1 2006/07 annual report presentation to the select committee on economic and foreign affairs 20...

TRANSCRIPT

1

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

PRESENTATION TO THE SELECT PRESENTATION TO THE SELECT COMMITTEE ON ECONOMIC AND FOREIGN COMMITTEE ON ECONOMIC AND FOREIGN

AFFAIRSAFFAIRS

20 FEBRUARY 2008

2

PRESENTATION CONTENTPRESENTATION CONTENT

Economic Contextdti Strategic Objectives2006/07 Achievements and Progress Six Year Expenditure ComparisonAnalysis of 2006/07 Under ExpenditureAnalysis of current MTEFYTD Expenditure – 31 August 2007Conclusion and challenges

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

3

ECONOMIC CONTEXTECONOMIC CONTEXT

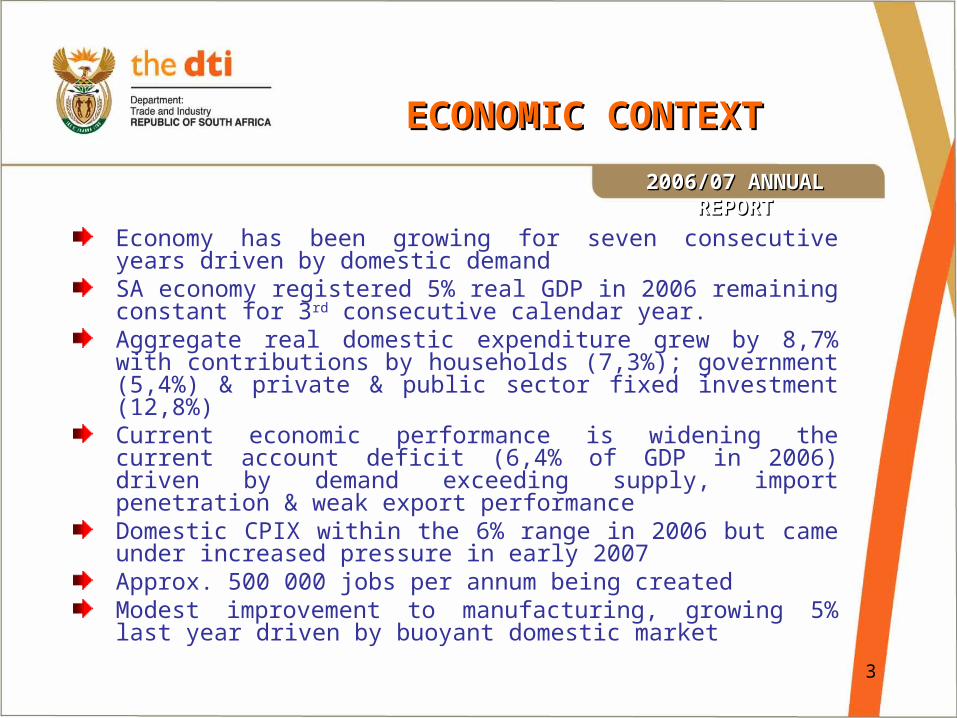

Economy has been growing for seven consecutive years driven by domestic demandSA economy registered 5% real GDP in 2006 remaining constant for 3rd consecutive calendar year.Aggregate real domestic expenditure grew by 8,7% with contributions by households (7,3%); government (5,4%) & private & public sector fixed investment (12,8%)Current economic performance is widening the current account deficit (6,4% of GDP in 2006) driven by demand exceeding supply, import penetration & weak export performanceDomestic CPIX within the 6% range in 2006 but came under increased pressure in early 2007Approx. 500 000 jobs per annum being createdModest improvement to manufacturing, growing 5% last year driven by buoyant domestic market

