-versus- present: feliciano p. legaspi, gomez...

TRANSCRIPT

REPUBLIC OF THE PHILIPPINES

SANDIGANBAYAN

Quezon City

Seventh Division \

PEOPLE OF THE PHILIPPINES, Crim. Case No. SB-16-CRM-0130Plaintiff,

-versus- Present:

FELICIANO P. LEGASPI, Gomez-Estoesta,J.,CteVpewonCRISTETA M. ESTEBAN, AND Trespeses, J., and

JacintoMANUEL R. MARCIAL,

Accused.

, J.

Promulgated:

DECISION

GOMEZ-ESTOESTA, J.:

Unexplained deductions from the GSIS life policy of a localgovernment employee brought to light the delayed remittance of GSIScontributions by the Municipality of Norzagaray, Bulacan, thrusting theaccused, Municipal Mayor Feliciano P. Legaspi, Municipal Treasurer CristetaM. Esteban, and Municipal Accountant Manual R. Marcial, to a criminalcharge for Violation of Section 52(g) in relation to Section 6(b) of R.A. No.8291, or the GSIS Act of 1997, in an Information which reads:

That on or about January 9, 2010, or sometime prior or subsequentthereto, in Norzagaray, Bulacan, Philippines, and within the jurisdiction ofthis Honorable Court, accused. Municipal Mayor Feliciano P. Legaspi,Municipal Treasurer Cristeta M. Esteban and Municipal AccountantManual R. Marcial, all public officers of the Municipality of Norzagaray,Bulacan, having the legal obligation to timely remit to the GovernmentService Insurance System (GSIS) the GSIS premium contributions of theemployees of the Municipality of Norzagaray, committing the offense inrelation to office and in confederation with one another, did then and therewillfully, unlawfully, and criminally fail to remit within thirty days from 10December 2009, the date when the payment is due and demandable, the saidGSIS premiums covering the month of November 2009, amounting to SixHundred Sixty Seven Thousand Eight Hundred Fifty Nine Pesos and 37/100

* Per A.O. No. 284-2017 dated August 18,2017

9

People V. Fellclano P. Legaspi 2 | P a g eCriminal Case No. SB-16-CRM-0130

DECISION

(P667,859.37), thereby causing delay in its remittance to the damage andprejudice of the municipal employees of Norzagaray, Bulacan.

CONTRARY TO LAW.'

A Hold Departure Order was issued against all the accused on April 5,2016,^ followed by a warrant of arrest on April 19, 2016.^ The accused eachposted cash bail for their provisional liberty.'^ When arraigned, all the accusedpleaded not guilty to the charge.^

The parties entered into a Joint Stipulation of Facts,^ whereby thefollowing facts were admitted:

I

ADMITTED FACTS

1. That all the accused at the time material to the case are public officersand that they are holding the public positions as described in theInformation.

2. That all the accused are the same persons as charged in the Information.

3. That accused Manuel Marcial is an accountant.

4. That Mr. Marcial being an accountant, one of his duties andobligation[s] is to make an accounting for remittance of whateverpayments to be made by the Municipality of Norzagaray.

5. That the remittance for the GSIS premiums of the municipal officialsand employees of Norzagaray, Bulacan for November and December2009 was delayed.

The following issue was defined:

Whether or not all the accused violated Section 52(g) in relation toSection 6(b) of R.A. 8291

EVroENCE FOR THE PROSECUTION

The Prosecution presented two (2) witnesses, who testified throughJudicial Affidavits, as follows:

1. Mila C. Chan ["Chan"] was Staff Officer III and ActingDivision Chief of the GSIS Claims Department in 2009. Her duties as suchincluded the review of documents and the approval of life insurance claims.

^ Records, Vol. 1, pp. 1-32/d,p. 56^ Id., p. 70^ Fellciano Legaspi -/d, pp. 73-78; Manuel Marcial -/d, pp. 79-84; Cristeta Esteban -/d, pp. 90-95® Id., pp. 104-109® Joint stipulation of Facts and Issue, Id., pp. 199-207; Pre-Trial Order dated September 14, 2016, Id., pp.208-214

^ Ibid.

rr'i

People V. Feliciano P. Legaspl 3 | P a g eCriminal Case No. SB-16-CRM-0130DECISION

At present, she is still Staff Officer III, but she was Acting Division Chief onlyuntil December 2011

Sometime in 2010, she approved the payment of the life insuranceclaim of one Yolanda C. Ervas, and prepared and signed the life insuranceclaim voucher pertaining thereto.^ On cross examination, Chan testified thatshe did not personally know Ervas and did not personally witness her receiptof the claim voucher.^®

Answering questions from the Court, Chan explained the itemsdescribed in the Life Insurance Claim Voucher, particularly those underPremium in Arrears. "PS" stood for Personal Share, while "GS" stood for

Government Share. These were both to be remitted by the LGU. The LifeInsurance Claim Voucher, however, did not indicate the length of time thatthe arrears have been pending.'^

2. Liza R. Asia ["Asia"] was Staff Officer II of GSIS-Bulacan in2010, and her duties included receiving collections firom the cashier. Theseincluded the cashier's detailed report, the official receipts and the orders ofpayment issued by the cashier.'^

