1 public pension reform and fiscal consolidation carlo cottarelli director fiscal affairs department...

TRANSCRIPT

1

Public Pension Reform andFiscal Consolidation

Carlo CottarelliDirector

Fiscal Affairs Department

May 20, 2010Paris

2

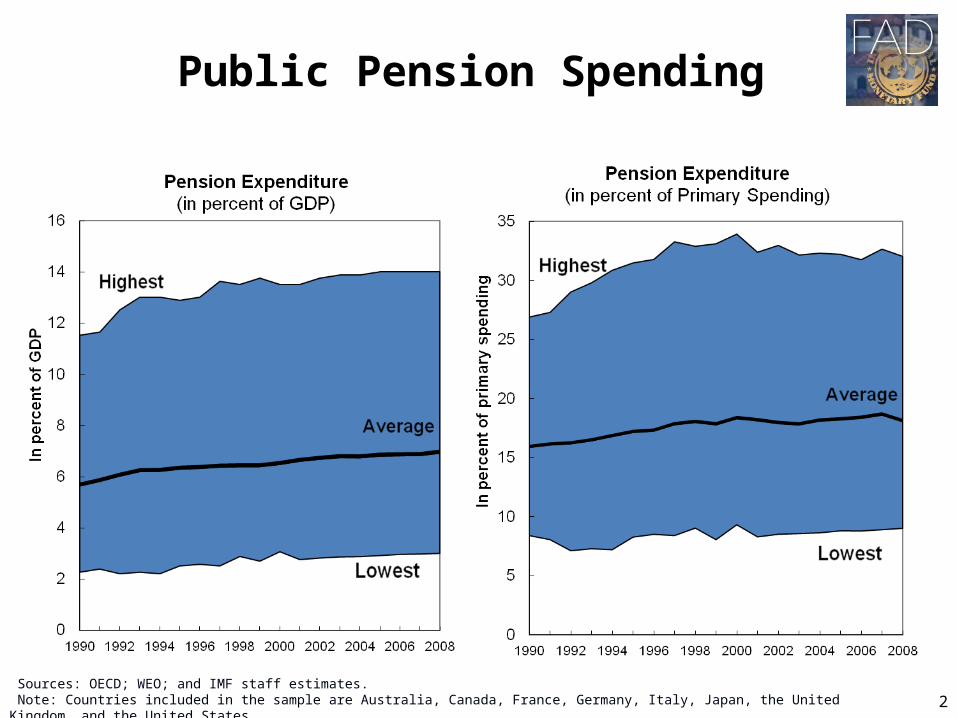

Public Pension Spending

Sources: OECD; WEO; and IMF staff estimates. Note: Countries included in the sample are Australia, Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States.

