1. the purpose of financial statements/final accounts is

TRANSCRIPT

1. The purpose of financial statements/final accounts is to ascertain-

a) Profit

b) Profit or Loss

c) Value of assets

d) Profit or loss and financial position

2. Financial statements are prepared–

a) at the end of calendar year

b) at the end of accounting year

c) at the end of assessment year

d) on every Diwali

3. Gross profit is ascertained by preparing–

a) Trial Balance

b) Trading a/c

c) Profit & Loss a/c

d) Balance Sheet

4. Suspense a/c appearing in the Trial Balance is shown in the –

a) Ledger

b) Trading a/c

c) P & L a/c

d) Balance Sheet

5. A bank pass book is copy of:

a) A customer’s account in the bank’s books

b) Cash book relating to bank column

c) Cash book relating to cash column

d) A bank’s account in the customers books

6. A bank reconciliation statement is prepared to know the causes for the difference between:

a) Balance as per cash column of cash book and pass book

b) Balance as per bank column of cash book and pass book

c) Neither of the two

d) (b) and (a)

7. Bank reconciliation statement is:

a) A ledger account

b) Part of the cash book

c) A statement separately prepared to find out the causes of difference between bank column of cash book and pass book

d) None of the above

8. Balance Sheet is prepared to know-

a) Gross Profit

b) Net Profit

c) Balances of Accounts

d) Financial Position

9. The statements showing assets and liabilities is-

a) Trial Balance

b) Trading a/c

c) P & L a/c

d) Balance Sheet

10. Working Capital is --

a) Proprietor’s own Capital

b) Borrowed Capital

c) Amount of Sale

d) Current Assets – Current Liabilities

11. Which one of the following statements is ‘False’?

a) Capital = Assets – Liabilities

b) Balance Sheet is an account

c) Balance Sheet may be prepared half-yearly or annually

d) Cash will be the first item is assets side of balance sheet if assets are arranged in the order of liquidity

12. Sales are equal to-

a) Gross profit – Cost of goods sold

b) Gross profit + Cost of goods sold

c) Cost of goods sold – Gross profit

d) Gross profit – Net profit

13. A bank reconciliation statement is prepared with the help of :

a) Bank pass book and bank column of cash book

b) Bank pass book and cash column of cash book

c) Bank pass book

d) Cash book of the party

14. A bank reconciliation statement is prepared by a:

a) Bank

b) Customer

c) Creditor

d) Debtor

15. A credit entry in pass book means a credit entry in cash book:

a) True

b) False

16. When a customer directly pays into bank, bank account is debited:

a) True

b) False

17. Normally if cash book shows a debit balance, pass book also show a debit balance:

a) True

b) False

18. Goods distributed as samples should be credited to-

a) Purchases a/c

b) Sales a/c

c) Advertisement a/c

d) P & L a/c

19. Interest on Drawings is –

a) Expenditure for the business

b) Income for the business

c) Asset for the business

d) Liability for the business

20. Outstanding Salaries are shown as-

a) Expenditure

b) Income

c) Asset

d) Liability

21. Which one of the following statements is ‘True’?

a) Stock at the end appearing in the trial balance is taken only to the Balance Sheet

b) All intangible assets are fictitious assets

c) Goods taken out by the proprietor from the business for personal use are credited to Sales a/c

d) The current liabilities mean the liabilities which are payable after a year

22. Which one of the following statements is ‘False’?

a) Creating a reserve for discount on creditors is not strictly according to the principle of conservatism

b) ‘Salary paid in advance’ is not an expense because it neither decreases assets nor increases liabilities

c) Stock at the end appearing in the trial balance is taken only to Balance Sheet

d) The terms ‘Accrued Income’ and ‘Income received in advance’ are the same thing.

23. For dishonored cheque deposited in the bank, bank account is credited:

a) True

b) False

24. A bank reconciliation statement is prepared periodically to find out the causes of difference between the balances of cash book and pass book:

a) True

b) False

25. A bank pass book shows credit balance of Rs.6200. Intt. Amounting to Rs. 200 has been credited in the pass book but not yet entered in cash book. To reconcile the same with cash book, from the pass book balance, the said amount shall be:

