thenextrecession.files.wordpress.com€¦ · web viewthat’s because trade among eu economies is...

TRANSCRIPT

The rise and (fall?) of the euroby Michael Roberts

The great European project that started after the WW2 had two aims: first, it was to ensure that there were never any more wars between European nations; and second, to make Europe an economic and political entity that could rival America and Japan in global capital. This project would be led by Franco-German capital. The euro project went further and aimed at integrating all European capitalist economies into one unit to compete with the US and Asia in world capitalism within a single market and with a rival currency to the dollar.

Has this worked and will the euro currency union survive?

Mainstream theory: OCA

Let’s start with some theory. Mainstream economic theory starts with the concept of an Optimal Currency Area (OCA), where all members benefit from a single currency and monetary policy.1

The OCA says it makes sense for national economies to share a common monetary policy if they (1) have similar business cycles and/or (2) have in place economic ‘shock absorbers’ such as fiscal transfers, labour mobility and flexible prices. 2

If (1) is true, then a one-size-fits-all monetary policy is possible.

If (2) is true, then a national economy can be on a different business cycle than the rest of the currency union and still do okay inside it.

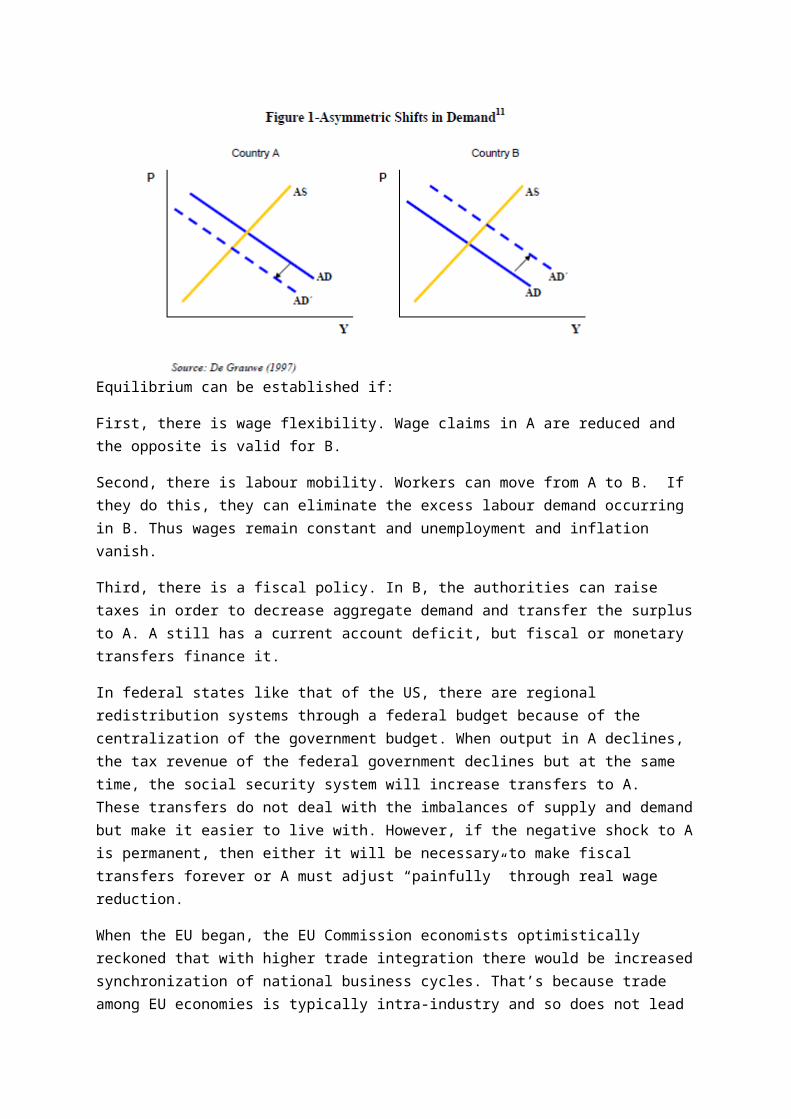

This neoclassical theory was propounded by Mundell (1961)3 who offered some non-exchange rate means (assuming no transaction costs) of achieving an optimal currency union, when in one country (A) the business cycle leads to a fall in demand and vice versa in country B.

Equilibrium can be established if:

First, there is wage flexibility. Wage claims in A are reduced and the opposite is valid for B.

Second, there is labour mobility. Workers can move from A to B. If they do this, they can eliminate the excess labour demand occurring in B. Thus wages remain constant and unemployment and inflation vanish.

