1. social media utilization - indocement.co.id · slide 2 - august 2017 q2 results - indocement...

TRANSCRIPT

INDOCEMENT

Slide 2 - August 2017

Q2 Results - Indocement

INDOCEMENT Indonesia Macroeconomic Overview

World Bank anticipates Indonesia’s economy to grow by 5.3% in 2017 and 5.5% in 2018

and 2019 supported by resilient domestic demand and improvement in private investment

IMF: In 2017, growth is expected to rise modestly to 5.1%, led by a gradual pickup in

private investment in response to stronger commodity prices, low interest rates, and a

recovery in external demand on the back of a pickup in global growth and trade

Bank Indonesia reaffirmed its estimate of 5.0% - 5.4% growth rate in the economy for

2017

Overall, we see the cautious early signs of green shoots – where Consumer Confidence

Index remain robust at the end of Q2 2017 with income boosted by Tunjangan Hari Raya,

end of elections, S&P rating upgrade for Indonesia (the last of the three key credit ratings

agencies to give investment grade status).

Source: Indonesia Statistic

Gross Domestic Product %

Slide 3 - August 2017

Q2 Results - Indocement

INDOCEMENT

Indonesian Cement Industry 2017 Landscape

Lafarge Indonesia

1.5 mio ton

0.2 mio ton (g)

Semen Baturaja

2.2 mio ton

0.7 mio ton (g) Semen Indonesia

15.2 mio ton

0.7 mio ton (g)

Semen Puger

0.5 mio ton

Semen Kupang/Merah Putih

0.4 mio ton

Jui Shin

1.8 mio ton

Holcim Indonesia

12.1 mio ton

Semen Indonesia

7.2 mio ton

0.9 mio ton (g)

Merah Putih

4.9 mio ton

2.8 mio ton (g)

Indocement

24.9 mio ton

Total Cement Capacity in 2017 of 103.8* mio tons,

from 98.5 mio tons in 2016

Source: ASI and internal estimation

Anhui Conch

4.5 mio ton

Panasia

1.8 mio ton

Siam Cement

1.8 mio ton

Semen Bosowa

4.4 mio ton

3.0 mio ton (g)

Semen Indonesia

7.4 mio ton

Anhui Conch

2.2 mio ton (g) * Total capacity in 2017 includes Finished Mills from Hao Han (0.6 mt), Semen

Jakarta (1.5 mt), and Sun Fook (0.6 mt)