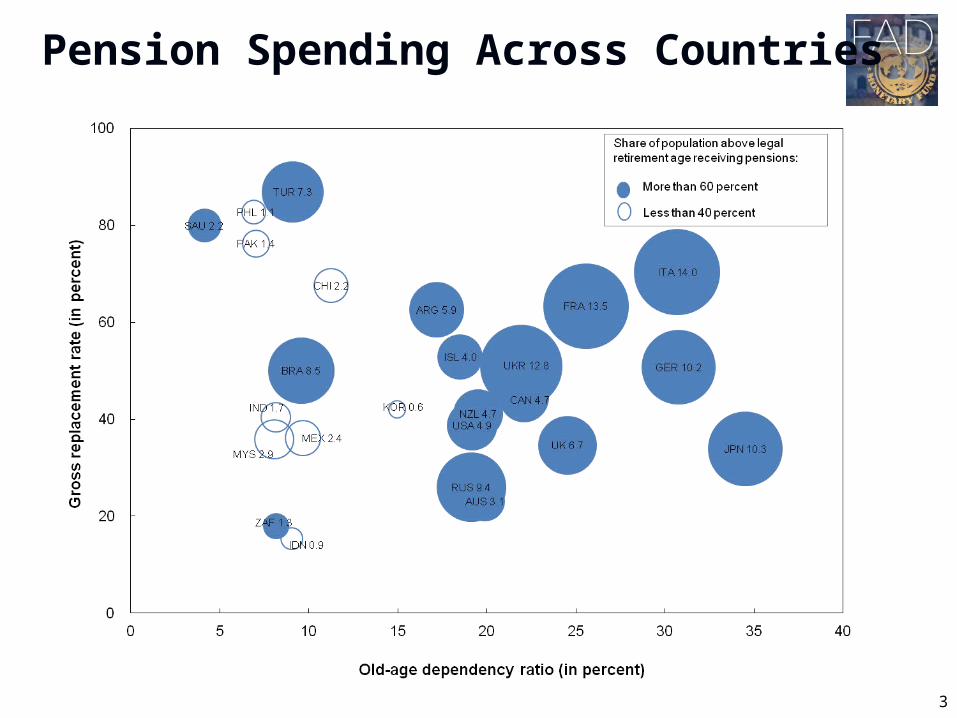

Pension Spending Across Countries

3

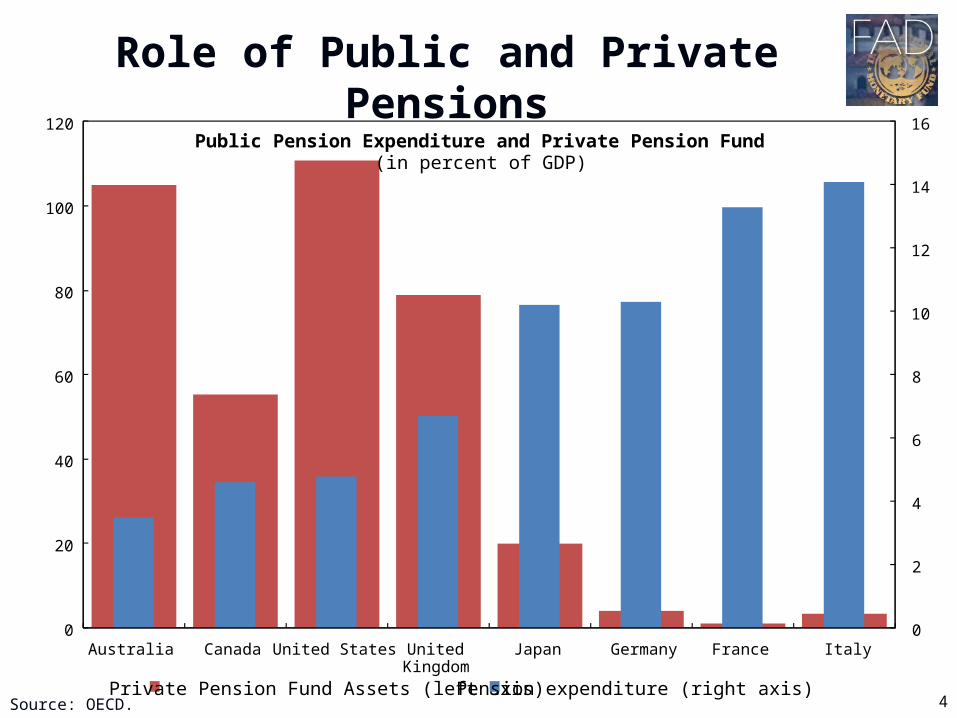

Role of Public and Private Pensions

4

0

2

4

6

8

10

12

14

16

0

20

40

60

80

100

120

Australia Canada United States United Kingdom

Japan Germany France Italy

Public Pension Expenditure and Private Pension Fund (in percent of GDP)

Private Pension Fund Assets (left axis) Pension expenditure (right axis)Source: OECD.

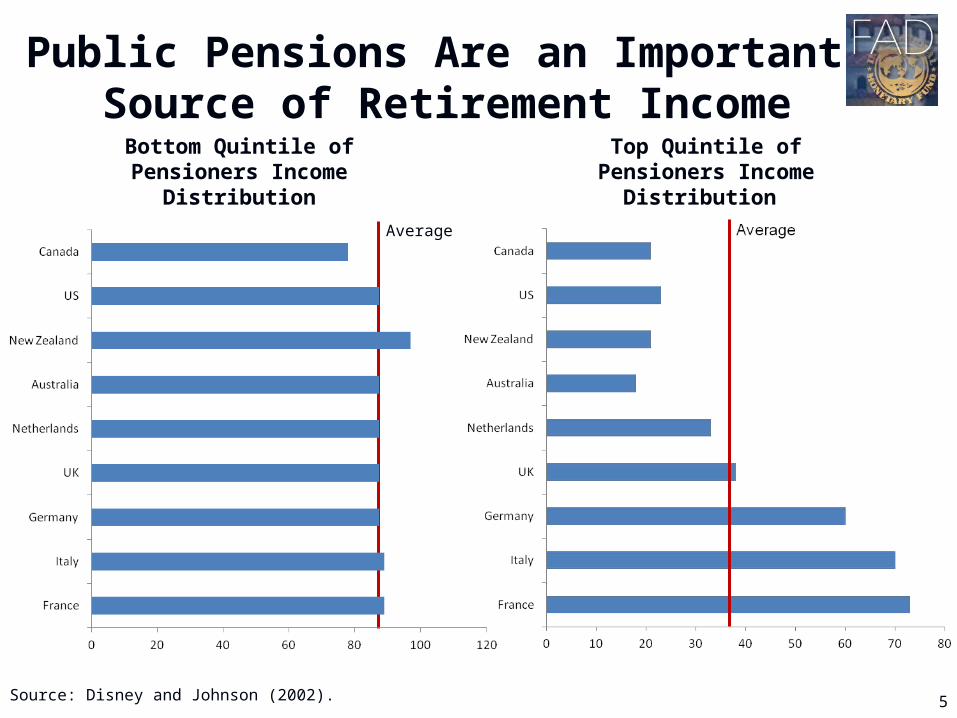

Public Pensions Are an Important Source of Retirement Income

5Source: Disney and Johnson (2002).