Asia recalled that among the official receipts she received from thecashier was O.R. No. 0000597712 dated February 12,2010, issued by LalaineMendoza, a teller.'^ She also received the Order of Payment pertaining toO.R. No. 0000597712, which indicated the remittance of (a) Cash AdvanceLoan (CAL), (b) Consolidated Loan (CONSOLOAN), (c) ECARDPLUS, (d)Employee Contribution (ECCONT), (e) Life & Retirement Government Share(LF/RETGS), (f) Life and Retirement Personal Share (LF/RETPS), (g) PolicyLoan Regular (PLREG), and (h) Salary Loan Regular (SLREG). The thirdcolunm of the Order of Payment indicated "11/2009" i.e., November 2009,which was the month that payment made on February 12,2010 was due.'"' Oncross examination, she testified that she could no longer recall if during thattime, there were other municipalities aside jfrom Norzagaray that were delayedin remitting GSIS contributions.'^

The Prosecution offered the following documentary exhibits on thesame day its witnesses were presented, as follows:

Exhibit Document

"A" Complaint-Affidavit of Yolanda C. Ervas and its annexes

"B" Life Insurance Claim Voucher of Yolanda C. Ervas

"C" Official Receipt No. 0000597712 dated February 12,2010"D" Order of Payment dated February 12,2010

® Judicial Affidavit of Mila Chan dated July 21, 2016, Records, Vol. 1, pp. 132-139, Q&A Nos. 2-6® Exhibit "B", Id., Q&A Nos. 7-17TSN dated September 13, 2016, p. 10" Id, pp. 12-13"Judicial Affidavit of Liza Asia dated July 22,2016, Records, Vol. 1, pp. 140-147, Q&A Nos. 4,6" Exhibit "C",/of., Q&A Nos. 9-11" Exhibit "D", Id., Q&A Nos. 19-21" TSN dated September 13,2016, p. 19 //■ If

People V. Feiiclano P. Legaspl ^ 4 | P a g eCriminal Case No. SB-16-CRM-0130

DECISION

By Order dated September 13,2016, Exhibits "A", "B", "C, and "D"were admitted.

EVIDENCE FOR THE DEFESE

In their defense, the accused presented four (4) witnesses, themselvesplus Marlene S. Cruz, who testified by Judicial Affidavits, as follows:

For accused Marcial:

1. Manuel R. Marcial [^'accused Marcial"] was the MunicipalAccountant of Norzagaray, Bulacan in 2009. His functions are those providedunder Sec. 474(b) of the Local Government Code, more pertinently No. 6thereof, i.e., "prepare statements of cash advances, liquidations, salaries,allowances, reimbursements and remittances pertaining to the localgovernment unit."^^

Accused Marcial confirmed Asia's testimony that the GSIS premiumsfor November 2009 were paid only on February 12, 2010, but firmly deniedthe charge against him, as he was not responsible for the delay in payment.As of December 4,2009, he has already prepared Disbursement Voucher No.101-09-12-3093 in the amount of PI 31,123.27 for the "payment of remittanceto VARIOUS LOANS of officials & municipal employees for the month ofNOVEMBER 2009,"^^ which he forthwith forwarded to the Office of theTreasurer. There was no delay in the preparation of the disbursement voucher,as under Sec. 52(g) of R.A. 8291 and its implementing rules, liability attachesonly when there is failure to remit by more than 30 days from the time theremittance becomes due. Moreover, it was not his duty to remit the premiumsto GSIS, and once the disbursement voucher has been indorsed to the Officeof the Treasurer, he no longer had control over the remittance of premiums.

In the same way. Disbursement Voucher No. 101-09-12-3169 in theamount of P536,736.10 for the "payment of LIFE & RETIREMENTPREMIUMS, EMPLOYEES['] COMPENSATION CONTRIBUTION ofofficials and municipal employees for the month of NOVEMBER 2009"^^was prepared on December 16,2009 by Marlene Cruz, who was next in rankto him, to avert delay in his absence. To his knowledge, Cruz also immediatelyindorsed the disbursement voucher to the Office of the Treasurer, although headmitted that he did not witness such indorsement by Cruz.^^ He later learnedthat the Treasurer's Office was unable to act immediately on the disbursement

Records, Vol. 1, pp. 196-198Judicial Affidavit of Manuel Marcial dated August 8,2016, Records, Vol. 1, pp. 172-183, Q&A Nos. 4,8

Exhibit "1" (Marcial)

Judicial Affidavit of Manuel Marcial, Q&A Nos. 10-1720 Exhibit "2" (Marcial)22 Judicial Affidavit of Manuel Marcial, Q&A Nos. 18-24, TSN dated October 10,2016, pp. 15-16

/•/

People V. Feliclano P. Legaspl 5 | P a g eCriminal Case No. SB-16-CRM-0130

DECISION

voucher for lack of cash, and the payment for the premiums was remitted onlyin February 2010.^^

Since the disbursement vouchers were prepared within a month fromDecember 10, 2009, when the pa3mients became due, and indorsed to theOffice of the Treasurer immediately thereafter, there was no merit in theaccusation against him.^^

On cross-examination, Marcial testified that someone from their officewas assigned to remit the GSIS premiums, who also prepared the statementswhich he later signed. The Municipal Treasurer only certifies as to theavailability of cash.^"^

