leadingage · • to highlight the rapid pace of change and the need for organizations to think...

TRANSCRIPT

2

LeadingAge – expanding the world of possibilities for aging

LarsonAllen is a 2011 LeadingAge Partner

3

Perhaps now, more than ever before the rapidity and quantity of change may seem to

be overwhelming and suggest that organizations shouldn‘t think about their future, until

the changes are better known or better defined.

But given the magnitude of opportunity as well as the potential challenges, there‘s no

better time than the present to develop an understanding of the potential changes and

to think about how we sustain our mission in such times.

As a result, this document was created by LeadingAge and LarsonAllen ….

• to provide organizations with an overview of key trends in the aging services field,

the implications of those trends and possible responses

• to highlight the rapid pace of change and the need for organizations to think

strategically about the future

• to offer organizations a document that can be used to foster discussion and action

4

Lots of uncertainty.

That‘s why LeadingAge members have embraced a bold

transformational agenda to confront uncertainty and with a mission of

expanding the world of possibilities for aging.

LeadingAge‘s Five Big Ideas are:

1. Quality

2. Transition

3. Talent

4. Finance

5. Technology

6

There are two revolutions occurring within the field of aging

services:

1. a revolution in payment for facility-based services (and others) –

driven by all sorts of factors that will challenge the payment

stream for traditional providers of facility based health care

services; and

2. a revolution in innovation – in terms of how to most effectively

provide at home and consumer-preferred services. The CLASS

Act – offers a way to thrive during both ‗revolutions‘. (More on

the CLASS Act later in the presentation.)

7

8

• Think global – Act local.

• Instant consumer accountability for quality.

• Battle for talent.

• Technology is an integrator … not a goal.

Health care and aging services are driven by local culture, customs, and care delivery patterns. Successful

strategic planning will require a comprehensive understanding of:

• Demographic characteristics

• Local culture norms and consumer preferences

• Area health care practice patterns

• Current program and service offerings

• The decision-makers for buying decisions

• Competitor advantages and distinctive characteristics

• Referral source needs and challenges

New systems and technology will be necessary to support our understanding of local health care markets

and the unmet community need

There is not one solution for aging services. The spectrum is broad and decision must be made in the

context of organizational mission (primary purpose and driver) and with consideration of the organizational

vision.

Organizational strategies emanate from this context but require leadership to continuously scan the

environment to collect market trend information in aging services and health care as well as related fields

such as banking and retail. Doing so will increase the likelihood that aging services providers are creating

effective and targeted strategies.

This is a different economic environment than we have experienced in the past, and as a result, depending

solely on aging service trends or even healthcare may cause an organization to react too slowly or perhaps

to over-react to micro indicators.

As a set up for our discussion, we want you to think about five (5) key

trends that are hitting the field of aging services like a sledge-hammer.

Proactively addressing the issues is critical to our long term success.

These trends bring to light seven (7) implications – consider these the

items we (and all our colleagues in the field) should be discussing. Some

of the implications are similar to the trends but, as you begin to frame the

direct effects on your business, the conversation should be framed slightly

differently.

These implications cause us to consider six (6) key strategies – consider

these the strategies that every organization engaged in the field of aging

services (whether health care, residential or service oriented; or, catering

to a private population or third-party payers) should discuss and apply

appropriate to their market, position and financial situations.

9

#1

Whether the health care reform laws withstand the legal challenges, we believe that payment reform will occur

with a focus on increasing “value,” which the market will define as an increasing level of quality and

continually lower costs. In other words, the best outcome by spending the least amount. Or said another way,

value is providing the most appropriate care in the least restrictive and costly setting. Shift from thinking about

reimbursement to thinking about revenue.

Context for trend:

Reimbursement models will continue to evolve over the next four years driven by the need to reduce Medicaid and

Medicare costs (in part driven by health care reform – but also driven by deteriorating state revenue and a potential sea

change concerning the national debt).

Payments for Medicare Advantage plans will be reduced by 2013.

Experience from numerous demonstration projects of new payment models will guide the evolution:

Medicare Value-Based Reimbursement Demonstrations for nursing homes began in 2009. CMS must submit a plan to

Congress by October 1, 2011 for how to transition nursing homes and home health agencies to a value-based

reimbursement model. The results of the demo in addition to stakeholder input will likely guide these

recommendations.

Other demos like Medicare Acute Care Episodes (―ACE‖) demonstration are testing bundled payment models for acute

care, inpatient episodes for cardiovascular and orthopedic procedures.

Physician Group Practice demonstration tested the Shared Savings and Accountable Care Organization concepts

(―ACOs‖).

ACOs are increasingly being looked to as a potential organizational form for receiving payments. Proposed regulations

are finally in hand – and the ACO formation activity can be expected to accelerate.

Stewardship – not-for-profit values.

