1 celebrating 30 years of excellence planning, saving & paying for college college financing...

TRANSCRIPT

1

Celebrating 30 years of ExcellencePlanning, Saving & Paying for College

College FinancingMEFA’s Guide to

Today’s Presenter: Joe Farragher, Ed.D.

2

• Massachusetts Educational Financing Authority• Not-for-profit state authority that works to

make higher education more accessible and affordable

• Created in 1982 by the State Legislature • Helping families:

o Plan: Extensive community outreacho Save: U.Fund® and U.Plan® college savings planso Pay: Affordable fixed interest rate college loans

for over 30 years

Facts About MEFA

3

You Can Do This

4

Videos/ Social Media

mefa.org/seniors

What’s Next: Your to-do list

Tools & Resources

Next

SlideGuidance: Financial Aid Info & Tips

5

EmailSign-up

mefa.org/seniors

What’s Next: Your to-do list

Tools & Resources

e-Book

Ask a MEFA Expert

6

7

• What is financial aid?

• How do students apply?

• How are financial aid decisions made?

• Financial aid awards

• Paying for college

• Free resources

Agenda

8

Overview of Financial AidUndergraduate Student Aid 2011-12 ($185.1

Billion)

Source: The College Board, Trends in Student Aid 2012

9

• Federal– Grants, work-study, loans, tax incentives

• Massachusetts– Grants, scholarships, tuition waivers, loans– www.osfa.mass.edu

• College/University (institutional aid)– Grants, scholarships, loans

• Outside Agencies– Scholarships

Sources of Financial Aid

10

• Awarded in recognition of student achievements (academic, artistic, athletic, etc.)

• Applicants often compared against one another

• May or may not be renewable

• Not offered at every school

Merit-Based Aid

11

• Awarded based on family’s financial eligibility as determined by standardized formula

• Includes grants, loans and/or work-study

• Most federal, state and institutional aid is awarded based on financial eligibility

Need-Based Aid

12

• Free Application for Federal Student Aid (FAFSA)

– Required by all colleges for federal and MA state aid– Open January 1st: FAFSA.gov– Must sign with a PIN: PIN.ed.gov– IRS Data Retrieval Tool – available February 1st

– Requires data from all parents who live together, married or not

The FAFSA

Must be completed

every year!

13

• CSS/Financial Aid PROFILE®

– Some colleges require for institutional aid– $25 for 1st school, $16 for each additional– Online application required: CollegeBoard.org– Noncustodial Parent PROFILE required when applicable– 31 MA Colleges and Universities

• College Financial Aid Application– Required by some colleges– Usually part of the admissions packet

Other Financial Aid Applications

Don’t wait until you’re accepted to

apply!

14

1. Colleges & state receive data electronically

2. You will receive (electronically or by mail):– Student Aid Report (SAR) – CSS/Financial Aid PROFILE® acknowledgement report

3. Review both & keep for records

4. Colleges may request Verification documents

5.With any special circumstances, contact Financial Aid Office at each college

What Happens After You Apply?

15

Total expenses for one year of college

Cost of Attendance (COA)

16

• Calculated amount the family has the ability to absorb for one year of college expenses

• Same federal formula used for every family

• Family has the primary responsibility for paying

• Not necessarily what the family will pay

Expected Family Contribution (EFC)

Visit mefa.org/seniors to use an EFC calculator

17

• Federal & institutional formulas are different– Federal formula for MA & federal aid– Institutional formula for aid from some colleges

• Includes income & asset protection allowances

• Parent & student info treated differently

• Does not include personal debt (credit cards, auto loans or personal loans)

EFC Formulas

18

Asset Impact on EFC

Based on 2014-15 Federal Methodology

Family A

Family B Family C

Parent Income

$60,000 $60,000 $60,000

Parent Assets $0 $75,000 $150,000

EFC $4,227 $5,461 $10,815

Difference $1,234 $6,588

An example. 4 in the family, 1 child in college:

19

Income Impact on EFC

Family A

Family B Family C

Parent Income

$60,000 $100,000 $150,000

Parent Assets $50,000 $50,000 $50,000

EFC $4,591 $16,552 $32,084

Difference $11,961 $27,493

Based on 2014-15 Federal Methodology

An example. 4 in the family, 1 child in college:

20

Cost of Attendance (COA) – Expected Family Contribution

(EFC)= Financial Aid Eligibility

Financial Aid Formula

Colleges fill in Financial Aid Eligibility with financial aid from multiple sources

21

How the Formula Works

$0$5,000

$10,000$15,000$20,000$25,000$30,000$35,000$40,000$45,000$50,000

College A College B College C College D

Eligibility

EFC

Co

st

of

Att

end

an

ce

22

Financial Aid Awarding

This example is an estimate only.