Slide 4 - August 2017

Q2 Results - Indocement

INDOCEMENT

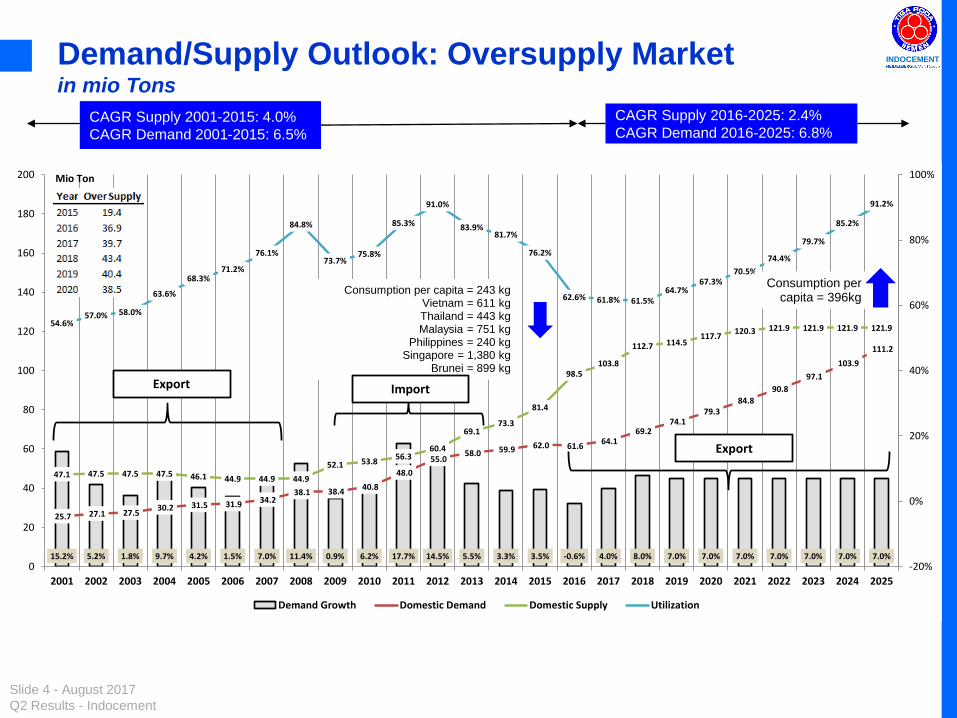

CAGR Supply 2001-2015: 4.0%

CAGR Demand 2001-2015: 6.5%

CAGR Supply 2016-2025: 2.4%

CAGR Demand 2016-2025: 6.8%

Demand/Supply Outlook: Oversupply Market in mio Tons

15.2% 5.2% 1.8% 9.7% 4.2% 1.5% 7.0% 11.4% 0.9% 6.2% 17.7% 14.5% 5.5% 3.3% 3.5% -0.6% 4.0% 8.0% 7.0% 7.0% 7.0% 7.0% 7.0% 7.0% 7.0%

25.7 27.1 27.5 30.2 31.5 31.9 34.2

38.1 38.4 40.8

48.0

55.0 58.0 59.9 62.0 61.6

64.1 69.2

74.1 79.3

84.8

90.8

97.1

103.9

111.2

47.1 47.5 47.5 47.5 46.1 44.9 44.9 44.9

52.1 53.8 56.3

60.4

69.1 73.3

81.4

98.5 103.8

112.7 114.5 117.7

120.3 121.9 121.9 121.9 121.9 54.6%

57.0% 58.0%

63.6%

68.3% 71.2%

76.1%

84.8%

73.7% 75.8%

85.3%

91.0%

83.9% 81.7%

76.2%

62.6% 61.8% 61.5% 64.7%

67.3% 70.5%

74.4%

79.7%

85.2%

91.2%

-20%

0%

20%

40%

60%

80%

100%

0

20

40

60

80

100

120

140

160

180

200

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Mio Ton

Demand Growth Domestic Demand Domestic Supply Utilization

Consumption per capita = 243 kg Vietnam = 611 kg Thailand = 443 kg Malaysia = 751 kg

