1 marketing and logistics product order processing and information inventory place/customer service...

TRANSCRIPT

1

Marketing and Logistics

Product

Order processing and information

Inventory

Place/customer service levels

PromotionPrice

Procurement Warehousing

Transportation

LO

GIS

TIC

SM

AR

KE

TIN

G

2

Logistics Operations

Demand

Transportation

Stock

Managem

ent Purchas

e Ord

ers

Proce

ssing

Handling Packaging

Purc

hase

Sales

ProductionScheduling

Warehousing

3

Value-Added Functions of Logistics

Production

Location

Time

ControlLogistics

4

Evolution of Logistical Integration, 1960-2000

Demand Forecasting

Purchasing

Requirements Planning

Production Planning

Manufacturing Inventory

Warehousing

Materials Handling

Packaging

Inventory

Distribution Planning

Order Processing

Transportation

Customer Service Strategic Planning

MaterialsManagement

PhysicalDistribution

LogisticsSupply ChainManagement

Information Technology

Marketing

1980s

1990s

2000s

5

The goal of supply chain management

“To manage upstream and downstream relationships with

suppliers and customers in order to create enhanced value in the final

market place at less cost to the supply chain as a whole.”

6

Changes in Global Trade Flows

Industrial Pole

Before 1990 After 1990

Developed Countries

Developing Countries

Developed Countries

Developing Countries

Flows of merchandises Flows of raw materials

7

Maritime Routes and Strategic Locations

SuezHormuz

PanamaMalacca

Bosporus

Magellan

Good Hope

Gibraltar

Bab el-Mandab

8

Major Economic Blocs, 2005

EU

EU Expansion

NAFTA

Mercosur

Andean Pact

ASEAN

EFTA

CAFTA

Caricom

Central America Europe

9

Levels of Economic Integration

Free trade between members: NAFTA, Mercosur, ASEAN (partial)

Free Trade

Common external tariffsCustoms Union

Factors of production move freely between members

Common Market

Common currency, harmonized tax rates, common monetary and fiscal policy: EU (partial)

Economic Union

Common governmentPoliticalUnion

Leve

l of i

nteg

ratio

n

Complexity

10

Global Exports of Merchandises, 1963-2003

0%

20%

40%

60%

80%

100%

1963 1975 1990 1994 2000 2003

Manufactured products

Mineral products

Agricultural products

11

Trade as Share of GDP

Less than 20%

20% to 40%

40% to 60%

60% to 100%

100% to 150%

More than 150%

Not Available

12

A B

Rail

Origin Destination

Transport Chain

Maritime Road

International Trade

Transshipment

International Trade and Transportation Chains

A B

Assembly Disassembly

Trade barrier

Customs

13

Average Tariffs after the Uruguay Round (%)

0 10 20 30 40 50 60 70

All industrial products

Textiles & clothing

Mineral products

Transport equipment

Fish & fish products

Leather, footwear & travel goods

Chemical & photographic supplies

Electrical machinery

Other manufactured articles

Wood, paper & furniture

Nonelectrical machinery

Metals

Reduction

Tariff

14

“Platform” Corporation

15

Complexity of the Supply Chain

FactoryDistribution center

Representative

National

International

National Supply Chain Multinational Supply ChainSimple Complex

High-throughputDC

16

Share of Containerized Cargo in Global Trade, 1980-2000

0

100

200

300

400

500

600

700

800

1980 1985 1990 1995 2000

Mill

ion

tons

Containerized Cargo

Other General Cargo

17

Product Life CycleS

ales

Stage 1 Stage 2 Stage 3

Monopoly Competition

Research anddevelopment

Maturity Decline

First competitors Mass production

Innovating firm

Competitors

Growth

Stage 4

PromotionIdeaDecline ofproduction

18

Product Life Cycle of a Television, 1960-1996

0

2

4

6

8

10

12

1960 1980 1990 1996

Year

s

Low

Medium

High

19

Shorter life cycles make timing crucial

Sales

Time

• Less time to make profit• Higher risk of obsolescence

Market

Late Entrant

ObsolescentStock

20

The role of cash in creating shareholder value

“the value of a company is determined by the discounted value of the cash that can be

taken out of the business during its remaining life”

