, McEuen– UC Berkeley - Yang– Harvard – Lieber, Park– MIT - Bawendi – Columbia - Brus– UCLA - Heath– Yussum, Hebrew Univ of Jerusalem – Banin– Chicago – Guyot-Sionnest

• The Scientific Advisory Board• Annual Revenues ~$3M

© Paul Atherton 2006

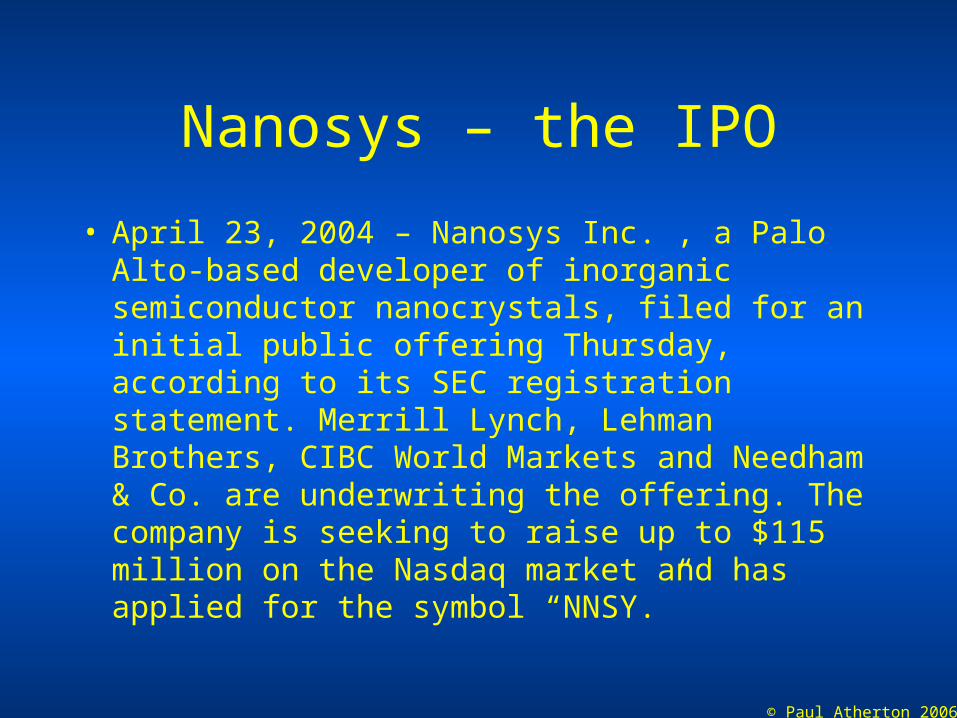

Nanosys – the IPO

• April 23, 2004 – Nanosys Inc. , a Palo Alto-based developer of inorganic semiconductor nanocrystals, filed for an initial public offering Thursday, according to its SEC registration statement. Merrill Lynch, Lehman Brothers, CIBC World Markets and Needham & Co. are underwriting the offering. The company is seeking to raise up to $115 million on the Nasdaq market and has applied for the symbol “NNSY.”

© Paul Atherton 2006

NANOSYS WITHDRAWS IPO

Aug. 4, 2004 – Nanosys Inc. has announced the withdrawal of its IPO. The Palo Alto, Calif.-based nanotech startup was expected to go public this week or early next week.

• "Based on adverse market conditions," the company said in a news release, "Nanosys has determined that it is not advisable at this time to proceed with the proposed offering."

• The company had proposed selling 6.25-million shares of stock and estimated the price between $15 and $17 per share.

© Paul Atherton 2006

• Press reports leading up to the expected week of the IPO lambasted Nanosys for having only $3 million in revenues in 2003. It was also pointed out that one of the few hard metrics available to value the firm - a price-to-revenue ratio over 120 - suggested it was a speculative investment, and that if it performed poorly, it would undermine the ability of other nanotechnology firms to access the public markets.