Third, there is a fiscal policy. In B, the authorities can raise taxes in order to decrease aggregate demand and transfer the surplus to A. A still has a current account deficit, but fiscal or monetary transfers finance it.

In federal states like that of the US, there are regional redistribution systems through a federal budget because of the centralization of the government budget. When output in A declines, the tax revenue of the federal government declines but at the same time, the social security system will increase transfers to A. These transfers do not deal with the imbalances of supply and demand but make it easier to live with. However, if the negative shock to A is permanent, then either it will be necessary to make fiscal transfers forever or A must adjust “painfully” through real wage reduction.

When the EU began, the EU Commission economists optimistically reckoned that with higher trade integration there would be increased synchronization of national business cycles. That’s because trade among EU economies is typically intra-industry and so does not lead to higher specialization, which could cause increased possibility of ‘asymmetric shocks’ ie differing business cycles.

This neoclassical view of mobility of labour and wage flexibility is disputed by Keynesian theory. Krugman (1993)4 argues that higher trade integration leads to higher specialization under the assumption of decreasing transport costs. Because of these economies of scale, higher integration leads to a regional concentration of industrial activity. As a result, asymmetric shocks are more likely to occur (since output is less diversified) and so bring extra costs to monetary union.

But Krugman’s view assumes that regional concentration of industry will not cross the borders of the countries that form the union. If it does, then asymmetric shock is not country-specific and floating exchange rate variation (Krugman’s solution) could not be used to deal with asymmetric shocks anyway.

The evidence

The essence of OCA theory is that trade integration and a common currency will lead to convergence of GDP per head and labour productivity among participants. The evidence for the success of common trade and free movement of labour between countries is that it has led to ‘convergence’ among participants in the EU. Convergence on productivity levels has been as strong as in fully federal US.

So the move to a common market, customs union and eventually the political and economic structures of the EU was a relative success. The EU-12/15 from the 1980s to 1999 managed to achieve a degree of harmonisation and convergence: with the weaker capitalist economies growing faster than the stronger.

But that was only up to the point of the start of EMU. The evidence for convergence under the EMU since 1999 is much less convincing. Rose (2015) finds that “there is no consistent evidence that EMU stimulated trade.” De Grauwe (2016)5 concludes that EMU is not an OCA because it lacks “a mechanism that can deal with divergent economic developments (asymmetric shocks) between countries.” Divergence, not convergence has been the order of the day and these divergent developments “often lead to large imbalances, which crystallise in the fact that some countries built up external deficits and other external surpluses”. Business cycles for economies within EMU are reasonably correlated but it seems that the weaker and more peripheral the economy, the less correlated they are.

Business cycle component of GDP growth

Correlation coefficients of cyclical components of GDP growth (1995-2014)

Those who wish the preserve the euro project – like the EU Commission, the majority of EU politicians and most capitalist corporations – recognize that the only way to do so is to extend the process towards more integration. That means a ‘banking union’ so that all the banks in the Eurozone are subject to control by the euro institutions like the ECB, and not national government regulators. Better still would be the establishment of a full ‘fiscal union’, so that taxes and spending are controlled by Eurozone institutions and deficits in one EMU state are automatically met by transfers from surplus states. That is the nature of a federated state like Canada, the US, or Australia. These transfers reach 28% of US GDP compared to the controlled and conditional transfers under EU budgets and bailouts of less than 10% of one state’s GDP.

28

9

6

3 1

0

5

10

15

20

25

30

US states Por Ire Gre Spa

Internal automatic fiscal transfer as % of GDPSource:OECD

In the EMU, there has not been enough ‘fiscal space’ (transfer mechanisms) or any debt consolidation (to write off past imbalances). So there remains a dilemma between moving to full fiscal union which would mean the abandonment of national sovereignty or maintaining “a balanced budget rule (that) would aggravate, rather than smooth out, the business cycle.” (Giancarlo Corsetti, Luca Dedola, Marek Jarociński, Bartosz Mackowiak, Sebastian Schmidt, 2017).6 Leaving national governments to decide their own fiscal policy “would make the business cycle more volatile.”

This dilemma was exposed in the euro debt crisis of 2011 onwards, which led to the so-called bailouts of Ireland, Portugal, Spain, Cyprus and the near exit of Greece. After much kicking and screaming, the Germans and the EU agreed to set up some fiscal transfer funds, first the EFSF and then the ESM. But these are not automatic fiscal union transfers; they are contingent and conditional on meeting fiscal targets set by a Troika (EU, IMF, ECB) program. There is not real EU budget and national governments can still set their own budgets. Germany, in particular, remains opposed to shelling out cash to ‘wayward’ countries which cannot get their public finances ‘in order’.