Warren Buffet

21

Logistics impact on operating income

Logistics variable

Customer service

Purchasing strategy

Capacity scheduling and control

Order processing

Transportation

Warehousing

Inventory control

Packaging

Support activities

Inventory carrying cost

Income statement

Net sales

Costs of goods sold

Selling and administration expense

Interest expenseIncome before tax

22

Logistics impact on the balance sheet

Logistics variable

Order cycle time

Order completion rate

Invoice accuracy

Inventory

Distribution facilities and equipment

Plant and equipment

Purchase order quantities

Financing options for inventory Plant and equipment

Balance sheetAssets

Cash

Receivables

Inventories

Property, plant and equipment

LiabilitiesCurrent liabilities

Debt

Equity

23

Routes to improved shareholder value

Boost shareholder value

Raise return on capital

Net income increase

Revenue growth

Innovation

Customer relationshipmanagement

Integrated supply chain

Cost optimisation

Capital reduction

Working capital

Inventory

Receivables

Payables

Fixed assets

Sourcing

Production

Logistics

Network

Facilities

Real estate

Source : Mercer Management Consulting

24

Logistics and economic value added

LabourLabour

Material &PurchasesMaterial &Purchases

OverheadsOverheads

Netreceivables

Netreceivables

InventoryInventory

CashCash

Cost ofsales

Cost ofsales

SalesSales

Netoperating

profit

Netoperating

profit

Cost ofdebt

Cost ofdebt

Cost ofequity

Cost ofequity

Net workingcapital

Net workingcapital

FixedassetsFixedassets

CapitalemployedCapital

employed

True costof capitalTrue costof capital

CapitalchargeCapitalcharge

Economicvalueadded

Economicvalueadded

+

+

+

+ +

x

25

Total Freight Costs for Imports in World Trade (% of Total Costs)

0 2 4 6 8 10 12 14

Word

Developed Countries

Developing Countries

Africa

America

Asia

Europe

Oceania

2000

1990

26

Market Share by Freight Transport Mode, Western Europe, 1980-2002 (in ton-km)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1980 1985 1990 1995 2000 2002

Inland Waterways

Road

Rail

27

Logistical Improvements, Manufacturing Sector, 1960-2000

0

2

4

6

8

10

12

14

16

18

20

1960s 1970s 1980s 1990s 2000s

% o

f GDP

0

5

10

15

20

25

30

35

40

Days

Logistics Costs (% GDP)

Inventory Costs (% GDP)

Cycle Time Requirements (days)

28

Worldwide Logistics Costs

39%

27%

24%

6%4%

Transportation

Warehousing

Inventory Carrying

Order Processing

Administration

29

Logistics Costs and Economic Development

Agriculture Mining Industry Services Information

Log

isti

cs C

osts

/ G

NP

Economic Development

United StatesJapan

Singapore

Argentina

Kenya

Brazil Poland

Ukraine

Belgium

Canada

30

Logistical Cost Trade-off

storage costs

inventory costs

transport costs

total distribution costs

cost

no. of warehouses

31

From Push to Pull Logistics

Supplier Supplier Supplier

Manufacturer

Customer

Distributor

Supplier Supplier Supplier Supplier

Supplier Supplier Supplier

Manufacturer

Distributor

Customer

3PL

Returns / Recycling Point-of-sale data

Freight flow

Push Pull

32

Average Order Lead Times of European Manufacturers, Wholesalers, and Retailers

0

5

10

15

20

25

30

1985 1990 1995 2000 2005

Days

33

Changes in the Relative Importance of Logistical Functions

in Distribution Systems

0% 20% 40% 60% 80% 100%

Supply Driven

Demand Driven

Inventory

Transport System

Information System

34

Conventional and Contemporary Arrangement of Goods Flow

Raw Materials & Parts Manufacturing Distribution

RawMaterials

Storage NationalDistribution

RegionalStorage

LocalDistribution

Retailers

Supply Chain Management

RawMaterials

DistributionCenter

RetailersManufacturing

Cu

sto

mers

Cu

sto

mers

Conventional

Contemporary

Material flow (delivery)

Information flow (order)