10

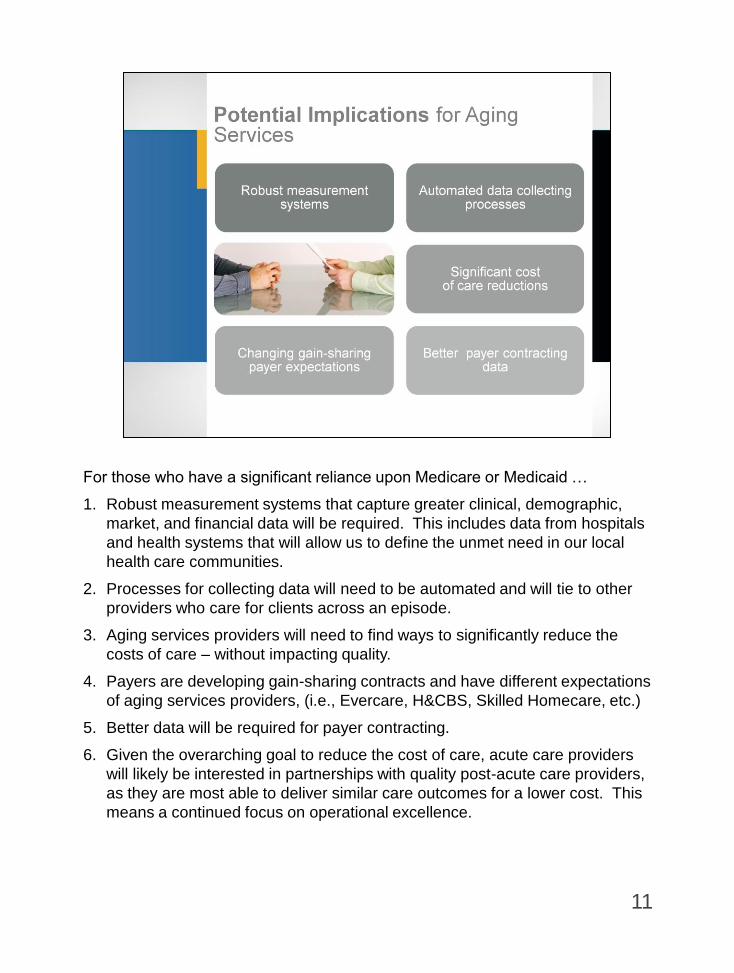

For those who have a significant reliance upon Medicare or Medicaid …

1. Robust measurement systems that capture greater clinical, demographic,

market, and financial data will be required. This includes data from hospitals

and health systems that will allow us to define the unmet need in our local

health care communities.

2. Processes for collecting data will need to be automated and will tie to other

providers who care for clients across an episode.

3. Aging services providers will need to find ways to significantly reduce the

costs of care – without impacting quality.

4. Payers are developing gain-sharing contracts and have different expectations

of aging services providers, (i.e., Evercare, H&CBS, Skilled Homecare, etc.)

5. Better data will be required for payer contracting.

6. Given the overarching goal to reduce the cost of care, acute care providers

will likely be interested in partnerships with quality post-acute care providers,

as they are most able to deliver similar care outcomes for a lower cost. This

means a continued focus on operational excellence.

11

#2

Referral Sources are instituting changes in preparation for different payment models. Context for trend:

The majority of physicians are now employed by organizations also owning hospitals.

Hospitals are rapidly implementing health information technology (e.g., Electronic Health Records, Computerized

Physician Order Entry, best practice protocols embedded in EHR, etc.) and states/regions are developing

interoperability standards and portals for the exchange of this HIT.

Payers and Hospitals/providers are collaborating to create new payment models that create shared risks and rewards.

Care management programs in physician offices (e.g., medical homes) and at hospitals are developing and are

spanning services provided across sites of services. Some managed care plans including Medicare Advantage and

Special Needs Plans (e.g., Evercare) have a care management component at the core of their model (e.g., nurse

practitioners in nursing homes, assigned care managers for community-based dual eligibles).

ACO = Accountable Care Organization VBP = Value-Based Purchasing

Bundled payment definition: A single, fixed per person payment paid to provider(s) for the provision of all services and

expenses for: 1) an episode of care, 2) management of a chronic condition or 3) an individual.

Value Based Performance Payment is a generic term for payments that: “improve beneficiary health outcomes and

experience of care by using payment incentives and transparency to encourage higher quality, more efficient

professional services.”

For nursing homes and home health: The HHS Secretary must submit a plan to Congress by FY2012 for

transitioning nursing homes and home health agencies to a value-based payment system.

Accountable Care Organizations – a group of health care providers working together to manage and coordinate care for

a defined population, that share in the risk and reward relative to the total cost of care and resident outcomes.

ACO Goals

• Reduce Growth in Cost per enrollee: Prevention/Wellness/Chronic Care Management; Reduce/eliminate

duplication; Improved Coordination; Consistent Application of Best Practices

• Improve/maintain quality: Eliminate avoidable readmissions; Improve resident outcomes12

Providers will need strong relationships with hospitals and

physicians/primary care practitioners at an organizational level to

assure they are included in the new contracts and payment models.