Philippines = 240 kg Singapore = 1,380 kg

Brunei = 899 kg

Export

Export

Import

Consumption per capita = 396kg

Slide 5 - August 2017

Q2 Results - Indocement

INDOCEMENT

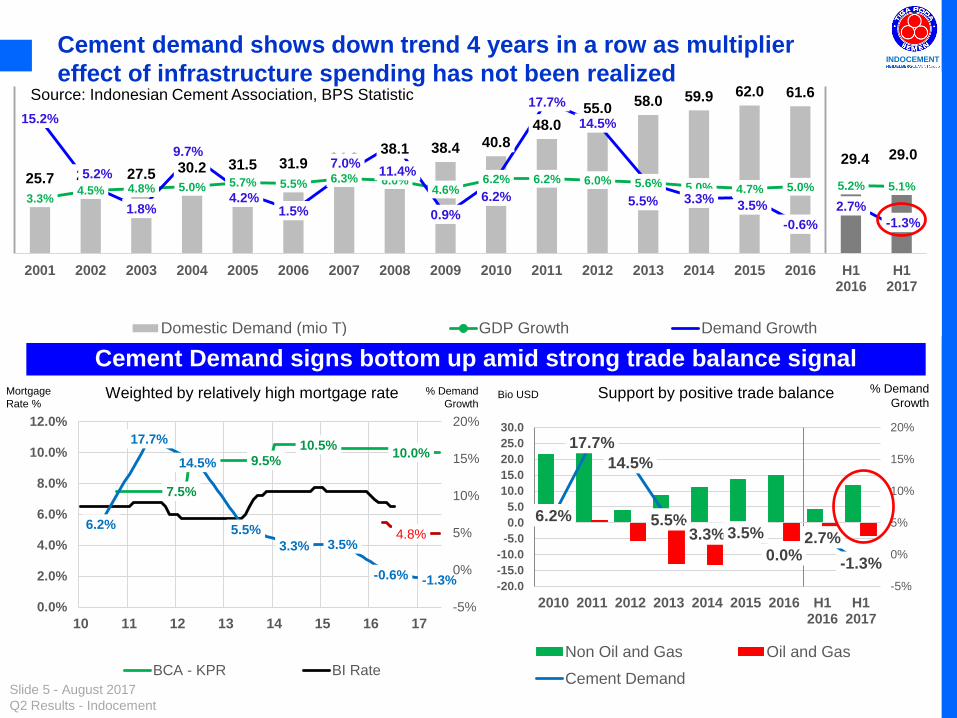

25.7 27.1 27.5 30.2 31.5 31.9 34.2 38.1 38.4 40.8

48.0 55.0

58.0 59.9 62.0 61.6

29.4 29.0

3.3% 4.5% 4.8% 5.0% 5.7% 5.5% 6.3% 6.0%

4.6% 6.2% 6.2% 6.0% 5.6% 5.0% 4.7% 5.0% 5.2% 5.1%

15.2%

5.2%

1.8%

9.7%

4.2% 1.5%

7.0% 11.4%

0.9%

6.2%

17.7%

14.5%

5.5% 3.3% 3.5%

-0.6%

2.7%

-1.3%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 H12016

H12017

Domestic Demand (mio T) GDP Growth Demand Growth

Cement demand shows down trend 4 years in a row as multiplier

effect of infrastructure spending has not been realized

Cement Demand signs bottom up amid strong trade balance signal

Bio USD % Demand

Growth Mortgage

Rate %

% Demand

Growth Support by positive trade balance Weighted by relatively high mortgage rate

