0001546341 523.finance.wharton.upenn.edu/~itayg/files/financialcrises...diamond–dybvig model, the...

TRANSCRIPT

C H A P T E R

36

Empirical Literature on Financial Crises:Fundamentals vs. Panic

I. GoldsteinUniversity of Pennsylvania, Philadelphia, PA, USA

O U T L I N E

Introduction 523

Empirical Evidence on the Role of Fundamentals 524Banking Crises 524Currency Crises and Twin Crises 526Contagion 526

What do we Learn from the Evidence about the Roleof Panic? 527

How can we Test for Panic? 529

Conclusion 532Acknowledgments 533Glossary 533References 533

INTRODUCTION

The process of financial globalization has given rise toan increase in the frequency of financial crises.1 With it,there has also been a surge in research about financialcrises. One of the key questions in this area is whethercrises are triggered by fundamentals or come as a resultof panic. Observing real-world events, many prominentresearchers, including Friedman and Schwartz (1963)and Kindleberger (1978), concluded that financial crisesare so strong and sudden that there must be an elementof panic in them. Yet, a large empirical literature(reviewed in the next section) has been able to establisha fairly strong link between crises and fundamentals.

Theoretically, the panic-based approach to bankingcrises was formalized by Bryant (1980) and DiamondandDybvig (1983). In theDiamond–Dybvigmodel,wheninvestors withdrawmoney from a bank, they deplete thebank’s capital, reducing the amount available for inves-tors who come in the future. This creates strategic

complementarities, such that investorswish towithdrawwhen they think others will do so. The result is multiplic-ity of equilibria. There is an equilibrium in which all theinvestors withdraw and an equilibrium in which noneof them does. Crises are then self-fulfilling; they occuronly because investors believe they will occur. In theDiamond–Dybvig model, the occurrence of a crisis can-not be linked to fundamentals. The fundamental-based(or information-based) approach has been modeled aswell, for example, in Chari and Jagannathan (1988),Jacklin and Bhattacharya (1988), and Allen and Gale(1998). The basic idea is simple. Bad fundamentals (ornegative information about fundamentals) lead banks’balance sheets to deteriorate, inducing investors to run.2

The tension between the self-fulfilling approach andthe fundamental approach to crises exists also in thecurrency-attack literature. The two classic approachesare presented by Krugman (1979) and Obstfeld (1996).According to Krugman (1979), the crisis is an inevitableresult of a government that runs a fiscal policy which is

1 In this chapter, financial crises include banking crises and currency crises. For evidence, see Bordo et al. (2001).2 The issues get more complicated in the information-based approach when there is asymmetric information, leading to learning,

herding, etc.

523The Evidence and Impact of Financial Globalization

http://dx.doi.org/10.1016/B978-0-12-397874-5.00038-5

# 2013 Elsevier Inc. All rights reserved.

inconsistent with the exchange rate regime, and hencethe currency collapse is predictable by fundamentals.On the other hand, in Obstfeld (1996), the currencycollapse might be self-fulfilling. If enough speculatorschoose to attack the currency, they will weaken the abil-ity of the government tomaintain the fixed exchange rateregime, leading to the collapse of the currency. Krugmanhimself later admitted that the fundamental approach isunable to explain the Asian crisis of the late 1990s, and inKrugman (1999), he proposed a model that is based onself-fulfilling beliefs and multiple equilibria.3

Differentiatingbetweenpanic-basedand fundamental-based crises is crucial for policy purposes. Many of thepolicies adopted against financial crises – such as depositinsurance, lender of last resort, and suspension ofconvertibility – are predicated on the idea that crises arepanic-based and result from a coordination failure.4

Hence, it isnotsurprising thatmanyempiricalpapershavetried to distinguish the two types of crises in the data.

The Section ‘Empirical Evidence on the Role ofFundamentals’ of this chapter reviews some of the em-pirical papers on financial crises and their conclusionon whether crises result from fundamentals or panic.The traditional view in this literature is that the panicapproach does not generate any testable implications(see Gorton, 1988). Hence, the focus has been on investi-gating whether crises can be linked to fundamentals. In-deed, by and large, the literature has found a strong linkbetween crises and fundamentals, and this was usuallyinterpreted as evidence in support of the fundamental-based approach and against the panic-based approach.

The Section ‘What Do We Learn from the Evidenceabout the Role of Panic?’ argues that, while the evidencecertainly speaks of the importance of fundamentals, itdoes not saymuch about the panic-based approach. Evenif crises are linked to fundamentals, it can still be the casethat they would not have occurred without coordinationfailures or self-fulfilling beliefs. That is, it is possible thatagents’ self-fulfilling beliefs about crises are triggered bylow fundamentals, and so the fundamentals are linked tocrises indirectly via the effect on coordinationpatterns. Inthis case, the panic amplifies the response to fundamen-tals and generates crises in levels of fundamentals thatcould support a different outcome. Indeed, the global-games approach – pioneered by Carlsson and vanDamme (1993) and then extended and applied to studyfinancial crises by Morris and Shin (1998), GoldsteinandPauzner (2005), and others – illustrates this idea. Thissection describes the paradigm and demonstrates that itgenerates self-fulfilling (or panic-based) crises that can belinked to fundamentals.

The Section ‘How Can We Test for Panic?’ askswhether there is a way to validate the panic-basedapproach in the data: can we identify that investors dosomething just because they believe others are doingthe same? This is clearly a difficult problem, as, in a non-experimental environment, running a regression of thebehavior of some people on the behavior of others iseconometrically invalid, as it suffers from the reflectionproblem (Manski (1993)). This section describes two re-cent papers that make progress in this direction.Hertzberg et al. (2010) provide evidence on peer effectsin lending by using a natural experiment in Argentinathat enables them to identify the effect of one bank’sexpected lending decision on other banks’ lending deci-sions. Chen et al. (2010) provide evidence on peer effectsin redemptions among US mutual fund investors byshowing the difference in behavior between funds thatexhibit strong complementarities and funds that exhibitweak complementarities. Going forward, the challengeis to identify panic or self-fulfilling beliefs in the ‘classic’crises datasets reviewed in the section ‘EmpiricalEvidence on the Role of Fundamentals.’

EMPIRICAL EVIDENCE ON THE ROLE OFFUNDAMENTALS

The empirical literature on banking crises and cur-rency crises has produced large evidence identifyingfundamental variables that either determine or providea warning sign for the occurrence of an upcoming crisis.This section reviews the main themes coming out of thisliterature. Note that this review is not meant to cover thewhole literature, but rather to draw some of the mainlessons.