Providers will need to define and evaluate the new roles they want to

play in the new models (i.e., partner vs. subcontractor, Fee for

Service vs. risk taker, exclusive to one system or ACO vs. contract

with many).

Care delivery models will be integrated with all providers serving the

consumer collectively with common goals.

Best practice protocols will be uniform across all sites of services.

Care managers and primary care practitioners (e.g., physicians,

nurse practitioners, physician assistants) will participate more in the

community and post-acute settings care delivery processes.

13

#3Hospitals will experience significant financial strains over the next 5 – 7 years.

Context for Trend:

• Significant payment reductions for hospitals will occur over the next 3 to 5 years.

• Additional quality metrics are proposed, which might result in reduced payments, (i.e., rehospitalization rates, health care acquired conditions)

• Expenses are increasing faster than revenues from most payers.

• Some hospitals will begin taking on greater risk for the costs of care delivery over a time period.

Note: Hospitals will experience reduced payments for high volumes of hospital-acquired conditions, readmissions and some will see reductions from redistributions resulting from value-based payments.

14

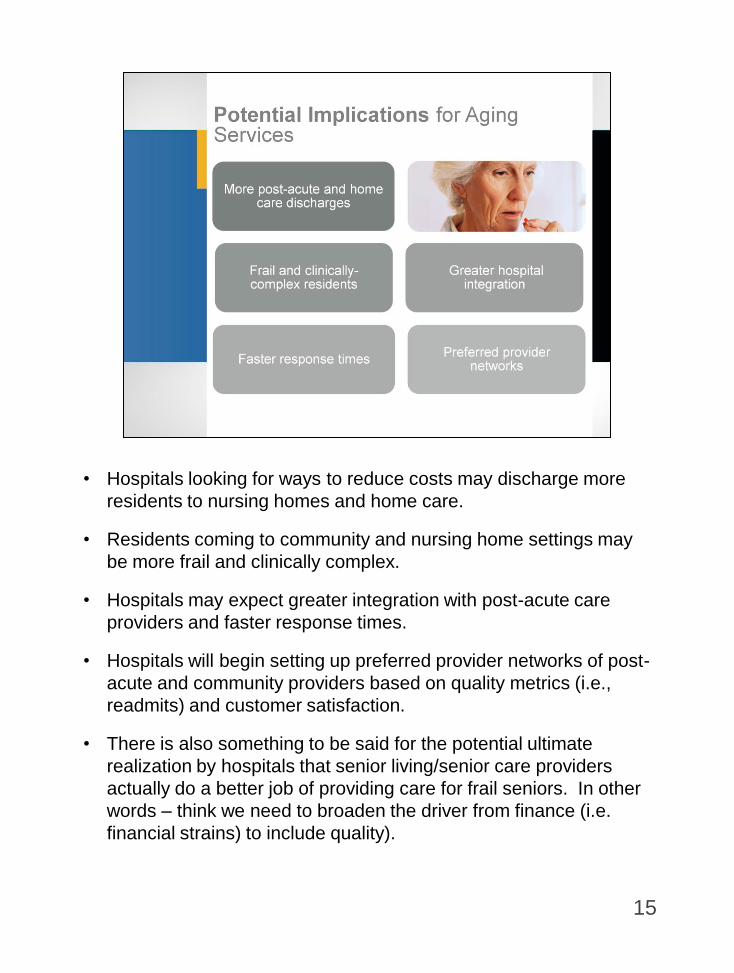

• Hospitals looking for ways to reduce costs may discharge more

residents to nursing homes and home care.

• Residents coming to community and nursing home settings may

be more frail and clinically complex.

• Hospitals may expect greater integration with post-acute care

providers and faster response times.

• Hospitals will begin setting up preferred provider networks of post-

acute and community providers based on quality metrics (i.e.,

readmits) and customer satisfaction.

• There is also something to be said for the potential ultimate

realization by hospitals that senior living/senior care providers

actually do a better job of providing care for frail seniors. In other

words – think we need to broaden the driver from finance (i.e.

financial strains) to include quality).

15

#4

Future customer buying practices will likely differ from historical patterns.

Context for Trend:

• Economic downturn of 2008 - 2010 has negatively impacted wealth and financial position of

elders and often their adult children.

Anecdotal and market research data indicate older adults are delaying moves to senior housing

perceiving that they would ―lose money‖ if they sold today.

• Older adult preferences are changing as they buy ―good enough.‖

• At the same time, people may be saying that if it isn‘t good enough, I am not going to make

the move

• People who saw their portfolio drop are thinking differently. They are more cautiously

approaching major decisions in their life.

The CLASS Act

• The CLASS plan provides those who participate with cash to help pay for needed

assistance, if they become functionally limited, in a place they call home — from

independent living to a nursing home, if they choose.

• Most provisions of the CLASS Act are ―effective‖ January 1, 2011. But before people can

begin signing up to participate, the secretary of Health and Human Services (―the

secretary‖) must develop the details of the plan and implement it. The law requires the

Secretary to release the details of the plan no later than Oct. 1, 2012. So it is likely that

people will be able to sign up sometime after that – in 2012 or 2013.

