00702710 en en uganda poverty alleviation project pper

TRANSCRIPT

AFRICAN DEVELOPMENT BANK GROUP

UGANDA

POVERTY ALLEVIATION PROJECT

Project Performance Evaluation Report (PPER)

OPERATIONS EVALUATION DEPARTMENT (OPEV)

14 June 2001

TABLE OF CONTENTS

Page No.

Abbreviations i Ratings ii Preface iii Basic Project Data iv Evaluation Summary vi

1. THE PROJECT 1 1.1 Country Context 1 1.2 Project Formulation 2 1.3 Objectives and scope at appraisal (Logical Framework) 3 1.4 Financing Arrangements 4

2. THE EVALUATION 4

2.1 Evaluation Methodology and Approach 4 3. IMPLEMENTATION PERFORMANCE 5

3.1 Loan Effectiveness, Start-up and Implementation (Compliance with Loan Conditions and Covenants, Procurement, Changes in Project Scope) 5

3.2 Adherence to Project Costs, Disbursements and Financial Arrangements 6 3.3 Project Management, Reporting, Monitoring and Evaluation Achievements 6

4. PERFORMANCE EVALUATION AND RATINGS 8

4.1 Relevance of Goals and Objectives and Quality-at-Entry Assessment 8 4.2 Achievements of Objectives and outputs (“Efficacy”) 10 4.3 Efficiency 15 4.4 Institutional Development Impact 15 4.5 Sustainability of PAP and the Micro-Projects 16 4.6 Aggregate Performance Indicators 18 4.7 Borrower Performance 18 4.8 Bank Group Performance 19 4.9 Major Factors Affecting Implementation Performance and Outcome 20

5. CONCLUSIONS, LESSONS AND RECOMMENDATIONS 21

5.1 Conclusions 21 5.2 Lessons Learnt 22 5.3 Recommendations 23 5.4 Plan of Action 25

LIST OF ANNEXES

No. of Pages

1. Performance Evaluation Ratings 4 2. Retrospective Logical Framework Matrix 4 3. Factors Affecting Implementation Performance and Outcome 2 4. Recommendations and Follow-up Action Matrix 2 ------------------------------------------------------------------------------------------------------------------------ This Project Performance Evaluation Report has been prepared by Mr N. SANGBE, Agroeconomist and Mr. A. Latigo, Consultant, following an Evaluation mission to Uganda in July, 2000. Contributions were received from OCOD, OESU and OCDE. Further information on this Report may be obtained from N. SANGBE on extension 4554 or Mr. G.M.B KARIISA, Director, OPEV, extension 4052.

ABBREVIATIONS

ADB : African Development Bank ADF : African Development Fund AMFIU : Association of Micro-enterprise Financial Institutions of Uganda ARMI : Association of Rural Micro-finance Institutions BOU : Bank of Uganda CAP : Community action Program CBO : Community Based Organisation CCIs : Cross Cutting Issues DPOs : District Project Officers CMF : Centre for Micro-finance EIA : Environmental Impact Assessment EIRR : economic Internal Rate of Return EU : European Union FIRR : Financial Internal rate of Return GDP : Gross Domestic Product GOU : Government of Uganda Ies : Intermediary Entities IGSU : Income Generating Support Unit MDIs : Micro-finance Deposit-taking Institutions MFIs : Micro-finance Institutions MPP : Micro-projects Program MSC : Micro-finance Support Centre MIS : Management Information System MFPED : Ministry of Finance, Planning and Economic Development NGO : Non Governmental Organisation NPSC : National Project Steering Committee NPEAP : National Poverty Eradication Action Plan NRM : National Resistance Movement OPM : Office of the Prime Minister PAP : Poverty Alleviation Project PAR : Project appraisal Report PASPSCAD : Program for Alleviating Poverty and social Adjustment PCR : Project Completion Report PDAOs : Project District Area Offices PPER : Project Performance Evaluation Report PPF : Project Preparatory Facility PRESTO : Private Support Training and Organisational Development Project PSDP : Private Sector Development Program RMSP : Rural Micro-finance Support Project RPPA : Rapid Participatory Poverty Assessment UA : Unit of Account UCB : Uganda Commercial Bank USAID : United States Agency for International Development

ii

WEIGHTS AND MEASUREMENTS Metric System

RATINGS

Evaluation Criteria PCR PPER Relevance

3

Satisfactory

3

Satisfactory

“Efficacy” 3 Satisfactory 3 Satisfactory Efficiency 3 Satisfactory 3 Satisfactory Institutional Development Impact 3 Satisfactory 3 Satisfactory Sustainability 3 Satisfactory 3 Satisfactory Aggregate Performance Indicator Not Available 3 Satisfactory Borrower Performance 3 Satisfactory 3 Satisfactory Bank Performance 3 Satisfactory 3 Satisfactory

iii

PREFACE

1. Poverty reduction has been for several years the overarching goal of the Bank Group and its Regional Member Countries (RMCs), which are now actively involved in promoting micro-finance as an important tool for poverty reduction. The Uganda Poverty Alleviation Project (PAP) was the first of its kind to be financed by the African Development Fund (ADF) in Uganda and also the first of its nature in Bank Group operations. The unique feature of the project is that it was the first ADF-financed project, which heavily relied on NGOs in delivering micro-finance services to the poor in project target areas, and it used a participatory approach, which relied on involvement of beneficiaries in all stages of micro-project development. This Project Performance Evaluation Report (PPER) also represents the first post-evaluation of poverty alleviation project of this nature. The Project Completion Report (PCR) was prepared in October 1999 by the Bank's experts. However, the PCR did not give an independent assessment of the efficiency of the Bank's activities and development effectiveness of the project, and its impact on the beneficiaries, with a view to assessing their sustainability. Hence, this PPER represents an independent review that supplements the findings of the PCR and through such a review draws lessons from the experience, for the purpose of improving future Bank operations in micro-financing.

2. The project goal was to assist in poverty reduction, while the project objective was to

improve access of the poor, especially women to productive assets (land and credit). This goal and objective were to be achieved through credit schemes to finance micro-projects; training and extension services to local communities; and institutional support (provision of long-term technical advisor, short-term consultants and training). To finance these activities, the Government of Uganda (GOU) received a total UA 9.21 million from the Bank Group. The project achieved both its goal and objective. It expanded micro-finance services to the poor people in Uganda, and of these, most are women, greatly reducing disparity in gender in terms of access to credit and non-financial services. It also increased savings by households, increased income and consumption, better education for children, and social exclusion, and greater security. Accompanying these achievements were the establishment of an autonomous operations oriented micro-finance institution in Uganda, and the development of a Micro-finance Policy and Regulatory Framework, which is being drafted into a law to regulate administration and delivery of micro-finance services by MFIs in Uganda.

3. While documenting the achievements the project has made, the report also tries to point

to the areas where extra efforts are now needed. Both the Bank Group and the Government will need to pay special attention to improving quality-at-entry, institutional analysis, financial management, strengthening the NGOs (intermediary entities) and project supervision of future projects. In a sense, the Bank Group as a financial development institution is entering yet another reform in its economic development strategy through empowering the poor, especially, women in rural areas by improving their access to micro-finance services.

iv

BASIC PROJECT DATA SHEET Preliminary Data Country : Uganda Project : Poverty Alleviation Project (PAP) Loan Number : F/UGA/PVA/93/94 Borrower : Government of Uganda Beneficiary and : Office of the Prime Minister

Executing Agency A. Basic Loan Data Request for Loan (01 March 1993) Amount (UA million) 9.21 Interest rate 0.00 Statutory Commission Commitment Charge 0.75% (on un-disbursed portion of the Loan) Repayment Period 40 Years Grace Period 10 Years Loan Negotiations date July 22-24, 1993 Loan Approval Date August 31, 1993 Loan Signature Date October 8, 1993 Loan Effectiveness Date June 20, 1994 B. Project Data Appraisal Estimate Actual

Total Cost 10.22 10.22 UA million equivalents 6.85 6.03 LC million equivalents 3.37 4.19 Financial Plan (UA million equivalents)