Accused Legaspi and Esteban adopted the testimony of accusedMarcial.^^

2. Marlene S. Cruz ["Cruz"] was employed in the Municipalityof Norzagaray in 2009 as Administrative Assistant IV.^^

Cruz testified that on December 16, 2009, she prepared DisbursementVoucher No. 101-09-12-3169 for the "payment of LIFE AND RETIREMENTPREMIUMS, EMPLOYEES COMPENSATION CONTRIBUTION ofofficials and employees for the month of NOVEMBER, 2009",^' which shesigned as next in rank in the absence of accused Marcial, then chief of theiroffice. She immediately indorsed the disbursement voucher to the Office ofthe Treasurer, but later learned that it was not acted upon immediately for lackof cash, and that the premiums for November 2009 were remitted only inFebruary 2010. The GSIS does not impose penalty or interest on themunicipality for the late payment of remittances. Neither was Mrs. Ervascharged with any such penalty or interest; instead, she was charged forpremium in arrears from salary differentials.^®

For accused Legaspi and Esteban

3. Feliciano P. Legaspi ["accused Legaspi"] was the MunicipalMayor of Norzagaray, Bulacan for 15 years, i.e., from 1995 to 2004, and from2007 to 2013.29

Accused Legaspi recalled that there was a continuous shortfall in cashcollections from 2007 to 2010, as shown by a summary of cash collections

Judicial Affidavit of Manuel Marcial, Q&A No. 25

^ Id., Q&A No. 27TSN dated October 10, 2016, pp. 14-15

25 id., p. 132® Judicial Affidavit of Mariene Cruz dated March 21,2017, Records, Vol. 1, pp. 309-317, Q&A No. 422 Exhibit "2" (Marcial)2® Judicial Affidavit of Marlene Cruz, Q&A Nos. 5-1625 Judicial Affidavit of Feliciano Legaspi dated October 10, 2016, Records, Vol. 1, pp. 225-254, Q&A Nos.20-21

tf- if

People V. Feliclano P. Legaspi 6 | PageCriminal Case No. SB-16-CRM-0130DECISION

and expenditures for said years.^® This was caused by the non-payment oftaxes by companies in the municipality.^^ He referred to three cementcompanies as substantial sources of income, but from whom the municipalityobtained minimal collections when the GSIS remittances were due at that

time.^^ While the salaries and wages of municipal officials and employeeswere included in the Annual Budget of the municipality, for first classmunicipalities like Norzagaray, such budget was a mere projection of themunicipality's income and expenditures, and the actual payment of salariesand wages depended largely on the municipality's revenue collections.^^Because of the shortfall in 2007-2010, the municipality was imable to fulfillsome of its obligations on time - the salaries and wages of the municipalofficials and employees were not paid, and their GSIS accounts were notremitted. Particularly, salaries from December 2009 to January 2010 had tobe paid using cash collections for January 2010.^"^ This was allowed underSection 337 of the Local Government Code.^^

Moreover, despite such shortfall, the Sangguniang Bayan wasconstrained to enact Sangguniang Bayan Ordinance No. 2009-12-12 onDecember 23, 2009,^^ which authorized the immediate payment of Cost ofLiving Allowance (COLA) to municipal officials and employees, includingMrs. Yolanda Ervas, private complainant in this case.^^ COLA was paid tomunicipal officials and employees starting January 25, 2010,^^notwithstanding that it was not included in the 2010 Annual Budget of themunicipality. The payment of COLA further set back the municipalityfinancially, hence, salaries and wages for January 16-31,2010 were paid onlyon February 12, 2010,^^ which would have been paid on time if not for theCOLA.40

Faced with these fmancial setbacks, the municipality had to prioritizethe payment of net salaries and wages and other necessary operationalexpenses, lest government operations be hampered. It was not feasible orpracticable to make prompt remittances to the GSIS for the months ofNovember and December 2009."^^ Even if the municipality did not have togive COLA to its employees, still, it might have been unable to pay the GSISpremium contributions for November 2009, because there was not enoughcollection for it."^^

Exhibit "2" (Legaspi and Esteban), Id., Q&A Nos. 23-26TSN dated November 16, 2016, p. 34Id., p. 48

33/d, Q&A Nos. 35-373^ Disbursement Vouchers, Exhibits "3", "4", and "5" (Legaspi and Esteban); Id., pp. 23-3433 Judicial Affidavit of Feliciano Legaspi, Q&A Nos. 27-3433 Exhibit "6" (Legaspi and Esteban), adopted as accused Marcial's Exhibit "4"32 Exhibits "8" and "14"

3® Disbursement Voucher Nos. 101-10-01-061, Exhibit "7"33 Judicial Affidavit of Feliciano Legaspi, Q&A Nos. 38-58^ TSN dated November 16, 2016, p. 39

Judicial Affidavit of Feliciano Legaspi, Q&A No. 59^2 TSN dated November 16,2016, p. 39 i7 ^

People V. Feliclano P. Legaspl 7 | P a g eCriminal Case No. SB-16-CRM-0130

DECISION

Accused Legaspi identified the Joint Counter-Affidavit"^^ he executedwith co-accused Esteban and Marcial in response to the Complaint filed byMrs. Yolanda Ervas, wherein she attributed the "premium in arrears" deductedfrom her GSIS life insurance claim to the municipality's failure to remit to theGSIS the amount it regularly deducted from her salary as her personal share.'^Accused Legaspi maintained that the GSIS never advised him or his co-accused that the interest and penalties incurred by Mrs. Ervas were because ofthe delayed remittance of GSIS contributions."^^ Accused Legaspi alsotestified that Mrs. Ervas had filed another case against him before the Officeof the Ombudsman, which was later dismissed."*^

