1 coporation income tax incentive in vietnam- opportunities and challenges for foreign direct...

TRANSCRIPT

1

COPORATION INCOME TAX INCENTIVE IN VIETNAM- OPPORTUNITIES and CHALLENGES

FOR FOREIGN DIRECT INVESTMENT

Enschede , March 2014

Ph.D. Ly Phuong Duyen

Academy of Finance, Viet Nam

Ph.D. Ly Phuong Duyen

Academy of Finance, Viet Nam

2

CONTENTS

1. Introduction

3. Corporation Tax Incentives in Vietnam

4. Opportunities and Challenges

2. Foreign Investment in Vietnam

5. Conclusions

3

INTRODUCTION

Corporation Income Tax Law has been approved by Vietnam’s National Assembly in 1997, with effect from 1.1.1999

CIT Law has been changed three times: in 2003, 2008 and 2013

The Corporate Income Tax in Vietnam provides for a series of tax incentives for different types of industries and their geographical location.

4

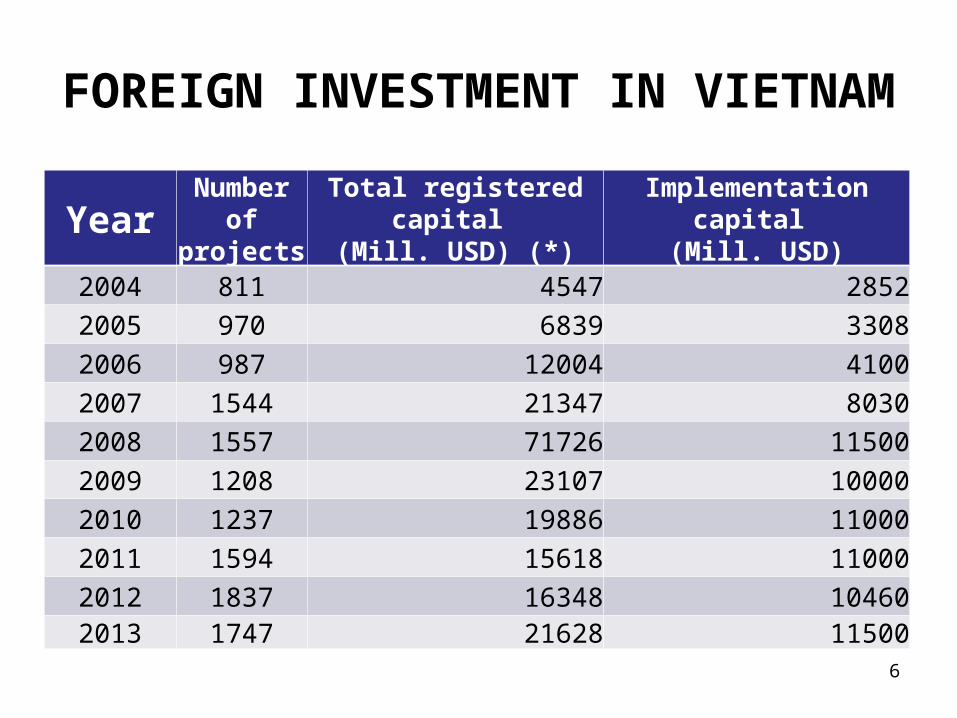

FOREIGN INVESTMENT IN VIETNAM

An average rate of attract FDI in Vietnam : 8.3% of GDP in the last five years (2008-2012), among the highest rates in the whole of the global

frontier and emerging Asian space. Much of the FDI inflows into Vietnam come from more

developed Asian countries: Japan, Singapore and Korea.

5

FOREIGN INVESTMENT IN VIETNAM

Sectors that have seen significant FDI inflows in recent years include banks, property and infrastructure.

However a shift is underway, with a rise in FDI into manufacturing, retail and technology, among others. Flows are becoming less speculative in nature than in some instances in the past, and they do more to add value and create jobs.