Marxist theory of currency unions

How does Marxist theory approach the issue? It starts from the opposite position of neoclassical mainstream. There is no tendency to equilibrium in trade and production cycles under capitalism. So fiscal, wage or price adjustments will not restore equilibrium and may be so huge as to be socially impossible without breaking up the currency union. Capitalism is an economic system that combines labour and trade, but unevenly. The centripetal forces of combined accumulation and trade are countered by centrifugal forces of uneven development.

The idea that ‘free trade’ is beneficial to all countries and to all classes is a ‘sacred tenet’ of mainstream economics. But it is a fallacious proposition based on the theory of comparative advantage: that if each country concentrated on producing goods or services where it has a ‘comparative advantage’ over others, then all would benefit. Trading between countries would balance and wages and employment would be maximised.

But this is empirically untrue. Countries run huge trade deficits and surpluses for long periods; have recurring currency crises; and workers lose jobs from competition from abroad without getting new ones from more competitive sectors.

The Marxist theory of international trade is based on the law of value. Take China. Chinese capital has a lower organic composition of capital (OCC) than the more technically advanced US. So the lower OCC country (China) will produce more value per unit of capital invested than the US. By exchanging each unit of output (and the value contained in it) for the product of the US with its higher OCC (which contains less value), China loses value to the latter. But if China produces more total output (value), then it can run a trade surplus with the US, while losing value to the US on each unit of trade. The US deficit with China means that it is receiving more value from China in the trade exchange but China can compensate for the transfer of value to the US by expanding its scale of production and so run an overall surplus

In the Eurozone, Germany has a higher OCC than Italy. Thus in any trade between the two, value is transferred from Italy to Germany. But Italy cannot compensate for this by increasing the scale of its production/export to Germany, unlike China. So it transfers value to Germany and it still runs a

deficit on total trade with Germany. In this situation, Germany gains within the Eurozone at the expense of Italy. As nearly all other member states cannot scale up their production to surpass Germany, unequal exchange is compounded across the EMU. On top of this, Germany runs a trade surplus with other states, which it can use to invest more capital abroad into the deficit countries.

This explains why the core countries of EMU diverged from the periphery and there was no convergence. With a single currency, the value differentials between the weaker states (lower OCC) and the stronger (higher OCC) were exposed with no option to compensate by devaluation of any national currency or scale up overall production. The weaker capitalist economies (in southern Europe) within the euro area lost ground to the stronger (in the north).

Franco-German capital expanded into the south and east to take advantage of cheap labour there, while exporting outside the euro area with a relatively competitive currency. But the weaker EMU states built up trade deficits with the northern states and were flooded with northern credit and capital that created property and financial booms out of line with growth in the productive sectors of the south.

Lessons of the euro crisis: the cause

The cause of the change from fast growth and convergence from the 1970s to slow growth and divergence from the 1990s can be found in the sharp decline in the profitability of capital in the major EU states (as elsewhere) after the end of the Golden Age of post-war expansion.

This led to fall in investment growth, productivity and trade divergence. European capital, following the model of the Anglo-Saxon economies, adopted neo-liberal policies: anti trade union laws, deregulation of labour and product markets, free movement of capital and privatisations. The aim was to boost profitability. This succeeded at least for the more advanced EU states of the north, but less so for the south.

The introduction of the euro added another limitation on growth in the south and convergence with the north. A strong euro was bad for exports in the south and gave investment power to the north. The debts being built up by the south with the north were exposed in the crash and sparked the ‘euro crisis’, but only after the global financial crash.

The EU leaders had set criteria for joining the euro, but these criteria were all monetary (interest rates and inflation) and fiscal (budget deficits and debt). There were no convergence criteria for productivity levels, GDP growth, investment or employment. Why? Because those were areas for

the free movement of capital (and labour) and capitalist production for the market and not the province of interference or direction by the state. After all, the EU project is a capitalist one.

The global slump dramatically increased the divergent forces within the euro. The fragmentation of capital flows between the strong and weak Eurozone states exploded. The capitalist sectors of the richer economies like Germany stopped lending directly to the weaker capitalist sectors in Greece and Slovenia, etc. As a result, in order to maintain a single currency for all, the official monetary authority, the ECB, and the national central banks had to provide the loans instead. The Eurosystem’s ‘Target 2’ settlement figures between the national central banks revealed this huge divergence within the Eurozone.

