1 the loan application starting point to a proper character investigation / background investigation...

TRANSCRIPT

1

The Loan ApplicationStarting Point to a Proper Character Investigation / Background Investigation (CIBI)

2

Introduction

The Loan Application is the 1st step in the Credit Investigation/ Background Investigation (CIBI) process.

The Loan Application Form is the source of initial information on an applicant and is filled in by the Account Officer during the initial interview with the applicant; the applicant signs the form after the interview.

The Loan Application form shows if the applicant meets the eligibility requirements of the bank’s MF loan product.

3

Objectives

By the end of the lesson, participants will be able to:

1. Conduct an interview with the applicant and get relevant information required in the application form

2. Evaluate if the applicant meets the bank’s loan eligibility criteria and make a decision whether or not to proceed with the thorough CIBI

4

How to Interview the Applicant & Character References

o Conduct the interview in a very cordial and friendly manner

o Avoid being offensive in delivering your thoughts, questions and inquiries. Once the applicant becomes defensive it would be difficult to extract information at his own free will. (Remember, the best source of information is the client).

o Do not confront the applicant on issues or answers that you do not agree with. Verify these issues from other sources

5

How to Interview the Applicant & Character References

o Make your queries short and straighto Later in the interview, inquire about personal

matters or problems affecting the applicant, offer some assistance, but refrain if you feel that the client resents this line.

o Do not conduct the interview as if you are interrogating the applicant.

o Prepare by studying the information on the loan application. If needed, write down important questions you want to ask from the applicant and character references.

6

The Loan Application Form

o There are two (2) types of Loan Application Forms - (1) for New Loans; and, (2) for Repeat Loans

o The Loan Application is a one pager form that has the basic information for an initial evaluation of client eligibility and risk

7

How to fill-out the form

General Guidelines

• Fill in all the information

• Put a √ in the appropriate boxes

• Do not leave blank spaces; put N/A if information is not applicable

8

New LoanNew Loan Application Form

9

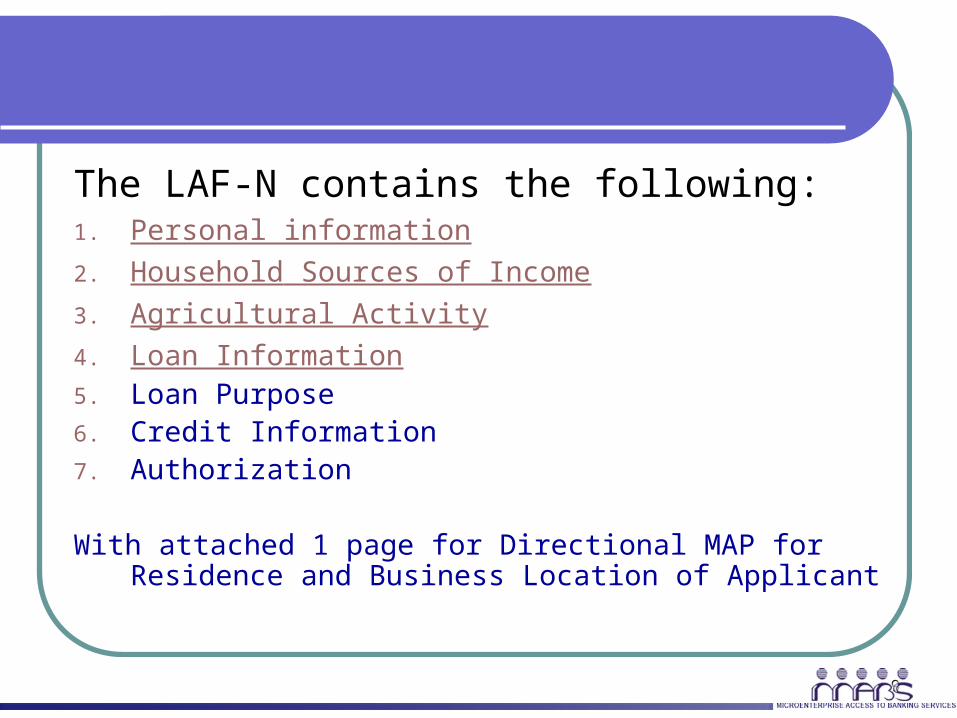

The LAF-N contains the following:1. Personal information2. Household Sources of Income3. Agricultural Activity4. Loan Information5. Loan Purpose6. Credit Information7. Authorization

With attached 1 page for Directional MAP for Residence and Business Location of Applicant