16

• Many older adults and their adult children have lost a significant portion of their total

assets during the economic downturn and may be impacted by low rates of return

and diminished interest rates on CDs. As a result, the consumer is likely to be more

focused on value (lower costs + high quality).

• Increased vacancies in independent living and assisted living units are being

reported as older adults delay moving in. (More for IL, less so for AL)

• Providers are developing new marketing messages and tools to attract customers

and helping them sell their homes.

• Short stay nursing home residents now make up a large potential market for aging

services. Remaining connected with these individuals will be critical as these

individuals will be future users of services (along with their family members).

• Care management will come into its own as an ―in-demand‖ profession. Physician

offices may seek additional help and services in managing older frail adults who

choose to remain in their own homes or others with chronic conditions.

• Adult children may be willing and need support services to help them care for their

aging parents (i.e., respite care, concierge services, others?). The more coordinated

and seamless the set of services – the more value that will ultimately be perceived

(and received).

17

18

#5

Health Care Reform legislation will create opportunities for aging services

providers.

Context for Trend:

• The Patient Protection and Affordable Care Act and the Health Care & Education

Affordability Reconciliation Act (PPACA) of 2010 were passed and will change health

care.

• The PPACA, better known as health reform legislation, has many implications for

aging services providers, their staff and their residents.

• These acts provide several hundred demonstrations, pilots and grant programs that

may present opportunities for providers, i.e., State Balancing Incentive Payments

Program, Community First Choice Option, SNF Value Based Reimbursements, etc.

• Health Care reform increases the focus on home and community-based services.

• The drivers of health care reform are what are most significant as even with

legislative changes that may be coming, and regulations that have yet to be issued,

those drivers (or some of those drivers) will guide the reform and evolution of the

system.

19

Health Care Reform will create both challenges and opportunities for aging services providers.

Providers will need to prepare for changes resulting from health care reform laws including:

• Health information exchange: providers will not only need to implement and use electronic health records but share the data in those records. Along with this, comes a need to analyze and understand the information collected to make care delivery changes and ensure best outcomes. This will likely require either existing staff to develop new skills (e.g., in technology, data analysis, etc.) or result in the creation of new job roles.

• Payment reform is a significant component of the Act. Given the escalating costs of health care, it is unlikely that payment reform will be significantly diluted through regulation or changes in the Health Care Reform Act.

• The focus on quality and performance measurement will increase – both from a resident outcome and a payment perspective

• Reductions in nursing home and home health payments

• As reform rewards value, increasingly more services will shift to lower cost care delivery settings positioning aging services/post-acute providers for increased business volumes.

• Dramatic growth in home and community-based services due to expanded eligibility and funding opportunities – as well as the consumer‘s preference to receive care in their home.

• Other o Possible reimbursement/payment for services not previously reimbursed but that

produce positive outcomes under new payment models.

o Will require/allow exploration and implementation of new care delivery models.

20

21

A time for discussion:

• Local implications of national trends?

• What are the competitors and collaborators in our market doing?

• How do we view our continuum (i.e. value and place of nursing care,

home health, housing, etc.)? Is our continuum broad enough for our

organization to meet the comprehensive needs of seniors. If not – what‘s

missing – should we provide, should we partner?

• Do we know what are our potential collaborators (hospital, physician,

other post-acute, etc.) are considering? If not, how can we best obtain

those insights? Should we look to partner and collaborate beyond our

current level of collaboration?

22

23

24

Question posed to leading CEOs and Boards: “What keeps you up at night?” ?”

The complexity and pace of change will provide opportunities to providers that adapt quickly and strategically and will present a threat to

those that do not.

1. Consumers and payers will demand increasing accountability and demonstration of value

2. Health care reform will drive tremendous change: new payment methods will require different business models and will be pursued by

both the public and private payer; specific to senior living (whether a Medicare provider or not) will include expectations for increased

quality and greater family caregiver responsibilities coupled with a focus on Home and Community Based Services (Medicaid

expansion in this area may be constrained by states‘ budgets).

3. Accessing capital will continue to be difficult and, therefore, require better financial performance, planning and positioning – rating will

matter – creativity will be the rule!

4. Technology today is used to manage information, monitor health status and, in some isolated cases, as part of a medical procedure;

in the future, senior living organizations must be able to exchange information, mine the data collected to improve care outcomes

(e.g., identify high risk residents, determine cost of care by diagnosis) and reduce costs, use it to improve care delivery (e.g.,

consistent application of best practices, remote physician consultations, resident monitoring,) or enhance medical procedures, and

improve productivity

5. Margins are likely to erode from both the economic recession (a new normal for many), effects of state budget deficits and anticipated

changes as a result of health care reform

Some color: Recession has had both positive and negative effects on aging services:

• Negative: "flat pricing growth‖…we are not able to pass on pricing increases

• Positive: more stable workforce/lower staff turnover and, continued slow move-ins in areas where real estate continues to sell

slowly. slower inflation on many costs items.

