1 3 march 2009 2009 economic outlook government economist

TRANSCRIPT

13 March 2009

2009 Economic outlookGovernment Economist

2

Global setting

3

Global financial turmoil mutated into global synchronised downturn

4

Job losses posing a severe drag on US consumption

-12

-8

-4

0

4

8

12

16

1/93 1/94 1/95 1/96 1/97 1/98 1/99 1/00 1/01 1/02 1/03 1/04 1/05 1/06 1/07 1/08 1/09-3

-2

-1

0

1

2

3

4

Retail Sales(LHS)

Employment(RHS)

Year-on-year growth rate (%) Year-on-year growth rate (%)

Jan09-2.5-9.7

5

US imports falling even faster, which impact severely on Asia’s exports

-20

-15

-10

-5

0

5

10

15

20

25

30

1/96 1/97 1/98 1/99 1/00 1/01 1/02 1/03 1/04 1/05 1/06 1/07 1/08

US's importsdemand

in real terms

Year-on-year growth rate (%)

US's importsfrom Asia in

nominal terms

Dec-9.8

-10.4

6

EU’s demand cut back sharply amid recession mode

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

35

01 02 03 04 05 06 07 08-6

-4

-2

0

2

4

6

EU's import demandin real terms (LHS)

EU's GDPannualised q-t-q rate of

change in real terms(RHS)

Year-on-yeargrowth rate (%)

Quarter-to-quarter growth rate (%)

Dec08-4.6%

Q408-5.8%

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

20

1/97 1/98 1/99 1/00 1/01 1/02 1/03 1/04 1/05 1/06 1/07 1/08 1/09

Feb09-39.8%

EU'sSentiment

Index

Year-on-year growth rate (%)

7

Similar situation in Japan

-50

-40

-30

-20

-10

0

10

20

30

40

50

95 96 97 98 99 00 01 02 03 04 05 06 07 08-5

-4

-3

-2

-1

0

1

2

3

4

5

Q408 Real GDPGrowth: -4.6%

Index

Q408 Tankan:-16

Japan GDP vs Tankan Survey

Japan GDP RealGrowth (RHS)

Japan TANKANLarge enterpriese (LHS)

%

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

14

1/01 1/02 1/03 1/04 1/05 1/06 1/07 1/08 1/09

Jan09:-10%

Japan Import Demand

Year-on-year growth rate in real terms (%)