Source: Indonesian Cement Association, BPS Statistic

7.5%

9.5% 10.5%

10.0%

4.8% 6.2%

17.7%

14.5%

5.5%

3.3% 3.5%

-0.6% -1.3%

-5%

0%

5%

10%

15%

20%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

10 11 12 13 14 15 16 17

BCA - KPR BI Rate

6.2%

17.7%

14.5%

5.5% 3.3% 3.5%

0.0% 2.7%

-1.3%

-5%

0%

5%

10%

15%

20%

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

2010 2011 2012 2013 2014 2015 2016 H12016

H12017

Non Oil and Gas Oil and Gas

Cement Demand

Slide 6 - August 2017

Q2 Results - Indocement

INDOCEMENT

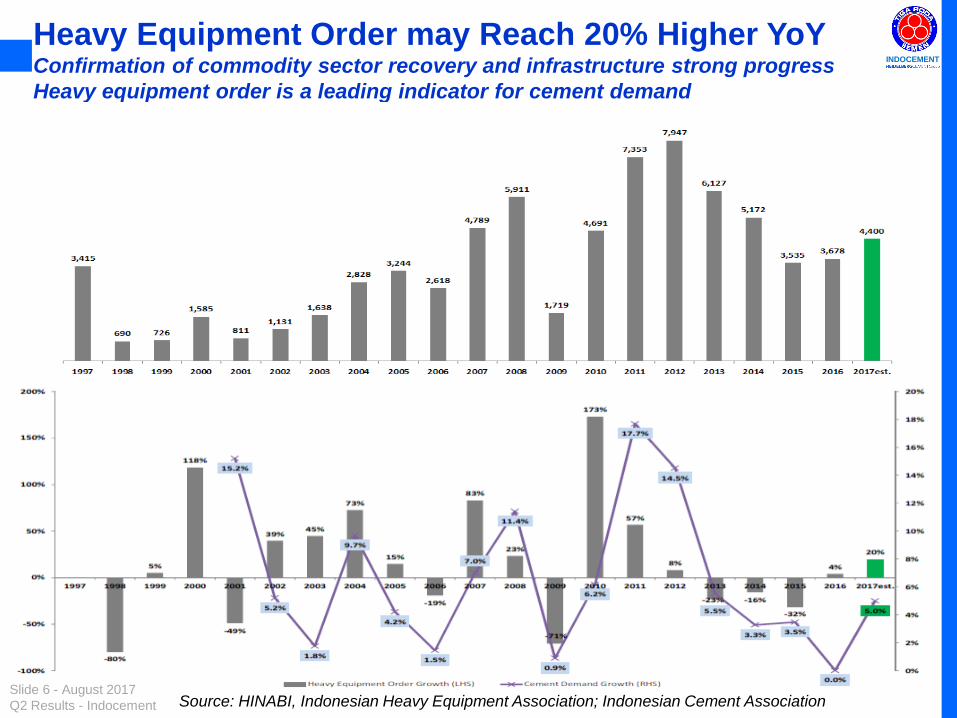

Heavy Equipment Order may Reach 20% Higher YoY Confirmation of commodity sector recovery and infrastructure strong progress

Heavy equipment order is a leading indicator for cement demand

Source: HINABI, Indonesian Heavy Equipment Association; Indonesian Cement Association

Slide 7 - August 2017

Q2 Results - Indocement

INDOCEMENT

Market Growth:

>15%

5-10%

0-5%

<0%

10-15%

Domestic Consumption Growth & Market Share per region YTD June 2017

Source: Indonesia Cement Association

Source: Indonesia Statistic (processed)

Note:

- Lebaran season in June 2017 corrected

the market growth +4.1% in Ytd May

2017.

- Contrary, prior year Lebaran that hit the

market was occurred in July 2016.

- In general Western Part of Java still

having sluggish demand while mid and

east significantly boosted by infra project.

- Outside java is mixture to slightly on

corrective growth (commodity recovery

still not translated to demand).

Slide 8 - August 2017

Q2 Results - Indocement

INDOCEMENT

73% 74% 75% 72% 73% 70% 74% 71% 72% 72% 73% 74%

27%

26%

25%

28%

27%

30%

26%

29%

28% 28%

27%

26%

22%

23%

24%

25%

26%

27%

28%

29%

30%

31%

67%

68%

69%

70%

71%

72%

73%

74%

75%

76%

Q1 '15 Q2 '15 Q3 '15 Q4'15 FY 2015 Q1 '16 Q2 '16 Q3 '16 Q4 '16 FY 2016 Q1 '17 Q2 '17

Java (LHS) Outside Java (RHS)

Java is still key market area in delivering strong results

• On absolute terms Java remains the dominant factors in delivering strong

results

• Indocement is able to protect home market and maintain stable sales, however

declining sales from outside Java brought down total domestic sales

Geographic composition of Sales

Slide 9 - August 2017

Q2 Results - Indocement

INDOCEMENT

14,459 14,568 12,943 12,518

6,068 5,820

3,517 3,931

4,109 3,860

1,838 1,740

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2013 2014 2015 2016 H1 '16 H1 '17

In thousand tons

Bag Bulk

The importance of bulk sales continues

• Portion of bag sales is lower than bulk due to declining sales especially in outside Java

for H1 2017

• Composition of bag vs bulk sales in H11 2017 is 77.0% vs. 23.0%

• Indocement positions itself as a reliable partner for infrastructure projects providing

quality bulk cement and concrete at timely delivery

• Stronger focus on increasing

bulk sales

• High bulk volume in Jakarta

• Indocement benefits from

proximity to Jakarta

Bag/Bulk sales composition Jan - Dec

20% 21%

24% 24%

23% 23%

Slide 10 - August 2017

Q2 Results - Indocement

INDOCEMENT

Continuous focus on cost control with disciplined

spending on promotional activities

• Increase in coal price caused increase in fuel and power cost due to gain in running the most

efficient kilns.