Banking Crises

A classic reference in the empirical banking crises lit-erature is Gorton (1988). He provides one of the first setsof evidence linking crises to fundamentals. Studying thenational banking era in the United States between 1863and 1914, he shows that crises were responses of depos-itors to an increase in perceived risk. He demonstratesthat crises occurred whenever key variables that arelinked to the probability of recession reached a criticalvalue. The most important variable is the liabilities offailed firms. He also shows an effect of other variables,such as the production of pig iron, which he uses asa proxy for consumption. When the perceived risk ofrecession based on these variables becomes high,

3 An interesting quote from Krugman (1999) is “I was wrong; Maury Obstfeld was right.”4 See Diamond and Dybvig (1983) and Rochet and Vives (2004).

524 36. EMPIRICAL LITERATURE ON FINANCIAL CRISES: FUNDAMENTALS VS. PANIC

V. CRISES

depositors believe that their deposits in banks – whichhave claims in firms – become too risky, and hence theydemand earlywithdrawal, leading, in aggregate, tomasswithdrawals.

While Gorton’s study focuses on crises in the UnitedStates in the nineteenth and early twentieth centuries,other papers conducted international studies trying tounderstand what brings down a whole banking sector.A banking crisis in this literature is manifested by largewithdrawals out of the banking system, leading to bankclosures, government help to banks, or suspension ofconvertibility. A leading paper is Demirguc-Kunt andDetragiache (1998). They conducted an internationalstudy to understand the determinants of banking crisesin a sample of developing and developed economies inlate twentieth century (1980–1994). They again foundthat a number of variables connected to the fundamentalstate of the economy are related to the occurrence ofcrises. The key predictors in their study are low GrossDomestic Product (GDP) growth (which reflects declin-ing economic activity that reduces the value of banks’ as-sets), high real interest rates and inflation (which bothinduce banks to offer higher deposit rates, while the rateson their loans are fixed, given that they are mostly long-term loans), and a high level of outstanding credit(which obviously makes the banking system fragile).They use these results to conclude that crises cannotbe solely explained by self-fulfilling beliefs and that theyare connected to the state of the economy. They also findthat the institutional environment in a country has an ef-fect on the likelihood of a banking crisis. Surprisingly,the presence of deposit insurance is associated with anincrease in the likelihood of a banking crisis. While de-posit insurance should mitigate the concerns leadingto a panic-based crisis, it also exacerbates the moral haz-ard problem in the banking system. This latter effect ispotentially the explanation for this result.5 Other factorsare the quality of the legal system and the structure ofliabilities of the banking system.

While the aforementioned papers look at economy-wide variables, others have analyzed bank-specificvariables and their relation with the withdrawals fromspecific banks. One example is Schumacher (2000),who is also interested in distinguishing betweeninformation-based runs, and what she calls ‘randomruns.’ She conducts her study around the runs on Argen-tine banks following the devaluation of the Mexican cur-rency in December 1994. The devaluation in Mexico wasof significance to the Argentine banks because it led tospeculation that Argentina would also have to devalueits currency, and hence led depositors to rush to

withdraw their deposits denominated in the domesticcurrency. While this had started to happen, the runquickly spread to dollar-denominated deposits, suggest-ing that what was going on was more than just a run onthe currency, but a general concern about the strength ofthe financial system. Schumacher conjectures that de-positors’ runs were triggered by information they hadabout the ability of banks to survive the currency col-lapse, and that according to this information, they trans-ferred money from banks they considered ‘bad’ to banksthey considered ‘good.’ She finds evidence in support ofthis conjecture by showing that the depositors took theirmoney out of banks that were fundamentally weaker, assuch banks had less adequate capital, poorer perfor-mance, more nonperforming loans, and lower liquidity.

In similar spirit, Martinez-Peria and Schmukler (2001)analyze the behavior of depositors in Argentina, Chile,and Mexico over two decades in the late twentieth cen-tury, asking whether they provide market discipline bywithdrawing money and/or demanding high interestrate from risky banks. Indeed, they generally find thatdepositors’ behavior is affected by banks’ risk character-istics. Deposits decrease and interest rates rise in bankswith a low ratio of capital to assets, low return on assets,high level of nonperforming loans, and high ratio ofexpenditures to assets. Surprisingly, they find that theeffects are quite similar among insured and uninsureddepositors, suggesting lack of confidence among depos-itors in the deposit insurance schemes. They also findthat the effect of risk characteristics on depositors’ be-havior increases after banking crises.

Finally, Calomiris and Mason (2003) study bankingcrises during the great depression. As mentioned inthe introduction, the famous study by Friedman andSchwartz (1963) attributes these bank runs to panic be-cause theywere not precededby significant deteriorationin macroeconomic fundamentals. But, it is possible thatFriedman and Schwartz’s conclusion can be overturnedif one looks at regional or bank-specific variables asdeter-minants. That is, it does not have to be that macroeco-nomic weakness was at the root of the crisis, but rathermicroeconomic issues could be behind the failure of spe-cific banks. Indeed,Calomiris andMason findsupport forthe ‘fundamental’ view by showing that bank-specificvariables – such as leverage, asset risk, and liquidity –affect the likelihood of failure, and so do variables thatcapture the local or regional economic situation. At thesame time, they show that there is a significant residualleft when trying to explain crises. In their view, this canindicate that the model of fundamentals is incompleteor that there was some element of panic involved.

5 See also Demirguc-Kunt andDetragiache (2002), who develop this result further, and show, among other things, that the effect of deposit

insurance on the probability of banking crises increases when institutions are weak.

525EMPIRICAL EVIDENCE ON THE ROLE OF FUNDAMENTALS

V. CRISES

Currency Crises and Twin Crises

In parallel to the banking crises literature, a literaturehas been developed to understand the determinantsof currency crises. A currency crisis is marked by a specu-lative attack on the domestic currency. It is usually mani-fested by one of the following three outcomes: largedepreciation (if speculators succeed in their attack), largeloss of reserves (as the government is trying to defendthe regime by selling its reserves at the current exchangerate), ora sharp increase in interest rate (as thegovernmentis trying to defend the regime with the interest rate tool).

Eichengreen et al. (1995) study the determinants ofcurrency crises and speculative attacks. They are ableto find a set of determinants for several types of eventsbut not for others. In particular, devaluations are pre-ceded by political instability, fast growth ofmoney, infla-tion, and budget and current account deficits. But, at thesame time, they find no early warning signs for changesin exchange rate regimes (e.g., floatation) that may fol-low a speculative attack. Hence, they conclude that thereis a great deal of self-fulfilling element in these events.

