1. scope of synopsis - oecd.org · scope of synopsis. a. industry ... health insurance mutual...

TRANSCRIPT

INDUSTRY SYNOPSIS:

SIC 6325 – ACCIDENT, HEALTH, AND MEDICAL INSURANCE CARRIERS

1. SCOPE OF SYNOPSIS

A. INDUSTRY DEFINITION: For purposes of this study, SIC 6321 and SIC 6324 have been combined into SIC 6325, Accident, Health, and Medical Insurance Carriers. The 1987 Standard Industrial Classification Manual defines SIC 6321, Accident and Health Insurance, as establishments primarily engaged in underwriting accident and health insurance. Establishments that provide health insurance protection for disability income losses and medical expense coverage on an indemnity basis are also included in SIC 6321. Although there are few exceptions, most of the products included in this industry are considered to be non-comprehensive, indemnity products. Indemnity is defined as a benefit paid by an insurance company for an insured loss. In the case of a traditional indemnity health plan, this includes payment to the health care provider for each service rendered (fee-for-service), a maximum dollar amount of benefits provided (benefit ceiling), and a limited amount of covered services (non-comprehensive). These insurance providers may be owned by stockholders, policyholders, or other insurance carriers. Establishments included in this industry are the following:

Accident and Health Insurance Insurance Carriers, Accident Assessment Associations, Accident and Insurance Carriers, Health Health Insurance Mutual Accident Associations Disability Health Insurance Reciprocal Inter-insurance Exchanges Fraternal Accident and Health Insurance Accident and Health Insurance Organizations Reinsurance Carriers, Accident and Health Insurance, Indemnity Plans: Health except Medical Service Plans Sick Benefit Associations, Mutual

According to the SIC Manual, establishments primarily engaged in providing hospital, medical, and other health services in accordance with prearranged agreements or service plans are classified under SIC 6324, Hospital and Medical Service Plans. Medical Service Plans are defined as service plans that provide benefits to subscribers or members in return for specified subscription charges plus additional charges for services rendered, if applicable. Participating hospitals or physicians provide the covered services to members while charging minimal additional fees, in any. In some cases, the plans may include a partial indemnity and service benefits component. All fee-for-service medical service plans included in this industry are considered to be managed indemnity products. They are not pure indemnity products. In addition, they are all prepaid health plans (medical service plans). Also included in this industry are separate establishments of health

1 6325

maintenance organizations that provide medical insurance. Establishments classified in SIC 6324 include the following:

Dental Insurance (providing services Hospital and Medical Service Plans by contracts with health facilities) Medical Service Plans Group Hospitalization Plans

Basically, the distinction between SIC 6321 and SIC 6324 is the method of reimbursement. The two industries essentially produce the same product, coverage against a loss incurred as a result of accident or illness. The distinction is becoming more blurred as many commercial insurers in SIC 6321 have begun offering HMO or other similar managed care products that typically fall under SIC 6324. Thus, with the implementation of the North American Industrial Classification System (NAICS), the Accident and Health Insurance industry and the Hospital and Medical Service Plan industry will be combined into the Direct Health and Medical Insurance Carriers industry (NAICS 524114). Disability Income Insurance Carriers (NAICS 524113), Other Insurance Funds (NAICS 525190) and Reinsurance Carriers (NAICS 524130) will not be included in NAICS 524114. Therefore, the following types of establishments will most likely be included in this industry:

Accident and Health Insurance Group Hospitalization Plans Assessment Associations, Accident and Hospital and Medical Service Plans Health Insurance Insurance Carriers, Accident Dental Insurance (providing services by Insurance Carriers, Health by contracts with health facilities) Medical Service Plans Fraternal Accident and Health Insurance Mutual Accident Associations Organizations Sick Benefit Associations, Mutual

NAICS 524114, does not include HMO’s that provide services at their own facilities or through physicians employed directly by the HMO. Primary Output The primary output of SIC 6325 is risk protection and financial intermediation. Financial intermediation is the service of managing someone else’s money generally with the goal of increasing its value. In order to assume the risk against a premature death, life insurance companies charge a premium which is insufficient to cover claims payments. Therefore, companies invest their premiums using the interest income generated to offset their lower premium rates in order to pay a death benefit to the beneficiary upon the death of the policyholder. Classification of Establishments Individuals may purchase health insurance from commercial insurers (stock or mutual companies), government agencies, associations such as Blue Cross and Blue Shield, fraternal organizations, assessment associations, high-risk state pools, and some employers who self insure. The most common types of accident and health insurance companies are commercial companies, which include stock companies and mutual companies. A stock company is a corporation, which is owned by stockholders. Most stock companies provide non-participating policies. That is, policyholders are not affected by any profits or losses of the company. A mutual company is a corporation, but it has no stockholders. Instead, it is owned by the policyholders themselves. Tax-free dividends are paid to policyholders essentially as reimbursement for the overpayment of

2

premiums. Commercial insurers are beginning to offer group health insurance only, although individual plans are still available from most. Due to the rise of managed care, many commercial insurers have begun offering HMO and PPO plans in addition to the traditional fee-for-service indemnity type policy. The federal government provides health insurance to many individuals through Medicare, the Civilian Health and Medical Program of the Uniformed Services (CHAMPUS), and the Civilian Health and Medical Program of the Department of Veterans Affairs (CHAMPVA). All of these government sponsored health insurance plans that are not paid through a private insurance company are considered to be out of scope. Except for Medicare Part B, these programs provided by the federal government do not require monthly premium payments for those who qualify. Private fee-for-service plans (PFFS), and Medicare HMO’s and Medicaid HMO’s can replace traditional Medicare Part’s A & B and may sometimes require a small premium to be paid by the member as well. The federal government provides funding in order to assist the state governments in providing health care coverage for the poor. This program is called Medicaid. As with the majority of federal programs, premiums are not required by participants. However, some states allow people to buy into the Medicaid program. One example is the Arizona Medicaid program. The federal government insures approximately 74 million Americans through Medicare and Medicaid. This represents almost one third of the population of the United States. Medicaid and Medicare Parts A & B are considered to be out of scope as well. Blue Cross and Blue Shield, commonly referred to as “The Blue’s”, are currently non-profit community health service corporations that contract with hospitals, physicians, and other health care providers to provide prepaid health care to “subscribers.” Blue Cross and Blue Shield are separate companies that usually share office space and have joint enrollment and billing. Blue Cross began as a hospital insurance provider only. Blue Shield began as a medical service and surgical provider. Today, Blue Cross/Blue Shield offers comprehensive health care policies. There is a national Blue Cross and Blue Shield Association in Chicago that coordinates the sixty local Blue Cross plans and sixty-five Blue Shield plans. The majority of Blue Cross’ and Blue Shield’s subscribers are in group plans, although individual plans are available. Unlike traditional commercial insurers, the Blues traditionally offer service benefits and first dollar coverage. The insured pays monthly premiums and does not have to pay additional charges for most medical services covered by the plan. Today, many of the Blues’ companies offer HMO and PPO plans. Also, some Blues are attempting to become for profit companies and model commercial insurers. Blue Cross and Blue Shield plans collectively insure approximately 68 million people. This represents one fourth of the total population of the United States. Fraternal Organizations are incorporated societies, which are formed solely for the benefit of their members and their beneficiaries. In the past, many fraternal organizations offered health insurance to their members through a self-funded plan. Today, many organizations negotiate special rates for their members through commercial insurers or other health plans. In this case, the fraternal organization would not be considered the health insurance provider. Assessment companies offer insurance to members of a fraternal organization as well as the general public. Like mutual companies, assessment companies offer dividends to their policyholders. However, these companies may also charge an additional premium or assessment. Another source of health coverage is a high-risk state pool. As of 1997, seventeen states had a high-risk pool. These risk pools offer guaranteed availability of health insurance to all individuals

