fadhilconsult.files.wordpress.com · web viewinterest can either be simple or compound simple...

TRANSCRIPT

1

WEEK 2

TIME VALUE OF MONEY

& FINANCIAL MATHEMATICS

FINANCIAL MANAGEMENT

2

Compound Interestis based

on the fact thatas

interest is calculated

(EVERY COMPOUNDING PERIOD)

it isadded

to the

balance

Simple Interest is calculated on

the original principle

Therefore, the amount of interest each period remains

the same

SIMPLE INTEREST IS SUCH THAT

COMPOUNDING DOES NOT OCCUR

The amount of simple

FINANCIALMATHEMATICS

Interest can either be simple or compound

Simple Interest Calculated only on the original principle.

Compound Interest Calculated on the principle and on

3

oraccumulated sum

interest is directly proportional to time.

ANNUITY

An ANNUITYrepresentsa stream

ofregular payments

usually of

equal amount

MostORDINARY ANNUITIES

AndANNUITIES DUEfall under the heading

ofSIMPLE ANNUITIES

which means thatINTEREST

is compoundedor

charged at the same frequencyas the

PAYMENTS

ORDINARY ANNUITIES

describe the situationwhere

INTERESTis

compoundedor

chargedat

DIFFERENT TIMESto when

PAYMENTSare made

ORDINARY ANNUITYAn Ordinary Annuity isone whose payments aremade at the end of each

period.

The value at time zero is the present value

4

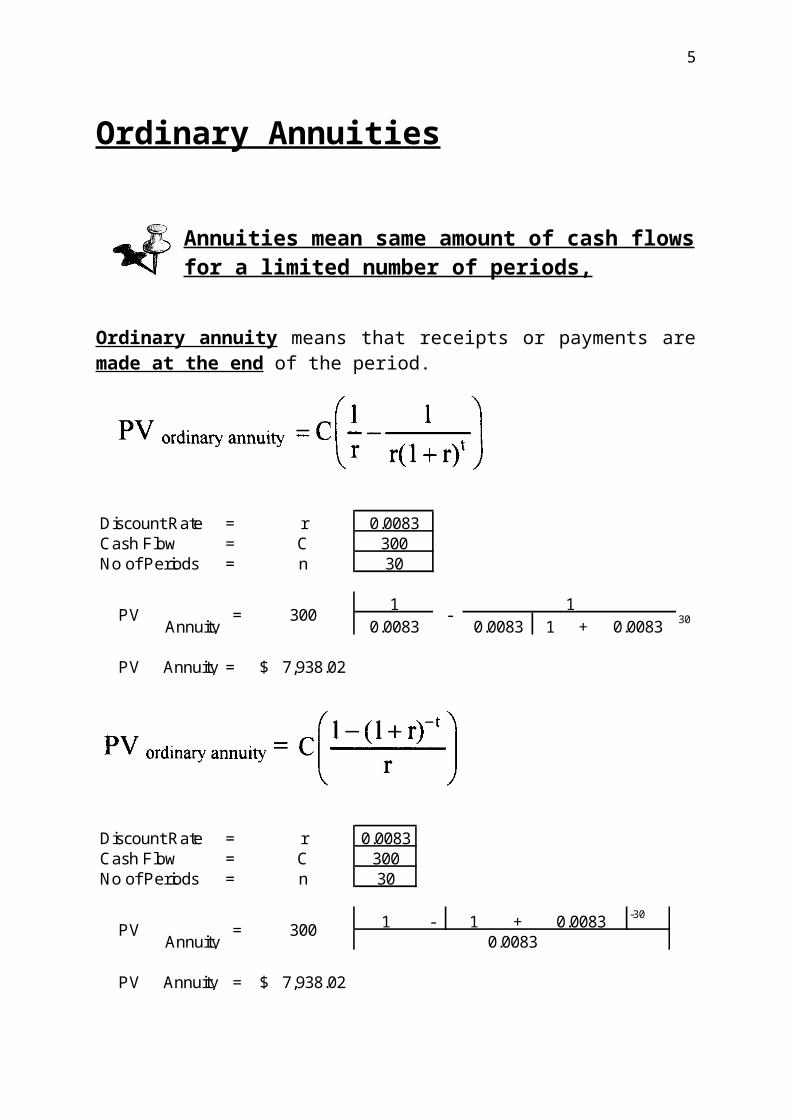

Ordinary Annuities

Annuities mean same amount of cash flows for a limited number of periods,

Ordinary annuity means that receipts or payments are made at the end of the period.

