1 stockholders’ equity acctg 5120 david plumlee. page2 business forms sole proprietorship and...

TRANSCRIPT

1

Stockholders’ equity

ACCTG 5120David Plumlee

page2

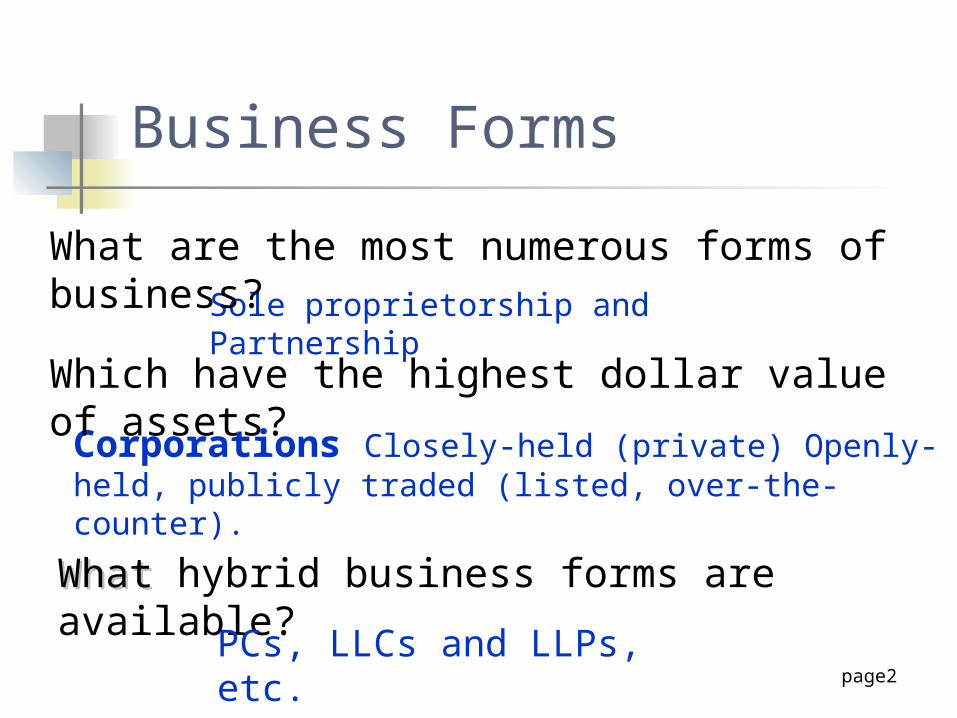

Business Forms

Sole proprietorship and Partnership

Corporations Closely-held (private) Openly-held, publicly traded (listed, over-the-counter).

What are the most numerous forms of business?

Which have the highest dollar value of assets?

What What hybrid business forms are available?PCs, LLCs and LLPs,

etc.

page3

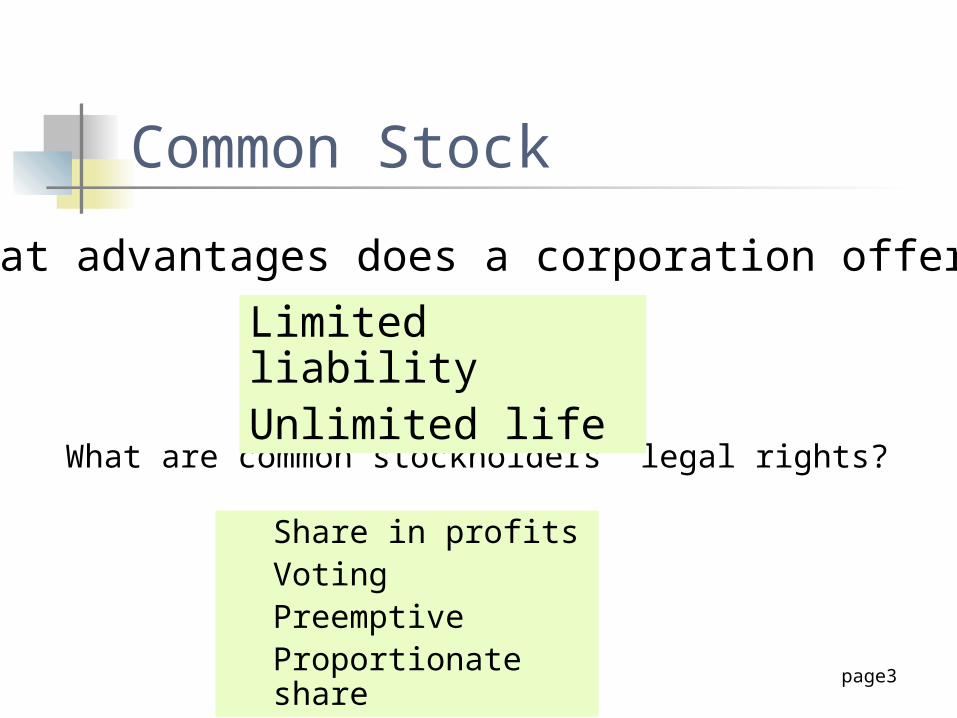

Common Stock

What are common stockholders’ legal rights?