10

Analyzing information

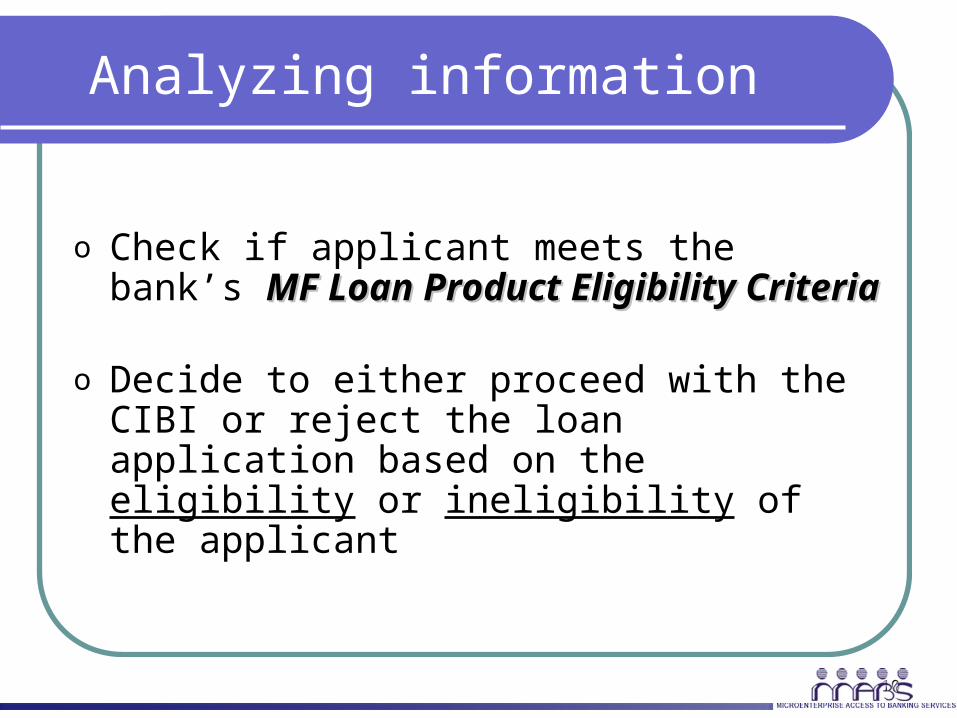

o Check if applicant meets the bank’s MF Loan MF Loan Product Eligibility CriteriaProduct Eligibility Criteria

o Decide to either proceed with the CIBI or reject the loan application based on the eligibility or ineligibility of the applicant

11

Repeat LoanRepeat Loan Application Form

12

Comparison of application forms

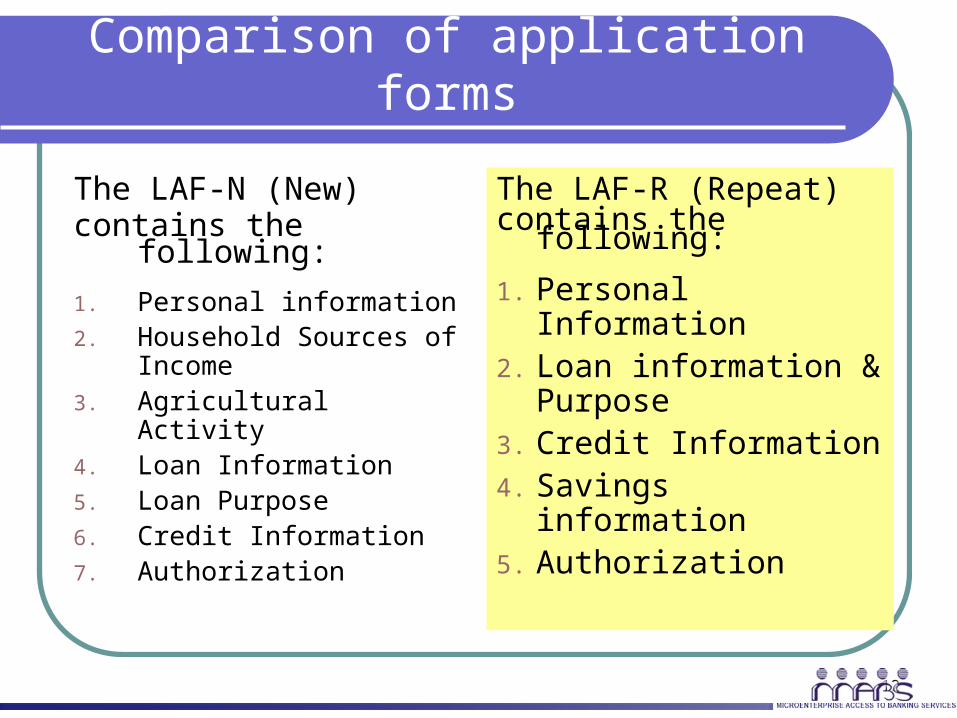

The LAF-N (New) contains the following:

1. Personal information2. Household Sources of

Income3. Agricultural Activity4. Loan Information5. Loan Purpose6. Credit Information7. Authorization

The LAF-R (Repeat) contains the following:

1. Personal Information2. Loan information &

Purpose3. Credit Information4. Savings information5. Authorization

13

Summary

The Loan Application Form is the initial source of information on the applicant/borrower and is filled out by the Account Officer during the interview.

