1 wolterskluwer august 12, 2003 - amsterdam first half year results 2003

TRANSCRIPT

1

WoltersKluwer

August 12, 2003 - Amsterdam

First Half Year Results 2003

2

Agenda

Highlights HY 2003 R. Pieterse

Cluster/Market Review R. Pieterse

Financials B. Beerkens

Summary, Outlook and Q&A R. Pieterse

3

Highlights

• Challenging economic environment for all clusters impacts revenues and income; EBITA margin under pressure

• Benchmark net profit -26% at constant currencies; (1st quarter 03, -31%)

• Electronic sales increase to 34% of total continuing revenues

• New executive team now in place

• Positive cash flow and tighter working capital control;29% reduction of net debt

• Acceleration of restructuring program and significant cost reductions – at least EUR 70 mln full year

• Organic staff reduction of 500 FTEs already achieved

4

Key Financial HY 03

Constant % Currencies

HY 03 %EUR million

Revenues

Ordinary EBITA

Ordinary EBITA margin %

Benchmark Net Profit

Ordinary EPS before amortization of

intangibles, and exceptionals (fully diluted)

Ordinary free Cash flow

1,609

230

14.3

120

0.42

74

1,917

347

18.1

194

0.66

42

(6)

(24)

(26)

HY 02

(16)

(34)

(38)

5

Organic Growth

Total organic

Acquisitions

Divestments

At constant rates

Currency

Total

HY 03 HY 02

Revenues Ordinary EBITA

% % % % (3.4) 1.5 (18.8) (5.5)

2.7 5.4 1.3 5.8

(4.9) (1.4) (6.8) (0.1)

(5.6) 5.5 (24.3) 0.2

(10.4) 0.5 (9.5) 0.6

(16.0) 6.0 (33.8) 0.8

HY 03 HY 02

6

Electronic Revenues

Internet/ On-line

CD-ROM

Electronic

59

115

174

9

19

28

47

121

168

7

20

27

26

(7)

2

Internet/On-lineCD-ROM

Electronic

136135

271

2526

51

124139

263

2225

47

10(3)

3

%LTB Europe (EUR mln) HY 03 %HY 02%

%LTB NA (USD mln) HY 03 %HY 02%

7

Electronic Revenues

Internet/On-lineCD-ROM

Electronic

610

16

1017

27

69

15

1016

26

02

(2)

Internet/On-lineCD-ROM

Electronic

6825

111

258

33

5833

91

1710

27

44(25)

21

%LTB AsiaPacific(AUDmln) HY 03 %HY 02%

%Health (USD mln) HY 03 %HY 02%

8

Electronic Revenues

Internet/On-lineCD-ROM

Electronic

72

9

62

8

51

6

41

5

4350

43

%Education (EUR mln) HY 03 %HY 02%

9

Rob Pieterse

Chairman Executive Board

Wolters Kluwer nv

Cluster & Market Review

10

LTB Europe

Revenues (EUR) EBITA (EUR)EBITA margin %

62810316.5

62111318.2

(10)(12)

27 4

(12)(2)

7(10)

Million TotalCurrencyAcquisition/DivestmentOrganicHY 02HY 03

Change (mln)

• Growth in revenues and EBITA impacted by disappointing results from UK, Belgium and the Netherlands

• Overall business affected by slow economic conditions;organic performance -1% (flat LY)

• Weak advertising trends cause revenue decline in France and the Netherlands; improving trends in non-advertising revenues in the Netherlands

• Good growth rates for Italy, Scandinavia, CEE, Spain and Teleroute

• Italian and Spanish software strong on back of tax developments

• 28% of revenues are electronic (5% Internet)

NL21%

UK16%

SC3%

BEL9%

GER/ AUS/CEE18%

I T/ SP10%

TLR5%

FR18%

11

LTB Europe

• Key focus on cost reduction

• Major initiatives to address organic growth and infrastructure enhancements

• Aggressive cost management in the UK and management changes

• Strong market positions across Europe; initiatives taken to enhance market share further

12

LTB North America

EBITA margin %

Revenues (USD)(EUR)

EBITA (USD)(EUR)

53148110494

15

-

(112)

(22)

(43)

(42)

(140)

(64)

555621142158

19.6 25.5

Million TotalCurrencyAcquisition/DivestmentOrganicHY 02HY 03

Change (mln)

16%

27%

13%

11%

29%

4%

• Cluster performance negatively impacted specifically by BSI and Aspen

• LIS flat compared to last year despite slow down in transactional markets

• CCH Tax Compliance grew solidly boosted by strong core and accelerated new products; CCH Canada also performed strongly

• Steady underlying performance from CCH overall despite economic conditions; retention rate stabilizing

CCH BSIAspen

CCH LIS

CCH Tax Compliance

CCH Canadian

CCH US Publishing

13

LTB North America

• Electronic revenues 51% of total; Internet/On-line 26%

• Benefits expected in second half from the reorganization of the cluster into customer facing groups, with significant cost reductions, appointment of CEOs and management changes at Aspen back office and finance teams

• Market share set to strengthen as a result of actions taken to upgrade content platform

• New product development and sales and marketing initiatives maintained despite cost reductions