While in the past, banking crises and currency criseswere treated as separate phenomena, an important as-pect of financial globalization is that they became inter-dependent. This phenomenon has been documented byKaminsky and Reinhart (1999) and is often referred to asthe ‘twin crises.’ Kaminsky and Reinhart observe a vi-cious circle between the two types of crises; each one am-plifies the prevalence of the other.

Theoretically, the ‘twin crises’ phenomenon has beenthe focus of several models, including Chang andVelasco (2000) and Goldstein (2005). In a developingcountry that opened its doors to foreign capital, we oftenobserve that banks suffer from a mismatch between lia-bilities that are denominated in foreign currency and as-sets that are denominated in domestic currency.6 Then, arun on the bank weakens the currency because it leads toan outflow of foreign reserves. At the same time, an at-tack on the currency weakens the bank, as depreciationleads to an increase in the value of the liabilities relativeto the value of the assets of the bank. Hence, a viciouscircle between the two crises ensues, amplifying the like-lihood of both.

Indeed, after studying a sample of 20 countries overthe period between 1970 and 1995, Kaminsky andReinhart find that, following the increase in liberaliza-tion of financial markets across the world, the 1980ssaw a huge increase in the link between banking crisesand currency crises. In most cases, the beginning of abanking crisis led to weakening of the currency and thento a currency crisis. The currency crisis, in turn, tends to

deepen the problems in the banking sector, and hencethe vicious circle arises. Aside from exposing the linkbetween banking and currency crises, Kaminsky andReinhart provide important evidence on the causes ofthe two, and hence inform the debate between the funda-mental-based approach and the panic-based approach tocrises. They show that both crises are preceded by dete-riorating economic circumstances: below-normal eco-nomic growth, declining stock prices, worsening termsof trade, overvalued exchange rates, and the rising costof credit. These fundamentals tend to be worse beforea twin crisis than before an episode where only one ofthese crises occurs. Also, a twin crisis causes more dam-age than either a banking crisis or a currency crisis alone.They also document the role of financial liberalization inthe emergence of crises. Prior to crises, there is usually aprocess of reduction in reserve requirements and an in-crease in credit.

Bordo et al. (2001) provide a historical perspectiveon international financial crises demonstrating that theyhave increased in frequency since 1973 to a level that iscomparable only to the 1920s and 1930s, but at the sametime they have not increased in severity or duration.Their explanation for the increase in crisis frequencyis the increase in capital mobility due to the liberalizationin capital accounts worldwide in the 1970s. Anotherfactor is the apparent safety nets provided by govern-ments, in the form of exchange rate pegs or deposit in-surance, which encourage risk taking and eventuallylead to crises.

Reinhart and Rogoff (2008) also provide a historicalperspective going even further back than the Bordoet al. study. They also document the same increase in fre-quency of banking crises since 1973. They show a highcorrelation between the liberalization of capital accountsand the incidence of banking crises. Interestingly, theyshow that banking crises are evenly spread betweendeveloped and developing economies. If anything, fi-nancial centers are very susceptible to banking crises.In terms of variables that lead to banking crises, they findthe following results: A sustained surge in capital in-flows is a common characteristic that leads to a bankingcrisis. Another factor preceding a banking crisis is a bub-ble in equity and housing markets, a bubble that starts toburst before the crisis.

Contagion

Some of the discussions about fundamental-basedversus panic-based crises are mirrored in the vast litera-ture on contagion. The forceful transmission of crisesacross countries and regions sometimes appears to be

6 Even if a bank’s loans to domestic firms are denominated in foreign currency, the firms will often have assets in domestic currency, and

hence they will suffer from the mismatch, which will indirectly affect the bank (as firms will have to default on their loans).

526 36. EMPIRICAL LITERATURE ON FINANCIAL CRISES: FUNDAMENTALS VS. PANIC

V. CRISES

pure panic that results from self-fulfilling beliefs. Yet, atthe same time, theories and evidence have emerged tosuggest that a lot of what we observe can be explainedwith fundamental reasons.

Kaminskyet al. (2003) provide a nice review of the the-ories behind financial contagion.7 They define contagionas an immediate reaction in one country to a crisis in an-other country. There are several theories that link suchcontagion to fundamental explanations. The clearestone would be that there is common information aboutthe different countries, and so the collapse in one countryleads investors to withdraw from other countries. Calvoand Mendoza (2000) present a model where contagionis a result of learning from the events in one countryabout the fundamentals in another country. They arguethat such learning is likely to occur when there is a vastdiversification of portfolios, as then the cost of gatheringinformation about each country in the portfolio becomesprohibitively large, encouraging investors to herd.

Another explanation is based on trade links (seee.g., Gerlach and Smets, 1995). If two countries competein export markets, the devaluation of one currency hurtsthe competitiveness of the other, leading it to devalue itscurrency as well. A third explanation is the presence offinancial links between the countries. In Kodres andPritsker (2002), investors optimize their portfolio alloca-tion. A decrease in the share of their portfolio held in onecountry due to a crisis leads them to rebalance by reduc-ing their holding in another country, and hence causes acomovement in prices. In Allen and Gale (2000), differ-ent regions insure one another against excessive liquid-ity shocks, but this implies that a shock in one region istransmitted to the other region via the insurance linkage.

Empirical evidence has followed the aforementionedtheories of contagion. The common information explana-tion has vast support in the data. Several of the clearestexamples of contagion involve countries that appearvery similar. Examples include the contagion that spreadacross East Asia in the late 1990s and the one in LatinAmerica in the early 1980s. A vast empirical literatureprovides evidence that trade links can account for conta-gion to some extent. These include Eichengreen et al.(1996) and Glick and Rose (1999). Others have shownthat financial linkages are also empirically importantin explaining contagion. For example, Kaminsky et al.(2004) have shown that US-based mutual funds contrib-ute to contagion by selling shares in one country when

prices of shares decrease in another country. Caramazzaet al. (2004), Kaminsky and Reinhart (2000), and VanRijckeghem and Weder (2003) show similar results forcommon commercial banks.

WHAT DO WE LEARN FROM THEEVIDENCE ABOUT THE ROLE OF PANIC?

