1 blueprint for bir development towards 2010. where we want to be tax effort ratio must rise from...

TRANSCRIPT

1

BLUEPRINT for BIR BLUEPRINT for BIR Development Development Towards 2010Towards 2010

Where We Want to Be Where We Want to Be

Tax Effort Ratio Must Rise from the Fall: Country Tax Effort Ratio Must Rise from the Fall: Country must regain No. 2 spot in the Region if not bettermust regain No. 2 spot in the Region if not better

Quality of Governance: World ClassQuality of Governance: World Class

Taxpayer Consciousness: Well-Informed and Self Taxpayer Consciousness: Well-Informed and Self Motivated to be Tax CompliantMotivated to be Tax Compliant

… … our Strategyour Strategy

Work ProgramWork Program for 2003 and Beyondfor 2003 and Beyond

I. Effective Taxpayer Compliance SystemsI. Effective Taxpayer Compliance Systems

Expansion of E-ServicesExpansion of E-Services

BIR-COA Leadership in Computerization and BIR-COA Leadership in Computerization and

Government ProcurementGovernment Procurement

Reforms in Business Tax Compliance ProcessesReforms in Business Tax Compliance Processes

Resolution of Industry IssuesResolution of Industry Issues

Better Taxpayer Education, Information and AssistanceBetter Taxpayer Education, Information and Assistance

Strategic Directions: From Where We Strategic Directions: From Where We

Are to Where We Want to BeAre to Where We Want to Be

Internet

BIReFPS

Banks

Taxpayer

in his office

/home/eCafe

Payment Confirmation

The First Genuine ePayment System The First Genuine ePayment System in our Governmentin our Government

• Electronic submission of tax return

• Electronic Debit Instruction by the Taxpayer from his terminal

• Automatic debit of tax payment from taxpayer account

• Automatic credit of collections to Bureau of Treasury account

• Automatic reporting of collections to BIR

• Available 24 x 7

Awarding to AyalaPort

April 23, 2003

Deployment of the New Expanded EFPS by Oct 31, 2003

Migration to the Internet Data Center by Aug 1, 2003

Review and Design of new eFPS June 30, 2003

eFiling and ePayment for Top 1000 of 43 Computerized RDOs by Dec 31, 2003

eFiling and ePayment of Top 1000 Taxpayers of All RDOs by Dec 31, 2004

eFiling and ePayment of all Taxpayers by 2005

Total Outsourcing of eFPS to an IDCEnhancement & Expansion + Capacity on Demand + More BIR Forms + All taxpayers

Long Range VisionLong Range Vision

• Taxpayer Has Many ChoicesTaxpayer Has Many Choices

• Anytime - AnywhereAnytime - Anywhere

Business Processes Needing Reform:Business Processes Needing Reform:

The Tax Compliance ProcessThe Tax Compliance Process

Registration Registration of CRM/POSof CRM/POS

&/or Securing &/or Securing of ATPof ATP

Issuance of Issuance of Receipts/ Receipts/ InvoicesInvoices

Recording and Recording and Reporting of Reporting of

SalesSales

Declaration of Declaration of Business TaxesBusiness Taxes

Encouraging the issuance of Encouraging the issuance of proper ORsproper ORs

3) Text raffle promo3) Text raffle promo

4) Business Education 4) Business Education “Infomercials/posters/etc”“Infomercials/posters/etc”

5) Modified TCVD5) Modified TCVD

On-Going Projects to ImproveOn-Going Projects to Improve

Tax Compliance in Business: Tax Compliance in Business:

A Holistic ApproachA Holistic Approach

Controlling RegistrationControlling Registration

1)1) Amending RR 10-99 “Accrediting Amending RR 10-99 “Accrediting a model of machine”a model of machine”

2)2) Electronic RegistrationElectronic Registration

Making sure businesses Making sure businesses properly report salesproperly report sales

6) Reporting of Machine 6) Reporting of Machine Readings thru Mobile Readings thru Mobile PlatformsPlatforms

7) Reform on Summary 7) Reform on Summary List SubmissionList Submission

Audit/selection methodAudit/selection method

8) Tax Compliance 8) Tax Compliance Report CardReport Card

9) 9) Intensified Audit of Intensified Audit of “Off-Benchmark” “Off-Benchmark” CompaniesCompanies

10) No Contact Audit10) No Contact Audit

Registration of Registration of CRM/POSCRM/POS

&/or Securing of &/or Securing of ATPATP

IIssuance of ssuance of Receipts/ Receipts/ InvoicesInvoices

Recording and Recording and Reporting of SalesReporting of Sales

Declaration of Declaration of Business TaxesBusiness Taxes

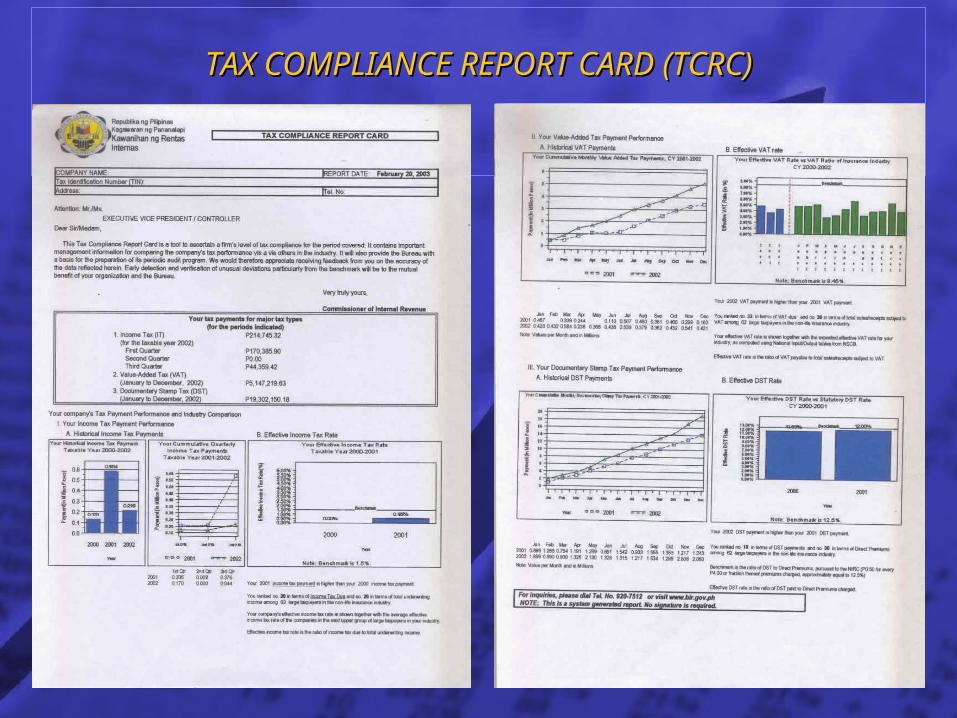

TAX COMPLIANCE REPORT CARD (TCRC)TAX COMPLIANCE REPORT CARD (TCRC)

TCRCTCRCMessageMessage

This Tax Compliance Report Card is a tool to ascertain a firm’s level of tax compliance for the This Tax Compliance Report Card is a tool to ascertain a firm’s level of tax compliance for the period covered. It contains important management information for comparing a company’s tax period covered. It contains important management information for comparing a company’s tax performance vis-à-vis others in the industry. It will also provide the Bureau with a performance vis-à-vis others in the industry. It will also provide the Bureau with a basis for the basis for the selection of companies for auditselection of companies for audit considering that it is the Bureau’s policy to focus its audit considering that it is the Bureau’s policy to focus its audit effort on less compliant taxpayers. We would therefore appreciate receiving feedback from you on effort on less compliant taxpayers. We would therefore appreciate receiving feedback from you on the accuracy of the data reflected herein. Early detection and verification of unusual deviations the accuracy of the data reflected herein. Early detection and verification of unusual deviations particularly from the benchmarks will be to the mutual benefit of your organization and the Bureau.particularly from the benchmarks will be to the mutual benefit of your organization and the Bureau.

Very truly yours,Very truly yours,

Commissioner of Internal RevenueCommissioner of Internal Revenue

Fax On Demand E-mail Web Interface

KnowledgeDB

BIR Contact Center: Taxpayer Information & Education

TP Contacts BIR

Contact Center Agent

responds to questions

Telephone

II. Effective Detection & Elimination of Revenue LeakagesII. Effective Detection & Elimination of Revenue Leakages

Third Party Information - Computer Linkages & Data Third Party Information - Computer Linkages & Data

MatchingMatching

–Expansion and Better Utilization of Existing TPI Expansion and Better Utilization of Existing TPI Databases: Quarterly Schedule of Sales Purchases, Databases: Quarterly Schedule of Sales Purchases, Imports DB, Government Purchases, Interest Payments to Imports DB, Government Purchases, Interest Payments to Foreign Creditors, Mortgaged Foreclosed Properties, etc. Foreign Creditors, Mortgaged Foreclosed Properties, etc.

–Expansion of Taxpayers Database: Joint Projects with Expansion of Taxpayers Database: Joint Projects with LGUs, BLGF; LRA and RPTA DB, LLDA, PDIC, BSP, SECLGUs, BLGF; LRA and RPTA DB, LLDA, PDIC, BSP, SEC

–Use of Government and Other Databases: SEC, BOI, Use of Government and Other Databases: SEC, BOI, LRA, LTO, PSE, BSP, SRA, Mines & Geo-Sciences Bureau, LRA, LTO, PSE, BSP, SRA, Mines & Geo-Sciences Bureau, DOE, National Tobacco AdministrationDOE, National Tobacco Administration

Our StrategyOur Strategy

TPI-RELIEF:TPI-RELIEF:

A FIRST NO CONTACT AUDIT SYSTEMA FIRST NO CONTACT AUDIT SYSTEM

Firm A’s Firm A’s Summary Summary

List of List of PurchasesPurchases

Supplier 1Supplier 1 22 33 .. .. nn

RELIEFRELIEF

Undeclared Undeclared VAT DueVAT Due

Letter NoticesLetter Notices

ITSITS

Report onReport onNon-VAT SuppliersNon-VAT Suppliers(disqualified input VAT)(disqualified input VAT)

•Supplier’s particulars are Supplier’s particulars are

matched with registration matched with registration

database to trap unqualified database to trap unqualified

input VATinput VAT

Firm B’s Firm B’s Summary Summary

List of SalesList of Sales

RELIEFRELIEF

Undeclared Undeclared VAT DueVAT Due

Letter NoticesLetter Notices

ITSITS

Report onReport onSales-PurchaseSales-Purchase

Discrepancy of “B”Discrepancy of “B”

- TPI -- TPI -Purchases Purchases

of GA’sof GA’s

DPWHDPWHDBMDBMDECSDECSDNDDND

othersothers

•Government and Large Taxpayers Government and Large Taxpayers

purchase database matched with purchase database matched with

supplier’s declared sales to trap supplier’s declared sales to trap

undeclared sales and unpaid taxesundeclared sales and unpaid taxes

TPI-RELIEF:TPI-RELIEF:

A FIRST NO CONTACT AUDITA FIRST NO CONTACT AUDIT SYSTEMSYSTEM

II. Effective Detection & Elimination of Revenue LeakagesII. Effective Detection & Elimination of Revenue Leakages

Strengthening of Withholding Tax Remittance, TCC/TDM Strengthening of Withholding Tax Remittance, TCC/TDM

and Revenue Accounting Systemsand Revenue Accounting Systems

Repair or Enhancement of Existing Detection SystemsRepair or Enhancement of Existing Detection Systems

–Stop Filers Task Force Detect Diverted Payments Stop Filers Task Force Detect Diverted Payments and Take Action on Non-Filersand Take Action on Non-Filers

–Delinquent Accounts SystemDelinquent Accounts System

–Case Management SystemCase Management System

Our StrategyOur Strategy

III. Intensified EnforcementIII. Intensified Enforcement Focused, Specialized and Short Duration AuditsFocused, Specialized and Short Duration Audits

RevalidaRevalida

Our StrategyOur Strategy

Special Operations on High Profile Evaders Special Operations on High Profile Evaders

Closure of Companies and Filing of Criminal CasesClosure of Companies and Filing of Criminal Cases

Separation of Enforcement Group from Legal GroupSeparation of Enforcement Group from Legal Group

IV. BIR-Private Sector Good and Honest Governance ProgramIV. BIR-Private Sector Good and Honest Governance Program

Tax Campaign and Information DisseminationTax Campaign and Information Dissemination

Completion of Process Re-engineering ProjectsCompletion of Process Re-engineering Projects

Web-based TIN application and processingWeb-based TIN application and processing

BIR-Private Sector Project Monitoring and Implementation BIR-Private Sector Project Monitoring and Implementation Unit (i.e. PRA, Huwag Tax-sil, Action for Economic Unit (i.e. PRA, Huwag Tax-sil, Action for Economic Reforms, MBC, PCCI, FCCC, BAP, MAP, FOCIG, Rotary Reforms, MBC, PCCI, FCCC, BAP, MAP, FOCIG, Rotary Club, etc.)Club, etc.)

Simplification of Tax Administration: Manual of Bank Simplification of Tax Administration: Manual of Bank Products; Manual of Tax Liabilities for Large TaxpayersProducts; Manual of Tax Liabilities for Large Taxpayers

Codification of Regulations and RulingsCodification of Regulations and Rulings

Our StrategyOur Strategy

V. Organizational AdjustmentsV. Organizational Adjustments Strengthening of the Large Taxpayer ServiceStrengthening of the Large Taxpayer Service

Regular Performance Review of RDs and RDOsRegular Performance Review of RDs and RDOs

Collaboration with RIPS, Ombudsman and PCAGC on Collaboration with RIPS, Ombudsman and PCAGC on lifestyle checklifestyle check

COA, BOI and other regulatory agencies’ support on COA, BOI and other regulatory agencies’ support on tax compliance of government projectstax compliance of government projects

Outsourcing of certain operations : eFPS; Computer Outsourcing of certain operations : eFPS; Computer Facilities ManagementFacilities Management

Technical Assistance from Donor Agencies: WB; Technical Assistance from Donor Agencies: WB; CIDA; IMFCIDA; IMF

Our StrategyOur Strategy

VI. Active Support to Legislative Revenue MeasuresVI. Active Support to Legislative Revenue Measures

Excise Tax IndexationExcise Tax Indexation

Transparency BillTransparency Bill

VAT on SugarVAT on Sugar

Mandatory recognition of role of BIR taxes in Mandatory recognition of role of BIR taxes in

government projectsgovernment projects

Our StrategyOur Strategy