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

4

ECONOMIC CONTEXTECONOMIC CONTEXT

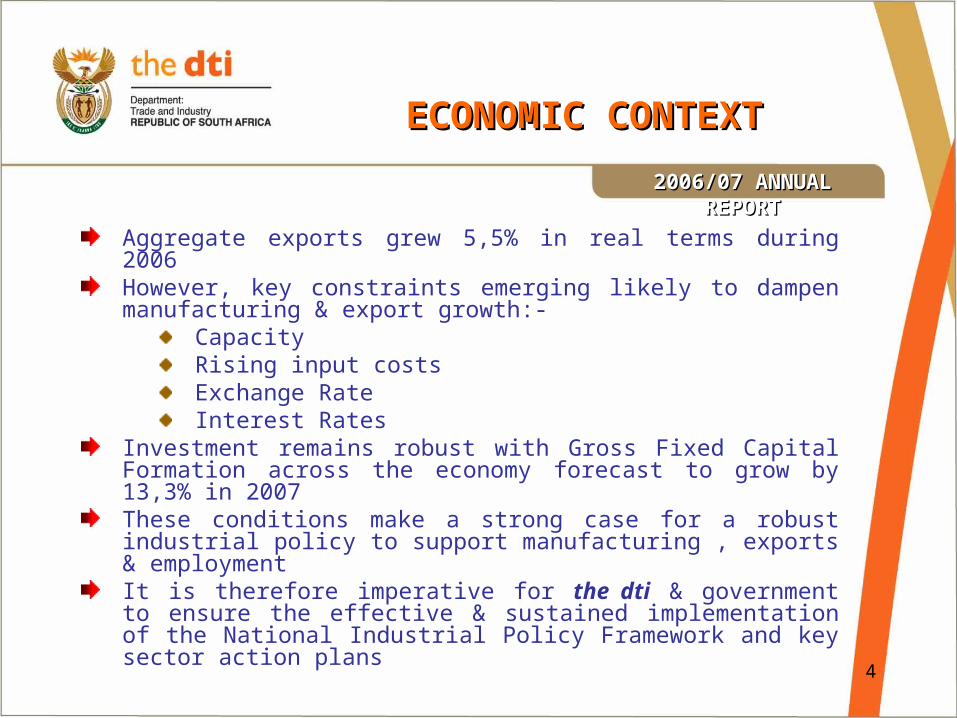

Aggregate exports grew 5,5% in real terms during 2006However, key constraints emerging likely to dampen manufacturing & export growth:-

CapacityRising input costsExchange RateInterest Rates

Investment remains robust with Gross Fixed Capital Formation across the economy forecast to grow by 13,3% in 2007These conditions make a strong case for a robust industrial policy to support manufacturing , exports & employmentIt is therefore imperative for the dti & government to ensure the effective & sustained implementation of the National Industrial Policy Framework and key sector action plans

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

5

STRATEGIC OBJECTIVESSTRATEGIC OBJECTIVES

Promoting coordinated implementation of the accelerated and shared growth initiativePromoting direct investment and growth in the industrial and service economy, with particular focus on employment creationRaising the level of exports and promote equitable global tradePromoting broader participation, equity and redress in the economy; andContributing to Africa's development and regional integration within the NEPAD framework

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

6

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

The department seeks to organise its work in terms of the following areas on which the annual report is based:-

Industrial development

Trade, investment and export

Broadening participation

Regulation

Administration and coordination

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

7

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

Industrial DevelopmentPurpose: Provide leadership in the development of policies and strategies that promote competitiveness, enterprise development and the efficient administration of support measures.