Appraisal Estimate ACTUAL Source F.E

L.C TOTAL % F.E L.C TOTAL %

ADF 6.85 3.37 9.21 90 6.03 3.17 9.21 90 GOU 0 1.01 1.01 10 0 1.02 1.01 10 Total 6.85 3.37 10.22 100 6.03 4.19 10.22 100

Projected Actual Project Preparation Date March 1993 1 March 1993 Project Appraisal Date April 19-30 1993 April 1993 Deadline for first Disbursement N/A 2 August 1994 Effective date of First Disbursement November 1993 2 August 1994 Deadline for Last Disbursement N/A 31 December 1998

v

C. Implementation Performance Indicators Cost Overrun (%) none Time Over runs 13 months (27%) Slippage on Effectiveness 27% Slippage on Completion date 25% Slippage on last Disbursement 19% Number of Extensions of last Disbursement Nil Project Implementation Status: Completed List of verifiable indicators, and Levels of achievement: Target districts 22 26 Total beneficiaries 26,000 25,877 Female beneficiaries (%) 60 62 Credit allocation (%) 77 72 D. Missions

No. Types of Missions No. of Missions

�Date No of Persons Person/Day

1 Identification N/A N/A N/A N/A 2 Preparation N/A March 1993 N/A N/A 3 Appraisal 1 19-30 April 1993 4 4 Post-Approval 5 Supervision 4 14 – 24 Nov. 1994

05 – 21 Nov. 1995 11 – 13 Mar. 1996 23 Feb – 08 Mar. 1998

3 2 5 4

10 16 3 14

6 Mid-term Review 1 June 1997 4 14 7 Completion 1 May 1999 2 14 8 Post-evaluation 1 16 July – 12 Aug.

2000 2 20

E. Disbursements (UA Million)

Annual Disbursements (UA '000 Equivalent)

Fiscal Year Projected Revised Actual 1994/95 2.68 2.59 0.891995/96 2.58 2.49 1.071996/97 2.48 2.39 2.391997/98 2.28 2.20 4.84Total 10.02 9.68 9.20

EVALUATION SUMMARY

1 This Project Performance Evaluation Report (PPER) reviews the Uganda Poverty Alleviation Project (PAP). The Project Completion Report (PCR) was prepared in 1999 by the Bank's experts. However, the PCR did not give an independent assessment of the efficiency of the Bank's activities and development effectiveness of the project, and its impact on the beneficiaries, with a view to assessing their sustainability. The PCR also did not adequately assess some aspects relating to the quality of the project including quantitative analysis of socio-economic indicators. .Hence, this PPER represents an independent review that supplements the findings of the PCR and through such a review draws lessons from the experience, for the purpose of improving future Bank operations in micro-finance.

2. At project appraisal in 1993, 96 per cent of Uganda’s population lived in rural areas, and

52.2% of the total population lived below poverty line and less than 1% of the poor population had access to institutional financial services. Therefore, the goal of the project was to assist in poverty reduction, while the objective was to develop human resources and institutional capital to enable the poor, especially, women in rural areas access effectively and productively financial services of the formal sector. To ensure viability, the project adopted market interest rate of 22% relevant to micro-credit and savings, and created an environment sufficiently flexible to attract a wide range of the Intermediary Entities (Ies) to deliver micro-finance services in rural areas. The project objective was to be achieved by three major activities: (i) credit schemes to finance income generating activities; (ii) training and extension services to local communities; and (iii) institutional support (provision of long-term technical advisor, short-term consultants and training). To finance these activities, the Government of Uganda (GOU) received a total UA 9.21 million from the Bank Group. The loan was approved in August 1993 and became effective in June 1994. The Borrower for this loan was the Ministry of Finance, Planning and Economic Development (MFPED).

3. Overall, the project had both strengths and weaknesses in conception and implementation.

The loan granted by the Bank Group was used effectively for implementing PAP, which was conceived and designed in accordance with its participatory bottom-up approach within Uganda's National Poverty Eradication Action Plan (NPEAP), and the Bank's Assistance Strategy of sustainable equitable growth and poverty reduction.

4. The project achieved its policy goal of assisting in poverty reduction, but Uganda remains

a very poor country, with about 44% of the total population still living below poverty line. This is because the national outreach to the poor is still limited despite the increased micro-finance services. Currently, only 1.5% of Uganda’s poor population has access to formal financial services. Poverty reduction requires continuous access to a broad range of financial and non-financial services not a one-time access to loans. Nevertheless, PAP’s contribution at the individual household level was significant.

5. The project also achieved its objective of developing human resources and institutional

capital, expanding access to credit by poor people, especially women, training and social intermediation to the target group, and providing institutional support. The project expanded micro-finance services including financial and social intermediation to over 25,000 poor people in Uganda, thus achieving its target set at appraisal. Of these, 62% or 15,500 are women, greatly reducing disparity in gender in terms of access to credit and non-financial services, and empowering women.

2

6. The projections for most physical objectives (outputs) were also satisfactorily achieved.

At appraisal, the project anticipated to finance more than 26,000 micro-projects in crop production, animal and fisheries, trade, and small-scale manufacturing. This target was achieved and a total of 26,636 micro-projects were financed as follows: crop production (35.4%); animal and fisheries (26.1%); trade (27.4%); small-scale manufacturing (6.9%; and others (4.1%). The highest proportion of the credit went to agriculture, shattering the myth that agriculture is not financially attractive enterprise to MFIs. And information from PAP reports and the clients met during the PPER and other Bank missions show overall increase in crop production, milk output, and poultry production. Other major achievements include increased savings by households, increased income and higher consumption, better education for children, social cohesion.

7. Probably one of the most significant results of the project was the establishment of an

autonomous operations oriented micro-finance institution in Uganda, as one of the first of its kind funded by the Bank Group in Africa. The project also generated the development of a Micro-finance Policy and Regulatory Framework, which is being drafted into a law to regulate administration and delivery of micro-finance services by MFIs in Uganda. The development of micro-finance institution in Uganda has set in motion a process of change from activity that was mostly subsidy dependent to one that can be a viable business. Probably, more than contributing to reducing national poverty, which is a long-term commitment, the expanded outreach and the development of a micro-finance institution are key achievements of PAP, making it a successful project. Today PAP is respected by its counterparts and donors for its effectiveness in establishing a micro-finance delivery system, which operates at market interest rates with high repayment rates comparable to internationally acceptable standards.

8. In terms of sustainability analysis based on technical soundness, borrower commitment,

socio-political support, economic viability and organisational effectiveness, the project results realised are likely to be sustained. However, the financial viability and sustainability of micro-finance institutions is a long-term commitment, which requires 5-10 years of investment. Nevertheless, PAP evolved around sound viability principles. Its generally high loan recovery rate of over 92% and commercial lending interest rates of 22% are indicators of cost-effective use of project resources and viability. It is envisaged that Phase II of Poverty alleviation programme (PAP) including Rural Micro-finance support (RMSP), will not have any significant recurrent cost implications on the Government budget. This is because the major part of project resources will be on lent to viable and self-sustainable micro-projects using improved internationally acceptable micro-finance best practices. These micro-projects will involve autonomous and viable MFIs and entrepreneurs who will bear the entire operating cost of running them. Strengthening institutional capacity of MFIs will be a major activity, resulting in Micro-finance Support Centre (MSC) withdrawing its presence from the districts. Furthermore, RMSP will operate as an autonomous entity that is run on best practices and will be operationally sustainable after the first three years of incurring deficit due to heavy expenditures on institutional development, technical assistance and operating cost. This deficit will be financed from the assets in the balance sheet (budget allocated funds plus funds rolled over from PAP). Thus, RMSP will reach out more clients and this will generate more interest income and with fee structure in place, additional income is expected to be generated to cover operating costs, therefore, accelerating the project's financial self-sufficiency and sustainability in the next 5 years and beyond.

3

9. The Bank performance on this project has been deficient at appraisal, and supervision

missions were inadequate in that only 4 missions visited the project over the 5-year period. As for project design and management, the Bank should have supported baseline studies and a computerised information management system that would have improved project monitoring, financial management and loan tracking system of IGSU. As poverty alleviation is the overarching goal of the Bank Group and that of the GOU, the Fund should have accorded painstaking diligence in the design of PAP.. Besides, Project Management has complained that the Bank often took long to respond to its communications, especially regarding disbursements, causing delay in project implementation..