• Manufacturing Overhead portion decreases due to cost savings activities including repairs.

• Ramping up of P14 kiln in H1 already starts to deliver savings; full savings expected starting in H2.

• Increase in SG&A relates to additional cost to support end user program and Rajawali promotion.

Fixed Cost Control – bio IDR Composition of Manufacturing Cost as %

Trend

25.4% 10.5% 42.8% 21.3%

25.7%

10.3%

40.9%

23.1%

23.2%

11.4%

44.4%

21.0%

0%

10%

20%

30%

40%

50%

Raw Materials Direct labor Fuel andPower

Man.Overhead

Jan - Jun 2015 Jan - Jun 2016 Jan - Jun 2017

1,095

965 1,027

340 319 326

-

200

400

600

800

1,000

1,200

H1 2015 H1 2016 H1 2017

Selling Expense G&A Expense

-7%

+7%

-12%

-6%

+6%

+2%

Slide 11 - August 2017

Q2 Results - Indocement

INDOCEMENT

Continue in Cost Leadership to maintain a decent margin

in H1 2017

Continue competitive environment, Management focus on taking respective initiatives early on during

the year:

Operational Excellence program

Fixed cost reduction program

Managing efficient kiln utilization

INTP EBITDA margin development

New market entrants leading to higher competition and pricing pressure

but Indocement maintains better margin compared to peers

INTP Gross margin development

44.5% 45.0% 44.6% 44.4%

43.2% 41.8% 41.7% 41.2%

34.5% 34.2%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

Jan-Mar Jan-Jun Jan-Sep Jan-Dec

2015 2016 2017

34.8% 34.5% 34.0% 33.8%

33.9% 31.8% 31.1% 30.3%

22.3% 22.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Jan-Mar Jan-Jun Jan-Sep Jan-Dec

2015 2016 2017

Slide 12 - August 2017

Q2 Results - Indocement

INDOCEMENT

H1 2017 H1 2016

Bio IDR Bio IDR %

Total Sales Volume (thousand tons) 7,932 8,129 -196.1 -2.4%

Domestic Sales Volume (thousand tons) 7,829 7,938 -109.2 -1.4%

Export Sales Volume (thousand tons) 103 190 -86.9 -45.7%

Net Revenues 6,543.7 7,741.9 -1,198.2 -15.5%

Cost of Revenues -4,302.5 -4,507.0 204.5 4.5%

GROSS PROFIT 2,241.2 3,234.9 -993.7 -30.7%

% of Net Revenues 34.2% 41.8%

Operating Expenses -1,352.7 -1,283.7 -69.0 -5.4%

Other Operating Income - Net 6.1 16.7 -10.6 -63.3%

OPERATING INCOME 894.6 1,967.9 -1,073.3 -54.5%

% of Net Revenues 13.7% 25.4%

EBITDA 1,438.8 2,460.6 -1,021.8 -41.5%

% of Net Revenues 22.0% 31.8%

Finance Income - Net 238.0 266.8 -28.8 -10.8%

Equity in Net Earnings of Associated Companies - Net 4.2 12.3 -8.1 -66.2%

INCOME BEFORE FINAL TAX AND INCOME TAX EXPENSE 1,136.8 2,247.0 -1,110.2 -49.4%

Final Tax -0.3 -0.4 0.0 11.9%

INCOME BEFORE INCOME TAX EXPENSE 1,136.5 2,246.7 -1,110.2 -49.4%

Income Tax Benefit (Expense) - Net -234.7 182.5 -417.2 -228.6%

INCOME FOR THE PERIOD 901.8 2,429.2 -1,527.3 -62.9%

Other Comprehensive Income (Loss) for the Period, Net of Tax 0.7 -6.2 6.9 110.7%

TOTAL COMPREHENSIVE INCOME FOR THE PERIOD 902.5 2,422.9 -1,520.4 -62.8%

VarianceDescription

Bio IDR

Financial Result Consolidated Statement of Comprehensive Income

• Operating margin reduction from 25.4% to 13.7% contributed by lower revenues by -15.5% due to strong competition on weak