Bottom Quintile of Pensioners Income

Distribution

Top Quintile of Pensioners Income

Distribution

Average

6

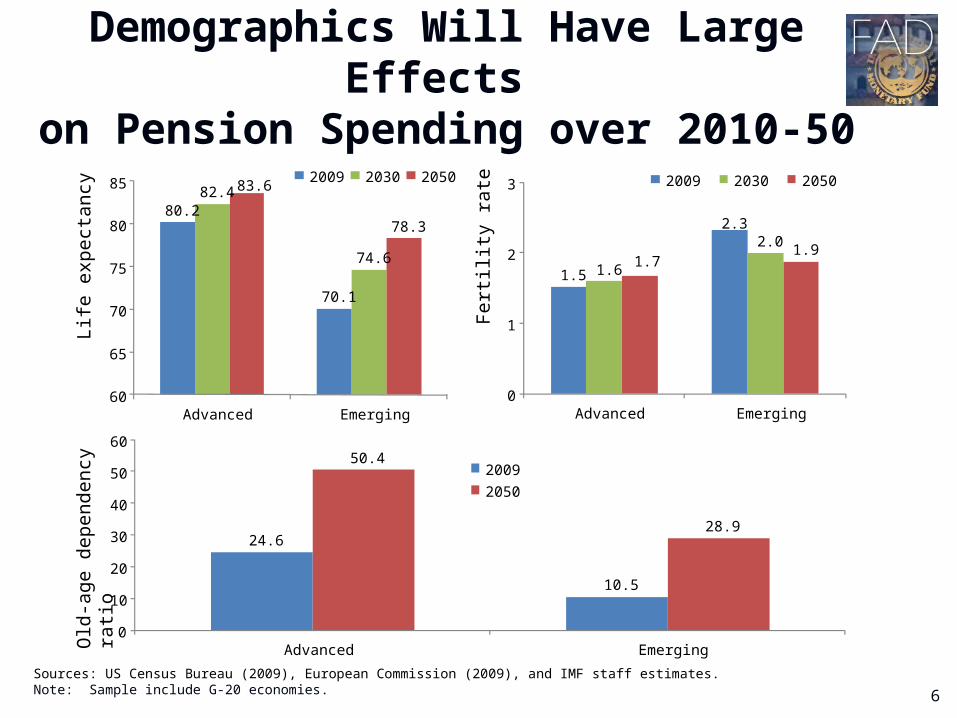

80.2

70.1

82.4

74.6

83.6

78.3

60

65

70

75

80

85

Advanced Emerging

Life

exp

ecta

ncy

2009 2030 2050

1.5

2.3

1.6

2.01.7

1.9

0

1

2

3

Advanced Emerging

Fer

tility

rat

e

2009 2030 2050

24.6

10.5

50.4

28.9

0

10

20

30

40

50

60

Advanced EmergingOld

-age

dep

ende

ncy

ratio

2009

2050

Demographics Will Have Large Effects on Pension Spending over 2010-50

Sources: US Census Bureau (2009), European Commission (2009), and IMF staff estimates.Note: Sample include G-20 economies.

6

7

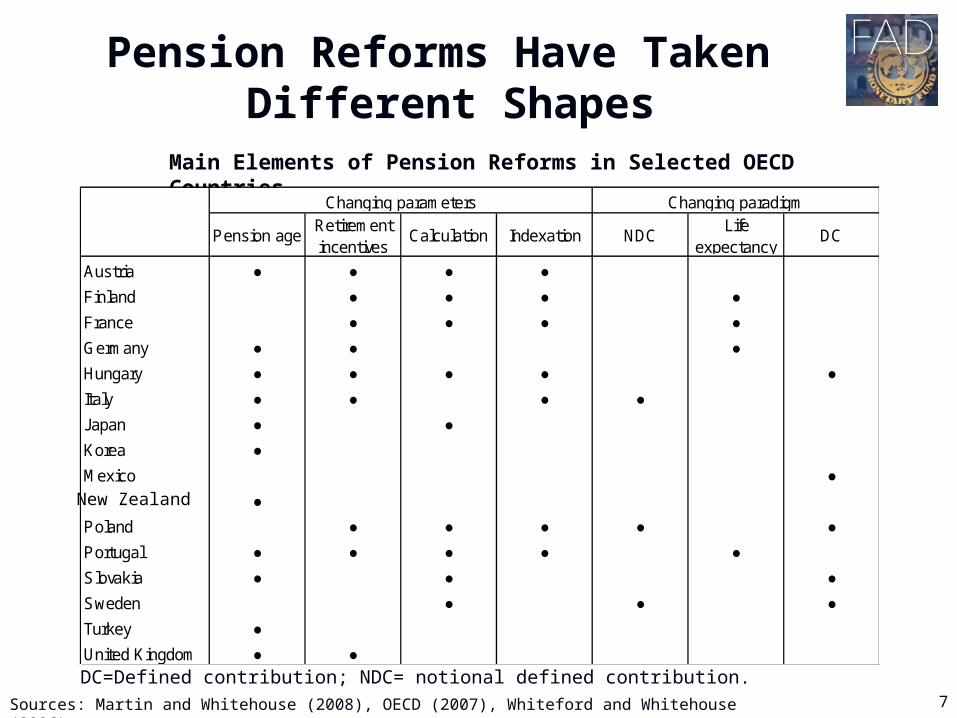

Pension Reforms Have Taken Different Shapes

Main Elements of Pension Reforms in Selected OECD Countries

Sources: Martin and Whitehouse (2008), OECD (2007), Whiteford and Whitehouse (2006).

Pension ageRetirement incentives

Calculation Indexation NDCLife

expectancyDC

Austria ● ● ● ●

Finland ● ● ● ●

France ● ● ● ●

Germany ● ● ●

Hungary ● ● ● ● ●

Italy ● ● ● ●

Japan ● ●

Korea ●

Mexico ●

NewZealand ●

Poland ● ● ● ● ●

Portugal ● ● ● ● ●

Slovakia ● ● ●

Sweden ● ● ●

Turkey ●

United Kingdom ● ●

Changing parameters Changing paradigm

DC=Defined contribution; NDC= notional defined contribution.

New Zealand

8

0

2

4

6

8

10

12

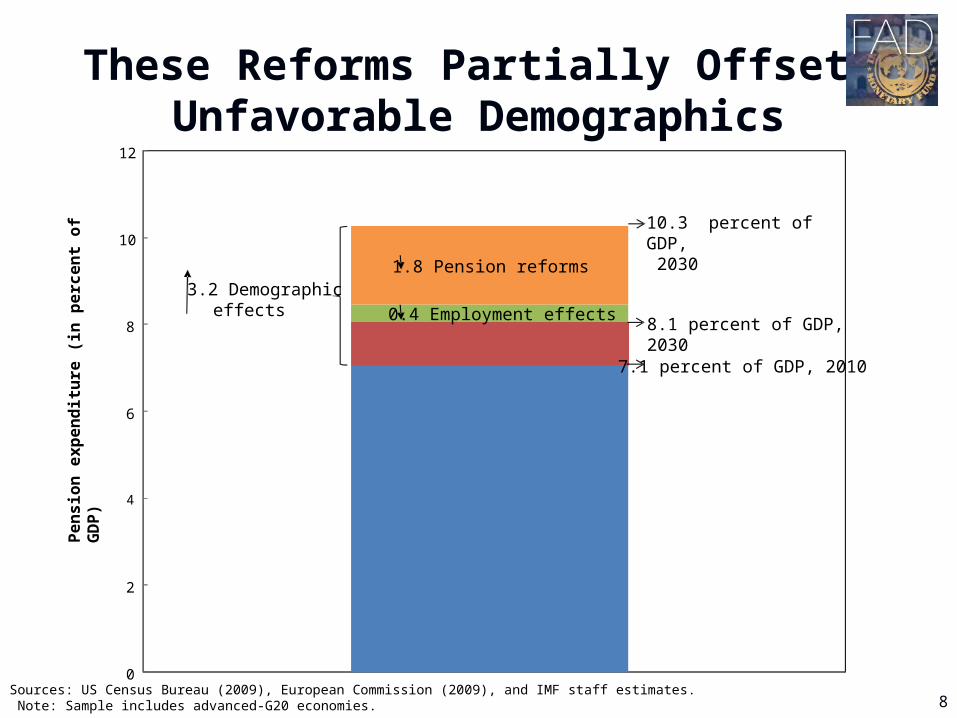

3.2 Demographiceffects 0.4 Employment effects

1.8 Pension reforms

7.1 percent of GDP, 2010

8.1 percent of GDP, 2030

Pe

ns

ion

ex

pe

nd

itu

re (

in p

erc

en

t o

f G

DP

)

10.3 percent of GDP, 2030

These Reforms Partially Offset Unfavorable Demographics

Sources: US Census Bureau (2009), European Commission (2009), and IMF staff estimates. Note: Sample includes advanced-G20 economies.