10. The deficiencies, especially at preparation and appraisal can be attributed to lack of

previous Bank experience in related projects. As for communication, since 1997, the Bank tried to ensure more prompt response to correspondences. In 2000, the Bank Group appointed a program officer for Kampala to assist in supervision of Bank portfolio in Uganda. Also, despite these shortcomings, the Fund’s financial contribution helped establish a micro-finance institution in Uganda, one of the first few in Africa that has generated development of micro-finance best practices and regulatory framework. The project has strengthened the social and human capital of the poor, especially, the rural women. Probably this is a more important outcome than poverty reduction, which is a long-term commitment. Overall, Bank performance is rated satisfactory.

11. The main lessons to be learnt from PAP are that : (i) adoption of the financial system

approach for poverty reduction is key to maximising increased outreach and development impact, through emphasis on: enabling policy environment; financial infrastructure; and development of Ies that are committed to achieving financial viability and sustainability within a reasonable period; (ii) the Ies should be able to provide a variety of financial services, not just credit, to the poor; (iii) the demand for savings services, micro-enterprises and credit is very strong in Uganda; (iv) the outcome of a project can be compromised without early and careful planning of the evaluation design and adequate institutional analysis to ensure that the right measurable and monitorable indicators are identified; (v) the quality of project implementation can be improved with a high quality computerised management information (MIS) established early in a project cycle; (vi) achievement of viability and sustainability in poverty alleviation projects are long-term, requiring a transformation process of between 5 to 8 years; (vii) credit for agriculture is attractive, and PAP has shattered the myth that poor households can not and do not save, and that savings can be successfully mobilised from poor households; and (viii) the poor are creditworthy (especially, poor women), and financial services can be provided to and accessed by the poor on a profitable basis at low transaction costs, without relying on physical collateral.

12. In recognition of PAP’s innovative performance in micro-finance delivery, the GOU

proposed that IGSU should manage other ADF financed projects with credit components to deliver the credit to target clients in the second phase of PAP. Two such projects that will be managed by IGSU are the Uganda Southeast and Southwest Integrated Watershed Management Project, and the Northwest Smallholder Agricultural development Project. Also, because of the good performance of the project, the Bank Group accepted to fund Phase II of the PAP.

4

13. In conclusion, despite the deficiencies in the project design, implementation and monitoring, the project achieved both its goal and objective. However, it is recommended that before the RMSP is transformed into MSC, the MFPED and BOU should carry out a study to review the future role of MSC in the micro-finance industry in Uganda. The review should among others, examine carefully the MSC’s capital structure, managerial and technical staff establishment, technical viability, and institute necessary changes. The Study should also ensure high quality managerial and technical staff on the establishment of MSC. The proposed re-capitalisation should be done only after the institutional issues cited above are adequately addressed and the report submitted to the Bank Group.

1. THE PROJECT 1.1 Country Context 1.1.1 This Project Performance Evaluation Report (PPER) is for Uganda Poverty Alleviation Project (PAP). In mid 1980s, economic stagnation and poverty were the major challenges facing the new Government of the National Resistance Movement (NRM) in Uganda. In response to these challenges, the NRM Government embarked, in 1987, on far-reaching policy reforms intended to restore macroeconomic stability and improve efficiency of resource allocation and utilisation in order to accelerate sustainable economic growth. However, though accelerating economic growth and restoring the developmental momentum remained principal policy objectives, it was also realised that poverty and related social problems should receive additional attention through the rehabilitation of the social infrastructure and financial support for well targeted projects. 1.1.2 During the consultative Group meetings, which were held in 1992 and 1993, the donors emphasised the need to put more resources for poverty alleviation in Uganda. Concerns were expressed about the needs of the population for basic services such as health, education, clean water, and sanitation facilities. The Government of Uganda (GOU), therefore, identified viable programmes and income generating activities, which could assist the vulnerable groups, such as, women, widows, demobilised soldiers and retrenched civil servants. 1.1.3 In 1992, the GOU requested the ADB Group to contribute to its Social Action Programme which was intended to alleviate poverty in Uganda and in particular in the districts of the North, North Eastern, West, South Western and Luwero Triangle. These were, at the time, areas with high incidence and severity of poverty and which were gravely affected by the civil war. At project appraisal in 1993, about 96% of Uganda’s population lied in rural areas, and 55.2% of the population lived below poverty line (Ushs.16,400 or US$15). In response to Government request, the ADB Group appraised the Poverty Alleviation Project (PAP) in April 1993, and approved the loan of UA 9.21 million (Loan No. UGA/PVA/93/94) in August 1993, signed in October 1993, and became effective in June 1994. Thus, poverty reduction was the country's priority and was also relevant to the Bank's Assistance Strategy of sustainable equitable growth and poverty reduction. 1.1.4 The project implementation was the responsibility of the Income Generating Support Unit (IGSU) housed in the Office of the Prime Minister (OPM) and supported by four Project District Area Offices (PDAOs) and Intermediary Entities (Ies) - mostly NGOs. The National Project Steering Committee (NPSC) was to oversee the project operations and provide policy and operational guidelines. The IGSU was responsible for the overall co-ordination, day to management and administration of project finances and monitoring and evaluation of project activities at the national level. On request from the GOU, IGSU will manage credit components of other ADF financed projects to deliver the credit to target clients in the second phase of PAP. These projects are the Uganda Southeast and Southwest Integrated Watershed Management Project, and the Northwest Smallholder Agricultural development Project. 1.1.5 PAP was the first of its kind to be financed by the African Development Fund (ADF) in Uganda and also one of the first of its nature in Bank Group operations. Also, PAP was the first ADF-financed project, which heavily relied on NGOs in delivering micro-finance services to the poor in project target areas. The project used a participatory approach, which relied on involvement of beneficiaries in all stages of micro-project development. The Project Completion Report (PCR) was prepared in 1999 by the Bank's experts. However, the PCR did not give an

2

independent assessment of the efficiency of the Bank's activities and development effectiveness of the project, and its impact on the beneficiaries, with a view to assessing their sustainability. The PCR also did not adequately assess some aspects relating to the quality of the project including quantitative analysis of socio-economic indicators. Hence, this PPER represents an independent review that supplements the findings of the PCR and through such a review draws lessons from the experience, for the purpose of improving future Bank operations in micro-financing. 1.2 Project Formulation 1.2.1 Overall, the project identification, preparation and appraisal focused on the appropriate issues relating to the poor and the vulnerable population in Uganda. At appraisal, 52.2% of the total population lived below poverty line and less than 1% of the poor population had access to institutional financial services. Thus, the project strategy for providing micro-finance services for the poor and vulnerable was sound. Also at appraisal, lack of an enabling policy environment for micro-finance was a major constraint in Uganda. Therefore, the project focused on creating an environment sufficiently flexible to attract a wide range of Ies to deliver micro-finance services in rural areas, and adoption of a lending interest rate of 22%, which is consistent with international best practices for poverty reduction programs. The project also focused on development of financial infrastructure including information, training and regulatory and supervisory systems for Ies and PAP staff to support, strengthen and ensure the sustainability of these institutions and PAP itself. Furthermore, institutional development was to be provided to ensure that there are viable financial institutions in place to deliver a diversified menu of products and services attractive to the poor. Above all, the project's social intermediation was a vital component for increasing the capacity of the poor to access and productively use micro-finance services. Social intermediation envisaged in PAP included investments in awareness building, information dissemination, basic skills training, and social mobilisation for group formation. 1.2.2 At appraisal time, the GOU was implementing the Program for Alleviating Poverty and Social Cost Adjustment (PAPSCAD), and the Community Action Program (CAP) projects, both of which aimed to support the poor and most vulnerable communities, focusing on the provision of basic social infrastructures. However, it was decided that building of basic social infrastructures should be left to sector projects and that efforts be directed to financing income and employment generating activities that would address the priority needs of the poor. Thus, GOU and the Bank Group recognised that providing micro-finance services for the poor was a critical element for poverty reduction strategy. And that, without permanent access to institutional micro-finance, most poor Ugandans who also lack basic skills would not actively participate in and benefit from the on-going development activities. 1.2.3 Although the formulation of the project focussed appropriately on poverty, which is the overarching goal of both the GOU and the Bank Group, it had some deficiencies. Critical was the omission of a baseline study to identify important performance indicators for monitoring and evaluating the impacts of the project, which resulted in lack of monitorable indicators for comparing before and after project poverty situation.. This deficiency was attributed partly to lack of experience in the Bank then to competently plan an evaluation design, and partly to the urgency of launching PAP to address the pressing negative impacts of civil war and impacts of structural adjustment program in Uganda. 1.2.4 The formulation of the project was also deficient in analysis of institutional and managerial issues. These deficiencies contributed to the delay of project implementation arising from over ambitious targets set during appraisal, and gross over-estimation of the capacity of Intermediary Entities (Ies) to deliver financial and non-financial services to the poor. As a result, resources needed for institutional capacity building for both the staff of IGSU and Ies were

