{ working for you } 601 gateway blvd., ste. 1140 so. san francisco, ca 94080 (415) 901-4000 ...

TRANSCRIPT

{ working for you }

601 Gateway Blvd., Ste. 1140So. San Francisco, CA 94080

(415) 901-4000

www.blueprintventures.com

CONFIDENTIAL 04/15/05

Venture Capital and IPVenture Capital and IP

Jim Huston Jim Huston Blueprint VenturesBlueprint Ventures

CONFIDENTIAL 22

{ working for you }

AgendaAgenda

Intro to Blueprint Ventures

Venture Capital

IP Overview

CONFIDENTIAL 33

{ working for you }

Blueprint VenturesBlueprint Ventures

Focus - Seed and early-stage IT infrastructure

Differentiated Investment Strategy– Capital efficiency

– Corporate IP (intellectual property) spinouts

– One foot in Silicon Valley, one foot in Oregon

Experienced investment team– Average of 15 years of operating experience, 7 years of

venture investing experience

CONFIDENTIAL 44

{ working for you }

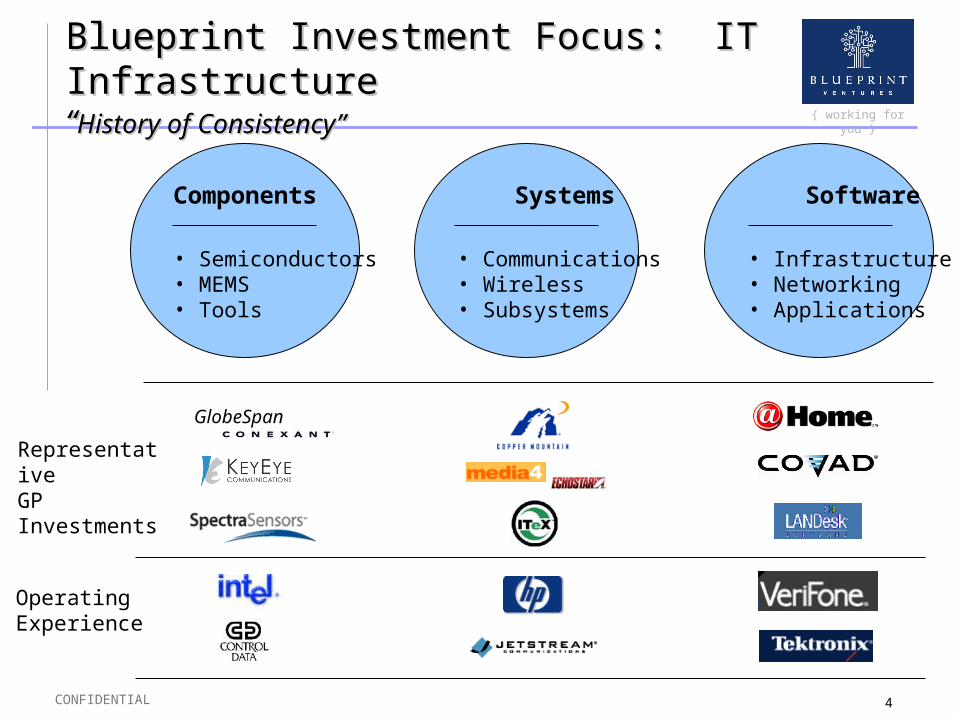

Blueprint Investment Focus: IT InfrastructureBlueprint Investment Focus: IT Infrastructure““History of Consistency”History of Consistency”

Components

• Semiconductors• MEMS• Tools

Systems

• Communications• Wireless• Subsystems

Software

• Infrastructure• Networking• Applications

RepresentativeGPInvestments

Operating Experience

GlobeSpan

CONFIDENTIAL 55

{ working for you }

Blueprint Portfolio by Sector and StageBlueprint Portfolio by Sector and Stage

Software

Systems

Components

Product Development Customer Adoption Revenue Growth

CONFIDENTIAL 66

{ working for you }

AgendaAgenda

Intro to Blueprint Ventures

Venture Capital

IP Overview

CONFIDENTIAL 77

{ working for you }

Raising MoneyRaising Money

Start-up CEO really only has 1 job – get money

– Investors and lenders

– Customers

Sources of Non-revenue Money

– Credit cards and 2nd mortgages

– Friends and family

– Government research grants

– Licenses / NRE from corporate “partners”

– “Angels”

– Banks

– VCs

CONFIDENTIAL 88

{ working for you }

About VCsAbout VCs

They have a fiduciary responsibility to their limited partners – expectations of 30-40% compound annual returns

Long term horizon – historical average is 7 years from company creation to exit, and must pass through “J curve”