FOREIGN INVESTMENT IN VIETNAM

YearNumber

ofprojects

Total registered capital (Mill. USD) (*)

Implementation capital (Mill. USD)

2004 811 4547 2852

2005 970 6839 3308

2006 987 12004 4100

2007 1544 21347 8030

2008 1557 71726 11500

2009 1208 23107 10000

2010 1237 19886 11000

2011 1594 15618 11000

2012 1837 16348 104602013 1747 21628 11500

6

7

CORPORATION INCOME TAX INCENTIVES

Before 2004:

CIT incentives varies from foreign company to domestic company

From 2004 to present:

the same CIT incentive regulations has been applied to both domestic and foreign company

8

CORPORATION INCOME TAX INCENTIVES IN VIETNAM

1. Source of Tax Law2. Regulations

9

SOURCE OF TAX LAW

1. The Corporation Income Tax Law No. 14/2008/QH12 of June 3, 2008;

2. The Tax Administration Law No. 78/2006/QH11 of November 29, 2006 ;

3. The Government’s Decree No. 124/2008/ND-CP of December 11, 2008;

4. The Government’s Decree No. 122/2011/ND-CP of December 27, 2011;

5. Circular No. 123/2012/TT-BTC of July 27, 2012

10

CORPORATION INCOME TAX INCENTIVES IN VIETNAM

1. Tax holiday, 2. Investment allowance and tax credits, 3. Reduced tax rates, 4. Loss carry forward, 5. Depreciation and 6. Special zone incentives;