8

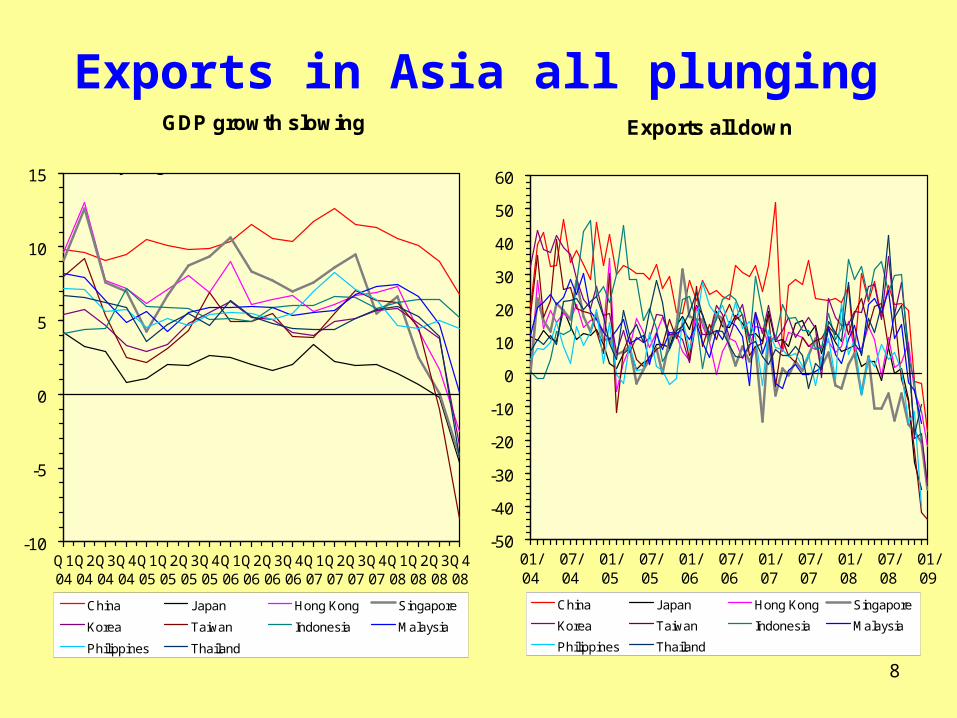

Exports in Asia all plunging GDP growth slowing

-10

-5

0

5

10

15

Q104

Q204

Q304

Q404

Q105

Q205

Q305

Q405

Q106

Q206

Q306

Q406

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

China Japan Hong Kong Singapore

Korea Taiwan Indonesia Malaysia

Philippines Thailand

Year-on-year growth rate (%)

Exports all down

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

01/04

07/04

01/05

07/05

01/06

07/06

01/07

07/07

01/08

07/08

01/09

China Japan Hong Kong Singapore

Korea Taiwan Indonesia Malaysia

Philippines Thailand

Year-on-year growth rate (%)

9

HK’s economic outlook in 2009

• Global economy mired in recession; many Asian economies bound to be significantly hit

• HK economy expected to contract by 2 - 3%, under the drag from shrinking external demand and dented sentiment

• Timing of global recovery remains uncertain

10

Downside risks

• Deeper and more protracted global recession

• Negative feedback loop between economic downturn,

credit crunch and financial market stress

• Concerns about the aftermaths of various aggressive

policy measures

• Disorderly unwinding of the global trade imbalances

• Rising protectionism

11

HK’s sound fundamentals will help us withstand the crisis better than many others

• Banks prudent in lending: high CAR

• Spending within our means: current account

surplus

• HK is a net creditor to rest of the world: strong

IIP

• Fiscal prudence

• 3rd most competitive economy in the world

12

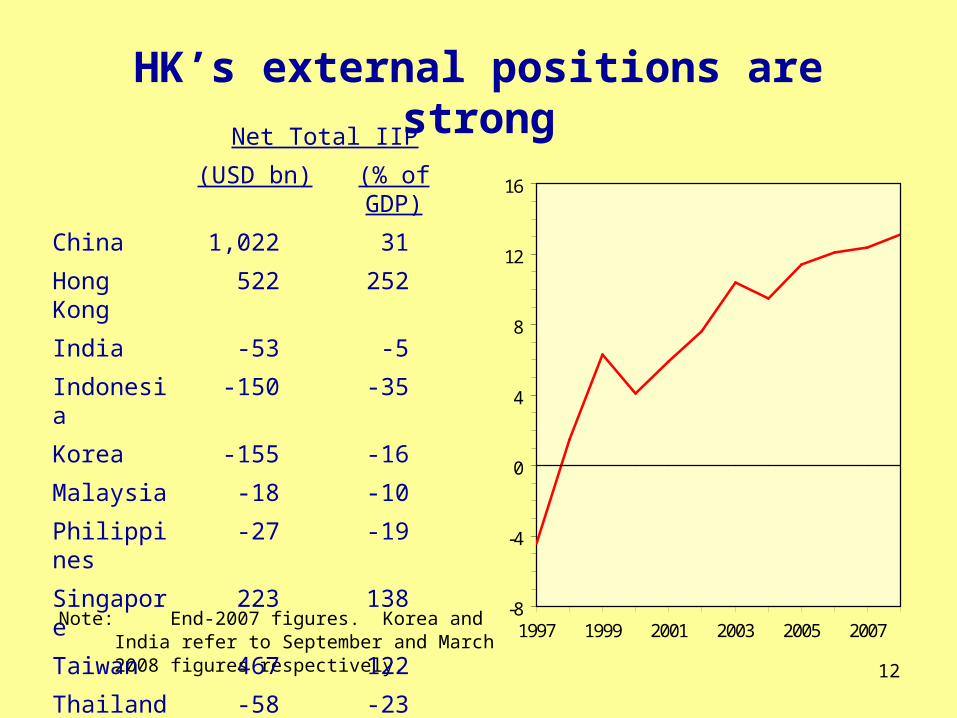

HK’s external positions are strong

Note: End-2007 figures. Korea and India refer to September and March 2008 figures respectively.

Net Total IIP

(USD bn) (% of GDP)

China 1,022 31

Hong Kong 522 252

India -53 -5

Indonesia -150 -35

Korea -155 -16

Malaysia -18 -10

Philippines -27 -19

Singapore 223 138

Taiwan 467 122

Thailand -58 -23-8

-4

0

4

8

12

16

1997 1999 2001 2003 2005 2007

13.1%Current account balanceas % of GDP

Percent

2008Q1-Q3

13

2009/10 Budget

14

Short term measures to tackle the global crisis

2009/10 Budget is a further package following a series of measures already implemented last year

$57 bn total of measures (3.5% of GDP)

100% deposit guarantee

$100 bn loan guarantee scheme for all enterprises except listed companies

Efforts to create jobs announced earlier

15

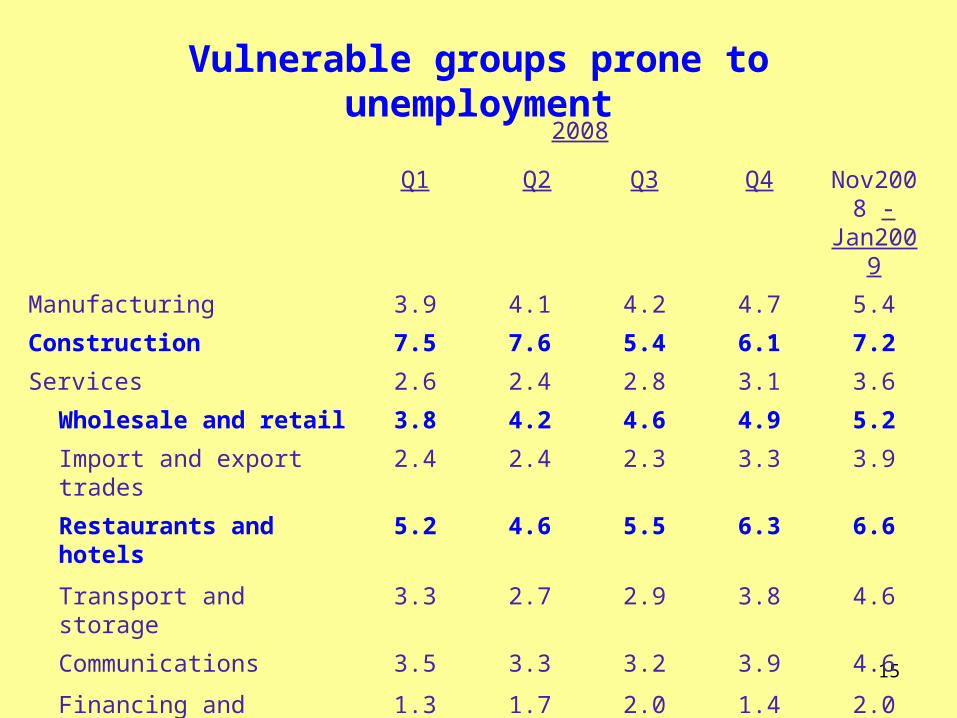

Vulnerable groups prone to unemployment

2008

Nov2008 -

Jan2009

Q1 Q2 Q3 Q4

Manufacturing 3.9 4.1 4.2 4.7 5.4

Construction 7.5 7.6 5.4 6.1 7.2

Services 2.6 2.4 2.8 3.1 3.6

Wholesale and retail 3.8 4.2 4.6 4.9 5.2

Import and export trades 2.4 2.4 2.3 3.3 3.9

Restaurants and hotels 5.2 4.6 5.5 6.3 6.6

Transport and storage 3.3 2.7 2.9 3.8 4.6

Communications 3.5 3.3 3.2 3.9 4.6

Financing and insurance 1.3 1.7 2.0 1.4 2.0

Real estate and business services

2.5 2.2 2.6 2.7 3.4

Overall 3.4 3.3 3.4 4.1 4.6

16

2009/10 Budget : focused efforts to help

the most vulnerable

Construction, esp decoration and maintenance

Youth unemployment and new graduates

Middle aged and disabled

17

In macro sense, 09/10 Budget is expansionary

Spending increase:

Recurrent spending : up $11.7 bn

Capital works expenditure: up $16.3 bn

Revenue concessions : $8.4 bn

Budget deficit : $39.9 bn (2.4% of GDP)

18

Further integration with the vibrant Mainland

economy and positioning ourselves strategically in

the PRD

Move towards higher value-added and knowledge-

based activities:

Strengthen HK as an international financial centre:

Green economy

Promote Innovation & Technology

Promote Creativity

Invest in infrastructure

Upgrade human capital

Looking beyond the financial crisis

19

Upgrading human capital is key to future success

15

17

19

21

23

25

27

29

31

33

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

31.2%

Share of tertiary educational attainmentin labour force

(% share)

20

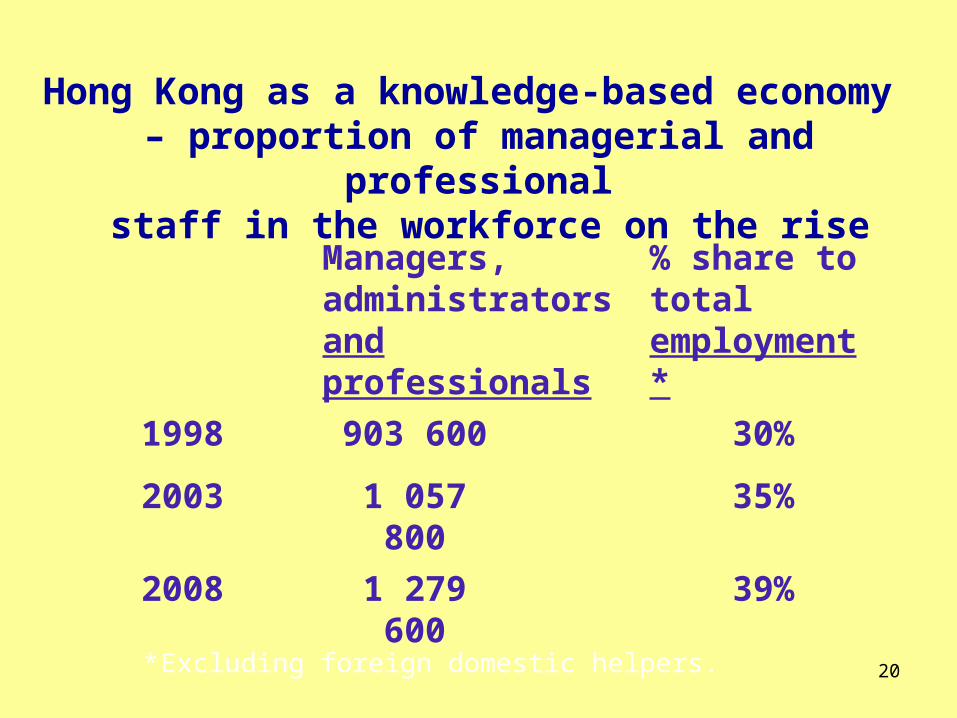

Managers, administrators and professionals

% share to total employment*

1998 903 600 30%

2003 1 057 800 35%

2008 1 279 600 39%

* Excluding foreign domestic helpers.

Hong Kong as a knowledge-based economy – proportion of managerial and professional

staff in the workforce on the rise

21

Hong Kong’s productivity growth

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.03.7%

Average annual rate of change (%)

2.9%

1.2%

1997-2000 2005-20082001-2004

223 March 2009

Thank you

23

Value added by major economic sectors

2004 2005 2006 2007 2008

H1

2008

Q3

% % % % % %

Services 9.9

7.5 7.1 7.0 5.4 1.9

Wholesale and retail6.9

8.3 7.1 6.8 7.4 2.6

Import and export trades 15.4

15.9 9.0 6.0 8.7 4.9

Restaurants and hotels23.0

6.8 9.4 11.0 4.2 2.0

Transport and storage13.7

6.9 6.6 5.1 6.1 1.4

Communications14.6

9.4 7.7 5.3 4.4 4.5

Financing and insurance21.0

11.9 19.7 17.6 7.4 -0.8

Real estate and business services 2.6

4.2 1.9 6.4 5.6 -0.2

Community, social and personal services 2.6

-0.1 1.3 1.7 1.1 1.6

Year-on-year rate of increase in value added in real terms

24

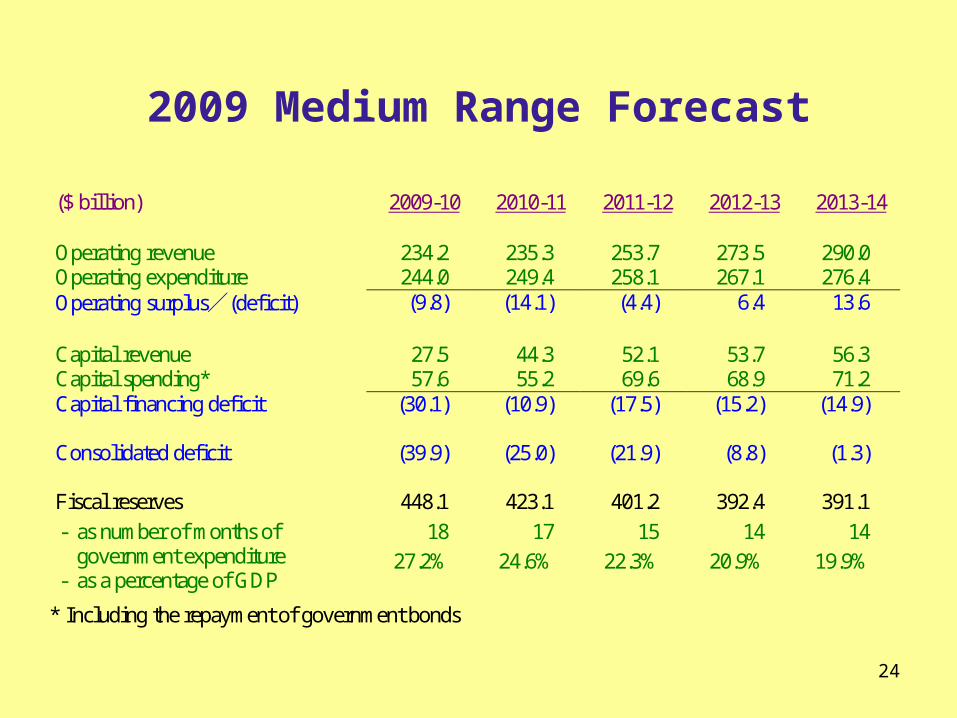

2009 Medium Range Forecast

($ billion) 2009-10 2010-11 2011-12 2012-13 2013-14

Operating revenue 234.2 235.3 253.7 273.5 290.0 Operating expenditure 244.0 249.4 258.1 267.1 276.4 Operating surplus/(deficit)

(9.8) (14.1) (4.4) 6.4 13.6

Capital revenue 27.5 44.3 52.1 53.7 56.3 Capital spending* 57.6 55.2 69.6 68.9 71.2 Capital financing deficit

(30.1) (10.9) (17.5) (15.2) (14.9)

Consolidated deficit

(39.9)

(25.0)

(21.9)

(8.8)

(1.3)

Fiscal reserves

- as number of months of government expenditure

- as a percentage of GDP

448.1

18

27.2%

423.1

17

24.6%

401.2

15

22.3%

392.4

14

20.9%

391.1

14

19.9%

* Including the repayment of government bonds