3 6325

regardless of their health. The pools are created for those who were denied health care coverage by commercial insurers due to a preexisting condition, those who have coverage at a high cost, or those who have coverage with severe limitations built into the policy. Although each state may have different rules governing its pool, the design of the pool is similar. In most cases, an association of all entities providing health insurance in the state, excluding large corporations that are self-insured, is created to offer insurance. One member of the association administers the plan under the guidelines for benefits, premiums, deductibles, and other matters as outlined in the state’s law. Residents that meet the eligibility requirements are able to purchase insurance from the plan. The states that currently have high risk pools are California, Colorado, Connecticut, Florida, Georgia, Illinois, Indiana, Iowa, Louisiana, Maine, Minnesota, Missouri, Montana, Nebraska, New Mexico, North Dakota, and Wyoming. Since these high-risk state pools are state subsidized, they are considered to be out of scope. Today, many corporations are providing health insurance benefits directly to their employees through a self-insured fund. Corporations providing insurance to their employees through this mechanism are not bound by the same regulation as commercial insurers and other providers. Self-insured plans are governed by ERISA (Employee Retirement Income Security Act). This type of insurance is out of scope for PPI but will be collected for CPI. However, the fees received by an insurance company for administering claims for these policies are in scope for PPI. Other SIC’s Possibly Confused with SIC’s 6321 and 6324 (NAIC 524114): SIC 6311 – Life Insurance Establishments primarily engaged in underwriting life insurance. Half of these establishments also provide health insurance. SIC 6331 –Fire, Marine, and Casualty Insurance (Property and Casualty Insurance) Establishments primarily engaged in underwriting fire, marine, and casualty insurance. SIC 6371 – Pensions, Health, and Welfare Funds Establishments primarily engaged in managing pension, retirement, health, and welfare funds. SIC 6399 – Insurance Carriers, Not Elsewhere Classified Establishments primarily engaged in underwriting insurance, not elsewhere classified, such as insuring bank deposits and shares in savings and loan associations.

**NOTE** Many health insurance companies provide life insurance and property and casualty insurance. Typically, there are separate departments with separate records for each service. Each department is to be considered a separate PMC.

B. CONTEXTUAL OVERVIEW

In 1992, total revenue of SIC 6321 was much lower than that of SIC 6324. Total revenue for SIC 6321 was $23 billion compared with $124 billion for SIC 6324. Revenues for both of these industries should increase as health care costs continue to rise and the population increases. In addition, the trend in federal legislation has been to require employers to offer policies providing

4

more coverage for longer periods of time, even after an employee is laid off. If legislation and medical inflation cause health insurance premiums to be so high that many more people will no longer be able to afford coverage, future revenue may decrease in this industry. Approximately 72% of households owned health insurance in 1998. Nearly 88% of all Americans had some form of coverage. As long as health care costs do not rise significantly, the number of those who own some form of health insurance coverage should continue to rise. HMO’s have enabled many to afford health insurance coverage by offering more coverage, less options, and containing health care costs in general. In fact, most of the growth in this industry will be fueled by HMO policies. The difference between managed care (HMO’s, PPO’s, etc.) and fee-for-service products will be discussed in Types of Services and Estimated Value of Output.

Currently, 80% of all Medicare recipients own supplemental or Medigap policies. As the population ages, more of these policies will be sold. In addition, more long-term care and disability policies will be sold. The following chart shows 1996 indemnity and managed care enrollment in the private, Medicaid and Medicare markets:

Indemnity & Managed Care Enrollment

55

112.5

34

419 13

020406080

100120

PrivateIndemnity

PrivateM anaged

Care

M edicareIndemnity

M edicareM anaged

Care

M edicaidIndemnity

M edicaidM anaged

Care

Type of Plan

Enro

llmen

t in

Mill

ions

This chart shows the difference between managed care and indemnity plan enrollment in the private and public sectors of the accident and health insurance industry. Sixty-eight percent of people enrolled in a private health plan, are members of a managed care plan. The remaining 32% own an indemnity plan. Conversely, 24% of people enrolled in either Medicare or Medicaid were enrolled in some type of managed care plan. Seventy-six percent of people enrolled in a government subsidized health plan were enrolled in an indemnity plan. The number of people enrolled in managed care plans has been steadily increasing in recent years. This number is expected to increase even more as more Medicare and Medicaid members make the transition from traditional indemnity to managed care plans. The anticipated growth in the managed care market will most likely be at the expense of the indemnity market. The federal government already pays a large portion of the total cost of individual health care in America. It should also be noted that 29%, or 70 million, of all Americans are enrolled in some type of federal government subsidized health insurance program, namely Medicare and Medicaid.

5 6325

As the population ages, this percentage and number is likely to increase. In addition, a severe recession may cause many more people to be eligible for Medicaid.

2. INDUSTRY OVERVIEW A. NUMBER OF ESTABLISHMENTS AND COMPANIES

According to the 1992 Census, there were 1,846 establishments in SIC 6325. The number of establishments has been steadily decreasing as mergers and acquisitions continue to occur in these industries. As competition increases, the need to be large enough to offer substantial cost savings to the consumer becomes more important. Approximately 96% of these companies were stock companies. The remaining establishments were mutual companies or non-profit corporations. In 1992, there were at least two companies domiciled in every state, including the District of Columbia.

B. SIZE AND TYPE OF PRODUCTION BY SIZE

The smaller health insurance companies generally solicit business in a very specific geographic area, near their respective headquarters. Larger companies tend to provide insurance nationwide or in multiple regions. However, the size of the company does not dictate the variety of health insurance products offered.

C. MAJOR SERVICE PROVIDERS AND CONCENTRATION RATIOS

The tables below provide a list of the top ten companies ranked by their assets for accident and health and medical service plan companies. In addition, the tables below give market share data.

ACCIDENT AND HEALTH INSURANCE Company Total Assets Market Share (in billions) 1. Prudential 219.3 9.0% 2. Lincoln National Corporation 119.1 5.0% 3. Cigna Corporation 108.2 5.0% 4. Connecticut General Life 108.0 5.0% 5. Northwestern Mutual Life 54.0 2.5% 6. Mass Mutual Life 53.3 2.5% 7. Principal Mutual 50.0 2.4% 9. Liberty Mutual 50.0 2.4% 10. Aetna 37.0 1.5% Source: The Information Access Company (IAC), 1997.

6

MEDICAL SERVICE PLANS

Company Total Assets Market Share (in billions) 1. Aetna 96.0 15.0% 2. Hartford Life 79.0 11.0% 3. Kaiser 11.0 3.0% 4. Group Health Coop of Puget Sound 5.8 1.5% 5. Pacificare 5.4 1.5% 6. Standard Insurance Company 4.1 1.3% 7. Foundation Health 4.0 1.3% 8. Wellpoint Health Networks 3.4 1.2% 9. Blue Cross/Blue Shield of MI 3.1 1.2% 10.Blue Cross/Blue Shield, FL 3.0 1.2% Source: Information Access Company, 1997 The following concentration ratios show the percentage of assets for the top 4, 8, 20, and 50 firms in each industry: Accident & Health Medical Service Plans Top 4 Firms 18% Top 4 Firms 15% Top 8 Firms 28% Top 8 Firms 22% Top 20 Firms 46% Top 20 Firms 41% Top 50 Firms 71% Top 50 Firms 65% Source: Information Access Company, 1997

D. STABILITY OF THE INDUSTRY

Health insurance is a growing industry. As long as the population continues to grow and age, there will be an increasing need for health, long-term care, and disability insurance. Health insurance especially, is considered to be a necessity. However, the number of uninsured increased from 1996 to 1997 and is expected to increase even more in the future. Today, 16.1%, or 40 million of all Americans are uninsured. This is equal to one in six Americans. In addition, 15% of American children are uninsured. The decrease in the number of people on Medicaid, medical inflation, and the increase in the percentage of workers working for small companies that do not offer health insurance are partly responsible for this increase. Medical inflation has been contained recently. However, it could cause major problems in the future if it becomes uncontrollable. Even if health care costs continue to rise, causing premiums to rise, the extra revenue collected from those insured will most likely exceed the loss of revenue from those who

7 6325

will no longer be able to afford coverage. Therefore, the outlook for revenue growth is still positive. Most small companies are able to compete with large companies through regional specialization. There are decreased costs associated with operating locally. In addition, many small firms exhibiting regional domination usually merge with or become acquired by a larger firm. Many of the companies formed more than fifty years ago are still in existence today.