-1500

-1000

-500

0

500

1000

1500

2016

Aug

2016

Apr

2015

Dec

2015

Aug

2015

Apr

2014

Dec

2014

Aug

2014

Apr

2013

Dec

2013

Aug

2013

Apr

2012

Dec

2012

Aug

2012

Apr

2011

Dec

2011

Aug

2011

Apr

2010

Dec

2010

Aug

2010

Apr

2009

Dec

2009

Aug

2009

Apr

Surplus countries Deficit countries

‘Target 2’ net settlement balance in Eurozone Ebn, Source: ECB

The evidence shows that those EU states that got a quicker recovery in profitability of capital were able to recover from the euro crisis (Germany, Netherlands, Ireland etc), while those that did not improve profitability stayed deep in depression (Greece).

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0Chg in net return on capital 2009-17 %

Source: AMECO

Lessons of the euro crisis: the neoclassical solution of austerity

The imposition of austerity measures by the Franco-German EU leadership on the distressed countries during the crisis was the result of this ‘halfway house’ of euro criteria. There was no full fiscal union (automatic transfer of revenues to those national economies with deficits) and there was no automatic injection of credit to cover capital flight and trade deficits – as there is in full federal unions like the United States or the United Kingdom. Everything had to be agreed by tortuous negotiation among the Euro states.

Why? Because Franco-German capital was not prepared to pay for the ‘excesses’ of the weaker capitalist states. Thus the bailout programmes were combined with ‘austerity’ to make the people of the distressed states pay with cuts in welfare, pensions and real wages, and to repay (virtually in full) their creditors (the banks of France and Germany and the UK). The debt owed to the Franco-German banks was transferred to the EU state institutions and the IMF – in the case of Greece, probably in perpetuity.

The ECB, the EU Commission, and the governments of the Eurozone proclaimed that austerity was the only way Europe was to escape from the Great Recession. Austerity in the public spending could force convergence on fiscal accounts too. But the real aim of austerity was to achieve a sharp fall in real wages and cuts in corporate taxes and thus raise the share of profit and profitability of capital. But now there has been a decade of austerity and very little progress has been achieved in meeting the fiscal targets (particularly in reducing debt ratios); and, more important, in reducing the imbalances within the Eurozone on labour costs or external trade to make the weaker more ‘competitive’.

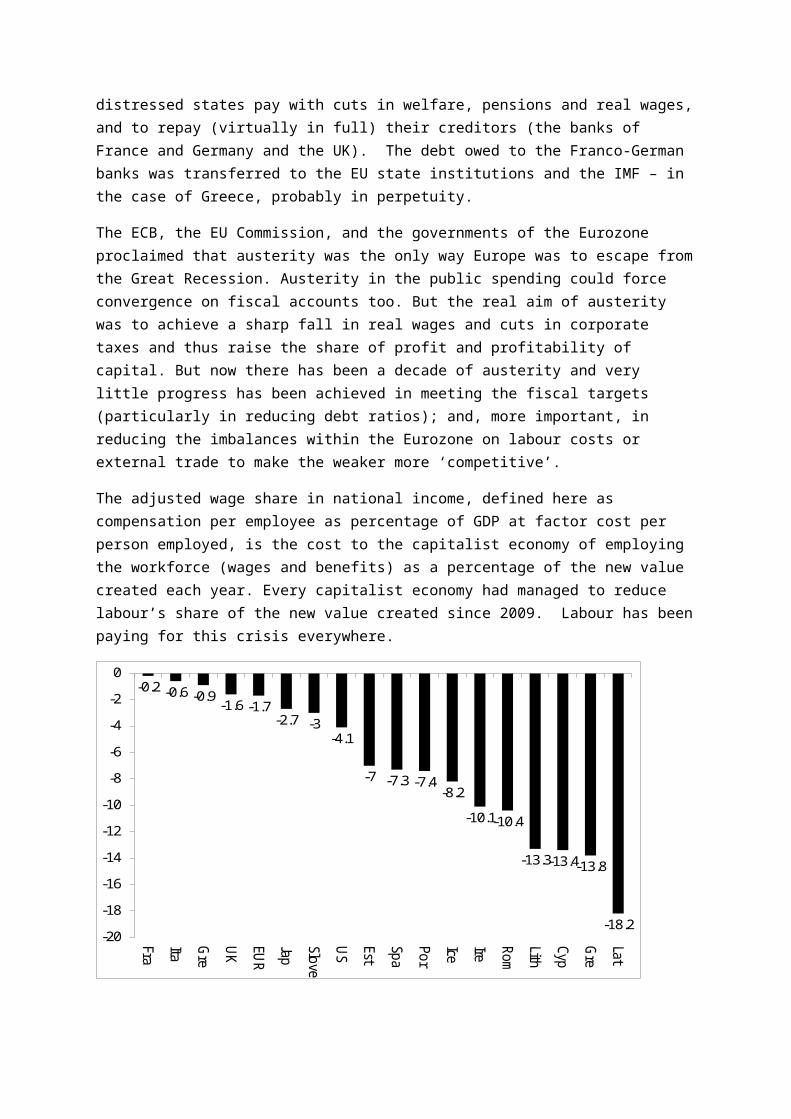

The adjusted wage share in national income, defined here as compensation per employee as percentage of GDP at factor cost per person employed, is the cost to the capitalist economy of employing the workforce (wages and benefits) as a percentage of the new value created each year. Every capitalist economy had managed to reduce labour’s share of the new value created since 2009. Labour has been paying for this crisis everywhere.