11

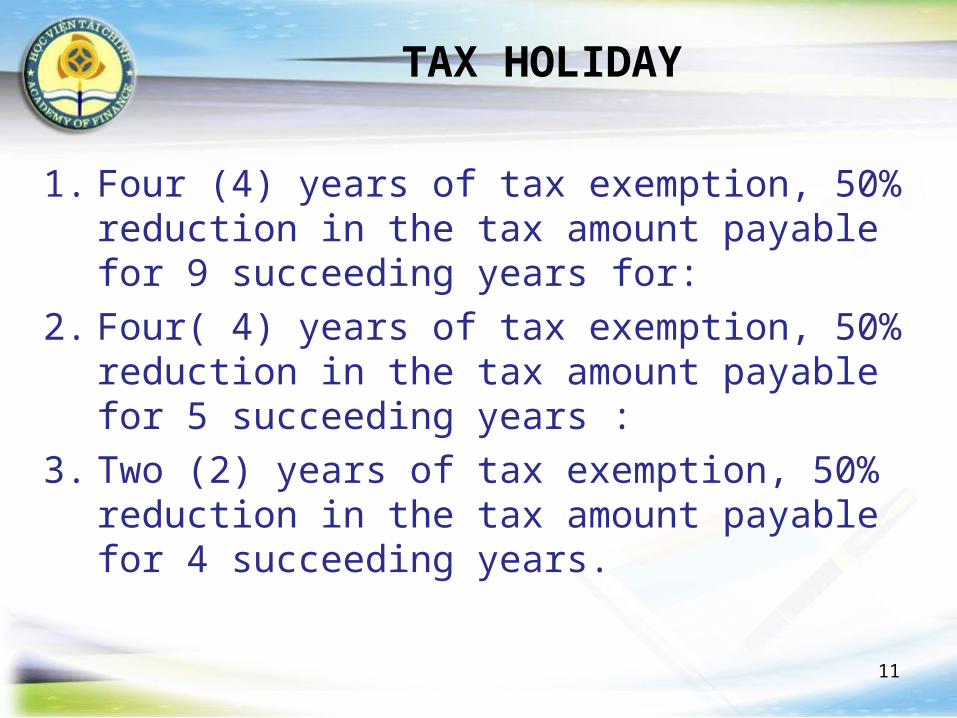

TAX HOLIDAY

1. Four (4) years of tax exemption, 50% reduction in the tax amount payable for 9 succeeding years for:

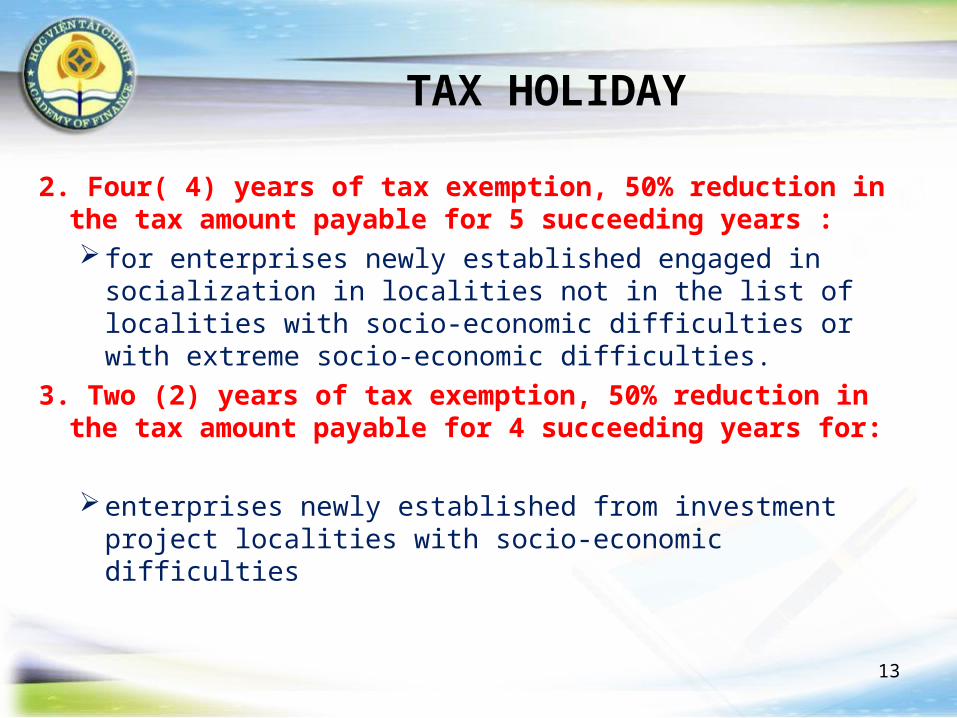

2. Four( 4) years of tax exemption, 50% reduction in the tax amount payable for 5 succeeding years :

3. Two (2) years of tax exemption, 50% reduction in the tax amount payable for 4 succeeding years.

12

TAX HOLIDAY

1. 4 years of tax exemption, 50% reduction in the tax amount payable for 9 succeeding years for:

Newly established enterprises from investment projects in areas with specially difficult socio-economic conditions, in economic zones and in high-tech zones;

Newly established enterprises from investment projects in the sectors of high-tech, scientific research and technological development, investment in development of specially important infrastructure facilities of the State, and production of software products;

Newly established enterprises operating in the sectors of education and training, occupational training, health care, culture, sport and the environment.

13

TAX HOLIDAY

2. Four( 4) years of tax exemption, 50% reduction in the tax amount payable for 5 succeeding years : for enterprises newly established engaged in socialization in

localities not in the list of localities with socio-economic difficulties or with extreme socio-economic difficulties.

3. Two (2) years of tax exemption, 50% reduction in the tax amount payable for 4 succeeding years for:

enterprises newly established from investment project localities with socio-economic difficulties

14

REDUCE TAX RATE

1. The tax rate of 10% for 15 years.

2. The tax rate of 10% apply to enterprises operating in the sectors of education and training, occupational training, health care, culture, sport and the environment.

3. The tax rate of 20% for 10 years to newly established enterprises from investment projects in areas with difficult socio-economic conditions.

4. The tax rate of 20% apply to agricultural service co-operatives and to people's credit funds.

15

REDUCE TAX RATE

The tax rate of 10% for 15 years.

Newly established enterprises from investment projects in areas with specially difficult socio-economic conditions, in economic zones and in high-tech zones;

Newly established enterprises from investment projects in the sectors of high technology, scientific research and technological development, investment in development of specially important infrastructure facilities of the State, and production of software products.

16

INVESTMENT ALLOWANCE AND TAX CREDITS

Enterprises established and operating under the law of Vietnam

shall be entitled to deduct a maximum of ten (10) per cent of their annual assessable income in order to establish the Science and Technology Development Fund of the enterprise.