Federal Work-Study $1,500

ANY college costs not covered by financial aid are the FAMILY’s responsibility!

COA = $30,000

Unmet Need $3,000

EFC $5,000

Scholarship $7,500

Student Loan $5,500

Grant $7,500

EFC = $5,000

23

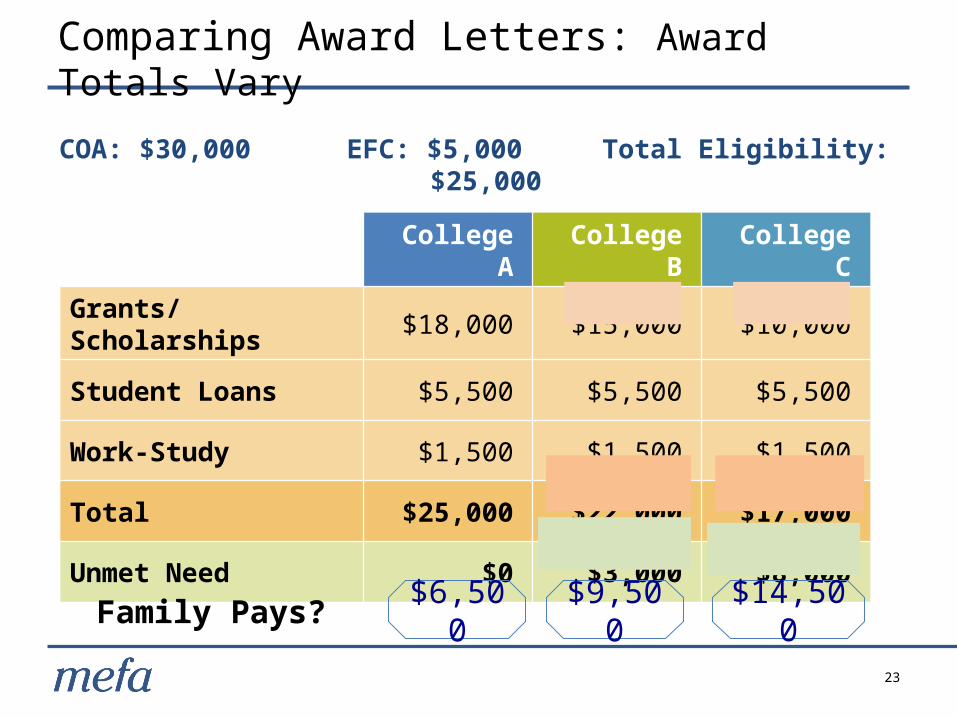

Comparing Award Letters: Award Totals Vary

COA: $30,000 EFC: $5,000 Total Eligibility: $25,000

College A

College B

College C

Grants/Scholarships

$18,000 $15,000 $10,000

Student Loans $5,500 $5,500 $5,500

Work-Study $1,500 $1,500 $1,500

Total $25,000 $22,000 $17,000

Unmet Need $0 $3,000 $8,000

Family Pays? $6,500 $9,500 $14,500

24

????