Returns driven by a few “home runs” – OK if most investments fail, but they need 10-20% to return 10X and 20-30% to return 3-4X

And … They are herd animals …

CONFIDENTIAL 99

{ working for you }

CONFIDENTIAL 1010

{ working for you }

Some Data on Venture Investing …Some Data on Venture Investing …

1111

{ working for you }

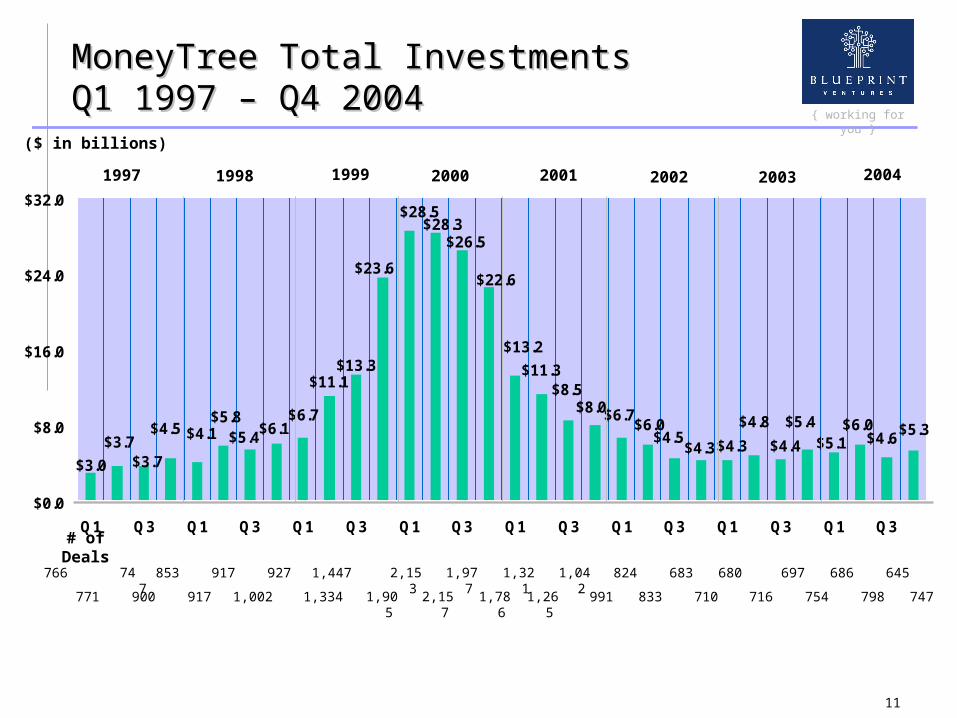

MoneyTree Total InvestmentsMoneyTree Total InvestmentsQ1 1997 – Q4 2004Q1 1997 – Q4 2004

$4.6$4.8

$4.3$4.3

$8.0$8.5

$11.3

$13.2

$22.6

$3.0

$3.7$3.7

$4.5 $4.1$5.8

$5.4$6.1

$6.7

$11.1$13.3

$23.6

$28.5$28.3

$26.5

$6.7$6.0

$4.5$4.4

$5.4 $6.0$5.1

$5.3

$0.0

$8.0

$16.0

$24.0

$32.0

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3

($ in billions)

1997 1998 1999 2000 2001

# of Deals

2002 2003 2004

1,334 1,905

2,157

1,786

1,265

991 833 710 716 754 798 7471,002917900771

927 1,447 2,153

1,977

1,321

1,042

824 683 680 697 686 645917853766 747

1212

{ working for you }

Investments by Industry - Investments by Industry - Annual Percent of Total U.S. InvestmentsAnnual Percent of Total U.S. Investments

(% of Total Dollars)

21.9%

4.0%

16.6%

2.4%3.2%

24.2%

7.9%

14.3%

5.0% 4.7%

23.3%

14.3%

11.7%

8.6%

5.8%

18.6%

10.1%

8.3%7.0%

24.1%

8.9% 8.7%7.8%

22.5%

18.3%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Software Biotechnology Telecommunications Medical Devices andEquipment

Semiconductors

2000 2001 2002 2003 2004

Top 5 Industries – 2000 to 2004

CONFIDENTIAL 1313

{ working for you }

First Round Deals in Startup & Early First Round Deals in Startup & Early Stage CompaniesStage Companies