While the evidence reviewed in the previous sectionprovides a strong case that fundamentals matter and cri-ses, in general, do not happen out of the blue, it does notresolve the question about whether there is also panic in-volved. To be precise, the word ‘panic’ here means thatcrises are not justified solely on the basis of fundamen-tals, as the fundamentals could have supported a noncri-sis outcome, but rather there is a crucial self-fulfillingelement behind the crisis. It should be clarified that find-ing correlation (even if it is very strong) between funda-mentals and crises is not a proof against the ‘panic’hypothesis. It is possible that the self-fulfilling expecta-tions are triggered by fundamentals, in which case fun-damentals are associated with crises, but crises wouldnot have occurred without the coordination failure.8

The global-games literature helps making these argu-ments more precise. This can be illustrated with the cur-rency-attack model by Morris and Shin (1998).9 In thismodel, thegovernmentmaintainsa fixedexchange rate re-gime at an overappreciated level. Speculatorsmay choosetoattack the regimebyselling the local currency to thegov-ernment. There is a variable y that captureshowstrong thefundamentals of the economy are (a higher y representsstronger fundamentals, and hence implies that the cur-rency is fixed at a level closer to its fundamental value).Speculators have to pay a transaction cost to attack theregime. Theymake a capital gain if the government aban-dons the regime, in which case their gain decreases in thefundamentals of the currency. The government abandonsthe regime if the cost of maintaining it is higher than thebenefit, where the cost is decreasing in the fundamentaland increasing in the number of speculators who attack.

In a framework with common knowledge about thefundamentaly, thepossibleequilibriumoutcomesdependonwhich one of the three regions the fundamental y is in.This is depicted inFigure36.1. Belowa threshold

�y, there is

a unique equilibrium where speculators attack the cur-rency and the government abandons the regime. Here,

7 For a broader review, see the collection of chapters in Claessens and Forbes (2001).8 Similarly, not finding evidence that fundamentals are associated with crises is also not proof that there is panic, as it could just be that the

econometricians were not able to identify all the relevant fundamental variables.9 Goldstein and Pauzner (2005) analyze a global-games model of bank runs. Their model is more involved because the bank-run problem

violates one of the central assumptions in the global-games literature – that agents’ incentive to take a certain action monotonically

increases in the proportion of other agents who take this action – and hence they develop a new proof technique.

527WHAT DO WE LEARN FROM THE EVIDENCE ABOUT THE ROLE OF PANIC?

V. CRISES

the fundamentals are so low that the government willabandon the regime no matter what speculators do (asthe cost of maintaining the regime is high due to the lowfundamentals), and hence each speculator undoubtedlyfinds it profitable to attack.Above a threshold �y (>

�y), there

is a unique equilibrium where speculators do not attackthe currency and the government maintains the regime.Here, the fundamentals are so high that speculators makeanet loss fromthe attack even if thegovernment abandonsthe regime (since the capital gain is lower than the transac-tion cost). Hence, they choose not to attack. Between

�y and

�y, therearemultiple equilibria.Eithereveryoneattacksandthegovernmentabandons theregimeornooneattacksandthe government maintains the regime. There are strategiccomplementarities, as speculators benefit from the attackif, and only if, other speculators attack, and hence thereare two possible equilibria.

The intermediate range between�y and �y captures the

traditional view of panic-based crises. Here, whetherthere is a currency crisis cannot be determined by funda-mentals and is left entirely to self-fulfilling beliefs. Atevery level of the fundamental in this range, a crisiscan either occur or not occur solely on the basis of self-fulfilling beliefs. A usual statement is that the occurrenceof a crisis is left to a sunspot – a nonfundamental event –that coordinates agents’ expectations on this outcome.10

However, introducing noise in speculators’ informa-tion about the fundamental y dramatically changes the

predictions of the model even if the noise is very small.The new predictions are depicted in Figure 36.2. Now,the intermediate region between

�y and �y is split into

two subregions: below y*, an attack occurs and the re-gime is abandoned, while above it, there is no attackand the regime is maintained.11

This result can be best understood by applying thelogic of a backward induction. Owing to the slight noisein agents’ information about y, agents’ decisions aboutwhether to attack no longer depend only on the informa-tion conveyed by the signal about the fundamental, butalso depend on what the signal conveys about otheragents’ signals. Hence, between

�y and �y, agents can no

longer perfectly coordinate on any of the outcomes (at-tack or not attack), as their actions now depend on whatthey think other agents will do at other signals. Hence, aspeculator observing a signal slightly below �y knowsthat other speculators may have observed signals above�y and chose not to attack. Taking this into account, hechooses not to attack. Then, knowing that speculatorswith signals just below �y are not attacking, and applyingthe same logic, speculators with even lower signals willalso choose not to attack. This logic can be repeated againand again, establishing a boundary well below �y, abovewhich speculators do not attack. The same logic can thenbe repeated from the other direction, establishing aboundary well above

�y, below which speculators do

attack. The mathematical proof shows that the two

Currencyattack

q q q

Multipleequilibria

No currencyattack

FIGURE 36.1 Currency attacks with commonknowledge: tripartite classification of the fundamen-tals. Reproduced from Morris, S., Shin, H.S., 1998. Uniqueequilibrium in a model of self-fulfilling currency attacks.

American Economic Review 88, 587–597.

Fundamental-based

currencyattack

q*q q q

Panic-basedcurrency

attack

No currencyattack

FIGURE 36.2 Equilibrium outcomes in acurrency-attack model with noncommon knowl-edge. Reproduced from Morris, S., Shin, H.S., 1998.

Unique equilibrium in a model of self-fulfilling

currency attacks. American Economic Review 88,

587–597.

10 It should be noted that even in Figure 36.1, there is some association between the fundamentals and panics, as panics occur only when

the fundamentals are in an intermediate range. Introducing noise makes this much stronger.11 This sharp outcome is obtainedwhen the noise in the signal approaches zero. For larger noise, the transition from attack to no-attackwill

not be so abrupt, but rather there will be a range of partial attack. This does not matter for the qualitative message of the theory.

528 36. EMPIRICAL LITERATURE ON FINANCIAL CRISES: FUNDAMENTALS VS. PANIC

V. CRISES

boundaries coincide at y*, such that all speculators attackbelow y* and do not attack above y*.

As Figure 36.2 shows, in the range between�y and �y,

the level of the fundamental now perfectly predictswhether or not a crisis occurs. In particular, a crisissurely occurs below y*. Crises in this range can bereferred to as ‘panic-based’ because a crisis in this rangeis not necessitated by the fundamentals; it occurs be-cause agents think it will occur, and in that sense, it isself-fulfilling. However, the occurrence of a self-fulfillingcrisis here is uniquely pinned down by the fundamen-tals. So, in this sense, the ‘panic-based’ approach andthe ‘fundamental-based’ approach are not contradictory.The occurrence of a crisis is pinned down by fundamen-tals, but crises are self-fulfilling as they would nothave occurred if agents did not expect them to occur.The key is that the fundamentals uniquely determineagents’ expectations about whether a crisis will occur,and in that, they indirectly determine whether a crisisoccurs. Agents’ self-fulfilling beliefs amplify the effectof fundamentals on the economy.