3

underestimated. Delays in implementation also arose from delays in procurement of goods and services and disbursement of loans due to the Bank's lengthy internal approval procedures, and inadequate understanding by the borrower regarding Bank’s rules and procedures for procurement and disbursement. However, when the Bank staff trained IGSU staff on Bank rules and procedures, subsequent delays did not occur. 1.3 Objectives and Scope at Appraisal (Logical Framework) 1.3.1 At appraisal, use of the Logical Framework Matrix was an up-front requirement of the Bank Group, but the matrices prepared in the project appraisal report (PAR) and PCR lacked essential components for an evaluation plan. A notable deficiency was the omission of measurable and monitorable indicators at the objective, output, and at goal levels. Specifically, targeting at appraisal lacked quantity and time measures, making it difficult to conduct objective monitoring (at the output level) and evaluation (at the objective level). 1.3.2 The Logical Framework Matrices in the PAR and PCR did not design activities with effective follow-up mechanism to verify what the Ies and the loan beneficiaries have learnt is being used, and the actual beneficiaries who have got loans. Moreover, there are a number of useful quantitative indicators at the goal, objective and output levels in the PCR, but these were not reflected in the log matrix in appraisal report or PCR. Hence, the need for a retrospective log matrix, which is presented in Annex 2 to this report as an improvement to that in the PCR, reflecting measurable targets. 1.3.3 The sector goal of PAP as stated in the PAR - “to assist in poverty alleviation” - is consistent with that in the Bank’s Country Strategy Paper (CSP). However, the project purpose in the PAR was re-formulated from "to provide affordable accessible credit scheme for the target groups in Uganda" to read "to develop human resources and institutional capital to enable the poor, especially, women in rural areas access effectively and productively financial services of the formal sector". The objective was re-formulated so that it is linked logically to the outputs and activities. 1.3.4 It was envisaged at appraisal that PAP would result to : (i) exposure of 40 PAP staff and 70 Ies to international best practices in micro-finance delivery; (ii) increased awareness among 26,000 clients on forma financial services and basic record keeping for micro-projects; (iii) improved access and efficient provision of savings, and credit services to 26,000 poor clients; (iv) reduced gender disparity in terms of access to credit and savings to women (60% of the clients would be individual or women groups); (v) creation per year of employment opportunities for the poor and the vulnerable rural communities especially women; and (vi) higher income and more diversified income sources, higher savings and consumption, better education and reduced poverty. 1.3.5 The major outputs envisaged at appraisal included:(i) IGSU supported by 4 District Area Offices established and delivering micro-finance services well; (ii) a NPSC established and operating well; (iii) a total of 70 Ies, 26,000 clients and 40 PAP staff trained in effective financial and social intermediation of micro-finance; (iv) a total of 40 technical staff and a technical advisor for PAP recruited; (v) a total of 14 vehicles, 8 motorcycles and office equipment procured for IGSU; (vi) about 77% of total project resources lent to 26,000 beneficiaries (15,600 women & 10,400 men) in 22 districts; (vii) more than 26,000 micro-projects financed in crop production; animal and fisheries; (viii) trade and small scale manufacturing; (ix) savings amounting to 20% of the total loan portfolio mobilized; and (x) loan loss of <10% and market lending interest rates used.

4

1.3.6 The principal inputs envisaged at appraisal were: (i) credit schemes to finance: small scale rural farming, bee-keeping, oil and grain milling, carpentry, bakery, brick-making, handicrafts, cloth manufacturing and trading; (ii) training and extension services to local communities; (iii) institutional support (provision of long-term technical advisor, short-term consultants and training). 1.3.7 Critical assumptions and risks at appraisal included:(i) adequate capacity of PAP staff, Ies and government extension staff; (ii) credit used effectively and sustainable credit programmes; (iii) credit used predominantly by the poor (no external interference); (iv) minimum rate of delinquencies; (v) good credit discipline developed; (vi) good management of the project; (vii) groups confident to borrow; and (viii) committed credible trainers available.

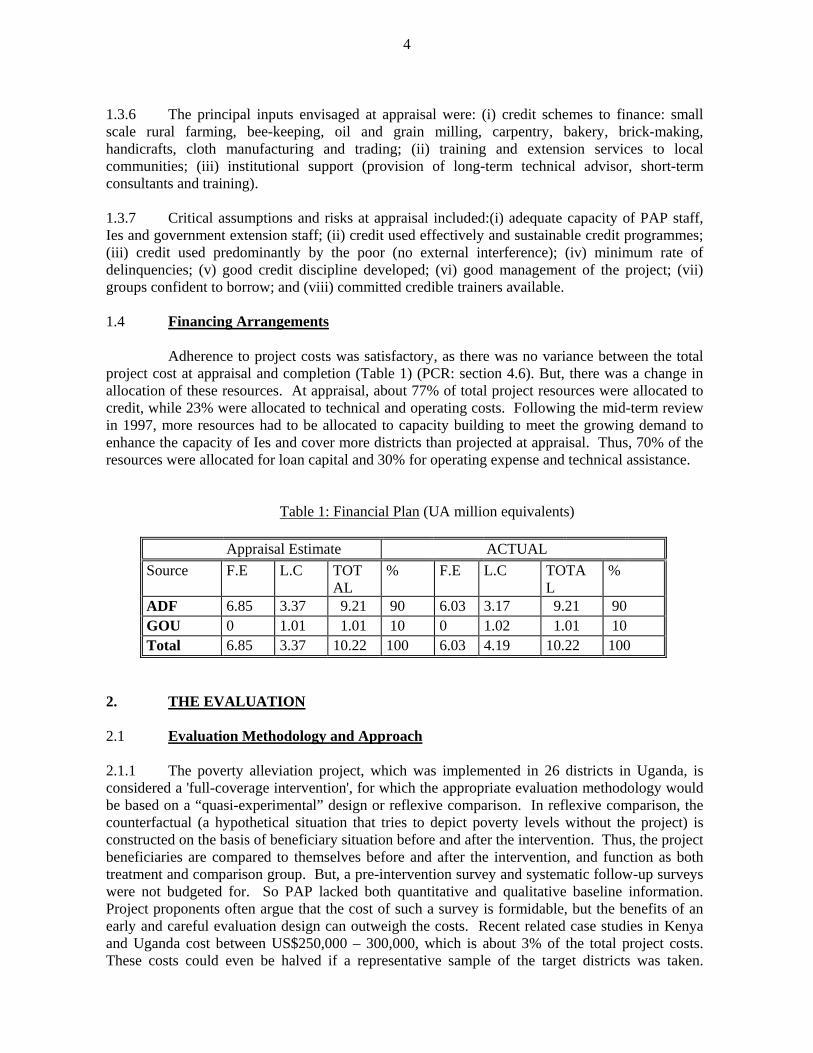

1.4 Financing Arrangements Adherence to project costs was satisfactory, as there was no variance between the total project cost at appraisal and completion (Table 1) (PCR: section 4.6). But, there was a change in allocation of these resources. At appraisal, about 77% of total project resources were allocated to credit, while 23% were allocated to technical and operating costs. Following the mid-term review in 1997, more resources had to be allocated to capacity building to meet the growing demand to enhance the capacity of Ies and cover more districts than projected at appraisal. Thus, 70% of the resources were allocated for loan capital and 30% for operating expense and technical assistance.