542

726806

950

1,758

594 546 608

2,479

889

35% 35%

32% 32%

23%

39%39%

25%

23%23%

0

500

1,000

1,500

2,000

2,500

3,000

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

# First Sequence Deals in Startup & Early Stage Companies % of All Investee Companies

CONFIDENTIAL 1414

{ working for you }

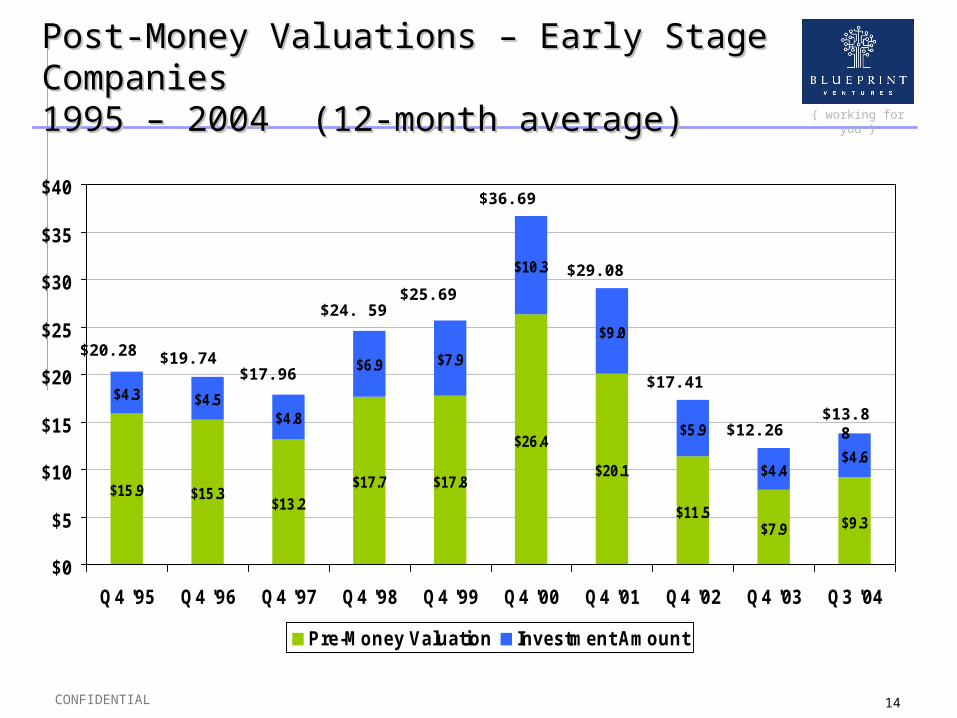

Post-Money Valuations – Early Stage CompaniesPost-Money Valuations – Early Stage Companies1995 – 2004 (12-month average)1995 – 2004 (12-month average)

$15.9 $15.3$13.2

$17.7 $17.8

$26.4

$20.1

$11.5$7.9 $9.3

$4.5$4.8

$6.9 $7.9

$10.3

$9.0

$5.9

$4.4$4.6

$4.3

$0

$5

$10

$15

$20

$25

$30

$35

$40

Q4 '95 Q4 '96 Q4 '97 Q4 '98 Q4 '99 Q4 '00 Q4 '01 Q4 '02 Q4 '03 Q3 '04

Pre-Money Valuation Investment Amount

$20.28 $19.74

$24. 59

$17.96

$25.69

$36.69

$29.08

$17.41

$13.88$12.26

CONFIDENTIAL 1515

{ working for you }

Post-Money Valuations – Later Stage CompaniesPost-Money Valuations – Later Stage Companies1995 – 2004 (12-month average)1995 – 2004 (12-month average)