demand situation which impact was reduced by cost efficiency in production (+4.5%) amidst cost pull from current soaring coal price.

• Active end user program initiated at beginning of year to support the volume performance.

Slide 13 - August 2017

Q2 Results - Indocement

INDOCEMENT Balance Sheet Consolidated Statement of Financial Position

• Outside dividend payment impact, inventories balance increased to anticipate peak volume in 2nd half.

Inline with production, payable balance slightly higher.

• Increase in Non-Current Assets compare to same period last year was mainly due to spending in capital

expenditures.

• Dividend Payment history:

Slide 14 - August 2017

Q2 Results - Indocement

INDOCEMENT Our P14 in Citeureup has already started

• Kiln line already fully operational starting end of last year and savings already started with full

benefit expected in H2.

• Currently its benefit USD 4-5/t.

A new Tiga Roda cement plant, with annual

installed production capacity of 4.4 million

cement at Citeureup, Bogor - Indonesia.

IDR ~6 Trillion investment.

A production line that equipped with modern and energy efficient facility.

Designed to utilized alternative fuels and materials and owns state-of-art emission system and

environment-friendly production facility with bag filter as effective dust filter in all production lines.

Slide 15 - August 2017

Q2 Results - Indocement

INDOCEMENT

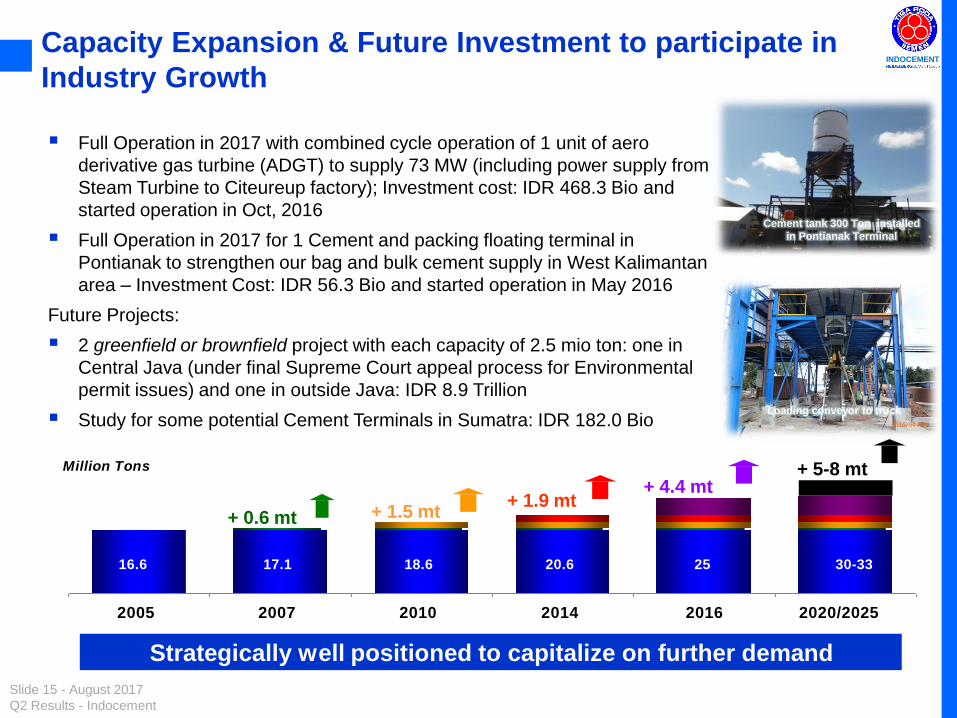

Full Operation in 2017 with combined cycle operation of 1 unit of aero

derivative gas turbine (ADGT) to supply 73 MW (including power supply from

Steam Turbine to Citeureup factory); Investment cost: IDR 468.3 Bio and

started operation in Oct, 2016

Full Operation in 2017 for 1 Cement and packing floating terminal in

Pontianak to strengthen our bag and bulk cement supply in West Kalimantan

area – Investment Cost: IDR 56.3 Bio and started operation in May 2016

Future Projects:

2 greenfield or brownfield project with each capacity of 2.5 mio ton: one in

Central Java (under final Supreme Court appeal process for Environmental

permit issues) and one in outside Java: IDR 8.9 Trillion

Study for some potential Cement Terminals in Sumatra: IDR 182.0 Bio

16.6 30-33 17.1 18.6 20.6 25

2005 2007 2010 2014 2016 2020/2025

Million Tons

+ 0.6 mt + 1.5 mt + 1.9 mt

+ 4.4 mt + 5-8 mt

Strategically well positioned to capitalize on further demand

Capacity Expansion & Future Investment to participate in