The interview conducted by the Account Officer with the applicant/borrower must be thorough to ensure that all the primary information required by the bank is obtained.

A review of the Client Eligibility Criteria Client Eligibility Criteria is done by the Account Officer and on the basis of the findings, the AO makes a decision whether or not to proceed with the CIBI process.

14

LINKS

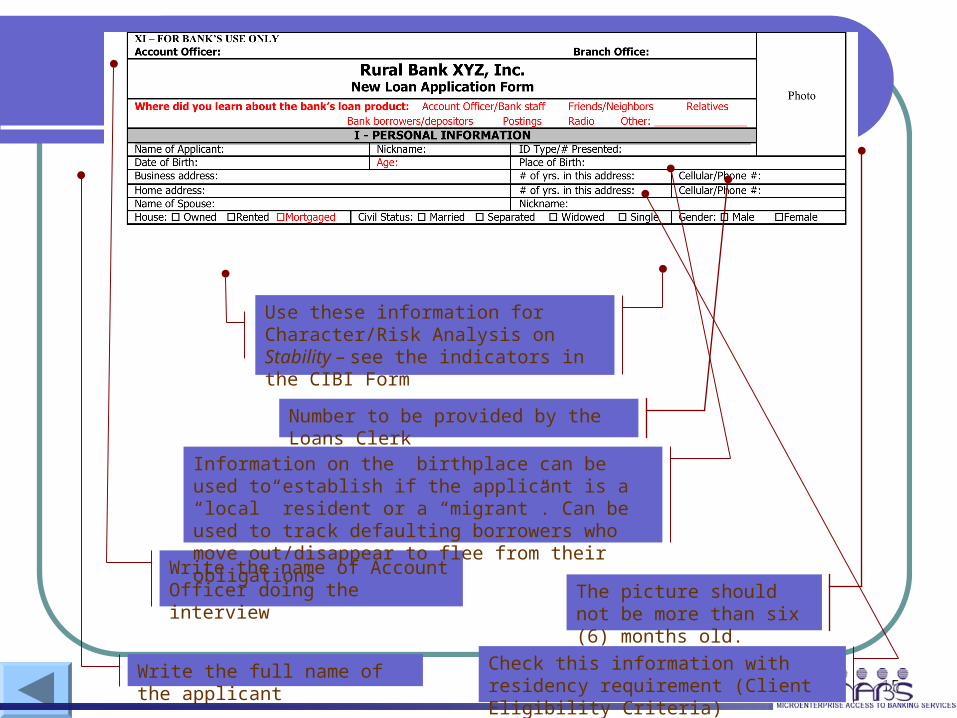

15Write the full name of the applicant

Use these information for Character/Risk Analysis on Stability – see the indicators in the CIBI Form

The picture should not be more than six (6) months old.

Write the name of Account Officer doing the interview

Information on the birthplace can be used to establish if the applicant is a “local” resident or a “migrant”. Can be used to track defaulting borrowers who move out/disappear to flee from their obligations

Number to be provided by the Loans Clerk

Check this information with residency requirement (Client Eligibility Criteria)