The discussion in the preceding paragraphs demon-strates why the evidence reviewed in section ‘EmpiricalEvidence on the Role of Fundamentals’ that fundamen-tals matter for crises does not speak against the validityof the panic-based approach to financial crises. Consis-tent with evidence, the global-games approach predictsthat criseswill occur at low fundamentals andwill not oc-cur at high fundamentals, but crises are still self-fulfilling(or panic-based). Hence, to detect the panic-based mech-anism in thedata, one needs to resort to other strategies.12

Such strategies are discussed in the next section.Before turning to the next section, it might be useful to

go back briefly to the issue of contagion that wasreviewed at the end of the section ‘Empirical Evidenceon the Role of Fundamentals.’ The fact that contagioncan be attributed to fundamental factors, again, doesnot imply that there is no panic element in it. For exam-ple, consider the model in Goldstein and Pauzner (2004).Contagion happens in this model due to a fundamentalfactor – diversification of investment portfolios. Yet, cri-ses are still self-fulfilling and would not occur if agentsdo not believe they are going to occur.13 In the model,there are two countries that have independent funda-mentals, but share the same group of investors. A crisismight erupt in each country because of self-fulfilling be-liefs. That is, there are strategic complementarities thatimply that investors are better off keeping their money

in a country only if they believe that other investorsare going to do so. Using the global-games technique,one can uniquely determine whether a crisis is goingto occur in each country as a function of the fundamen-tals in that country. Contagion then occurs as a result of awealth effect. The occurrence of a crisis in one countrymakes investors poorer and hence more risk-averse.Then, they are more averse to the strategic risk involvedin keeping their money in the other country and beingdependent on what others do, so they are more likelyto run. Hence, a crisis in the other country becomes morelikely, and the contagion ensues. In summary, a funda-mental cause – financial link – creates contagion, but con-tagion is still self-fulfilling. In fact, the crisis in onecountry makes investors more risk-averse and hencemore likely to ‘panic’ in the other country.

HOW CAN WE TEST FOR PANIC?

To fix ideas, onemight speculate onwhatwould be theideal way to capture ‘panic’ in the data. Ideally, onewould like to show that investors withdraw capital be-cause they believe that other investors are going to with-draw capital. So, in a laboratory, we could tell subjectsabout the upcoming behavior of others and see how theychange their own behavior (making sure that they do notinfer anything about the fundamentals from the behaviorof others). Clearly, the realworld is not a laboratory, and itis quite difficult to find a situation that is close to this ex-periment. Outside a controlled experiment, running a re-gression where the behavior of some investors isexplained by the behavior of others is not a valid econo-metric approach, as it suffers from the reflection problem(seeManski, 1993). That is, finding that investors aremorelikely to run when others run is not a proof for panic orstrategic complementarities, as it is very possible that theydo the same thing because they all observed some funda-mental variable that led them to run.

In a recent paper, Hertzberg et al. (2010) use a naturalexperiment that comes very close to the desired con-trolled environment mentioned earlier. Their natural ex-periment is based on the expansion of the Public CreditRegistry in Argentina in 1998. The role of the registry isto aggregate information about borrowers and tomake itavailable to potential lenders. The information includesassessments by current lenders of the creditworthinessof the borrower. Prior to 1998, the registry only provided

12 The issue of panic versus fundamental crisis is parallel to the question of illiquidity versus insolvency. A panic-based run is said to occur

when a bank is solvent, but illiquid. That is, when the fundamentals are good enough that the bankwould survive had investors not run, but

if they ran they can bring the bank down. The problem is that illiquidity and insolvency are intertwined. The fact that fundamentals decrease

might bring the bank closer to insolvency, but thismay also trigger the illiquidity risk. This point is illustratedparticularlywell byMorris and

Shin (2010). They show that investors are more likely to coordinate on a self-fulfilling attack when the risk of insolvency is high.13 See also Dasgupta (2004) for a model of contagion of self-fulfilling crises due to interbank connections.

529HOW CAN WE TEST FOR PANIC?

V. CRISES

information about borrowerswhose total debtwas above$200000. This is due to the cost of distributing informa-tion for a large number of small borrowers. In 1998, fol-lowing the adoption of CD-ROMs, the need for thethreshold was eliminated, leading to the disclosure of in-formation about 540000 borrowers, for which credit as-sessments were previously only known privately.

The reform was announced in April 1998 and imple-mented in July of that year. Hence, the experiment givesrise to three distinct periods. The first is the period beforethe announcement, during which lenders providedloans to borrowers who owe less than the threshold,expecting that their information will not be observedby anyone else. The second period is the interim periodbetween the announcement and the implementation,during which the information was still available onlyto the lender, but it was already known that it would be-come available to other lenders soon. Finally, the thirdperiod is after the announcement, when the informationabout the creditors became available publicly.

Hertzberg, Liberti, and Paravisini identify the pres-ence of complementarities in lending by studying the dif-ference in lenders’ behavior between the first period andthe intermediate period. Consider a lender who had neg-ative information about a borrower, for whom the infor-mation was not initially disclosed (since the borrowerowed less than $200000 in total). From the point of viewof this lender, no new information has arrived betweenthe twoperiods. Theonlydifference is that in the interme-diate period, he realizes that the informationwill becomeavailable publicly. The authors show that for these bor-rowers, the amount of credit has decreased between thefirst and intermediate period. This is supposedly becausethe lenders realized that making this information publicwill make other lenders reduce credit. Hence, since theycare about what other lenders do, they reduced credit aswell. To further support their case, they use a differences-in-differences approach and show that the decrease indebt in the interim period is not observed for firms thatwere slightly above the threshold (forwhom the informa-tion was always available) and for those who borrowfrom only one lender (for whom there is no coordinationproblem). Their results are demonstrated in Figure 36.3.

The paper by Hertzberg, Liberti, and Paravisinispeaks of an important aspect of coordination problems,which is the public information multiplier. That is, be-cause of coordination motives, information disclosedpublicly ends up having a larger effect than private in-formation. This aspect has been the subject of a large lit-erature starting from Morris and Shin (2002). It suggeststhat public information may have adverse effects, and

hence there may be a welfare gain in reducing disclo-sure. In the context studied by Hertzberg, Liberti, andParavisini, lenders act on their information only whenthey realize it is going to become public. Hence, the dis-closure of public information seems to play an importantrole in triggering a coordination failure among lenders.

