1 © 2012 john wiley & sons, ltd, accounting for managers, 4th edition, 9781119979678 chapter 14...

TRANSCRIPT

1© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Chapter 14Strategic Investment Decisions

Overview

• Strategy and capital investment decisions• Three methods

– Accounting rate of return– Payback– Discounted cash flow

• Net present value• Internal rate of return

– Comparison and criticism of techniques

2© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Strategy

• Alternative views:

• Objectives SWOT strategic decisions– Ansoff (1988)

• Logical incrementalism– Quinn (1980)

• Deliberate & emergent strategies– Mintzberg & Waters (1985)

3© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Strategy & investment appraisal

• Investment decisions need to be– Consistent with strategy– Able to generate sufficient returns to contribute to

overall business returns• Types of investment

– new facilities for new product/services;– expanding capacity to meet demand;– replacing assets in order to reduce production

costs or improve quality or service

4© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Investment appraisal

• Process– Generate ideas based on opportunities or solutions – Research all relevant information– Consider possible alternatives– Evaluate the financial and non-financial

consequences of each – Decide to proceed and implement the proposal– Monitor actual results compared to plan

5© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Investment appraisal

• Decisions:– whether or not to invest– whether to invest in one project or one piece of

equipment rather than another– whether to invest now or at a later time

6© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Methods of investment appraisal

• Accounting rate of return• Payback• Discounted cash flow

– Net present value (NPV)– Internal rate of return (IRR)

7© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Comparison of methods

Based on profit or cash flow?

Accounts for time value of money?

Accounting rate of return

Profit No

Payback Cash flow No

Discounted cash flow

Cash flow Yes

8© 2012 John Wiley & Sons, Ltd, Accounting for Managers, 4th edition,

9781119979678

Predicting future profits & cash flows

• Profits and cash flows are estimated and include:– Incremental revenue and operating costs,– Incremental income tax and changes in working

capital – These are based on expected market share, volumes,

unit prices and costs, etc.• All investment decisions involve an initial cash outflow

(period 0)• All other cash inflows and outflows are assumed to take

place at the end of years 1,2,3 etc.• Financing decisions are separate decisions. Investment

appraisal is concerned with the investment decision • Each organization determines its own planning horizon

9© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Cash flows for three projects

10© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Accounting rate of return

• Profit generated as a percentage of the investment – investment value is the depreciated value each

year– For the whole investment period, the accounting

rate of return is the average annual return divided by the average investment

Total profits/No. of yearsInitial investment/2

11© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Depreciated value of investments

12© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

ARR for Project 1

13© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Accounting rate of return – average

• Similar to the ROI calculation in financial accounting– On an individual asset basis

• Project 1– Total profits £25,000– Average profit £5,000 (£25,000/5)– Average investment £50,000 (£100,000/2)– Average ARR £5,000/£50,000 = 10%

14© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Comparison of projects: ARR

Alternative ARR Ranking

Project 1 10% 3

Project 2 16% 1

Project 3 12% 2

15© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Payback (in US, “Break Even”)

• The number of years it will take to recover the initial investment– cash flow, not profits– the shorter the payback period, the better the

investment

16© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Payback

• Project 1: 4 years• Project 2: 3.57 years• Project 3: 3 years

17© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Comparison of projects: Payback

Alternative Payback Ranking

Project 1 4 years 3

Project 2 3.57 years 2

Project 3 3 years 1

18© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Discounted cash flow (DCF)

• Neither the accounting rate of return nor the payback method considers the time value of money

• Discounts the future cash flows to present values using a discount rate (cost of capital)

• Net present value (NPV)• Internal rate of return (IRR)

19© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Cost of capital

• Weighted average cost of capital– Debt: weighted average interest rate– Equity: cost of equity (dividend plus capital

growth expected)– May be risk-adjusted– Cost of capital is calculated for each

organization by corporate finance staff

20© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Time value of money

Assumes compound interest£100 today Plus 10% p.a. interest = £10= £110 in 1 years’ timePlus £10% interest = £11= £121 in 2 years’ timePlus 10% interest = £12.10= £133.10 in 3 years time (Future Value) Present value brings this sum back to today’s equivalent

21© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Net present value

Present value (PV) of cash flows = cash flow x discount factor (based on number of years in the future and the cost of capital)

Net present value (NPV) = present value of future cash flows – initial capital investment

22© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Present value tablesYears 1% 2% 3% 4% 5% 6% 7% 8% 9% 10%

1 0.9901 0.9804 0.9709 0.9615 0.9524 0.9434 0.9346 0.9259 0.9174 0.9091

2 0.9803 0.9612 0.9426 0.9426 0.9070 0.8900 0.8734 0.8573 0.8417 0.8264

3 0.9706 0.9423 0.9151 0.8890 0.8638 0.8396 0.8163 0.7938 0.7722 0.7513

4 0.9610 0.9238 0.8885 0.8548 0.8227 0.7921 0.7629 0.7350 0.7084 0.6830

5 0.9515 0.9057 0.8626 0.8219 0.7835 0.7473 0.7130 0.6806 0.6499 0.6209

6 0.9420 0.8880 0.8375 0.7903 0.7462 0.7050 0.6663 0.6302 0.5963 0.5645

7 0.9327 0.8706 0.8131 0.7599 0.7107 0.6651 0.6227 0.5835 0.5470 0.5132

8 0.9235 0.8535 0.7894 0.7307 0.6768 0.6274 0.5820 0.5403 0.5019 0.4665

9 0.9143 0.8368 0.7664 0.7026 0.6446 0.5919 0.5439 0.5002 0.4604 0.4241

10 0.9053 0.8203 0.7441 0.6756 0.6139 0.5584 0.5083 0.4632 0.4224 0.3855

23© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Net present value for Project 1

24© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Net present value using spreadsheet

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5Cash flow -$100,000 $25,000 $25,000 $25,000 $25,000 $25,000PV of cash flows $94,770NPV -$5,230

Formula for PV=PV(.10,c2:g2)

25© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Evaluating NPV

• If the NPV is negative, the project should not be accepted, as the returns do not exceed the cost of capital, and shareholder value is being eroded

26© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Comparison of projects: NPV

Alternative NPV Ranking

Project 1 -$5,250 No investment

Project 2 $7,650 1

Project 3 $3,300 2

27© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Comparing NPVs

Cash Value Added (CVA) or profitability index is the ratio of the NPV to the initial capital investment.

Cash value added = NPVInitial capital investment

28© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

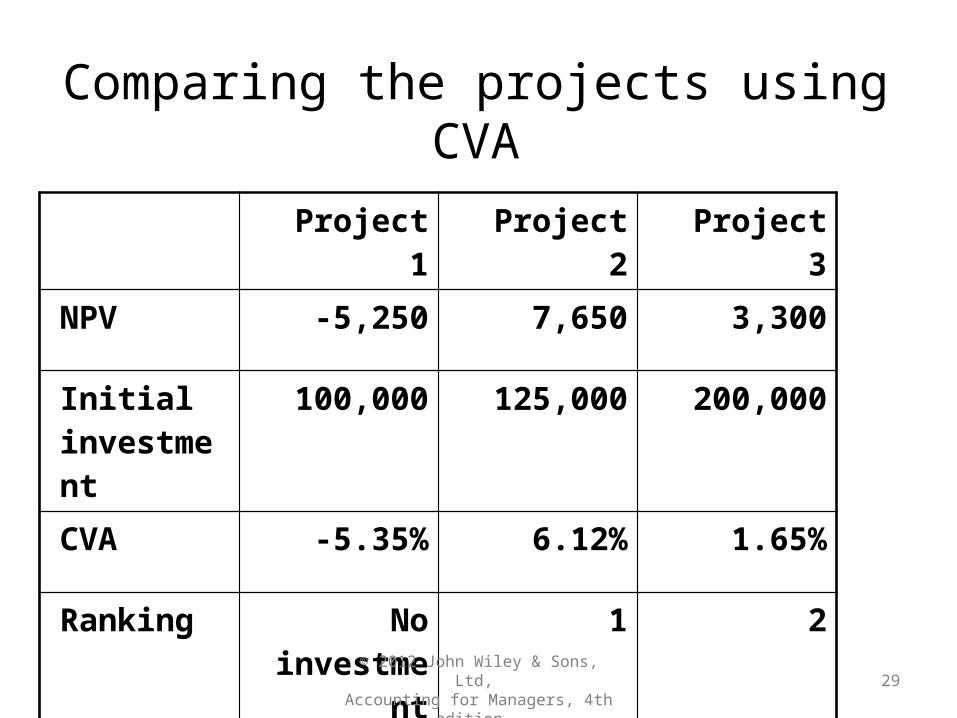

Comparing the projects using CVA

Project 1 Project 2 Project 3

NPV -5,250 7,650 3,300

Initial investment

100,000 125,000 200,000

CVA -5.35% 6.12% 1.65%

Ranking No investment

1 2

29© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Internal rate of return

• Determines the discount rate which produces a net present value of zero– presents the return on cash flows as an effective

interest rate– the project with the highest internal rate of return

would be preferred, provided that the rate exceeds the cost of capital

30© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Internal rate of return: By spreadsheet

Year 0 1 2 3 4 5Cash flow - Project 1 -100,000 25,000 25,000 25,000 25,000 25,000IRR 7.9%Cash flow - Project 2 -125,000 35,000 35,000 35,000 35,000 35,000IRR 12.4%Cash flow - Project 3 -200,000 60,000 60,000 80,000 30,000 30,000IRR 10.7%

=IRR(B6:G6)

31© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Comparison of projects: IRR