6. Business relationships will expand and leadership within organizations will be challenged to keep referrals moving. In other words,

today, business growth is driven by personal relationships at the practitioner level. In the future, referral will be driven by

organizational relationships – as economic incentives tie organizations together.

7. Everything points to the desire for greater value –defined as lower cost and higher quality. Value… stop thinking cost management;

stop thinking quality is equated to the amount of time you invest. Quality is in the mind and eye of the purchaser… the customer…

specifically, the resident, client or their family. Payers will insert themselves on behalf of this consumer but make no mistake as to

who will define quality.

25

26

The ―New Normal‖ for many Americans

What we don‘t know is how long some of the lingering effects will last

• Significant budget deficits – federal and state

o Looking for new tax revenue sources (Tax-exempts?)

o Pressure to cut reimbursement

• Declines in net income and net worth for older adults. While the stock

market is up and portfolios have rebounded – the issue short term is

income ala CD rates and long term there may be an issue regarding baby

boomer income and wealth

• Housing market – length of time on the market, sales prices

• High unemployment, especially of unskilled workers

• Pricing pressure from consumers and payers

• Investment earnings are diminished offering limited or no arbitrage

• Financing hurdles are more challenging

Buying habits have changed.

27

Health care payment reform is a reality. Regardless of whether the current form prevails, change is imminent. Business-as-usual will be impossible to maintain. The following are emerging:

1. Providers will be asked to accept greater financial risk for outcomes2. Operational efficiency will be critical3. Collaboration among all providers will be required for survival4. Significant investments in technology will be necessary5. Increased quality expectations, reporting and monitoring6. Elevated regulatory risk7. Increased focus on community-based services and care will result

Forces driving reform: • Growing uninsured populations;• Exponential growth in expenditures;• Looming Medicare solvency; • Cost to quality comparisons;• Reform is a must! Cost is too high;• Quality is too low.

Cost Cutting: Market basket update adjustments for productivity reduce reimbursement.

Delivery System Reforms: Implements VBP, reduced payments for high volumes of hospital-

acquired conditions and readmissions, and pilot programs to test bundled payments ACOs and

medical homes.

Independent Payment Advisory Board: Creates MedPac-like commission that has Medicare

rate setting authority (starts 2015); Not applicable to PPS hospitals until 2019.

Medicaid: Expands Medicaid to 133% (2014) of FPL and uses revised definition of income.

Tax Exempt Status: Includes 4 new criteria hospitals must satisfy to retain not-for-profit status.

Mandates: Individuals: must purchase insurance or pay penalty. Businesses: must provide

affordable insurance (if more than 50 employees) or pay penalty if any of their employees

receive federal premium or cost-sharing subsidies.

28

Access to capital will continue to be very difficult for weak credits and

providers will explore a variety of options.

1. Interest rates for non-rated credits remain high and ratings

present a competitive advantage.

2. Different sources of capital must be considered (i.e.

contributions, endowments and investors)

3. Fitch Ratings… ―maintains its negative outlook for the senior

living sector‖ for 2011.

4. Operating results AND balance sheet strength define borrowing

capacity.

5. Rating matters!

6. Access to capital may drive affiliations.

29

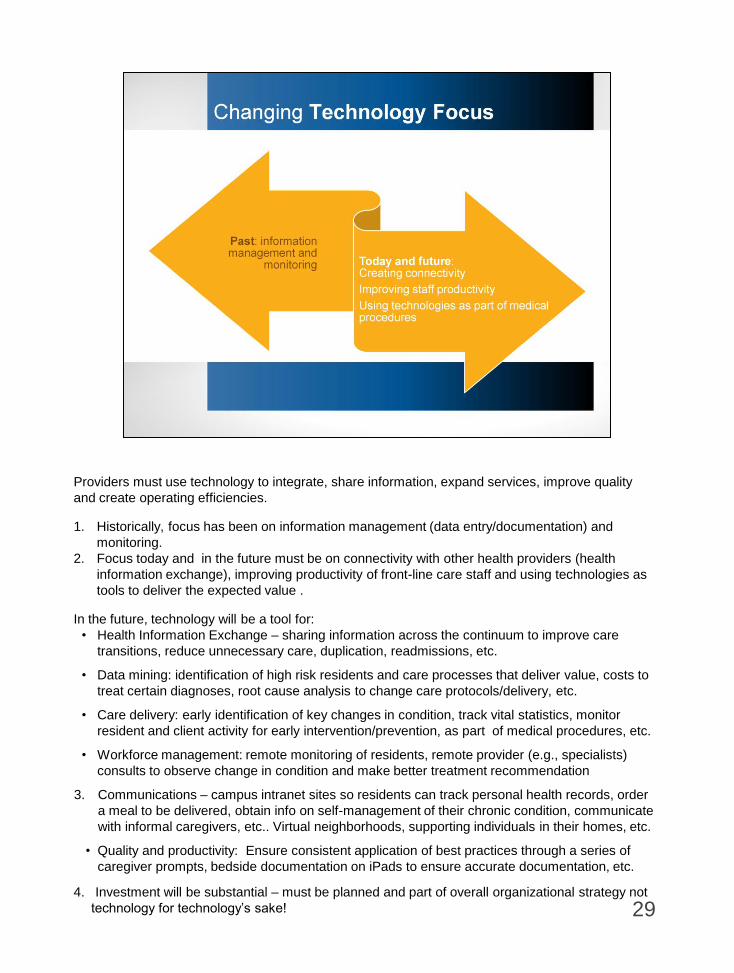

Providers must use technology to integrate, share information, expand services, improve quality