16

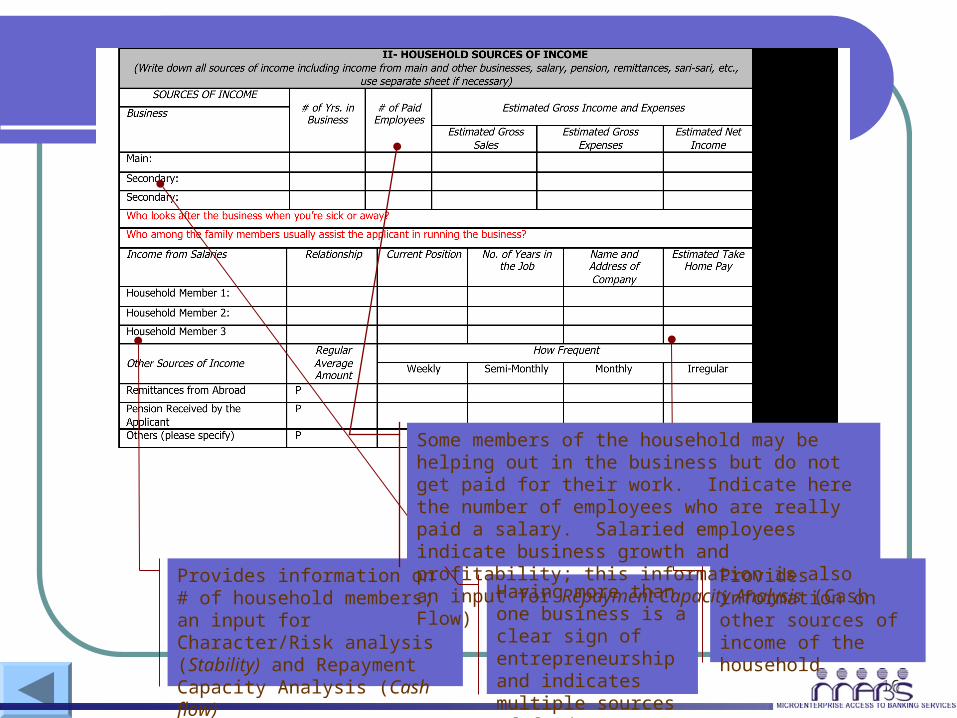

Provides information on other sources of income of the household

Provides information on # of household members; an input for Character/Risk analysis (Stability) and Repayment Capacity Analysis (Cash flow)

Having more than one business is a clear sign of entrepreneurship and indicates multiple sources of funds to pay the loan

Some members of the household may be helping out in the business but do not get paid for their work. Indicate here the number of employees who are really paid a salary. Salaried employees indicate business growth and profitability; this information is also an input for Repayment Capacity Analysis (Cash Flow)

17

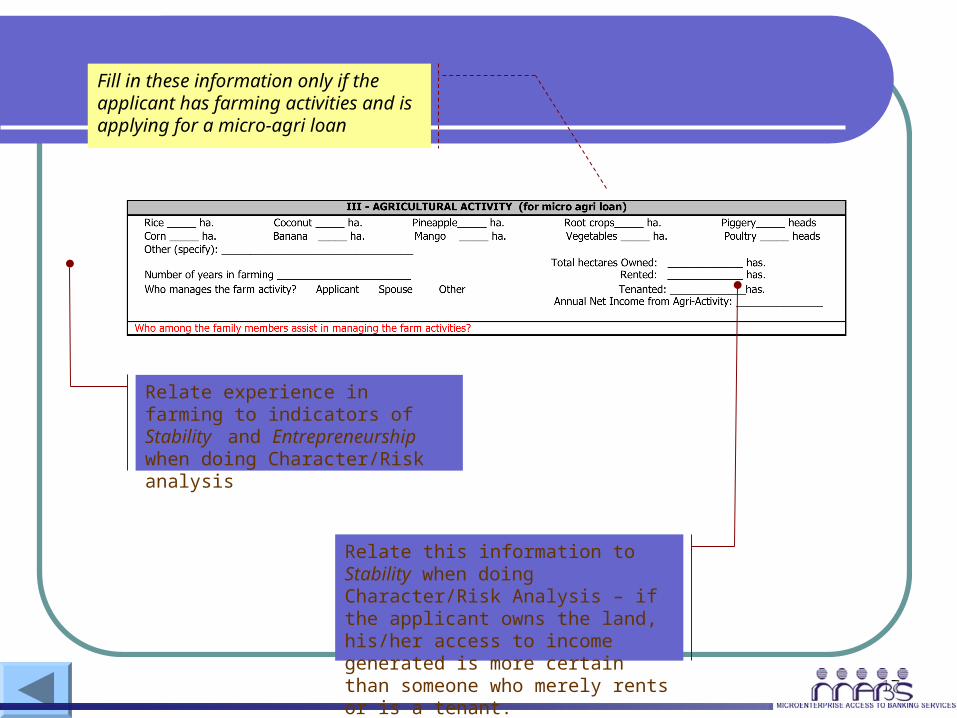

Fill in these information only if the applicant has farming activities and is applying for a micro-agri loan

Relate experience in farming to indicators of Stability and Entrepreneurship when doing Character/Risk analysis

Relate this information to Stability when doing Character/Risk Analysis – if the applicant owns the land, his/her access to income generated is more certain than someone who merely rents or is a tenant.