$43.4 $36.8

$61.8 $54.3

$104.4

$129.0

$77.4

$48.4 $54.3 $54.0

$8.0$8.0

$9.8$11.6

$20.0

$28.4

$19.5

$15.9$13.4 $16.2

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

Q4 '95 Q4 '96 Q4 '97 Q4 '98 Q4 '99 Q4 '00 Q4 '01 Q4 '02 Q4 '03 Q3 '04

Pre-Money Valuation Investment Amount

$51.35$44.81

$65.91$71.68

$124.37

$157.43

$96.86

$67.73 $70.23$64.25

CONFIDENTIAL 1616

{ working for you }

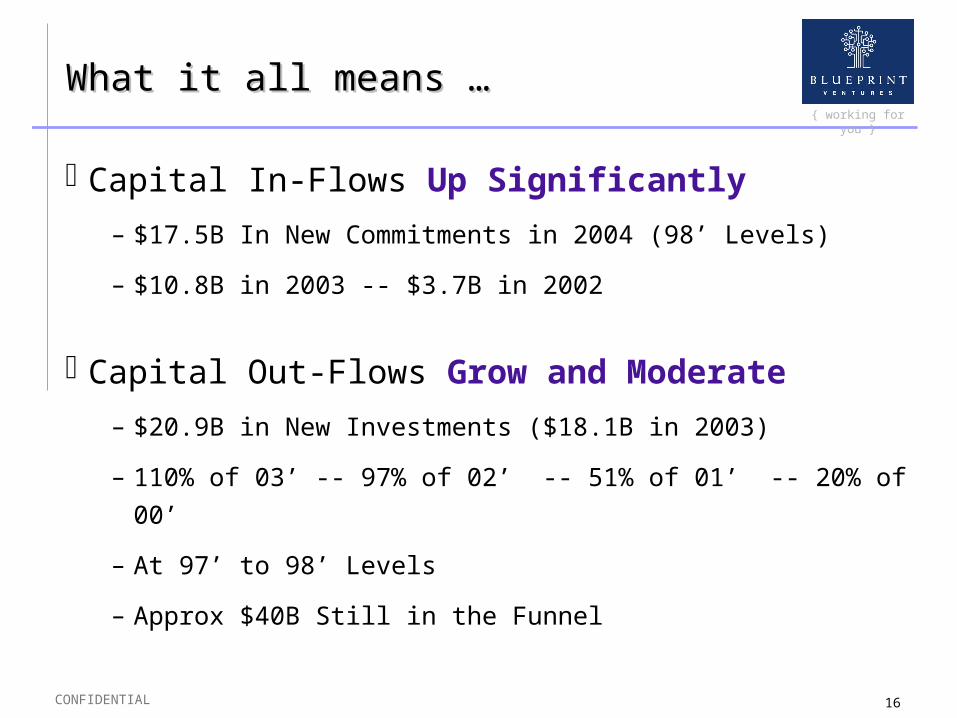

What it all means …What it all means …

Capital In-Flows Up Significantly

– $17.5B In New Commitments in 2004 (98’ Levels)

– $10.8B in 2003 -- $3.7B in 2002

Capital Out-Flows Grow and Moderate

– $20.9B in New Investments ($18.1B in 2003)

– 110% of 03’ -- 97% of 02’ -- 51% of 01’ -- 20% of 00’

– At 97’ to 98’ Levels

– Approx $40B Still in the Funnel

CONFIDENTIAL 1717

{ working for you }

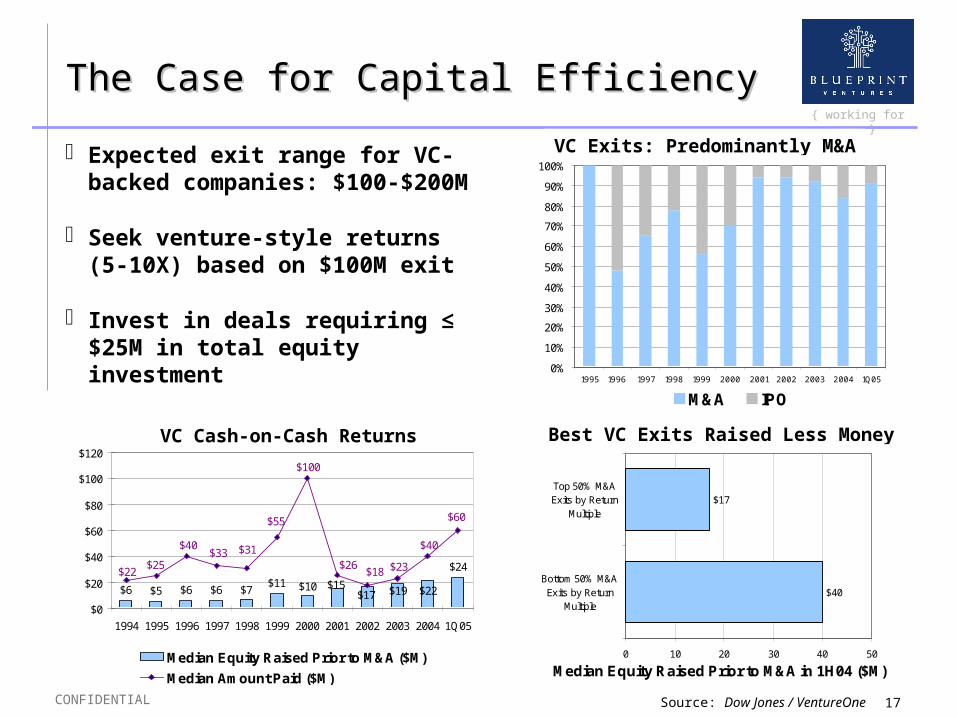

The Case for Capital EfficiencyThe Case for Capital Efficiency

VC Exits: Predominantly M&A

Source: Dow Jones / VentureOne

Best VC Exits Raised Less Money

Expected exit range for VC-backed companies: $100-$200M

Seek venture-style returns (5-10X) based on $100M exit

Invest in deals requiring ≤ $25M in total equity investment

$40

$17

0 10 20 30 40 50

Bottom 50% M&AExits by Return

Multiple

Top 50% M&AExits by Return

Multiple

Median Equity Raised Prior to M&A in 1H04 ($M)