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

ProgressCabinet endorsement of National Industrial Policy Framework, followed by outline of the Industrial Policy Action PlanFinalisation of key sector strategies (eg chemicals & pharmaceuticals; automotives, metals & capital equipment; forestry, pulp, paper & furniture; & clothing & textiles)Implementation of key sector strategies (BPO&O, tourism)Implementation of the National Industrial Participation Programme (150 projects, US$7.5 billion 12,000 direct jobs)

8

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

Industrial Development

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

Progress – cont.Key incentives have contributed to the manufacturing & services industries:

SMEDP - 11,309 projects approved since 2000 with R12,7b in incentive value. Since April 2006 2,501 projects approved with incentive value of R2,96bStrategic Industrial Projects (SIP) – 45 approved projects in July 2005 when scheme expired. Estimated value of ongoing investment of R28,7b with estimated 8,446 direct & 104,545 indirect jobs being created. 22 of the approved projects already established with investment of R10b.

9

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

Industrial Development2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

Progress – cont.Critical Infrastructure Programme (CIP) – 19 projects approved to date with qualifying investment of R32b & infrastructure investment of R9,2bIndustrial Development Zones – attracting growing investor interest with commitments currently valued at R28b. Film & TV production – 31 productions approved since 2004 with R1,8b in local expenditure. In 2006/07 four local productions assisted to the value of R31,3m incl. Oscar winning Tsotsi

Support for technology & innovation:-Support Programme for Industrial Innovation (SPII) – 85 projects endorsed to the value of R250m (18% female & 34% BEE)

10

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

Industrial Development2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

Progress – cont.Technology & Human Resources for Industry Prgramme (THRIP) – assisted 746 researchers; 3,178 students & 371 industry partners (36% female & 55% BEE)The South African National Accreditation System (SANAS) & the South African Bureau of Standards are also major contributors to this area of the dept’s work

Centres of Excellence established to increase manufacturing skills (i.e. Aerospace, Clothing & Textiles, Advanced Eng., etc.)Launched support measures for the development of the aerospace industry (eg. aerospace village) Comprehensive review of all major incentives undertaken to guide future support for Industrial Policy

11

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

Trade, Investment and ExportPurpose: To promote economic development by working to build an equitable multilateral trading system that facilitates development; strengthening trade and investment links with key economies; and by fostering African development including through regional and continental integration and development co-operation in line with NEPAD

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

ProgressLeadership role in WTO Doha Round negotiationsKey bilateral trade links and negotiations (EU, EFTA, USA, India, Brazil (and IBSA), China)EFTA agreement ratified by South Africa. Lesotho, Namibia & Swaziland to ratify agreementSACU-Mercusor PTA – major progress made & negotiations expected to be finalised in the current financial year.

12

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

Trade, Investment and Export2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

Progress – cont.SACU-US – a Trade Investment & Development Co-operation Agreement proposed as framework for these relationsClothing and textile quotas against import surges from China instituted to provide relief to local manufacturersOngoing negotiations to promote African and regional economic integrationBilateral Investment Treaties - signed with one country; negotiations concluded with 7 countries; ongoing negotiations with 3 countries; & planned negotiations with 9 countriesEngaged in the set-up of new SACU institutional arrangements

13

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

Trade, Investment and Export2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

Progress – cont.Ongoing export promotion activities on the basis of a revamped export strategy, including trade missions & national pavilions, identification & dissemination of trade leads & financial assistance to exhibitors & market researchersWide range of investment promotion activities undertaken, including investment pavilions & seminars; ministerial & presidential missions; international investment council meetings; investment conferences & sector specific briefs

14

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

Trade, Investment and Export2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

Progress – cont.Networks established with Provincial Investment Agencies, with meetings every quarterJoint collaboration and co-ordination with Provinces on investment & international projectsEMIA scheme hosted workshops in all provincesProvinces encouraged to participate in all missions & pavilions locally & internationally & access funding through the EMIA scheme5 export ready seminars attended by 410 SMEs

15

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

Broadening ParticipationPurpose: Lead in the development of policies and strategies that promote enterprise growth, empowerment and equity in the economy

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

Progress

Support for small enterprise development through increased financing of SMEs by Khula, NEF & IDC and the rollout of SEDA & SAMAF:- 47 SEDA offices 103 Enterprise Information Centres 18 Incubation Centres 13 Retail finance partners through which Khula lends 13 Khula Mentorship offices 8 SA Micro finance Apex Fund (SAMAF) Provincial offices