Limited liability Unlimited life

Share in profitsVotingPreemptive Proportionate share

What advantages does a corporation offer?

page4

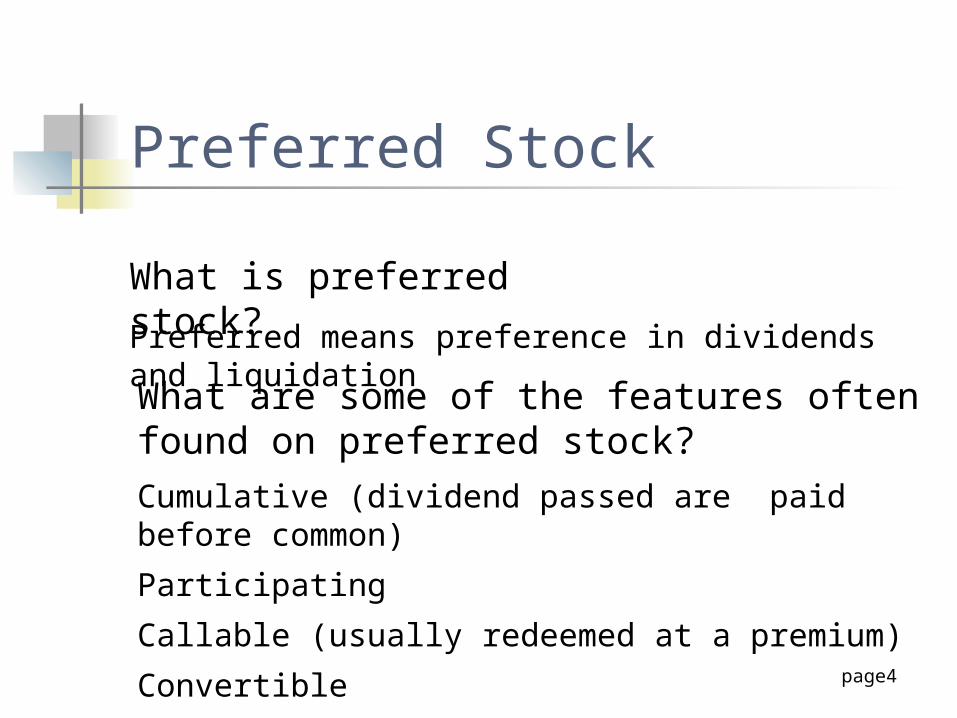

Preferred Stock

Preferred means preference in dividends and liquidation

Cumulative (dividend passed are paid before common)

Participating

Callable (usually redeemed at a premium)

Convertible

What is preferred stock?

What are some of the features often found on preferred stock?

page5

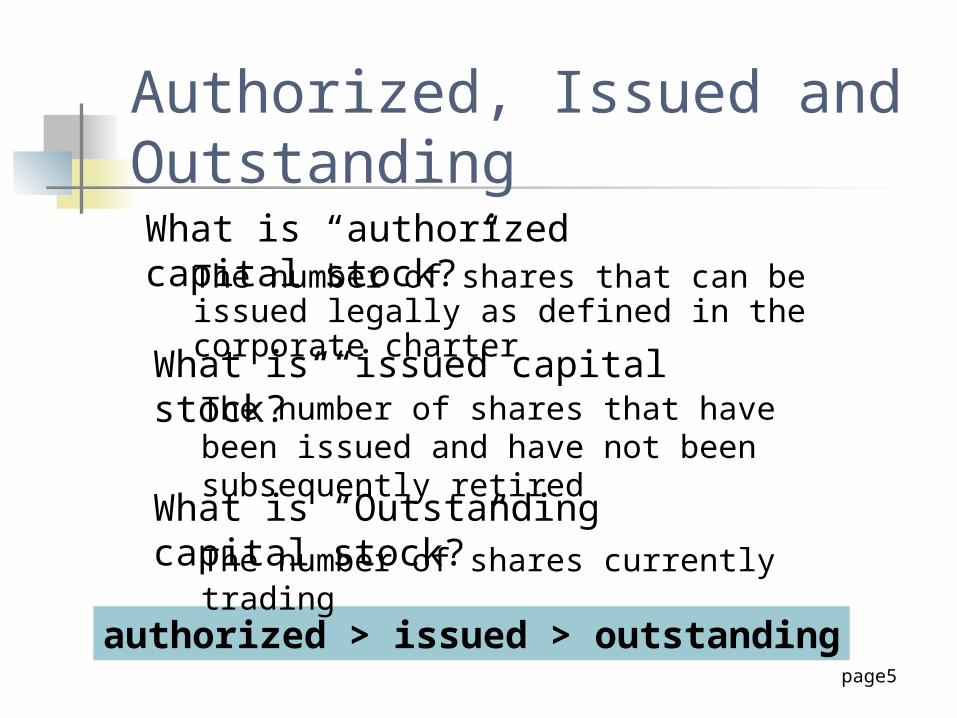

Authorized, Issued and Outstanding

authorized > issued > outstanding

What is “authorized capital stock?”The number of shares that can be issued

legally as defined in the corporate charter

What is “issued capital stock?”The number of shares that have been issued and have not been subsequently retired

What is “Outstanding capital stock?”The number of shares currently trading

page6

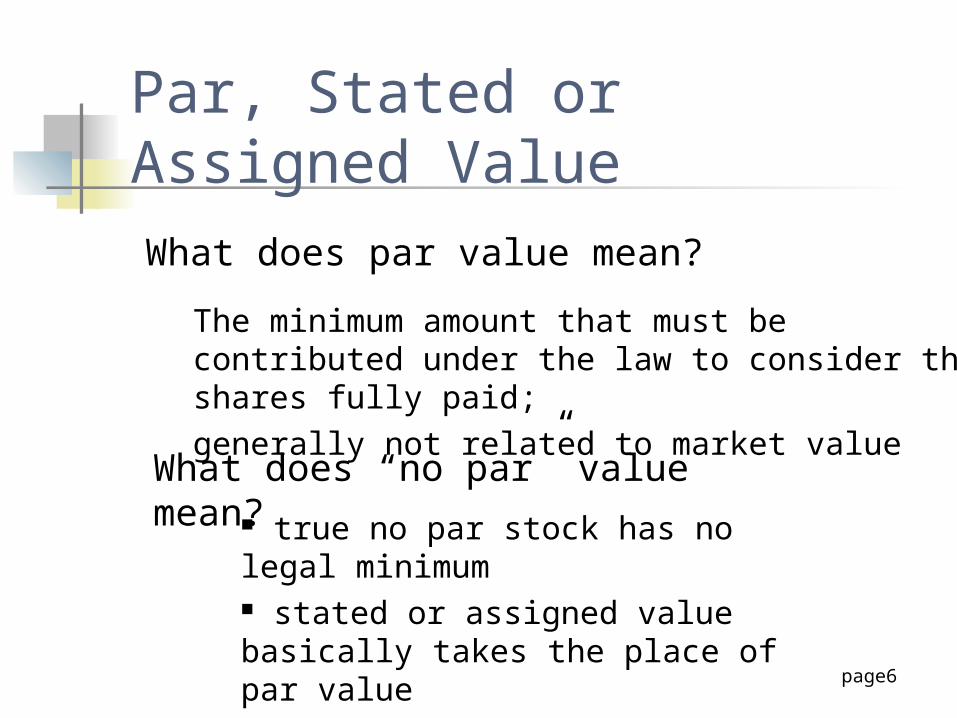

Par, Stated or Assigned ValueWhat does par value mean?