VC Cash-on-Cash Returns Squeezed

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 1Q05

M&A IPO

$6 $5 $6 $6$11

$24

$7 $10$17 $19 $22$15

$60

$18 $23$26

$40

$22$25

$40$33 $31

$55

$100

$0

$20

$40

$60

$80

$100

$120

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 1Q05

Median Equity Raised Prior to M&A ($M)

Median Amount Paid ($M)

CONFIDENTIAL 1818

{ working for you }

Successful Exits Remain ConstrainedSuccessful Exits Remain Constrained

Date Company Name $ Invested M&A Price

2/04 RAIDCore $5M $16.5M

4/04 Widcomm $58M $49M

4/04 Sand Video $9M $77.5M

6/04 M-Stream $1.5M $10M

9/04 AlphaMosaic $30M $123M

3/05 Zeevo $89M $32M

MEDIAN $20M $41M

Date Company Name $ Invested

M&A Price

1/03 Okena $16.7M $154M

11/03 Latitude Comm. $18.5M $80M

3/04 Riverhead Networks $14.8M $39M

6/04 Actona Technologies $25M $82M

6/04 Procket Networks $272M $89M

7/04 Parc Technologies $26.5M $9M

8/04 P-Cube $70.2M $200M

9/04 DynamicSoft $74.5M $55M

10/04 Perfigo $2.8M $74M

12/04 Protego Networks $6.3M $65M

1/05 Airespace $58M $450M

4/05 Topspin $68M $250M

MEDIAN $25.8M $81M

Source: Blueprint research, VentureSource, Capital IQ(only includes transactions where acquisition price was disclosed)

Date Company Name $ Invested M&A Price

4/03 BoldFish $18.3M $5M

10/03 UpShot $76M $55.4M

1/04 Ineto Services $42M $4.8M

4/04 Eontec $35.4M $70M

12/04 eDocs $85M $115M

MEDIAN $42M $55.4M

Venture-Backed High-Tech Acquisitions, 1/2003—4/2005

CONFIDENTIAL 1919

{ working for you }

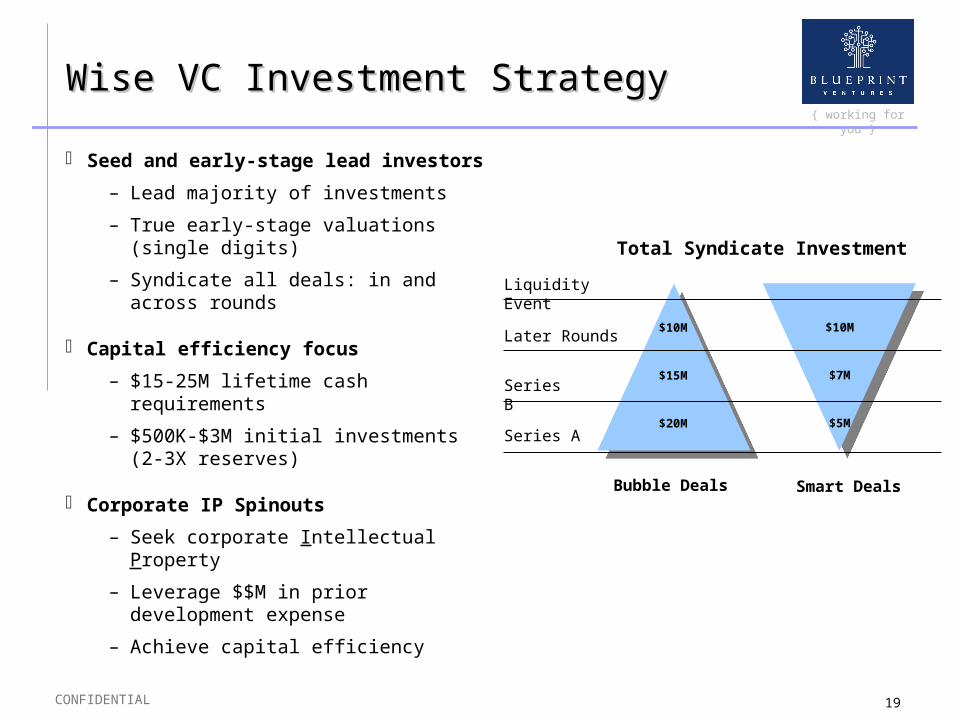

Wise VC Investment StrategyWise VC Investment Strategy

Seed and early-stage lead investors

– Lead majority of investments

– True early-stage valuations (single digits)