-0.2 -0.6 -0.9 -1.6 -1.7

-2.7 -3 -4.1

-7 -7.3 -7.4 -8.2

-10.1 -10.4

-13.3 -13.4 -13.8

-18.2 -20

-18

-16

-14

-12

-10

-8

-6

-4

-2

0

Fra

Ita Gre

UK EUR

Jap

Slove

US Est

Spa

Por

Ice

Ire Rom

Lith

Cyp

Gre

Lat

Reduction in labour’s share of new value added 2009-15 (%)Source: AMECO, author’s calculations

Not surprisingly, it has been the workers of the Baltic states and the distressed Eurozone states of Greece, Ireland, Cyprus, Spain, and Portugal who have taken the biggest hit to wage share in GDP. In these countries, real wages have fallen, unemployment has rocketed, and hundreds of thousands have left their homelands to look for work somewhere else. That has enabled companies in those countries to sharply increase the rate of exploitation of their reduced workforce, although so far that has not been enough to restore profitability to levels before the Great Recession and thus sustain sufficiently high new investment for a sustained path of growth.

Emigration: the safety valve

One of the striking contributions to the fall in labour’s share of new value has been from emigration. This was one of the OCA criteria for convergence during crises and it has become an important contribution in reducing costs for the capitalist sector in the larger economies like Spain. Before the crisis, Spain was the largest recipient of immigrants to its workforce: from Latin America, Portugal, and North Africa. Now that has been completely reversed.

Hundreds of thousands of migrants are heading back home every year, and the country’s overall population is falling for the first time since records began. Spain’s population jumped from 40m in 1999 to more than 47m in 2010, one of the most pronounced demographic shifts experienced by a European country in modern times. The surge was almost entirely the result of migrants from countries such as Ecuador, Bolivia, Romania, and Morocco. The number of foreigners living in Spain increased eightfold in just over a decade, while their share of the population soared from less than 2% in 1999 to more than 12% in 2009.

But during the Euro crisis, there was net emigration. In 2008, one year after the start of the crisis, Spain still recorded 310,000 more migrant arrivals than departures. That number fell to just 13,000 the following year before turning negative in 2010. In 2012 there were over 140,000 more departures than arrivals, and the pace of the exodus is picking up fast. According to the national statistics office, the foreign-born population now stands at 6.6m, down from more than 7m just two years ago.

This net emigration acted a safety valve for Spanish capitalism – unemployment would have been even higher without it. It helped the capitalist sector get labour costs down without provoking a social explosion. However, over the longer term, this spells deep trouble for capitalist expansion in Spain. There remains a huge overhang of unfilled real estate from the property boom that triggered the crisis in Spain. A falling population means that this form of unproductive capital will continue to weigh down Spain’s recovery. And with a public-sector debt-to-GDP ratio hitting 100%, there will be fewer workers to extract value to service that debt.

The Keynesian solution

Keynesians blame the crisis in the Eurozone on the rigidity of the single-currency area and on the strident ‘austerity’ policies of the leaders of the Eurozone, Germany. But the euro crisis is only partly a result of the policies of austerity being pursued, not only by the EU institutions, but also by states outside the Eurozone like the UK. Alternative Keynesian policies of fiscal stimulus and/or devaluation where applied have done little to end the slump and still made households suffer income losses. Austerity means a loss of jobs and services and thus nominal income. Keynesian policies mean a loss of real income through higher prices, a falling currency, and eventually rising interest rates.