The minimum amount that must be contributed under the law to consider the shares fully paid;generally not related to market value

true no par stock has no legal minimum stated or assigned value basically takes the place of par value

What does “no par” value mean?

page7

Stock Issue

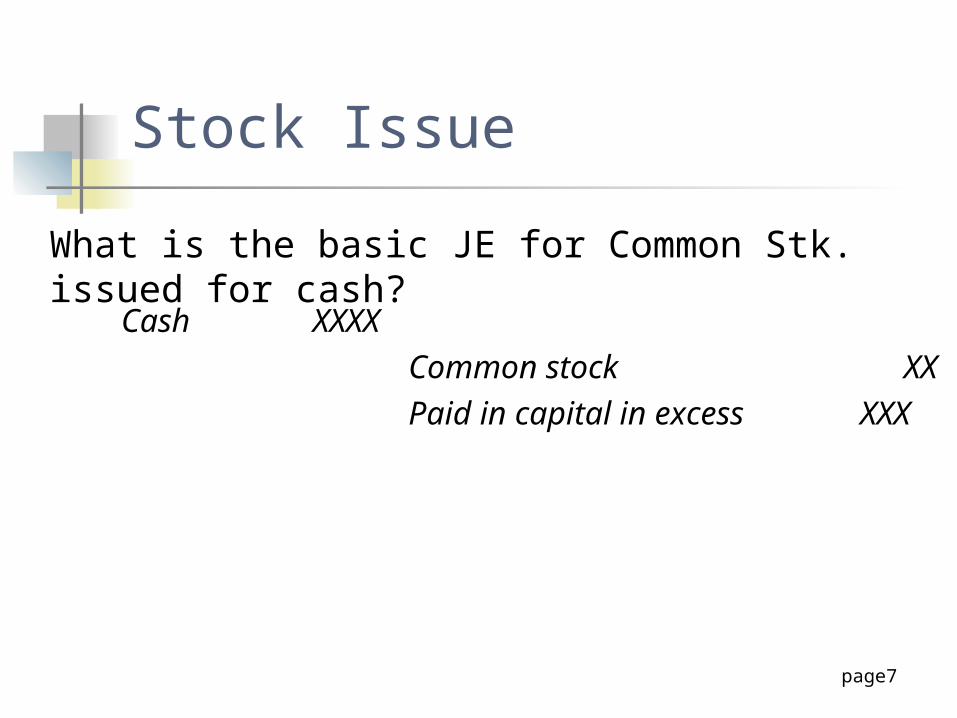

What is the basic JE for Common Stk. issued for cash?

Cash XXXXCommon stock

XXPaid in capital in excess

XXX

page8

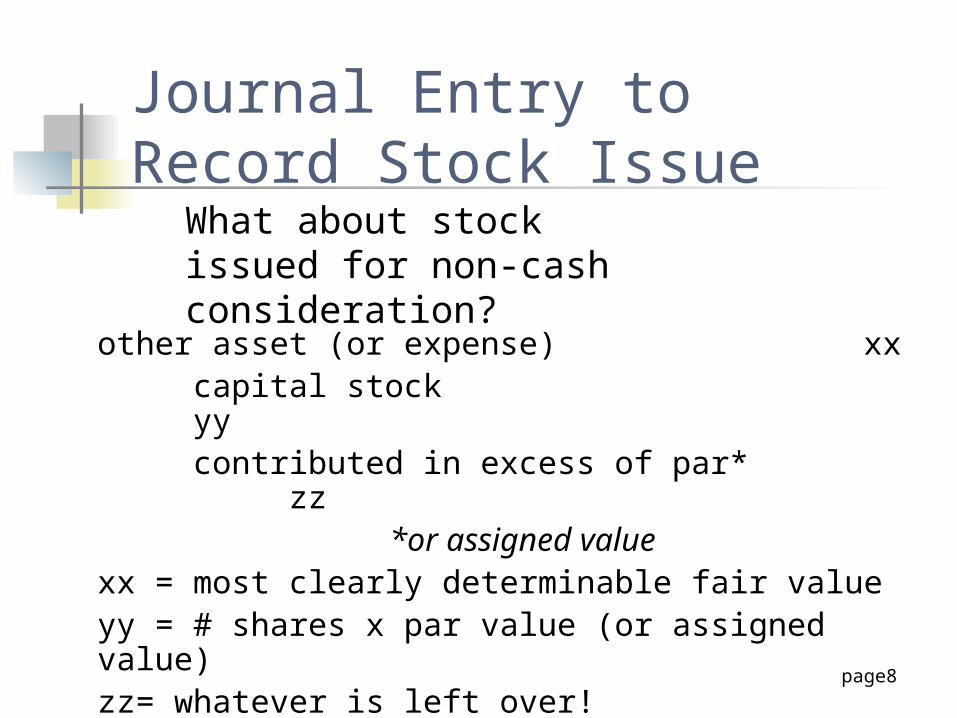

Journal Entry to Record Stock Issue

other asset (or expense) xxcapital stock yycontributed in excess of par* zz

*or assigned valuexx = most clearly determinable fair valueyy = # shares x par value (or assigned value)zz= whatever is left over!