17

LOSSES CARRY FORWARD

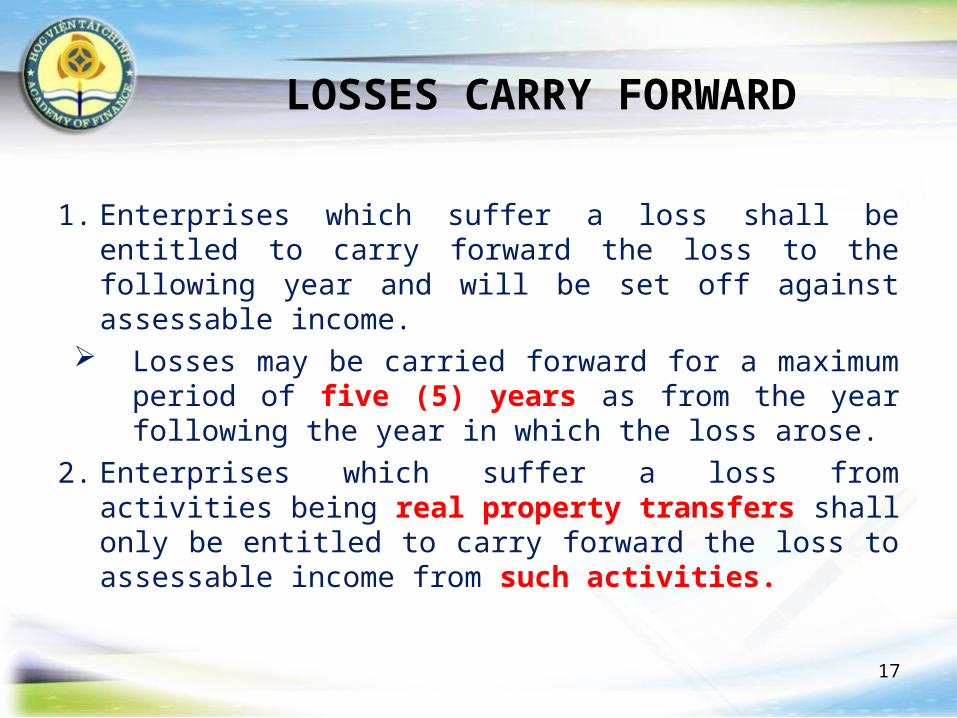

1. Enterprises which suffer a loss shall be entitled to carry forward the loss to the following year and will be set off against assessable income. Losses may be carried forward for a maximum period

of five (5) years as from the year following the year in which the loss arose.

2. Enterprises which suffer a loss from activities being real property transfers shall only be entitled to carry forward the loss to assessable income from such activities.