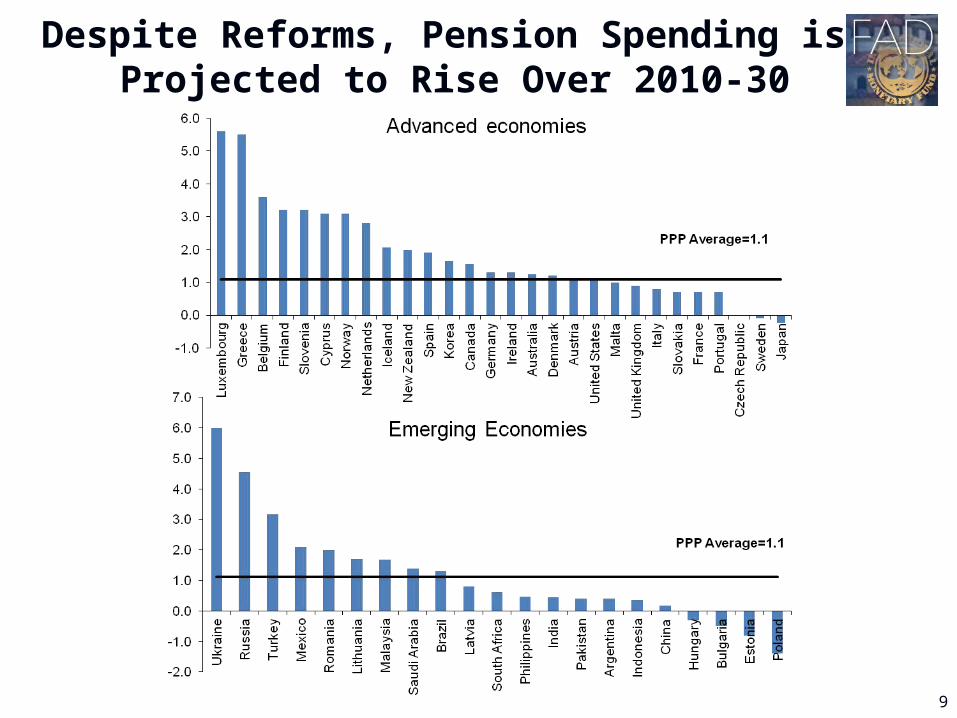

Despite Reforms, Pension Spending is Projected to Rise Over 2010-30

9

Future Pension Spending Will Add Substantially to Public Debt

10

Net Present Value of Future Pension Spending Increases

(in percent of GDP)