© Paul Atherton 2006

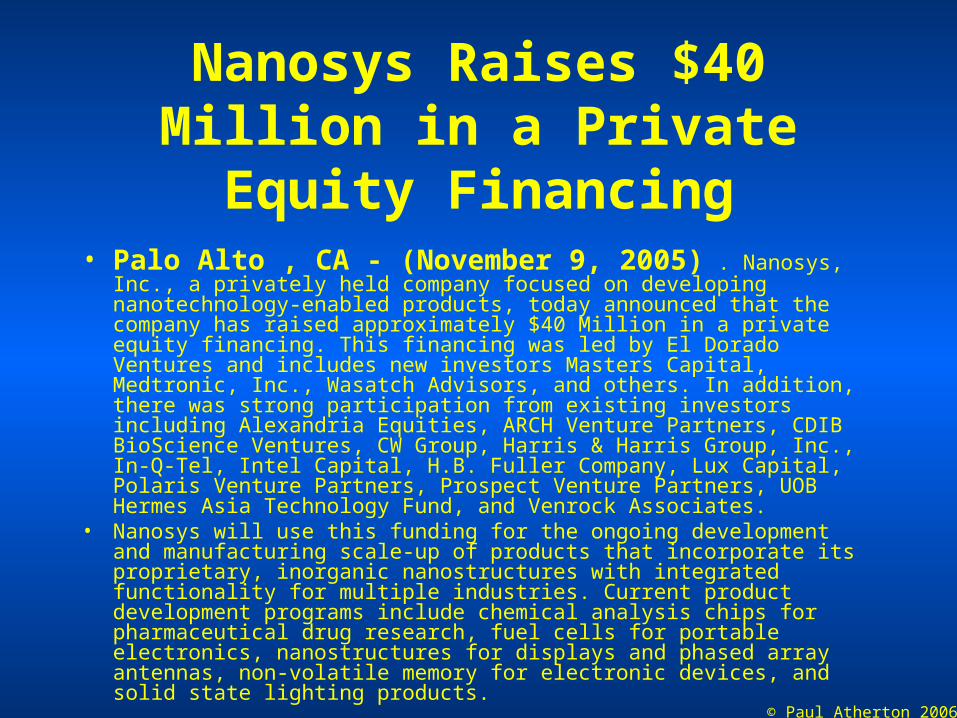

Nanosys Raises $40 Million in a Private Equity Financing

• Palo Alto , CA - (November 9, 2005) . Nanosys, Inc., a privately held company focused on developing nanotechnology-enabled products, today announced that the company has raised approximately $40 Million in a private equity financing. This financing was led by El Dorado Ventures and includes new investors Masters Capital, Medtronic, Inc., Wasatch Advisors, and others. In addition, there was strong participation from existing investors including Alexandria Equities, ARCH Venture Partners, CDIB BioScience Ventures, CW Group, Harris & Harris Group, Inc., In-Q-Tel, Intel Capital, H.B. Fuller Company, Lux Capital, Polaris Venture Partners, Prospect Venture Partners, UOB Hermes Asia Technology Fund, and Venrock Associates.

• Nanosys will use this funding for the ongoing development and manufacturing scale-up of products that incorporate its proprietary, inorganic nanostructures with integrated functionality for multiple industries. Current product development programs include chemical analysis chips for pharmaceutical drug research, fuel cells for portable electronics, nanostructures for displays and phased array antennas, non-volatile memory for electronic devices, and solid state lighting products.

© Paul Atherton 2006

Oxonica

• Oxford University spin out – Pete Dobson,

• Inorganic Nanoparticles– Fuel additives (sunscreens (Soltan), bio-tags

• 1999 – angel round• 2002 - £4M investment (BASF and others)• 2004 - £4.2M investment• 2005 – AIM flotation

– raised £7.1M at market cap of £35M– Float price of 95.8p per share

© Paul Atherton 2006

Oxonica Market Capitalisation £60M

© Paul Atherton 2006

Oxonica

• Panmure Gordon 12 May 2006– Initiates coverage– Analyst issues BUY recommendation– Price target £2.00

© Paul Atherton 2006

Observations

• Few ‘pure play’ publicly quoted nanotech companies.

• ‘Profound’ nanotech companies have still to reach the market

• Valuations can be very high!!!

• Revenues are very low!!

• Big companies working hard on nanotech

© Paul Atherton 2006

• L’Oreal - >200 patents on nanoparticles

© Paul Atherton 2006

© Paul Atherton 2006

How will nanotech be commercialised ?

• Nanotechnology is mainly about processes• Licensing of process technology to large

companies• University spin outs – product based• Transfer of trained people• Long slow steady quiet process• Technology commercialisation is a slow

process – nanotech is pretty slow• Only start ups call themselves nanotech

companies

© Paul Atherton 2006

Investment Areas• Materials and Manufacturing

– Lighter stronger smarter materials, catalysts– Smart packaging, fuel cells and batteries

• Electronics and IT– Solar cells, semiconductors and storage, displays, RFIDS – Printable electronics (ink jet techniques)– Smart dust and ambient intelligence

• Healthcare– Regenerative medicine

• Artificial bone and skin– Drug Discovery– Diagnostics – point of care– Embedded devices (implants, monitors, pumps, pacemakers, cochlear

implants)– Personalised medicine

© Paul Atherton 2006

Thank You