and create operating efficiencies.

1. Historically, focus has been on information management (data entry/documentation) and

monitoring.

2. Focus today and in the future must be on connectivity with other health providers (health

information exchange), improving productivity of front-line care staff and using technologies as

tools to deliver the expected value .

In the future, technology will be a tool for:

• Health Information Exchange – sharing information across the continuum to improve care

transitions, reduce unnecessary care, duplication, readmissions, etc.

• Data mining: identification of high risk residents and care processes that deliver value, costs to

treat certain diagnoses, root cause analysis to change care protocols/delivery, etc.

• Care delivery: early identification of key changes in condition, track vital statistics, monitor

resident and client activity for early intervention/prevention, as part of medical procedures, etc.

• Workforce management: remote monitoring of residents, remote provider (e.g., specialists)

consults to observe change in condition and make better treatment recommendation

3. Communications – campus intranet sites so residents can track personal health records, order

a meal to be delivered, obtain info on self-management of their chronic condition, communicate

with informal caregivers, etc.. Virtual neighborhoods, supporting individuals in their homes, etc.

• Quality and productivity: Ensure consistent application of best practices through a series of

caregiver prompts, bedside documentation on iPads to ensure accurate documentation, etc.

4. Investment will be substantial – must be planned and part of overall organizational strategy not

technology for technology‘s sake!

30

Reaction to environmental and business factors will require:

1. Managing referral relationships while developing organizational relationships

with various types of service providers.

2. A willingness and ability to broaden relationships and add value in the ―care

delivery‖ stream.

3. Improved communication among providers and information. This will not

always need to be sophisticated but may include standardizing transfer form

information, asking physicians their preferred form of communication (e.g.,

email, text, call cell phone) when there is a change in resident or client

condition, etc. or as sophisticated as electronic access to a password

protected web portal to share resident information.

4. Adaptation of management and governance activities to drive change.

5. Shift in internal culture at the direct care worker level.

31

Consumers and Payers will Demand increasing accountability and demonstration of value .

A combination of regulatory and consumer changes will give rise to changing expectations.

1. Quality and value targeted under Healthcare Reform.

2. Person-centered post-acute care system (―culture change‖). CMS will define person-

centered care for the Medicare Shared Savings/ACO program. This standard may trickle

down to the post-acute setting.

3. Home and community-based services – consumer choice.

4. The CLASS Act offers the opportunity to revamp funding for aging services.

5. Living arrangements.

6. Expectation of ―Free!‖

Accountability is key concept!

Changing business model that requires organizations to look at senior living (housing, services

and health care) differently than rehabilitative (post-acute) services .

CMS Vision for Future:

“The person-centered post-acute care system of the future will: Optimize choice and control of

services; Ensure that placement decisions are based on resident needs; Provide coordinated,

high quality care with seamless transitions between settings; Reward excellence by reflecting

performance on quality measures in payment; Recognize the critical role of family care giving;

and Utilize health information technology.‖ Source: CMS Policy Council Document, 9/28/06

―Post-Acute Care Reform Plan; reviewed at MedPac 1/07

Value = lower costs and high quality

Value = the extras, for free

Value = great communication and helpful information

Value = I want it my way and I want it my now.