E. GEOGRAPHIC DISPERSION

Geographic dispersion in these industries tends to be fairly even. However, the highest concentration of these companies tends to be in the South and Northeast. The geographic breakdown is given in the table below. REGION % OF COMPANIES West 18% South 29% Midwest 23% Northeast 27% Source: AM Best, 1996.

F. SAMPLE INFORMATION

The sample design was developed with an attempt to meet the needs of both PPI and CPI. For PPI we require a nationwide sample of companies sampled systematically with probability proportional to a measure of size. We also require that items be selected from these companies so that all of our product categories are publishable. The requirements from CPI include that all 87 of their primary sample units (PSU) are covered. The PSUs will be covered by sampling in the states in which the PSUs are located.

3. PRODUCTION INFORMATION

A. SERVICE DELIVERY PROCESS

The primary service of the health insurance industries, as in all insurance industries, is the protection from the risk of a potential loss as well as some degree of financial intermediation.. The main risk is the potential expense and/or income loss associated with either an accident or an illness. Policies included in SIC 6321 or SIC 6324 are promises to pay medical expenses and/or an income loss associated with an illness. In addition, a policy may cover an income loss resulting from a serious accident and subsequent disability. In order to provide this service, accident and health insurance companies are involved in rate determination, underwriting, marketing, and financial activities.

8

Rate Determination: Accident and health insurance policies are priced with the intention of covering all of the related costs associated with conducting business in addition to attaining a certain desired level of profit. Administrative and overhead costs are fairly easy to project. Claims costs are the most significant component of the premium rate. The costs associated with claims are directly related to health care costs in general. If hospital costs increase, claims costs will most likely increase. Thus, premiums will have to be increased in order to attain the same previous level of profit, provided everything else is constant. In addition, insurance companies are required to maintain a certain percentage of premiums as claims reserves. These reserves are used to fund claims, which are made at a later date. This cost is essentially a claims cost as well. Underwriting: Through underwriting, an insurer determines whether or not a potential client is a good risk. In addition, the rate a prospective client is ultimately charged is determined through underwriting. Basically, the underwriter uses various demographic statistics in order to determine the degree of risk and the premium rate. Age, gender, race, geographic location, occupation, marital status, and medical history are all examples of demographic statistics underwriters use to determine the degree of risk of a potential client. Less underwriting is needed for group policies than individual policies. The risk associated with an individual is greater than the risk associated with a group. Therefore, medical history is more likely to be a major consideration in the underwriting process for an individual versus a group. In fact, very little underwriting is necessary for large groups. For small groups, the medical histories and ages of potential group members may be more scrutinized during the underwriting process. Distribution: Since all forms of health insurance companies create similar products in the same way, it is important to mention how these products are distributed. Product distribution is a differentiating factor in the accident and health insurance industry. Agency System: Some agents operate independently, while others operated in company owned field offices. This is the main distribution method use by insurance companies to market their products. Long-term care, accident and disability products are most often sold through independent agents, whereas health insurance is most often sold through company employed field agents. Direct Response Distribution: Through this method, companies make their products available to consumers via television, magazine, telemarketing, and radio advertising. This method is not used very often. Financing: Insurance companies are involved in many investment activities. By investing in various types of high yield investments, insurance companies are able to avoid substantial premium costs and still be able to fund future claims costs and other expenses. However, this is less of a factor in the

9 6325

accident and health insurance industry than it is in the life insurance industry. The main reason being that accident and health insurance companies receive claims almost instantaneously whereas life insurance companies usually do not receive claims until many years after the policy is initiated. In addition, claims costs are the most significant portion of the premium rate in the accident and health insurance industry. Thus, accident and health insurance companies have less money to invest and less time in which to invest it.

B. TYPES OF SERVICES AND ESTIMATED VALUE OF OUTPUT

The health insurance industries provide coverage against a loss incurred as a result of an accident or illness. This coverage is provided through health and medical insurance plans. These insurance plans can take on many different forms. The following pages describe the major service lines of this combined industry. The table below shows the value of receipts for each major service line within SIC 6325 and the percentage of total industry revenue that each service line represents. In addition, primary and other services are presented.

Service Value of Shipments Percent (in 1000) Accident, Health, and Medical Insurance 148259000 100.00% Medical Service Plans 124813000 84.19% Group medical service plans 90400000 60.97% Managed care medical service plans 61200000 41.28% Fee-for-service medical service plans 29200000 19.70% Individual medical service plans 10300000 6.95% Dental service plans (stand alone) 9100000 6.14% Supplemental Medicare service plans 7650000 5.16% Other medical service plans 7363000 4.97% Accident and health insurance 19762400 13.33% Disability 9492856 6.40% Long term care 3279350 2.21% Hospital indemnity 3020454 2.04% Specified disease 1553376 1.04% Accidental death & dismemberment 1294480 0.87% Third-party administrative services 3683600 2.48%

MEDICAL SERVICE PLANS The primary types of medical service plans include managed care, fee-for-service dental, and supplemental Medicare policies. Dental and supplemental Medicare policies can be offered as fee-for-service or managed care products as well. Both fee-for-service and managed care medical service plans are comprehensive plans with unlimited benefits. The fee-for-service plans are “managed indemnity” products. These plans are comprehensive, have unlimited benefits and have some form of utilization review in order to contain costs.

10

It should be noted that group business accounts for a much larger percentage of total industry revenue than individual business. Group business represents 85% of total industry revenue. For both health insurance and dental insurance, 90% of all policies sold are group policies. However, only ten percent of supplemental Medicare policies are group policies. The table below lists the various types of managed care medical service plans available to the consumer. In addition, fee-for-service medical service plans and dental medical service plans sold separately are included in the table. This table will be discussed in the next few pages. The main distinction between a managed care and a fee-for-service product is the method of payment by the client. Clients that own a managed care product generally pay a premium to establish benefits and copayments when services are rendered. Clients that own a fee-for-service product pay a premium to establish benefits and deductibles and coinsurance when services are rendered. Providers are reimbursed differently under the two systems as well. Once again, those that own a managed care product typically have less choice with regard to providers than do those that own a fee-for-service product. By giving up a certain degree of choice, clients that own a managed care product typically pay lower premiums and pay less out of pocket expenses for similar services received. In general, the method of payment is similar for each managed care plan and the degree of choice is different. Any differences in the method of payment between the various managed care plans will be discussed in subsequent pages. The chart shows the typical method of payment and the fee-for-service or managed care designation for each health insurance product type. PRODUCT NAME COVERED SERVICES PAYMENT CHOICE ________________________________________________________________________________ FEE-FOR-SERVICE INPATIENT – HOSPITAL PREMIUM UNLIMITED SURGICAL DEDUCTIBLES MATERNITY COINSURANCE MENTAL HEALTH SUBSTANCE ABUSE PHARMACEUTICALS EMERGENCY LIMITED DENTAL AND VISION ________________________________________________________________________________ PPO SAME AS ABOVE PREMIUM HIGH MANAGED CARE DEDUCTIBLES COINSURANCE ________________________________________________________________________________ POS SAME AS ABOVE PREMIUM MEDIUM MANAGED CARE COPAYMENTS ________________________________________________________________________________ EPO SAME AS ABOVE PREMIUM LOW MANAGED CARE COPAYMENTS ________________________________________________________________________________ HMO SAME AS ABOVE PREMIUM LOW MANAGED CARE COPAYMENTS ________________________________________________________________________________ DENTAL PREVENTIVE PREMIUM UNLIMITED FEE-FOR-SERVICE DIAGNOSTIC DEDUCTIBLES PURCHASED RESTORATIVE COINSURANCE SEPARATELY EXTRACTIONS ________________________________________________________________________________ DENTAL (DHMO, DPPO) PREVENTIVE PREMIUM LOW - DHOM PURCHASED DIAGNOSTIC COPAYMENTS HIGH - DPPO SEPARATELY RESTORATIVE EXTRACTIONS