Table 1: Financial Plan (UA million equivalents)

Appraisal Estimate ACTUAL Source F.E L.C TOT

AL % F.E L.C TOTA

L %

ADF 6.85 3.37 9.21 90 6.03 3.17 9.21 90 GOU 0 1.01 1.01 10 0 1.02 1.01 10 Total 6.85 3.37 10.22 100 6.03 4.19 10.22 100

2. THE EVALUATION 2.1 Evaluation Methodology and Approach 2.1.1 The poverty alleviation project, which was implemented in 26 districts in Uganda, is considered a 'full-coverage intervention', for which the appropriate evaluation methodology would be based on a “quasi-experimental” design or reflexive comparison. In reflexive comparison, the counterfactual (a hypothetical situation that tries to depict poverty levels without the project) is constructed on the basis of beneficiary situation before and after the intervention. Thus, the project beneficiaries are compared to themselves before and after the intervention, and function as both treatment and comparison group. But, a pre-intervention survey and systematic follow-up surveys were not budgeted for. So PAP lacked both quantitative and qualitative baseline information. Project proponents often argue that the cost of such a survey is formidable, but the benefits of an early and careful evaluation design can outweigh the costs. Recent related case studies in Kenya and Uganda cost between US$250,000 – 300,000, which is about 3% of the total project costs. These costs could even be halved if a representative sample of the target districts was taken.

5

Appropriate evaluation design results to development of “a best practice” example for future projects, enhanced project quality-at-entry, and increased value to projects. Bank staff attribute the omission of baseline and follow-up surveys to the Bank’s lack of previous experience in the design and implementation of related projects. 2.1.2 The project carried out an impact evaluation study in 16 out of the 26 project districts in 1997. However, given that baseline information was lacking and the assessment was not a post-intervention or an evaluation of the entire project area, the PPER mission draws only partial qualitative information from the study. The GOU also commissioned national household surveys between 1993 and 1995, but due to sample size limitations, the data would need substantial adjustments and time before it could be used for poverty comparison in the PAP districts. Due to these limitations, the PPER mission used the 'Rapid Participatory Poverty Assessment (RPPA)' approach for the evaluation. The RPPA as an iterative, participatory research process was used to ensure involvement and consultation of a wide range of stakeholders of PAP through individual and/or focus group discussions. The mission used a list of open-ended questions to approach the stakeholders including the beneficiaries to solicit their views on PAP. In addition to meeting stakeholders in and around Kampala, the mission visited 10 of the 26 target districts: Mubende, Rakai, Kabale, Mukono, Pallisa, Kumi, Soroti, Katakwi, Apac and Lira.

2.1.3 The mission held discussions with the following key informants: (i) the OPM; (ii) Ministry of Finance, Planning and Economic Development (Borrower); (iii) Ministry of Agriculture, Animal Industry and Fisheries; (iv) Uganda Bureau of Statistics; (v) Ministry of Gender, Labour and Social Development); and (vi) the District Authorities. The mission also held discussions with , Ies/Micro-finance institutions (MFIs), clients, officials of commercial banks, the Private Sector Development Programme, the Economic Policy Research Centre, and Bank staff including the ADB Programme Officer in Kampala. The evaluation strategy also draws on secondary data from: (i) Project Appraisal Report (PRA); (ii) Borrower's and Bank PCRs; (iii) reports from the IGSU and its clients; and (iv) recent reports of NGOs, MFIs, and donors.

2.1.4 Using the Revised Evaluation Guidelines of the Bank Group (April 2000), the evaluation focused on the impact of PAP on the beneficiaries, and on the overall development in the sector as well as the sustainability of the project results. Due to lack of pre-intervention data and proper record keeping by the clients, no attempt was made to assess the outcome of the project in terms of income and consumption levels. Thus the evaluation focused on available measurable indicators including exposure of PAP staff and Ies to best practices of micro-finance delivery; access to credit and savings by clients; number of micro-projects developed; and number of women empowered. It also examined the financial and loan performance of the IGSU. It further reviewed the impacts of the institutional strengthening of the project on the performance of the IGSU. Lessons were drawn from the performance of IGSU, the GOU, the Bank and the beneficiaries. Thus, this PPER is based on assessment of the results of the Borrower's and Bank PCRs, and the PPER mission. The performance indicators (projected and actual) are given in the retrospective project matrix in Annex 2.

3. IMPLEMENTATION PERFORMANCE 3.1 Loan Effectiveness, Start Up and Implementation (Compliance with Loan

Conditions and Covenants, Procurement, Changes in Project Scope) 3.1.1 The loan was approved in August 1993, signed in October 1993 and declared effective in June 1994. Overall, loan effectiveness and start-up were satisfactory. All covenants and conditions stipulated in the loan agreement were fulfilled (PCR: section 4.1), but the borrower did

6

not comply with two conditions satisfactorily. Firstly, the borrower failed to reactivate the NPSC which upon establishment to oversee the project operations and provide policy guidelines, became ineffective and held only one meeting over the entire project period instead of the agreed monthly meetings. Secondly, the borrower did not follow the Bank’s procurement rules and bought several items including vehicles for PAP without the required no objection from the Bank, escalating the total cost allocated for capital expenditure from US$150,000 to US$640,000. However, these issues were adequately addressed during a visit of IGSU staff to the Bank Group Headquarters in March 1996, when the delegation met with the relevant Bank officials. 3.1.2 While most conditions were fulfilled timely, the recruitment of staff and the preparation of the operations manual were slightly delayed. The one-year delay in preparing the project promotional material and operational manual due to lack of project preparatory facility (PPF) delayed project implementation. The delay in staff recruitment and procurement can be attributed to weakness in project appraisal arising from over-ambitious targets set during appraisal, gross overestimation of the capacity of PAP staff and Ies, resulting in deficiency in resources for institutional capacity building. Later in 1997, a joint GOU/ADB supervision mission agreed to make necessary changes relating to procurement, disbursement and institutional arrangements. Thus, the project recruited eight more District Project Officers (DPOs); and attracted more Ies by increasing their commission from 10% to 15% (PCR: section 4.2.1). 3.1.3 The Bank's less frequent and inadequate supervision at the start of project implementation further contributed to these delays. Delays in implementation also arose from slow procurement of goods and services and disbursement of loans due to the Bank's lengthy internal approval procedures. Due to the delays cited above, the project did not meet its targets during the first two years of its implementation. Nevertheless, most of these problems were addressed in subsequent years and overall, the project implementation was satisfactory. The PCR in section 4.3.3 attributed this achievement to the satisfactory quality of preparation of PAP in terms of the project's unique approach to mobilise the poor through the bottom-up participatory approach, and using Ies for financial and social intermediation. 3.2 Adherence to Project Costs, Disbursements and Financial Arrangements Adherence to project costs was satisfactory, as there was no variance between the total project cost at appraisal and completion. The proposed disbursement at appraisal was UA 10.22 million, but this was later revised to UA9.68 million during a project mid-term review in 1997 against actual disbursement of UA 9.20 million (Disbursement Plan, Basic Data Sheet). However, disbursement was unsatisfactory especially in the first two years when only 41% of the projected US$4.6 million was disbursed. This delay was due to the Bank's lengthy and stringent internal approval procedures that took on average 35 days instead of the stipulated 14 days. While IGSU attributes these delays also to the misunderstanding between the Bank and borrower on the list of goods and services, the Bank feels that the delay was due to IGSU’s lack of understanding or compliance to Bank requirements. The use of a revolving fund disbursement method also contributed to these delays, as the bulky documentation involved in the revolving fund method would require more time to verify. However, disbursement improved substantially during the last three years of project implementation when the Bank Group trained project staff, indicating that training of project staff in procurement and disbursement procedures at the start of a project is vital. 3.3 Project Management, Reporting, Monitoring and Evaluation Achievements 3.3.1 According to the loan agreement for PAP, between the borrower and the Bank Group, the project implementation was the responsibility of the IGSU, which was housed in the OPM