What about stock issued for non-cash consideration?

page9

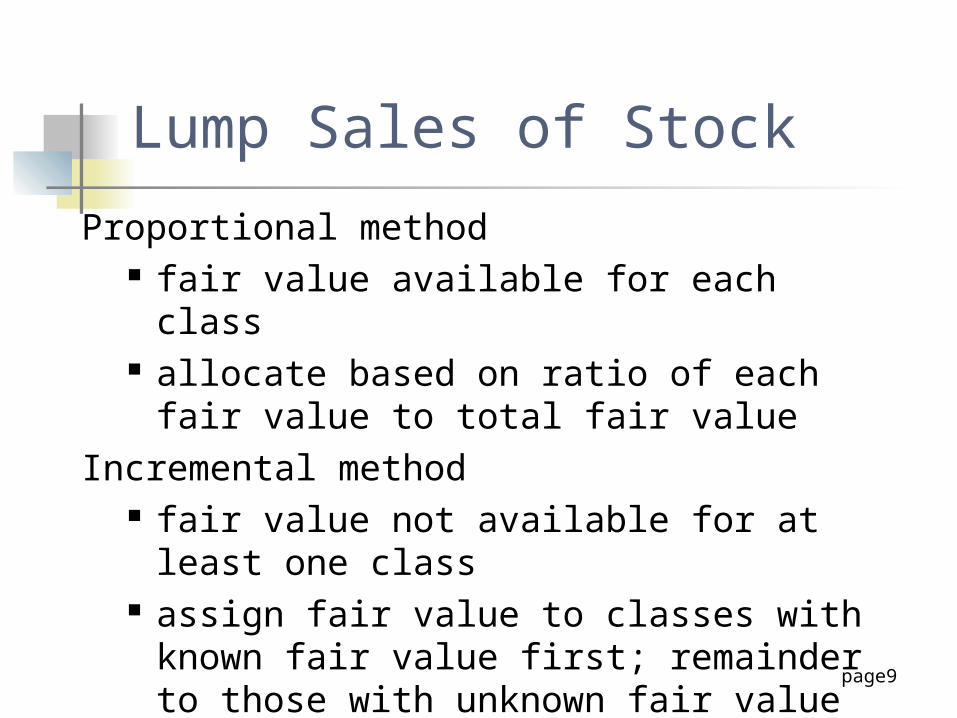

Lump Sales of Stock

Proportional method fair value available for each class allocate based on ratio of each fair

value to total fair valueIncremental method

fair value not available for at least one class

assign fair value to classes with known fair value first; remainder to those with unknown fair value

page10

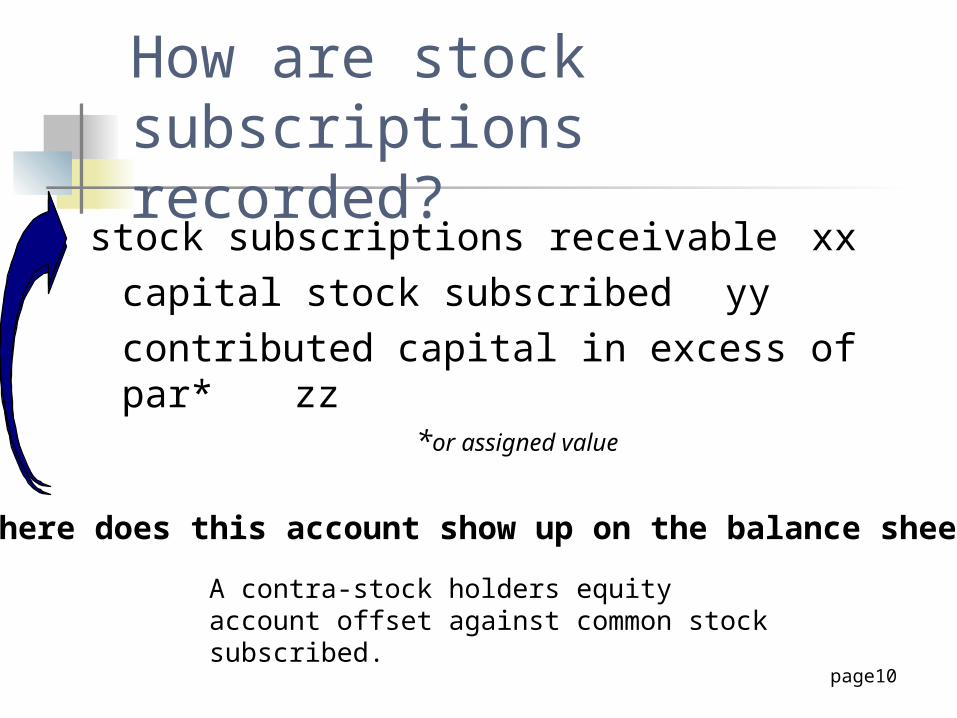

How are stock subscriptions recorded?

stock subscriptions receivable xxcapital stock subscribed yycontributed capital in excess of par*zz

*or assigned value

Where does this account show up on the balance sheet?

A contra-stock holders equity account offset against common stock subscribed.

page11

Default on Subscriptions

Return all payments made Issue shares equivalent to # paid in full All payments made forfeited Resale under a lien

reimbursed to extent net receipts > original subscription price not to exceed payments made

What if the subscriber What if the subscriber defaults??