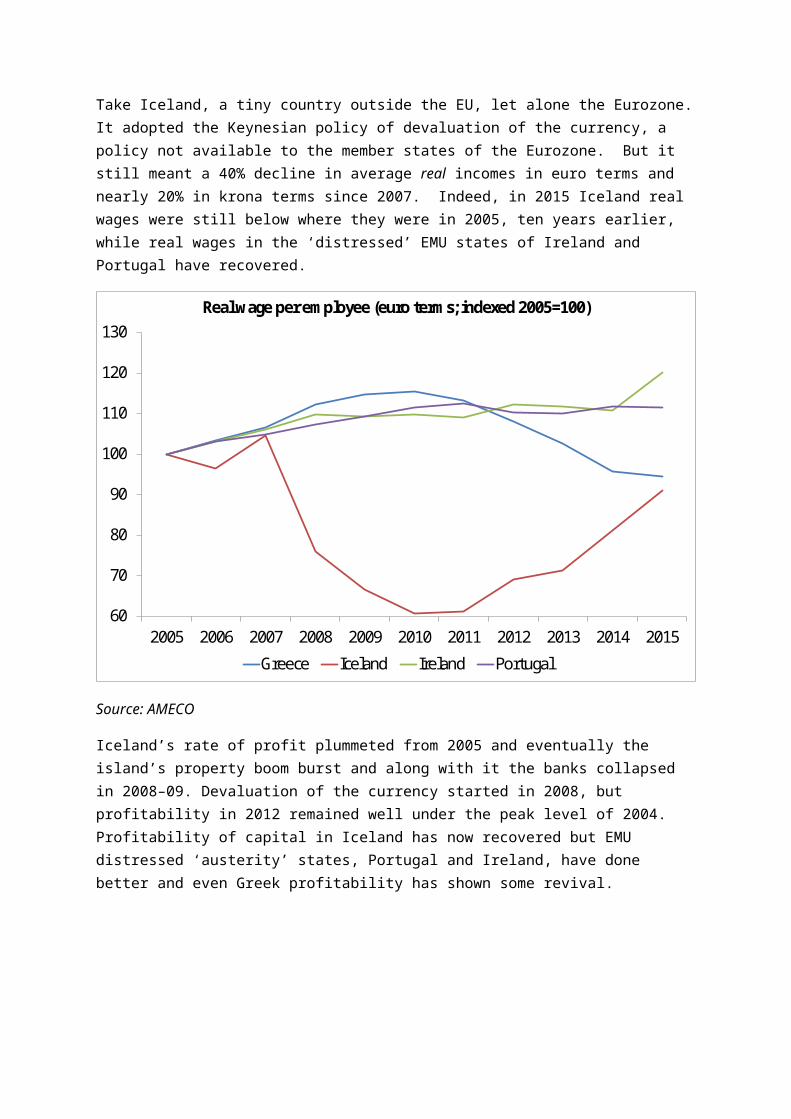

Take Iceland, a tiny country outside the EU, let alone the Eurozone. It adopted the Keynesian policy of devaluation of the currency, a policy not available to the member states of the Eurozone. But it still meant a 40% decline in average real incomes in euro terms and nearly 20% in krona terms since 2007. Indeed, in 2015 Iceland real wages were still below where they were in 2005, ten years earlier, while real wages in the ‘distressed’ EMU states of Ireland and Portugal have recovered.

60

70

80

90

100

110

120

130

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Real wage per employee (euro terms; indexed 2005=100)

Greece Iceland Ireland Portugal

Source: AMECO

Iceland’s rate of profit plummeted from 2005 and eventually the island’s property boom burst and along with it the banks collapsed in 2008–09. Devaluation of the currency started in 2008, but profitability in 2012 remained well under the peak level of 2004. Profitability of capital in Iceland has now recovered but EMU distressed ‘austerity’ states, Portugal and Ireland, have done better and even Greek profitability has shown some revival.

80

90

100

110

120

130

140

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Greece Iceland Ireland Portugal