7

(PPER: section 1.1.4). However, contrary to this condition, in May 2000 the Cabinet decided to transfer PAP from the OPM to the Ministry of Gender, Labour and Social Development. This anomaly was resolved by a high-level ministerial meeting held on 7th July 2000 under the Chairmanship of the Prime Minister. The meeting recommended to the Cabinet to change its decision to relocate PAP as this may result in ADB canceling the loan. Subsequently, the Cabinet endorsed the reversal of the decision on 23 August 2000. While this issue did not affect project implementation, the PPER mission feared that the transfer could risk the sustainability of PAP if left unresolved. 3.3.2 Overall, the project implementation was satisfactory despite its complex nature. The implementation of the project activities was carried out in accordance with the planned management structure and all the activities were managed satisfactorily. PAP contributed in developing micro-finance in Uganda and facilitated more than 25,000 poor people to access credit without collateral through use and strengthening of Ies as conduits for delivering services to the poor. Generally, the management of the credit delivery system by PAP-supported Ies was satisfactory relative to other international NGOs such as PRIDE, FINCA and FAULU which support activities mostly in urban areas, and have no significant presence in rural areas. 3.3.3 The low level of social development in Uganda is considered a major constraint on the sustainable expansion of micro-finance services. PAP’s strategy in social intermediation to improve the capacity of the poor in this regard was thus necessary and included: (i) awareness building on micro-finance and formal bank transactions; (ii) basic skills training and record keeping; and (iii) social mobilisation for formation of community and solidarity groups. 3.3.4 Despite the "good practice" example of PAP in developing micro-finance sector in Uganda, the PCR findings (PCR: section 4.1) indicated that both the IGSU and the Ies have a weak institutional capacity, and that this is a critical factor which delayed the implementation and performance of the project. There is a general lack of understanding of the best practices of micro-finance by Ugandan MFIs, NGOs and community-based organisations (CBOs). The PPER mission found that while many Ies lack skilled staff in accounting, finance and management, the majority lacks basic logistics, such as safe deposits, means of transportation, and secure facilities to operate from. Most Ies also lack capacity to expand the scope and outreach of services on a sustainable basis to most of the potential clients. Specifically, many Ies (i) lack capacity to leverage funds, including public deposits, in commercial markets; (ii) can not provide a range of products and services acceptable to the clients; and (iii) have inadequate network and delivery mechanisms to cost-effectively reach the poor in low populated areas. 3.3.5 Recent study in Uganda shows that of the 60 Ies collaborating with PAP, only 16 can be considered as viable and able to provide professional services that are sustainable. Viability is important from an equity perspective because only viable institutions can leverage funds in the market to serve a significant number of clients and contribute to broad-based development. Viability is also vital to be able to reach a large number of the poor, which in turn is essential to have significant impact on poverty reduction. 3.3.6 At appraisal, the aim was to establish a streamlined project implementation unit with a minimum number of staff while field operations would be mainly entrusted to the Ies. The creation of such a framework was based on the assumption that there was adequate capacity for the PAP staff, Ies identified and the existing Government extension staff to ensure smooth and successful implementation of the project (PCR: section 6.2.1). However, during implementation, it was realised that the administration and management requirements of the IGSU and Ies were under-estimated, resulting in inadequate staffing and skill mix, which seriously hampered its

8

capacity to deliver services. Thus, the number of project staff was increased and operating cost at completion was 30% of total project cost instead of 23% planned at appraisal. 3.3.7 The PAP also had some major institutional weakness in financial management as reported in the audit reports which the PPER mission reviewed. The IGSU attributed some of these shortcomings, especially, weakness in loan tracking to the Fund not approving a request by the unit in 1995 for a Management Information System (MIS) software costing US$3,000. The Fund denied the request, as the item was not on the approved list of goods and services for the Project. However, what IGSU needed was not just a software but a fully-fledged MIS. According to recent estimates for (PAP II), an MIS would cost more than US$200,000. In absence of an MIS the project operated a manual loan tracking system that is not only slow but also inefficient. The system lacked reliable portfolio (asset) quality measurements in terms of portfolio at risk, loan reserve ratio, and loan write-off ratio. Portfolio at risk ratio represents the percentage of the portfolio that is in danger of not being collected. The IGSU has no policy on loan write-off, or on insurance for clients against bad loans in event of death of clients and their next of kin, or natural calamity. The mistargetting and embezzlement of loan funds, which could not be readily traced can be attributed to weakness in loan tracking system (para. 4.4.3). Moreover, mechanisms to monitor benefits, (which was also weak) should have been integrated into MIS of IGSU. However, the IGSU will acquire an MIS and is now establishing a loan write-off policy. 3.3.8 The IGSU bases its cut-off period for determining portfolio at risk on the mode of loan cycle. For loans, which had a period of 1 year (for 1994 – 1999), all loans outstanding with 90 days or more past due is considered at risk. The bulk of PAP loans disbursed are in this category. For the current "loan cycle" methodology, which started in 1999 has a minimum loan period of 6 months and a maximum of 1 year and a monthly repayment. In this case, all outstanding loan balance with 30 days (one instalment missed) or more past due is at risk. The project has been ageing the outstanding loans with payments past due according to the following categories: 31-60 days, 61-90 days, 92-180 days, 181-365 days, 366-730 days, and over 730 days. 3.3.9 The ageing stretches up to 730 days (>2 years) because PAP did not write off any loan, and the PPER mission confirmed that these bad loans are still in the books of account. However, PAP has put in measures to improve the quality of its loan portfolio through shorter loan and grace periods, and staff and client training, and the MIS , which the RMSP will acquire will also improve monitoring and evaluation (M&E) of the project’s loan portfolio. 3.3.10 The Project's reporting on the implementation and auditing were satisfactory, but a review by the Bank Group of the Audited Accounts of PAP for the Periods ending 30th June 1998 and 1999 revealed some financial mismanagement by IGSU. The review shows that control over cash is loose and there is no proper safekeeping of project records, files and assets. To this effect, the Bank suggested to the Borrower to have PAP accounts audited by a private firm, and appoint urgently a new National Project Co-ordinator and Financial Controller. 4. PERFORMANCE EVALUATION AND RATINGS 4.1 Relevance of Goals and Objectives and Quality-at-Entry Assessment 4.1.1 The goal and the objective PAP with its participatory bottom-up approach are realistic and highly relevant to Uganda's National Poverty Eradication Action Plan (NPEAP), and the Bank's Assistance Strategy of sustainable equitable growth and poverty reduction. Given that by 1999, 44% of all Ugandans still lived below poverty line, poverty reduction remains the country's overarching goal for development strategy. The project goal of assisting in sustained economic

9

growth with poverty reduction in rural and urban areas was relevant to the country's macro-economic policy. Moreover, the project objective is also relevant and consistent with Uganda's NPEAP that aims to improve access to the poor, especially women to productive assets (land and credit), raising the return on these assets. 4.1.2 Most of the project’s clients are the rural poor and dependent on agriculture. This was relevant to Uganda's public sector reform including, the Plan for Modernisation of Agriculture, industrialisation, institutional and capacity developments including the decentralisation policy for economic growth to reduce poverty and improving efficiency and effectiveness of the public service delivery. The project's objective is consistent with Uganda's institutional framework for NPEAP that supports the empowerment of women, youth, and local committees and also encourages their participation in local development, social and gender equality. Most micro-finance initiatives in Uganda address women's practical needs, and over 60% of the beneficiaries of PAP were women. 4.1.3 The project's concern for environmental sustainability is directly related to the National Environment Policy (1994) and NPEAP which ensures that economic growth and poverty reduction efforts address efficient use of natural resources and prevent environmental degradation. The NPEAP also recognises that environmental degradation is both a cause and a consequence of poverty. Therefore, the environmental management plan incorporated in the design of PAP is relevant to the NPEAP. For example, the PAP exposed its clients to sound ecological principles (e.g. afforestation and soil fertility management) with clear guidelines to mitigate against adverse impacts of some micro-projects. In brick making, the pits dug for the clay have been refilled with compost manure, which enhanced soil fertility (PCR: para. 7.2.2). 4.1.4 As regards human resources development, one of the three major PAP activities focused on training of clients, Ies and PAP staff. This is consistent with NPEAP, which includes training, adult literacy and primary education as actions, which directly improve the quality of life of the poor. The project was also relevant to institutional development as set in the NPEAP. The project set up a micro-finance institution; facilitated access of the poor especially women to micro-finance services; and enhanced skills of the poor in banking and managing micro-projects. 4.1.5 While the goal and objective of PAP are relevant to NPEAP, the project's quality at entry lacked rigour to allow for credible benefit monitoring and impact evaluation. In particular, the project did not provide for pre-intervention study that would have covered a detailed social analysis of target groups including, clientele needs, demands, and adsorptive capacity. Better analyses in this regard should include benchmark surveys to identify key performance variables such as beneficiaries' income and consumption, assets, nutrition, and other social indicators, which would be tracked annually and analysed at the midterm review and upon project completion. 4.1.6 Although PAP's emphasis was on empowering women, gender analysis was marginal at appraisal. Gender analysis is critical in a poverty alleviation project particularly for : (i) work activities differentiated on the basis of gender; (ii) delivering of credit in areas where the legal rights of women to get credit are constrained through customs and laws; and (iii) organisation of groups to design and implement projects in areas where the roles of men and women are rigidly defined. 4.1.7 The project preparation lacked rigour in the framework for monitoring and evaluating the benefits of the project. While the project appraisal used the logical framework matrix, the use of performance indicators, assumptions, pre-conditions and risks was marginal. Indicators used in the appraisal report emphasised on quality, but were not precise in terms of quantity, time, place or