18

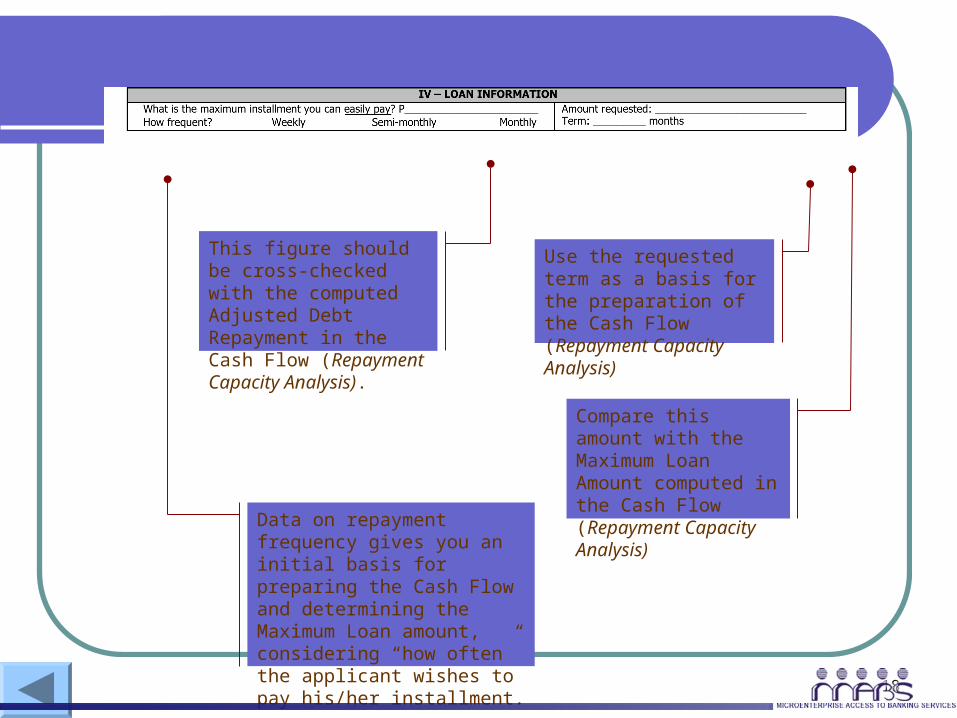

This figure should be cross-checked with the computed Adjusted Debt Repayment in the Cash Flow (Repayment Capacity Analysis).

Data on repayment frequency gives you an initial basis for preparing the Cash Flow and determining the Maximum Loan amount, considering “how often” the applicant wishes to pay his/her installment.

Compare this amount with the Maximum Loan Amount computed in the Cash Flow (Repayment Capacity Analysis)

Use the requested term as a basis for the preparation of the Cash Flow (Repayment Capacity Analysis)

19

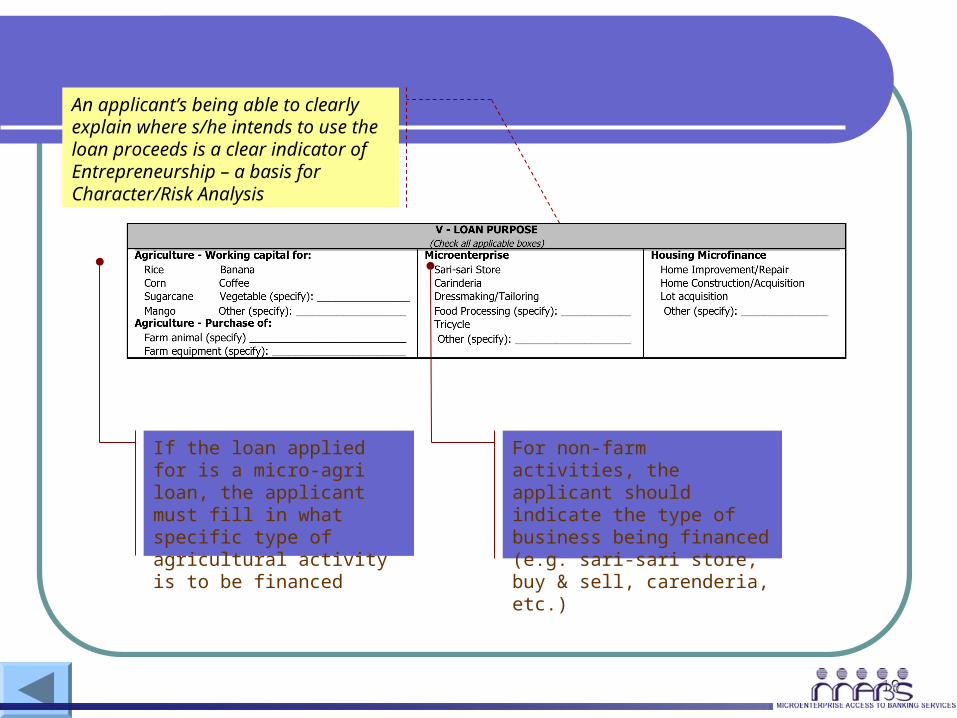

An applicant’s being able to clearly explain where s/he intends to use the loan proceeds is a clear indicator of Entrepreneurship – a basis for Character/Risk Analysis