2010-2030 2030-2050

Average 8.3 23.2

Advanced 8.7 21.5

Emerging 7.8 25.9

11

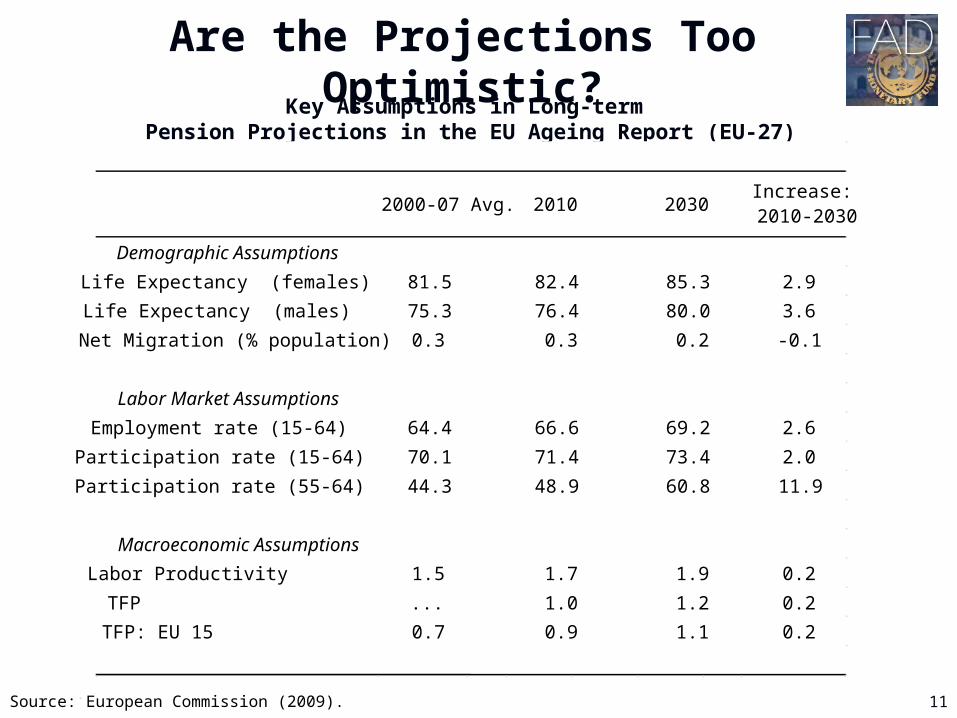

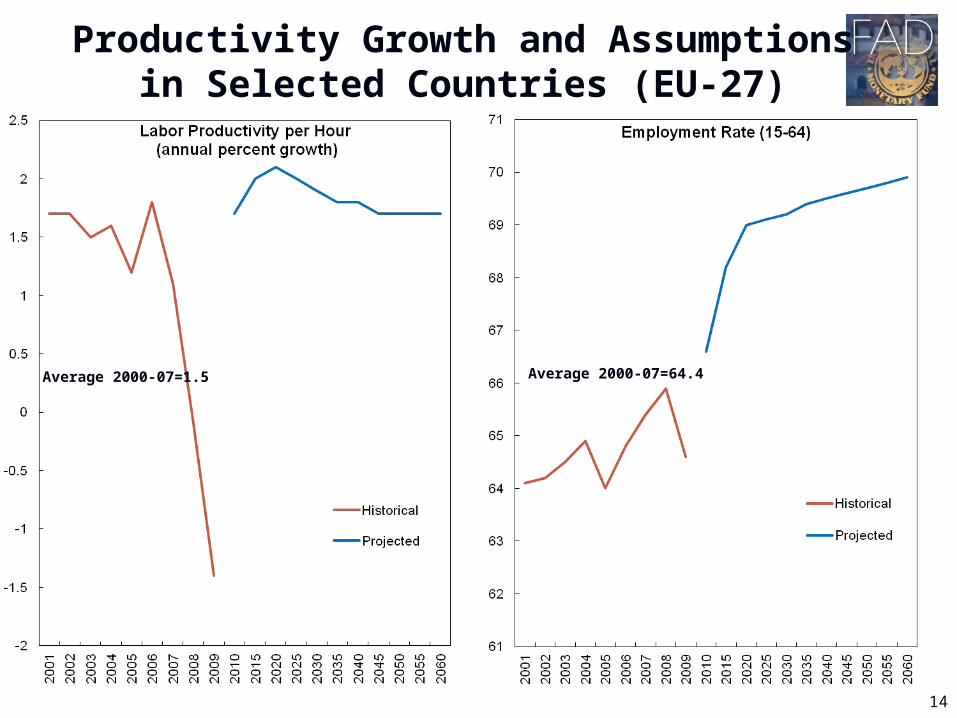

Key Assumptions in Long-term Pension Projections in the EU Ageing Report (EU-27)

Are the Projections Too Optimistic?

Source: European Commission (2009).

2000-07 Avg. 2010 2030Increase:

2010-2030

Demographic Assumptions

Life Expectancy (females) 81.5 82.4 85.3 2.9

Life Expectancy (males) 75.3 76.4 80.0 3.6

Net Migration (% population) 0.3 0.3 0.2 -0.1

Labor Market Assumptions

Employment rate (15-64) 64.4 66.6 69.2 2.6

Participation rate (15-64) 70.1 71.4 73.4 2.0

Participation rate (55-64) 44.3 48.9 60.8 11.9

Macroeconomic Assumptions

Labor Productivity 1.5 1.7 1.9 0.2

TFP ... 1.0 1.2 0.2

TFP: EU 15 0.7 0.9 1.1 0.2

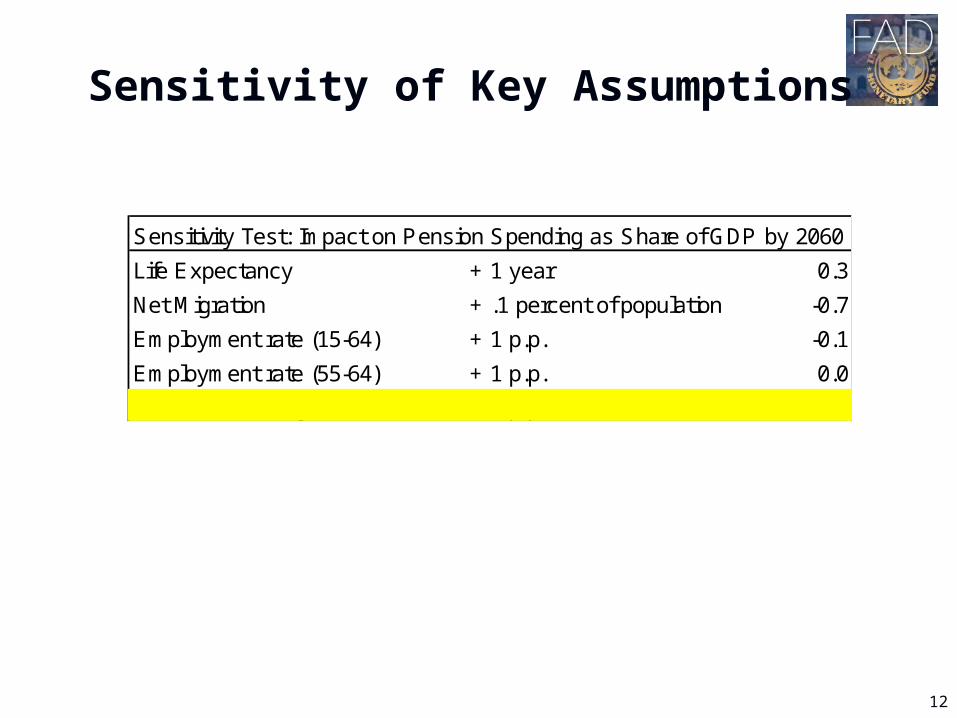

Sensitivity of Key Assumptions

12

Sensitivity Test: Impact on Pension Spending as Share of GDP by 2060

Life Expectancy + 1 year 0.3

Net Migration + .1 percent of population -0.7

Employment rate (15-64) + 1 p.p. -0.1

Employment rate (55-64) + 1 p.p. 0.0

Labor Productivity + 1 p.p. -1.6

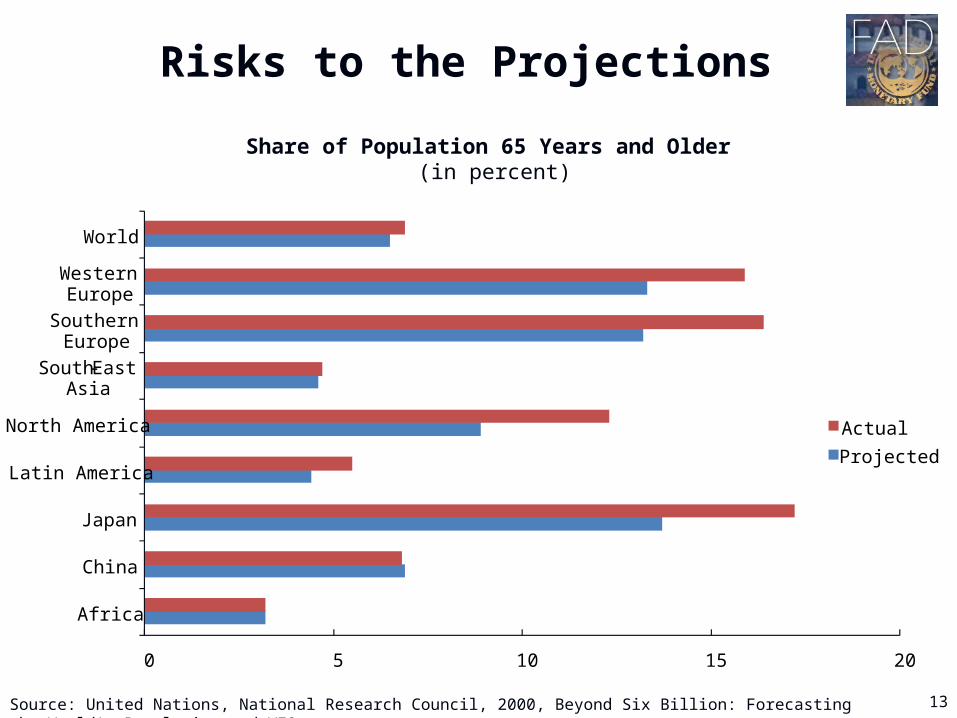

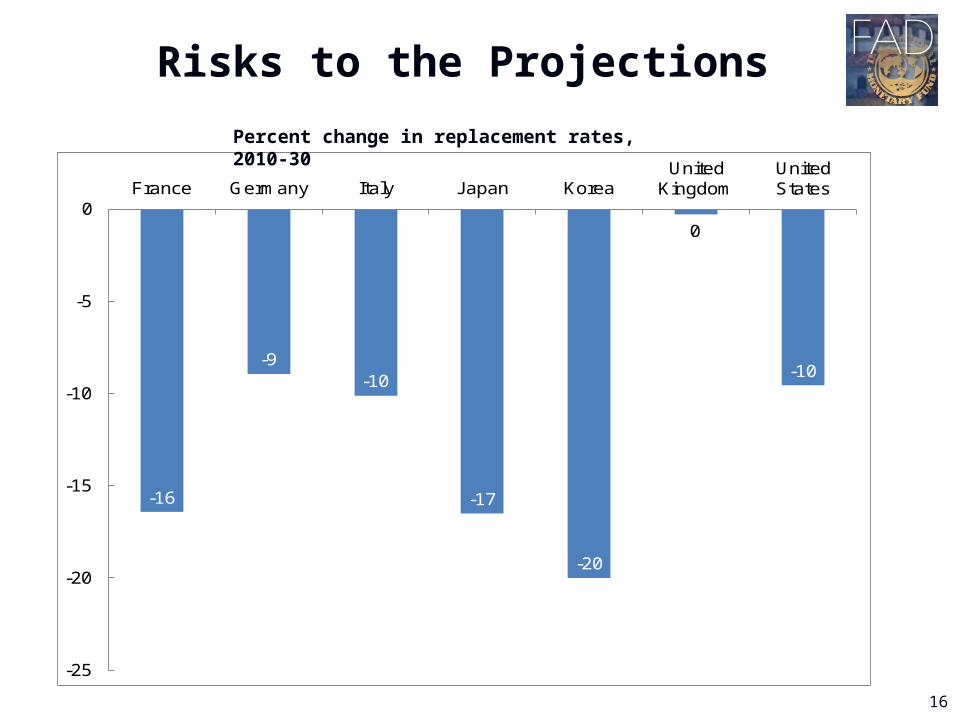

Risks to the Projections

13Source: United Nations, National Research Council, 2000, Beyond Six Billion: Forecasting the World's Population and WEO.

Share of Population 65 Years and Older (in percent)

0 5 10 15 20

Africa

China

Japan

Latin America

North America

South-East Asia

Southern Europe

Western Europe

World

Actual

Projected

Productivity Growth and Assumptions in Selected Countries (EU-27)

14

Average 2000-07=64.4 Average 2000-07=1.5

15

A Look at Output Levels

Advanced Economies Emerging Economies

Current WEO

Oct. 2007 WEO

Real GDP (In levels, 2000=100)