a) Added

b) Deducted

c) No treatment

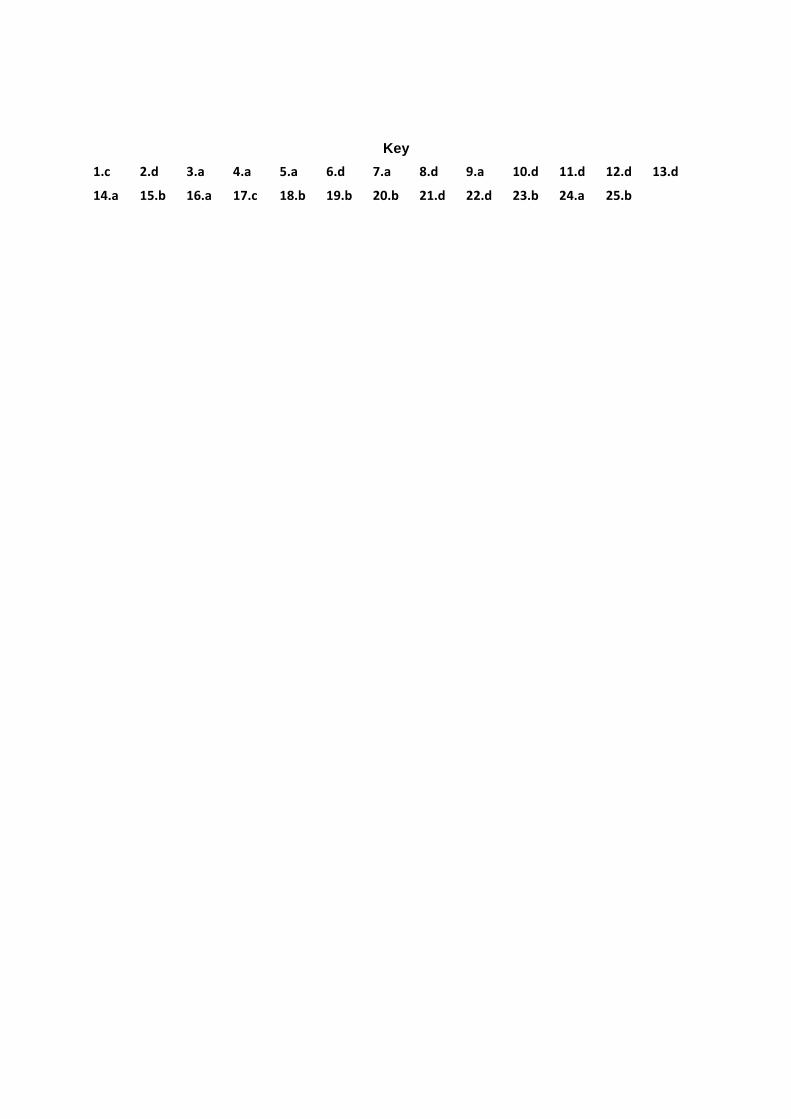

Key

1.d 2.b 3.b 4.d 5.a 6.b 7.c 8.d 9.d 10.d 11.b 12.b 13.a

14.b 15.b 16.a 17.b 18.a 19.b 20.d 21.a 22.d 23.a 24.a 25.b

1. As per cash book of customer the balance with bank is Rs. 5610 (debit) and bank has paid LIC premium of Rs. 150 to comply a standing instruction. To reconcile the cash book with bank pass book, the said amount shall be: a) Added

b) Deducted

c) No change shall be made

2. Stock appearing outside the Trial Balance will be shown in-

a) Trading a/c

b) P & L a/c

c) Balance Sheet

d) Trading a/c Balance Sheet

3. The balance of petty cash is-

a) An expense

b) An income

c) An asset

d) A liability

4. An asset has-

a) Debit balance

b) Credit balance

c) Sometimes debit and sometimes credit balance

d) Debit balance in the beginning and credit balance at the end

5. A liability has –

a) Debit balance

b) Credit balance

c) Sometimes debit and sometimes credit balance

d) Credit balance in the beginning and credit balance at the end

6. There is overdraft of Rs. 5500 as per cash book of the customer and a cheque is deposited with the bank for Rs. 400, which is not credited by the bank. What will be balance in pass book of the bank? a) Rs. 5100

b) Rs. 5500

c) Rs. 5900

d) None of the above

7. As per pass-book there is bank overdraft of Rs. 6500. A cheque is issued for Rs. 3000 but it has not been presented. What shall be balance as per cash book? a) Rs. 3500

b) Rs. 6500

c) Rs. 9500

d) None of the above

8. As per cash book there is overdraft of Rs. 210. Bank recovers commission of Rs. 39. What shall be balance in the bank pass book?

a) Rs. 210

b) Rs. 171

c) Rs. 249

d) None of the above

9. Overdraft balance as per cash book of the customer is Rs. 5500. Bank charges an interest of Rs. 60 and a cheque has been issued for Rs. 1350 but it is not presented for payment. What will be balance in the bank pass book?

a) 4210

b) 4150

c) 4090

d) 5440

10. Net profit is –––– of the firm:

a) an asset

b) a liability

c) an expenditure

d) an extra ordinary income

11. Net loss is –––– of the firm

a) an asset

b) a liability

c) an income

d) an extra ordinary expenditure

12. Which of the following is a contingent liability?

a) Bank overdraft

b) Short-term loan

c) Long-term loans

d) Liability on bills discounted

13. Goods costing Rs. 8,000 were damaged by fire. Insurance company admitted a claim of Rs. 6,500. Profit & Loss a/c will be debited with–

a) Rs. 8,000

b) Rs. 6,500

c) Rs. 14,500

d) Rs. 1,500

14. A manager is entitled to receive a commission @ 5% on net profit after charging commission. Gross profit of the firm is Rs. 2, 00,000 and selling and administrative expenses amount to Rs. 1, 47,500. His commission will be-

a) Rs. 5,250

b) Rs. 2,625

c) Rs. 2,500

d) Rs. 10,000

Solution :

Net Profit = Gross Profit – Selling and administrative expenses

= 2,00,000- 1,47,500=Rs. 52,500

Manager’s Commission after charging such commission

= Net Profit x �

�����.�.,����

= 52, 500 x ���

� = Rs. 2,500

15. There is overdraft of Rs. 10000 as per bank pass book. A cheque is issued but not paid into bank for Rs. 20000 and cheque of Rs. 15000 is issued but not cleared. What shall be balance in cash book?

a) 5000

b) 25000

c) 45000

d) 20000

16. A firm had deposited with the bank Rs. 20000 cash but bank credited this amount to another account. A cheque issued by the firm for Rs. 15000 has been dishonored due to the above reason. The balance as per cash book is Rs. 6012. What is the balance as per pass book?