18

DEPRECIATION

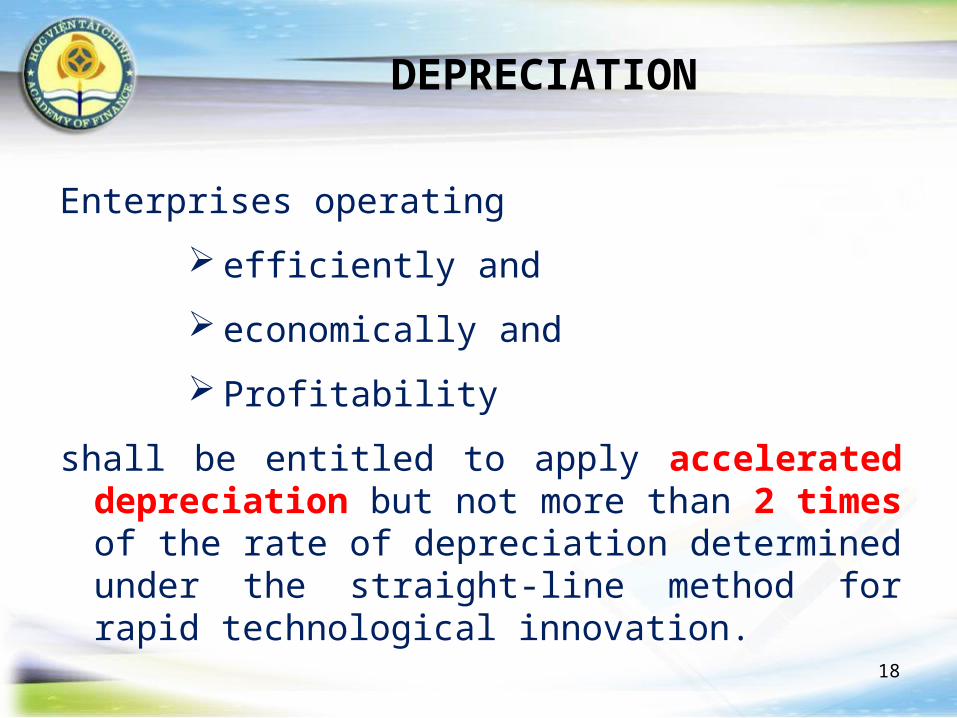

Enterprises operating

efficiently and

economically and

Profitability

shall be entitled to apply accelerated depreciation but not more than 2 times of the rate of depreciation determined under the straight-line method for rapid technological innovation.

19

SPECIAL ZONE INCENTIVES- EXEMPT INCOME

1. Incomes from farming, breeding, aquaculture, salt production of cooperatives

2. Undistributed incomes of of private organizations, which make investment in education, health, and other fields.

3. Income from transfer of certified emission reductions (CERs)

20

SPECIAL ZONE INCENTIVES - EXEMPT INCOME

4. Income from the performance of duties by the State Development Bank Vietnam (VDB), Bank for Social Policy (BSP)

5. Incomes from transfer of technologies that are prioritized to be to organizations and individuals in localities facing extreme socio-economic difficulties.”

6. Income earned from activities of production [and/or] business in goods and services by enterprises employing specified numbers of disabled people, reformed addicts and people infected with HIV.

21

OPPORTUNITIES and CHALLENGES

22

OPPOTUNITIES

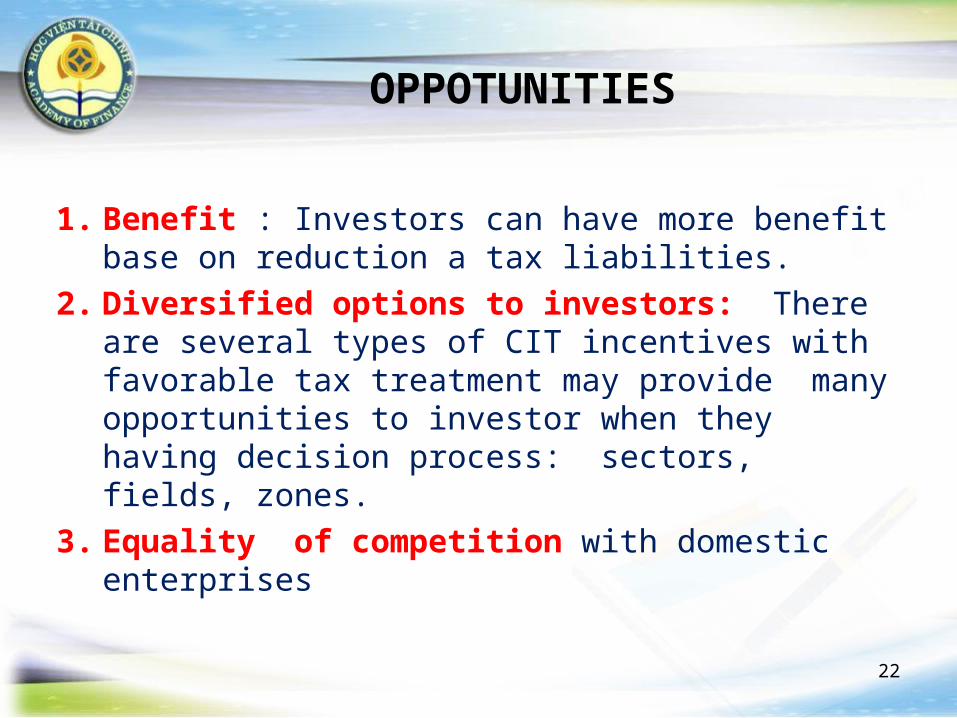

1. Benefit : Investors can have more benefit base on reduction a tax liabilities.

2. Diversified options to investors: There are several types of CIT incentives with favorable tax treatment may provide many opportunities to investor when they having decision process: sectors, fields, zones.