page12

Treasury Stock

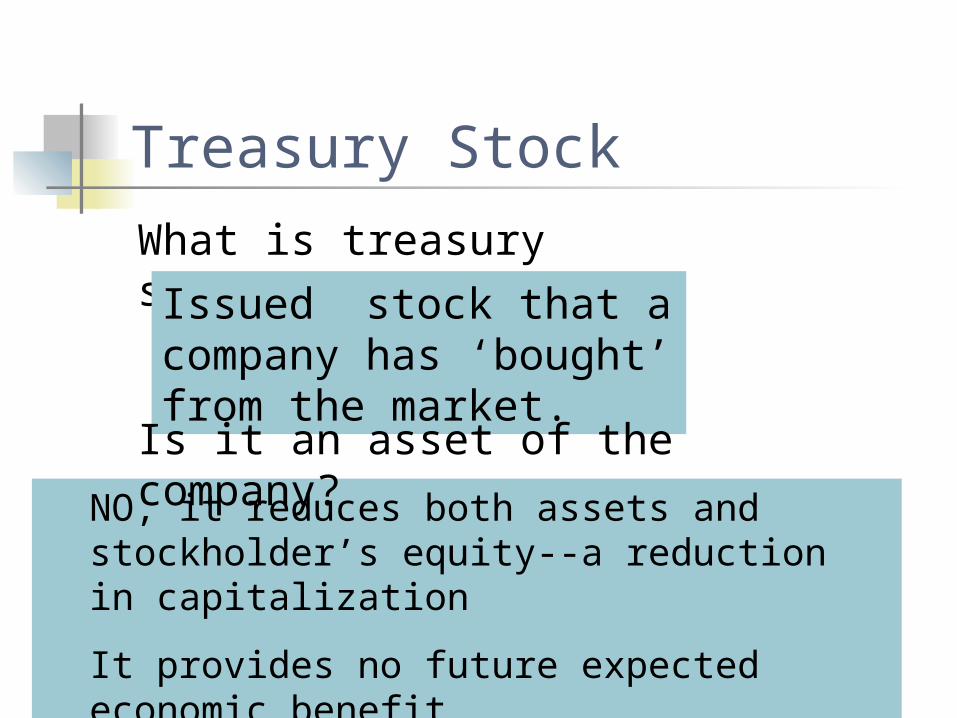

What is treasury stock?

Issued stock that a company has ‘bought’ from the market.

NO, it reduces both assets and stockholder’s equity--a reduction in capitalization

It provides no future expected economic benefit

Is it an asset of the company?

page13

Accounting for Treas. Stk.

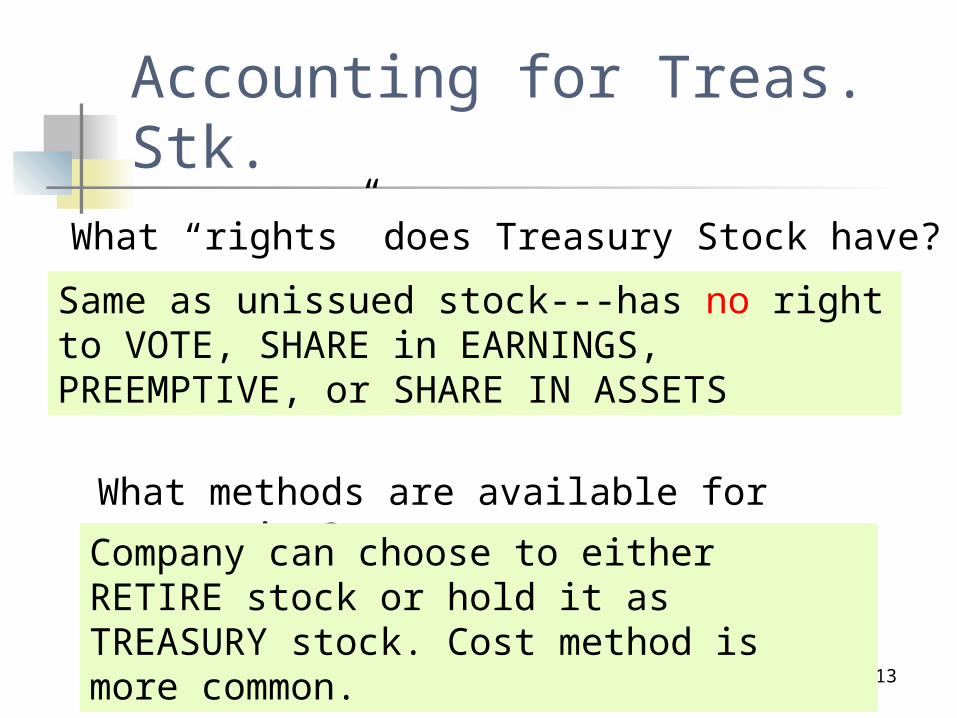

Same as unissued stock---has no right to VOTE, SHARE in EARNINGS, PREEMPTIVE, or SHARE IN ASSETS

What “rights” does Treasury Stock have?

What methods are available for accounting?

Company can choose to either RETIRE stock or hold it as TREASURY stock. Cost method is more common.

page14

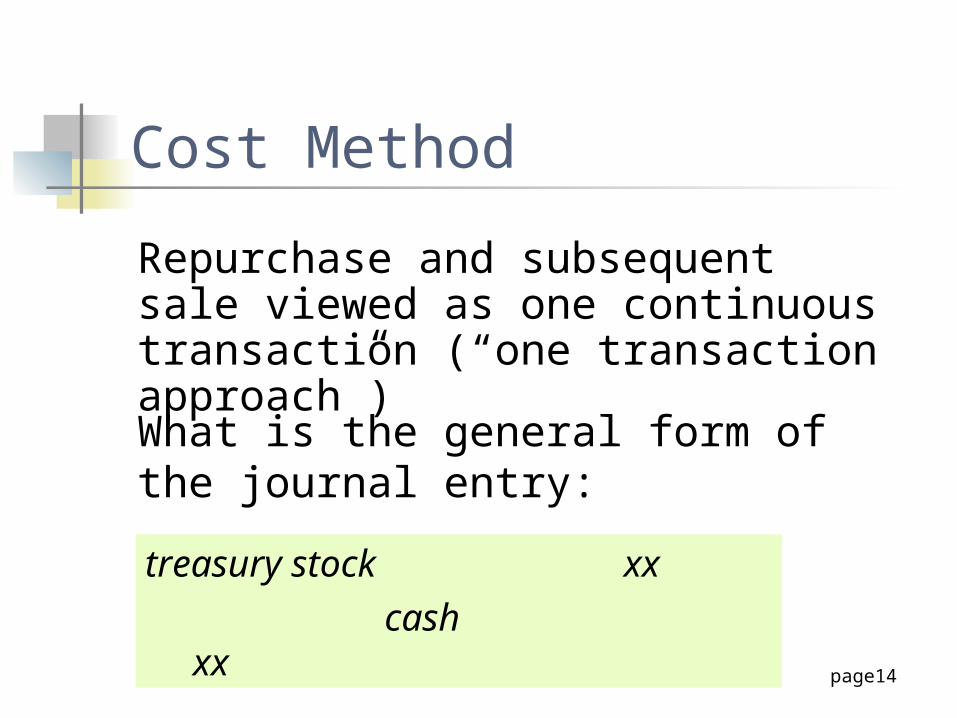

Cost Method

Repurchase and subsequent sale viewed as one continuous transaction (“one transaction approach”)