10

cost. Targeting at appraisal means putting numbers and dates on indicators, and this is important if the monitoring (at the output level) and evaluation (at the objective level) are to be carried out objectively (Annex 2). The project quality-at-entry was also deficient in formulating delivery mechanisms for micro-finance services. And, the project did not adequately analyse the capability of IGSU and the Ies to deliver services in ways that are commensurate with the adsorptive capacity of the clients. 4.1.8 As for policy environment, when PAP was appraised there was no enabling policy environment for micro-finance, and it was anticipated that PAP would accumulate additional resources to cover its operating cost by depositing loan-able funds in interest bearing accounts. This was not possible, as the laws in Uganda would not allow this. 4.2 Achievements of Objectives and Outputs (Efficacy) (a) Policy Goals 4.2.1 The main goal of the GOU at the time of appraisal was to put the economy into the path of economic recovery program to achieve economic growth and poverty reduction by supporting income and employment generating activities undertaken by the poor and the most vulnerable groups. Although Uganda continues to make progress in consolidating macroeconomic stability and in furthering structural reforms, policy goals of rapid economic growth and poverty reduction were not achieved. While Uganda still remains a very poor country, the project on its part achieved its goal of assisting in poverty reduction through increasing beneficiary income and propensity to save. 4.2.2 Experience in Asia shows that early micro-finance projects failed to make significant contribution to poverty reduction because of their limited outreach. This is also true for Uganda where a recent study shows that only 1.5% of Uganda's poor population (which is 44% of Uganda's total population) have access to formal financial services provided by approximately 95 MFIs. Of the total 146,536 clients reached by these MFIs by 1998, 26,000 clients accessed PAP's services. Thus, much as PAP contributed to poverty reduction among its clients, the limited outreach to the poor by PAP and other MFIs had little positive impact on national poverty, and mechanism still lacks for many MFIs to sustain this impact beyond the project period. Poverty reduction requires continuos access to a broad range of financial services, not a one-time access to loans. 4.2.3 The limited outreach to the poor by financial services in Uganda can be attributed to a number of major problems. Firstly, Uganda has among the lowest gross domestic savings in Africa. In 1997, the ratio was 8.6% against 16.9% for the continent. This situation could partly be due to inadequate financial infrastructure including, legal, information, and regulatory systems for financial institutions and markets. Only 5% of Uganda’s population own bank accounts (i.e. 1.2 million out of 11 million who are above 15 years of age). This in turn can be attributed to lack of a clear policy and regulatory framework in Uganda to guide the provision of financial services to micro entrepreneurs, and innovative savings technologies that would encourage even the poorest to save. Without domestic savings, the country is forced to depend on external credit, and this deepens the level of poverty in the country.

4.2.4 Secondly, while the Financial Institutions Statute (FIS) of 1993 allows formal banking institutions to provide financial services to the whole country, its overall framework is not conducive to most MFIs. Generally, the rural poor are considered risky borrowers and costly to service, and to address these issues PAP triggered the preparation of a Micro-finance Policy. But, most of the PAP-assisted Ies will not be regulated by the new law or supervised by the Bank of

11

Uganda (BOU) that regulates Banks, Credit Institutions and Micro-finance Deposit-taking Institutions (MDIs). The Ies fall under non-deposit taking institutions such as credit-only NGOs and small member based groups mobilising subscriptions from members. 4.2.5 Thirdly, the limited outreach to the poor by the formal financial institutions and the MFIs is another impediment to Uganda's financial sector growth. Recent studies show that these institutions are concentrated in major urban areas, and there is no leverage between the informal and formal financial institutions to increase funds available for lending to the sector. Over 80% of Ugandan population live in rural areas, but only 15-20% of the MFIs is found in rural areas. Also, private sector MFIs are unwilling to invest in social intermediation which enables the poor to access effectively the financial services of the formal sector. This is due to the costly of such investments. Increased outreach requires supporting social intermediation on a large scale. 4.2.6 Fourthly, formal banks and the MFIs are biased towards financing agricultural enterprises. Agricultural growth significantly influences rural financial market development, accounting for about 42% of the country's GDP, but it is not adequately financed. Statistics of credit disbursements to various sectors of Ugandan economy between 1988 and 1996 show a decline of 33.4% in agricultural financing and an increase of 19% in trade and commerce financing. During 1998, the actual share of agriculture financed activities by MFIs in Uganda was only 21%. The insufficient investments in physical infrastructure (especially irrigation; roads; electricity; and support services for marketing, business development, and extension) continue to increase the risk and cost of micro-finance and particularly discourage private investments in the delivery of financial services on a significant scale. Thus, unless the MFIs begin targeting the poor rural majority with increased agriculture financing, the prospects of continued economic growth and poverty reduction through modernisation of agriculture will fail. (b) Physical Outputs

4.2.7 Generally, the projections for most physical objectives (outputs) were satisfactorily achieved. At appraisal, the project aimed to finance more than 26,000 micro-projects. Although the benchmark for the lines of credit was not set at appraisal, a total of 26,636 micro-projects were financed: crop production (35.4%); animal and fisheries (26.1%); trade (27.4%); small-scale manufacturing (6.9%; and others (4.1%). The highest proportion of the credit went to agriculture, shattering the myth that agriculture is not financially attractive to MFIs. PAP reports, the PPER and other Bank missions show overall increase in crop production, milk output, and poultry production. (c) Financial Targets 4.2.8 The project's analysis of financial performance at appraisal was unsatisfactory. The analysis of project viability and its operational sustainability was too simplistic and largely qualitative. The project did not set financial targets in terms of financial viability, cost recovery, and return on investment etc. Thus, key ratios such as loan loss reserve ratio, self-financing ratio, and levels of accounts receivable could not be quantified to assess, for example, achievements in levels of self-financing of investments. However, PAP assessed its loan performance on the basis of 92% recovery rate and loan loss provision of less than 10%, which are the standard set rates by micro-finance institutions in the region. The project was able to maintain these rates satisfactorily, making PAP’s performance far better than other government-supported micro-finance projects such as “Entandikwa” and EU-financed Micro-finance project, which had low recovery rates of 20-40%.