11 6325

**NOTE**

Comprehensive health insurance establishments can be organized as fee-for-service or managed care companies. However, the manner in which a company is organized does not limit the types of products it can provide. Many companies offer both fee-for-service and managed care products. Many of the larger companies offer all product types. It is important to note that PPO’s are generally the only managed care type whereby the insured pays deductibles and coinsurance for services received. There may be exceptions. Most PPO’s are offered by fee-for-service companies. Managed Care Medical Service Plans Unlike fee-for-service medical service plans, where the insured pays a premium, deductibles, and a percentage of the fees for services provided (coinsurance), managed care is generally a prepaid plan. The client pays a monthly or quarterly premium and small copayments when services are received. Managed care plans provide comprehensive health services to their members and offer financial incentives for patients who use plan providers. Office visits, hospital, surgical, emergency, maternity, mental health, substance abuse, dental, vision, and pharmaceutical benefits are all included in a comprehensive medical service plan. There are a variety of managed care plans that provide comprehensive medical coverage. The various managed care plans include health maintenance organizations (HMO’s), preferred provider organizations (PPO’s), point of service organizations (POS’s), and exclusive provider organizations (EPO’s). In both an HMO and an EPO, the client must receive care from plan providers. A plan member selects a primary care physician who coordinates the client’s care, including providing referrals to specialists and hospitals. PPO’s and POS organizations allow for reimbursement if care is provided from a provider outside of the plan network. When using a provider outside of the plan network, the level of reimbursement is lower than if a provider within the network is used. As for all insurance products, the choices available to the consumer with regard to health insurance are really part of a menu of options from which a consumer can choose the services, method of provision, and method of payment that most suits their needs. The health insurance product types differ in three aspects: degree of choice, premium amount, and method of payment as services are rendered. It is evident from the table on the previous page that the HMO product type offers the customer a low degree of choice. However, fees for services received are generally lower for managed care plans versus fee-for-service plans. In addition, the premiums paid for an HMO product are typically the lowest of all health insurance plans. The EPO is the PPO’s answer to the HMO. This product type offers a low degree of choice and a low premium. The POS product type offers slightly more choice for a slightly higher premium. Non-affiliated providers may be used, but the customer is generally reimbursed less for these services than if they use an affiliated provider. The PPO product type offers the most choice of any managed care product type. It is generally the most expensive as well. In general, fee-for-service plans offer the most choice for the highest premium price. In general, fees for surgery and check up’s are more expensive with this plan type than for any of the managed care product types.

12

In general, HMO’s are the least expensive and require the least out of pocket expense for most types of medical care. Of course, the premium amount will depend on the company and the plan selected. HMO’s are able to offer increased benefits at a lower cost by using utilization review to limit customer choice and the performance of unnecessary medical procedures. Patients choose a primary care physician from a list of approved physicians provided by the insurance company. This primary care physician acts as a “gatekeeper”. He or she decides which specialists will be seen, if at all. Physician decisions are then reviewed by the insurance company. In addition, specialists must be part of the HMO system, limiting choice even further. Should a customer use a non-affiliated provider or hospital, he or she must pay the entire cost. If an affiliated provider is used, the client generally pays a small copayment. This copayment generally ranges from $5 to $10 for office visits and pharmaceuticals, and $50 to $100 for surgery and emergency care. There are no deductibles for this type of plan nor coinsurance should affiliated providers be used. Major procedures, such as surgery, must be approved by the insurance company as well as the primary care physician. This extensive review procedure helps to contain costs. In most cases, premiums are less for HMO’s than all other health insurance product types, especially fee for service. Again, the total price of an HMO plan is dependent upon the company, and its ability to contain costs. In addition, premium amounts depend on the profit goals of a particular company. EPO’s are very similar to HMO’s. However, the premiums are generally slightly more expensive. This is because EPO’s are generally offered by PPO’s in order to compete with HMO products. Utilization review is not as extensive for this product type as it is for HMO’s. Should a customer use a non-affiliated provider or hospital, he or she must pay the entire cost. If an affiliated provider is used, the client generally pays a small co-payment. This copayment generally ranges from $5 to $10. EPO’s are the least popular managed care product type. POS plans offer still more choice for a slightly higher premium. Customers may use non-affiliated providers and generally pay slightly more than if they use an affiliated provider. Copayments are made for office visits and other medical procedures should an affiliated provider be used. Should a non-affiliated provider be used, coinsurance rates will apply. However, customers are generally not responsible to pay the full amount, as is the case with an HMO or EPO. The preferred provider organization is similar to an HMO in terms of structure. PPO’s are panels of physicians, hospitals, dentists, and other providers who negotiate with employers, insurance companies, or other organizations in order to provide services at reduced fees to members of a specified group. PPO’s may be group practices, individual providers, or facilities that offer a range of services or a limited set of services. Customers have the most choice and pay higher premiums than any other managed care product type if they are enrolled in a PPO. This type of product is a combination of a fee-for-service and a managed care product. Small deductibles must be met for some services before benefits are received. Once deductibles are met, the insurer pays a certain percentage and the customer pays a percentage (coinsurance). Coinsurance rates are generally less for a PPO than for a fee-for-service product. Customers may use non-affiliated providers at a similar cost, but are generally rewarded if they use affiliated providers.

13 6325

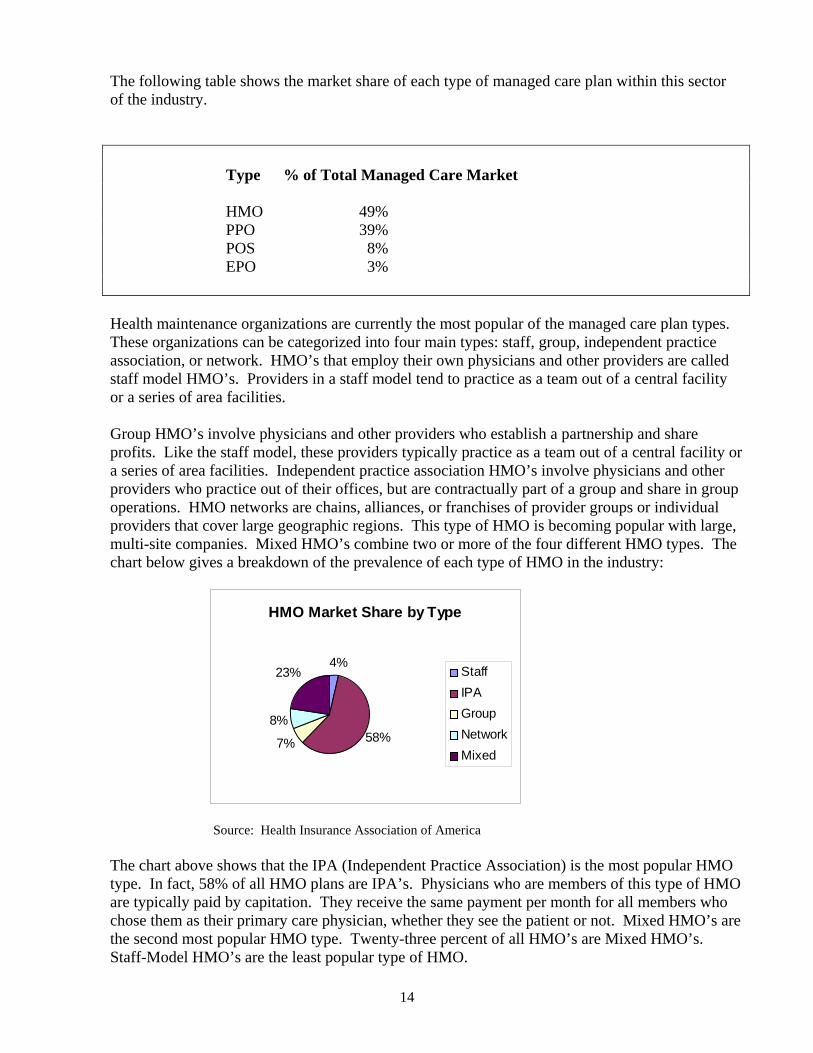

The following table shows the market share of each type of managed care plan within this sector of the industry. Type % of Total Managed Care Market HMO 49% PPO 39% POS 8% EPO 3% Health maintenance organizations are currently the most popular of the managed care plan types. These organizations can be categorized into four main types: staff, group, independent practice association, or network. HMO’s that employ their own physicians and other providers are called staff model HMO’s. Providers in a staff model tend to practice as a team out of a central facility or a series of area facilities. Group HMO’s involve physicians and other providers who establish a partnership and share profits. Like the staff model, these providers typically practice as a team out of a central facility or a series of area facilities. Independent practice association HMO’s involve physicians and other providers who practice out of their offices, but are contractually part of a group and share in group operations. HMO networks are chains, alliances, or franchises of provider groups or individual providers that cover large geographic regions. This type of HMO is becoming popular with large, multi-site companies. Mixed HMO’s combine two or more of the four different HMO types. The chart below gives a breakdown of the prevalence of each type of HMO in the industry:

HMO Market Share by Type

4%

58%7%

8%

23% StaffIPAGroupNetworkMixed

Source: Health Insurance Association of America

are t of all HMO’s are Mixed HMO’s.

taff-Model HMO’s are the least popular type of HMO.