3. Equality of competition with domestic enterprises

23

CHALLENGES

1. Forgone revenues: the losses in tax revenue from CIT incentives may bring burden to other indirect tax, such as VAT, excise duties…

2. Resource allocation (neutrality) costs: originated when CIT incentives create distortions on investment choices among sectors or activities instead of correcting market failures.

24

CHALLENGES

3. Enforcement and compliance costs: These costs increase with the complexity of the tax

system and the system of fiscal incentives (in terms of qualifying and reporting requirements, different schemes).

There is a problem of perception of lack of fairness when targeted incentives are used, which reduces compliance and, therefore, increases enforcement efforts.

25

CHALLENGES

4. Lack of transparency: When the rationale for granting tax incentives is based

more on discretionary and subjective qualification requirements, instead of automatic and objective requirements, they can originate rent-seeking behaviour and facilitate officials’ abuse on the granting process.

26

CONCLUSIONS

27

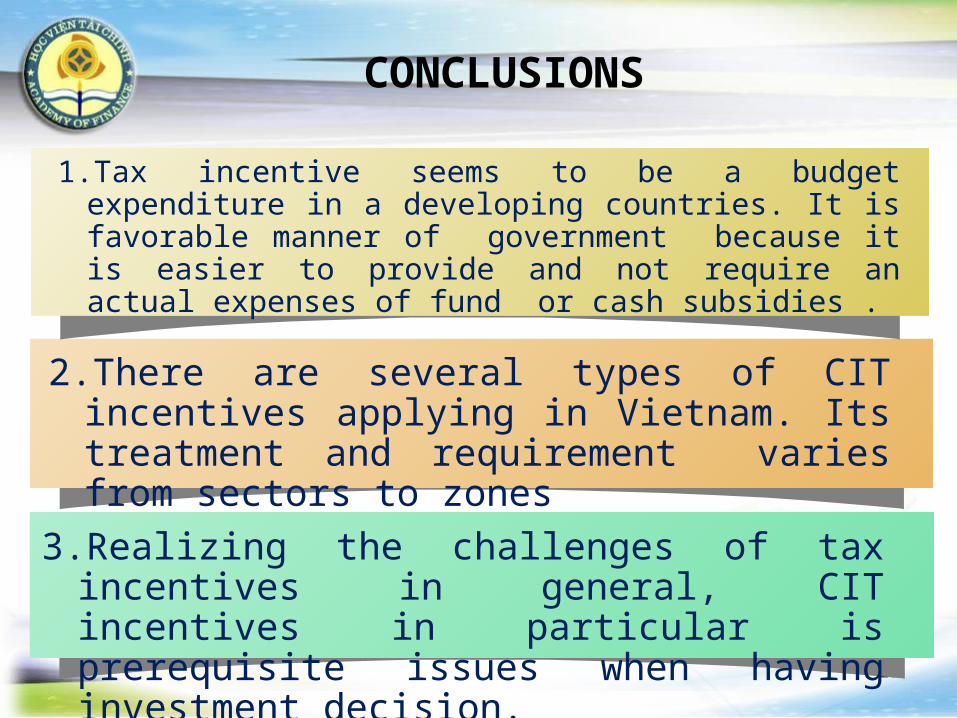

1.Tax incentive seems to be a budget expenditure in a developing countries. It is favorable manner of government because it is easier to provide and not require an actual expenses of fund or cash subsidies .

CONCLUSIONS

2.There are several types of CIT incentives applying in Vietnam. Its treatment and requirement varies from sectors to zones

3.Realizing the challenges of tax incentives in general, CIT incentives in particular is prerequisite issues when having investment decision.

28

I would like to sincerely thank the School of Finance & Accounting, Saxion University of Aplied Sciences for

providing financial support for my trip to the Netherland to attend this excellent meeting.

Acknowledgements

29

Thank you for your attention!

www.themegallery.com 30

Ha Noi Capital

Hue City

Ho Chi Minh City