a) 11012

b) 21012

c) 41012

d) 1012

17. While examining its bank account, a company finds that as per bank statement of account, the balance is Rs. 210000 in their cash credit account. It is observed that bank ahs debited Rs. 1950 as interest during the month and credited Rs. 14000 deposited directly by a customer to the company for repayment o his dues. The bank did not remit Rs. 1200 for which an instruction was sent by the company to the bank. What is the balance as per cash book?

a) 223250

b) 253250

c) 243250

d) 233250

18. The output of financial accounting is –

a) the measurement of accounting income

b) the measurement of taxable income

c) the preparation of financial statements

d) the preparation of financial position

19. Income of a business concern-

a) is measured as per the requirements of tax authorities

b) is measured as per the articles of association

c) is subjective and influenced by the wishes of the accountant

d) can never be measured objectively to give an accurate figure

20. The basic objective of accounting is to-

a) satisfy the legal requirements

b) satisfy the listing requirements of stock exchanges

c) report to the shareholders

d) provide quantitative information to the users of financial statements

21. Information about the performance of a business enterprise is disclosed by-

a) Trading a/c

b) Trading a/c P & L a/c

c) Balance Sheet

d) Cash Flow Statement

22. The cash book of the firm shows credit balance of Rs. 90120 with the bank and on comparison of the bank statement with cash book, following is observed:

a) A cheque of Rs. 1200 has been debited twice by the bank.

b) A cheque of Rs. 12090 deposited with the bank has been dishonored and bank recovered Rs. 120 on account of returning charges.

c) Rs. 16 has been credited on account of postal charges refunded by the bank which were double charged by them earlier.

Find the balance as per pass book.

a) 102514

b) 103514

c) 105314

d) 115014

23. Your firm’s account pass book shows a credit balance of Rs. 16000 but you observe that firm had issued a cheque of Rs. 1600 which bank had debited to your personal account, a dividend of Rs. 200 has been credited in the account. What will be balance as per cash book?

a) 12400

b) 14400

c) 14200

d)16200

24. While preparing reconciliation statement, an accountant observed that following entries are disagreement between pass book and firm’s cash book:

a) A personal cheque of Rs. 3000 issued by the partner has been paid from firm’s account

b) A bank draft of Rs. 3950 was got issued from bank account and bank had debited commission of Rs. 60 on that account.

c) Bank and recovered Rs. 200 on one occasion and Rs. 300 on another occasion on account of inspection charges.

Pass book presently shows a debit balance of Rs. 319200, what should be the balance as per cash book.

a) 315460

b) 314560

c) 315640

d) 340640

25. External reporting is the result of-

a) Financial Accounting

b) Management Accountant

c) Cost Accounting

d) Human Resource Accounting

Key

1.b 2.d 3.c 4.a 5.b 6.c 7.c 8.c 9.a 10.b 11.a 12.d 13.d

14.c 15.b 16.d 17.a 18.c 19.c 20.d 21.b 22.b 23.c 24.c 25.a

1. Special purpose financial statements are prepared by-

a) Financial Accounting

b) Management Accountant

c) Cost Accounting

d) Both (a) and (b)

2. Assets are usually shown in the Balance Sheet at-

a) revalued cost

b) replacement cost

c) net realizable cost

d) unexpired cost

3. The most acceptable way of measuring income is-

a) to match the costs with revenue

b) to apply normal rate of return on capital invested

c) to apply the average rate of return in industry on capital employed

d) to find out the difference in net worth as on two dates

4. A commercial limited period activity by two or more persons, not being a partnership in which some activity is carried on, is called :

a) Partnership

b) Joint stock company

c) Joint venture

d) Joint ownership

5. A firm’s current account with bank shows a balance of Rs. 43010. Firm had deposited cheques of Rs. 15000 out of which a cheques of Rs. 6000 only have been credited to their account. Similarly, cheques worth Rs. 15000 have been paid by the bank out of total cheques of Rs. 17000 issued by them. What will be balance as per cash bank, if bank had also debited Rs. 10 as charges for returned cheques?