16

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

Broadening ParticipationPurpose: Lead in the development of policies and strategies that promote enterprise growth, empowerment and equity in the economy

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

ProgressCodes of Good Practice for BBBEE adopted by Cabinet, gazetted in February 2007 & under implementation (incl. Sector Charters)Regional Industrial Development work being linked to the National Industrial Policy Framework & Local Economic Development workBEE and women empowerment also supported by key incentive schemes:- BBSP, SPII & THRIP

17

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

Broadening Participation2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

Progress – cont.Training workshops on women empowerment and access to finance through SAWENCooperative legislation developed and support to cooperatives provided – 4 large projects totaling R9m & 16 small projects totaling R3,78m Products for targeted procurement from SMEs by government departments identified Publications, road shows and imbizo’s to promote awareness of the dti’s services and offerings

18

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

RegulationPurpose: Develop and implement coherent, predictable and transparent regulatory solutions that facilitate easy access to redress and efficient regulatory services for economic citizens.

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

ProgressNational Credit Act proclaimed and Regulator establishedCompanies Bill published for public commentConsumer Protection Bill published for public commentCompetition Policy Review completed & drafting of amendments to Act startedCorporate laws Amendment Bill introduced in 2006Processed the FIFA request for trademark protection & issued public notice

19

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

Regulation

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

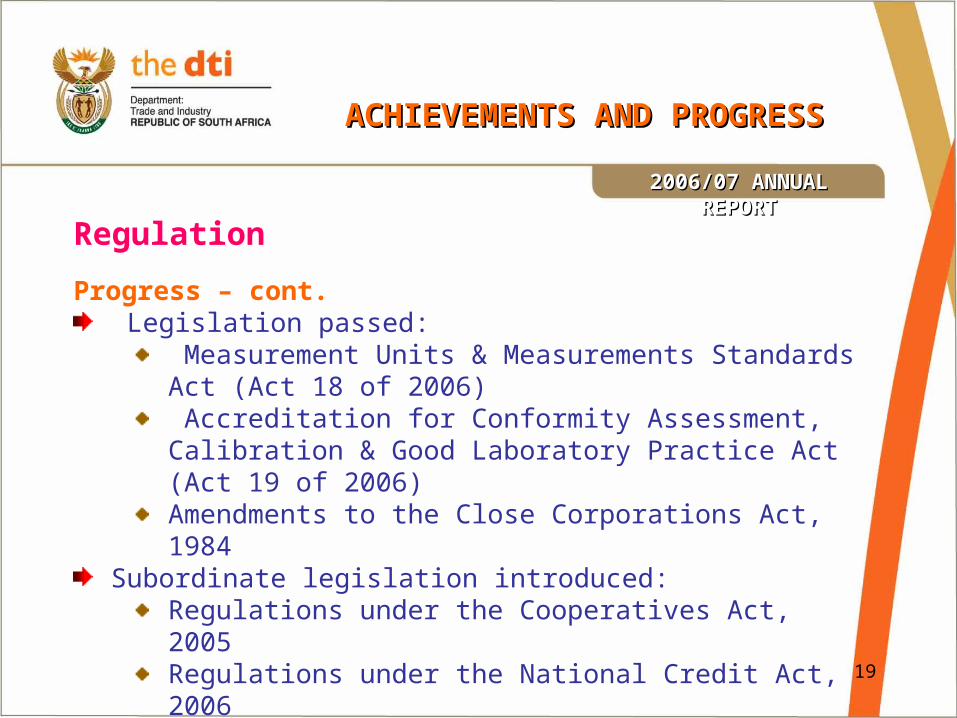

Progress – cont. Legislation passed:

Measurement Units & Measurements Standards Act (Act 18 of 2006) Accreditation for Conformity Assessment, Calibration & Good Laboratory Practice Act (Act 19 of 2006)Amendments to the Close Corporations Act, 1984

Subordinate legislation introduced:Regulations under the Cooperatives Act, 2005Regulations under the National Credit Act, 2006Amendments to regulations made under Legal Metrology Act 1973

20

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

RegulationWork undertaken on the following legislation for introduction in 2007/08

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

The Consumer Protection BillIntellectual Property Law Amendment BillCompetition Amendment BillCompanies BillNational Gambling Amendment BillNational Regulator for Compulsory Specifications BillThe Standards BillThe Lotteries Amendment Bill

21

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

Regulation2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

ProgressQuarterly meetings of the National Consumer Protection Forum, which include Provincial offices of consumer protection, to co-ordinate consumer protection activities.Capacity building programmes in alternative dispute resolution arranged by Office of Consumer Protection & to be rolled out to ProvincesLiquor Awareness Campaign is a partnership between the National Liquor Authority, provinces, SAPS, business and civil society. Campaign encourages responsible trading and drinking.Bi-annual meetings of the National Gambling Policy Council and the National Liquor Policy Council to advise the Minister on policy issues

22

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

Administration and co-ordinationPurpose: Ensure efficient and effective coordination and systems within the dti and with stakeholders & partners

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

ProgressHR is a critical challenge & ongoing efforts made to fill key vacancies, incl. use of specialized recruitment agencies213 vacancies were filled out of 323 in the year to 31 March 2007, & the vacancy rate stood at 27% An integrated HRD strategy under development, covering recruitment, retention & trainingGreater alignment, co-operation & co-ordination with the dti agencies (COTII), including leveraging capacity in agencies (eg. IDC)

23

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

Administration and co-ordination

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

Progress – cont.

Strong Corporate Governance maintainedUnqualified dti audits over several years & unqualified COTII audits in 2006/07, except for two agenciesAll COTII agencies tabled annual reports timeously

Key Boards of Directors & CEO appointments madeEstate Agency Affairs Board (EAAB)Small Enterprise Development Agency (SEDA)South African Bureau of Standards (SABS)SABS Trade Metrology Advisory Committee (TMAC)National Credit Regulator (NCR)International Trade Administration Commission of SA (ITAC)

24

ACHIEVEMENTS AND PROGRESSACHIEVEMENTS AND PROGRESS

Administration and co-ordination

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

Progress – cont.South African Micro-finance Apex Fund (SAMAF)Companies & Intellectual Property Registration Office (CIPRO)National Metrology Institute of South Africa (NMISA)Commissioner of the Competition Commission