If the loan applied for is a micro-agri loan, the applicant must fill in what specific type of agricultural activity is to be financed

For non-farm activities, the applicant should indicate the type of business being financed (e.g. sari-sari store, buy & sell, carenderia, etc.)

20

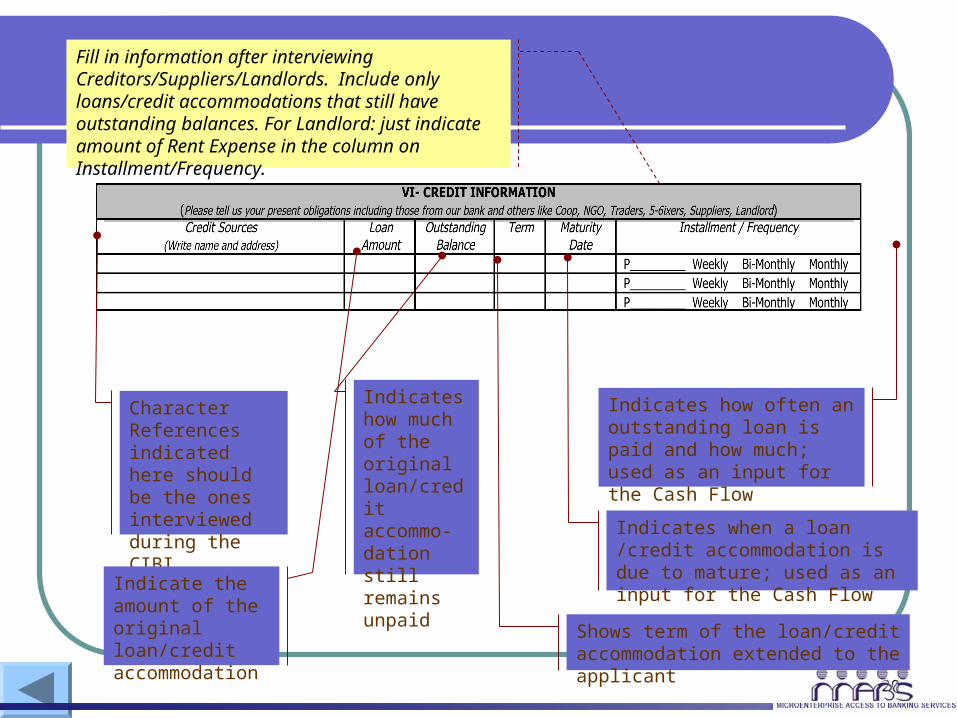

Fill in information after interviewing Creditors/Suppliers/Landlords. Include only loans/credit accommodations that still have outstanding balances. For Landlord: just indicate amount of Rent Expense in the column on Installment/Frequency.

Character References indicated here should be the ones interviewed during the CIBI.

Indicates how much of the original loan/credit accommo-dation still remains unpaid

Indicate the amount of the original loan/credit accommodation

Shows term of the loan/credit accommodation extended to the applicant

Indicates when a loan /credit accommodation is due to mature; used as an input for the Cash Flow

Indicates how often an outstanding loan is paid and how much; used as an input for the Cash Flow