a) 50020

b) 50200

c) 50220

d) 52020

6. A trial balance is a:

a) Real account

b) Nominal account

c) Personal account

d) List of balances

7. The trial balance checks:

a) Arithmetical accuracy of books

b) Honesty of the book keeper

c) Accuracy of the book keeper

d) None of the above

8. Trial balance is prepared to detect:

a) Errors of omission

b) Errors of principle

c) Errors of commission

d) None of the above

9. Balance Sheet is prepared primarily with the following group in view –

a) Owners

b) Debtors

c) Creditors

d) Management

10. Goodwill is an example of-

a) Fixed asset

b) Factious asset

c) Current asset

d) Intangible fixed asset

11. Which one of the following is example of an intangible asset?

a) Building

b) Investments

c) Discount on issue of shares and debentures

d) Copyrights

12. Which one of the following is an example of current asset?

a) Machinery

b) Vehicles

c) Patents

d) Prepaid expenses

13. Which one of the following is an example of current liability?

a) Share Premium

b) Workmen’s Compensation Fund

c) 10% Debentures

d) Bank Overdraft

14. In trial balance, cash in hand will indicate:

a) a debit balance

b) a credit balance

c) It could be any

d) None of the above

15. In trial balance the wages outstanding will show a:

a) Debit balance

b) Credit balance

c) Nil

d) None of the above

16. An entry of Rs. 500 wrongly posted to the wages account instead of building account is an:

a) Error of principle

b) Error of commission

c) Error of omission

d) None of the above

17. Sale of Rs. 50000 on cash basis not recorded in to sales book:

a) Error of principle

b) Error of commission

c) Error of omission

d) None of the above

18. Total of purchase book undercast by Rs. 800:

a) Error of principle

b) Error of commission

c) Error of omission

d) All the above

19. Balance Sheet is –

a) a statement showing flows of funds

b) a statements of position

c) a statements showing income

d) a statements showing only current assets

20. The excess of current assets over current liabilities is called-

a) Gross working capital

b) Net working capital

c) Gross tangible worth

d) Net tangible worth

21. Unexpired income as on the date of Balance sheet, is shown as-

a) an expenditure

b) a revenue

c) an asset

d) a liability

22. Both assets and owners’ equity would be increased by –

a) Proprietors’ drawings

b) Payment from debtors

c) Payment to creditors

d) Capital brought in by the proprietors

23. An entry of Rs. 68 was debited to Ravinder’s account as Rs. 86. This will be:

a) Error of principle

b) Error of commission

c) Error of omission

d) All the above

24. Stationery worth Rs. 50 used by the proprietor debited to office expenses account. It is an:

a) Error of principle

b) Error of commission

c) Error of omission

d) All the above

25. Wrong balancing of an account is:

a) Error of principle

b) Error of commission

c) Error of omission

d) All the above

Key

1.c 2.d 3.a 4.a 5.a 6.d 7.a 8.d 9.a 10.d 11.d 12.d 13.d

14.a 15.b 16.a 17.c 18.b 19.b 20.b 21.d 22.d 23.b 24.a 25.b

1. Goods returned by the customer worth Rs. 700 taken into stock but no entry passed. This is an:

a) Error of principle

b) Error of commission

c) Error of omission

d) All the above

2. Bills receivable book is a part of:

a) Journal

b) Ledger

c) Profit and loss account

d) Balance sheet

3. a bills receivable book is a :

a) Principle book

b) Subsidiary book

c) Book containing blank forms for writing bill of exchange

e) None of the above

4. Bills payable book is part of the :

a) Journal

b) Ledger

c) Profit and loss account

d) Balance sheet

5. If Ravi’s acceptance that was endorsed by us to Saleem is dishonored, the amount should be debited in our books to :

a) Saleem account

b) Ravi account

c) Bills receivable account

d) Bills payable account

6. The net worth of a limited company is equal to-

a) Fixed Assets – Fixed Liabilities

b) Current Assets – Current Liabilities

c) Fixed Assets – Current Liabilities

d) The total of shareholders’ funds

7. An outstanding expense can best be described as an amount-

a) not paid and not currently matched with revenue

b) not paid and currently matched with revenue

c) paid and not currently matched with revenue

d) paid and currently matched with revenue

8. The term’ Reserve’ in financial statements signifies-

a) the amount of provision for bad debts

b) the amount of provision for taxation

c) the amount set apart for contingent liabilities

d) the amount of profits set apart for general specific purpose

9. If the total assets increased by Rs. 1,50, 000 and the total liabilities increased by Rs. 60, 000 in the same accounting period, the capital in that period would-

a) decrease by Rs. 60, 000

b) decrease by Rs. 90, 000

c) increase by Rs. 60,000

d) increase by Rs. 90, 000

10. Outstanding expenses appearing in the trial balance are shown in-

a) Debit side of P & L a/c only

b)Credit side of P & L a/c only

c) Assets side of Balance Sheet only

d) Liabilities side of Balance Sheet only

11. Bills receivable account is an example of :

a) Personal account

b) Real account

c) Nominal account

d) Both personal and real a/c

12. Retiring a bill under rebate means :

a) Making payment for the bill before the due date

b) Making payment for the bill after due date

c) Dishonoring the bills

d) None of the above

13. A pays Rs.300 to B on maturity of the bill he had accepted. The amount will be credited in cash account and debited to:

a) A

b) B

c) Bills receivable account

d) Bills payable account

14. A profit and loss account is prepared:

a) For a certain period

b) At a particular point of time

c) On a fixed date

d) On a particular month

15. Which one of the following statements ‘True’?

a) The accounting policies do not differ from enterprise to enterprise

b) Reserves of a business enterprise always represent the amount which it can spend readily

c) The figures as shown in the balance sheet, are the future estimated values of assets and liabilities

d) Balance Sheet is a statements of assets and liabilities as on a given date

16. Which one of the following statements is ‘False’?

a) A Balance Sheet can only indicate the items that can be expressed in terms of money

b) Security, capable of being realized ad not held with the intention of retaining it for more than one year, is a current asset

c) An iron safe is a fixed asset for a medical shop and a current asset for s shop dealing in iron safes