– Syndicate all deals: in and across rounds

Capital efficiency focus

– $15-25M lifetime cash requirements

– $500K-$3M initial investments (2-3X reserves)

Corporate IP Spinouts

– Seek corporate Intellectual Property

– Leverage $$M in prior development expense

– Achieve capital efficiency

Liquidity Event

Series A

Series B

Later Rounds$10M

$15M

$20M

Bubble Deals Smart Deals

Total Syndicate Investment

$10M

$7M

$5M

CONFIDENTIAL 2020

{ working for you }

Lessons Blueprint Has LearnedLessons Blueprint Has Learned

Capital efficiency– Small A rounds ($ and

valuation)

– Follow winners

Like-minded co-investors

Activist mentality– CEO replacement

– Cash management

– Corporate governance

Exit focus

Average Initial RoundInvestment Amount ($M)

Average Blueprint Initial RoundPre-Money Valuation ($M)

CONFIDENTIAL 2121

{ working for you }

VC SummaryVC Summary

2004 – The Fundamentals “Restored”– Capital Flows into VC Fund approaching $20B

– VC Investments stabilize around $20B

– IPO Window and Increased M & A activity renews cycle of positive returns

The Venture Community– Consolidation continues – still adopting to the new

“Reality”

– Venture Firms still at the low-end of the historical “experience curve”

– Syndication – rediscovery of the lost art

CONFIDENTIAL 2222

{ working for you }

AgendaAgenda

Intro to Blueprint Ventures

Venture Capital

IP Overview

CONFIDENTIAL 2323

{ working for you }

Intellectual Property RightsIntellectual Property Rights

Patents

– Protect against unauthorized use of invention

Trade Secrets

– Protect against unauthorized disclosure of confidential information

Copyright

– Protect against unauthorized copying of expression of idea

Trademark

– Protect against unauthorized use of logo or other product identifier

What is Technology?

– Technology is the “thing” itself

CONFIDENTIAL 2424

{ working for you }

Trade SecretsTrade Secrets

If it’s really important to keep secret, don’t tell anyone!

State law rather than Federal

Can be very effective:

– No expiration date

– No need to ever disclose your secrets

But …

– Knowledge workers are mobile

– If not properly protected, all rights can be gone

– Does not protect against reverse engineering or independent development

CONFIDENTIAL 2525

{ working for you }

CopyrightsCopyrights

Protects works of authorship (software, documentation etc....)

Protects the expression, not the idea

Exclusive rights of copyright owner:– Reproduce, Prepare Derivative Works, Perform, Display,

Distribute

CONFIDENTIAL 2626

{ working for you }

Some Software Licensing BasicsSome Software Licensing BasicsBuyer / Seller ContrastsBuyer / Seller Contrasts

Buyer Term - Perpetual

New Releases

Source Code

Right to Modify

Licensee owns derivatives

No Use Restrictions

Licensor cannot cancel for convenience,

Royalty Cap (dollar, time based, annual cap, buyout)