The chart above shows that the IPA (Independent Practice Association) is the most popular HMO type. In fact, 58% of all HMO plans are IPA’s. Physicians who are members of this type of HMOare typically paid by capitation. They receive the same payment per month for all members who chose them as their primary care physician, whether they see the patient or not. Mixed HMO’sthe second most popular HMO type. Twenty-three percenS

14

HMO policies can be purchased through companies, unions, commercial insurers, Blue Cross anBlue Shield, associations, hospitals, medical centers, and other health organizations. Some are non-profit and others are for-profit. Like commercial insurers, most regulation is handled bystates, although applicable federal HMO laws and regulations exist. An example of federal legislation is the Health Maintenance Organ

d

the

ization Act of 1973. This act provides the minimum tandards for “federally qualified” HMO’s.

ee-for-Service Medical Service Plans

d coinsurance and some sort of utilization review takes place in order to ttempt to contain costs.

he

g r procedures which are not deemed medically necessary by the provider and the company.

ce

f

rse s”

review and the insurance company is not involved in the provision of health care

ervices.

ental Service Plans

ely

s F Fee-for-service plans offer unlimited choice, but higher deductibles and coinsurance than a PPO product. In addition, premiums for fee-for-service plans are generally the highest of any health insurance product type. Fee-for-service medical service plans can also be considered “managed indemnity plans”. Providers are reimbursed on a discounted fee-for-service basis, the insured pays a premium, deductibles ana A fee-for-service plan pays a medical provider a discounted fee for each service rendered. This serves to reduce the costs of the insurer. Insurers are able to pass some of these savings on to tconsumer based on contractual agreements between the insurance company and a provider or group of providers. Providers receive a guaranteed volume of business. Insurance companies receive lower costs and the ability to employ utilization review in order to determine whether a procedure is “medically necessary” or not. Fee-for-service insurers generally reimburse nothinfo Fee-for-service medical service plan products are also comprehensive health insurance plans. Under this type of plan, the client selects any medical service provider and the medical serviprovider submits a claim to the insurance company. In general, this type of policy does not reimburse one hundred percent of the claim. The level of reimbursement depends on the terms othe policy with regard to deductibles and coinsurance. Typically, the higher the deductible, the lower the premiums will be. These policies also have an annual, out-of -pocket maximum and a lifetime ceiling on benefits provided. Even though fee-for-service plans have a “lifetime” ceiling on benefits provided, they are not traditional indemnity plans. Indemnity plans do not reimbuthe service provider on a discounted fee-for-service base. They are “compensation for lospolicies meaning they pay the exact cost for services provided. These plans assign a low maximum dollar amount to benefits provided, are usually not comprehensive, do not employutilizations D Dental insurance can be purchased as part of a managed care or fee-for-service product, separatas a dental managed care product, or as a dental fee-for-service product. There are two dental managed care product types, the DHMO and the DPPO. The DHMO is very similar to an HMO and the DPPO is very similar to a PPO with regard to structure, method of payment, and provider reimbursement. Most of the revenue for dental insurance products sold separately is from the two managed care product types, approximately 90%. In addition, most dental insurance sold separately is group business, approximately 90%. Thus, experience rating is used based on groups

15 6325

of similar size, in a similar industry and a similar geographic region of the country. Only 10% ofdental insurance sold separately is purchased by individuals. Rating criteria for dental insurance sold separately is less detailed and stringent than rating criteria for health insurance plabenefits include check-up’s and x-ray’s (diagnostic), cleanings (preventative), fillings (restorative), extractions and anesthesia (oral surgery), gum treatment (periodontics), braces (orthodontics), crowns, dentures and bridges (prothodontics), and root canals (endodontics). The same dental benefits are usually offered when dental insurance is included with a fee-for-servior manag

ns. Typical

ce ed care, medical service plan product. However, the degree of benefits will vary of

ourse.

upplemental Medicare Medical Service Plans

.

private duty st

s

made ls the gaps”

ifferently. Medigap plans can be fee-for- service or managed care plans.

roduct.

entucky, Minnesota, Missouri, North Dakota, Ohio, Texas, Washington and Wisconsin.

**NOTE**

ed

government purchases coverage from a private surance company, this service is in scope.

benefits through enrollment in ne of an array of private health plans that contract with HCFA.

e

c S This type of policy is private insurance. Medicare was never designed to be an all-inclusive health care plan. Currently, Medicare has very high deductibles and does not cover many itemsMedicare does not cover skilled nursing facilities beyond one hundred days per benefit period, skilled nursing facilities not approved by Medicare, out of hospital prescription drugs,nursing, care received outside the United States, routine check-ups, dental care, moimmunizations, cosmetic surgery, routine foot care, eyeglasses, and hearing aids. Medigap. Since Medicare is so limited, 80% of seniors currently own Medigap policies. The Medicare Part B premium must be paid in order to purchase a Medigap policy. Medigap policiemust cover certain gaps in Medicare. In addition, Medigap insurance may cover certain things, which Medicare does not cover at all. There are 10 standard plans available, designated by the letters A through J. All ten plans may not be available in every state, but Plan A must beavailable to all Medicare recipients. Each plan covers different things or “fild Medicare Select. This is a Medigap insurance product that may be available in designated states through either HMOs or insurance companies. It is essentially a managed care, Medigap pThe states where these policies are currently authorized to be sold are Alabama, Arizona, California, Florida, Indiana, K

Medigap policies, including Medicare Select, are the only Medicare policies that are considerto be in-scope for this industry. All other types of Medicare policies are either completely orpartially subsidized by the federal government. Insurance coverage provided by the federal government is out-of-scope. However, if the in Medicare Plus Choice. This is a HCFA (Health Care Financing Administration) program through which eligible individuals may elect to receive Medicareo Traditional Medicare includes Medicare Parts A & B. In addition, seniors may purchase privatfee-for-service insurance, managed care coverage, or a Medicare medical savings account. In order for the Medicare beneficiary to be eligible to choose one of these alternative plan types, heor she must first be enrolled in Medicare Part’s A & B and pay the Medicare Part B premium..

16

The managed care company is paid a set monthly amount per member should the managed careoption be chosen. Seniors can choose between HMO, PPO, or POS coverage. In addition, the Medicare member may pay a premium to the managed care company. A Medicare memberchoose private fee-for-service insurance instead of the traditional Medicare Part A (fee-for-service) option. Under this arrangement, Medicare will pay the plan premium for Medicare covered services. The insurance company may charge the Medicare member a premium as wMedicare medical savings accounts (MSA’s) are functionally similar to traditional MSA’s. Medicare will pay the premium of a high-deductible, medical expense plan and deposit some money into a savings account. The Medicare beneficiary can use the money deposited into thiaccount to pay for routine medical expenses or deductibles. The medical expense policy will cover catastrophic illnesses or accidents. The tabl

may

ell.

s

e below clarifies which Medicare policies are ublic, private, fee-for-service, or managed care.

