1 fifth third bank | all rights reserved the u.s. economy: taking measure of 2012 presented by:...

TRANSCRIPT

1 Fifth Third Bank | All Rights Reserved

The U.S. Economy:The U.S. Economy:Taking Measure of 2012Taking Measure of 2012

Presented by:

Jeff Korzenik SVP, Chief Investment Strategist

Fifth Third Bank

2 Fifth Third Bank | All Rights Reserved

Beginning at the End

In 2011 the Economy was:

“A Glass Half-Empty”— Weak GDP growth, particularly for this

stage of the business cycle

— Weak but noticeable employment growth

— Deleveraging of the household balance sheet

— A new age of limits for state and local governments

— Federal government unable to make substantive progress in addressing imbalances

— Economic “headwinds” from events overseas

In 2012 the economy will be:

“A Glass Half-Full”— Weak GDP growth, particularly for this

stage of the business cycle

— Weak but noticeable employment growth

— Deleveraging of the household balance sheet

— A new age of limits for state and local governments

— Federal government unable to make substantive progress in addressing imbalances

— Economic “headwinds from events overseas

3 Fifth Third Bank | All Rights Reserved

“A Glass Half-Empty”— Estimated real GDP Growth of 1.8%

— CPI: 3.0%

— Core CPI: 2.2%

— 10-year Treasury yield fell from 3.37% to 1.87%

— The total return of the S&P500 was 2.11%, almost all of which was attributable to dividends

2011 in Review

4 Fifth Third Bank | All Rights Reserved

The Historical Case for Robust Recoveries

Source: Ned Davis Research charts are used with permission

Monthly Data 7/31/1986 - 11/30/2011

(E576)

Unemployment Rate (Labor)

11/30/2011 = 8.6% Shaded area represents NDR-defined band aroundCBO estimates of the Nonaccelerating Inflation Rate of Unemployment (NAIRU) 3.5

4.0 4.5 5.0 5.5 6.0 6.5 7.0 7.5 8.0 8.5 9.0 9.5

3.5 4.0 4.5 5.0 5.5 6.0 6.5 7.0 7.5 8.0 8.5 9.0 9.5

Capacity Utilization (Capital)

11/30/2011 = 77.8%Capacity Tightening

Slack Capacity

68

70

72

74

76

78

80

82

84

68

70

72

74

76

78

80

82

84

Office Vacancy Rate (Capital)

3/31/2011 = 16.9%

Source: Cushman and Wakefield Average of downtown and suburban office rates 9 1011121314151617181920

9 1011121314151617181920

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Resource Utilization

Copyright 2012 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. . www.ndr.com/vendorinfo/ . For data vendor disclaimers refer to www.ndr.com/copyright.htmlSee NDR Disclaimer at

5 Fifth Third Bank | All Rights Reserved

Corporate Earnings Follow the Playbook

(S686)

Monthly Data 12/31/1953 - 2/29/2012 (Log Scale)

Latest Reported 4Q EPS (9/30/2011) = $86.98

S&P 500 (GAAP) Earnings Per Share:

S&P 500 Earnings Gain/ % Model: Annum of Time

Above 80% 20. 4 40. 4

* Between 40% and 80% 14. 8 35. 0

40% and Below -22. 3 24. 6

Source: Standard & Poor's 2.2 2.7 3.3 4.0 4.9 6.0 7.3 8.9

10.813.216.119.724.029.235.643.452.964.578.6

2.2 2.7 3.3 4.0 4.9 6.0 7.3 8.9

10.813.216.119.724.029.235.643.452.964.578.6

2/29/2012 = 79%

Strong Earnings Growth

Weak Earnings Growth

Source: Ned Davis Research, Inc.0 5

101520253035404550556065707580859095

100

0 5

101520253035404550556065707580859095

100

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

S&P 500 GAAP Earnings Per Share

S&P 500 Earnings Model Copyright 2012 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.

. www.ndr.com/vendorinfo/ . For data vendor disclaimers refer to www.ndr.com/copyright.htmlSee NDR Disclaimer at

6 Fifth Third Bank | All Rights Reserved

Source: Bureau of Labor Statistics

But Employment Doesn’t:

Source: FactSet Charts are use with permissions.