12

4.2.9 At appraisal the viability of PAP and its operational sustainability was not tested, but the PCR estimates that the operating cost ratio was about 30% to average loans outstanding. However the portfolio at risk remains high, given the nature of clients and risks associated with providing financial services to remote areas and insecurity prone areas. 4.2.10 Although the project increased its interest income and loan portfolio by 60% (at UA 3.38 million), the project incurred a deficit in the 5-year project period due to the heavy expenditures on institutional development, technical assistance and operating cost. However, the shortfall was financed from the ADF resources since the government contribution was not sufficient to cover this project operating cost. At appraisal it was anticipated that PAP was to achieve self-sufficiency after project completion of the first phase. Sustainability analysis of RMSP shows that if the loan default rate remains less than 10%, and the loan portfolio continues to earn an interest of not less than 12% per annum, RMSP will reach the break even position in year 2004 and generate a profit of US$420,000, with self-sufficiency rate of 126%. This scenario simply shows that viability and sustainability are a long-term plan that could not have been achieved within PAP's 5-year implementation, rather it requires a transformation process of between 5 to 8 years. Even then, RMSP will need external financial support for capitalisation and operating expense on declining bases. 4.2.11 The inadequate review and conduct of financial performance is attributed to the absence of a computerised loan tracking system. Thus, the loan monitoring system and financial records used by PAP remained fragmented and too simplistic to provide a reliable analysis of loan and overall financial performance. (d) Institutional Development Objectives 4.2.12 It was planned at appraisal that a viable micro-finance institution would be established to provide effective pro-poor financial and non-financial services including policy guidance. This output was realised. The IGSU supported by 4 PDAOs was established (albeit with a slight delay) and working well. It also supported the establishment of the Association of Rural Micro-finance Institutions (ARMI) to provide policy guidance, and the Association of Micro-enterprise Financial Institutions of Uganda (AMFIU) to supervise Ies. The ARMI, which represents indigenous grassroots CBOs and NGOs and MFIs mostly collaborating with PAP, provides fora for participation/consultation gauging consensus among stakeholders on key design issues during preparation and appraisal of the RMSP. 4.2.13 PAP was to establish the NPSC to oversee the project, and to provide policy and operational guidelines. The NPSC was established, but was ineffective as it only held one meeting in the entire project life instead of the planned monthly meetings, constituting a direct breach by the borrower on loan agreement. Attempts by the Fund to remind the borrower to re-activate the committee failed. 4.2.14 The project was also to strengthen the capacity of 40 PAP staff and 70 Ies in best practices of micro-finance administration and delivery to the poor, and to empower up to 26,000 clients in micro-finance services. By 1998, a total of 60 Ies, 25,877 clients and 48 PAP staff and 88 stakeholders were trained, thus satisfactorily achieving appraisal projections. The joint GOU/ADB supervision of PAP in 1997 revealed that PAP staff capacity at appraisal was underestimated and this prompted recruitment of 8 more DPOs. PAP was also to strengthen IGSU with 14 vehicles and 8 motorcycles and office equipment. This target was achieved, and the recruitment of additional DPOs necessitated procurement of 3 vehicles and 5 motorcycles above appraisal projections.

13

(e) Social Objectives and Targets 4.2.15 Overall, the project has achieved its social objectives and targets set at appraisal. The project's objective as stated at appraisal was to develop human resources and institutional capital to enable the poor; especially women in rural areas access effectively and productively financial services of the formal sector. At appraisal, the project's outreach was to reach 26,000 clients: women, widows, orphans, retrenched civil servants, demobilised soldiers, youth and the disabled. Although the project did not set outreach benchmarks for the various target groups, the project planned to reach, 60% were to be women. The project was able to achieve this target at project completion with an increase of 2% above projection, reflecting a clear reduction in gender disparity in terms of access to financial and social intermediation by women. The loan recovery rate for women was 95% compared to 88% for men. The PAP, its Ies and clients have shown that the poor (poor women in particular) are creditworthy and financial services can be provided to and accessed by the poor on profitable basis at low transaction costs without physical collateral. Moreover, PAP's micro-finance services have triggered a process toward broadening and deepening rural financial markets. This development in micro-finance in Uganda has set in motion a process of change from activity that was mostly subsidy dependent to one that can be a viable business. 4.2.16 In a recent survey conducted by PAP, 75% of females interviewed indicated that PAP interventions had contributed to their empowerment in terms of overall positive impact on their lives. About 80% of the women indicated economic improvements, and 54% pointed out that PAP enhanced self-reliance, improved decision making, financial management, interaction with local authorities, awareness levels and social networks. 4.2.17 The project was also to mobilise savings amounting to 20% of the total portfolio of Ushs 8.931 billion for increased investments and economic growth. At project completion, PAP mobilized Ushs 3,435 saving accounts amounting to 13.4% of the total loan portfolio. This translates to 60% increase of beneficiary propensity to save. Given that Uganda has among the lowest gross domestic savings in Africa, this is probably a more important achievement of micro-finance in the country than the expanded outreach in access to credit noted above. The achievement has shattered the myth that poor households can not save, and proved that savings can be mobilized from poor households to realise the savings the country badly needs. It also raised awareness of the rural poor population on the services and usefulness of the formal banking system. (f) Environmental Objectives 4.2.18 According to the Bank classification of projects in terms of environmental impacts, PAP would fall under category II; most of the micro-projects financed being agriculture, small-scale manufacturing, trade and services. This category of projects requires some environmental analysis and is assigned to projects whose impacts are less significant and not as sensitive, numerous, major, or diverse. Few of the impacts are very well known and mitigation measures can be more easily designed. At preparation and appraisal, no environmental impact assessment (EIA) of the project was undertaken. Therefore it was not possible for the PPER mission to evaluate environmental impacts of the project without baseline information. 4.2.19 The potential impacts of the project would include deforestation and soil erosion arising from farming practices. In the case of brick making, the pits dug for clay making could be hazardous to human beings and livestock that can easily drown in water that often fills such pits after a rainfall. If the pits are not refilled with soil, they can become breeding grounds for vectors of environmentally related diseases such as malaria.

14

4.2.20 Although formal EIA was not undertaken. The project exposed its clients to sound ecological principles (e.g. afforestation and soil fertility management) with clear guidelines to mitigate against adverse impacts of some micro-projects (PCR: section 7.2.2). The brick making enterprises led to improved housing conditions with a possible improvement of human health. (g) Private sector Development Objectives 4.2.21 Given the increasing potential for the private sector to profitably and efficiently provide micro-finance services, PAP attracted and strengthened 60 Ies to expand financial and non financial intermediation to the private sector. Through these Ies, PAP accessed about 26,000 micro-entrepreneurs, all of which are in the private sector. PAP has thus contributed significantly to the development of micro-finance industry in the private sector. Moreover, the project helped establish ARMI and AMFIU. Currently, ARMI is a forum for policy dialogue and a voice of the private sector to influence government policy in micro-finance, while AMFIU helps IGSU to supervise Ies. 4.2.22 PAP's institutional capacity building component is yet an important strategy for sustainability and expanding outreach to the private sector. Strong Ies with good governance are required to provide quality services to the poor on a permanent basis. Thus, PAP aims to strengthen Ies with commitment to develop capacity to: (i) mobilise resources in the market, including public deposits, to meet its own resources; (ii) provide products and services that are attractive at minimal transaction costs to the clients and the institution itself; and (iii) offer competitive prices to the clients. 4.2.23 PAP emphasises on strengthening the financial viability of Ies as a critical requirement for outreach. The institutional services of PAP to the Ies and its clients in the private sector include: (i) delivery of training; (ii) development of a diversified menu of products and services attractive to the poor; (iii) procedures and financial technology for reducing transaction costs through solidarity groups. 4.2.24 As part of the on-going privatisation process in Uganda, the Small and Micro Enterprise Policy Unit in the MFPED, in collaboration with the AMFIU, ARMI and donors active in the sector, undertook a number of studies to review the current status and operations of Rural Financial Institutions and their institutional arrangements. A key finding of these studies is that a number of Government supported micro-finance projects are disrupting the micro-finance market by introducing subsidies and do not follow industry best practice principles. Also, it was found that their clients took these loans as political handouts, which need not to be repaid. This is particularly true for the Government supported program of ‘Entandikwa’, which typically had very low recovery rates of 20-40%. The studies recommended that the Government leave the sector for private practitioners who have comparative advantage in delivering micro-finance services. 4.2.25 Furthermore, in the light of PAP's performance the study recommended that the IGSU which has managed and continue to manage PAP be transformed into a Government owned Company Limited by Guarantee (and not shares), and be given the responsibility of as a central apex organisation for wholesaling funds to MFIs, as well as the co-ordination of their activities. Besides wholesaling funds to MFIs, the IGSU is expected to build the capacity in the industry. Being registered as a company limited by guarantee run on commercial principles will also provide a window for private sector investment (domestic and international) and could serve as a Government arm to build up a pool of funds for lending to MFIs. It is expected that the profits generated by MSC will be re-invested to ensure operational and financial self-sustainability.

15