4. Cristeta M. Esteban ["accused Esteban"] was the Treasurer ofthe Municipality of Norzagaray in 2007 to 2010."^^ As such, it was her duty totimely remit the GSIS premiums of the municipality's officials andemployees."^® She corroborated accused Legaspi's testimony on themunicipality's financial woes in 2007 to 2009, which caused the delay in thepayment of the salaries and wages of its employees and the remittance of theirGSIS contributions/premiums. There was no more shortfall of funds after2010, and GSIS premiums have since been remitted regularly She alsoadded that the COLA paid on January 25,2010 included backpay from 1989to 2004.5®

i

Accused Esteban believed that the late remittances to GSIS had no

effect on Mrs. Ervas' life insurance policy. According to her, under the GSISLaw, interest and penalties for the late remittance of contributions wereimposed not against the employee but against the employer, but in this case,the municipality was not notified by the GSIS of any interest or penalties ondelayed remittances for November and December 2009. She explained thatMrs. Ervas was already an employee sometime in 1991,^^ when the GSISpremiums and contributions were remitted to the GSIS through IRAdeductions. Because of discrepancies between the computer-generated billingby the GSIS, which the municipality was not aware of, and the actualpremiums remitted by the municipality, there were delays in the release of theIRA to the municipality, and consequent delays in the GSIS remittances. Shewas also told that the premiums and arrearages of Mrs. Ervas in the amountof P27,558.11 were brought about by a retroactive salary increase without anaccompanying adjustment in premium contributions.^^

The accused then proceeded to formally offer the following exhibits:

Exhibit "1" (Legaspi and Esteban), adopted as accused Marclal's Exhibit "3"^ Judicial Affidavit of Feliclano Legaspi, Q&A Nos. 7-14

/d., Q&A No. 62

Q&A Nos. 3-4

Judicial Affidavit of Cristeta Esteban dated October 10,2016, Records, Vol. 1, pp. 255-284, Q&A No. 17TSN dated March 29, 2017, p. 15

^'/d.,pp. 20-215°/d., pp. 17-18

GSIS remittances through IRA deductions - Yolanda Ervas for 1991-1994, Exhibits "10", "11", "12", "13"(Legaspi and Esteban)" Judicial Affidavit of Cristeta Esteban, Q&A Nos. 52-58

%

People V. Fellclano P. LegaspiCriminal Case No. SB-16-CRM-0130DECISION

8 I P a g e

Exhibit DocumentMarcial Legaspi &

Esteban

Disbursement Voucher No. 101-09-12-3093

"2" Disbursement Voucher No. 101 -09-12-3169<43 « Joint Counter-Affidavit of Feliciano Legaspi, Cristeta Esteban

and Manuel Marcial dated September 4,2011«4" "6" Sangguniang Bayan Ordinance No. 2009-12-12 dated

December 23,2009"2" Summary of Cash Collection and Expenditures for 2009"3" Disbursement Voucher No. 101-09-17-3276"4" Disbursement Voucher No. 101-10-01-0005

«5" Disbursement Voucher No. 101-10-01 -046

Disbursement Voucher No. 101-10-01-061

«8" General Payroll of the Municipality of Norzagaray, Bulacanfor 2010

Disbursement Voucher No. 101-10-02-224a

"10" IRA Deductions for 1993

"11" IRA Deductions for 1994

"12" IRA Deductions for 1991

"13" IRA Deductions for 1992

"14" Payment of COLA to Mrs. Yolanda Ervas

In a Resolution dated May 24, 2017,^^ this Court admitted all theexhibits filed by the accused.

With the filing of the parties' Memoranda, this case was submittedfor decision.

THE COURT'S RULING

This case arose from a complaint filed by Ms. Yolanda Ervas, agovernment employee whose GSIS life insurance policy has matured, but whofailed to claim on her entire policy. She attributed the deductions madetherefrom to the municipality's delayed payment of GSIS contributions.

In her bid to present evidence of delayed remittances pertaining to herlife insurance policy, which matured in April 2009, she uncovered delayedremittances beyond such date, or for November 2009, which is now thesubject of this case.

The accused, municipal mayor, treasurer, and accountant ofNorzagaray, Bulacan, are charged wiA the violation of Section 52 of R.A.8291 or the GSIS Act of 1997, which provides:

SECTION 52, Penalty, —

(g) The heads of the offices of the national government, itspolitical subdivisions, branches, agencies and instrumentalities, includinggovernment-owned or controlled corporations and government financialinstitutions, and the personnel of such offices who are involved in thecollection of premium contributions, loan amortization and other accounts

" Id., pp. 392-394Memorandum for accused Legaspi and Esteban dated June 29,2017, Records, Vol. 2, pp. 18-26;

Memorandum for the Prosecution dated July 3,2017, Id., pp. 29-43; Memorandum for accused Marclaldated July 5, 2017, Id., pp. 47-52

'V

f

People V. Fellciano P. Legaspl 9 | P a g eCriminal Case No. SB-16-CRM-0130DECISION

due the GSIS who shall fail, refuse or delay the payment, turnover,remittance or delivery of such accoimts to the GSIS within thirty (30) daysfrom the time that the same shall have been due and demandable shall, uponconviction by final judgment, suffer the penalties of imprisonment of notless than one (1) year nor more than five (5) years and a fine of not less thanTen thousand pesos (PI 0,000.00) nor more than Twenty thousand pesos^20,000.00), and in addition shall suffer absolute perpetual disqualificationfrom holding public office and from practicing any profession or callinglicensed by the government.

