1 august-september/2002. 2 agenda abamec bradesco 2001 historical performance main events...

TRANSCRIPT

1

August-September/2002August-September/2002

2

AgendaAgenda

ABAMEC Bradesco 2001ABAMEC Bradesco 2001

Historical PerformanceHistorical Performance

Main Events Main Events

Competitive AdvantagesCompetitive Advantages

ManagementManagement CharacteristicsCharacteristics

PerspectivesPerspectives

3

Creating Value to our ShareholdersCreating Value to our Shareholders

R$ 849 million of Interest on Own Capital / Dividends related to 2001 fiscal year (41% of adjusted Net Income)

Acquisitions - Mercantil de São Paulo, BEA and Cidade, Ford’s Loan Portfolio, Deutsche Asset Management, and Postal Bank

Transparency - 2001 Atlantic Rating Award(Retail Bank Category)

320 Meetings and Conferences Organized by the IR Area

NYSE - Listing on November 21st, 2001 (BBD)

Integration of Back-Offices

4

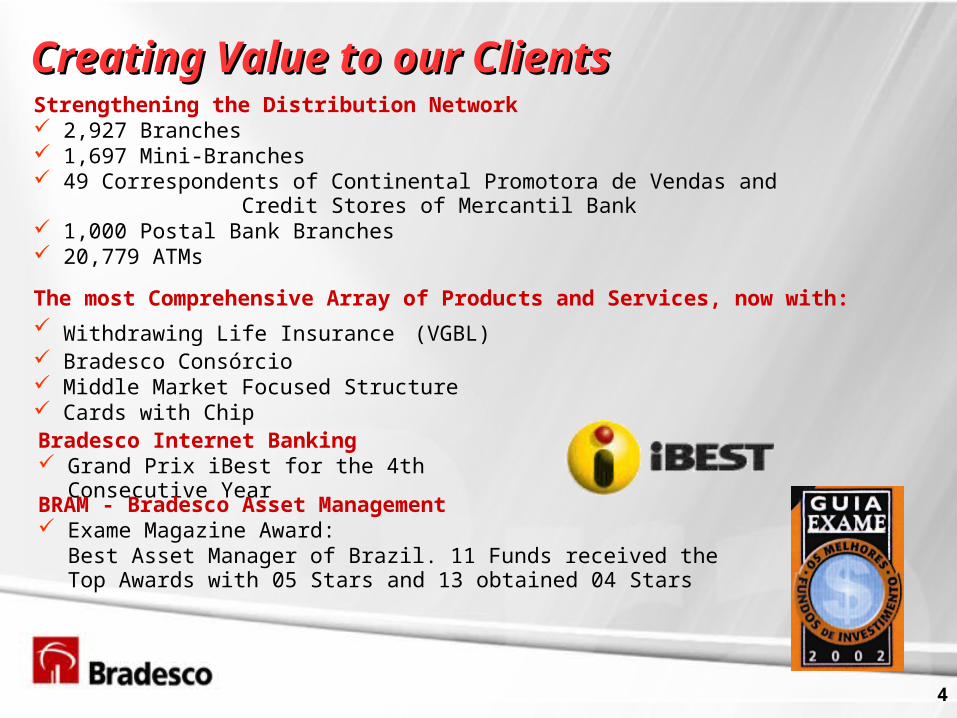

CreatCreatinging Value to our Value to our ClientsClientsStrengthening the Distribution Network 2,927 Branches 1,697 Mini-Branches 49 Correspondents of Continental Promotora de Vendas and

Credit Stores of Mercantil Bank 1,000 Postal Bank Branches 20,779 ATMs

The most Comprehensive Array of Products and Services, now with: Withdrawing Life Insurance (VGBL) Bradesco Consórcio Middle Market Focused Structure Cards with ChipBradesco Internet Banking Grand Prix iBest for the 4th Consecutive Year

BRAM - Bradesco Asset Management Exame Magazine Award:

Best Asset Manager of Brazil. 11 Funds received the Top Awards with 05 Stars and 13 obtained 04 Stars

5

Creating Value to our EmployeesCreating Value to our Employees

In 2000, We were Elected one of the 100 Best Companies to Work for in Brazil by Exame Exame MagazineMagazine.

2001, We were Elected Again.

2002, We were Elected Once More.

In 2001, Bradesco spent R$ 3.4 billion in Salaries, Benefits and Training.

6

CreatCreatinging Value to the Society Value to the Society

R$ 112.1 millionR$ 112.1 million Invested in 2001

R$ 119.8 millionR$ 119.8 million Forecasted for 2002

455 thousand455 thousand Undergraduate Students were qualified by Bradesco Foundation during the past 45 years

103 thousand103 thousand Students admitted in 2001, of which 90% are members of the community

7

AgendaAgenda

ABAMEC Bradesco 2001ABAMEC Bradesco 2001

Historical Historical Performance Performance

Main Events Main Events

Competitive AdvantagesCompetitive Advantages

ManagementManagement Characteristics Characteristics

PerspectivesPerspectives

8

Total AssetsTotal Assets

Historical PerformanceHistorical Performance

RR$ Billions$ Billions

CAGR = 16.3%

124.5124.5

101.8101.8

84.084.0

76.976.968.068.0

5050

6060

7070

8080

9090

100100

110110

120120

130130

1H 981H 98 1H 991H 99 1H 001H 00 1H 011H 01 1H 021H 02

9

Securities PortfolioSecurities Portfolio

37.937.935.535.5

29.729.7

23.223.2

14.014.0

30.4%34.9%

35.3%30.2%

20.6%

10

20

30

40

50

1H 98 1H 99 1H 00 1H 01 1H 02

10

20

30

40

50

Securities Portfolio % of Total Assets

Historical PerformanceHistorical Performance

RR$ Billions$ Billions

10

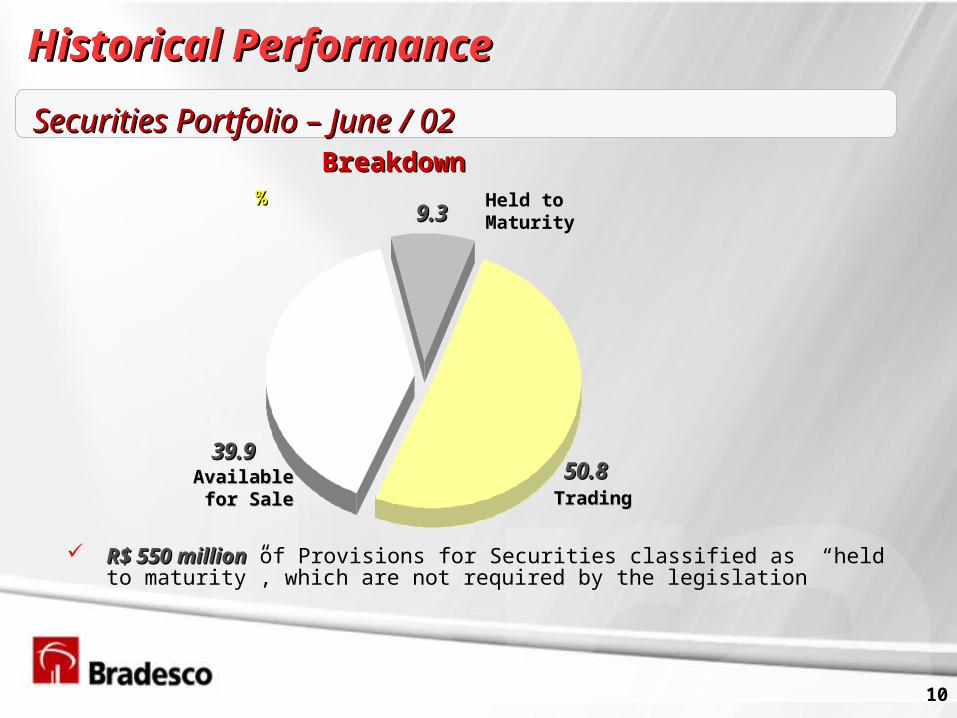

R$ 550 millionR$ 550 million of Provisions for Securities classified as “held to maturity”, which are not required by the legislation

Securities Portfolio – June / 02Securities Portfolio – June / 02

50.850.8

9.39.3

39.939.9

Held to Maturity

TradingTradingAvailableAvailable

for Salefor Sale

BreakdownBreakdown%%

Historical PerformanceHistorical Performance

11

(*) Includes Investments on Quotes of Mutual Funds

36.336.3

26.926.9

33.533.531 to 180 days31 to 180 days

More than 360 daysMore than 360 days

1 to 30 days1 to 30 days

Maturity (*)Maturity (*)

3.33.3181 to 360 days181 to 360 days

%%

Securities Portfolio – June / 02Securities Portfolio – June / 02

Historical PerformanceHistorical Performance

12

Loan Portfolio *Loan Portfolio *

* Excludes Sureties and Guaranties (R$ 3.4 billion as of June / 02)

52.652.6

43.843.8

30.630.6

26.226.225.025.0

43.0%

36.4%34.1%

36.7% 42.2%

20

30

40

50

60

1H 98 1H 99 1H 00 1H 01 1H 0220

30

40

50

Loan Portfolio % of Total Assets

R$ BillionsR$ Billions

Historical PerformanceHistorical Performance

13

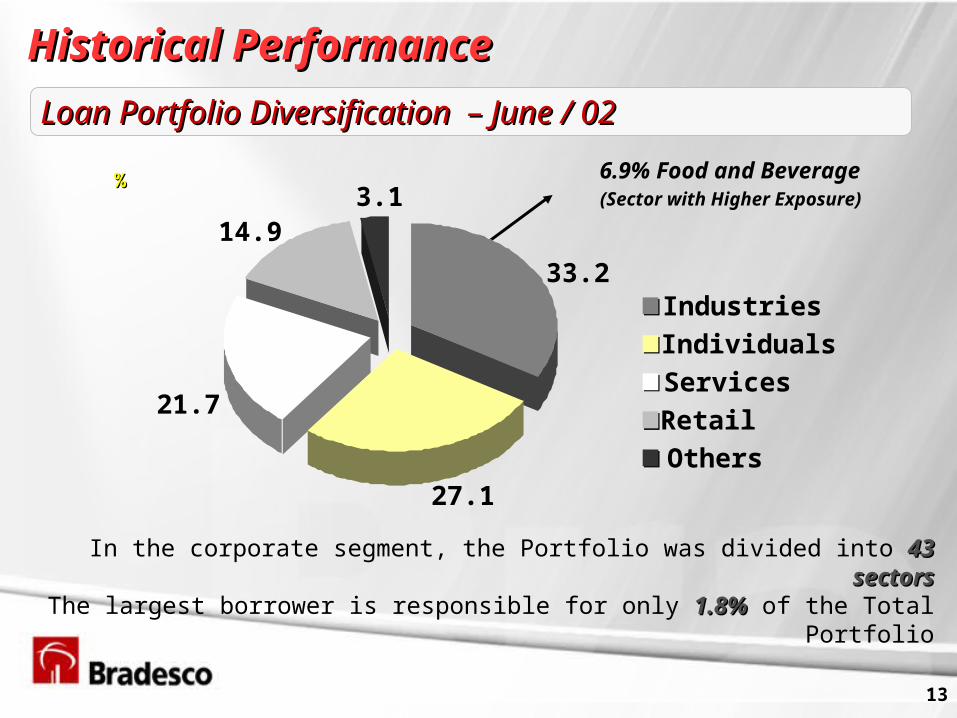

Loan Portfolio Diversification – June / 02Loan Portfolio Diversification – June / 02

In the corporate segment, the Portfolio was divided into 43 sectors43 sectorsThe largest borrower is responsible for only 1.8%1.8% of the Total Portfolio

6.9% Food and Beverage (Sector with Higher Exposure)

33.2

3.114.9

21.7

27.1

IndustriesIndividualsServicesRetailOthers

% %

Historical PerformanceHistorical Performance

14

Total Provisions cover 114.3%114.3% of Past Due and Falling Due Loans over 60 days

The Excess of Provisions for Loans amounts R$ 289 millionR$ 289 million

Asset QualityAsset Quality

9.9

90.1

9.3

90.7

8.9

91.1

1H 00 1H 01 1H 02

D - H

AA - C

%%

Historical PerformanceHistorical Performance

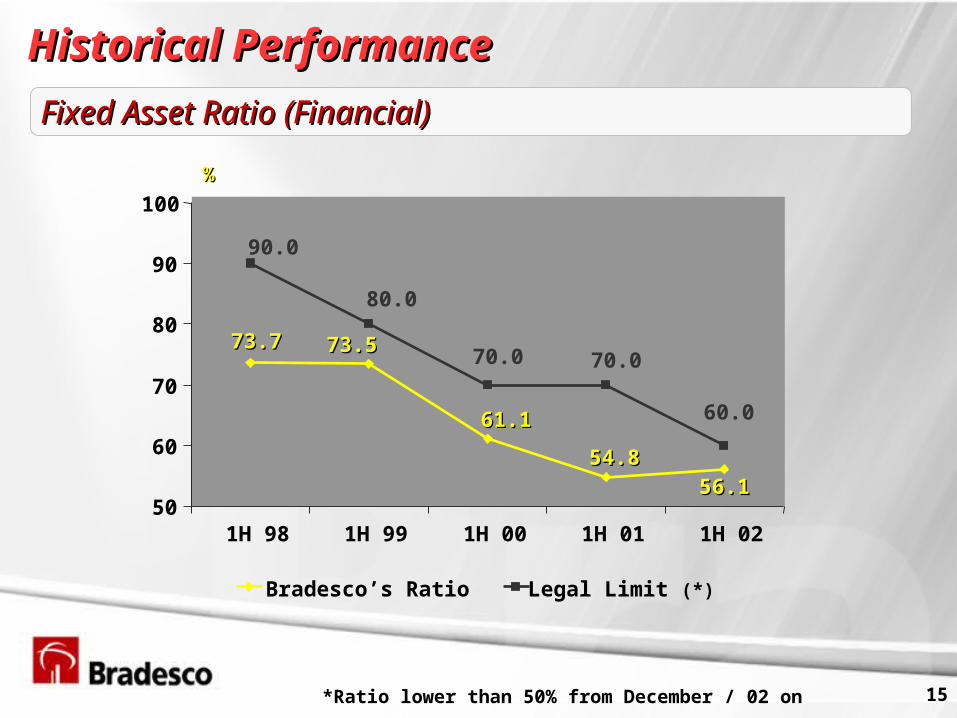

15*Ratio lower than 50% from December / 02 on

Fixed Asset Ratio (Financial)Fixed Asset Ratio (Financial)

56.156.154.854.8

61.161.1

73.573.573.773.770.0 70.0

60.0

80.0

90.0

50

60

70

80

90

100

1H 98 1H 99 1H 00 1H 01 1H 02

Bradesco’s Ratio Legal Limit (*)

%%

Historical PerformanceHistorical Performance

16

DepositsDeposits

50.850.8

36.936.933.633.634.134.1

26.926.9

6.6 7.1 10. 05.75.0

18.918.917.517.517.117.117.317.314.814.8

0

10

20

30

40

50

60

1H 98 1H 99 1H 00 1H 01 1H 02

Total Demand Savings Accounts

R$ BillionsR$ Billions

CAGR = 17.2%

Historical PerformanceHistorical Performance

17

On the 2nd Quarter 2002, Deposits increased by R$ 4.9 billionR$ 4.9 billion, of which R$ 3.5 billionR$ 3.5 billion migrated from Asset Management

Breakdown of Deposits – June / 02Breakdown of Deposits – June / 02

42.8

0.3

37.2

19.7

Time

Savings Accounts

Demand

Interbank

%%

Historical PerformanceHistorical Performance

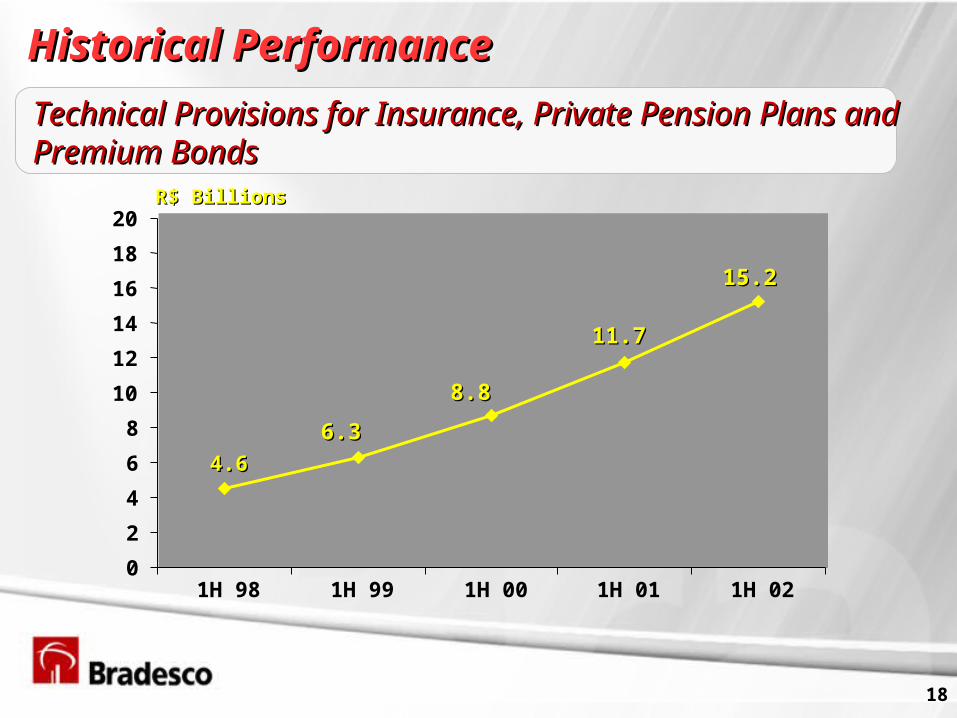

18

Technical Provisions for Insurance, Private Pension Technical Provisions for Insurance, Private Pension Plans and Premium BondsPlans and Premium Bonds

15.215.2

11.711.7

8.88.8

6.36.34.64.6

0

2

4

6

8

10

12

14

16

18

20

1H 98 1H 99 1H 00 1H 01 1H 02

R$ BillionsR$ Billions

Historical PerformanceHistorical Performance

19

Stockholders’ EquityStockholders’ Equity

R$ BillionsR$ Billions

10.110.19.19.1

7.07.06.86.86.16.1

0

5

10

15

1H 98 1H 99 1H 00 1H 01 1H 02

Historical PerformanceHistorical Performance

20

17.117.116.516.5

14.114.113.413.4

14.7*14.7*

10

11

12

13

14

15

16

17

18

1S 98 1S 99 1S 00 1S 01 1S 02

*Tier I: 12.2% Tier II: 2.5%

BIS Ratio (Financial)BIS Ratio (Financial)

%%

Legal Limit (Brazil)Legal Limit (Brazil)

Historical PerformanceHistorical Performance

21

Recurring Net IncomeRecurring Net Income

904904

1,0421,042

606606

461461431431

200

400

600

800

1,000

1,200

1H 98 1H 99 1H 00 1H 01 1H 02

R$ MillionsR$ Millions

Historical Historical Performance Performance

22

Recurring ROE (Annualized)Recurring ROE (Annualized)

%%

18.718.7

24.124.1

19.019.0

14.014.014.614.6

10

15

20

25

30

1H 98 1H 99 1H 00 1H 01 1H 02

Historical PerformanceHistorical Performance

23

Recurring ROA (Annualized)Recurring ROA (Annualized)

%%

1.51.5

2.12.1

1.41.4

1.21.21.31.3

1.0

1.5

2.0

2.5

1H 98 1H 99 1H 00 1H 01 1H 02

Historical PerformanceHistorical Performance

24

Operating Expenses / Average AssetsOperating Expenses / Average Assets

4.04.0

3.33.3

3.63.63.53.5

3.23.2

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1H 98 1H 99 1H 00 1H 01 1H 02

%%

Historical PerformanceHistorical Performance

25

Efficiency Ratio (Recurring)Efficiency Ratio (Recurring)

56.656.6

53.553.5

58.558.5

55.655.6 55.355.3

50

52

54

56

58

60

1H 98 1H 99 1H 00 1H 01 1H 02

%%

Historical PerformanceHistorical Performance

26

Insurance GroupInsurance Group

95.495.4

99.499.4100.7100.7

106.7106.7

89.389.3

96.995.9

91.9

98.2

91.9

86

90

94

98

102

106

110

1S 98 1S 99 1S 00 1S 01 1S 02

Combined Ratio - International

Extended Combined Ratio

%%

Historical PerformanceHistorical Performance

27

Insurance, Private Pension PlansInsurance, Private Pension Plans,, and Premium Bondsand Premium Bonds

1H 011H 01 1H 02 1H 02

Auto/RCF

Health

Life and Private Pension Plans

Premium Bonds

R$ 724 million

R$ 989 million

R$ 1.50 billion

R$ 485 millionR$ 1.29billion

+10.8%

+15.3%

+28.0%

ChangeChange

Result R$ 324 million +6.5%

VGBL (Launched on March / 02): 47,767participants and sales of R$ 476 million

Provisions:

R$ 802 million

R$ 1.14 billion

R$ 1.92 billion

R$ 422 millionR$ 1.37 billion

R$ 345 million

-13.0%+6.2%

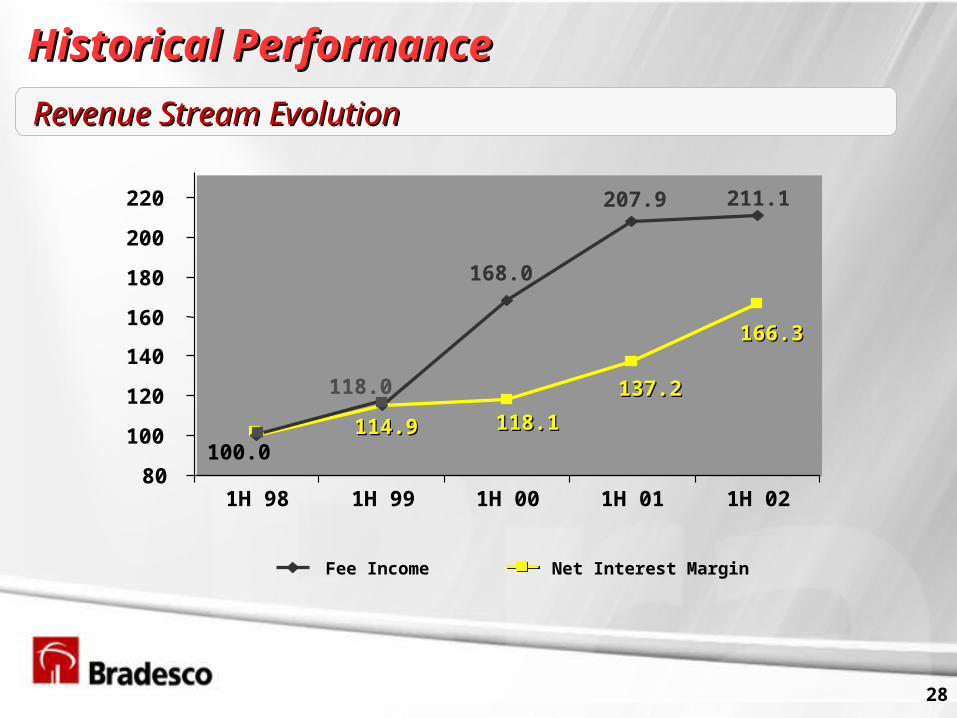

28

Revenue Stream EvolutionRevenue Stream Evolution

211.1207.9

168.0

114.9114.9 118.1118.1

137.2137.2

166.3166.3

118.0

80

100

120

140

160

180

200

220

1H 98 1H 99 1H 00 1H 01 1H 02

100.0

Fee Income Net Interest Margin

Historical PerformanceHistorical Performance

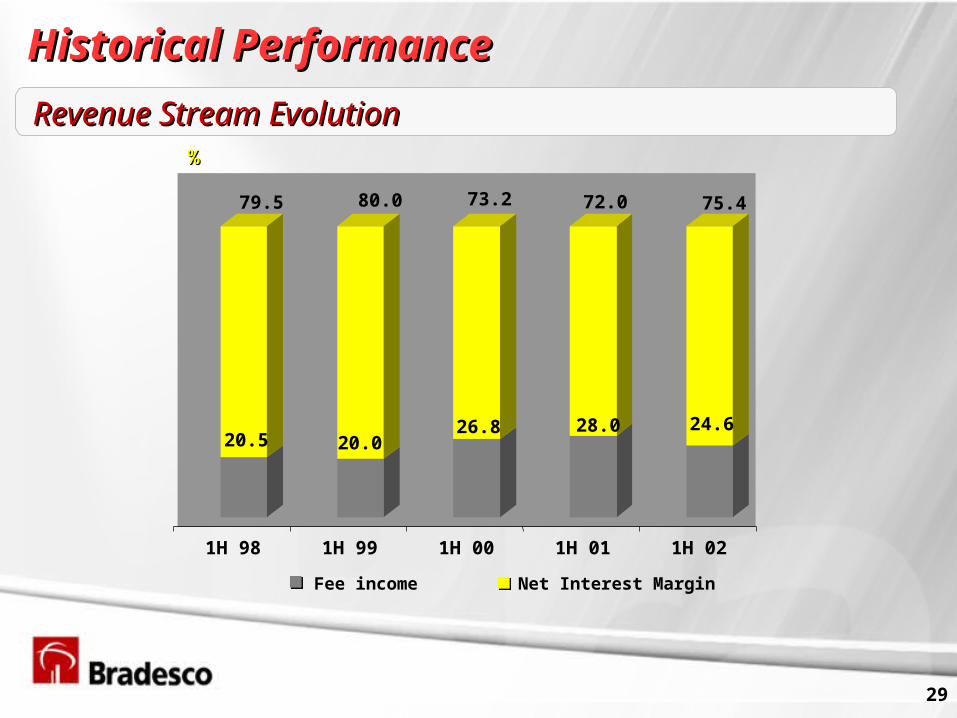

29

Historical PerformanceHistorical Performance

20.5

79.5

20.0

80.0

26.8

73.2

28.0

72.0

24.6

75.4

1H 98 1H 99 1H 00 1H 01 1H 02

Fee income Net Interest Margin

Revenue Stream EvolutionRevenue Stream Evolution%%

30

Cash GenerationCash Generation

3.63.63.53.5

2.82.8

3.63.6

2.22.2

0

1

2

3

4

5

1H 98 1H 99 1H 00 1H 01 1H 02

R$ BillionsR$ Billions

Historical PerformanceHistorical Performance

31

Outstanding Performance of First Half / 02Outstanding Performance of First Half / 02

International Area Market Share:

21.4%21.4% of Exports and 9.8%9.8% of Imports

Finance Portfolio: US$ 6.0 billionUS$ 6.0 billion (including onlendings)

Credit Cards R$ 5.4 billionR$ 5.4 billion of Gains

Increase of 26% 26% during the period

Capital Markets Market Share: 73.2%73.2% of Issuance registered with CVM

Secondary Public Offering of Voting Shares of CVRD (March / 02 : R$ 4.5 billionR$ 4.5 billion)

32

AgendaAgenda

ABAMEC Bradesco 2001ABAMEC Bradesco 2001

Historical PerformanceHistorical Performance

Main Events Main Events

Competitive AdvantagesCompetitive Advantages

ManagementManagement Characteristics Characteristics

PerspectivesPerspectives

33

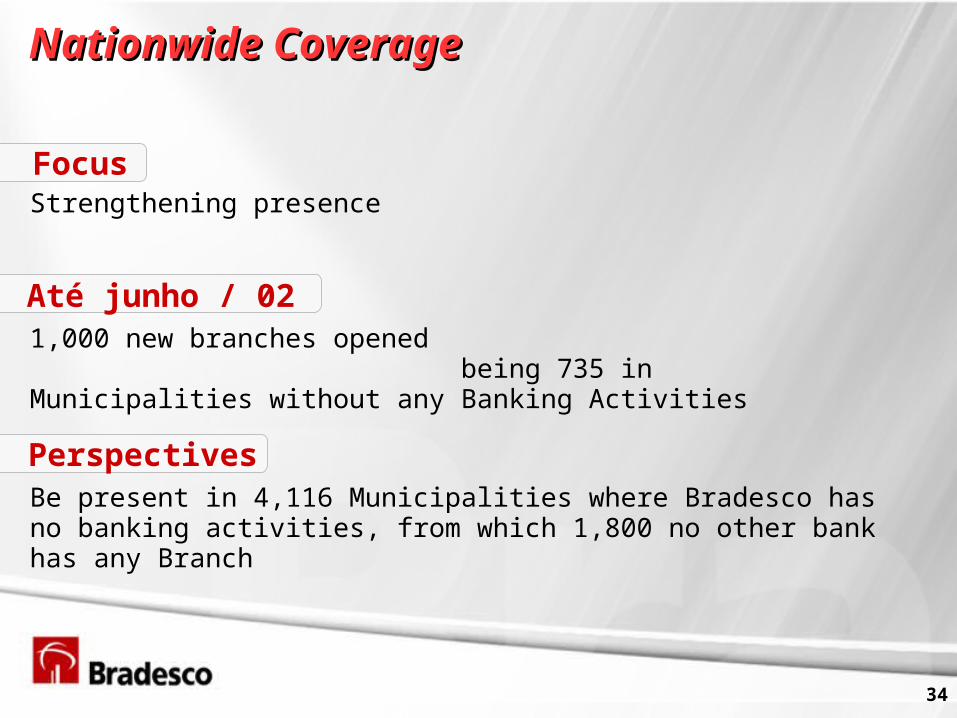

34

Nationwide CoverageNationwide Coverage

FocusStrengthening presence

Até junho / 021,000 new branches opened being 735 in Municipalities without any Banking Activities

PerspectivesBe present in 4,116 Municipalities where Bradesco has no banking activities, from which 1,800 no other bank has any Branch

35

Bradesco

36

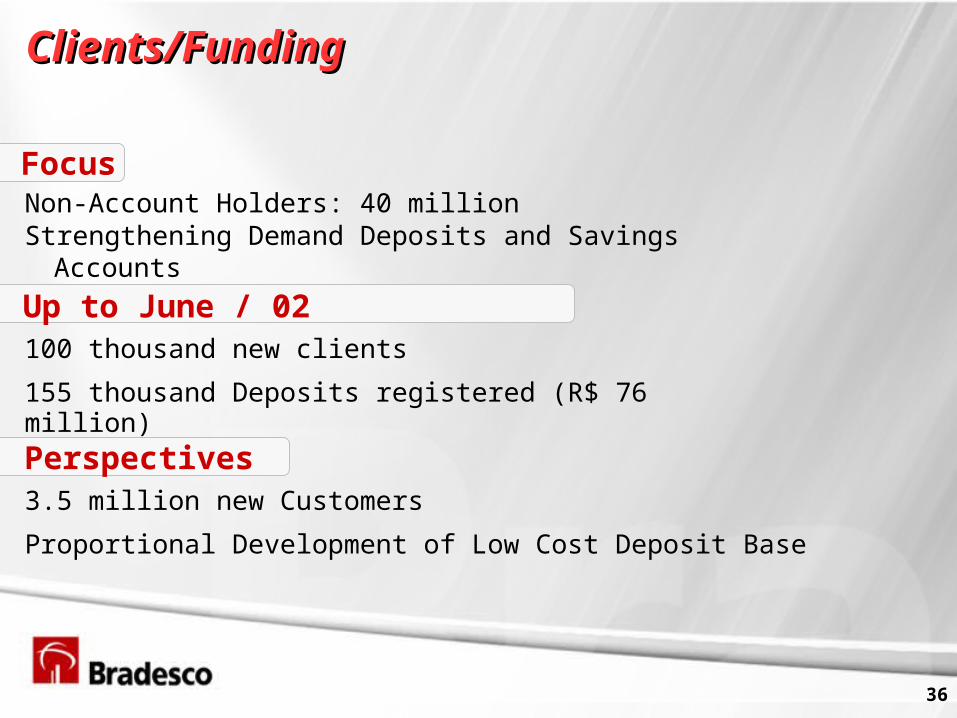

Clients/FundingClients/Funding

FocusNon-Account Holders: 40 millionStrengthening Demand Deposits and Savings Accounts

Up to June / 02100 thousand new clients

155 thousand Deposits registered (R$ 76 million)

Perspectives3.5 million new Customers

Proportional Development of Low Cost Deposit Base

37

EfficiencyEfficiency

FocusTo reduce the cost of a new Bradesco Branch, representing at least R$ 150 thousand for a Instore Branch

Up to / 02Initial Cost for Opening 5,299 Branches stood at R$ 200 million

Perspectives2,000 Branches on the 2nd Half

Targeting of High Net Worth Individuals in Regions that are not explored by Banks

Finding Prospect Regions / Potential Markets

Fostering the Local Economy

Other Benefits

38

39

Banco Mercantil de São PauloBanco Mercantil de São PauloFocusAcquisition of differentiated Client Base and the FINASA brandSynergy GainsStrengthening presence in the Automobile Financing Industry

Up to June / 02The Evolution of Client Base in June (725 thousand 87% Individuals)17 Departments and Areas have already been IntegratedLoan Portfolio reaches R$ 1.1 Billion

PerspectivesStrengthening the utilization of the brand FINASA and the sales of products, particularly the Insurance Related ones

Increase in Scale

Increase in Market Share

40

41

AgendaAgenda

ABAMEC Bradesco 2001ABAMEC Bradesco 2001

Historical PerformanceHistorical Performance

Main Events Main Events

Competitive AdvantagesCompetitive Advantages

Management CharacteristicsManagement Characteristics

PerspectivesPerspectives

42

Program of Goals

Sales Sales ManagementManagement

ClientsClients

Loyalty&

Retention

The points are

accounted just in

case of

Excellence of

Customer

Satisfaction

BusinessesBusinesses ResultsResults Customer Customer SatisfactionSatisfaction

Funding

Cards

Insurance

Life &Private

Pension Plans

Annuities

Efficiency Ratio

Revenue Growth

Loans Recoveries

Balanced Performance Index

23 goals23 goals have to be followed by the 22 Regional Directors 22 Regional Directors and their related Branches

GDAD:GDAD: A System of Evaluation and Planning the Budget of Bradesco

43

Where, How Much and How the Bank Gains

ABC System MethodologyABC System Methodology(Activity-Based Costing)(Activity-Based Costing)

Identifies and Clusters Activities Related to the Processes

Allocates Costs to the Activities Accordingto Demanded Resources

Turning Departments into Results Centers

Costs Costs ManagementManagement

44

Risk Risk ManagementManagementCredit Risk

Credit Granting

BranchesCredit

Department

Daily Credit

Committee

ExecutiveCredit

Committee

Credit Score

Up to R$ 6 million

Between R$ 6 and 20 million

Over R$ 20 million

45

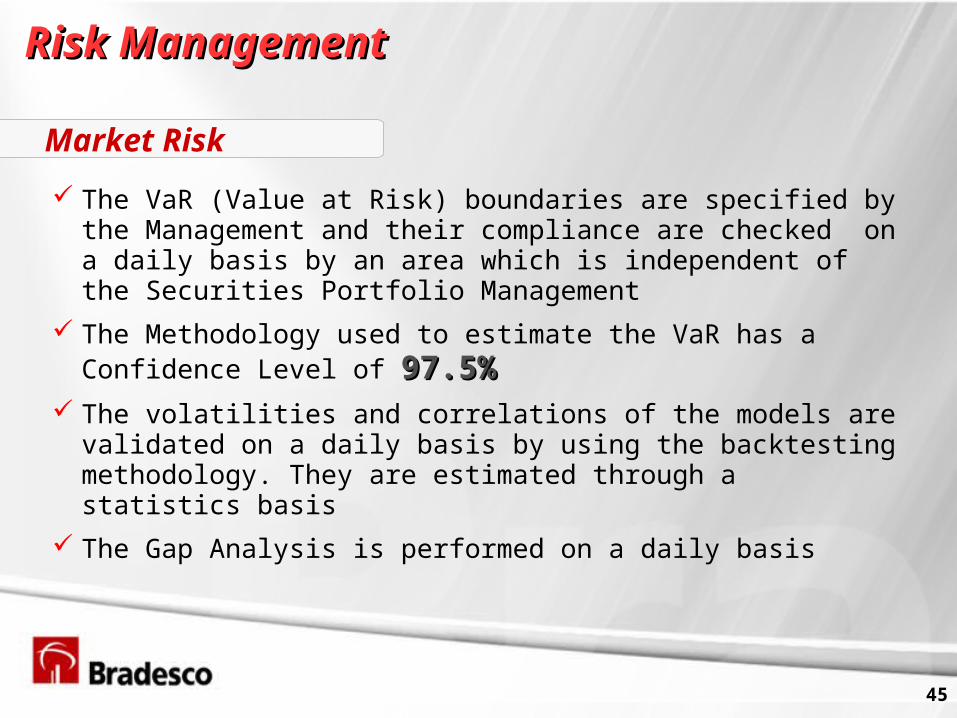

Market Risk

The VaR (Value at Risk) boundaries are specified by the Management and their compliance are checked on a daily basis by an area which is independent of the Securities Portfolio Management

The Methodology used to estimate the VaR has a Confidence Level of 97.5%97.5%

The volatilities and correlations of the models are validated on a daily basis by using the backtesting methodology. They are estimated through a statistics basis

The Gap Analysis is performed on a daily basis

Risk Risk ManagementManagement

46

Risks inherent to the activities that support businesses related to data processing and communication, transmission, and registration of data electronically

Business Disruption Systems Fail Errors Omissions Frauds External Events

Auditing Committee composed by members of the Management and the Board

Operating Risk

Risk Risk ManagementManagement

47

Controls the Mismatches of Maturity of Assets and Liabilities

A Group of Controlling Tools Permanently Evaluates the Positions Accepted

Liquidity Risk

Risk Risk ManagementManagement

48

R$ Millions

Adjusted Stockholders’ Equity

Total Risk Weighted Assets

Weighted Assets

Weighted Compensation Accounts

BIS RatioBIS Ratio

11,594

79,143

76,540

2,603

14.65%14.65%

Capital Risk

Financial Consolidated

Risk Risk ManagementManagement

49

AgendaAgenda

ABAMEC Bradesco 2001ABAMEC Bradesco 2001

Historical PerformanceHistorical Performance

Main Events Main Events

Competitive AdvantagesCompetitive Advantages

Management CharacteristicsManagement Characteristics

PerspectivesPerspectives

50

Competitive AdvantagesCompetitive Advantages

Retail BankRetail Bank

Service BankService Bank

High Net Worth High Net Worth BankBank

Private BankPrivate Bank

(Bradesco Private)(Bradesco Private)

Corporate BankCorporate Bank(Bradesco Corporate(Bradesco Corporate)) ClientsClients

Distribution NetworkDistribution Network

TechnologyTechnology

Middle Market BankMiddle Market Bank(Bradesco Empresas)(Bradesco Empresas)

51

Professional Management, which Possesses a Vast Experience, in addition to Entrepreneurial Spirit

The Most Extensive portfolio, Providing Individuals and Companies with Insurance, Private Pension Plans, and Annuities

Solid Financial Structure, in addition to a Leadership Positioning in the Main Insurance and Banking Segments

Bradesco is a Bradesco is a Financial Conglomerate withFinancial Conglomerate with::

52

Bradesco Seguros has more than over 67 years of Experience

Bradesco, BCN, and Mercantil Distribution Network

8.5 million Insurance Customers

Approximately 23,000 Independent Brokers

Works as a Bankinsurance Works as a Bankinsurance Conglomerate...Conglomerate...

53

The Most Extensive Array of The Most Extensive Array of Services...Services...

R$ 102.5 billion

R$ 41.5 billion

R$ 75 billion

R$ 42 billion

R$ 56.9 billion

Collections:

Balance of Collections:

Payments of Suppliers:

Payment of Taxes:

Custody Services:

54

State of the Art State of the Art Technology…Technology…

108.7108.7

245.8245.8

398.8398.8354.9354.9

234.6234.6

80

160

240

320

400

480

1H 98 1H 99 1H 00 1H 01 1H 02

R$ MillionsR$ Millions

InvestmentsInvestments

55

Telebanco

Bradesco.com

Through Alternative Channels Through Alternative Channels

4.3 million Heavy Users 121.8 million TransactionsR$ 4.7 billion Operations

ShopCreditShopCredit180 thousand TransactionsR$ 51 million Operations

BradescoNetBradescoNetEmpresaEmpresa

598 thousand Transactions24,196 Clients that Operates ActivelyR$ 1.1 billion Operations

ShopFácilShopFácil6.8 million TransactionsR$ 521 million Operations

InternetInternetBankingBanking

142 thousand Transactions498 thousand SubscribersR$ 674 million Operations

ShopInvestShopInvest

114.6 million Calls2.4 million UsersR$ 2.0 billion Transactions

56

ElectronicTransmission

11.5 Branches17.7

Direct Debit1.6

Call Center (Telebanco)11.3

Internet Banking

8.5

ATMs49.5

June / 02%%

Millions of Transactions

ATMs 756.5Branches 269.9

Call Center (Telebanco) 172.8Internet Banking 129.5Direct Debit 24.2

TotalTotal 1,528.31,528.3

Electronic Transmission 175.5

Through Alternative Channels Through Alternative Channels

57

AgendaAgenda

ABAMEC Bradesco 2001ABAMEC Bradesco 2001

Historical PeriodHistorical Period

Main Events Main Events

Competitive AdvantagesCompetitive Advantages

Management CharacteristicsManagement Characteristics

PerspectivesPerspectives

58

PerspectivesPerspectives

MinimizeMinimizeCostsCosts

Maximize Maximize SalesSales

ABC Methodology

Efficiency Ratio: 50%

Integration ofBack Offices

Asset Quality

Alternative Channels

Cross Selling

Customer Satisfaction

Continuous Improvement of the Portfolio of Products / Services

Postal Bank:Non-Account Holders

Segmentation

Organic Growth x AcquisitionsOrganic Growth x AcquisitionsBankasuranceBankasurance

59

ContactsContacts

XX - 11 - 3684-9229 3684-9302 3684-2086 3684-9231

Email Email ::

Investor Relations AreaInvestor Relations Area

www.bradesco.com.br

Phones:Phones:

This presentation contains forward-looking statements. Such statements are not This presentation contains forward-looking statements. Such statements are not statements of historical fact, and reflect the beliefs and expectations of the statements of historical fact, and reflect the beliefs and expectations of the Company's management. The words "anticipates", "believes", "estimates", Company's management. The words "anticipates", "believes", "estimates",

"expects", "forecasts", "intends", "plans", "predicts", "projects", "targets" and "expects", "forecasts", "intends", "plans", "predicts", "projects", "targets" and similar words are intended to identify these statements, which necessarily involve similar words are intended to identify these statements, which necessarily involve

known and unknown risks and uncertainties. Known risks and uncertainties known and unknown risks and uncertainties. Known risks and uncertainties include, but are not limited to, the impact of competitive services and pricing, include, but are not limited to, the impact of competitive services and pricing,

market acceptance of services, service transitions by the Company and its market acceptance of services, service transitions by the Company and its competitors, regulatory approval, currency fluctuations, changes in service mix competitors, regulatory approval, currency fluctuations, changes in service mix offered, and other risks described in the Company's registration statement and offered, and other risks described in the Company's registration statement and other Securities and Exchange Commission filings. Forward-looking statements other Securities and Exchange Commission filings. Forward-looking statements

speak only as of the date they are made, and Banco Bradesco does not undertake speak only as of the date they are made, and Banco Bradesco does not undertake any obligation to update them in light of new information or future developments.any obligation to update them in light of new information or future developments.

60