COA: $30,000 EFC: $5,000 Total Eligibility: $25,000

Comparing Award Letters: Award Totals Are Equal

College ACollege

BCollege C

Grants/Scholarships

$15,000 $5,000 $0

Student Loans $5,500 $5,500 $5,500

Parent Loan $0 $10,000 $16,500

Work-Study $1,500 $1,500 $0

Total $22,000 $22,000 $22,000

Unmet Need $3,000 $3,000 $3,000

Family Pays? $9,500 $19,500 ????$24,500

25

UMass-Amherst

26

Bentley University

27

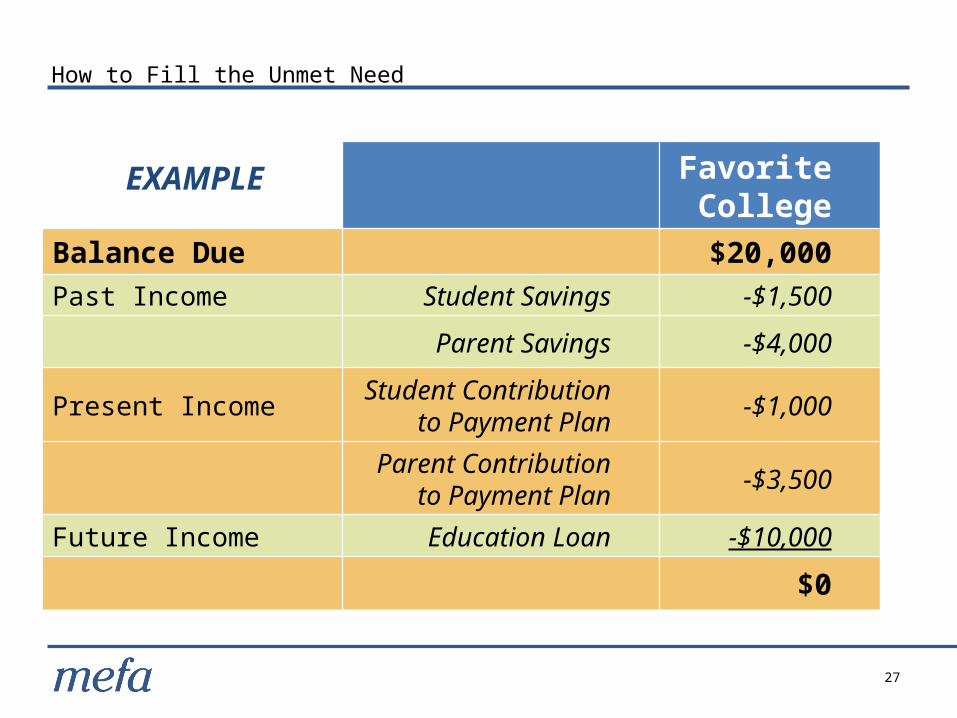

How to Fill the Unmet Need

Favorite College

Balance Due $20,000Past Income Student Savings -$1,500

Parent Savings -$4,000

Present IncomeStudent

Contribution to Payment Plan

-$1,000

Parent Contribution to

Payment Plan-$3,500

Future Income Education Loan -$10,000

$0

EXAMPLE

28

• Student is the sole borrower

• No credit check

• Annual limits

• 3.86% fixed interest rate for 2013-14

• Repayment– No payments due while enrolled– Approximately $300/month for 10 years for $27,000