Core component

35

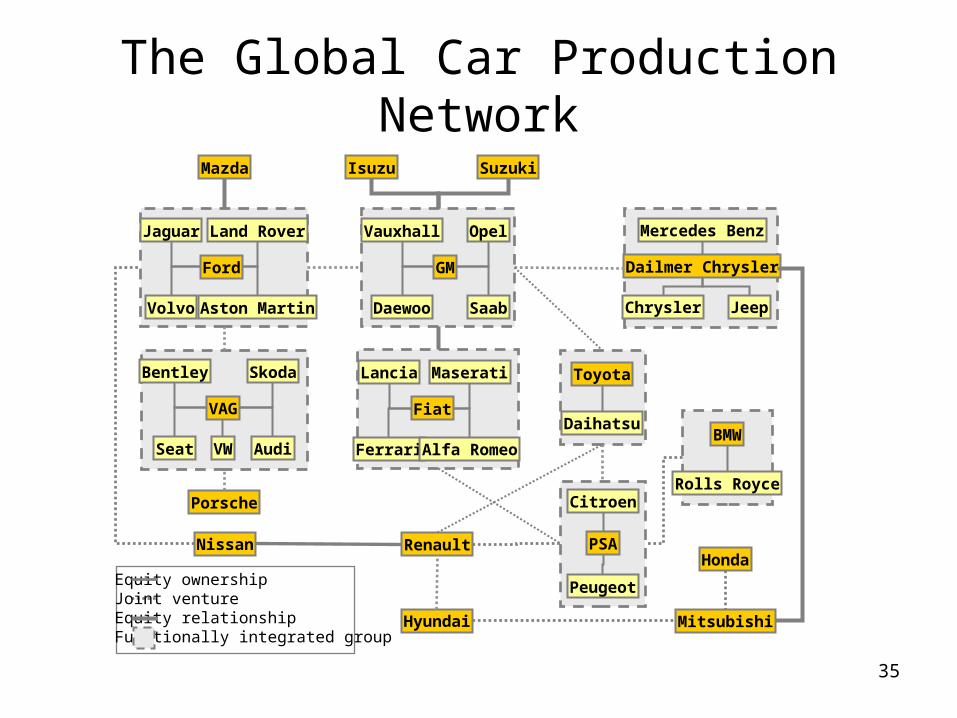

The Global Car Production Network

Ford

Jaguar Land Rover

Volvo Aston Martin

Mazda Isuzu Suzuki

GM

Vauxhall Opel

Daewoo Saab

VAG

Bentley Skoda

Seat AudiVW

Dailmer Chrysler

Mercedes Benz

Chrysler Jeep

Fiat

Lancia Maserati

Ferrari Alfa Romeo

Toyota

Daihatsu

Porsche

Nissan Renault

Hyundai

PSA

Peugeot

Citroen

BMW

Rolls Royce

Mitsubishi

HondaEquity ownershipJoint ventureEquity relationshipFunctionally integrated group

36

The Automobile Supply Chain

Supplyingindustries

Steel and other metals

Rubber

Electronics

Plastic

Glass

Textiles

Bodies

Components

Engines and transmissions

Final Assembly

Manufacture and stamping of body

panels

Body assembling and painting

Manufacture of mechanical and electrical components (wheels, tires, seats, breaking

systems, windshields, exhausts, etc.)

Forging and casting of engine and transmission

components

Machining and assembly of engines and transmissions

Consumer market

37

Cereals Supply Chain

Farm

Wood Pulp Mfg

Processing Facility

Packaging

Label Mfg

Converter Distributor Store

Packaged Cereal

Packaged Cereal

Grain

Wood Pulp

Paperboard

LabelsWood Pulp

Cereal

Distribution and Retailing

ManufacturingExtraction

38

Third and Fourth Party Logistics Providers

39

Ten Largest Global Logistics Service Providers

0 5 10 15 20 25 30 35 40 45 50

GEODIS

Schenker

TNT Post Group

Deutsche Bahn Cargo

NFC/Exel

Kuhne & Nagel

Danzas

Maersk Moeller

Panalpina

Deutsche Post FrachtEmployees (thousands)

Revenue (Billion $US)

40

Forward and Reverse Distribution

Con

su

mers

Producers Distributors

CollectorsRecyclers

Forward ChannelReverse Channel

Su

pp

liers

41

Characteristics of Large-scale Distribution Centers

Size Larger More throughput and less warehousing.

Facility One storey; Separate loading and unloading bays

Sorting efficiency.

Land Large lot Parking space for trucks; Space for expansion.

Accessibility Proximity to highways Constant movements (pick-up and deliveries) in small batches; Access to corridors and markets.

Market Regional / National Less than 48 hours service window.

IT Integration Sort parcels; Control movements from receiving docks to shipping dock; Management systems controlling transactions.