In relation thereto, Section 6(b) mandates:

SECTION 6, Collection and Remittance of Contributions, —

(b) Each employer shall remit directly to the GSIS theemployees' and employers' contributions within the first ten (10) days ofthe calendar month following the month to which the contributions apply.The remittance by the employer of the contributions to the GSIS shall takepriority over and above the payment of any and all obligations, exceptsalaries and wages of its employees.

The Information charges the accused with having delayed theremittance of GSIS contributions for November 2009, a fact which the partieshave stipulated on.^^ The Prosecution has further presented evidence to provethat the GSIS contributions for November 2009 amounting to P667,859.37were only remitted on February 12, 2010.^^ These dates and the amountcorrespond to those in the Disbursement Vouchers presented by the accused.^^

Under Sec. 52(g), there is delay in the remittance of GSIS contributionsif such remittance was made more ihan thirty (30) days from the time theyshall have been due and demandable, which is within the first ten (10) days ofthe calendar month following the month to which the contributions apply. Asthere is no dispute that the GSIS contributions of the municipalemployees for November 2009 were paid only in February 2010, therewas clearly a delay in the remittance of GSIS contributions.

The question is whether such delay made accused Legaspi, asMunicipal Mayor; accused Esteban, as Municipal Treasurer; and accusedMarcial, as Municipal Accountant, criminally liable therefor.

In Matalam v. People the Supreme Court explained the importanceof remitting GSIS contributions:

The GSIS was created for the purpose of providing social securityand insurance benefits as well as promoting efficiency and the welfare ofgovernment employees. To this end, the state has adopted a policy ofmaintaining and preserving the actuarial solvency of GSIS funds at alltimes. The fund comes from both member and employer contributions.

Pre-Trial Order dated September 14, 2016, Records, Vol. 1, p. 209Official Receipt dated February 2, 2017 (Exh. "C"), Order of Payment dated February 12, 2010 (Exh. "D")" Exhs. "1" (Marcial) and "2" (Marcial)s® G.R. Nos. 221849-50, April 4, 2016

f

People V. Feliciano P. LegasplCriminal Case No. SB-16-CRM-0130

DECISION

10 I P a g e

Hence, non-remittance of the contributions threatens the actuarialsolvency of the fund, (emphasis supplied)

The non-remittance of contributions proscribed under Sec. 52(g) ofR.A. 8291 is malum prohibitum. What the law punishes is the failure, refiisal,or delay without lawflxl or justifiable cause in remitting or paying the requiredcontributions or accounts.^^

In acts mala prohibita, the only inquiry is, has the law been violated?^®There being no dispute about the delay in remittance, which is a violation ofSec. 52(g) of R.A. 8291, We turn to the merit of the accused's defense.