d) The closing stock of office stationery is credited to Trading a/c

17. A balance sheet discloses the financial position of an entity:

a) For a given period

b) On a particular point of time

c) On a certain fixed day

18. Profit and loss account shows the :

a) Profit earned by the business

b) Total capital employed

c) Profit and loss through sale of assets

d) Profit or loss earned by the business

19. Balance sheet shows the :

a) Profit earned by the business

b) Financial position of a business

c) Balance of all accounts

20. Expenses relating to sale of goods are shown in:

a) Trading account

b) Manufacturing account

c) Profit and loss account

d) Balance sheet

d) None of the above

d) Loss made by the business

21. Stock in trade is:

a) A current asset

b) a fixed asset

c) An intangible asset

d) A fictitious asset

22. Valuation of closing stock is at:

a) Cost price

b) Market price

c) Realisable value

d) Whichever is lower of the three

23. Closing stock is recorded in:

a) Balance sheet and trading account

b) Balance sheet only

c) Profit and loss account only

d) None of the above

24. If closing stock appears in the trial balance, it is transferred to :

a) Trading account

b) Profit and loss account

c) Balance sheet

d) Trading a/c and balance sheet

25. Marshalling of balance sheet:

a) Ordering of its assets and liabilities

b) Totalling of its assets and liabilities

c) both the above

d) None of the above Key

1.c 2. B 3.b 4.b 5.b 6.d 7.b 8.d 9.d 10.d 11.a 12.a

13.d 14.a 15.d 16.d 17.b 18.d 19.b 20.c 21.a 22.d 23.a 24.c 25.a

1. Which does not form part of the term financial expenses:

a) Discount allowed

b) Interest on loans

c) Interest on capital

d) Legal expenses

2. which of the following should not form part of profit and loss account:

a) Salaries

b) Insurance paid

c) Carriage inward

d) Selling expenses

3. Premium paid on the life policy of the proprietor is debited to Profit & Loss Account. (True/False)

4. The closing stock of office stationery is credited to Trading Account.

(True/False)

5. Provision for discount on debtors is shown on debit side of Profit & Loss Account. (True/False)

6. Income received in advance and unearned income are different items.

(True/False)

7. Drawings Account is a real account.

(True/False)

8. Outstanding Expenses Account is a nominal account.

(True/False)

9. Prepaid Expenses Account is a representative personal account.

(True/False)

10. Goods distributed as samples should be credited to Purchases Account.

(True/False)

11. A revenue expenditure has been treated as a capital expenditure. This error is :

a) Error of principle

b) Error of omission

c) Error of commission

d) Compensating error

12.A transaction is not recorded in the books, this is :

a) Error of principle

b) Error of omission

c) Error of commission

d) Compensating error

13. An entry is incorrectly recorded either wholly or partially by incorrect posting, calculation, casting or balancing:

a) Error of principle

b) Error of omission

c) Error of commission

d) Compensating error

14. Gross profit + Opening stock + Purchases + Direct expenses – Sales = –––––

15 . The arrangement of assets and liabilities in the balance sheet in liquidity or permanence order , is called––––

16. Sales-tax charged from customers and payable to the authorities, is a –––––

17. Indirect expenses are shown in the debit side of ––––

18. Final accounts are prepared with the figures taken out from–––––

19. A heavy amount spent on advertisement which will benefit the concern for many years, is a ––––– expenditure

20. Accrued income is ––––––––

21. When error is counter-balanced by another error in such a way that it is disclosed by trial balance, it is :

a) Error of principle

b) Error of omission

c) Error of commission

d) Compensating error

22. Machinery purchased worth Rs. 25000 has been debited to purchases account. This entry can be rectified:

a) Debit machinery .account and credit cash account

b) Debit purchase account to cash account

c) Debit machinery account and credit purchases account

d) None of the above

23. The agreement of trial balances means fulfillment of the following objectives:

a) That both the aspect of each transaction i.e. debit and credit are recorded

b) That the books are arithmetically accurate

c) a and b both

d) None of the above

24. Mr. X is debtor of Y for Rs. 20, 000 and creditor of Y for Rs. 12,000, His common debit will be –––– :

25. Interest on drawings is deducted from––––– :

Key

1.d 2.d 3.F 4.F 5.T 6.F 7.F 8.F 9.T 10.T 11.a 12.b

13.b 14.c 15. Closing Stock 15. Marshalling 16. Liability

17. (Profit & Loss account) 18. (Trial Balance) 19. (Deferred revenue)

20. Asset 21. d 22.c 23.c 24. (Rs. 12,000) 25. (Capital)

1. Prepaid expenses are shown on –––––– side of Balance Sheet :

2. Interest on drawings is credited to––––– :

3. Provision for doubtful debts created at the end of the year is debited to ––––– and deducted from ––––– in balance sheet.

4. Claim admitted for stock destroyed by fire will be credited to –––– and will be shown on –––– of balance sheet.

5. The agreement of trial balance would not disclose following kinds of errors:

a) Errors of omission

b) Wrong entries in any original records

c) Errors of principle

d) Compensating errors

e) Posting to wrong heads of accounts

f) All the above

6. The total Returns Inwards Book has been added Rs. 90 short. The debit side of trial balance presently shows a total of Rs. 200090. How much should it actually be?

a) 200000

b) 200180

c) 200910

d) None

7. A credit sale of Rs. 20000 to Ramesh wrongly debited to Suresh’s Account. The credit side of trial balance is showing a total of Rs. 1980000. What is should be?

a) 200000

b) 1960000

c) 1980000

d) Any of above

d) None of the above

8. Machinery worth Rs. 25,0000 purchased on credit has been wrongly recorded in the Purchases book of the firm. Which accounts will be debited and credited to rectify this transaction?

a) Debit machinery/purchases

b) Debit purchases/credit machinery

c) Debit purchases/credit repairs to machinery

9. –––––– is peculiar of banking company accounts :

a) A. T. M

b) Bank Draft

c) Slip System

d) Cheque Book

10. The various items of assets in the Balance Sheet of a banking company

a) liquidity

b) permanency

c) tangibility

d) floating

11. Bills Receivables being Bills for Collection appear on – side of Balance Sheet of banking company

a) only assets side

b) only liabilities side

c) both sides

d) sometimes on assets side and sometimes on liabilities side

12. Rebate on bills discounted for a banking company is–

a) an expense

b) an income

c) a banking asset

d) None of the above

d) a liability

13. A non-banking asset must be disposed of by the banking company within–

a) two years

b) five years

c) seven years

d) one year

14. An entry of Rs.5000, relating to the Bills Receivable book has been posted to the debit of Bills Payable Account. The debit and credit sides of the trial balance show a total of Rs. 205000. What should be the correct total?