treasury stock xxcash

xx

What is the general form of the journal entry:

page15

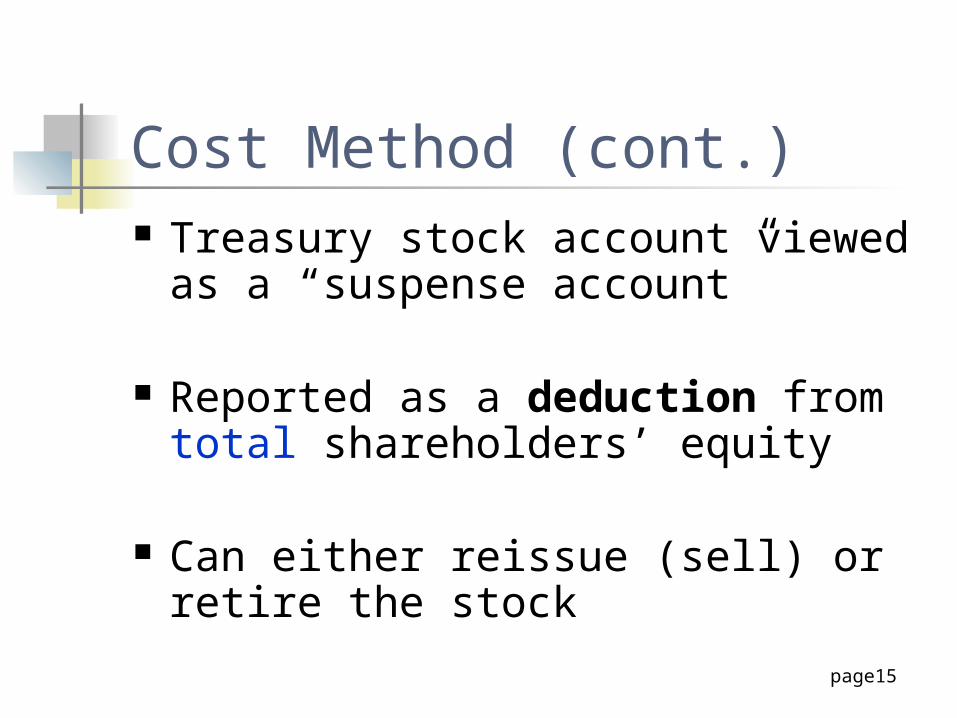

Cost Method (cont.) Treasury stock account viewed as

a “suspense account”

Reported as a deduction from total shareholders’ equity

Can either reissue (sell) or retire the stock

page16

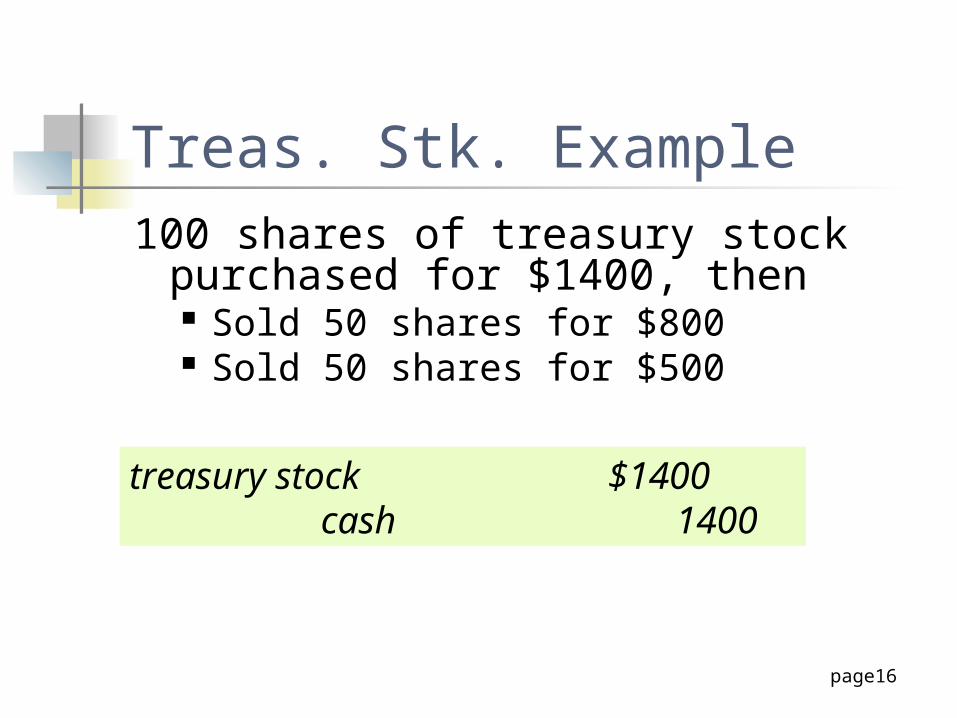

Treas. Stk. Example100 shares of treasury stock

purchased for $1400, then Sold 50 shares for $800 Sold 50 shares for $500

treasury stock $1400cash 1400

page17

Cost Method - Resale When resale price > acquisition

cost Remove acquisition cost from

treasury stock account difference between cost and sale

price is credited to “contributed capital from TS transactions”