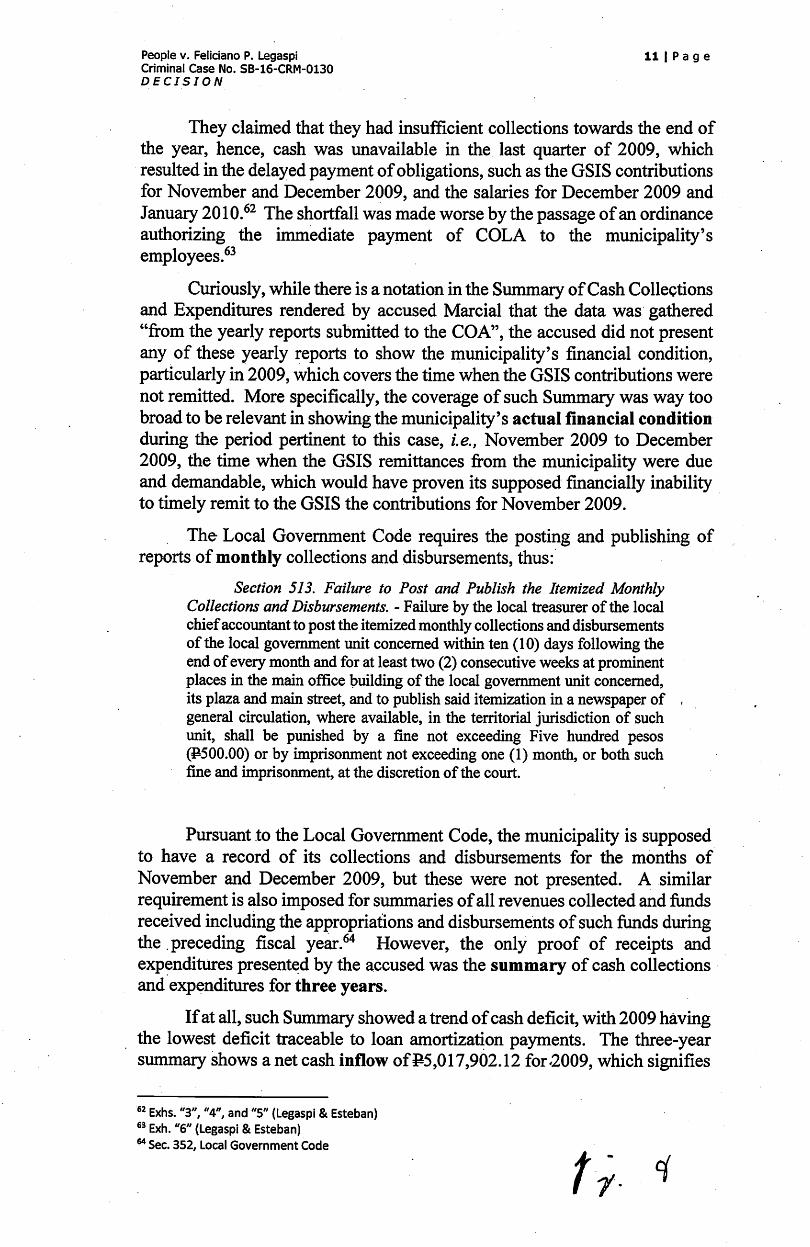

Accused Legaspi and Esteban, municipal mayor and treasurer,respectively, attributed such delay to a "continuous shortfall of cash collectionfrom 2007 to 2009". They presented a Summary of Cash Collections andExpenditures for 2007 to 2009 which showed a cash outflow (deficit) ofP8,421,321.22 in 2007; P5,390,745.42 in 2008; and Pl,627,872.65 in 2009,thus:

MUNiaPAUTY OF NORZAGARAY

ProvincoofButeean

SUMMARY OF CASH COLIECIIONS AND EXPENDITURESFOR THREE (3) CONSECUTIVE YEARS •

CASH REVINUE COIUCTIONS (OF/HQ • InSowi

Eiptnific

Ptfiaa.1 Scnkts

MMflttowtt A Other OpMKki^ CANOin* •FtntncWCot!

TBUI ' . . _

CiplttlOutUvs

TatelCesh Outflows

iiCTCASHwnjowijooTnawsiKioRtHruvKaAiAcnwfrr

CASH AROWSIOOTflOWSVFiieMRKAKaAlAAtVITY: •ADCfc

loan AcqulrtO (PHSAhF)

LESS:

lOM Annitiuttsn Pavntrox

NET CASH BtHOWIOUniOW) •

g.

17S.:27,S99JO lOtA'USAjOl 2lSj07S.tl9 77

SS.9SA^CS«SJ$«.41C.41

S5tl.7t&0>

7S.S9Sja2.60

76.ssu4asa

2.«4.420<a

8i.ass.<42Aa

t6g0t6J096 7<

lAMtSAj:

ISS.4St.Sia.<0 lS<J6i.7S1.2a 17U«U»).U

SUS0.S7e.40 SLSt2JM.fS ».««9j02001

nt.SSS.S92.G0 2aaA47.03S.91 2CaAS5A13.6S

-10,4S9.S9SJO •llAWAai.90 SA17A02.12

• is.9soiaoopo lajsaisaxo laioojooooc

. Xl.SJl.727.72 UJ79.861.S2 ISASS.774.77

. ■iA21.S21.22 -5J90.7SS.42 ■1.627.I72.CS

nardal • . ^Munldptl Aoeountint

Note; . . ,1. All dstss wtre gsthcrcO from lite Votrly Roport SubmiRetJ to CCA.

Legend;6F-General FundNC • Norugaray CoaegcPNB-Philippine National Bank .IBP • land Bank of the PhilippinesCOA • Commission on Autilt

PWK oopyj

59 Ibid.50 Dunlao v. CA, etaL, G.R. No. 111343, August 22,19965^ Exh. "2" (Legaspl & Esteban)

f/.. ^

People V. Fellclano P. Legaspl 11 | P a g eCriminal Case No. SB-16-CRM-0130

DECISION

They claimed that they had insufficient collections towards the end ofthe year, hence, cash was unavailable in the last quarter of 2009, whichresulted in the delayed payment of obligations, such as the GSIS contributionsfor November and December 2009, and the salaries for December 2009 andJanuary 2010.^^ The shortfall was made worse by the passage of an ordinanceauthorizing the immediate payment of COLA to the municipality'semployees.^^

Curiously, while there is a notation in the Summary of Cash Collectionsand Expenditures rendered by accused Marcial that the data was gathered"from the yearly reports submitted to the COA", the accused did not presentany of these yearly reports to show the municipality's financial condition,particularly in 2009, which covers the time when the GSIS contributions werenot remitted. More specifically, the coverage of such Summary was way toobroad to be relevant in showing the municipality's actual financial conditionduring the period pertinent to this case, i.e., November 2009 to December2009, the time when the GSIS remittances from the mxmicipality were dueand demandable, which would have proven its supposed financially inabilityto timely remit to the GSIS the contributions for November 2009.

