1. 2 presentation to investment analysts’ society 3 rd /4 th march 2004

TRANSCRIPT

1

2

Presentation toInvestment Analysts’

Society

3rd/4th March 2004

www.liberty.co.za

3

Operating climate

• Increasing compliance and regulatory requirements

• Low interest rate/low inflation environment

• Strengthening of the Rand• Volatile investment markets• Risk averse investors• Perception of industry

4

Operations

5

Liberty Personal Benefits -market share

• Strong Excelsior investment product sales• Property-backed products very popular• Risk product launched – Lifestyle Protector R120 million sales since launch

6

Liberty Personal Benefits –average recurring premiums

All officesLarge officesLiberty Personal BenefitsLPB as % of all officesLPB as % of large offices

30 Sept2003*

Rm

31 Dec2002Rm

%Change

2 1412 8436 796316,2

%238,1

%

2 2982 7546 443280,4

%234,0

%

(735

)

* Source: LOA statistics

7

Liberty Personal Benefits

• Represents 70% of total business based on value of liabilities (low percentage smoothed bonus business)

Focus on:• Integration of Healthcare operations• Restructuring of operations• Customer service and costs• Implementation of FAIS legislation• Partial commission uncapping• Further leveraging channel capabilities

8

Liberty Corporate Benefits

• 9% reduction in headcount• Building on packaged product model• Focusing on service delivery• Risk margins maintained (despite

HIV/AIDS)• Standard Bank opportunity• Small pension fund audit exemption

withdrawal

9

Liberty Corporate Benefits(continued)

• IEB purchase price: R130 million• Smooth integration to date• 2-3 years to rationalise fully• Efficiency opportunity• Current performance approximating

expectations

10

Consultancy

• Agency Division– Introduction of graduated managers from

the Academy– Additional branches created

• Franchise Division– Elimination of non-producing franchises– Productivity enhanced

11

Consultancy(continued)

• Broker Division– Expanded number of supporting brokers– Gauteng focus– Administration hubs provide a higher level

of service

• SBFC– Increased manpower – benefits in 2004– Consumer consultants strategy

12

Consultancy(continued)

• Legislation– FAIS implementation– Commission de-regulation– FICA implemented

13

Properties

Portfolio value (Rm)Comprising: Office buildings (%) Shopping malls (%) Hotels (%) Other (%)

2003 2002 %

Change

10 449,8

20 65 12

3100

9 601,8

22 64 11 3

100

9

5 year compound annual bonus rate to RA policy- holders of 11,6% vs headline CPI of 5,2%

14

Properties (continued)

• Property sales amounted to R150,1 million in 2003

• Liberty Midlands Mall completed in 2003 - valued at R325 million

• 50% of Greenacres Shopping Centre acquired for R150 million

• Vacancies at 31 December 2003: 13,9%(2002 : 12,1%)

15

STANLIBTotal assets under management

(excluding common assets)

Life fundsSegregated fundsUnit trustsStructured products and other

Money market as % of total

59554024

17814%

53482919

14911%

1215382619

2003Rbn

2002Rbn

%Chang

e

16

STANLIB(continued)

• Net inflows positive R12 billion• Investment performance mixed:

– Good fixed interest performance– Balanced portfolios underperformed median

by 1% to 2%– Returns generally acceptable in absolute

terms

• Normalised earnings up 4% to R136 million

17

STANLIB(continued)

• Integration costs and other once-off costs higher than expected

• Staff numbers reduced by 98 people (net)• Annualised cost saving of approximately

R30 million• STANLIB brand now well-established in

both retail and institutional markets• Looking for improved investment

performance

18

ErmitageAssets under management

Hedge fundsLong-only fundsMoney funds

Third party funds as % of total funds

1 292,71 059,5

600,32 952,5

41%

806,8791,6667,3

2 265,7

44%

6034

(1030

)