Effective & efficient use of allocated funds

25

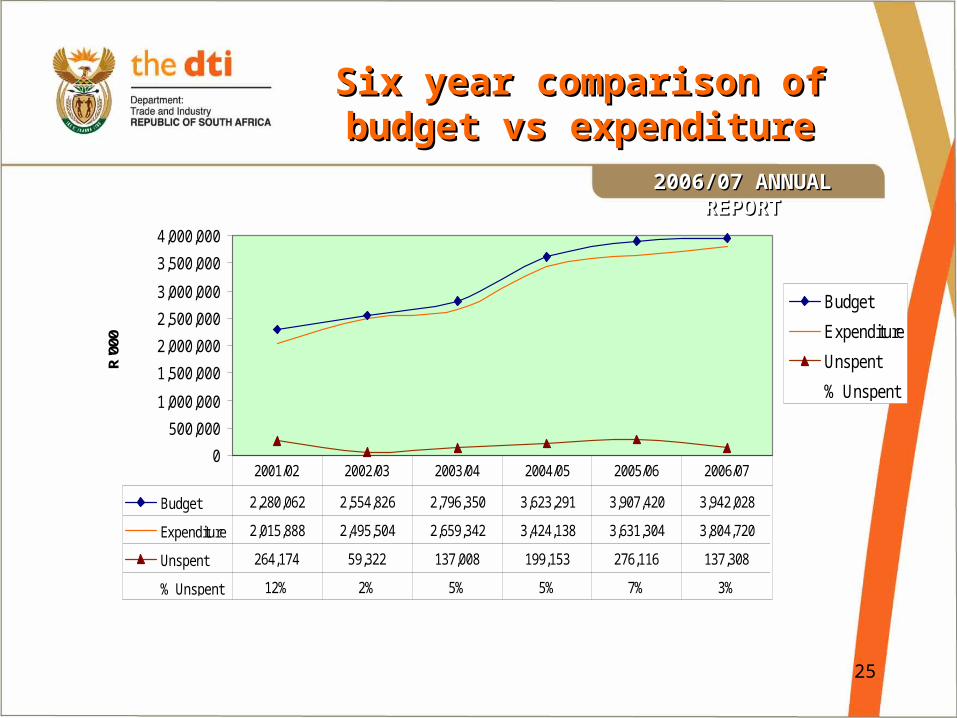

Six year comparison ofSix year comparison ofbudget vs expenditurebudget vs expenditure

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

R'0

00

Budget

Expenditure

Unspent

% Unspent

Budget 2,280,062 2,554,826 2,796,350 3,623,291 3,907,420 3,942,028

Expenditure 2,015,888 2,495,504 2,659,342 3,424,138 3,631,304 3,804,720

Unspent 264,174 59,322 137,008 199,153 276,116 137,308

% Unspent 12% 2% 5% 5% 7% 3%

2001/02 2002/03 2003/04 2004/05 2005/06 2006/07

26

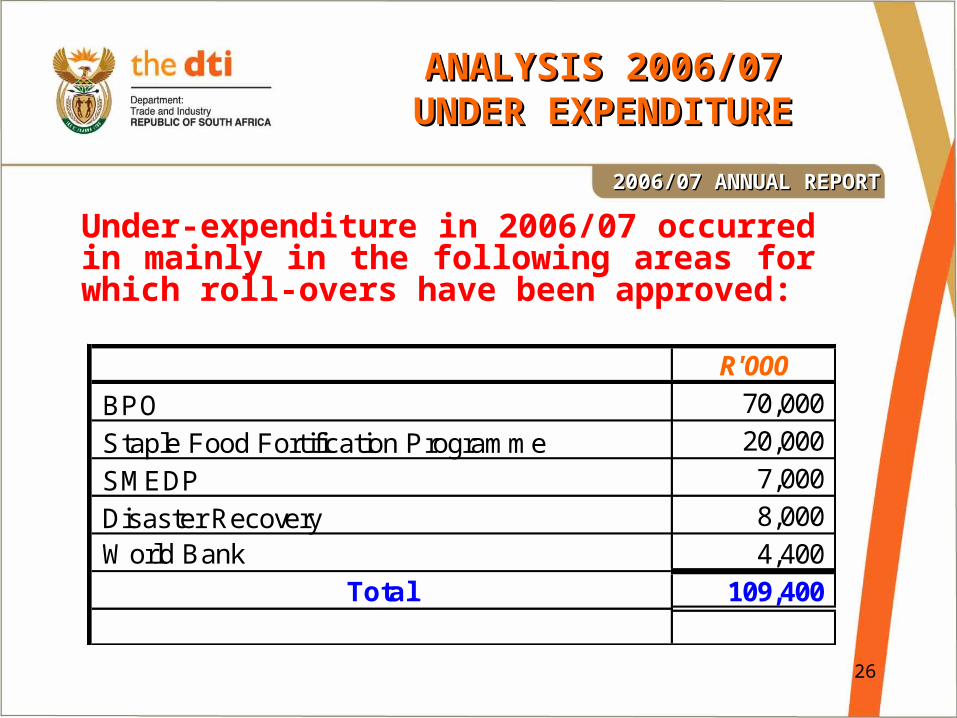

ANALYSIS 2006/07ANALYSIS 2006/07UNDER EXPENDITUREUNDER EXPENDITURE

Under-expenditure in 2006/07 occurred in mainly in the following areas for which roll-overs have been approved:

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

R'000

BPO 70,000

Staple Food Fortification Programme 20,000

SMEDP 7,000

Disaster Recovery 8,000 World Bank 4,400

Total 109,400

27

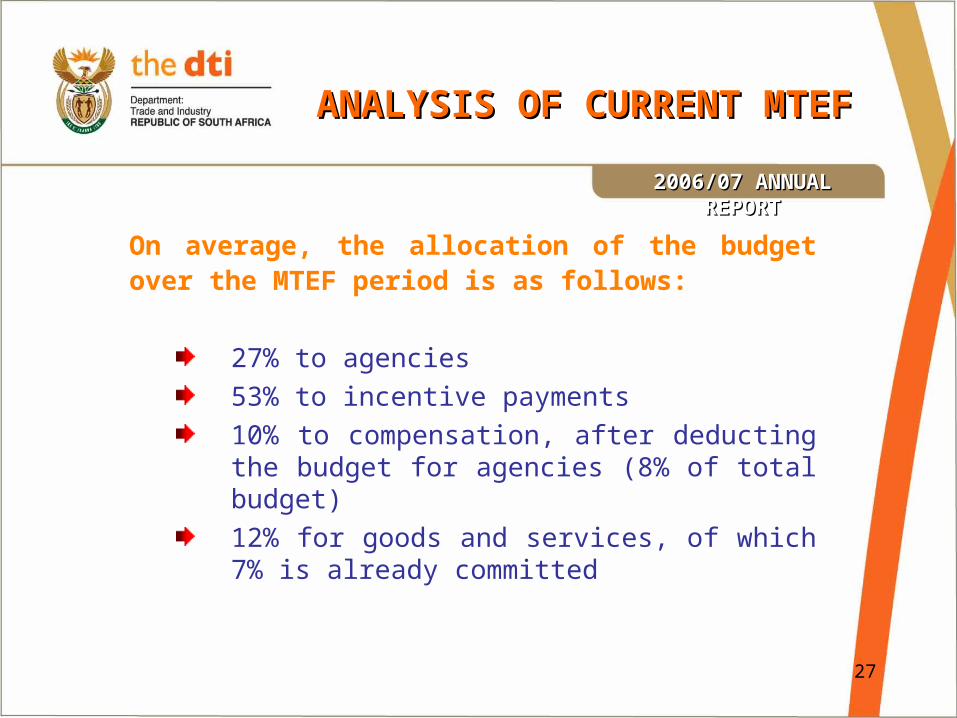

ANALYSIS OF CURRENT MTEFANALYSIS OF CURRENT MTEF

On average, the allocation of the budget over the MTEF period is as follows:

27% to agencies

53% to incentive payments

10% to compensation, after deducting the budget for agencies (8% of total budget)