16

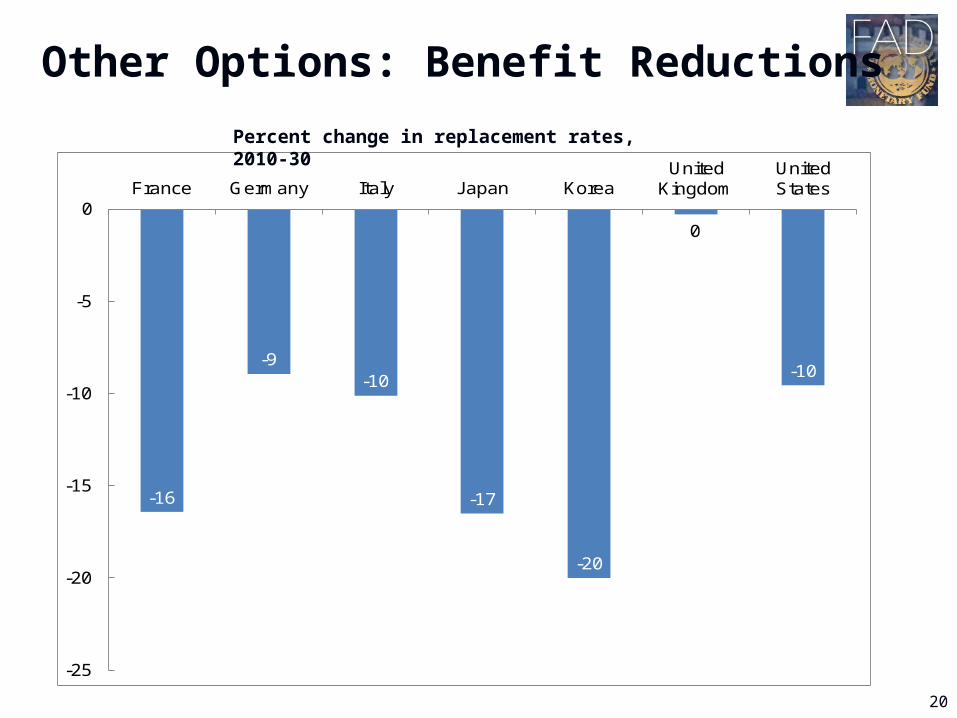

-16

-9-10

-17

-20

0

-10

-25

-20

-15

-10

-5

0France Germany Italy Japan Korea

United Kingdom

United States

Percent change in replacement rates, 2010-30

Risks to the Projections

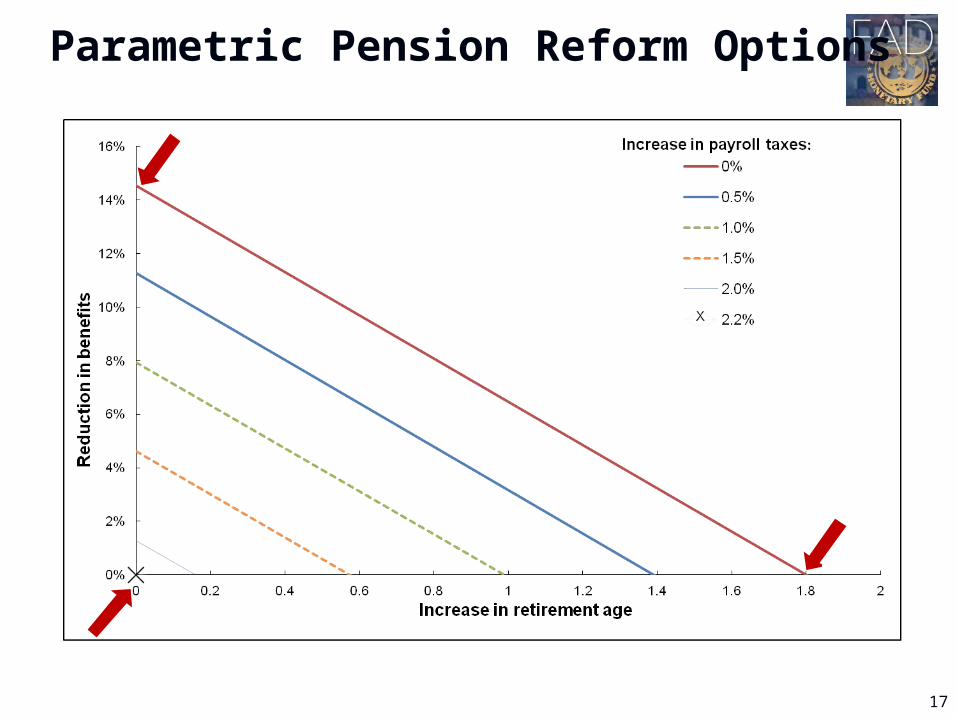

Parametric Pension Reform Options

17

18

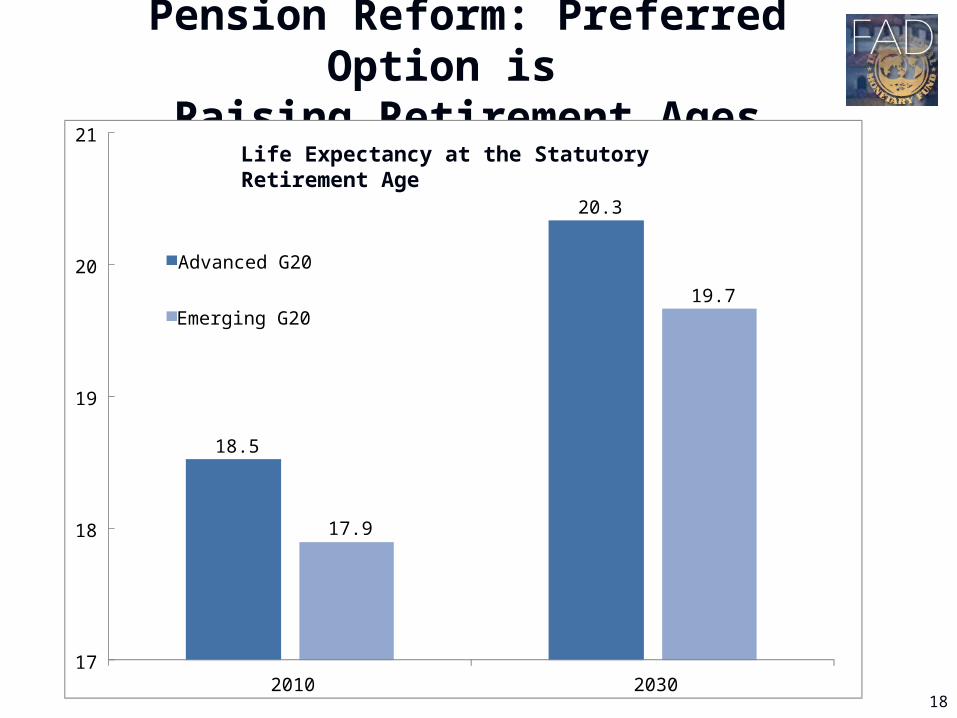

Pension Reform: Preferred Option is Raising Retirement Ages

18.5

20.3

17.9

19.7

17

18

19

20

21

2010 2030

Advanced G20

Emerging G20

Life Expectancy at the Statutory Retirement Age

19

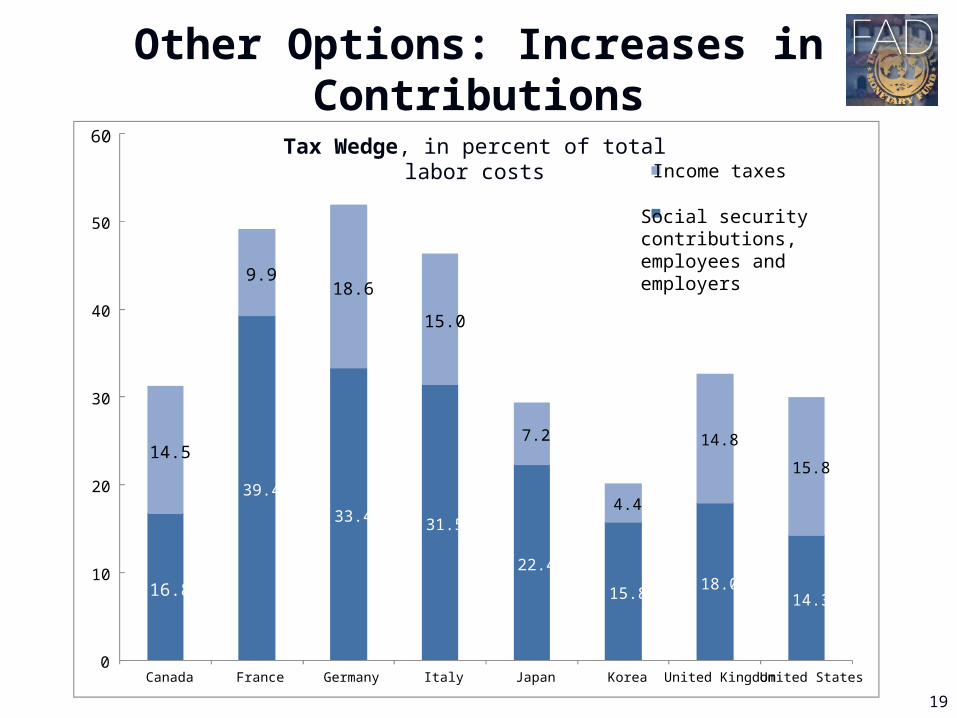

Other Options: Increases in Contributions

16.8

39.4

33.4 31.5

22.4

15.818.0

14.3

14.5

9.918.6

15.0

7.2

4.4

14.8

15.8

0

10

20

30

40

50

60

Canada France Germany Italy Japan Korea United Kingdom United States

Income taxes

Social security contributions, employees and employers

Tax Wedge, in percent of total labor costs

20

-16

-9-10

-17

-20

0

-10

-25

-20

-15

-10

-5

0France Germany Italy Japan Korea

United Kingdom

United States

Percent change in replacement rates, 2010-30

Other Options: Benefit Reductions

EU-5 Countries: Outlook for Fiscal Balance Versus 2006 Stability Program 1/