Seller Short Term - 1-3 years

Maintenance Releases Only

Object Only

No Right to Modify

Licensor owns derivatives

Narrow Use Restrictions

Licensor can cancel for convenience

No Royalty Cap or Buyout

CONFIDENTIAL 2727

{ working for you }

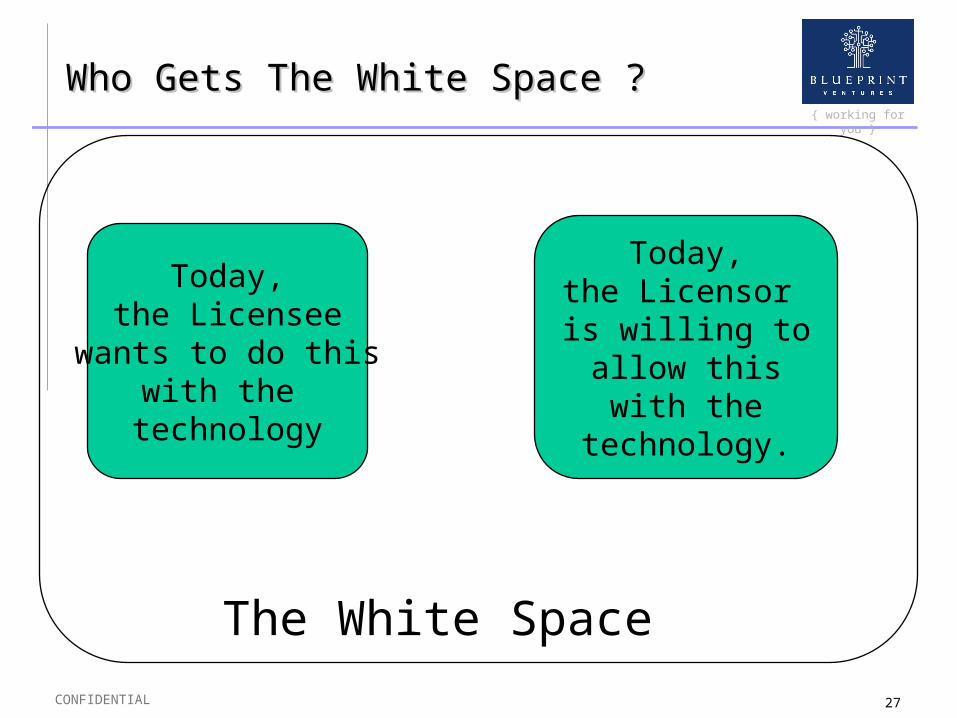

Who Gets The White Space ?Who Gets The White Space ?

Today,the Licensor is willing toallow thiswith the

technology.

Today,the Licensee

wants to do thiswith the

technology

The White Space

CONFIDENTIAL 2828

{ working for you }

Who Gets the White Space ?Who Gets the White Space ?

Use Restrictions– You can do only this, or

– You can do anything except this

Ownership of derivatives

Ownership of the White Space is important because you always end up in it !

CONFIDENTIAL 2929

{ working for you }

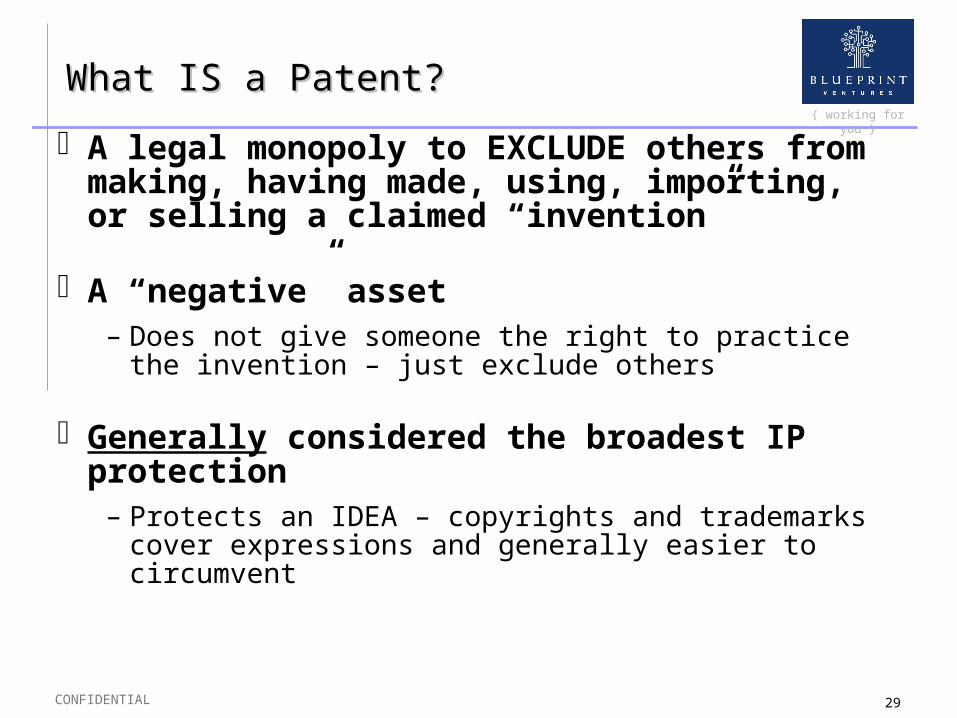

What IS a Patent?What IS a Patent?

A legal monopoly to EXCLUDE others from making, having made, using, importing, or selling a claimed “invention”

A “negative” asset– Does not give someone the right to practice the

invention – just exclude others

Generally considered the broadest IP protection

– Protects an IDEA – copyrights and trademarks cover expressions and generally easier to circumvent

CONFIDENTIAL 3030

{ working for you }

Basic Patent StructureBasic Patent Structure

Cover page – Abstract, Prior Art, Assignee, Inventor, File Date, Issue Date

Description of an invention and how to make and/or use it

– Drawings and Specifications

Claims – the “metes and bounds” of a protectable invention

The real value of a patent is in the claims

CONFIDENTIAL 3131

{ working for you }

What is a “Good Patent”?What is a “Good Patent”?