12% for goods and services, of which 7% is already committed

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

28

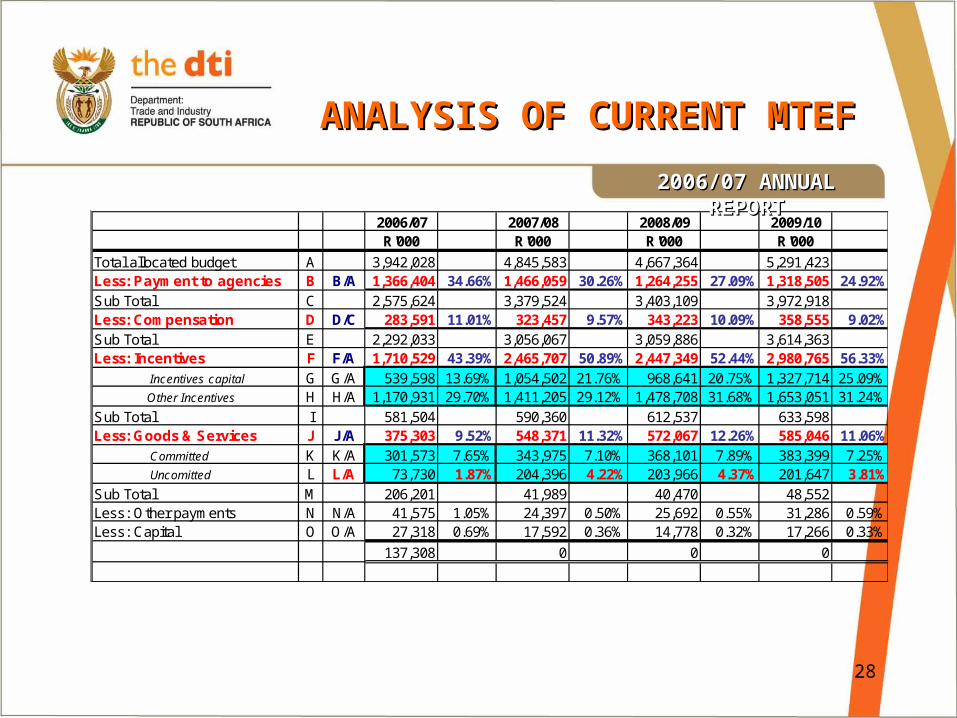

ANALYSIS OF CURRENT MTEFANALYSIS OF CURRENT MTEF

2006/07 2007/08 2008/09 2009/10R'000 R'000 R'000 R'000

Total allocated budget A 3,942,028 4,845,583 4,667,364 5,291,423Less: Payment to agencies B B/A 1,366,404 34.66% 1,466,059 30.26% 1,264,255 27.09% 1,318,505 24.92%Sub Total C 2,575,624 3,379,524 3,403,109 3,972,918Less: Compensation D D/C 283,591 11.01% 323,457 9.57% 343,223 10.09% 358,555 9.02%Sub Total E 2,292,033 3,056,067 3,059,886 3,614,363Less: Incentives F F/A 1,710,529 43.39% 2,465,707 50.89% 2,447,349 52.44% 2,980,765 56.33%

Incentives capital G G/A 539,598 13.69% 1,054,502 21.76% 968,641 20.75% 1,327,714 25.09% Other Incentives H H/A 1,170,931 29.70% 1,411,205 29.12% 1,478,708 31.68% 1,653,051 31.24%Sub Total I 581,504 590,360 612,537 633,598Less: Goods & Services J J/A 375,303 9.52% 548,371 11.32% 572,067 12.26% 585,046 11.06%

Committed K K/A 301,573 7.65% 343,975 7.10% 368,101 7.89% 383,399 7.25% Uncomitted L L/A 73,730 1.87% 204,396 4.22% 203,966 4.37% 201,647 3.81%Sub Total M 206,201 41,989 40,470 48,552Less: Other payments N N/A 41,575 1.05% 24,397 0.50% 25,692 0.55% 31,286 0.59%Less: Capital O O/A 27,318 0.69% 17,592 0.36% 14,778 0.32% 17,266 0.33%

137,308 0 0 0

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

29

CHALLENGESCHALLENGES

In conclusion

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT

Overall we have achieved our targets for the reporting periodChallenge is to enhance impact of the department through:-

Ensuring effective programme & project performance Stronger strategic & operational managementGreater integration of work, including with agencies

Adequate financial resources for extensive dti programmesHR challenge of recruitment, retention and developmentImproved cluster co-ordination

30

THANK YOU

&

QUESTIONS

2006/07 ANNUAL REPORT2006/07 ANNUAL REPORT