PUB C PRIVAT FEE-FOR RVICE MANAGED CARE PREMIUM

p

LI E -SEMEDICARE PART A X X N/A MEDICARE PART B $4 ) X X 5.50 (1999MEDICARECHOICE

PLUS X X X X VARIES

MEDIGAP X X X VARIES

Other Medical Service Plans

are,

may

n the

ally the only o characteristics needed in order for an insurer to provide a price for these policies.

.

ctually the insurer. If the employer is acting as the insurer, these services are out of scope.

. Prescription Drug Plan: Most health insurance plans, either fee-for-service or managed cprovide benefits for prescription drugs. Some stand-alone dental plans offer coverage for prescription drugs as well. However, the benefits these plans provide for prescription drugs be limited. Stand alone prescription drug plans are supplemental plans that usually provide benefits after a deductible is met. Once the deductible is met, a small copayment is required for each prescription. The copayment for brand name prescriptions is usually slightly higher thacopayment for generics. In addition, there is usually a maximum amount of yearly benefits provided. The age of the insured and number of people included in the policy are usutw Vision Expense Insurance: This type of policy provides reimbursement for routine eye examinations, eyeglass lenses, contact lenses, and the purchase and fitting of frames. Vision carepolicies are usually integrated into a major medical plan or are part of an employer, self-insured plan. Vision services included with a fee-for-service or managed care health insurance plan areusually very minimal. One eye exam and lenses may be covered. Frames are rarely coveredEmployers typically offer this as a benefit to their employees. In this case, the employer is a

17 6325

ACCIDENT AND HEALTH INSURANCE

Accident and health insurance policies include disability, long-term care, hospital indemnity, specified disease, and acciden

tal death and dismemberment. With the exception of disability surance and credit health, all accident and health products are indemnity products. In addition,

e and they have a lifetime ceiling on the dollar mount of benefits provided.

or those

ability insurance generally provides come replacement should an accident or illness cause the insured to be unable to work for a

ribes g n these two service

inthese insurance products are not comprehensiva Disability and Long-Term Care Insurance Disability and long-term care insurance products are similar in that they provide benefits in the case of an accident or illness, which leaves the insured disabled either temporarily or permanently. However, long-term care insurance provides nursing home or home health care coverage fwho are disabled and generally over age 65. Long-term care insurance generally provides benefits for supportive functions that provide assistance with daily activities in order to minimize, rehabilitate, or compensate for loss of functioning due to disability. In addition, disabled individuals do not always require long-term care services. Disinprolonged period of time. The table below desc eneral services included ilines, services they are likely to cover, and payment methods. PRODUCT SERVICES PROVIDED METHOD OF PAYMENT ____________________________________________________________________________ SHORT-TERM INCOME REPLACEMENT PREMIUM DISABILITY SIX MONTHS TO TWO YEARS __________________________________________ _ ____________________ ______ _______ LONG-TERM INCOME REPLACEMENT PREMIUM D FIVE YEARS UP TO IND N ISABILITY EFI ITELY___________________ _________ ______ ________________________ _ ________________LONG-TERM CARE NURSING HOME CARE PREMIUM RESIDENTIAL COMMUNITY CARE DEDUCTIBLES HOME HEALTH CARE COINSURANCE

s, until age 65, or

indefinitely. Benefits typically expire at age 65. Maternity insurance is not sold separately, but

rt-

t

Disability Insurance: This type of insurance provides partial income replacement in case the insured is unable to work as a result of an accident or illness. The insured receives benefits aslong as the accident or illness is not covered by workers’ compensation. Short-term disability insurance generally pays benefits up to twenty-six weeks, but can provide benefits as long as twoyears. Long-term disability insurance pays benefits for five years, ten year

may be included with the benefits of a long-term disability insurance product. The benefits are usually short-term unless complications arise as a result of the pregnancy.

There are five different types of disability income insurance that can be purchased as either shoterm or long-term coverage. These include general DI (disability income), DI-loss of earnings, DI-overhead expense, DI-buyout, and DI-key person. The first two have to do with the coverage for individuals. The last three have to do with coverage for businesses. DI-overhead expense provides benefits for all overhead expenses, including salaries of and benefits to all employees thaare not owners, should the principal owner of the business become disabled. DI-buyout provides

18

a lump-sum benefit should the insured become disabled. The insurance company agrees to buy the insured’s share of the business for a predetermined amount. DI-key person provides benefits

the owner of a company should a key person of the firm become disabled. Benefits are paid to

lude

benefit. Typically businesses can only purchase the additional purchase benefit. However, they may ometimes purchase a future increase benefit. The options available to businesses depend on the

cribes t

tothe business until a replacement in found. If a replacement is found during the benefit period, a replacement benefit will be paid to the owner of the company. Several riders or additional services can be purchased as part of a disability policy. These incadditional purchase benefit, waiver of premium benefit, rehabilitation benefit, deferred disability benefit, future increase benefit, indexed income benefit, and a social security substitute

scompany. The table below des he additional benefits available to individuals.

Additional Purchase Benefit . Additional coverage can be purchased as income increases Waiver of Premium Benefit If the disability lasts longer than a certain period of time,

the premium may be waived until the disability no longer exists.

Rehabilitation Benefit Rehabilitative therapy is included. Deferred Disability Benefit Provides retirement benefits. Future Increase Benefit The maximum benefit amount is increased to account for

inflation. Benefits are usually indexed to the CPI. Indexed Income Benefit After twelve months of disability, the benefit is indexed to

account for inflation. Social Security Substitute Increases the benefit at age 65 if benefits are not available from Social Security or a state plan. Long-Term Care: This type of insurance covers medical care, nursing care, and other assistanceon a fee-for-service basis in the event that the person insured is unable to care for themselvesan extended period of time. Services covered under this type of policy are not typically covered under other health insurance policies. Usually, these policies pay a fixed dollar amount for each day care is received. Many of these policies have an inflation adjustment feature in order to

for

rovide adequate coverage in the future. Thirty- percent of long-term care policies are owned by dividuals who belong to a group plan. Seventy-percent of long-term care policies are owned by dividuals. The table below describes possible services covered by long-term care policies.

pinin

19 6325

Nursing Home Daily maximum between $50 and $200 B Reserves a bed in a nursing home in the caseed Reservation of a temporary

hospitalization. Benefits up to the daily maximum amount are usually paid. In addition, benefits

are paid up to a maximum number of days. Alternate Facility Includes care given in an assisted living facility or Alzheimer’s care facility. Usually pays a percentage of the daily nursing home maximum. Home Health Care Includes care given at home or at Adult Day Care Centers. A percentage

of the daily nursing home maximum is usually paid. Respite care is also included. This gives the informal care-giver a break from providing care. Benefits are provided on a twenty four hour basis for a maximum number of days.

t

payment is made directly to the client who can use the money any ay they choose. The client must be hospitalized for a certain number of days before the policy

up .

it of a basic medical policy is low. This is a fee-for-service product. These policies ay include a maximum lifetime benefit of a high dollar amount. Supplemental medical expense

ccidental Death and Dismemberment Insurance: This form of health and accident insurance of

ccident Insurance: This is a type of insurance insures against a loss caused by accidental purchased in order to compensate the beneficiary

r a loss incurred as a result of work related travel.

e installment loan. This type of insurance can be purchased to cover a credit card loan, car loan,

Hospital Indemnity: This type of insurance policy provides a per diem cash benefit to the clienfor each day he/she is hospitalized. There is usually a maximum number of days for which benefits are provided. The cashwwill be paid. Hospital/surgical policies include surgery benefits, should surgery be performed during a hospital stay, as well. Major Medical Expense: Insurance that provides benefits for most types of medical expenses to a high maximum benefit. Such contracts are normally subject to deductibles and coinsuranceThis type of policy provides hospital and medical expenses above a certain deductible. This type of policy is selected as a safeguard to cover the costs of a catastrophic illness when the lifetime benefit limmpolicies may be purchased to supplement a hospital indemnity or MSA (medical savings account) product. Aprovides payment to an insured’s beneficiary in the event of death or the insured in the event specific bodily losses resulting from an accident. Abodily injury. This type of insurance is usually fo Other Accident and Health Insurance Plans Credit Health: This type of insurance will pay a particular installment loan for an individual should the individual be too sick or injured to work. The premium is paid monthly and added to th