The Local Government Code requires the posting and publishing ofreports of monthly collections and disbursements, thus:

Section 513. Failure to Post and Publish the Itemized MonthlyCollections and Disbursements. - Failure by the local treasurer of the localchief accountant to post the itemized monthly collections and disbursementsof the local government unit concerned within ten (10) days following theend of every month and for at least two (2) consecutive weeks at prominentplaces in the main office building of the local government unit concerned,its plaza and main street, and to publish said itemization in a newspaper of ,general circulation, where available, in the territorial jurisdiction of suchunit, shall be punished by a fine not exceeding Five hundred pesos^500.00) or by imprisonment not exceeding one (1) month, or both suchfine and imprisonment, at the discretion of the court.

Pursuant to the Local Government Code, the municipality is supposedto have a record of its collections and disbursements for the monAs of

November and December 2009, but these were not presented. A similarrequirement is also imposed for summaries of all revenues collected and fundsreceived including the appropriations and disbursements of such funds duringthe preceding fiscal year.^"^ However, the only proof of receipts andexpenditures presented by the accused was the summary of cash collectionsand expenditures for three years.

If at all, such Summary showed a trend of cash deficit, with 2009 havingthe lowest deficit traceable to loan amortization payments. The three-yearsummary shows a net cash inflow of P5,017,902.12 for'2009, which signifies

" Exhs. "3", and "5" (Legaspl & Esteban)Exh. "6" (Legaspl & Esteban)

^ Sec. 352, Local Government Code

People V. Fellciano P. LegasplCriminal Case No. SB-16-CRM-0130DECISION

12 I P a g e

an excess of revenues over expenses. This actually contradicts the testimonyof accused Legaspi, who explained the reason for ̂ e municipality's financialwoes, as follows:

DIR. PADACA

Q: In Question No. 23, you answered that during those years,from calendar 2007 to 2009, there was a continuous shortfallof cash collections from 2007 to 2009. Is that correct, sir?

WITNESS:

A

Q

A

Yes, ma'am.

Sir, what was the reason of such shortfall of cash collection?

Because of the non-payment of the taxes of thecorresponding companies and different businessmen in ourcommunity.65

XXX

AJ TRESPBSES:

A

Q

A

Q

So, are you telling us that during that time... that the periodwherein there was a late payment of the salaries and wages,especially the GSIS, this was the most severe shortfall thatthe municipality has encountered?

I am assuming it, your Honor.

The most severe?

Yes, your Honor.

And would you be able tell us what was the reason why therewas that severe shortfall in cash collections?

I understand that during those days, there were smallcollections on the part of the - - we have three differentcement factories. Actually the cement factories in our townare the big source of our income. So that if they're goingto pay the taxes on time, we will have many cash to pay allthe obligations.^^

As alluded to by accused Legaspi, the actual payment of themunicipality's obligations, in this case, the employees' salary, firom whichtheir GSIS contributions are deducted,^^ depend largely on the municipality'srevenue collections. Under existing law, local government units, in additionto having administrative autonomy in the exercise of their functions, enjoyfiscal autonomy as well. Fiscal autonomy means that local governments havethe power to create their own sources of revenue in addition to their equitableshare in the national taxes released by the national government, as well as thepower to allocate their resources in accordance with their own priorities. Itextends to the preparation of their budgets, and local officials in turn have to

® TSN dated November 16, 2016 (p.m.), pp. 33-34®®/d,p. 48(57Sec. 6, R.A. 8291

f/. ^

People V. Feliclano P. Legaspl 13 | P a g eCriminal Case No. SB-16-CRM-0130

DECISION

work within the constraints thereof.^® A consistent financial shortfall, aspresented by the accused in their defense, actually demonstrates less thaneffective fiscal management. This, however, is hardly justified in this case.

As appearing in Exhibit "2", the resulting deficit in 2009 does not showa direct relation to the delay in payment of GSIS remittances covering themonth of November 2009. If at all, the expenses for Personal Services,Maintenance and other Operating Expenses, Financial Cost, and CapitalOutlay were sufficiently met by the Cash Revenue Collections. The deficitappeared to have arisen from the payment of "Loan Amortization Payments"which was not inter-related by the accused to the payment of GSIS premiumpayments. We cannot, therefore, be made to speculate and attribute the reasonfor the delay in GSIS remittances to a perceived shortfall in cash collection.

Neither may the delay in remittance to GSIS be validly attributed to thebackpa3mient of COLA on January 25, 2010, by which time the November2009 GSIS remittances were already delayed. Worse, if the delay inremittance was indeed attributable to die payment of COLA, it would meanthat the funds earmarked for the payment of GSIS contributions / loanamortizations were used for the payment of the COLA, which was admittedlynot even in the annual budget.^^ This is contrary to the Local GovernmentCode, which mandates that funds shall be available exclusively for thespecific purpose for which they have been appropriated.^^

The head of office and the personnel of such office who are involved inthe collection of premium contributions, loan amortization and other accountsdue the GSIS are liable for delays in remittance under Sec. 52 of R.A. 8291.As municipal mayor, accused Legaspi is the chief executive of the municipalgovemment,^^ and as such, is liable pursuant to R.A. 8291.

As municipal treasurer, accused Esteban was in charge of thedisbursement of dl local government funds.^^ As such, it was her duty toremit to the GSIS the contributions deducted fi*om the municipal employees'salaries.