(In percent of GDP)

21

1/ Solid line refers to 2006 Stability Program.Dashed line refers to IMF, World Economic Outlook, April 2010 estimates and projections.EU-5 denotes simple average of France, Germany, Italy, Spain, and United Kingdom.

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

2005 2006 2007 2008 2009

22

0

20

40

60

80

100

120

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

Canada

0102030405060708090

100

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

France

0

10

20

30

40

50

60

70

80

90

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

Germany

0

20

40

60

80

100

120

140

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

Italy

0

50

100

150

200

250

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

Japan

0

50

100

150

200

250

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

United Kingdom

0

20

40

60

80

100

120

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

United States

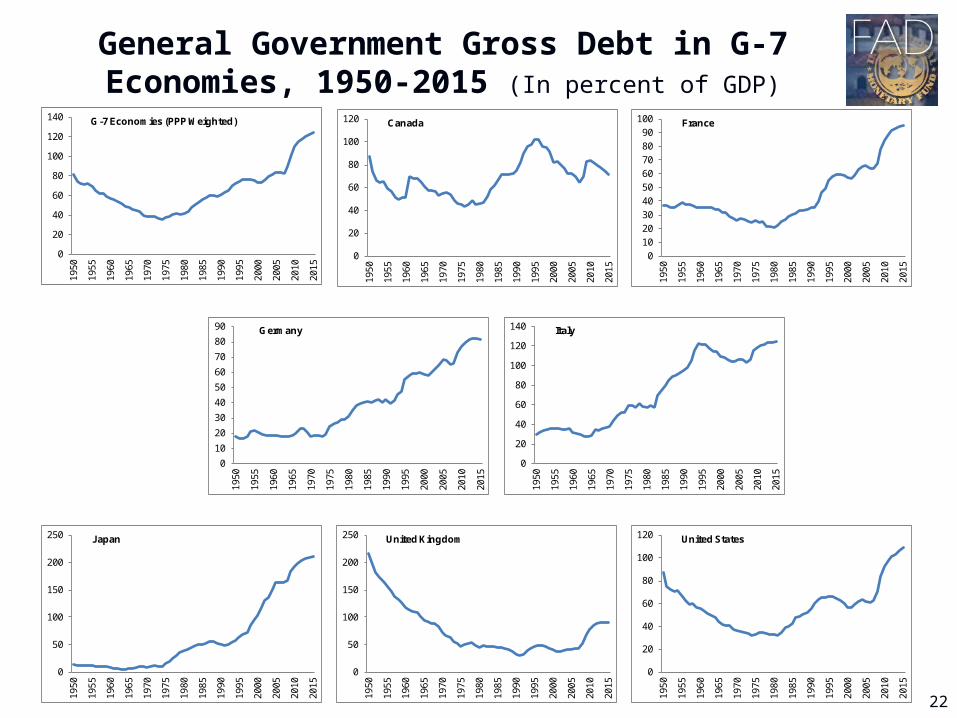

General Government Gross Debt in G-7 Economies, 1950-2015 (In percent of GDP)

0

20

40

60

80

100

120

140

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

G-7 Economies (PPP Weighted)

Thank You!