20

or an installment home equity loan. Coverage only applies to the loan for which credit health insurance is owned. A separate policy for each loan must be owned in order for coverage to apply Medical Savings Account (MSA): This instrument was created by Congress in the summer of 1996. An MSA is an individual savings account, which is used to cover office visits and generalhealth care expenses. These accounts provide tax-free savings, tax-free payment of medical bills,and tax-free use of savings for any reason after the age of 65. Currently, this type of plan iavailable to the self-employed and small businesses with less than 50 employees. Congress has limited the number of MSA’s that can be sold through the year 2000 to 750,0

.

s only

00. In conjunction ith an MSA, one must also have a high deductible, fee-for-service, catastrophic medical surance product. The catastrophic medical policy will cover medical expenses above a certain

deductible. The savings port ible.

tain price per member in order to receive this service. Since this type of lan is really a contract to administer the claims process for a company or organization, it is

s a

, known as the remium equivalent, paid to the employer providing the policy influences the price for these

sold rance and medical service plans.

er ts

ith an insurance company to pay claims if claims in a given period should exceed 100% of the

a

m

e for should they exceed 90% of the expected claims. This

service is very similar to a Stop/Loss contract and is typically sold in conjunction with an ASO or many different types of accident and health

insurance and medical service plans.

win

ion of an MSA is used to cover the deduct

3RD PARTY ADMINISTRATIVE SERVICES Administrative Services Only Contracts (ASO): This is a contract whereby the insurance company agrees to administer the claims process for a self insured, employer health plan. The client agrees to pay a cerpneither a fee-for-service, nor a managed care product. ASO contracts account for $4.5 billion of total industry revenue. Insurers typically determine the price based on the total number of members in the group or apercentage of total average or anticipated claims. The insurer may also look at the average number of claims per member in order to provide a price. In addition, the premiumpcontracts. The price is usually quoted as a price per member per month. ASO contracts arefor virtually all types of accident and health insu Special procedures for collecting this type of service are presented in Types of Prices and Industry Specific Questions and Procedures. Stop/Loss Contracts: This type of insurance policy is for self-insured employers, (an employthat both administers and pays claims against large fluctuations in claims). An employer contracwexpected claims. Stop/Loss contracts are sold for many different types of accident and health insurance and medical service plans and are very often sold in conjunction with ASO contracts. Minimum Premium Plan (MPP): An arrangement under which an insurance carrier will, forfee, handle the administration of claims and insure against large claims for a self- insured group. Under this type of plan, the insurance company will receive a certain percentage of the premiuand pay claims should they reach a certain level, less than 100% of the expected claims. For example, an insurance company may agree to receive ten percent of the premium in exchangthe guarantee that they will pay claims

contract. Minimum premium plans are sold f

21 6325

C. PRICE DETERMINING CHARACTERISTICS

is typically set for policies purchased by companies located in several regions or ationwide. The guidelines for receiving a national rate can vary amongst insurance companies.

ies purchased by companies with fewer locations. This rate will be ased on the region, state, or city in which the policyholder is located.

f y

ilar groups in similar dustries. Basically, an average claims cost per individual is determined for similar groups and

tal number of individuals in the group. All other costs and desired profit argins are then added in order to determine the final rate for the group.

nderwriting small group olicies. Thus, the underwriter may use the claims experience of similar groups in the same

nce again, large group policies generally require minimal underwriting. The list below presents

mount of Coverage (Richness of Benefits): The number of covered services, the dollar amount of

ensus class: Prices for the same service within the same group will differ according to the rate or

he

whereby e employer pays 100% of the premium. The percentage contribution of the employer or the

All policies Rates for insurance policies are set on either national or regional (region, state, or city) basis. A national ratenThis rate is generally the same for all employees within the same rate (or census) class regardless of location. A regional rate is set for policb Large Group Policies: Large groups usually require minimal underwriting. Groups are typically considered to be large ithey have more than 300 members. However, the distinction between small and large will vary bcompany. In general, experience rating is used in order to determine a rate for these groups. These groups are rated based on the company’s claims experience with siminthen multiplied by the tom Small Group Policies: A combination of experience rating and individual rating is used in upindustry and consider the demographic and health characteristics of every individual in the group. These are the most difficult policies for which to determine a price. Oall possible price-determining characteristics used by underwriters when determining a price for either a large or small group policy: Type of Coverage: Underwriters will require different information in order to provide prices for medical service plans, disability, long-term care and other services. Acoverage for each service, and the maximum dollar amount of coverage will all influence the policy price. Ccensus class. Generally, families will pay a higher premium than an individual within the same group plan. Voluntary vs. Non-Voluntary (Contributory vs. Non-Contributory) For our purposes, voluntary(contributory) group policies will be defined as policies for which the employee pays 100% of tpremium. Non-voluntary (non-contributory) group policies will be defined as policies th

22

employee can vary anywhere between 0.0 and 100.0%. The total will always sum to 100.Utilization tends to increase as the percentage contribution of the employee increases.

0%.

roup composition: The combination of gender and age ranges is an important factor in

and children.

ccupation: People employed in dangerous occupations will generally pay more than those in

The zip code sually the first three digits) is used for underwriting purposes. For large groups, or small groups

arnings: As incomes rise, utilization rates tend to increase. Thus, premiums tend to increase as ice for disability

surance. Maximum benefits paid are usually based on income.

tus: Smokers generally pay higher premiums than non-smokers.

ype of Company: Premiums of mutual companies are generally less than those of stock

ividual policies is usually the most stringent. This may include health screening, in addition to analyzing the individual price determining characteristics listed above for

. Again, individual policies (non-group) represent approximately 10% of total industry revenue.

D. CU

payment is the primary

rm of customization in this industry. Clients can be given different payment options including ayment of the entire annual premium in advance as well as quarterly or monthly payments. An centive may be offered for payment of the annual premium in advance.

Gdetermining the premium. Therefore, companies require the age and gender of each person covered by the policy, including spouses Medical History: Previously healthy people will generally pay lower premiums than those who have a record of health care utilization. Osedentary, low risk occupations. The SIC code of the industry is usually used for underwritingpurposes. Geographic Location: People who live in areas in which natural disasters often occur and/or pollution is a problem will generally pay higher premiums than those who do not. (uwhich are geographically dispersed, several zip codes/geographic regions may apply. However, a national rate may be used if a group is very well dispersed throughout the nation. Eincome increases as well. Earnings will be most important in determining a prin Smoking Sta Tcompanies. Individual Policies: The number of rating structures and the complexity with which individuals are rated vary from company to company within the industry. Since the risk of underwriting one individual is so great, rating for ind

small group policies

STOM SERVICES

Among individual policies, products are generally standard industry wide. However, many grouppolicies can be tailored in order to satisfy customer needs. The method of fopin

23 6325

E. SEASONALITY

Health and medical insurance services are not seasonal. F. SE

The only foreseen need to substitute would be to replace an actual policy that is no longer in force or to replace

4. MARKET AND TRANSACTION INFORMATION A. IN

stry for either SIC 6324 or SIC 6321 is unknown. However, the

ercentage is likely quite small. Reinsurance will not be included with one of these two industries aptured in the collection of the SIC 6311 – Life Insurance or SIC 6331 –

Property and Casualty Insurance.

B. PR

crease in

lation, eneral inflation, an increase in AIDS related diseases, and the performance of unnecessary edical procedures have all contributed to the rapid rise in health care costs. Today, national

lth care expenditures represent nearly 14% of the nation’s Gross Domestic Product.

RVICE SUBSTITUTION

a policy that is no longer sold by the company.