a) 200000

b) 210000

c) 215000

d) 195000

15. Depreciation amounting to Rs. 1500 on machinery has not been posted to the Depreciation account. The debit side of trial balance shows a total to Rs. 198500. What it should be?

a) 197000

b) 195500

c) 200000

d) 201500

16. A credit purchases of Rs. 1500 from Ramesh had been correctly entered in Purchases book but was posted As Rs. 150 in Ravinder’s Account. The credit side of trial balance of the firm is showing total at Rs. 401350. What it should be?

a) 401350

b) 400000

c) 402700

d) 404050

17. Rs. 23300 spent by a firm for repairs of its building has been debited to Building Account. Pass the journal entry for rectification of its:

a) Debit repairs/credit cash

b) Debit building /credit cash

c) Debit building /credit repairs

18. The formats of the Profits & Loss Account and Balance Sheet in the case of banking company have been revised w.e.f-

a) 1st April, 1949

b) 1st April, 1991

c) 1st April, 1992

d) 1st April, 2000

19. This item is not included in Schedule 13 of Profit & Loss Accountant of a bank-

a) Income on investments

b) Interest on advances

c) Interest on borrowing of R.B.I

d) None of the above

20. The regulation of banking in India before 1936 was done-

a) Under Indian Banking Companies Act

b) Under Banking Regulation Act

c) Under Companies Act

d) All of the above

21. Fourteen major banks were nationalized in the year-

a) 1969

b) 1971

c) 1973

d) 1993

22. In the amended formats of final accounts of a bank, the total number of schedules prescribed is-

d) Debit repairs/credit building

a) 8

b) 10

c) 12

d) 16

23. Rs. 139 discount allowed to a customer wrongly credited to Discount Account. Total of debit side of the trial balance shows Rs. 39278. What it should be?

a) 39000

b) 39139

c) 39556

d) 39417

24. Rs. 545 paid for wages debited to Wages Account as Rs. 455. The total of debit side of trial balance is Rs. 91010. What it should be?

a) 91100

b) 90920

c) 90000

d) 90555

25. Rs. 265 paid as salary to a clerk has been debited to his personal account. What shall be the journal entry to rectify the error?

a) Debit cash and credit personal account

b) Debit salary and credit cash account

c) Debit salary and credit personal account

d) Debit personal account and credit cash

Key

1. Asset 2. Profit $ Loss Account 3. Profit & Loss Account; Debtors

4. Profit & Loss Account; assets side 5. F 6.b 7.c 8.a 9.c 10.a 11.c

12.d 13.c 14.b 15.c 16.c 17.d 18.b 19.b 20.c 21.a

22.d 23.c 24.a 25.c

1. An amount of Rs. 300 received from Bhupinder which was written off as bad debt last year, has been credited to his account. Pass the journal entry to record this transaction.

a) Debit Bhupinder and credit bad debt recovered account

b) Debit cash and credit bad debt recovered account

c) Debit bad debt recovered account and credit cash

d) Debit Bhupinder account and credit cash

2. Indian Banking Companies Act 1949 was changed in 1996 with the new name of-

a) Indian Banking Regulation Act, 1949

b) Indian Banking Regulation Act, 1966

c) Indian Banking Companies Act, 1966

d) Indian Banking Act, 1949

3. The rate as percentage of net profits of Statutory Reserve to be maintained by a bank under Sec. 17 of Indian Banking Regulation Act, 1949, is-

a) 10%

b) 15%

c) 20%

d) 25%

4. In a banking company, interest on doubtful debts is credited to-

a) Customer’s a/c

b) Interest Suspense a/c

c) Interest a/c

d) Accrued Interest a/c

5. When customer gets a bill discounted , the bank debits Bills Discounted a/c and credits-

a) Customer’s a/c

b) Interest Suspense a/c

c) Interest a/c

d) Accrued Interest a/c

6. Furniture worth Rs. 200 purchased from A on credit, omitted to be recorded in the books. The total side of trial balance is Rs. 20800. What it should be?

a) 20600

b) 20400

c) 21000

d) 21200

7. Goods worth Rs. 150 taken by the proprietor omitted to be recorded in the books. The net balance of capital account is showing a balance of Rs. 44150cr. What it should be?

a) 44300

b) 44000

8. A sale of old machinery amounting to Rs. 750 had been credited to Sales Account. Pass the necessary journal entry.

a) Debit machinery and credit cash

b) debit cash and credit machinery

c) Debit machinery and credit sales

d) Debit sales and credit machinery

9. The discount column of the Cash book representing discount allowed to customers has been over-added by Rs. 10. The total of debit side of trial balance is Rs. 30990. What it should be?