7 Fifth Third Bank | All Rights Reserved

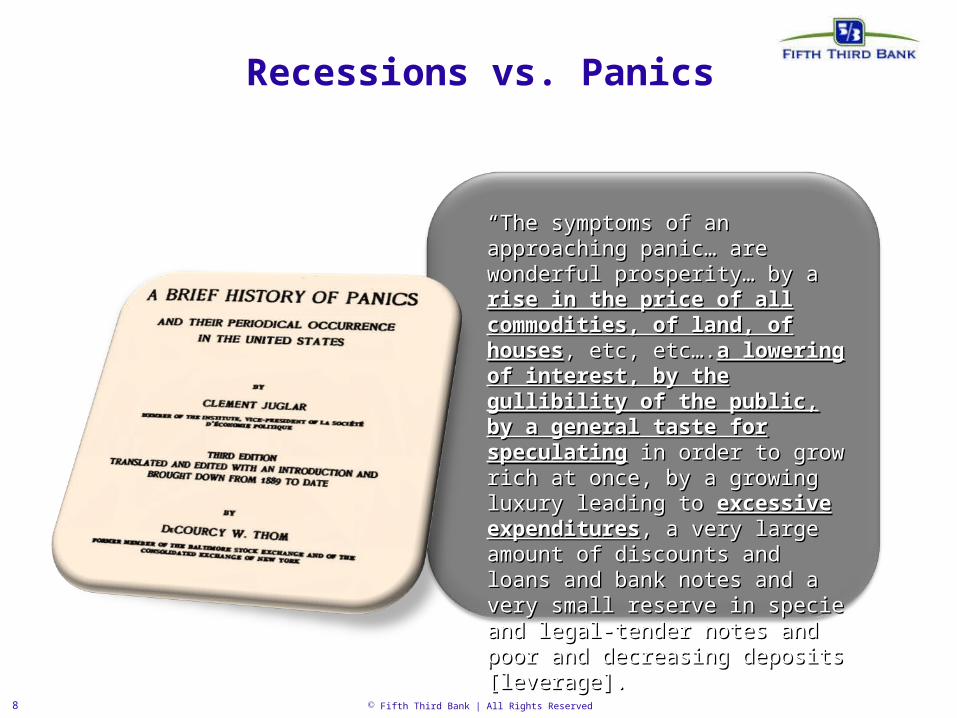

Recessions vs. Panics

8 Fifth Third Bank | All Rights Reserved

Recessions vs. Panics

““The symptoms of an approaching The symptoms of an approaching panic… are wonderful prosperity… by panic… are wonderful prosperity… by a a rise in the price of all rise in the price of all commodities, of land, of housescommodities, of land, of houses, , etc, etc….etc, etc….a lowering of interest, by a lowering of interest, by the gullibility of the public, by a the gullibility of the public, by a general taste for speculatinggeneral taste for speculating in in order to grow rich at once, by a order to grow rich at once, by a growing luxury leading to growing luxury leading to excessive excessive expendituresexpenditures, a very large amount of , a very large amount of discounts and loans and bank notes discounts and loans and bank notes and a very small reserve in specie and and a very small reserve in specie and legal-tender notes and poor and legal-tender notes and poor and decreasing deposits [leverage].decreasing deposits [leverage].

9 Fifth Third Bank | All Rights Reserved

Copyright 2011 Ned Davis Research, Inc

Deleveraging the Private SectorQuarterly Data 12/31/1951 - 12/31/2011

(E0503)

%

Shaded areas represent National Bureau of Economic

Research Recessions

12/31/2011 Debt = $ 24. 9 Trillion12/31/2011 GDP = $ 15. 3 Trillion

= 162.2%

97.5

102.3

125.7

181.3

92.3

96.3

115.5

Data Subject To Revisions ByThe Federal Reserve Board

Mean = 108.0%

54576063666972757881848790939699

102 105 108 111 114 117 120 123 126 129 132 135 138 141 144 147 150 153 156 159 162 165 168 171 174 177 180