While the paper by Hertzberg, Liberti, and Paravisiniprovidesaverycleanexperiment that enablesdirect iden-tification of complementarities in lending, its limitation isthat it identifies a very local effect. That is, it tells us aboutthe behavior of lenders to borrowerswho borrow around$200000. Findingmore general evidence for complemen-tarities requires one to look outside the narrow frame-work of a natural experiment. In another recent paper,Chen et al. (2010) provide an empirical test for the effectof strategic complementarities among US mutual fundinvestors and show how they create financial fragility.They attempt to identify the effect of strategic comple-mentarities by investigating whether the response ofinvestors to fundamentals is stronger in caseswhere com-plementarities are expected to be stronger. That is, theystudy whether the strategic complementarities amplifythe effect of fundamentals on outflows, and hence createfinancial fragility. Finding such evidence is an indicationof the presence of panic, as it implies that investors actmore forcefully just because of the expected action ofothers.

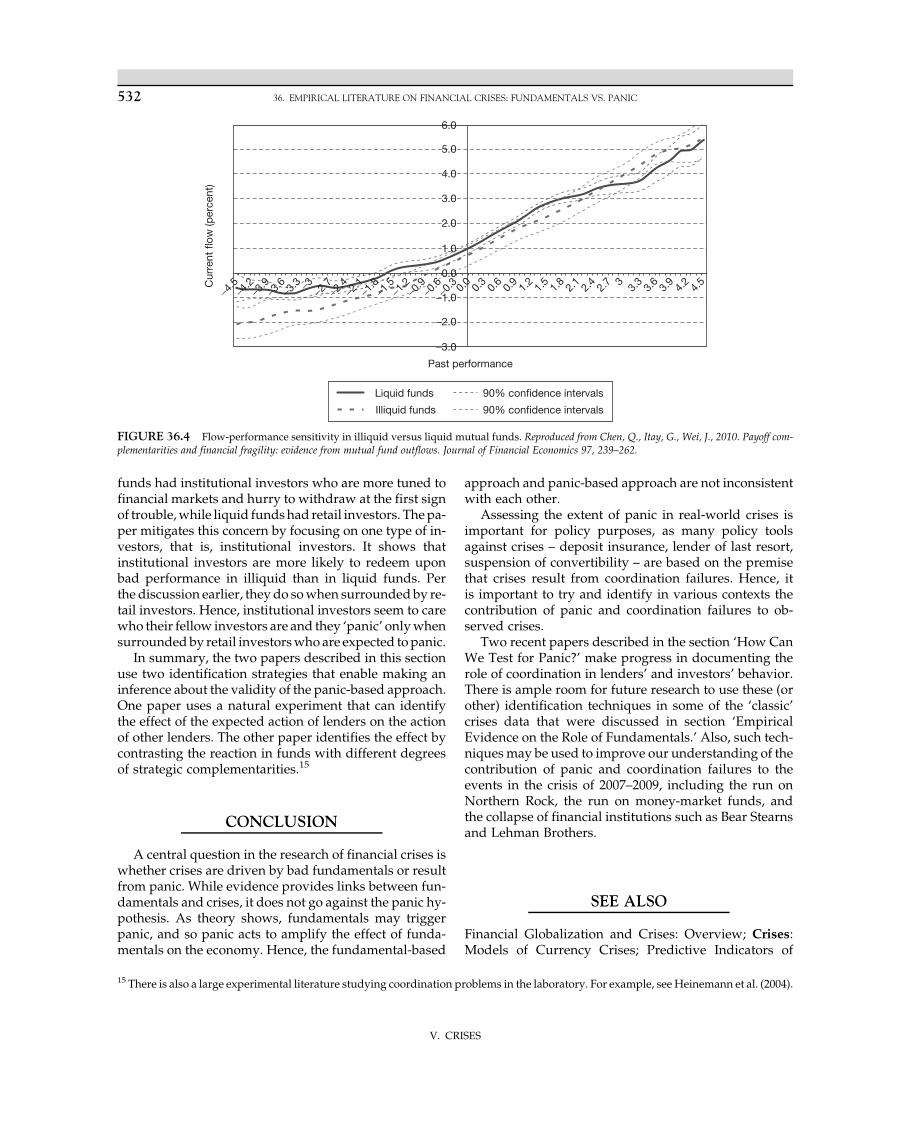

The study is motivated by the institutional back-ground of the open-end mutual fund industry. Investorsin open-end mutual funds have the right to redeem theirshares at net asset value every business day. Theirredemptions are costly to the mutual fund because themutual fund needs to sell assets to accommodate thewithdrawals or otherwise deviate from the plannedportfolio holdings. The key feature is that this cost ismostly transferred to investors who stay in the fundrather than being borne by those who redeem. The rea-son is that funds conduct transactions after the day ofwithdrawal, and so the net asset value as of the dayof withdrawal does not reflect the full damage of thewithdrawal. This creates strategic complementarities:the expectation that other investors are going to redeemincreases the incentive to redeem and avoid the damagefrom staying in the fund and bearing the cost of redemp-tion. Crucially, this mechanism is strong in funds withilliquid assets (for which transaction costs are high)rather than in those with liquid assets. Hence, if strategiccomplementarities matter, one should observe a stron-ger response of outflows to bad performance in illiquidthan in liquid funds. Chen, Goldstein, and Jiang find thisresult. It is demonstrated in Figure 36.4.14

14 The graph shows results from a semiparametric analysis that does not assume linearity. Hence, the confidence intervals are wide. In the

paper, the regression analysis establishes highly significant results.

530 36. EMPIRICAL LITERATURE ON FINANCIAL CRISES: FUNDAMENTALS VS. PANIC

V. CRISES

The paper goes on to provide further tests. Anothercut at the data is obtained by considering the type of in-vestors in the mutual fund. As we learn from the paperby Corsetti et al. (2004), large investors are less likely tofall into a coordination failure, as they internalize someof the externalities by being large. This then injects stabil-ity to the fund. Hence, taking this insight into the currentcontext, one would expect that the effect of illiquidity onthe sensitivity of outflows to bad performance will beweaker among funds that are held mainly by large/institutional investors.This is indeedconfirmed in thedata.

Finally, since the identification relies on the idea thatdifferences in liquidity proxy for differences in thestrength of complementarities across funds, it is impor-tant to make sure that differences in liquidity do not

capture other important differences across funds. Twoalternative stories come to mind. First, in the spirit ofthe fundamental-based approach reviewed earlier,maybe investors in illiquid funds are more responsiveto bad performance because in these funds bad perfor-mance is more indicative of future performance, thatis, it is fundamentally justified to be more sensitive tobad performance in these funds. Chen, Goldstein, andJiang mitigate this concern by showing in different waysthat the returns in illiquid funds do not show more per-sistence than in liquid funds.

