1. introduction

TRANSCRIPT

AN INTRODUCTION

An effort to find out the fairness and to establish the reliability or unreliability of an entity’s financial

statement. Profit & Loss

Balance Sheet

Cash Flow Statement

Statement of Changes in Owner’s equity

“An audit is the independentexamination of, and expresssion ofopinion on, the financial statement ofan enterprise by an appointed auditorin pursuance of that appointment andin compliance with any relevant

statutory obligatios.”

The extent of audit tasks which aredetermined by an auditor forconducting the audit of a company.

According to AS 1

“ The audit procedures deemednecessary in the circumstancesto achieve the objective of theaudit.”

Factors which determines the scope:

1. Statutory Requirements ( Rules and Regulations

formed by the statute of Country)

2. Proper Planning ( To cover all aspects of entityrelevent to the financial statement)

3. Reasonable Assurance ( financial statementtaken as a whole are free from material misstatement)

4. Proper Evidence ( To check the correctness andadequacy of accounting records)

According to AS 1

“To enable the auditor to expressthe opinion whether the financialstatement are prepared, in allmaterial respects, in accordancewith the identified fianacialreporting framework.”

True and Fair View

Obtain all information necessary for Audit

B/S, P & L represent true and fair view

Proper accounting record

Prepare in accordance with the provision of Company Ordinance

Errors and Defalcations

May Audit fail to detect errors and irregularities

However sound audit procedure may enable auditor to discover material irregularities

Internal ControlAssist the management in

maintaining an adequate system of internal control by pin pointing the weak areas.

Constructive Advice and GuidelinesAuditor has thorough knowledge

about his client’s business

Delegate by

Shareholders

Accepted by

Directors (Management)

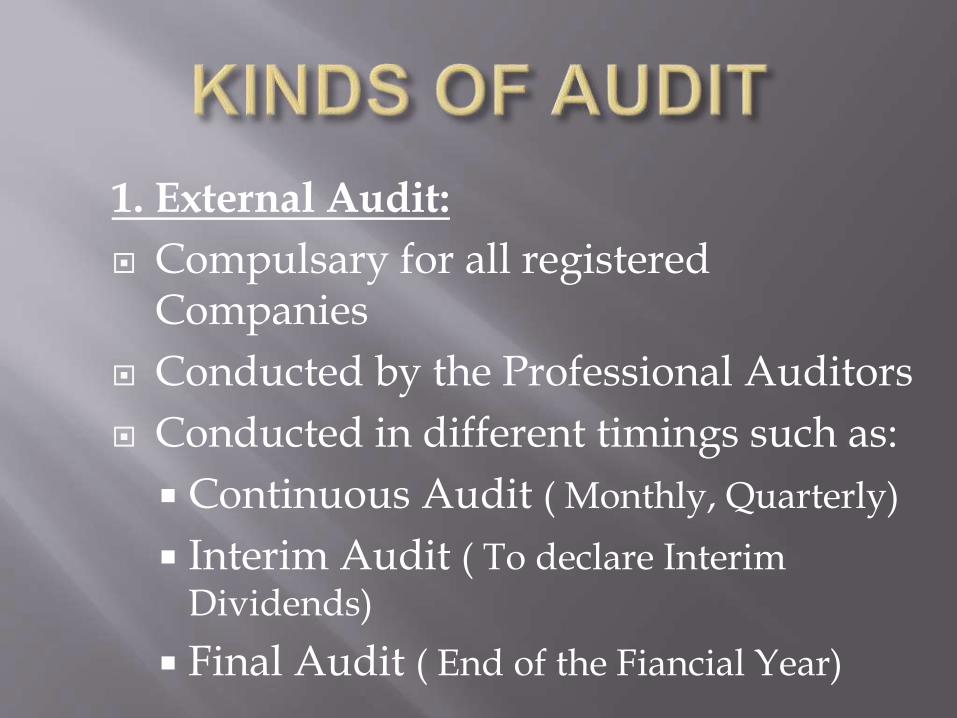

1. External Audit:

Compulsary for all registered Companies

Conducted by the Professional Auditors

Conducted in different timings such as:

Continuous Audit ( Monthly, Quarterly)

Interim Audit ( To declare Interim Dividends)

Final Audit ( End of the Fiancial Year)

2. Internal Audit

Process of reviewing and appraisingactivities pertaining to accounting,financial and other information.

Conducted by Internal Auditor

Aim to build sound and satisfactoryinternal control system

3. Cost Audit

Verification and examination of books ofcost accounts in accordance with costaccounting standards.