54576063666972757881848790939699

102 105 108 111 114 117 120 123 126 129 132 135 138 141 144 147 150 153 156 159 162 165 168 171 174 177 180

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Private Domestic Nonfinancial Debt as a % of GDP

Copyright 2012 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. . www.ndr.com/vendorinfo/ . For data vendor disclaimers refer to www.ndr.com/copyright.htmlSee NDR Disclaimer at

10 Fifth Third Bank | All Rights Reserved

Copyright 2011 Ned Davis Research, Inc

Deleveraging the Private SectorQuarterly Data 3/31/1980 - 12/31/2011

(E0509A)

Financial Obligations Ratio 12/31/2011 = 15.93%

Mean = 17.17%

Adjusted Financial Obligations Ratio(excludes government transfer payments

from Disposable Personal Income)12/31/2011 = 19.88%

Mean = 20.35%

FORs include vehicle leases, rent, insurance, and property taxesin addition to required mortgage and consumer debt payments

Correlation Coefficient = 0.93

15.615.816.016.216.416.616.817.017.217.417.617.818.018.218.418.618.819.019.219.419.619.820.020.220.420.620.821.021.221.421.621.822.022.222.422.622.8

15.615.816.016.216.416.616.817.017.217.417.617.818.018.218.418.618.819.019.219.419.619.820.020.220.420.620.821.021.221.421.621.822.022.222.422.622.8

1980 1985 1990 1995 2000 2005 2010

Household Financial Obligations Ratios

Copyright 2012 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. . www.ndr.com/vendorinfo/ . For data vendor disclaimers refer to www.ndr.com/copyright.htmlSee NDR Disclaimer at

11 Fifth Third Bank | All Rights Reserved

Source: Federal Reserve, Pew Center for the States

Traditional Debt

Unfunded PensionLiabilities

Unfunded RetireeHealth Benefits

Deleveraging the Public Sector:It’s Worse Than We Thought

12 Fifth Third Bank | All Rights Reserved

States Lead the Way

2001 2010

Source: Pew Center on the States

13 Fifth Third Bank | All Rights Reserved

Source: Strategas Research, used with permission

Deleveraging the Public Sector:Washington’s turn next?

Components of the 2013 Fiscal Drag, $BNHealthcare

Sequester, -12.0Affordable Care Act Taxes, -26.0

Other, -14.8

Non-Defense Disc Sequester, -31.0 2010 Tax Cut

Extension, -303.3

Payroll Tax, UI-92.7

Defense Sequester

-55.0

14 Fifth Third Bank | All Rights Reserved

The Vicious Cycle of Long-Term Unemployment

Long-term unemployment leads to long-term unemployment

Weak housing lessens labor mobility

Hiring “intensity” stays weak

Average Duration on Unemployment in the U.S.(weeks, seasonally adjusted)

Source: BLS

Source: FactSet Research System charts are use with permission.

15 Fifth Third Bank | All Rights Reserved

Deconstructing Inflation: Wage Pressures

Source: Bloomberg Charts are used with permission.

YOY change: US Avg Hourly Earnings

U.S. Unemployment Rate

16 Fifth Third Bank | All Rights Reserved

Deconstructing Inflation: Commodity Pricing

Source:http://climatechange.thinkaboutit.eu/think4/post/homo_ecologicus_end_of_greed Source:http://en.wikipedia.org/wiki/An_Essay_on_the_Principle_of_Population

17 Fifth Third Bank | All Rights Reserved

Deconstructing Inflation:Commodity Pricing

'57 '59 '61 '63 '65 '67 '69 '71 '73 '75 '77 '79 '81 '83 '85 '87 '89 '91 '93 '95 '97 '99 '01 '03 '05 '07 '09 '11

100

200

300

400

500

600

©FactSet Research Systems

CRB Index: 2 Year Moving Average

Crb Spot Index, 1967=100 - United States (MOV 2Y) Crb Spot Index, 1967=100 - United States

Source: FactSet Charts are use with permission.