Second, maybe investors in illiquid funds aremore re-sponsive tobadperformance than in liquid fundsbecausethe two types of funds simply have different types of in-vestors. This would make sense, for example, if illiquid

5.5

Firms with multiple lenders before expansion announcement

Firms with a single lender before expansion announcement

5.4

5.3

5.2

5.1

5In (t

otal

deb

t)

4.9

4.8

4.7

Jan-

98

Feb

-98

Mar

-98

Ap

r-98

May

-98

Jun-

98

Jul-

98

Aug

-98

Sep

-98

Oct

-98

5.5

5.4

5.3

5.2

5.1

5In (t

otal

deb

t)

4.9

4.8

4.7

(b) Jan-

98

Feb

-98

Mar

-98

Ap

r-98

May

-98

Jun-

98

Jul-

98

Aug

-98

Sep

-98

Oct

-98

Treatment Control

(a)

FIGURE 36.3 Debt levels of firms around the credit reg-istry expansion in Argentina; treatment firms have debtlevels between $150000 and $200000 and control firms havedebt levels between $200000 and $250000. Reproduced from

Hertzberg, A., Jose, M.L., Daniel, P., 2010. Public information

and coordination: evidence from a credit registry expansion. Jour-nal of Finance.

531HOW CAN WE TEST FOR PANIC?

V. CRISES

funds had institutional investors who are more tuned tofinancial markets and hurry to withdraw at the first signof trouble,while liquid fundshad retail investors. Thepa-per mitigates this concern by focusing on one type of in-vestors, that is, institutional investors. It shows thatinstitutional investors are more likely to redeem uponbad performance in illiquid than in liquid funds. Perthe discussion earlier, they do sowhen surroundedby re-tail investors. Hence, institutional investors seem to carewho their fellow investors are and they ‘panic’ onlywhensurroundedby retail investorswhoare expected topanic.

In summary, the two papers described in this sectionuse two identification strategies that enable making aninference about the validity of the panic-based approach.One paper uses a natural experiment that can identifythe effect of the expected action of lenders on the actionof other lenders. The other paper identifies the effect bycontrasting the reaction in funds with different degreesof strategic complementarities.15

CONCLUSION

A central question in the research of financial crises iswhether crises are driven by bad fundamentals or resultfrom panic. While evidence provides links between fun-damentals and crises, it does not go against the panic hy-pothesis. As theory shows, fundamentals may triggerpanic, and so panic acts to amplify the effect of funda-mentals on the economy. Hence, the fundamental-based

approach and panic-based approach are not inconsistentwith each other.

Assessing the extent of panic in real-world crises isimportant for policy purposes, as many policy toolsagainst crises – deposit insurance, lender of last resort,suspension of convertibility – are based on the premisethat crises result from coordination failures. Hence, itis important to try and identify in various contexts thecontribution of panic and coordination failures to ob-served crises.

Two recent papers described in the section ‘How CanWe Test for Panic?’ make progress in documenting therole of coordination in lenders’ and investors’ behavior.There is ample room for future research to use these (orother) identification techniques in some of the ‘classic’crises data that were discussed in section ‘EmpiricalEvidence on the Role of Fundamentals.’ Also, such tech-niquesmay be used to improve our understanding of thecontribution of panic and coordination failures to theevents in the crisis of 2007–2009, including the run onNorthern Rock, the run on money-market funds, andthe collapse of financial institutions such as Bear Stearnsand Lehman Brothers.

SEE ALSO

Financial Globalization and Crises: Overview; Crises:Models of Currency Crises; Predictive Indicators of

6.0

5.0

4.0

3.0

2.0

1.0

Cur

rent

flow

(per

cent

)

0.0

−1.0

−2.0

−4.5

−4.2

−3.9

−3.6

−3.3 −3 −2

.7−2

.4−2

.1−1

.8−1

.5−1

.2−0

.9−0

.6−0

.3 0.0

0.3

0.6

0.9

1.2

1.5

1.8

2.1

2.4

2.7 3

3.3

3.6

3.9

4.2

4.5

−3.0

Past performance

Liquid funds 90% confidence intervals

90% confidence intervalsIlliquid funds

FIGURE 36.4 Flow-performance sensitivity in illiquid versus liquid mutual funds. Reproduced from Chen, Q., Itay, G., Wei, J., 2010. Payoff com-

plementarities and financial fragility: evidence from mutual fund outflows. Journal of Financial Economics 97, 239–262.

15 There is also a large experimental literature studying coordination problems in the laboratory. For example, see Heinemann et al. (2004).

532 36. EMPIRICAL LITERATURE ON FINANCIAL CRISES: FUNDAMENTALS VS. PANIC

V. CRISES

Financial Crises; Definitions and Types of Financial Con-tagion; East-Asian Crisis of 1997.

Acknowledgments

The authors thank Franklin Allen, Philip Bond, Stijn Claessens, AlexEdmans, and Wei Jiang for their helpful comments. They also thankCarrie Wu for her research assistance.

Glossary

Banking crisis The failure of banks due to runs by creditors, a deteri-oration in banks’ asset values, or a combination of both.

Contagion A scenario in which crises spread across banks, regions, oreconomies.

Currency crisis A speculative attack on a currency regime, leading to alarge depreciation, loss of reserves, or a sharp interest-rate increase.

Global games In economics and game theory, global games are gameswhere agents receive noisy information about the state. Thesegames often overturn the multiplicity of equilibria result in gamesof complete information.

Self-fulfilling beliefs In economics and game theory, self-fulfillingbeliefs are equilibrium outcomes that occur only because agents be-lieve they will occur.

Strategic complementarities In economics and game theory, strategiccomplementarities exist when agents want to take similar actions toother agents.

Twin crisis A combination of a banking crisis and a currency crisis.

References

Allen, F., Gale, D., 1998. Optimal financial crises. Journal of Finance 53,1245–1284.

Allen, F., Gale, D., 2000. Financial contagion. Journal of Political Econ-omy 108, 1–33.

Bordo,M., Eichengreen, B., Klingebiel, D.,Martinez-Peria,M.S., 2001. Isthe crisis problem growingmore severe? Economic Policy 16, 51–82.

Bryant, J., 1980. A model of reserves, bank runs, and deposit insurance.Journal of Banking and Finance 4, 335–344.

Calomiris, C., Mason, J.R., 2003. Fundamentals, panics, and bank dis-tress during the depression. American Economic Review 93,1615–1647.