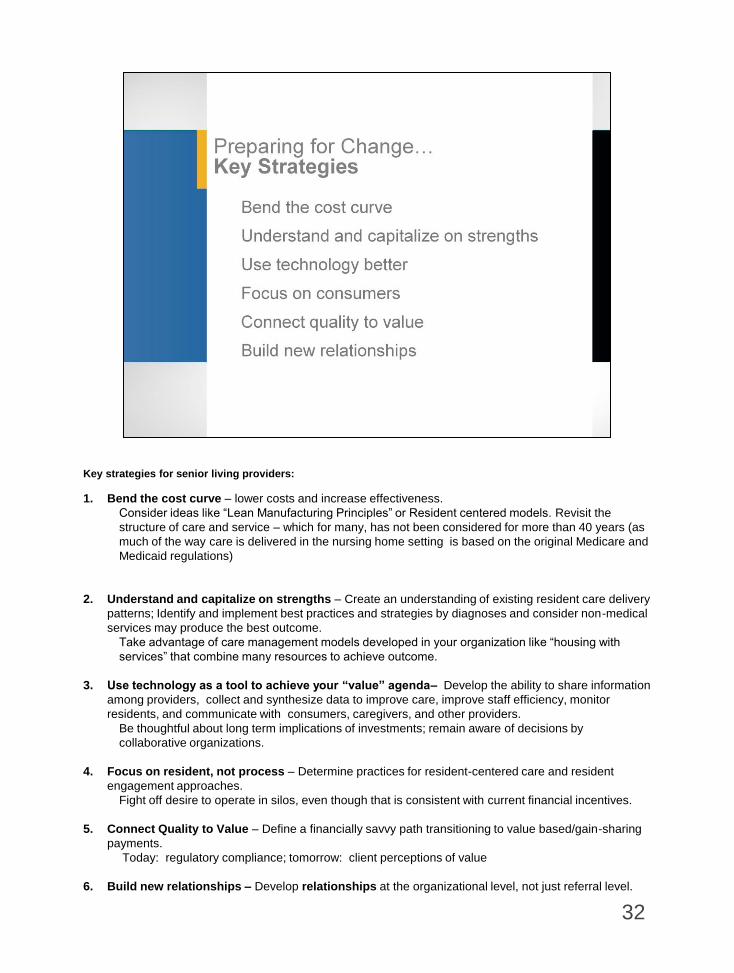

Key strategies for senior living providers:

1. Bend the cost curve – lower costs and increase effectiveness.

Consider ideas like ―Lean Manufacturing Principles‖ or Resident centered models. Revisit the

structure of care and service – which for many, has not been considered for more than 40 years (as

much of the way care is delivered in the nursing home setting is based on the original Medicare and

Medicaid regulations)

2. Understand and capitalize on strengths – Create an understanding of existing resident care delivery

patterns; Identify and implement best practices and strategies by diagnoses and consider non-medical

services may produce the best outcome.

Take advantage of care management models developed in your organization like ―housing with

services‖ that combine many resources to achieve outcome.

3. Use technology as a tool to achieve your “value” agenda– Develop the ability to share information

among providers, collect and synthesize data to improve care, improve staff efficiency, monitor

residents, and communicate with consumers, caregivers, and other providers.

Be thoughtful about long term implications of investments; remain aware of decisions by

collaborative organizations.

4. Focus on resident, not process – Determine practices for resident-centered care and resident

engagement approaches.

Fight off desire to operate in silos, even though that is consistent with current financial incentives.

5. Connect Quality to Value – Define a financially savvy path transitioning to value based/gain-sharing

payments.

Today: regulatory compliance; tomorrow: client perceptions of value

6. Build new relationships – Develop relationships at the organizational level, not just referral level.

32

33

A time for discussion:

• Local implications of national trends?

• What are the competitors in our market doing?

• How do we view our continuum (i.e. value and place of skilled,

home health, housing, etc.)? Is our continuum broad enough for

our organization to meet the comprehensive needs of seniors. If

not – what‘s missing – should we provide, should we partner?

• Do we know what are our potential collaborators (hospital,

physician, other post-acute, etc.) considering? If not, how can we

best obtain those insights? Should we look to partner and

collaborate beyond our current level of collaboration?

34

35

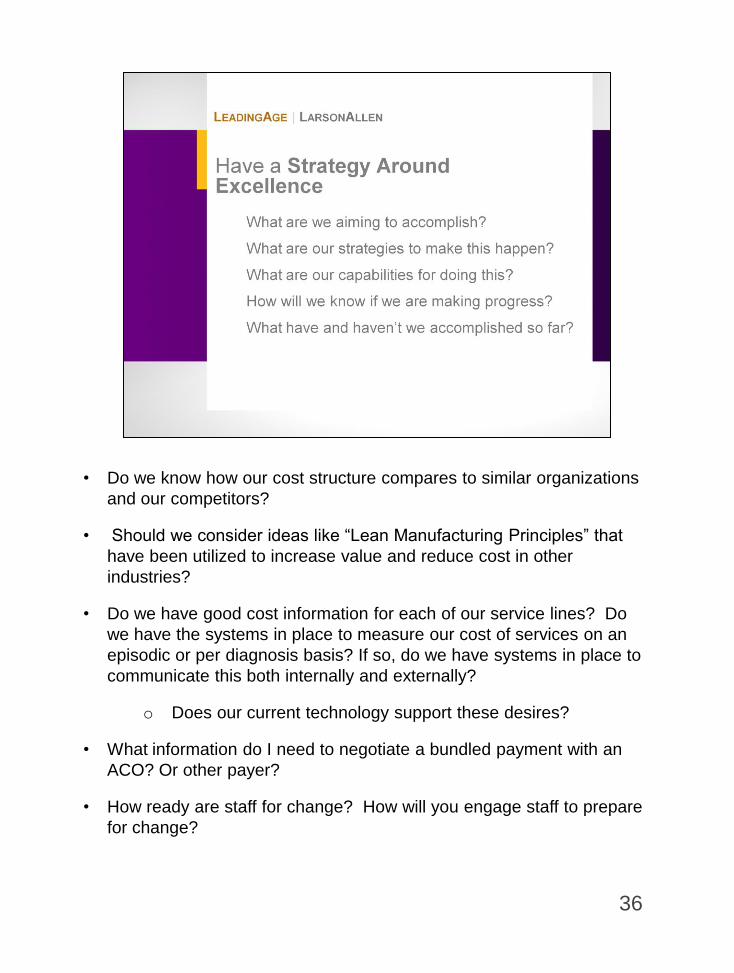

• Do we know how our cost structure compares to similar organizations

and our competitors?