18 Fifth Third Bank | All Rights Reserved

Source: Cleveland Fed (Haubrich, Pennacchi, Ritchken)

Deconstructing Inflation: Expectations

19 Fifth Third Bank | All Rights Reserved

Deconstructing Inflation: The Real Risk

20 Fifth Third Bank | All Rights Reserved

Global Impacts in 2012

21 Fifth Third Bank | All Rights Reserved

Anticipating the Impactof Euro Zone Recession

Source: FactSet

22 Fifth Third Bank | All Rights Reserved

When a Half-Full Cup Beats One Half-Empty

S798 © Copyright 2011 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html For data vendor disclaimers refer towww.ndr.com/vendorinfo/

S&P 500 Earnings Yield vs. 10-Year Treasury Yield Monthly Data 1966-01-31 to 2011-08-31

S798 © Copyright 2011 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html For data vendor disclaimers refer towww.ndr.com/vendorinfo/

S&P 500 Earnings Yield vs. 10-Year Treasury Yield Monthly Data 1966-01-31 to 2011-08-31

1966 1968 1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15S&P 500 Earnings Yield (est.) -- Solid Blue Line 2011-08-31 = 6.88%

10-Year Treasury Yield -- Dashed Red Line 2011-08-31 = 2.30%

-4

-3

-2

-1

0

1

2

3

4

5

6

-4

-3

-2

-1

0

1

2

3

4

5

6 Earnings Yield Minus Treasury Yield 2011-08-31 = 4.58%

23 Fifth Third Bank | All Rights Reserved

percentage of the adult, nonbusiness-owner population that starts a business each month

The Potential For Upside Surprises

24 Fifth Third Bank | All Rights Reserved

Potential Upside in Reshoring Manufacturing

Source: BLS

$ Labor Costs in Manufacturing vs. U.S.

25 Fifth Third Bank | All Rights Reserved

Will Manufacturing Return?

Source: Bloomberg Charts are use with permissions

$/ Chinese Yuan

26 Fifth Third Bank | All Rights Reserved

Looking At 2012 Consensus

Federal ReserveEstimate

Wall StreetConsensus

Surprise PotentialBias vs Street

Real GDP 2.45% 2.2% Higher

Unemployment 8.35% 8.2% Lower

CPI 1.60% 2.30% Same

Fed Funds Rate n/a 0.25% Same

10-Year Tsy n/a 2.56% Lower

27 Fifth Third Bank | All Rights Reserved

Disclosures & Definitions

Opinions are provided by Fifth Third Private Bank.This information is intended for educational purposes only and does not constitute the rendering of investment advice or a specific recommendation on investment activities and trading. The mention of any specific security does not constitute a solicitation or an offer to buy or sell any security. This information is current as of the date of this presentation and is subject to change at any time, based on market and other conditions.

The Standard & Poor's 500 Stock Index is a composite of the 500 largest companies in the United States and it often used as a measure of the overall U.S. stock market.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market of goods and services purchased by individuals. The weights of components are based on consumer spending patterns

U.S. Treasury notes are issued with maturities of one to 10 years in denominations beginning at $1,000. Investors purchase bills at a discounted price from their face value. At maturity, the Treasury redeems the bills at full face value. The difference between the discounted price paid and the face value of the bill when it is redeemed is its return.

U.S. GDP (Gross Domestic Product) is the total market value of all final goods and services produced in a country in a given year, equal to total consumer, investment and government spending, plus the value of exports, minus the value of imports

CRB/Reuters Futures Price Index is an equal-weighted geometric average of commodity price levels relative to the base year average price.

Indexes are unmanaged and do not incur investment management fees. You cannot invest directly in an index. Past performance is no guarantee of future results.

Ned Davis Research Charts, Bloomberg Charts and FactSet Charts are used with permissions.

Fifth Third Bancorp provides access to investments and investment services through various subsidiaries. Investments and Investment Services:

Are Not FDIC Insured Offer No Bank Guarantee May Lose Value

Are Not Insured By Any Federal Government Agency Are Not A Deposit

28 Fifth Third Bank | All Rights Reserved

The U.S. Economy:A Difference of Kind

Q Q & & AA