Calvo, G., Mendoza, E., 2000. Rational contagion and the globalizationof securitiesmarkets. Journal of International Economics 51, 79–113.

Caramazza, F., Ricci, L., Salgado, R., 2004. International financial con-tagion in currency crises. Journal of International Money and Fi-nance 23, 51–70.

Carlsson, H., van Damme, E., 1993. Global games and equilibrium se-lection. Econometrica 61, 989–1018.

Chang, R., Velasco, A., 2000. Financial fragility and the exchange rateregime. Journal of Economic Theory 92, 1–34.

Chari, V.V., Jagannathan, R., 1988. Banking panics, information, and ra-tional expectations equilibrium. Journal of Finance 43, 749–760.

Chen, Q., Goldstein, I., Jiang, W., 2010. Payoff complementarities andfinancial fragility: evidence from mutual fund outflows. Journalof Financial Economics 97, 239–262.

Claessens, S., Forbes, K. (Eds.), 2001. International Financial Contagion.Kluwer Academic, Norwell, MA.

Corsetti, G., Dasgupta, A., Morris, S., Shin, H.S., 2004. Does one Sorosmake a difference? A theory of currency crises with large and smalltraders. Review of Economic Studies 71, 87–114.

Dasgupta, A., 2004. Financial contagion through capital connections:a model of the origin and spread of bank panics. Journal of theEuropean Economic Association 2, 1049–1084.

Demirguc-Kunt, A., Detragiache, E., 1998. The determinants of bankingcrises: evidence from developed and developing countries. IMFStaff Papers 45, 81–109.

Demirguc-Kunt, A., Detragiache, E., 2002. Does deposit insuranceincrease banking system stability? An empirical investigation. Jour-nal of Monetary Economics 49, 1373–1406.

Diamond, D.W., Dybvig, P.H., 1983. Bank runs, deposit insurance, andliquidity. Journal of Political Economy 91, 401–419.

Eichengreen, B., Rose, A., Wyplosz, C., 1995. Exchange market may-hem: the antecedents and aftermath of speculative attacks. Eco-nomic Policy 10, 249–312.

Eichengreen, B., Rose, A.,Wyplosz, C., 1996. Contagious speculative at-tacks: first tests. The Scandinavian Journal of Economics 98,463–484.

Friedman, M., Schwartz, A.J., 1963. A Monetary History of the UnitedStates: 1867–1960. Princeton University Press, Princeton, NJ.

Gerlach, S., Smets, F., 1995. Contagious speculative attacks. EuropeanJournal of Political Economy 11, 45–63.

Glick, R., Rose, A., 1999. Contagion and trade: why are currencycrises regional? Journal of International Money and Finance 18,603–617.

Goldstein, I., 2005. Strategic complementarities and the Twin Crises.The Economic Journal 115, 368–390.

Goldstein, I., Pauzner, A., 2005. Contagion of self-fulfilling financialcrises due to diversification of investment portfolios. Journal ofEconomic Theory 119, 151–183.

Goldstein, I., Pauzner, A., 2005. Demand deposit contracts and theprobability of bank runs. Journal of Finance 60, 1293–1328.

Gorton, G., 1988. Banking panics and business cycles. Oxford EconomicPapers 40, 751–781.

Heinemann, F., Nagel, R., Ockenfels, P., 2004. The theory ofglobal games on test: experimental analysis of coordinationgames with public and private information. Econometrica 72,1583–1599.

Hertzberg, A., Liberti, J.M., Paravisini, D., 2011. Public information andcoordination: evidence from a credit registry expansion. Journal ofFinance 66, 379–412.

Jacklin, C.J., Bhattacharya, S., 1988. Distinguishing panics andinformation-based bank runs: welfare andpolicy implications. Jour-nal of Political Economy 96, 568–592.

Kaminsky, G.L., Lyons, R., Schmukler, S.L., 2004. Managers, investors,and crises: mutual fund strategies in emerging markets. Journal ofInternational Economics 64, 113–134.

Kaminsky, G.L., Reinhart, C.M., 1999. The twin crises: the causes ofbanking and balance-of-payments problems. American EconomicReview 89, 473–500.

Kaminsky, G.L., Reinhart, C.M., 2000. On crises, contagion, and confu-sion. Journal of International Economics 51, 145–168.

Kaminsky, G.L., Reinhart, C.M., Vegh, C.A., 2003. The unholy trinity offinancial contagion. Journal of Economic Perspectives 17, 51–74.

Kindleberger, C.P., 1978. Manias, Panics, and Crashes: A History ofFinancial Crises. Basic Books, New York, NY.

Kodres, L.E., Pritsker, M., 2002. A rational expectations model of finan-cial contagion. Journal of Finance 57, 769–799.

Krugman, P., 1979. A model of balance-of-payments crises. Journal ofMoney, Credit, and Banking 11, 311–325.

Krugman, P., 1999. Balance sheets, the transfer problem, and financialcrises. International Tax and Public Finance 6, 459–472.

Manski, C., 1993. Identification of endogenous social effects: the reflec-tion problem. Review of Economic Studies 60, 531–542.

Martinez-Peria, M.S., Schmukler, S.L., 2001. Do depositors punishbanks for bad behavior? Market discipline, deposit Insurance,and banking crises. Journal of Finance 56, 1029–1051.

533CONCLUSION

V. CRISES

Morris, S., Shin, H.S., 2010. Illiquidity Component of Credit Risk, Prin-ceton University Working Paper.

Morris, S., Shin, H.S., 1998. Unique equilibrium in a model of self-fulfilling currency attacks. American Economic Review 88, 587–597.

Morris, S., Shin, H.S., 2002. Social value of public information.American Economic Review 92, 1521–1534.

Obstfeld, M., 1996. Models of currency crises with self-fulfillingfeatures. European Economic Review 40, 1037–1047.

Reinhart, C.M., Rogoff, K.S., 2008. Banking Crises: An Equal Opportu-nity Menace, NBER Working Paper 14587.

Rochet, J.-C., Vives, X., 2004. Coordination failures and the lender oflast resort: was Bagehot right after all? Journal of the EuropeanEconomic Association 2, 1116–1147.

Schumacher, L., 2000. Bank runs and currency run in a system withouta safety net: Argentina and the ‘tequila’ shock. Journal of MonetaryEconomics 46, 257–277.

Van Rijckeghem, C., Weder, B., 2003. Spillovers through banking cen-ters: a panel data analysis of bank flows. Journal of InternationalMoney and Finance 22, 483–509.

534 36. EMPIRICAL LITERATURE ON FINANCIAL CRISES: FUNDAMENTALS VS. PANIC

V. CRISES