Cash $800Treasury stock 700

APIC – Treasury Stock 100

page18

Cost Method - ResaleWhen resale price < acquisition cost

Remove acquisition cost from treasury stock account

Then debit “contributed capital from TS transactions”

(same class) if available remaining amount --debit retained earnings

Cash $500APIC – T/Stock 100RE 100

Treasury stock 700

page19

Cost Method - Retirement Remove acquisition cost from treasury stock Then remove stock…

reduce capital stock for par reduce PIC for amount paid in when stock

was issued If you need a debit to balance

APIC from TS transactions (same class) retained earnings

If you need a credit difference to be allocated contributed capital from TS transactions

page20

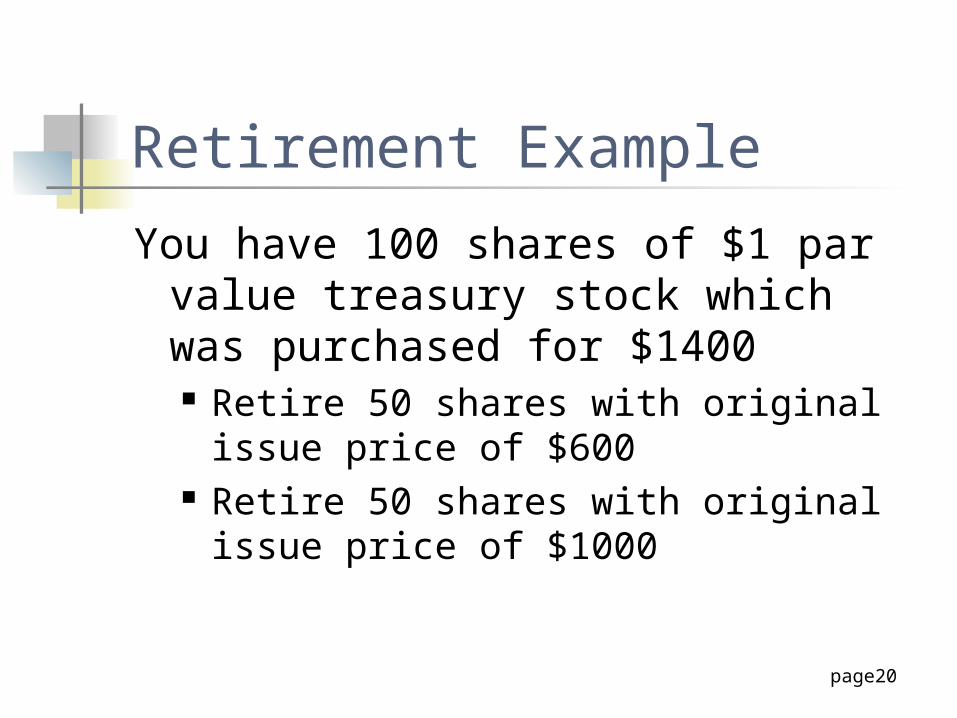

Retirement Example

You have 100 shares of $1 par value treasury stock which was purchased for $1400 Retire 50 shares with original issue

price of $600 Retire 50 shares with original issue

price of $1000

page21

Example EntriesCom/stk. $ 50

APIC in excess 550

RE 100

Treasury Stock $700

Com/stk. $ 50

APIC in excess 950

APIC-t/s retirement $ 300 Treasury Stock 700

page22

Cost method: T/S is subtracted at the bottom of the shareowner equity section at cost. It is included in the “regular” shares above as well.

Presentation of Treasury Stock

page23

Exchange of rights for other rights: Hybrid of debt and ownership characteristics.

Dividends paid are a % of par or $ per share. Preferred shareholders’ claim on earnings generally

precedes common shareholders’ Dividends

Cumulative (arrearages) vs. noncumulative stock Participating

Fully Partially Non

Preferred Stock

page24

Debt or Equity? Debt related

Stated return Non-voting Preference at liquidation Non-participating

Equity Return not mandatory Dividends, not interest expense Participating

page25 3636

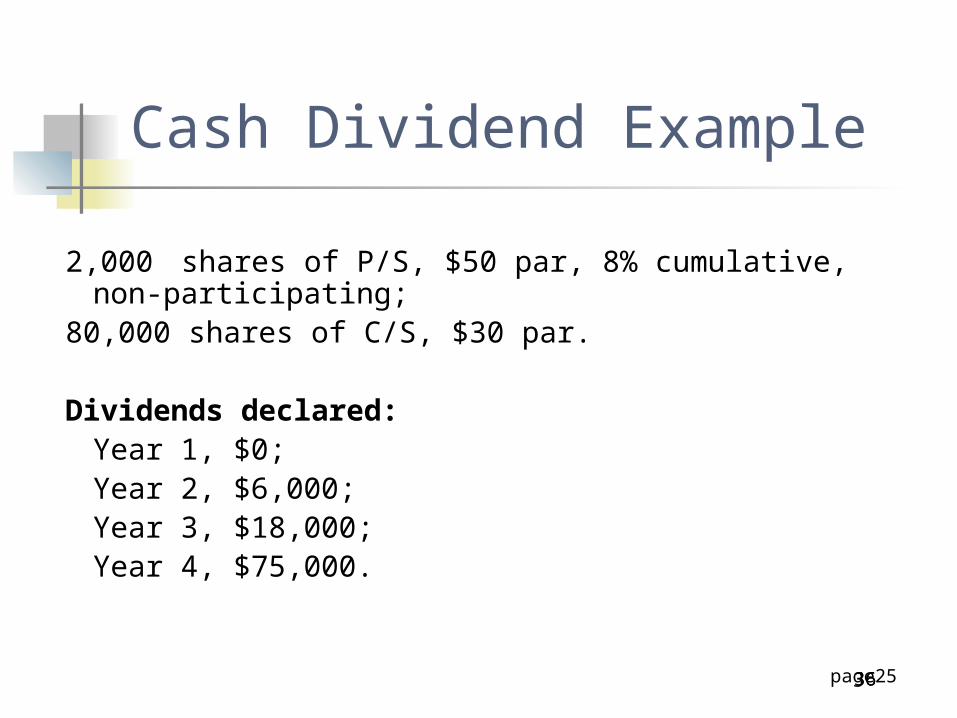

Cash Dividend Example

2,000 shares of P/S, $50 par, 8% cumulative, non-participating;

80,000 shares of C/S, $30 par. Dividends declared:

Year 1, $0; Year 2, $6,000; Year 3, $18,000; Year 4, $75,000.

page26 3636

Cash Dividends

To P/S Arrearage To C/S

Year 1 Year 2

Year 3 Year 4

How much is the preferred dividend?