Industry Growth

Cement tank 300 Ton installed

in Pontianak Terminal

Loading conveyor to truck

Slide 16 - August 2017

Q2 Results - Indocement

INDOCEMENT

Ready Mix Concrete and Aggregates Expansion • Strengthening Ready-Mix Concrete business particularly high-

grade quality in order to meet the increase demand of

infrastructure development in Indonesia.

• Current focus is on infrastructure projects and its domino-effect on

development of residential, industrial area and high rise building.

• H1 2017 sales volume decreased by 27.1% due to slowing down

construction activities across Indonesia and lower economic growth

in general as well as heavy competition.

• Pionirbeton, a subsidiary, is one of market leaders in RMC

business.

• Secured concrete market by signing exclusive and long-term

contract of andesite and sand supply from Ketapang and Belitung.

800 630 683

930 956

1,221

2,429

3,517

4,430

3,947

3,377

2,988

1,483

1,081

0

300

600

900

1,200

1,500

1,800

2,100

2,400

2,700

3,000

3,300

3,600

3,900

4,200

4,500

4,800000m3

RMC Sales Volume AGG Sales Volume

Slide 17 - August 2017

Q2 Results - Indocement

INDOCEMENT CEMENT MARKET Outlook for 2017

Market Condition

• National cement consumption growth started to turn positive and expected to

grow around 4-5% in 2017 (versus negative growth of -0.6% in 2016)

• Consumption in 2017 will increase in line with higher Government’s projects and

some commercial and residential projects after Tax Amnesty, decrease of

mortgage (KPR) interest, loosened regulation on LTV ratio, second mortgage

availability for “off-plan” properties, reduction in tax for transfer of ownership,

clarity in property ownership by foreigners, and simplification of regulations.

• Strong concrete and bulk cement demand anticipated in outside Java and more

spread area in Java due to faster Government’s infrastructure projects in 2017

Expansion in Cement Terminals and Batching Plants are required.

• Over supply of about 36.9 mio tons in 2016 and up to 39.7 mio tons in 2017 will

change the cement market outlook and we expect the continuing tight

competition among 19 brands from 15 players (from 9 brands and 9 players

previously)

• Recent hike in coal price will curb the potential further drop in prices in near

future and possible consolidation. Coal price has slide back to $75.5 in June

2017 from peak of $102 in December 2016 however, remain considerably higher

than last year.