debt

Federal Direct Student Loans

29

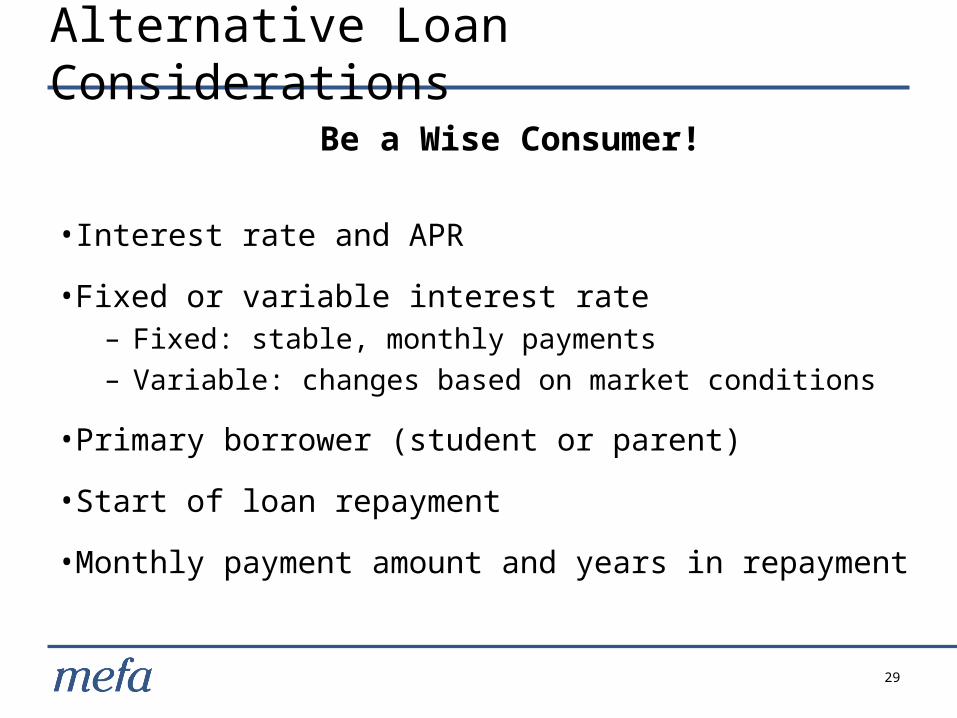

Be a Wise Consumer!

•Interest rate and APR

•Fixed or variable interest rate– Fixed: stable, monthly payments– Variable: changes based on market conditions

•Primary borrower (student or parent)

•Start of loan repayment

•Monthly payment amount and years in repayment

Alternative Loan Considerations

30

Free assistance in completing the FAFSA!

• Over 25 locations across Massachusetts

• Sunday, January 26, 2014 at 1:00 p.m.

• Sunday, February 23, 2014 at 1:oo p.m.

• Additional dates and all locations listed at fafsaday.org

FAFSA Day Massachusetts

31

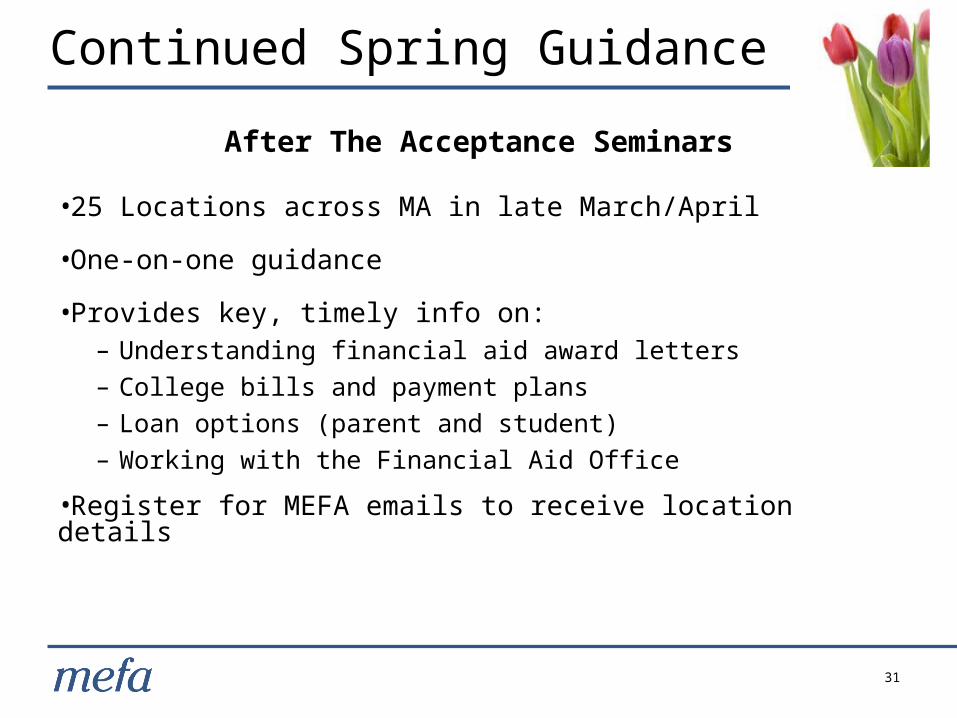

After The Acceptance Seminars

•25 Locations across MA in late March/April

•One-on-one guidance

•Provides key, timely info on:– Understanding financial aid award letters– College bills and payment plans– Loan options (parent and student)– Working with the Financial Aid Office

•Register for MEFA emails to receive location details

Continued Spring Guidance

32

• Research financial aid deadlines & requirements

• Partner with MEFA:– Sign up for MEFA emails– Download the College Financing e-book– Bookmark mefa.org/seniors

• Net Price Calculator Site: – http://collegecost.ed.gov/netpricecenter.aspx

• You Can Do This

What You Can Do Now

33

Questions or Comments?

Please take a moment to complete the seminar evaluation

Presenter:

Joe Farragher, Ed.D.

Thank You