P/S dividend = 2,000 shares x $50 par x .08 = $8,000

$0 $8,000 $0$6,000 $10,000 $0

$18,000 $0 $0

$8,000 $0 $67,000

page27 37

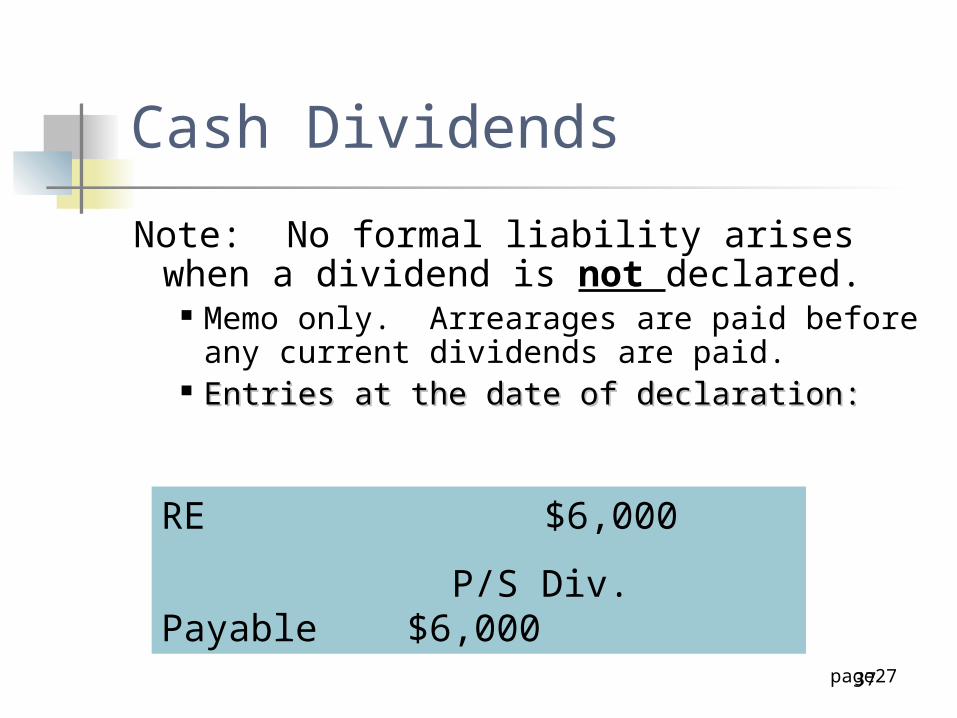

Note: No formal liability arises when a dividend is not declared.

Memo only. Arrearages are paid before any current dividends are paid.

Entries at the date of declaration:Entries at the date of declaration:

Cash Dividends

RE $6,000

P/S Div. Payable $6,000

page28

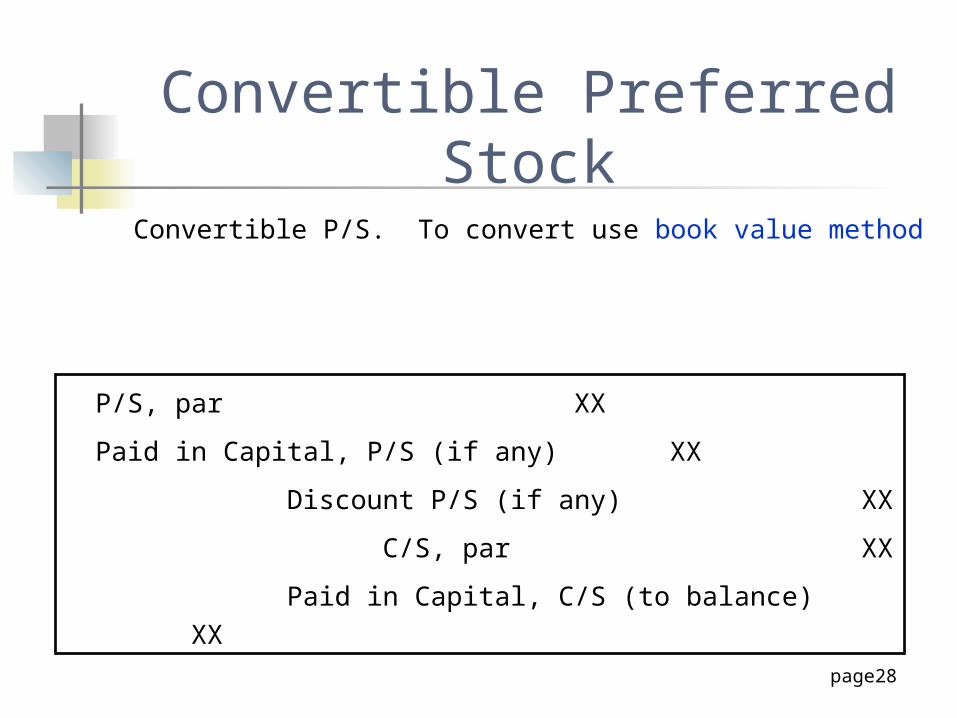

Convertible P/S. To convert use book value method

Convertible Preferred Stock

P/S, par XX

Paid in Capital, P/S (if any) XX

Discount P/S (if any) XX

C/S, par XX

Paid in Capital, C/S (to balance) XX