4. Government Audit

To examine the government accountsunder prescribed rules and to suggest totake remedial actions

5. Proprietory Auditor

To see the justification of costexpenditures incurred by the company.

6. Management Audit

To reveal the shortcomings orirregularities in Management forimproving operational profitability.

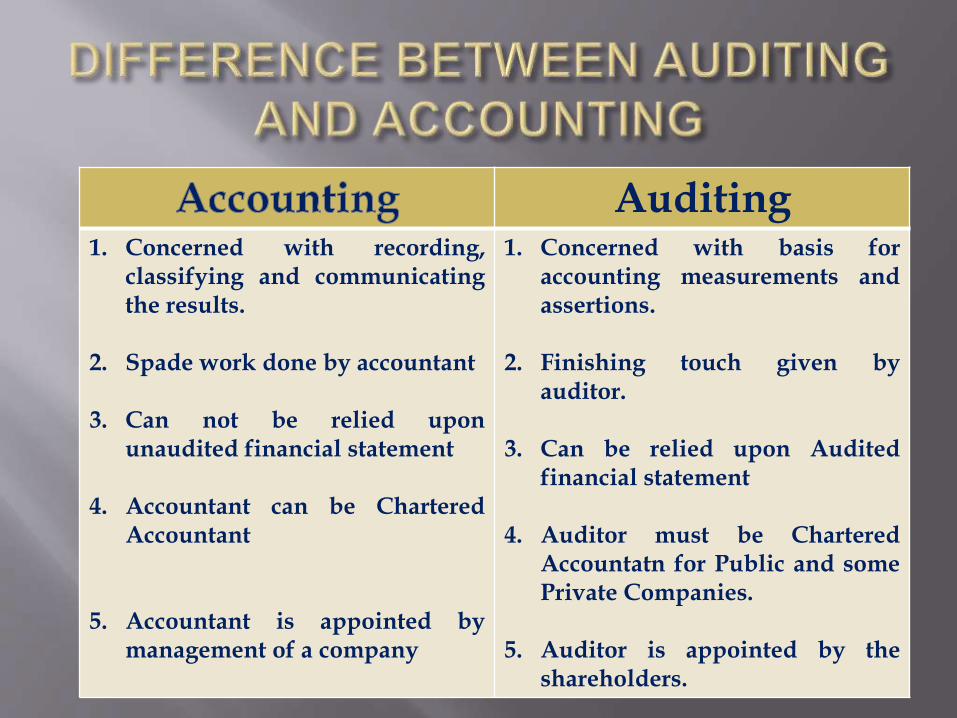

Auditing1. Concerned with recording,

classifying and communicatingthe results.