For his part, accused Marcial interposed the lone defense that hisfunctions as municipal accountant did not involve the collection andremittance of GSIS contributions and loan amortizations, and he, in factprepared the disbursement voucher for these remittances before they weredue. Under the Local Government Code, the municipal accountant has thefollowing functions:

(b) The accountant shall take charge of both the accounting and internalaudit services of the local government unit concerned and shall:

Pimentel v. Aguirre, G.R. No. 132988, July 19, 2000

Joint Counter-Affidavit of Legaspi, Esteban and Marcial, Exh. "1" (Legaspi & Esteban), "3" (Marcial), p. 2;TSN dated March 29, 2017, p. 16

Sec. 336, Local Government Code

Sec. 444, Local Government CodeId., Sec. 470(d)(2)

People V. Feiiciano P. Legaspl 14 | P a g eCriminal Case No. SB-16-CRM-0130DECISION

(1) Install and maintain an internal audit system in the localgovernment unit concerned;

(2) Prepare and submit financial statements to the governor ormayor, as the case may be, and to the sanggunian concemed;

(3) Appraise the sanggunian and other local government officials onthe financial condition and operations of the local government unitconcemed;

(4) Certify to the availability of budgetary allotment to whichexpenditures and obligations may be properly charged;

(5) Review supporting documents before preparation of vouchers todetermine completeness of requirements;

(6) Prepare statements of cash advances, liquidation, salaries,allowances, reimbursements and remittances pertaining to the localgovernment unit;

(7) Prepare statements of joumal vouchers and liquidation of thesame and other adjustments related thereto;

(8) Post individual disbursements to the subsidiary ledger and indexcards;

(9) Maintain individual ledgers for officials and employees of thelocal government unit pertaining to payrolls and deductions;

(10) Record and post in index cards details of purchased furniture,fixtures, and equipment, including disposal thereof, if any;

(11) Accoxmt for all issued requests for obligations and maintain andkeep all records and reports related thereto;

(12) Prepare joumals and the analysis of obligations and maintainand keep all records and reports related thereto; and

(13) Exercise such other powers and perform such other duties andfunctions as may be provided by law or ordinance.^^

Indeed, none of these functions relate to the collection anddisbursement of GSIS contributions. Notably, the delayed remittance to theGSIS was not attributed to the delayed issuance of the Disbursement Voucher,but to the shortfall in funds. The Prosecution likewise failed to prove thataccused Marcial was responsible for the collection and remittance of GSIScontributions for November 2009.

For this reason, accused Marcial shall be exculpated firom the charge.

Finally, that the deductions made fi*om private complainant YolandaErvas' life insurance policy did not result fi*om the delay in the November2009 remittance to the GSIS need not detain us at length. As stated at the

Id., Sec. 474

fr. r

People V. Fellclano P. LegaspiCriminal Case No. SB-16-CRM-0130

DECISION

15 I P a g e

outset, Ervas' life insurance policy has in fact already matured prior thereto,or in April 2009. This, however, does not change the fact that Sec. 52(g) ofR.A. 8291 has been violated, and an offense has been committed. Theimportance of the timely remittance to the GSIS of contributions / otheraccounts deducted from employees' salary cannot be gainsaid. The GSIS wascreated for the purpose of providing social security and insurance benefits aswell as promoting efficiency and the welfare of government employees.^"^This purpose would be defeated if the GSIS Social Insurance Fund used tofinance the benefits administered by the GSIS^^ runs short because of thefailure, refusal or delay in the remittances by the government.

Nominal though a delay in the payment of one month of remittancesmay seem, when considered with the wide coverage of the GSIS, and in lightof the potential urgency of its members' claims, it has to be dealt with as thelaw intended.

WHEREFORE, accused FELICIANO P. LEGASPI and CRISTETAM. ESTEBAN are found GUILTY beyond reasonable doubt of violation ofSec. 52(g) of R.A. 8291 in relation to Section 6(b) of the same law. They areeach sentenced to suffer the penalty of imprisonment of ONE (1) YEAR andto pay a fine of Ten Thousand Pesos ̂ 10,000.00) and suffer absoluteperpetual disqualification from holding public office and from practicing anyprofession or calling licensed by the government.

On reasonable doubt, accused MANUEL R. MARCIAL isACQUITTED of the charge.

SO ORDERED.

MA. THERESA DOQIORES C. GOMEZ-ESTOESTAAssociate Justice, Chairperson

WE CONCUR:

Assoc

SPESES

Justice

BAYANI q. JACINTOAssociate Justice

GSIS V. CA, eta!., 6.R. No. 128471. March 6,1998

Sec. 34, R.A. 8291

People V. Feliclano P. LegasplCriminal Case No. SB-16-CRM-0130DECISION

16 i P a g e

ATTESTATION

I attest that the conclusions in the above Decision were reached in

consultation before the case was assigned to the writer of the opinion of theCourt's Division.

i?(Dq^LoMA. THERESA DqgLDRES C. GOMEZ-ESTOESTAChairperson, Seventh Division

CERTIFICATION

Pursuant to Article Vin, Section 13 of the Constitution, and theDivision Chairman's Attestation, it is hereby certified that the conclusions inthe above Decision were reached in consultation before the case was assignedto the writer of the opinion of the Court's Division.

AMPARO MrC^^OTA^-TPresiding Justice

H