Slide 18 - August 2017

Q2 Results - Indocement

INDOCEMENT Indocement’s Action Plan in 2017

• Run P14 production (10,000 tpd) in full-swing in 2017 will help to reduce further

production cost by about USD 4-5 per ton

• Optimize product mix from 13 line of cement production will bring competitive

advantages of Indocement to introduce different types of cement (OPC, PCC,

PPC, TR Rapid, PCC Industry and future products- slag cement)

• Clinker exports and domestic clinker sales will be done more during

oversupply. (2016: cement export 72,000 ton, clinker export 319,000 ton; target

2017: cement export 168,000 ton, clinker export 333,000 ton)

• Strengthen our Pull demand in bagged cement segment from end-user

customers and Retail/ Distribution channel to strengthen our Brand, TIGA

RODA Cement

• Using RAJAWALI brand as fighting brand to get some volume for customer

who perceive cement as “commodity” product and in low-price cement

segment - in competition with 2nd tier brands out of new players

• Develop new business line of prefabricated affordable housing products

“Rumah Pabrikasi Indocement” through new subsidiary

• Strong balance sheet with no gearing is an important winning factor in

competition and in future consolidation phase if happen in near future

Slide 19 - August 2017

Q2 Results - Indocement

INDOCEMENT New Brand of “RAJAWALI” as “fighting brand”

• Through its existing distribution

channel, Rajawali was initially

launched on Oct 10, 2016 with

presence in three cities in 2016

and already available in 30 cities,

like: Jakarta, 15 cities in West

Java, 6 Cities in Banten, and 8

Cities in Central Java.

Sticky, Strong & More

environmentally cement

product!!!

• Quality assurance from Indocement.

• Produced with Indocement standard

technology, equipment and materials,

• Semen Rajawali has a very consistent

quality.

• Not easy to crack.

• Specially designed for easy builders as it

suitable for any building type from

structural work, plaster, acian and others.

• Manufactured with environmentally

friendly technology.

• … Affordable prices!

Video:

https://youtu.be/Q9DXnCHEH3U

Slide 20 - August 2017

Q2 Results - Indocement

INDOCEMENT End User Program

source: www.sementigaroda.com

INDOCEMENT

42 Years Building Indonesia KOKOH

THANK YOU

Slide 22 - August 2017

Q2 Results - Indocement

INDOCEMENT Important Notice Disclaimer

This presentation contains general information which provided without any representations or warranties, express or implied and does not

constitute or form part of, and is not made in connection with, any offer for sale or subscription of or solicitation, recommendation, or invitation of

any offer to buy or subscribe for any securities nor shall it or any part of it form the basis of or be relied on in connection with any contract,

commitment, or investment decision whatsoever.

Terms of Use

Slides prepared in this presentation are strictly confidential and have been prepared as a support for verbal discussions only. The information

contained in this presentation is being presented to you solely for your information and may not be reproduced or redistributed to any other person,

in whole or in part. You acknowledge that, because of the limited nature of communication through our presentation features, any assistance you

may receive using any such features is likely to be incomplete and may even be misleading.

Forward-Looking Statements

This presentation includes forward-looking statements, which are based on the expectation or forecast about future events, formed by Indocement

after reviewing existing data and research. Such statements involve known and unknown risks including factors such as: (i)Global macroeconomic

and geopolitical situations; (ii) Indonesia macroeconomic and geopolitical situation; (iii) Competition from incumbents and new players; (iii)

Changes in laws, regulation, taxation, or accounting standards or practices; (iv) Acquisitions, divestitures, and various business opportunities that

we may pursue; (v)Force majeure; (vi)Labor unrest or other similar situations; (vii)Outcome of pending or threatened litigation

Indocement does not give assurance that such outcome will be attained. If you have any specific questions about any legal, financial or tax matter,

you should consult your lawyer/financial/tax Consultant or other professional legal services provider.

For further information please contact

PT Indocement Tunggal Prakarsa Tbk.

Wisma Indocemen, 8th Floor

Jl. Jend. Sudirman Kav 70 - 71

Jakarta 12910, Indonesia

Phone : +62 21 2512121

e-mail: [email protected].

©2017, PT Indocement Tunggal Prakarsa Tbk. All rights reserved.