a) 30980

b) 31000

c) 30970

d) 31010

10. Overdraft facility is given by the bank only to such customer who already has-

a) Savings Bank a/c

c) 44450

d) 39850

b) Fixed Deposits a/c

c) Recurring a/c

d) Current a/c

11. In the new formats of final accounts of a Bank, Balance Sheet consists of Schedule No.1 to ––– and Profit & Loss a/c from Schedule No.13 to ––––

a) 5;16

b) 7;16

c) 12;16

d) 10;14

12. Claims against the bank acknowledged as debt is contingent liability and is shown in Schedule No –––– of the balance sheet

a) 5

b) 7

c) 12

d) 15

13. Non-banking assets acquired in satisfaction of claims are shown under Schedule No.11 bearing the heading-

a) Other Assets

b) Non-banking Assets

c) Advances

d) Investments

14. Sales book was overcast by Rs. 1,000. If the total of credit side of trial balance is showing Rs. 82000, what should be the actual balance?

a) 81000

b) 83000

c) 84000

d) 80000

15. An amount of Rs. 250 written off as depreciation on building was not posed to the depreciation Account. What journal entry would be passed?

a) Debit machinery and credit depreciation

b) Debit machinery and credit machinery

c) Debit depreciation and credit cash

d) None of the above

16. An entry of Rs. 95 representing the selling price of goods returned to Rao & Co., has been made in Returns Outwards book and posted. The amount should have been Rs. 80-the invoice value of the goods in question. What should be journal entry?

a) Debit Rao and credit returns outwards

b) Debit returns outward and credit Rao

c) Debit creditors and credit sales

17. The total of the returns Inwards book was added more by Rs. 20. If the debit side of trial balance is showing Rs. 80000, what it should actually show?

a) 79980

b) 80020

c) 80040

d) None of the above

18. When the report of bad financial position of a customer is received, the bank, for the interest due, debits Customer’s a/c credits–

a) Interest a/c

b) Interest Suspense a/c

c) Outstanding Interest a/c

d) Accrued Interest a/c

19. Banks prepare their accounts for the-

a) Calendar year

b) Financial year

d) Debit sales and credit Rao

c) Assessment year

d) Diwali year

20. For a bank, Rebate on bills discounted is an item of–

a) an income

b) an expenditure

c) an accrued income

d) an income received in advance

21. The heading ‘Other Assets’ does not include-

a) gold

b) silver

c) interest accrued

d) inter-branch adjustments (Dr.)

22. Discount amounting to Rs. 100 allowed by the creditors was posted to the debit of the Discount Account. By how much amount will the total of credit side of trial balance increase?

a) Nil

b) 100

c) 200

d) -100

23. Sale of Rs. 300 to A omitted to be recorded in the books. If the existing balance of debit side of trial balance is Rs. 20000, what will be the total of credit side, presently?

a) 19700

b) 19600

24. Rs. 100 is posted to the Depreciation Account as depreciation on furniture but was not posted to Furniture Account. If total of debit side of the trial balance is Rs. 12100. What it should be after rectification of the error.

a) 12100

b) 12200

c) 20300

d) 20000

c) 12000

d) None of the above

25. A non-banking asset is-

a) furniture, fixtures and fittings

b) office equipment

c) money at call and short notice

d) an asset acquired from the debtors in satisfaction of claims against them

Key

1.a 2.a 3.c 4.b 5.a 6.c 7.b 8.d 9.a 10.d 11.c 12.c 13.a

14.a 15.d 16.b 17.a 18.b 19.b 20.d 21.a 22.c 23.c 24.c 25.d

1. When income of a bank is to be recognized on cash basis, a distinction must be made between –

a) Current and non-current assets

b) Banking and non-banking assets

c) Monetary and non-banking assets

d) Performing and non-performing assets

2. A non-performing asset of a bank is-

a) Cash balance

b) Cash balance with RBI

c) Money at call and short notice

d) An asset which ceases to generate income

3. Banks show the Provision for Income-tax under the head-

a) Deposits

b) Borrowings

c) Contingent Liabilities

d) Other Liabilities and Provisions

4. Purchases Book is overcast by Rs. 1,000. What would be amount of the gross profit which is shown as Rs. 9000, presently?

a) 10000

b) 8000

c) 9000

d) None

5. Returns outwards Book is overcast by Rs. 100. Gross profit is Rs. 12900 presently. What it should be?

a) 12800

b) 13000

c) 14000

d) None

6. Machinery was purchased on credit for Rs. 5,400 but journal entry was passed for Rs. 4,500. What will be amount of gross profit of the firm, if presently it is Rs. 8100?

a) 8100

b) 9000

c) 7200

d) None of the above

7. Rs. 350 received from Surinder in settlement of account, posted to the credit of Sales Account. Pass the journal entry to rectify the error.

a) Debit sales and credit Surinder

b) Debit Surinder outward and credit cash

c) Debit cash and credit Surinder

d) Debit sales and cash

8. Which one of the following statements is ‘True’?

a) State Bank of India is not a nationalized bank

b) Schedule No.9 ,10, 11, and 12 are shown in Profit & Loss Account of a bank

c) Rebate ob bills discounted is the discount received by bank in the previous year

d) Bank’s advances included loans, cash credits, overdrafts, and discounting and purchase of bills

9. Which one of the following statements is ‘False’?

a) A bank must transfer at least 20% of net profits of the year prior to declaration of dividend to statutory reserve, unless the central government condones this binding

b) Slip system in a bank is not a different accounting

system but a method of rapid posting in the books of account

c) Schedule 6 deals with ‘Other Liabilities and Provisions’ of a bank

d) State Bank of India is a nationalized bank

10.No adjustment entry was passed for an amount of Rs. 300 relating to outstanding salary. The gross profit which is presently Rs. 9200 will come down to Rs. –––

a) 8900

b) 9500

c) 9200

d) No change

11. Rs. 100 paid for purchase of stationery was wrongly debited to Purchases Account. The amount of net profit which is shown as Rs. 9100 would actually be Rs. –––––?