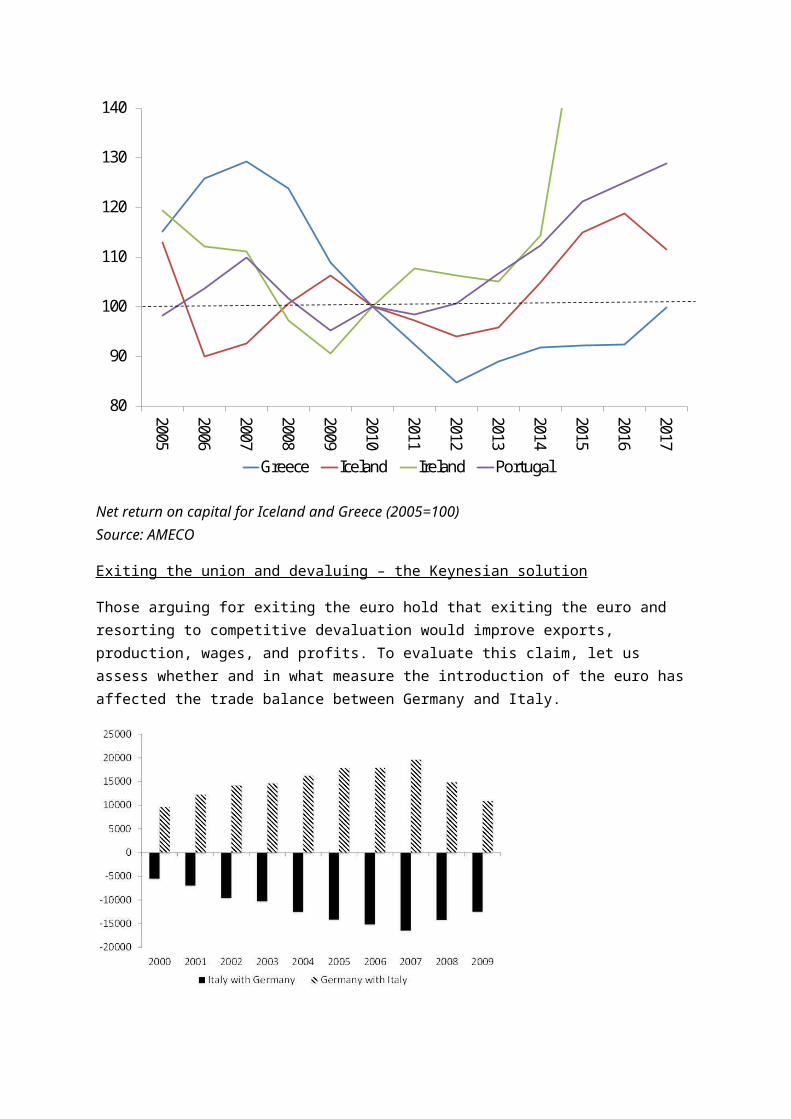

Net return on capital for Iceland and Greece (2005=100)Source: AMECO

Exiting the union and devaluing – the Keynesian solution

Those arguing for exiting the euro hold that exiting the euro and resorting to competitive devaluation would improve exports, production, wages, and profits. To evaluate this claim, let us assess whether and in what measure the introduction of the euro has affected the trade balance between Germany and Italy.

Germany-Italy trade balance (€m)

It is mistaken to ascribe Italy’s negative trade balance to the euro. The cause of Italy’s negative performance is its backward technological base relative to Germany’s. 7

As argued above, Marx’s theory of production prices holds that when two commodities are exchanged at their production price (after the equalization of the profit rates), the manufacturer of the commodity produced with a lower organic composition (OCC) loses value to the manufacturer of the commodity produced with a higher organic composition of capital. The focus here is on exchange within the same national economy and using the same currency.

But this theory can be applied to the international economy and to different currencies as mediums of payment. Given the formation of international production prices, if two commodities are exchanged at their production price, one produced in a country by a capital with a lower OCC (Italy) and the other produced in another country by a capital with a higher OCC (Germany), that exchange implies a loss of value by Italy to Germany.

Now suppose Italy exits the euro and reverts to the lira while Germany keeps the euro. Under the assumption that there are international production prices, if Italy produces with a lower OCC than that used by the German producer, there is a loss of value from the Italian to the German producer. Yes, there is equilibrium in the two countries’ balance of payments. But behind it, there is the Italian exporter’s loss of value and its appropriation by the German importer. Therefore, there is a fall in Italy’s profitability and a rise in that of Germany. A balanced trade hides a worsening of the technologically weaker country’s profitability.

Now if Italy devalues its currency by half, the German importer can buy twice as much of Italy’s exports but the Italian importers can still only buy the same amount of German exports. In short, the Italian producer loses value, which is appropriated by Germany’s importing capital. In terms of use values, there is lost consumption or investment in Italy. In terms of value, Italy’s rate of profit falls.

It falls not only by the surplus value contained in that commodity, but by its whole value. The loss of value inherent in competitive devaluation is thus greater than that inherent in the formation of (international) production prices because what is lost is the whole of surplus value plus constant and variable capital. Sure, in lira terms, there is no loss of profit, but in international production value terms, there is a loss. The fall in the value rate of profit is hidden by the improvement in the money rate of profit.

However, this is a static analysis. The Keynesian reply would be that Italy’s output would increase because of foreign demand. This would lead to higher consumption and investment. The Keynesian multiplier is set in motion. In reality, however, even if nominal wages and employment might increase, real wages (in terms of the consumption goods available on the domestic market) will fall – see Iceland above.

What jump-starts the economy is not only greater production, investment, and consumption but also and chiefly, a higher average profitability. And this depends on what has been called the Marxist multiplier, i.e. on whether at the end of the chain of the demand-induced investments, the average OCC has risen or fallen. Extra investment or consumption is likely to go to those to producers with lower prices and they must those who use new techniques with higher OCC. So the most likely

outcome is a fall in the average rate of profit. In the figure below, there is a high correlation between changes in the average profitability of capital in each economy and real GDP – evidence of the Marxist multiplier at work.