2. Spade work done by accountant

3. Can not be relied uponunaudited financial statement

4. Accountant can be CharteredAccountant

5. Accountant is appointed bymanagement of a company

1. Concerned with basis foraccounting measurements andassertions.

2. Finishing touch given byauditor.

3. Can be relied upon Auditedfinancial statement

4. Auditor must be CharteredAccountatn for Public and somePrivate Companies.

5. Auditor is appointed by theshareholders.

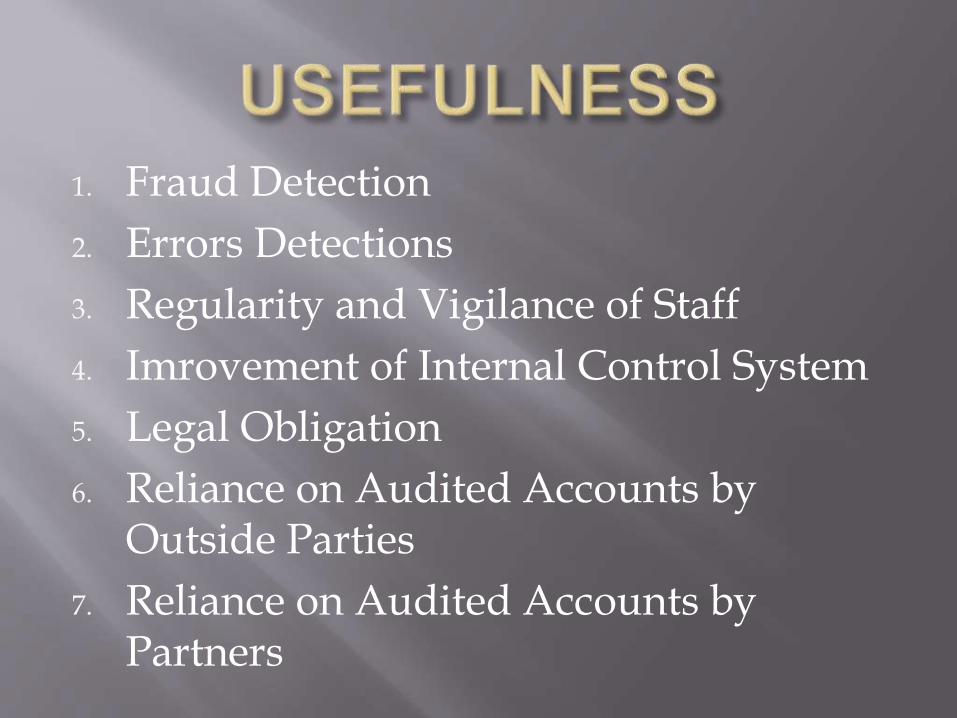

1. Fraud Detection

2. Errors Detections

3. Regularity and Vigilance of Staff

4. Imrovement of Internal Control System

5. Legal Obligation

6. Reliance on Audited Accounts by Outside Parties

7. Reliance on Audited Accounts by Partners

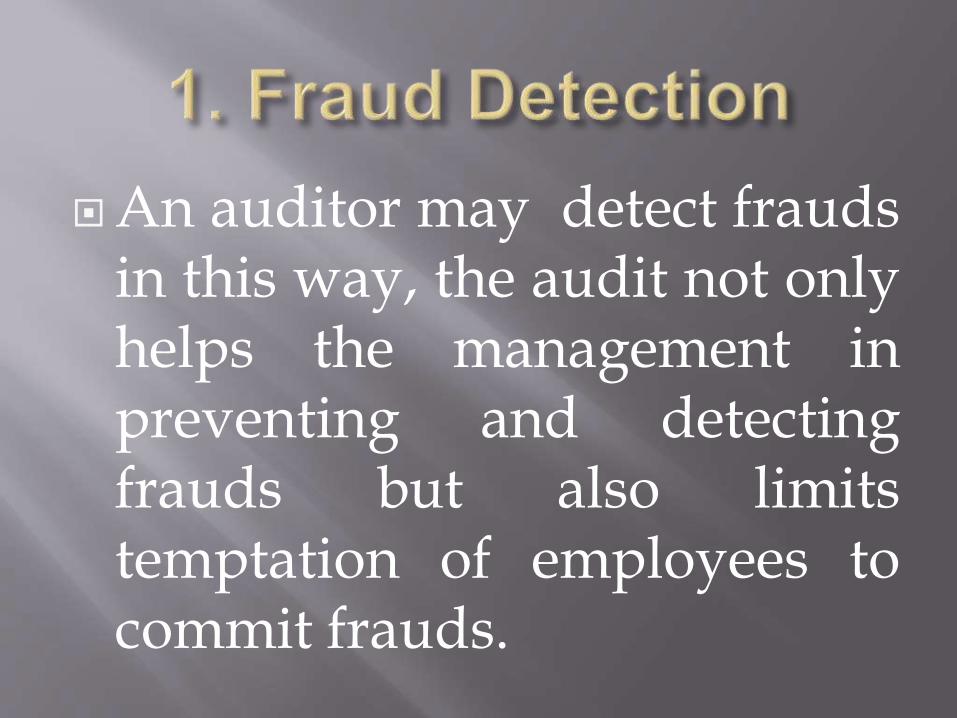

An auditor may detect fraudsin this way, the audit not onlyhelps the management inpreventing and detectingfrauds but also limitstemptation of employees tocommit frauds.

Sound system of audit maydetect material errors andprovide assurance to themanagement of the businessregarding accuracy of accountsand effectiveness of the internalcontrol system.

The staff of the accounts departmentbecome regular and vigilant due tothe conduct of an audit .

They keep the books of accounts upto-date and correct .

Thus the management can get anydesired information easily from theaccounts department without anydelay.

An independent audit of entity’saccounts may pin point the weakarea of the internal control of theorganization and provide valuablesuggestions to the management forimproving the internal control andaccounting procedure.

A business must follow the acts andordinance regarding business and ithas been become a regular feature tohave accounts audited by all concerns.

Business managed by CEO, Director(Shareholders not take active part inbusiness)

Public Corporations must haveaudited.

Audited accounts and financialstatements are considered to be themore reliable for the purpose of

1. Income tax assessments

2. Claim for compensation

3. Raising a loan

4. Proposed sales of business

Audited accounts may ensure theprovisions or the partnership agreementsrelating the rights and obligations ofpartners.

Enable the partners to settle the accounts ofa retiring partner.

Enable an incoming partner to assess theworth of the firm.

Facilitate the settlement of accountsbetween the existing partners and tend toprevent any future dispute.