• Should we consider ideas like ―Lean Manufacturing Principles‖ that

have been utilized to increase value and reduce cost in other

industries?

• Do we have good cost information for each of our service lines? Do

we have the systems in place to measure our cost of services on an

episodic or per diagnosis basis? If so, do we have systems in place to

communicate this both internally and externally?

o Does our current technology support these desires?

• What information do I need to negotiate a bundled payment with an

ACO? Or other payer?

• How ready are staff for change? How will you engage staff to prepare

for change?

36

• Have we developed an objective assessment of our strengths and

our weaknesses?

• Have we established and documented best practices around care

delivery systems?

• Have we created systems to measure the outcomes/quality of our

services?

• Can we ―tell our story‖ to referral relationships? Can we prove our

quality?

• Do we know what diagnosis we are really good at treating? Do

they match with the unmet need in the community?

37

• Does our organization have an up-to-date technology plan in place – that

considers our current position and anticipates future strategic needs and

opportunities?

• Do we have the financial capacity to acquire, deploy and utilize the

technology?

• In terms of health care reform:

o Does our organization have the resources and the willingness to make

the necessary upfront investments to succeed at payment reform (e.g.,

EHR, care coordination )?

o Do we have an Electronic Health Record? Can we share it with other

provider groups?

o What kinds of technology will be required to develop/participate in an

ACO across organizational participants?

o What are we doing in terms of the utilization of technology in our care

delivery model?

38

• Have we established best practices around resident-centered

care?

• Are our residents active in the decisions around their care?

• Is our governance and management philosophy consistent with

the demands of a new generation of consumers?

39

• How do we track quality currently? How do we rank on quality benchmarks currently

compared to our peers? Where do we need to improve on quality and efficiency?

• Can we prove our quality? Are we part of Quality First and/or the Advancing Excellence in

America‘s Nursing Homes Campaign?

• Are we an integrated system with all of the components of the health care system? Or do we

need to develop relationships with other providers in order to more effectively participate?

• Accountable Care Organization readiness:

o Does my organization want to be part of an ACO? If so, why?

o Is my organization prepared to lead an ACO?

o Do I want to be part of more than one ACO?

o How much risk am I willing to take to participate in ACO?

o Payment

o Participation vs. opting out of an ACO

o Do we want to be the administrator of the bundled payment or subcontract with

another provider/organization/system to provide certain services?

40

• Overall: Have we thought strategically about the value of

affiliations/relationships or have we only thought about affiliation as a

last resort?

• Programmatically: What value do our current collaborative

relationships have? Are they serving the original/intended objectives?

• Health Care Reform:

o Are there providers in your community that have formed or are

exploring becoming an ACO?

o If so, how are they deciding which providers to include in the

ACO?

o Who are our natural partners?

o What type of legal structure must be in place to receive a

bundled payment? Do we have it? Should we pursue it?

• With whom will we need to form partnerships, relationships with in the

future?

41

42

43

LeadingAge is an association of 5,400 not-for-profit organizations

dedicated to expanding the world of possibilities for aging. We

advance policies, promote practices and conduct research that

supports, enables and empowers people to live fully as they age.

The LeadingAge Mission

Expanding the World of Possibilities for Aging.

The LeadingAge Vision

Continually transforming society‘s vision and deepening members‘

commitment to expanding the ―world of possibilities‖ for aging.

The LeadingAge Position

The most trusted advocate for aging whose spirit of transformational

stewardship and close collaboration with members consistently

improves lives.

The LeadingAge Promise

Inspire. Serve. Advocate.

44

LarsonAllen is a 2011 LeadingAge Partner.

LarsonAllen225 individuals, including 50 principals dedicated to health care

Serving more than 4,800 health care providers across the United States, including senior living,

senior care, hospitals, physicians, and home care and hospice

Providing a diverse and comprehensive set of services

ThirdAge, a division of LarsonAllen

500+ clients served, in more than 35 States

Focus on continuing care, assisted living, nursing care, home care and leading edge ‗at-home‘

services

Our Unique Capabilities – Noticeably Different!Assurance and accounting

Tax

Financial services

Outsourcing

International

Specific to health care industry:

Strategy development and execution

Comprehensive market research

Executive search

Marketing and sales

Affiliations and mergers

Project development

Operations

Feasibility

45

LarsonAllen is a 2011 LeadingAge Partner.

46