21

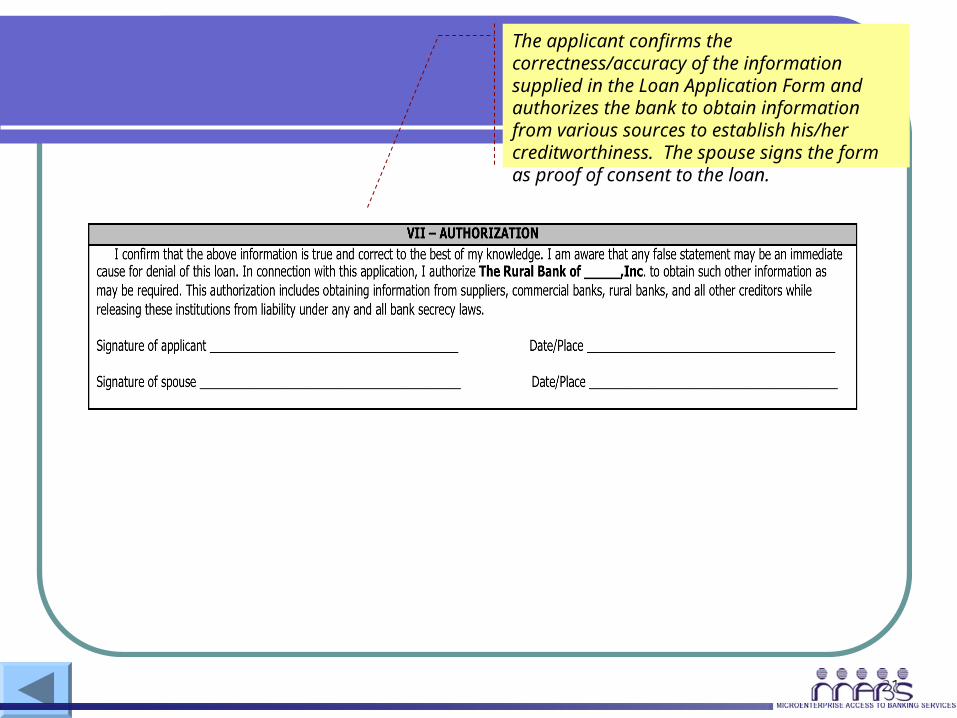

The applicant confirms the correctness/accuracy of the information supplied in the Loan Application Form and authorizes the bank to obtain information from various sources to establish his/her creditworthiness. The spouse signs the form as proof of consent to the loan.

22

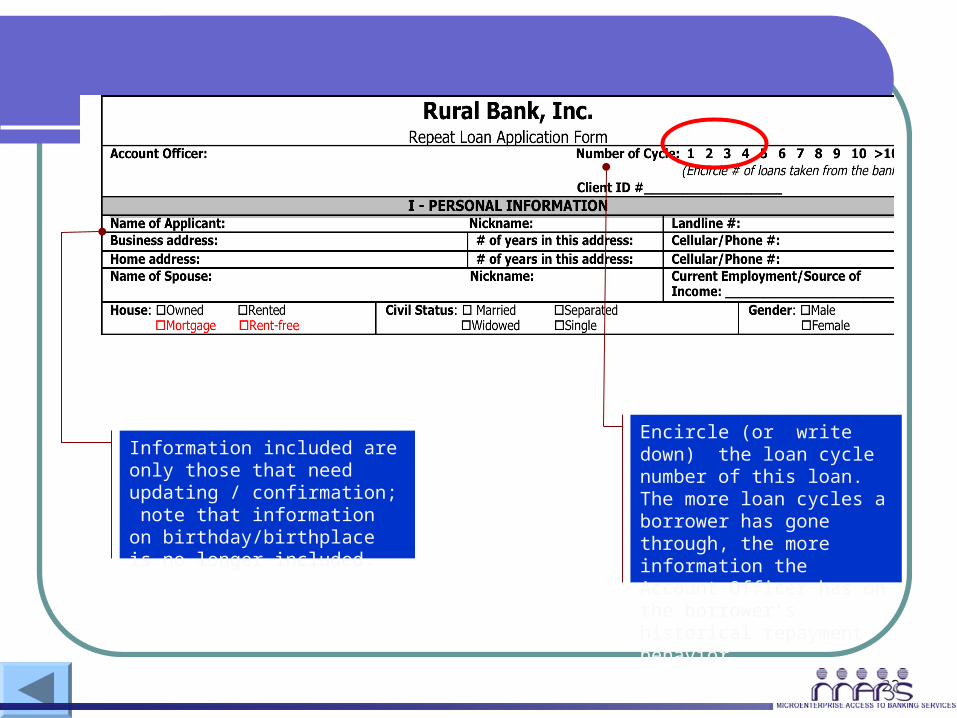

Encircle (or write down) the loan cycle number of this loan. The more loan cycles a borrower has gone through, the more information the Account Officer has on the borrower’s historical repayment behavior.

Information included are only those that need updating / confirmation; note that information on birthday/birthplace is no longer included.