Discount Rate = r 0.0083Cash Flow = C 300No of Periods = n 30

10.0083 0.0083 1 + 0.0083 30

PV Annuity = 7,938.02$

1PV

Annuity= 300 -

Discount Rate = r 0.0083Cash Flow = C 300No of Periods = n 30

1 - 1 + -30

PV Annuity = 7,938.02$

PVAnnuity

= 300 0.00830.0083

5

Growth Annuity

Discount Rate = r 0.1Growth Rate = g 0.04Cash Flow = C 100000No of Periods = n 20

1 + 20

0.1 - 0.04 0.1 - 0.04 x 1 + 0.1 20

PV Annuity = 1123839.178

PVAnnuity

= 100000 1 - 0.04

8.3 I30 n

300 +/- PMTCOMP PV

= 7938.02

6

ANNUITY DUE

An Annuity Due is one whose payments are made at the

beginning of each period.

The first payment is due immediately

Place calculator in BEGIN mode

Discount Rate = rCash Flow = CNo of Periods = n

1 - 1 + -2

PV Annuity =

0.10.1

273.55$

0.1100

3

PVAnnuity

= 100 + 100

7

10 I3 n

100 +/- PMTCOMP PV

= 273.55

DEFERRED ANNUITY

A Deferred Annuity Due is one whose payments commence only after a certain number of periods have elapsed.

A Deferred Annuity due means that receipts or payments begin at some time in the future.

1Discount Rate Discount Rate 1 + Discount Rate no of periods

1 + Discount Rate no of periods

-1

PVAnnuity

= Cash Flow

Discount Rate = r 0.1Cash Flow = C 100000No of Periods = n 20No of Periods before beginning 4

10.1 0.1 1 + 0.1 20

1 + 0.1 4

PV Annuity = 581,487.86$

= 100000 -1

PVAnnuity

8

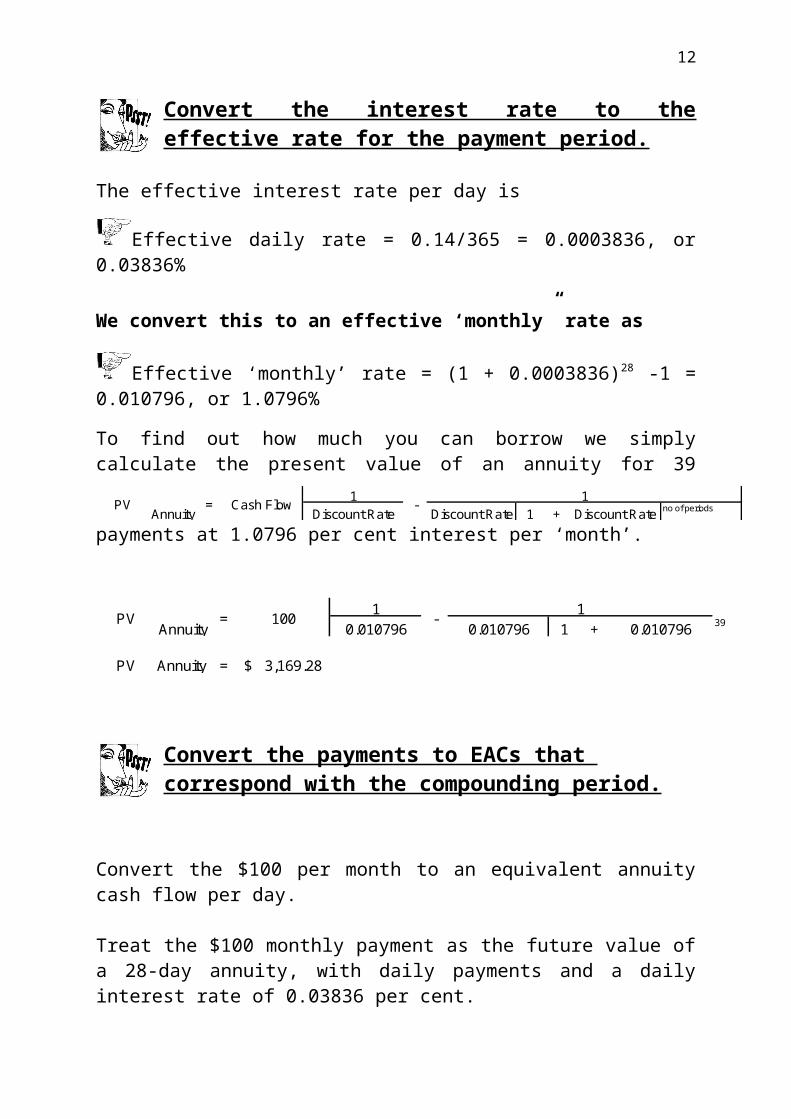

GENERAL ANNUITIES

Note that the frequency with which the annuity payments are made does affect the present value of the investment. For example, payments are made monthly, but the interest may be compounded daily. Such annuities are called General Annuities. In order to value such annuities, the payment intervals and the compounding intervals should be the same.