TERPLANT AND INTRAINDUSTRY SALES

Reinsurance is the only known form of intraindustry sale in the accident and health insurance industry. Reinsurance is the practice whereby the original underwriter, known as the direct-writing or ceding company transfers either part or all of the liability of a policy to another underwriter(s). The company that assumes a portion of the risk is known as the reinsuring or assuming company. It is a contract made between insurers. The original insured has no right to make a claim against the ceding company in the case of a loss. The percentage of total indurevenue that reinsurance comprisespjust as it was not c

ICE BEHAVIOR

Prices in the industry increased substantially during the 1980’s. The rise of managed care companies during the late 1980’s and early 1990’s have contributed to the more stable inhealth care costs recently. Today, 110 million people belong to some form of managed care program. Currently, premium prices are increasing only slightly more than the general inflation rate. The table below shows the amount of per capita health care expenditures and their percentage change from the previous year. Technological improvements, an aging popugmhea YEAR PER CAPITA HEALTH % CHANGE CARE EXPENDITURES 1994 $ 3,510 5.3% 1993 $ 3,331 6.0% 1992 $ 3,144 8.3% 1991 $ 2,902 8.0% 1990 $ 2,688 11.0% Source: Health Insurance Association of America

24

PES OF PRICES C. TY

For all services, the item being priced is a medical service plan or accident and health insurance

tput. Since the premium for risk protection is considered to be set below market rates, the return earned for investing those premiums should be included in the price. Without the investment earnings, companies would not be able to cover

primary component of this price is the premium. his premium should be reported on a per person (or per family) basis for the selected policy.

he other price component is the earned rate on investments. The rate to be collected is the nt and health insurance

ervices.

lude any pass-through expenses, such as broker fees, paid by the elf-insured company purchasing the administrative services contract. These expenses are often

ong to the appropriate entity as part of the dministrative service provided.

ote: There is no earned rate component for this type of price. Self-insured companies are of their employees. Thus, the insurance company providing

e administrative services do not bear any risk.

remium equivalent. For third party administrative services plans, duplicate quotes will be aid to an employer who self-

insures its employees. While self-insurance is out of scope for PPI, it is in scope for CPI.

policy. As explained under Industry Specific Questions and Procedures, the policy will either be hypothetical or live.

For all services except the third party administrative services, the type of price is a combination of the premium and investment income. Investment income is included to represent the financial intermediation component of the industry ou

claims unless premiums were much higher.

TYPE OF PRICE FOR ALL SERVICES EXCEPT THIRD PARTY ADMINISTRATIVE SERVICES Premium plus earned rate on investments. TheT Enter the annual premium as the ITEM PRICE. Tannual rate that the sample unit earns on its investments related to accides Enter the earned rate on investments as an ADJUSTMENT TO PRICE. TYPE OF PRICE FOR THIRD PARTY ADMINISTRATIVE SERVICES (PPI only) Flat fee. Self-insured companies pay the insurance company a flat fee on either a monthly or annual basis. This fee should excsincluded in the contract fees, but are then passed ala Enter this fee as the ITEM PRICE for PPI quotes. Nresponsible for covering the claimsth TYPE OF PRICE FOR CPI QUOTES Pcreated for CPI. The premium equivalent represents the premium p

25 6325

Enter the premium equivalent as the ITEM PRICE for CPI quotes.

D. TY

be protected against the ossibility of a loss due to an accident or an illness. These policies can be purchased separately or

company or government sponsored employee group plan.

E. DI

lti-

s may be provided to the insured if the performance of the company

favorable. Dividends should be recorded in the adjustments to price section of the transaction ND.

F. AD

ade. It is only known that riders exist for isability, long-term care, accident, and accidental death and dismemberment insurance. These

ined in a previous section.

G. SIZ

e with high maximum dollar amounts for various covered ervices and low deductibles or copayments, will be more expensive than the same type of service

ims is limited. For groups of 100-150, the insurance company is paid a fixed amount er month. If claims experience is favorable, then dividends or rate credits are given at the end of

H. CO

ontract between the insurance company and the insured. The insurance ompany promises to pay a certain amount of expenses and/or income replacement in the advent

red,

must accompany the application in order for the policy to become effective on the

PES OF BUYERS Any individual, group, or corporation can purchase policies in order to pas part of a

SCOUNTS

The only known discounts for accident and health insurance and medical service plans are muproduct discounts. These discounts are given to clients that purchase more than one product from the company. Not all companies provide multi-product discounts. Dividends should also be excluded from the price of insurance. Since the policyholders of mutual companies actually ownpart of the company, dividendischecklist under DIVIDE

DITIONAL CHARGES

Additional charges may be applied should riders be purchased or if non-standard financial arrangements for the payment of premiums are mdriders have been def

E OF PURCHASE

As mentioned previously, the premium will increase as the richness of benefits increases. For example, the premium for a servicswith benefits that are less “rich”. For group insurance, pricing varies with the size of the group. For large groups (over 150), thereis a flexible funding arrangement. The employer pays claims, expenses, and profits. The amount paid in clapthe year.

NTRACTS

An insurance policy is a ccof an accident or illness. Creation of this contract begins with the filing of an application. In turn, the company issues a policy, the terms of which are determined by the application. The contract identifies the insuthe beneficiary, the type of policy, the amount of coverage, premiums, etc. The first premiumpayment

26

desired date. Also, delivery of the policy establishes the precise moment at which coverage

ong-term contracts are sometimes signed. However, most insurance companies renew contracts en increasing so much lately.

I. OT

The main priority of the federal overnment is to maintain the competitiveness of the industry. There is a long list of disclosure

ims reserve requirements. As a result, insurers ccumulate more reserves than they would if there were no minimum level. The amount of assets

the reserve requirements.

es are orted.

ifficulty. States also regulate the operation of an insurer by requiring the fair treatment of cludes regulation of policy forms, rates, conduct and settlement practices.

rities laws. Many of these ws revolve around acquisitions and mergers. At this time, there is legislation pending that could

78. This amendment requires employers to treat regnancy the same as any illness. This includes the payment of disability income and medical

g in all areas of employment, including mployee benefits, against individuals 40 or older. The law provides for a reduction in disability

oyment, transportation, public facilities, and lecommunications. This has been interpreted to include health insurance and other benefits that

begins. Leach year since medical expenses have be

HER VARIABLES AFFECTING PRICE

Federal and state governments regulate insurance premiums. gregulations that work to enhance industry competitiveness. The industry is regulated indirectly through claausually determines State Regulation: State regulations focus on the financial stability of the insurer. These regulations include reserve requirements, nature of permitted investments, and capital and surplus requirements. Reservrequired for unearned premiums, future payments on claims received, and claims not yet repStates oversee the licensing of insurance companies and agents, examination of companies, approval of policy forms, and liquidation of insurance companies in the advent of financial dpolicyholders. This in Federal Regulation: Health insurance companies are subject to federal antitrust and seculacreate direct regulation for the solvency of insurance companies. Title 7 of the Civil Rights Act of 1964 makes it unlawful for an employer to discriminate on the basis of race, color, religion, sex, or national origin. Thus, employees involved in an employer-sponsored health insurance program are guaranteed equal health care coverage under this act. Title 7 of the Civil Rights Act was amended in 19pexpense benefits under fringe benefits programs. The Age Discrimination in Employment Act (ADEA), which was enacted in 1967, prohibits employers with 20 or more employees from discriminatinebenefits, as long as the reduction is actuarially justified. The Americans with Disabilities Act (ADA), enacted in 1990, bans discrimination against disabled people in the areas of empltemay be provided by an employer.

27 6325

The Family and Medical Leave Act (FMLA), enacted in 1993, allows eligible employees to take up to 12 work weeks of unpaid leave in a twelve month period for several reasons. Acceptable reasons include birth, adoption, a serious health condition that prohibits the employee from doing

e essential functions of his or her job, and caring for a child, spouse, or parent with a serious

HMO movement in an ttempt to improve the health care delivery system in the United States. Amendments were made

he Profit margin is the esired return a company would like to realize as a reward for assuming risk. A contingency argin is a buffer in case of unexpected, adverse claims experience.

STRY INFORMATION AND RELATIONS

A. IND

th Plans (AAHP) et, NW, Suite 600

Washington, DC 20036-3421

inistration (HCFA) alth and Human Services

Baltimore, MD 21207-0519 atistics

ance Association of America (HIAA) st

(202)824-1600 ch

ssociation of Insurance Commissioners st

(202)624-7790 Contact: Marcia A. Marshall, Health Analyst