Alternative IRR Ranking

Project 1 7.9% No investment – less than 10% cost of capital

Project 2 12.4% 1

Project 3 10.7% 2

32© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

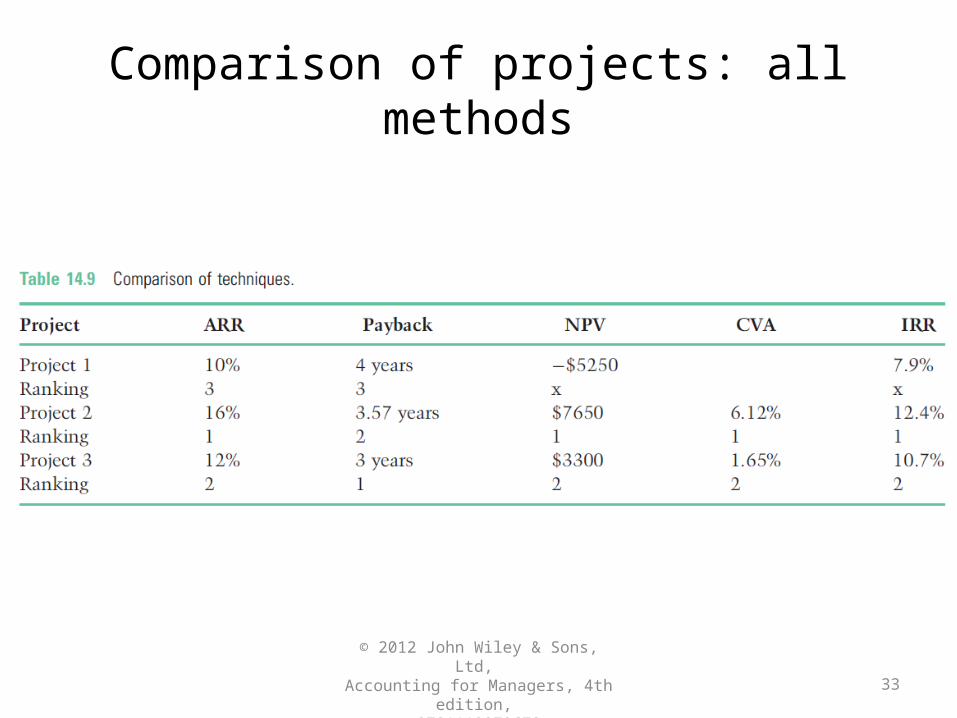

Comparison of projects: all methods

33© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

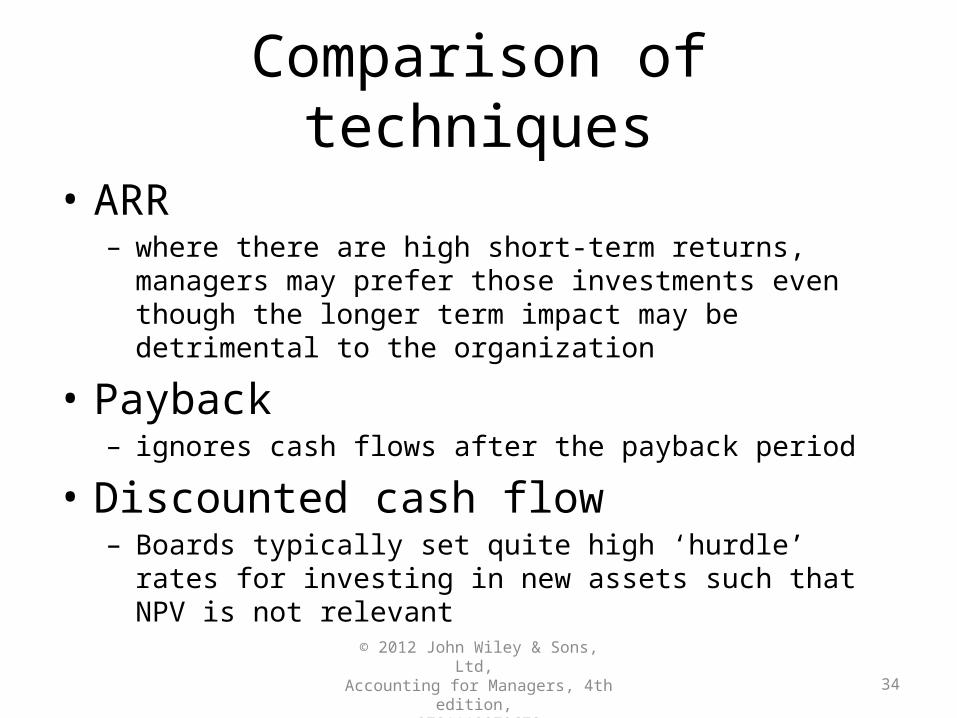

Comparison of techniques

• ARR– where there are high short-term returns, managers may

prefer those investments even though the longer term impact may be detrimental to the organization

• Payback– ignores cash flows after the payback period

• Discounted cash flow– Boards typically set quite high ‘hurdle’ rates for investing in

new assets such that NPV is not relevant

34© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Criticisms of investment evaluation

Assumption that future cash flows can be predicted with some accuracy

Decisions may be made subjectively which are then justified after the event by overly optimistic estimates of future cash flows

NPV approach is limited in high technology situations as it may not capture the ‘richness’ of the investment problem – Shank (1996)

35© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678

Key points

• Differentiate profits and cash flows• Ranking investments

– ARR, – Payback, and – DCF techniques: NPV, CVA & IRR

• Compare strengths and weaknesses of each method

36© 2012 John Wiley & Sons, Ltd,

Accounting for Managers, 4th edition, 9781119979678