-25.0

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

-10.0 -5.0 0.0 5.0 10.0 15.0 20.0 25.0 30.0 35.0

% change in net return on capital 2010-15

% change in real GDP 2010-15

Correlations: G6 0.74 GIPS 0.86 ALL 0.48

Source: AMECO, author

In sum, if Italy devalues its currency, its exporters may improve their sales and their money rate of profit. Overall employment and investments might also improve for a while. But there is a loss of value inherent in competitive devaluation. Inflation of imported consumption will lead to a fall in real wages. And the average rate of profit will eventually worsen with the concomitant danger of a domestic crisis in investment and production. Such are the consequences of competitive devaluation.

The outcome could be different when the currency is controlled and owned by one country. Valle8 finds that, in the case of the US, can borrow indefinitely and thus raise the mass and rate of profit. But as Valle says, “this seems to give a new meaning to the Kaleckian statement that capitalists earn what they spend, except that it is a profit that they will have to return in the future.”

Brexit and EMU

The UK’s plan to leave the EU raises all these issues. The UK government imagines that it can negotiate a trade pact with the EU and then establish trade deals unilaterally with other major economies. It also imagines that it can turn its sizeable trade deficit into surplus by these deals and by devaluing when necessary.

But devaluation only really affects demand. The other side of the equation is supply and productive capacity. Devaluation doesn’t necessarily do anything to promote investment and higher productivity. Some even argue that devaluation can reduce the incentive to be efficient because you become competitive without the effort of increasing productivity. What really matters is what is going to happen to business investment and profitability.

And here the prospect of Brexit is already been damaging to British capital.

Higher production costs from imports, weaker demand at home and abroad are likely to discourage UK companies from investing at home and foreign investors from stepping in. And overall profitability of UK companies is still below the peak of 1997, while profitability in the key manufacturing sector for exports was half that of 1997.

The UK is likely to suffer a relative decline compared to other European capitals for some time after it leaves in March 2019, even with the so-called transition period up to 2022 in place.

Will the euro survive?

There are two ways a capitalist economy can get out of slump. The first is by raising the rate of exploitation of the workforce enough to drive up profits and renew investment. The second is to liquidate weak and unprofitable capital (i.e. companies) or write off old machinery, equipment, and plant from company books (i.e. devalue the stock of capital). Capitalists attempt to do both in order to restore profits and profitability after a slump.

This is taking a long time in the current crisis since the bottom of the Great Recession in mid-2009. Progress in raising the rate of exploitation has been considerable. But progress in devaluing and deleveraging the stock of capital and debt built up before is slow and even being postponed by easy monetary policy.

Ultimately, whether the euro will survive is a political issue, depending on the majority view of the strategists of capital in the stronger economies and on the balance of class forces within the Eurozone. Will the people of Greece, Portugal, Spain, Italy, Cyprus, Slovenia, and Ireland endure more years of austerity, creating a whole ‘lost generation’ of unemployed young people, as has already happened in Greece and will happen in Spain, Italy, Portugal, and Slovenia?

Or will the electorate lose patience and remove pro-austerity, pro-Euro governments as in Greece (only to be disappointed)? The EU leaders and strategists of capital need economic growth to return soon or further political explosions are likely. But, given the current level of profitability, it may take too long before, perhaps, the world economy drops into another slump. Then all bets are off on the survival of the euro.

1 Frankel, J. A. and Rose, A. K. (1998), The Endogenity of the Optimum Currency Area Criteria. The Economic Journal, 108: 1009–1025. doi:10.1111/1468-0297.003272 Bayoumia T,Eichengreen B, Ever closer to heaven? An optimum-currency-area index for European countries, European Economic Review Volume 41, Issues 3–5, April 1997, Pages 761-770

3 Mundell, RA. "A Theory of Optimum Currency Areas." The American Economic Review 51, no. 4 (1961): 657-65. http://www.jstor.org/stable/1812792.4 Krugman P, NBER Macroeconomics Annual 2013 27:1, 439-448

5 De Grauwe P, Economics of Monetary Union (2016)

6 Corsetti, Dedola, Jarociński, Bartosz Mackowiak, Schmidt. Business cycle stabilisation in the Eurozone: Ways forward, 23 October 2017

7 Carchedi G, From the crisis in surplus value to the crisis in the euro, in World in Crisis, ed Carchedi and Roberts, (2018 forthcoming).

8 Valle Baeza, Mendieta Munoz, Profit and Trade Deficit in the U. S. Economy - A Marxist perspective, Marxism 21