Two MethodsExample

Suppose you plan to buy a car and finance it with a loan.

10 I20 n

100000 +/- PMTCOMP PV

= 851356.37

10 I4 n

851356.37 +/- FVCOMP PV

= 581487.86

Step 1

Step 2

9

You believe you can afford repayments of $100 per month. The bank will give you a three-year loan at an interest rate of 14 per cent per year

compounded daily with payments monthly. What sort of car can you afford to buy? Assume that ‘monthly’ loan payments means a payment every four weeks (28

days), which totals 39 payments over the three years.

10

Convert the interest rate to the effective rate for the payment period.

The effective interest rate per day is

Effective daily rate = 0.14/365 = 0.0003836, or 0.03836%

We convert this to an effective ‘monthly” rate as

Effective ‘monthly’ rate = (1 + 0.0003836)28 -1 = 0.010796, or 1.0796%

To find out how much you can borrow we simply calculate the present value of an annuity for 39 payments at 1.0796 per cent interest per ‘month’.

10.010796 0.010796 1 + 0.010796 39

PV Annuity = 3,169.28$

PVAnnuity

= 1001

-

Convert the payments to EACs that correspond with the compounding period.

Convert the $100 per month to an equivalent annuity cash flow per day.

Treat the $100 monthly payment as the future value of a 28-day annuity, with daily payments and a daily interest rate of 0.03836 per cent.

Solving for the daily payment in the following equation gives us the daily EAC:

1Discount Rate Discount Rate 1 + Discount Rate no of periodsPV

Annuity= -

1Cash Flow

11

TO CALCULATE EACAnnual Days

Discount Rate = r 0.00038 0.14 365Payment = C 100No of Periods = n 28

1Discount Rate Discount Rate 1 + Discount Rate no of periods

10.00038 0.000383562 1 + 0.000383562 28

= EAC 27.84$

= 3.5913$ EAC

100

-1

= EAC -1

Payment

100

= Cash Flow

Now we find the value of the loan that runs for 1092 days (39 x 28 days)

1Discount Rate Discount Rate 1 + Discount Rate no of periods

10.000384 0.000384 1 + 0.000384 1092

PV Annuity = 3,203.53$

-1

PVAnnuity

= 3.59133 -1

PVAnnuity

= Cash Flow

12

PERPETUIY

AnANNUITY

whosePAYMENTS

areintended

toCONTINUEFOREVER

PERPETUITYPRESENT VALUE

(Simple ordinary Perpetuity)

R = Payment (PMT)i = Interest

Note*** There is no Future Value for Perpetuities

The present value of perpetuities that are not growing is calculated using this formula:

Cash FlowDiscount RatePerpetuity

PV =

Cash Flow 100Discount Rate 0.07

1000.07

PV Perpetuity = 1,428.57$

PV Perpetuity

=

The present value of perpetuities that are growing is calculated using this formula, that is, cash flow (C) is constant.

Discount Rate - Growth RateCash FlowPV

Perpetuity=

Cash Flow 6500Discount Rate 0.12Growth Rate 0.05

0.12 - 0.05

PV Perpetuity = 92,857$

6500PV Perpetuity

=

13

NOMINAL INTEREST RATE

14

EFFECTIVE RATE OF INTEREST

15

The formula used to convert nominal to AER is as follows:

NOMINAL INTEREST RATE Nominal interest rates are interest rates before taking out the effects of inflation.

16

Real Nominal RateInterest = Interest - of

Rate Rate Inflation

Nominal Real RateInterest = Interest + of

Rate Rate Inflation

therefore

Example

17

When the bank quotes you a 10 per cent interest rate it is quoting you a nominal interest rate. The rate tells you how rapidly your money will grow:

11001.06

= 1,037.74$

The bank account offers a l0 per cent nominal rate of return or the bank offers a 3.774 per cent expected real rate of return.

The formula that relates the nominal interest rate to the real rate is:

In our example

1.10 = (1.03774)(1.06)

However, with an inflation rate of 6 per cent you are only 3.774 per cent better off at the end of the year than

at the start: