1 cancellation of debt for individuals - presentation for enrolled agents october 16, 2008 tucson,...

TRANSCRIPT

1

Cancellation of Debt for

Individuals - Presentation

for Enrolled Agents

October 16, 2008

Tucson, AZby Tom Rex CPA

2

General Overview

Cancellation Of Debt for Individuals

3

Where are you in the matrix?

Know where you are so you don’t get lost.

It’s easy to go down the wrong rabbit hole! esp. with PDF documents and hyperlinks

4

New IRS Pub 4681

Issued in June 2008

5

COD income

Taxable unless there’s an Exception or Exclusion (these are all defined)

If there’s an exclusion, then taxpayer must reduce the tax attributes

In other words, if no exceptions or exclusions, COD is taxable income! It’s helpful to think in both directions.

per Pub 4681, page 3 6

Canceled debts -

General rule COD income in whole or in part is taxable

unless exceptions or exclusions apply

E.g., discounts and loan modifications that includes principal reduction (personally liable or not)

Taxable as COD income unless exceptions or exclusions apply

per Pub 4681, page 3 and 4 7

Canceled debts -

Exceptions Amounts Otherwise Excluded From Income Student Loans Deductible Debt Price Reduced After Purchase

These exceptions apply before the exclusions

8

If there’s an exclusion

Which one to use?

Which elections to make for part I of Form 982

How much is excluded? Depends There may be an exclusion limitation

Exclusions are for amount on part I, line 2 of Form 982

per IRC sec. 108 9

COD - exclusions

Title 11 bankruptcy case Insolvency Qualified farm indebtedness Qualified real property business

indebtedness Qualified principal residence indebtedness

Extended through 2012

10

Ordering of exclusions

Bankruptcy InsolvencyQualified Farm

Indebtedness

Qualified Real Property Business Indebtedn

ess

Qualified Principal Residenc

e Indebtedn

ess

Bankruptcy yes n/a n/a n/a n/a

Insolvency n/a 1st n/a n/a election

Qualified Farm Indebtedne

ssn/a 2nd yes n/a could be in part

Qualified Real Property Business

Indebtedness

n/a 2nd n/a election could be in part

Qualified Principal

Residence Indebtedne

ss

n/a election could be in part could be in part 1st

Per Form 982, and instructions 11

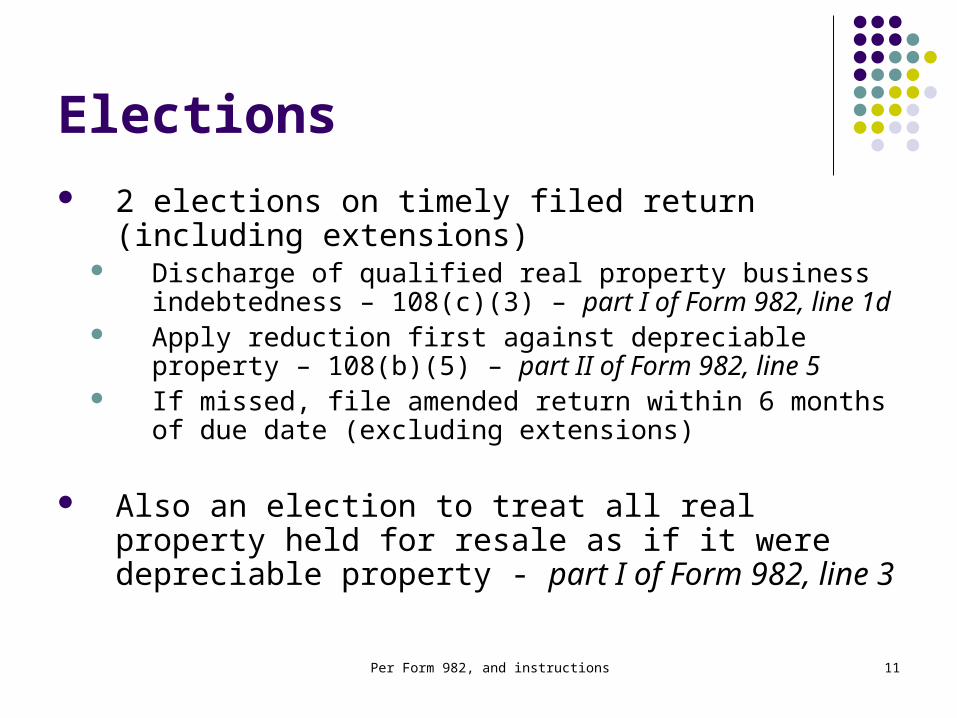

Elections

2 elections on timely filed return (including extensions)

Discharge of qualified real property business indebtedness – 108(c)(3) – part I of Form 982, line 1d

Apply reduction first against depreciable property – 108(b)(5) – part II of Form 982, line 5

If missed, file amended return within 6 months of due date (excluding extensions)

Also an election to treat all real property held for resale as if it were depreciable property - part I of Form 982, line 3

per Pub 4681, starting on page 7 12

Reduction of tax attributes

Different for – Bankruptcy and Insolvency

Qualified principal residence debt

Qualified farm debt

Qualified real property business debt (election)

per Pub 4681, page 7 and 8 13

Reduction of tax attributes

For Bankruptcy and Insolvency - General ordering rules for reductions

How much is reduced? Can be less than the canceled debt excluded from income.

Reductions are made after taxes for year are calculated

Need to reduce bases proportionally for property, held as of beginning of next tax year.

per Pub 4681, pages 7, and 8-9 14

Reduction of tax attributes

Other rules for – Qualified principal residence debt

Basis of residence is reduced if still owned after cancellation

Qualified farm debt Same as for Bankruptcy and Insolvency except there are

different rules for basis reduction

Qualified real property business debt Reduce basis of depreciable real property, held as of

beginning of next tax year, unless disposed of earlier.

15

See the instructions to Form 982, page 2

If discharged debt being excluded is Qualified principal residence indebtedness

A non business debt, other than qualified principal residence indebtedness, such as a car loan or credit card debt, and No other tax attributes listed in Part II (other than

a basis in non depreciable property). Only for a title 11 case or when insolvent

Any other debt

16

If there are disposals Of secured assets -

Foreclosures and repossessions Is taxpayer personally liable or not?

Abandonments Is there a foreclosure or repossession later?

Of assets whose basis was reduced, it depends on which exclusion was used and when they were disposed of: Same year or subsequent year

Also, there could be recapture of basis reductions under Bankruptcy and Insolvency rules

17

Reporting

On which tax return does this all wind up? Depends on who the debtor is

Where could it go on the tax return? Anywhere

Gets complicated if there are there splits between personal and business or rentals?

per Pub 4681, page 3 18

Canceled debts later repaid

If canceled debt is later repaid May be able to file 1040X if the year the amount

was included in income is still open

19

IRS Guidance Prior to Pub 4681

May still be helpful

20

IRS Guidance Prior to Pub 4681

IRS Pubs 17 – federal income tax for individuals, chapter

12 (other income) 525 – taxable and nontaxable income, COD

under misc. income

For exclusions 908 – bankruptcy (and insolvency) 225 – farmers, chapter 3 334 – small businesses (schedule C) chapter 5

21

IRS Guidance Prior to Pub 4681

For qualified principal residence indebtedness -

IRS News Release IR 2008-17 FAQs on IRS website Instructions to revised Form 982 Pub 523 – selling your home

22

IRS Guidance Prior to Pub 4681

Other IRS Pubs 544 – sales and other dispositions of assets:

chapter 1 for Abandonments and Foreclosures and Repo’s

and chapter 3 for depreciation recapture 535 – business expenses (recapture) 551 – basis of assets

Adjusted basis Increases and decreases to basis

23

Form 982

Revised February 2008

24

Form 982 Part I

25

Form 982 Part I

Box 2 – amount excluded from gross income

Exclusion limitations for: Qualified farm indebtedness Qualified real property business indebtedness Qualified principal residence indebtedness

26

Form 982 – Part II

27

Form 982

Part II – Reduction of tax attributes

Dollar for each dollar, in general 33 1/3 cents for each dollar, for credits

28

Exclusions

29

Title 11 Bankruptcy Cases

Exclusion – 108(a)1(A)

per Pub 4681, page 4 and Form 982 instructions 30

Definition - Title 11 case

A title 11 case is a case under title 11 of the United States Code (relating to bankruptcy), but only if the taxpayer is under the jurisdiction of

the court in the case and the discharge of indebtedness is granted by

the court or is under a plan approved by the court.

31

Title 11 bankruptcy cases Chapter 12 – The chapter of the Bankruptcy Code providing for

adjustment of debts of a "family farmer," as that term is defined in the Bankruptcy Code. http://www.uscourts.gov/bankruptcycourts/bankruptcybasics/chapter12.html

Chapter 13 – The chapter of the Bankruptcy Code providing for adjustment of debts of an individual with regular income, often referred to as a "wage-earner" plan. Chapter 13 allows a debtor to keep property and use his or her disposable income to pay debts over time, usually three to five years. http://www.uscourts.gov/bankruptcycourts/bankruptcybasics/chapter13.html

per Pub 908, page 2 32

Title 11 bankruptcy casesIndividuals in Chapter 12 or 13

A separate estate, for tax purposes, is not created for an individual who files a petition under Chapter 12 or 13 of the Bankruptcy Code.

Continue to file the same federal income tax return that was filed prior to the bankruptcy petition.

Do not include any debt canceled (because of bankruptcy) in income on individuals return. However, they must reduce (to the extent that they have)

certain losses, credits or basis in property by the amount of canceled debt.

33

Title 11 bankruptcy cases Chapter 7 – The chapter of the Bankruptcy Code providing for

"liquidation," that is, the sale of a debtor's nonexempt property and the distribution of the proceeds to creditors. http://www.uscourts.gov/bankruptcycourts/bankruptcybasics/chapter7.html

Chapter 11 – A reorganization bankruptcy, usually involving a corporation or partnership. A Chapter 11 debtor usually proposes a plan of reorganization to keep its business alive and pay creditors over time. People in business or individuals can also seek relief in Chapter 11. http://www.uscourts.gov/bankruptcycourts/bankruptcybasics/chapter11.html

per Pub 908, page 2 34

Title 11 bankruptcy casesIndividuals in Chapter 7 or 11

A separate “estate” is created consisting of property that belonged to the individual before the filing date.

This bankruptcy estate is a new taxable entity, completely separate from the individual taxpayer.

See page 4 of Pub 908 for list of attribute carryovers the estate gets

If later dismissed, file 1040X

per Pub 908, pages 2 and 3 35

Responsibilities of the individual debtor under Chapter 7 or 11

The individual debtor, generally must file income tax returns during the period of the bankruptcy proceedings.

Do not include on those returns, the income, deductions, or credits belonging to the separate bankruptcy estate.

Also do not include as income on those returns, the debts canceled because of bankruptcy. However, the bankruptcy estate must reduce certain losses,

credits, and the basis in property (to the extent of these items) by the amount of canceled debt.

per Pub 4681, page 4 36

How to report the bankruptcy exclusion

Attach Form 982 to the respective federal income tax returns and check the box on line 1a.

Enter the total amount of debt canceled in the taxpayers title 11 bankruptcy case on line 2.

per Pub 4681, page 4 37

How to report the bankruptcy exclusion

The taxpayer must also reduce their tax attributes in Part II of Form 982 as explained under Reduction of Tax Attributes later.

38

Insolvency

Exclusion – 108(a)1(B)

per Pub 4681, page 4 39

Insolvency

Do not include a canceled debt in income to the extent that the taxpayer was insolvent immediately before the cancellation.

They were insolvent immediately before the cancellation to the extent that the total of all of their liabilities exceeded the FMV of all of their assets immediately before the cancellation.

per Pub 4681, page 4, 40

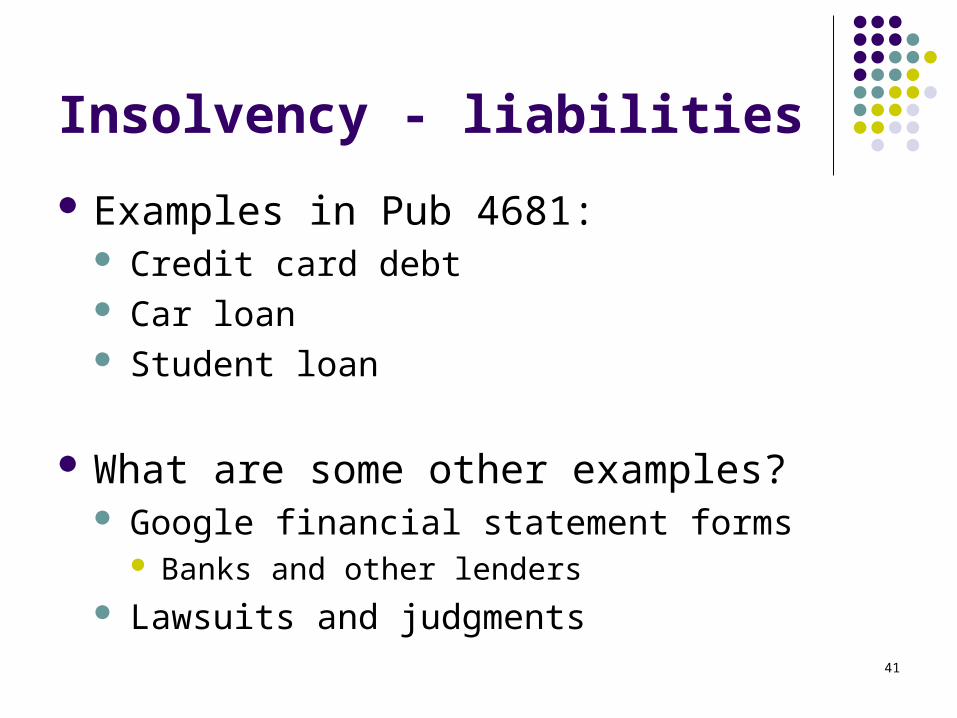

Insolvency - liabilities

Liabilities include: The entire amount of recourse debts, and The amount of nonrecourse debt that is not in excess of

the FMV of the property that is security for the debt.

Don’t forget taxes – Income taxes Property taxes Sales taxes, if a business Payroll taxes, if a business

41

Insolvency - liabilities

Examples in Pub 4681: Credit card debt Car loan Student loan

What are some other examples? Google financial statement forms

Banks and other lenders Lawsuits and judgments

per Pub 4681, page 4 42

Insolvency - assets

Assets include the value of everything the taxpayer owns including assets that serve as collateral for debt, and exempt assets which are beyond the reach of

their creditors under the law, such as their interest in a pension plan and the value of their retirement account.

43

Insolvency - assets

Examples of other assets on page 7 of Pub 4681 car at FMV furniture at FMV jewelry at FMV savings account

What are some other examples? Google financial statement forms

Banks and other lenders, e.g., John Deere’s, if farmer Lawsuits and judgments 1099 forms – indicators for financial assets

44

Fair market value IRS definition

Not defined in Pub 4681 Not defined in Pub 908

Per Pub 551 Basis of Assets FMV is the price at which property would change hands

between a buyer and a seller, neither having to buy or sell, and both having reasonable knowledge of all necessary

facts.

Also some guidance in Pub 526 for contributions of property http://www.irs.gov/pub/irs-pdf/p526.pdf

per Pub 4681, page 4 45

How to report the insolvency exclusion

Attach Form 982 to the taxpayer’s federal income tax return and check the box on line 1b.

On line 2, include the smaller of the amount of the debt canceled or the amount by which the taxpayer was

insolvent immediately before the cancellation.

per Pub 4681, page 4 46

How to report the insolvency exclusion

The taxpayer must also reduce their tax attributes in Part II of Form 982 as explained under Reduction of Tax Attributes later.

47

Insolvency exclusion

See examples on page 4 of Pub 4681

Greg

48

Reduction of tax attributes for

Bankruptcy and Insolvency

per Pub 4681, page 7 and Form 982 instructions 49

Bankruptcy and Insolvency

Reduction of tax attributes per IRS Pub 4681

No tax attributes other than basis of personal use property

See Form 982 instructions, page 2 if discharged debt being excluded is

A non business debt, other than qualified principal residence indebtedness, such as a car loan or credit card debt

per Pub 4681, pages 7 and 8 50

Bankruptcy and Insolvency

Reduction of tax attributes per IRS Pub 4681

All other tax attributes General ordering rules

Exempt property under sec. 522 of title 11 – basis not reduced, per Pub 908, page 23

per Pub 4681, pages 7 and 8 51

Bankruptcy and Insolvency

Also, see the instructions to Form 982, page 2

if discharged debt being excluded is a non-business debt or any other debt, (other than qualified principal residence indebtedness)

per Pub 4681, pages 7 and 8 52

Bankruptcy and Insolvency

Reduction of tax attributes per IRS Pub 4681

Election to reduce the basis of depreciable property before reducing other tax attributes

Ordering rules somewhat similar to basis reduction under general ordering rules

Reduction limit doesn’t apply if this election is made – per Pub 908, page 22

per Pub 4681, pages 7 and 8 53

Bankruptcy and Insolvency

Reduction of tax attributes per IRS Pub 4681

Recapture of basis reductions if sold or disposed of at a gain

Taxed as ordinary income as depreciation recapture

54

Bankruptcy and Insolvency

See example on page 7 of Pub 4681

Kyra

See detailed example on page 15 of Pub 4681

3) Kathy and Frank Willow

55

Qualified Farm Indebtedness

Exclusion – 108(a)1(C)

per Pub 4681, page 5 56

Qualified farm indebtedness

The taxpayer can exclude canceled farm debt from income if all of the following apply. The debt was incurred directly in connection with the

operation of the trade or business of farming. 50% or more of their total gross receipts for the prior three

years were from the trade or business of farming. The cancellation was made by a qualified person who is

actively and regularly engaged in the business of lending money, (Includes any federal, state, or local government, agency or instrumentality thereof. The United States Department of Agriculture is a qualified person.)

per Pub 4681, page 5 57

Qualified farm indebtedness The cancellation was made by a qualified person who is actively

and regularly engaged in the business of lending money

This person cannot be related to the taxpayer,

be the person from whom they acquired the property (or a person related to this person),

or be a person who receives a fee due to their investment in the property (or a person related to this person).

For the definition of the term “related person,” see Related persons under At-Risk Amounts in Publication 925.

per Pub 4681, page 5 58

Exclusion limit

The amount of canceled qualified farm debt that can be excluded from income cannot exceed the sum of the taxpayer’s adjusted tax attributes (see list on page 5 of Pub 4681)

and the total adjusted bases of qualified property they held at the beginning of the following tax year.

The above are determined after any reduction of tax attributes required because of the application of the insolvency exclusion.

per Pub 4681, page 5 59

Exclusion limit - definition

Qualified property is any property that is used or held for use in a trade or business or for the production of income.

per Pub 4681, page 5 60

How to report the qualified farm indebtedness exclusion

Attach Form 982 to the taxpayer’s federal income tax return and check the box on line 1c.

On line 2 of Form 982, include the amount of qualified farm debt canceled, but not more than the amount of the exclusion limit.

per Pub 4681, page 5 61

How to report the qualified farm indebtedness exclusion

The taxpayer must also reduce their tax attributes in Part II of Form 982 as explained under Reduction of Tax Attributes later.

per Pub 4681, page 8 62

Qualified farm indebtedness Reduction of tax attributes

Reduce the tax attributes by the amount excluded under the insolvency exclusion before applying this exclusion

Follow the ordering rules for reduction of tax attributes, under Bankruptcy and Insolvency, except item 5. Basis

Instead, reduce the basis of qualified property in the following order

Depreciable qualified property. Can elect on Form 982 to treat real property held primarily for sale to

customers as if it were depreciable property Land that is qualified property and is used or held for use in the

taxpayer’s farming business Other qualified property

63

Qualified farm indebtedness

See examples on page 5 of Pub 4681

Chuck Bob

64

Qualified Real Property Business

Indebtedness

Exclusion – 108(a)1(D)

per Pub 4681, page 5 65

Qualified real property business indebtedness Qualified real property business indebtedness is

debt (other than qualified farm debt) that meets all of the following conditions. It was incurred or assumed in connection with real property

used in a trade or business. It is secured by such real property. It was incurred or assumed at either of the following times.

Before 1993. After 1992, if the debt is either (i) qualified acquisition

indebtedness or (ii) debt incurred to refinance qualified real property business debt incurred or assumed before 1993 (but only to the extent the amount of such debt does not exceed the amount of debt being refinanced).

It is debt to which an election is made to apply these rules.

per Pub 4681, pages 5 and 6 66

Qualified acquisition indebtedness - definition

Debt incurred or assumed, to acquire, construct, reconstruct, or substantially improve real property that secures such debt, or

Debt resulting from the refinancing of qualified acquisition indebtedness, to the extent the amount of such debt does not exceed the amount of debt being refinanced.

per Pub 4681, page 6 67

How to elect the qualified real property business debt exclusion

Make an election on a timely-filed (including extensions) federal income tax return (can be revoked only with the consent of the IRS). If they timely filed their tax return without making this

election, they can still make the election by filing an amended return within 6 months of the due date of the return (excluding extensions). Enter “Filed pursuant to sec. 301.9100-2” on the amended return and file it at the same place they filed the original return.

The election is made by completing Form 982.

per Pub 4681, page 6 68

Exclusion limit - of canceled qualified real property business debt

If the taxpayer excluded canceled debt from income under the insolvency exclusion, they must reduce their tax attributes to account for the amount of the canceled debt excluded under the insolvency exclusion before determining the limit on the exclusion of canceled qualified real property business debt.

The exclusion for canceled qualified real property business debt is limited to the excess (if any) of: The outstanding principal amount of the qualified real property

business debt (immediately before the cancellation), over The FMV (immediately before the cancellation) of the business

real property securing such debt, reduced by the outstanding principal amount of any other qualified real property business debt secured by that property (immediately before the cancellation).

per Pub 4681, page 6 69

Exclusion limit - of canceled qualified real property business debt

In addition to this limit, the amount of canceled qualified real property business debt that can be excluded from income cannot exceed the total adjusted bases (determined after any

attribute reductions under Internal Revenue Code sections 108(b) and (g)) of depreciable real property held immediately before the cancellation (other than depreciable real property acquired in

contemplation of the cancellation).

per Pub 4681, page 6 70

How to elect the qualified real property business debt exclusion

Attach Form 982 to the taxpayer’s federal income tax return and check the box on line 1d.

Include the amount of canceled qualified real property business debt (but not more than the amount of the exclusion limit) on line 2 of Form 982.

per Pub 4681, page 6, and Regs 71

How to elect the qualified real property business debt exclusion

The taxpayer must reduce tax attributes in Part II Line 4 of Form 982 as explained under Reduction of Tax Attributes later.

Regulations § 1.1017-1(f) Election to treat IRC § 1221(a)(1) real property as

depreciable is not available for basis reductions under IRC § 108(c) for qualified real property business debt

per Pub 4681, page 8 72

Qualified real property business indebtedness

Reduction of tax attributes reduce the basis of depreciable real property

(but not below zero) by the amount of canceled qualified real property business debt excluded from income

the basis reduction is made at the beginning of the next tax year

if the depreciable real property is disposed of before the beginning of the next tax year, reduce the basis of the depreciable real property (but not below zero) immediately before the disposition

73

How to elect the qualified real property business debt exclusion

See examples on page 6 of Pub 4681

Curt

on page 8 of Pub 4681 Curt Bob

74

Qualified Principal Residence

Indebtedness

Exclusion – 108(a)1(E)

for 2007, 08, and 09Extended through 2012 by

Emergency Economic Stabilization Act of 2008

per Pub 4681, page 6 75

Qualified principal residence indebtedness Qualified principal residence indebtedness is any debt incurred in

acquiring, constructing, or substantially improving the taxpayer’s principal residence and which is secured by their principal residence.

Qualified principal residence indebtedness also includes any debt secured by the taxpayer’s principal residence resulting from the refinancing of debt incurred to acquire, construct, or substantially improve their principal residence but only to the extent the amount of debt does not exceed the amount of the refinanced debt.

The taxpayer’s principal residence is the home where they ordinarily live most of the time. They can have only one principal residence at any one time.

per Pub 4681, page 6 76

Exclusion limit

The maximum amount that can be treated as qualified principal residence indebtedness is $2 million ($1 million if married filing separately). A mortgage loan in excess of the maximum exclusion

amount may qualify for another exclusion. The taxpayer cannot exclude canceled qualified

principal residence indebtedness from income if the cancellation was for services performed for the lender or on account of any other factor not directly related to a decline in the value of their residence or to their financial condition.

per Pub 4681, page 6 77

Ordering rule

If only a part of a loan is qualified principal residence indebtedness, the exclusion from income for canceled qualified

principal residence indebtedness applies only to the extent the amount canceled exceeds the amount of the loan (immediately before the cancellation) that is not qualified principal residence indebtedness.

The remaining part of the loan may qualify for another exclusion.

78

Ordering rule

See example on page 6 of Pub 4681

Ken

per Pub 4681, page 7 79

How to report the qualified principal residence indebtedness exclusion

Attach Form 982 to the taxpayer’s federal income tax return and check the box on line 1e.

On line 2 of Form 982, include the amount of canceled qualified principal residence indebtedness, but not more than the amount of the exclusion limit. Any amount in excess of the excluded amount

may result in taxable income.

per Form 982 instructions, page 2 80

How to report the qualified principal residence indebtedness exclusion

If the taxpayer continues to own their residence after a cancellation of qualified principal residence indebtedness, they must reduce their basis in the residence. Enter on line 10b of Form 982 the smaller of

(a) the amount of qualified principal residence indebtedness included on line 2 or

(b) the basis of their principal residence. See Pub 523.

If the taxpayer disposed of their residence, they may also be required to recognize a gain on its disposition. Main home exclusion may apply. COD excluded from income is a basis reduction for other 4 exclusions, per

Pub 551, page 6, revised in 2002 before this exclusion came into law.

There may also be recapture of any Federal mortgage subsidy. See Pub 523, page 29.

81

Qualified principal residence indebtedness

See example on page 6 of Pub 4681

Becky

See detailed examples Starting on page 10 of Pub 4681

1) Nancy Oak – page 10 2) John and Mary Elm – page 13 3) Kathy and Frank Willow – page 15

82

Foreclosures and Repossessions

per Pub 4681, pages 9 and 10 83

Foreclosures and Repossessions

Tax treatment depends if it is:

Recourse debt – personally liable

Non-recourse debt – not personally liable

per Pub 4681, pages 9 and 10 84

Foreclosures and Repossessions

Recourse debt – personally liable There may be COD income The amount realized includes the smaller of:

The outstanding debt immediately before the transfer reduced by any amount for which the taxpayer remains personally liable immediately after the transfer, or

The FMV of the transferred property. The amount realized also includes any

proceeds received from the foreclosure sale

per Pub 4681, pages 9 and 10 85

Foreclosures and Repossessions

Non-recourse debt – not personally liable No COD income The amount realized includes the full amount

of the outstanding debt immediately before the transfer

per Pub 4681, page 9 86

Foreclosures and Repossessions

Use the IRS worksheet - Table 1-1 from Pub 4681 to figure the COD income Gain or loss

per Pub 4681, page 9 87

88

Foreclosures and Repossessions

See examples on page 9 of Pub 4681

Recourse Tara Lil

on page10 of Pub 4681 Non-recourse

Tara Lil

89

Abandonments

per Pub 4681, page 10 90

Abandonments The abandonment of property is a disposition

when the taxpayer voluntarily and permanently gives up possession and use of the property with the intention of ending their ownership but without passing it on to anyone else.

Loss from the abandonment of business or investment property is deductible as an ordinary loss, even if the property is a capital asset. The loss is the property's adjusted basis when abandoned.

However, if the property is later foreclosed on or repossessed, gain or loss is figured as discussed earlier.

Can’t deduct any loss from abandonment of a home or other property held for personal use.

per Pub 4681, page 10 91

Abandonments

Canceled debt If the abandoned property secures a debt for

which the taxpayer is personally liable and the debt is canceled, they will realize ordinary income equal to the canceled debt. which is separate from any loss realized from

abandonment of the property.

They must report this income, unless certain exceptions or exclusions apply.

92

Abandonments

See example on page 10 of Pub 4681

Anne

93

Abandonments

Questions When or why would someone abandon their personal use

property? Earthquake or other acts of the gods Disasters

What if the money was borrowed with someone else, and both receive a 1099-A?

Is there always a foreclosure or repo later? What if it takes place in a different tax year?

94

Forms 1099 A and C

95

Forms 1099 A and C

1099-A - Acquisition or abandonment of secured property

1099-C – Cancellation of debt

96

Form 1099-A

1099-A - Acquisition or abandonment of secured property

Acquisition results in gain or loss Abandonment results in separate income and loss

See the Instructions for Borrower included with the form

The taxpayer should contact the creditor if they don’t agree with the information on the 1099-A

97

Form 1099-C 1099-C – Cancellation of debt

If interest is included in the amount of debt canceled, check if –

Interest would not be deductible – include box 2 in income Interest would be deductible – include net amount of box 2 less

box 3 in income Check for prior deduction and tax benefit rule

See the Instructions for Debtor included with the form

The taxpayer should contact the creditor if they don’t agree with the information on the 1099-C

98

Property Used Partly for Business or Rental

see Pub 544, page 4 and Pub 523, starting on page 19

99

Property used partly for business or rental, and partly for personal use

Cancellation of debt, IRC § 108(h) Principal residence has same meaning as

used in IRC § 121

Allocate based on use of debt (tracing rules in Pub 535, page 11

Also need to determine if debt is qualified

100

Property Used Partly for Business or Rental

Dispositions

per Pub 523, page 19 101

Property used partly for business or rental, and partly for personal use

Business or rental part is within home No need to allocate Could be main home exclusion of gain Form 4797 not required Depreciation recapture Use Worksheet 2 in Pub 523 to calculate

Business or rental part is separate from home May need to allocate between

business or rental part personal part

per Pub 523, page 19 and 20 102

Business or rental part is separate from home

Use test – main home 2 out of 5 year period ending on date of sale Use test not met for business part

Use test met for business part (business use in year of sale)

Use test met for business part (no business use in year of sale)

per Pub 523, page 19 103

Business or rental part is separate from home

Use test not met for business part Need to allocate

Could be main home exclusion of gain Form 4797 required

Depreciation recapture

Use Worksheet 2 in Pub 523 to calculate

per Pub 523, page 19 104

Business or rental part is separate from home

Use test met for business part (business use in year of sale) Need to allocate

Could be main home exclusion of gain Form 4797 required

Depreciation recapture

Use Worksheet 2 in Pub 523 to calculate

per Pub 523, page 20 105

Business or rental part is separate from home

Use test met for business part (no business use in year of sale) No need to allocate Could be main home exclusion of gain Form 4797 not required Depreciation recapture

Use Worksheet 2 in Pub 523 to calculate

106

Home Changed to Business or Rental Use

and used as such at time of sale

107

Home changed to business or rental use

Be careful of deducting interest on debt refinanced before or after the change, where additional proceeds were not used for additions or improvements to the home What about when the FMV of the home is less than the

acquisition indebtedness?

Cancellation of debt - Allocate based on use of debt (tracing rules in Pub 535,

page 11 Also need to determine if debt is qualified

per Pub 544, page 4 108

Home changed to business or rental use

Disposals Gains and losses computed differently

Loss is limited if fair market value was less than adjusted basis when converted

Full amount of gain is recognized unless main home exclusion applies–

main home 2 out of 5 year period ending on date of sale

depreciation recapture

109

Partnerships

K-1 Form 1065

110

Partnerships

Certain provisions applied at partner level IRC § 108(d)(6)

K-1 for Form 1065, and partners instructions (box 11, Other Income, code E)

Partnership interest treated as depreciable property – elections under 108(b)(5) or 108(c)

If applicable, under Regulations § 1.1017-1(g) partnership consent statements for Form 982 to reduce

inside basis of its depreciable property with respect to the taxpayer

111

S-corporations

K-1 Form 1120S

112

S-corporations

Certain provisions applied at corporate level IRC § 108(d)(7) Special rules for S Corp’s

COD income not on K-1

113

Where to Report on Form 1040

Schedules and Forms

114

Where to report on Form 1040 Form 1040, line 21 for non-business debt Schedule C (could be SE tax) Schedule E

Rentals Form 4835 farm rentals Partnership K-1’s

Schedule F (could be SE tax) Gains and losses

Schedule D Form 4797

Depreciation recapture Recapture of basis reductions

per Pub 4681, page 3 115

Where to report on Form 1040

Schedule B - Dividend income Stockholder debt canceled

COD is construction distribution, generally dividend income

116

Cross References to Code and Regulations

117

Cross references to code and regulations

IRC § 61(a)(12) COD is generally taxable income

IRC § 108 Income from discharge of indebtedness

Regulations include 1.108-2 Acquisition of indebtedness by person

related to debtor (IRC § 108 (e)(4))

118

Cross references to code and regulations

IRC § 1017 Discharge of indebtedness re: reduction of basis Regulations § 1.1017-1 includes

(b)(2) Multiple discharged indebtedness (d) Changes in security for indebtedness (e) Definition of depreciable property

119

Planning Ideas

120

Tax planning for taxpayers

Abandonment vs. foreclosure or repossession

Workout with lender, if possible Reduce amount, change terms, etc.

Get the settlement amount in writing, e.g. with credit cards, in case someone comes back later for the canceled balance

121

Planning for taxpayer’s income tax returns

Heads up for clients – get them started early

Check the Forms 1099 A and/or C with their records.

For credit card debt, does the amount canceled include itemized deductions? 1040 page one adjustments? Remember, that exceptions come before exclusions.

122

Planning for taxpayer’s income tax returns

Heads up for clients – get them started early

Insolvency balance sheets, for each discharge: immediately before the cancellation, at FMV immediately after the cancellation, at bases at the beginning of following year, at tax bases

For canceled debts, secured by property Basis of assets, adjusted for all increases and decreases,

esp. personal use property not already on the tax return Calculate depreciation included in the standard

mileage rates for vehicles (Pub 463)

123

Planning for taxpayer’s income tax returns

If no elections on Form 982, then have to use the general ordering rules for reduction of tax attributes.

Which elections to use may buy the taxpayer time, depending on how soon the assets are disposed of. Treating all real property held for resale as

depreciable property may speed up the time to recognize the reductions

124

Planning for taxpayer’s income tax returns

How soon will the carryovers, which come before basis reduction, be utilized NOLs General business credits Minimum tax credits Capital losses

Contributing property after basis reductions can affect charitable deductions (see Pub 526)

125

Planning for taxpayer’s income tax returns

Partnerships If applicable, obtain the required partnership consent

statements for Form 982 Regulations § 1.1017-1(g)

If in bankruptcy per Pub 908, page 3 – Election for 2 (or 3) short years

ending day before filing, and normal year end First short year return due by 15th day of 4th month

Joint or separate returns, if married?

126

Planning for payment of tax

Do they have the money to pay? If, not –

Form 9465 Installment Agreement Request A Notice of Federal Tax Lien may be filed If in bankruptcy or IRS has accepted an offer-in-

compromise, do not file this form Bankruptcy or offer-in-compromise

local IRS Insolvency function for bankruptcy Technical Support function for offer-in-compromise

127

Planning for tax preparers

Advocacy vs. ethics

How comfortable are we with the taxpayer’s facts and circumstances to do the return? Let client know early if you can’t do their return

What does Circular 230 say? What does I.R.C. § 7525 say re: tax advice?

What do the commentators say?

128

Circular 230 - § 10.34(d) Relying on information furnished by clients

Generally we may rely in good faith without verification upon information furnished by the client.

However, we can’t ignore the implications of information furnished to, or actually known by, us, and

we must make reasonable inquiries if the information as furnished appears to be incorrect, inconsistent with an important fact or another factual

assumption, or incomplete.

129

Client Privilege under IRC § 7525

It’s for tax advice May be asserted only in -

noncriminal tax matters before the IRS

noncriminal tax proceedings in Federal court

Not applicable for tax shelters (for which there may be COD income?)

130

Client Privilege under IRC § 7525

There is overwhelming support, including Congressional intent, for the proposition that tax advice does not include the actual tax preparation.

http://www.cba.uri.edu/faculty/higgins/Homepages/2004%20ATA%20Mid-Year%20Meeting/Oliva.pdf

131

Client Privilege under IRC § 7525

The privilege does not apply to tax preparation for two reasons. First, some courts hold that tax preparation services are

not legal services but instead are accounting services. More importantly, communications occurring in the process

of tax preparation do not have an expectation of confidentiality.

http://www.nysscpa.org/cpajournal/1998/1098/Features/F141098.html

132

Client Privilege under IRC § 7525

Does privilege attach to communications when tax preparation services are coupled with tax consultation? Per the Courts, the answer is No and Yes

http://www.nysscpa.org/cpajournal/1998/1098/Features/F141098.html

per Circular 230 133

§ 10.32 Practice of law

Nothing in the regulations in this part may be construed as authorizing persons not members of the bar to practice law.

134

Attachments

135

Attachments

Excel worksheet for ordering of exclusions Form 982 Forms 1099 A and C K-1 for Form 1065 IRS Pub 4681 Various other IRS Publications