2003US$m

2002US$m

%Change

Operating profit up 117% in Pounds Sterling

19

The year in numbers

20

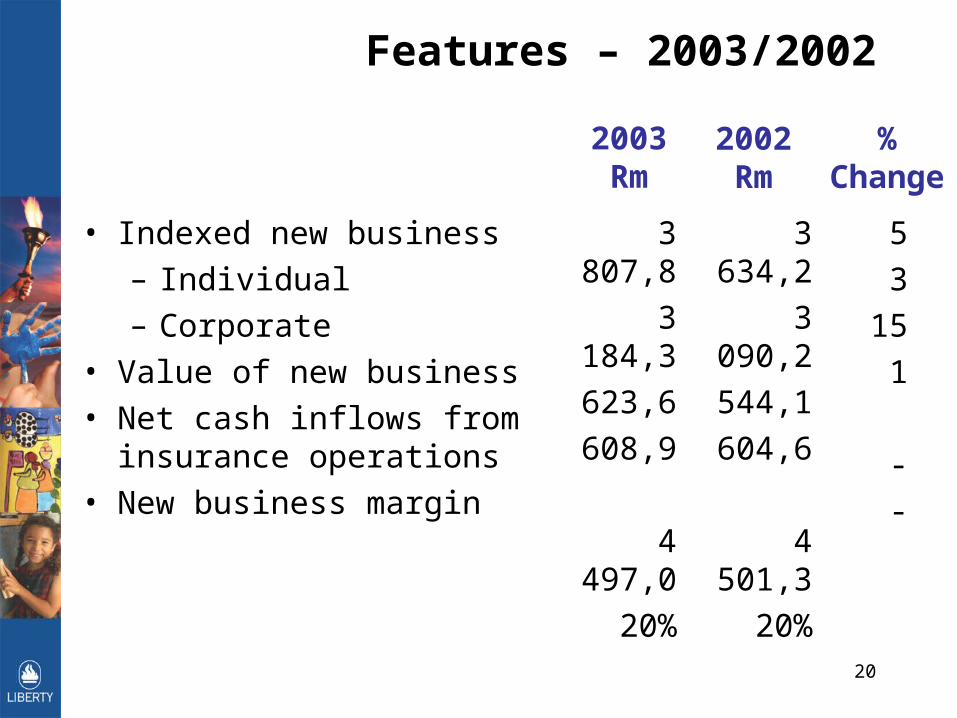

Features – 2003/2002

• Indexed new business– Individual– Corporate

• Value of new business• Net cash inflows from

insurance operations• New business margin

3 807,83 184,3

623,6608,9

4 497,020%

3 634,23 090,2

544,1604,6

4 501,320%

53

151

--

2003Rm

2002Rm

%Change

21

Features – 2003/2002(continued)

• Headline earnings per share (cents)

• Headline earnings per share pre AC 133 (cents)

• Final dividend per share• Embedded value per

share: (Rand)• Capital adequacy

requirement (times covered)

346,4

359,6

116,0

57,58

2,6

391,5

391,5

116,0

55,28

3,0

(11

(8-

4

2002%

Change2003

)

)

22

Headline earnings

Operating profit from insurance operations netof tax

Revenue earnings – shareholders’ funds

Preference dividendHeadline earningsHeadline earnings

pre-AC 133

2003Rm

2002Rm

%Change

)

)

719,5

324,8 (95,2949,1

985,5

889,1

261,6 (81,9

1 068,8 1

068,8

(19

24 16(11

(8

)

) )

23

Operating profit from insurance operations

Operating profit from insuranceoperationsBefore AC 133 adjustmentAC 133 adjustment

2003Rm

2002Rm

%Change

• 2002 includes releases from the life fund of approximately R350 million after tax• Improvement in weighted policyholder investment portfolio in 2003• Implementation of AC 133

719,5755,9(36,4

889,1889,1

(19(15

)

))

24

Investment returns(Weighted average of equity, managed

and foreign assets portfolios)

25

Expenses

Total group expensesSubsidiariesCompany expensesInsurance expensesIndividualCorporate Benefits

2003 2002 %

Change

1 860,9(381,8

1 479,11 281,8

935,1346,7

1 690,9(462,6

1 228,31 150,6

864,4286,2

10(1720118

21

) ))

*Includes IEB costs of R33 million

*

26

Expenses – cost per policy

Renewal cost per policyincreased/(decreased) by

Acquisition cost per policyincreased/(decreased) by

2003%

2002%

Significant non-recurring expenses incurred in 2003

6,5

7,2

(1,6

(1,3

)

)

27

Non-recurring expenses

• Non-recurring expenses of R111,3 million

in 2003– Retrenchment and discontinued salary costs– Previously incurred corporate activity costs– Pension fund provision– Post-retirement medical liability increase– Retention bonuses– Non-capitalised renovation costs– Impairments and other provisions

28

Revenue earnings – shareholders’ funds

Financial services operationsListed investmentsOther

2003Rm

2002Rm

%Change

199,932,992,0

324,8

159,639,962,1

261,6

25(184824

)

• Electric Liberty investment portfolio trading profit of R47 million in 2003• Liberty Ermitage headline earnings of R43 million up 54%• Higher cash balances and preference shares increased other earnings

29

Future earnings

• International Accounting Standards• Stochastic modelling of investment

guarantees• Investment returns impact 10%

entitlements

30

Embedded value

Shareholders’ fundsNet value of life business

in-forceFair value adjustmentTotalEmbedded value per

share(Rand)