Broad claims

Easy to detect

Hard to design around or design out

Evidence of usage – standards, competitors, other “parties of interest” (IF you want to assert these are good)

Clear title / ownership

Minimal encumbrances (licenses, CNTS, standards body affiliations, etc.)

Early filing dates

CONFIDENTIAL 3232

{ working for you }

Good Patents ≠ Good TechnologyGood Patents ≠ Good Technology

Common Complaint: “The technology is fantastic – what do you mean the patents are worthless?”

Explanation: Claim Coverage is weak

Patents typically a feature – not the product

CONFIDENTIAL 3333

{ working for you }

Most patents are worthless …Most patents are worthless …

Study of 741 licensed patents from 6 universities (AUTM, 2001) – Lifetime royalties:

– 50% less than $10K lifetime

– 71% less than $50K lifetime

– 83% less than $100K lifetime

– Only 1.5% over $1 million

10% of US/German patents accounted for ~90% of value Scherer, Harhoff, Kukies, 1998

5% of electronics patents accounted for 55% of value Schankerman, 1998

CONFIDENTIAL 3434

{ working for you }

Value of a Patent to a Start-upValue of a Patent to a Start-up

Protects their invention … maybe

A fund raising tool … maybe

A marketing tool … maybe

A recruiting tool … maybe

Why all the “Maybes”?

CONFIDENTIAL 3535

{ working for you }

Costs of Patents to a Start-upCosts of Patents to a Start-up Expensive

– ~$15-50k per patent in US

– Perhaps 3-5x that for foreigns

Time consuming

Many start-ups only patent narrow claims – which typically result in worthless patents

Unless you intend to USE (assert) them, they may be worthless

Discloses your secrets

Good VCs now more savvy – Patent counts not an IPO ticket

CONFIDENTIAL 3636

{ working for you }

Patent Licenses & StrategiesPatent Licenses & Strategies

“Carrot” licensing – Offers value added business case to licensee

“Stick” licensing – Offers the opportunity to stop infringing and incurring further damages. Also known as “the tax man” approach.

Different industries / companies have different patent strategies. E.g. Semiconductors:– Micron / AMD – Patents as a marketing tool

– IBM / TI – Multi $B patent license program

– Intel – Patent cross licenses; primarily “freedom to operate”

– Many consumer electronics companies – Patent pools

– Qualcomm – Patents used to drive standards (e.g. CDMA)

– Rambus / Immersion – IP shops (aka Patent “trolls”)

CONFIDENTIAL 3737

{ working for you }

APPENDIX

CONFIDENTIAL 3838

{ working for you }

Effect of Participating PreferredEffect of Participating Preferred

Example 1– Assumptions

o VC invests $5M at a $50M post-money valuationo The Company is later sold for $60M casho VC is the only investor

– ResultsTotal proceeds $60.0M $60.0MLess: Participation $5.0M $0.0MNet to common $55.0M $60.0MVCs common ownership 10.0% 10.0%Proceeds from common $5.5M $6.0MTotal Proceeds to VC $10.5M $6.0M% of Proceeds 17.5% 10.0%

With Without

CONFIDENTIAL 3939

{ working for you }

Effect of Participating PreferredEffect of Participating Preferred

With Without

Example 2– Assumptions

o VC invests $5M at a $50M post-money valuationo The Company is later sold for $10M casho VC is the only investor

– ResultsTotal proceeds $10.0M $10.0MLess: Participation $5.0M $0.0MNet to common $5.0M $10.0MVC common ownership 10.0% 10.0%Proceeds from common $0.5M $1.0MTotal Proceeds to VC $5.5M $1.0M% of Proceeds 55.0% 10.0%

CONFIDENTIAL 4040

{ working for you }

““Typical” Cap StructureTypical” Cap Structure

Company Common Options Warrants Series A Series B Total Shares F/D OwnershipShare Price $0.20 $0.50 $2.25Employees 500,000 4,000,000 4,500,000 17.6%

Unexercized Options 2,500,000 2,500,000 9.8%Exercized Options 500,000 500,000 2.0%Options Available for Grant 1,500,000 1,500,000 5.9%

Founders 5,000,000 1,000,000 6,000,000 23.5%Angels 500,000 25,000 525,000 2.1%VC 1 - Series A Lead 500,000 5,000,000 2,000,000 7,500,000 29.4%VC 2 2,000,000 1,000,000 3,000,000 11.8%VC 3 - Series B Lead 4,000,000 4,000,000 15.7%Total Shares 6,000,000 5,000,000 500,000 7,025,000 7,000,000 25,525,000 100.0%

Invested Dollars $100,000 $3,512,500 $15,750,000

Post Money Valuation $9,262,500 $57,431,250

• Company raises angel round and 2 rounds of VC money