42

Cross-Docking Distribution Center

Suppliers

Customers

Receiving

Shipping

Sorting

Distribution Center Before Cross-Docking

LTL

Suppliers

Customers

After Cross-Docking

TL

TL

Cross-Docking DC

43

National Semiconductors, Supply Chain, 1993, 2001, 2005

Wafer Fabrication Assembly & Testing Distribution Center

South Portland (Maine)

Salt Lake City (UT)

Santa Clara (CA)

Arlington (TX)

Greenock (Scotland)

Migdal Haemek (Israel) Cebu (Philippines)

Bangkok (Thailand)

Penang (Malaysia)

Melaka (Malaysia)

Toa Payoh (Singapore)

Santa Clara

Swindon (UK)

Tokyo

Hong Kong

South Portland

Regional Distribution Centers (1993)

South Portland (Maine)

Salt Lake City (UT)

Santa Clara (CA)

Arlington (TX)

Greenock (Scotland) Cebu (Philippines)

Bangkok (Thailand)

Penang (Malaysia)

Melaka (Malaysia)

Toa Payoh (Singapore)

Global Distribution Center (2001)

Singapore (GDC)

Singapore (GDC)

South Portland (Maine)

Arlington (TX)

Greenock (Scotland)

Supply Chain Rationalization (2005)

Suzhou (China)

Melaka (Malaysia)

Toa Payoh (Singapore)

Cu

sto

mers

44

Gaining competitive advantage

“A business is profitable if the value it creates exceeds the cost of performing the value activities. To gain competitive advantage over its rivals, a company must either perform these activities at a lower cost or perform them in a way that leads to differentiation and a premium price (more value).”

Michael Porter

45

Achieving an integrated supply chain

Stage One: BaselineMaterialflow

Customerservice

MaterialControl

Purchasing Production Sales Distribution

Stage Three: Internal IntegrationMaterialflow

Customerservice

ManufacturingManagement

MaterialsManagement Distribution

Stage Two: Functional IntegrationMaterialflow

Customerservice

ManufacturingManagement

MaterialsManagement

Distribution

Stage Four: External IntegrationMaterialflow

Customerservice

Internal SupplyChain

Suppliers Customers

46

The two dimensions of supply chain excellence

• Cost advantage :

Lower end-to-end delivered cost

• Value advantage :

Creating superior customer value through enhanced service

47

Supply chain excellence

RelativeCustomer

Value

RelativeDelivered Cost

High

Low

LowHigh

48

Gaining competitive advantage through logistics

Value Advantage

Logistics Leverage Opportunities:• Tailored service• Reliability• Responsiveness, etc

Cost Advantage

Logistics Leverage Opportunities:• Capacity utilisation• Asset turn• Schedule integration

49

How long is the logistics pipeline?

CumulativeLead-Time

(Procurementto Payment)

Raw Material Stock

Sub-Assembly Stock

Intermediate Stock

Product Assembly

Finished Stock at Central Warehouse

In-Transit

Regional Distribution Centre Stock

Customer Order Cycle (Order-Cash)

50

Logistics and E-commerce

Retailer

Supply chain

E-Retailer

Customers Customers

Supply chain

Warehousing

Warehousing

Tra

dit

ion

al Log

isti

cs

E-L

og

istic

s

51

Shifts of Logistical Operations in the Internet economy

Traditional logistics E-logistics

Orders Predictable Variable

Order cycle time Weekly Daily or hourly

Customer Strategic Broader base

Customer service Reactive, rigid Responsive, flexible

Replenishment Scheduled Real-time

Distribution model Supply-driven (push) Demand-driven (pull)

Demand Stable, consistent More cyclical

Shipment type Bulk Smaller lots

Destinations Concentrated More dispersion

Warehouse reconfiguration Weekly or monthly Continual, rules-based

International trade compliance Manual Automated

52

Producer and Buyer-driven Commodity Chains

Manufacturers DistributorsRetailers and

Dealers

Producer-driven

Domestic and foreign subsidiaries and subcontractors

Buyer-driven

Factories

Traders

OverseasBuyers

BrandedManufacturers

Retailers

BrandedMarketers

International National

53

Producer-Driven and Buyer-Driven Global Commodity Chains

Producer-Driven Commodity Chains Buyer-Driven Commodity Chains

Drivers of Global Commodity Chains

Industrial Capital Commercial Capital

Core Competencies Research & Development; Production Design; Marketing

Barriers to Entry Economies of Scale Economies of Scope

Economic Sectors Consumer Durables; Intermediate Goods; Capital Goods

Consumer Nondurables

Typical Industries Automobiles; Computers; Aircraft Apparel; Footwear; Toys

Ownership of Manufacturing Firms

Transnational Firms Local Firms, predominantly in developing countries

Main Network Links Investment-based Trade-based

Predominant Network Structure

Vertical Horizontal

54

Benefits of Demand-Driven Supply Systems

Inventory turnover Working capital

Cause Consequence

Customer service Net income

Labor productivity Operating expenses

Capacity utilization Return on assets

Logistics costs Operating expenses