2003Rm

2002Rm

%Change

8 782,2

6 493,8540,9

15 816,9

57,58

8 588,1

5 700,4838,1

15 126,6

55,28

)

2

14(36

5

4

31

Fair value adjustment

Liberty Group PropertiesLiberty Ermitage JerseySTANLIBCarrying value of in-force business acquired from Investec Employee Benefits

2003Rm

2002Rm

216,0140,0306,9

(122,0540,9

240,0190,4407,7

838,1

)

• Liberty Ermitage multiple reduced from 15 to 10• STANLIB valued at approximately R1,4 billion

32

New business – percentage increase

RecurringSingleTotal

Index

IndividualBusiness

%

CorporateBusiness*

%

Total

%

6(7(4

3

16347

15

633

5

))

*Excludes IEB business acquired

33

Market share individual business

(including Charter)

Individual recurring Individual singles

30 Sept2003

%

31 Dec2002

%

23,522,4

23,620,2

• Sales force productivity• Independent broker support• Investment performance• Property portfolio• Lifestyle protector

Source: LOA statsplus Charter Life

34

Value of new business

Value of new business (Rm)New business margin (%)Individual (%)Corporate (%)

2003 2002

608,92022

8

604,6202211

35

Net fund inflows

Total premiums and inflowsunder investment contracts

Claims, policyholder benefits andpayments under investmentcontracts

Net fund inflows

2003Rm

2002Rm

%Change

18 121,8

13 624,8

4 497,0

16 415,1

11 913,84 501,3

10

14-

• Two investment only funds to STANLIB of approximately R700 million

36

Capital adequacy cover

Capital adequacy requirement (Rm)Times covered

3 402,7

2,6

2 856,6

3,0

2003 2002

Charter Life investment guarantees

37

Dividend

2003cents per

share

2002cents per

share

162

116

278

162

116

278

Interim

Final

38

When we last spoke…

39

Focus areas for second half 2003

• Improve service levels• Emphasis on cost reduction• Domestic operations/other market

segments and Africa• Renewed emphasis on people• Address capital situation

40

Since we last spoke…

41

Improve service levels

• Appointed MD Group Customer Service

– Alan Woolfson

• Appointed internal ombudsman• Launching staff initiative• Tracking system for complaints

42

Cost reduction

• Cost reduction initiated – second half 2003• Cost savings of approximately R75 million

for Liberty• Reduced net headcount

– Liberty: 135– STANLIB: 98

• General staff incentive scheme introduced based on cost reduction targets

• No real cost growth budgeted for 2004

43

Domestic operations/other market segments and Africa

• Some internal issues – – LPB restructure– IT centralised (again)– Finalised Healthcare integration into LPB

• Charter explores new opportunities (see next slide)

• Namibia life license• Stanbic Africa footprint offers future

opportunity• Canned future offshore expansion for now• Western Cape?

44

Businessas usual

New businessinitiatives

Charter Life2004

Customerservice

Cost management

Right people- right jobs

- Grow CC’s aggressively- Continue IFA’s, networking and Liberty Agency/Franchise

(Long-term repositioningstrategy)- LSM 5-8- Products - Administration- Marketing- Distribution

Charter Life – eventually doing something

45

People

• Four new board appointments• Appointed MD Charter Life – Bobby

Malabie• Appointed CEO STANLIB – Bruce Hemphill• Looking for marketing head• IEB staff integrated well• Employment equity remains an issue• Restructured STANLIB

46

Capital management

• More proactive capital management• Capital committee formed• Sold 2 million Edcon and 1 million GoldFields• Restructured and cleaned up portfolios• Overcapitalised – but

– BEE contingency– stochastic modeling– be patient!

47

In addition…

• Market uptick – thank heavens! • Financial Sector Charter signed

– Dedicated Exco member heading initiative– Implementation committee set up

• STANLIB BEE deal finalised• AC 133 implemented• Life product launched

48

Liberty Foundation – focus on education

• Mindset Network began broadcasting• Pilot programme initiated for Health

Channel and we continued with –– Liberty Learning Channel on SABC– Learn.co.za website– Liberty/Sunday Times ReadRight project

• Working closely with Standard Bank

49

Focus areas for next six months – nothing complicated

Continue -• to improve service levels• emphasis on cost reduction• focus on domestic operations/other

market segments and Africa• emphasis on people

50

Focus areas for next six months – nothing complicated

Continue –• monitoring capital position• Financial Sector Charter implementation

and in addition we will –• reposition brand• focus on product development

51

Focus areas for next six months – nothing complicated

Everything we do mustfocus on adding value forour customer

52

Panel

Myles Ruck Chief Executive

Andrew Lonmon-Davis Statutory Actuary

Deon de Klerk Chief Financial Officer

53