23

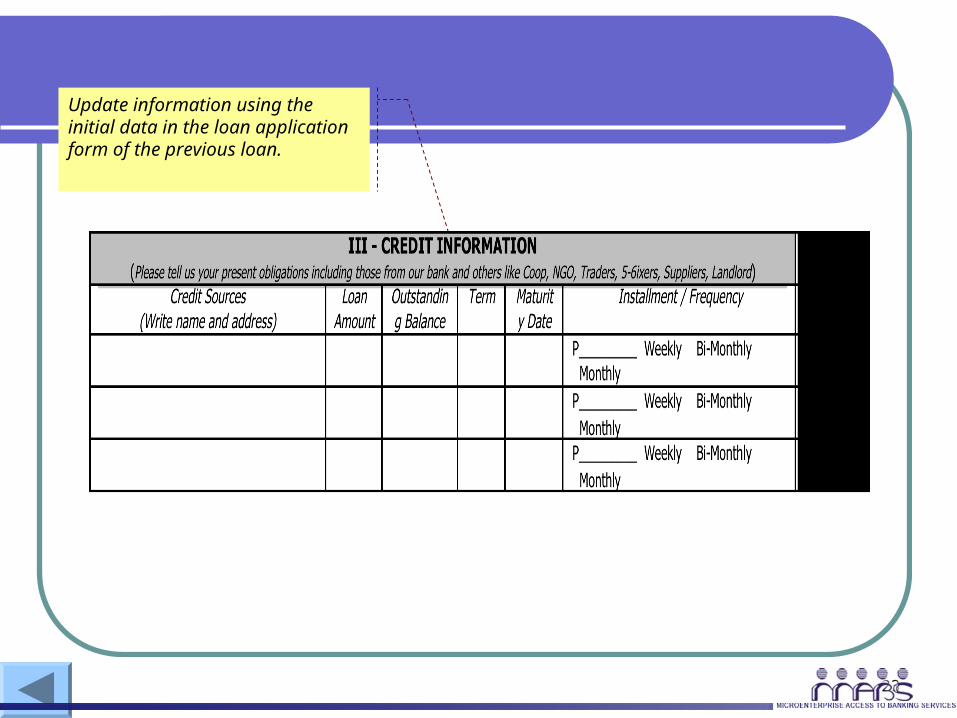

Update information using the initial data in the loan application form of the previous loan.

24

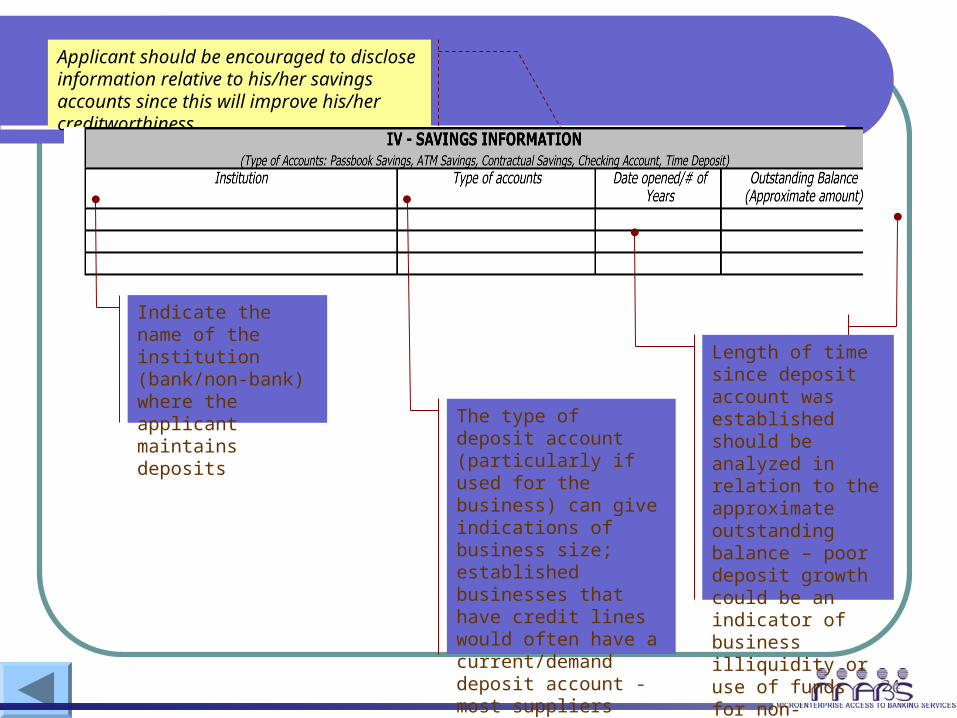

Applicant should be encouraged to disclose information relative to his/her savings accounts since this will improve his/her creditworthiness

Length of time since deposit account was established should be analyzed in relation to the approximate outstanding balance – poor deposit growth could be an indicator of business illiquidity or use of funds for non-business expenses

The type of deposit account (particularly if used for the business) can give indications of business size; established businesses that have credit lines would often have a current/demand deposit account - most suppliers require post-dated checks-PDCs)

Indicate the name of the institution (bank/non-bank) where the applicant maintains deposits