a) 9100

b) 9200

c) 9000

d) None of the above

12. Sale of Rs. 1,800 to A omitted to be posted to his account. The debit side total of trial balance which is Rs. 98100 presently should actually be Rs. –––––?

a) 97300

b) 99900

c) 98100

d) None of the above

13. Amount received from A but wrongly credited to B’s account Rs. 10000. The entry can be corrected by:

a) Debit cash account to B

b) Debit cash account to A

c) Debit B and credit A

14. Capital Reserve of bank shall include any account regarded as fee for distribution through Profit & Loss Account:

(True/False)

15. Surplus on translation of the financial statements of foreign branches of bank is not a revaluation reserve.

(True/False)

16. Interest payable by bank on deposits which has accrued but not due, should be shown under other liabilities.

d) None of the above

(True/False)

17. Matured time deposits and cash certificates in a bank should not be treated as demand deposits.

(True/False)

18. Inter-office transactions of a bank should be shown as borrowings.

(True/False)

19. If any instrument for remittance of funds (like drafts, cheques, pay orders, etc.) remains uncashed on the day of preparation of final accounts, should be shown under the heading ‘Bills Payable’.

(True/False)

20. In cash credit facility, the borrower is required to draw at once the whole amount of the cash credit limit and start paying interest on that.

(True/False)

21. Machinery sold worth Rs. 25000 credited to sales account. What shall be rectification entry:

a) Debit cash account to sales account

b) Debit cash account to machinery account

c) Debit sales account to machinery account

d) None of the above

22. If there is an error in a nominal account, it shall directly effect:

a) Profit and loss account

b) Balance sheet

c) Both the above

d) None of the above

23. If there is an error in a real account, it shall affect:

a) Profit and loss account

b) Profit/loss appropriation a/c

c) Balance sheet

d) None of the above

24. If there is an error in a personal account, it shall affect:

a) Profit and loss account

b) Trading account

c) Balance sheet

d) All the above

25. In discounting of bills, net amount after deducting the amount of discount is credited by bank to the customer’s amount.

(True/False)

Key

1.d 2.d 3.d 4.a 5.a 6.a 7.a 8.d 9.c 10.d 11.a 12.b 13.c

14.F 15.T 16.F 17.F 18.F 19.T 20.F 21.c 22. a 24.c 25.T

1. Cash credit is an arrangement whereby borrower is allowed to borrow money up to a certain limit.

(True/False)

2. Term loans are usually for a fixed term not exceeding one year.

(True/False)

3. An advance which remains out of order for 90 days is a non-performing asset. (NPA). (True/False)

4. In a term loan, if interest or instalments remains overdue for more than 180 days, it is a non-performing asset with just (NPA).

(True/False)

5. In bills purchased /discounted account, if bills remain overdue and unpaid for 120 days, is a non-performing asset (NPA).

(True/False)

6. A standard asset is that which is a performing asset with just normal risk attached to it.

(True/False)

7. The provisioning requirement for a sub-standard asset is 0.25%. (Correct answer is 10%).

(True/False)

8. Compensating errors will cause a difference in trial balance:

a) True

b) False

c) Incomplete statement

d) None of the above

9. Only one sided errors affect the trial balances:

a) True

b) False

c) Incomplete statement

d) None of the above

10. Only double sided errors are rectified through suspense account?

a) True

b) False

c) Incomplete statement

d) None of the above

11. Every error effects the agreement of trial balance:

a) True

b) False

c) Incomplete statement

d) None of the above

12. The securities held for trading are to be sold within 90 days.

(True/False)

13. The profit/loss on securities ‘held to maturity’ is ultimately transferred to Capital Reserve and need not be marked to market.

(True/False)

14. –––––– of posting is peculiar of banking company accounts

15. The various items of assets in the balance sheet of a banking company are arranged according to –––– order .

16. The investment under ‘held to maturity’ is like ‘old permanent category’ and should not exceed 25% of bank’s total investments.

(True/False)

17. The ‘balancing of books’ in a bank refers to preparation of balance sheet.

(True/False)

18. In a bank, the amount of advantage given to an employee is debited to Sundry Expenses Account.

(True/False)

19. A banking company cannot grant loan to its directors.

(True/False)

20. Errors of omission arise due to complete omission of the transaction in the books or omission of posting to the ledger:

a) True

b) False

c) Incomplete statement

d) None of the above

21. Under or over casting of a subsidiary book is an example of error of commission:

a) True

b) False

c) Incomplete statement

d) None of the above

22. What will be adjustment entry for closing stocks:

a) Debit closing stock to trading account

b) Debit closing stocks to balance sheet

c) Closing stocks to profit & loss account

23. What will be adjustment entry for outstanding expenses:

a) Debit expenditure account outstanding expenses

b) Debit outstanding expenses to expenditure

c) Debit expenditure account to balance sheet

24. Rebate on bills discounted is an income for a banking company.

(True/False)

25. Provision for bad and doubtful debts is shown as deduction from interest earned in the Profit & Loss Account of a banking company.

(True/False)

Key

1.T 2.F 3.T 4.T 5.T 6.T 7.F 8.b 9.a 10.b 11.b 12.T 13.T

14. Slip system 15. Liquidity 16.T 17.F 18.F 19.T 20.T 21.T 22.a 23.a 24.F

25.F