14

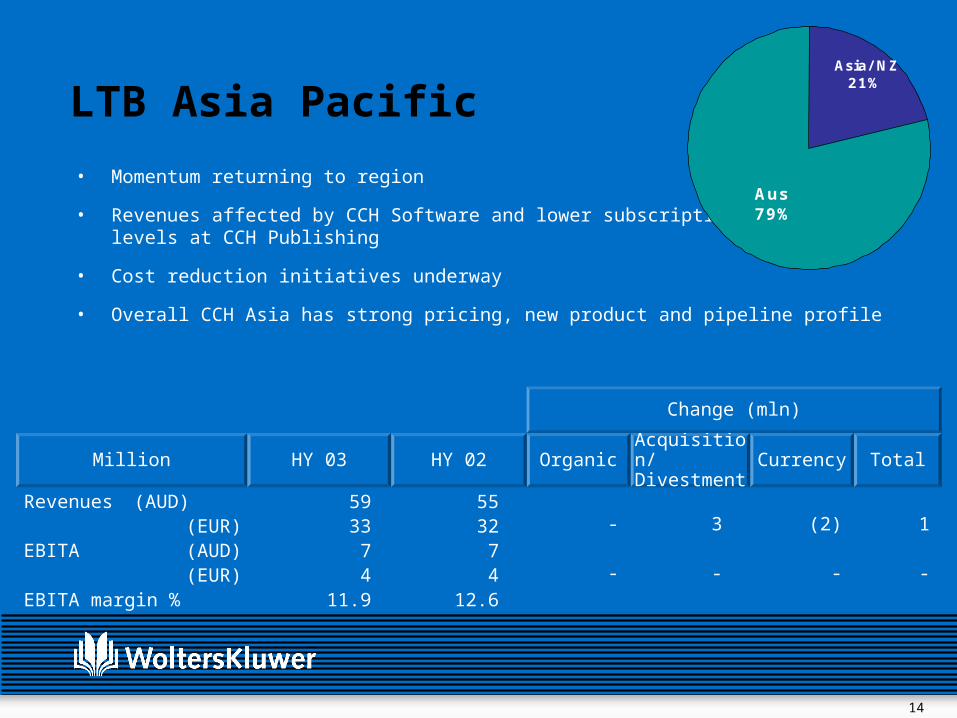

LTB Asia Pacific

• Momentum returning to region

• Revenues affected by CCH Software and lower subscription levels at CCH Publishing

• Cost reduction initiatives underway

• Overall CCH Asia has strong pricing, new product and pipeline profile

Revenues (AUD)(EUR)

EBITA (AUD)(EUR)

EBITA margin %

5933

74

11.9

3

-

(2)

-

-

-

1

-

5532

74

12.6

Million TotalCurrencyAcquisition/DivestmentOrganicHY 02HY 03

Change (mln)

Aus79%

Asia/ NZ21%

15

Health• Professional & Education performing well – strong

revenue and cost management profile especially in Nursing and Health Professional titles

• Good showing from Clinical Tools in Facts & Comparisons and Medispan; integration going according to plan

• Lower revenues mainly due to Medical Research (phasing issues, softness in the international market and reduced advertising revenues)

• Weaker journal and book revenues at Pharma Solutions

Revenues (USD)(EUR)

EBITA (USD)(EUR)

EBITA margin %

3333024238

12.5

2

1

(70)

(9)

(3)

(5)

(71)

(13)

3343734651

13.7

Million TotalCurrencyAcquisition/DivestmentOrganicHY 02HY 03

Change (mln)

18%30%

8%

44%

Medical Research

Pharma Solutions

Prof. & Education

Clinical Tools

16

Health

• Customer focused initiatives being intensified

• Continuing production efficiencies

• Major new book program at Professional and Education underway

• Increased focus on targeting society journals (new contracts booked)

• New intra-cluster product development initiatives

• Actions taken are further strengthening Wolters Kluwer’s strong positions in key Health market segment

• Expected growth for Health above company average

17

Education

• Seasonal business balanced towards second half of year

• Revenues down:

primary education negatively affected as government funded book budgets have been cut

adverse market conditions in UK and Sweden

• Management changes in the UK and the Netherlands

• Strong focus on cost control throughout cluster

Revenues (EUR) EBITA (EUR)EBITA margin %

1175

4.6

120108.0

(3)(4)

1(1)

(1) (3)(5)

Million TotalCurrencyAcquisition/DivestmentOrganicHY 02HY 03

Change (mln)

Sweden30%

UK16% Other

19%

Netherlands 35%

18

Education

• Focus on improved sales and marketing; cross cluster efficiencies and improved cost structure

• Investment in development of blended learning solutions: ready for commercial launch in a number of key markets: Digicoach

• Cooperation with IBM to provide e-learning solutions to schools in UK and the Netherlands

• Businesses aligned to take full advantage of 2004-2006 cycle peak in secondary education

• Education Cluster Day – November 24th, Amsterdam

19

Boudewijn Beerkens

Member Executive Board / CFO

Wolters Kluwer nv

Financials

20

Actions Taken

• Impairments

• Currency Hedging

• Share Buy-Back

• Dutch GAAP (moving to IAS/IFRS); RJ 270 and RJ 271

• Cash Flow & Working Capital Management

• Stricter Acquisition Policy

21

Overview

• Economic environment puts pressure on Wolters Kluwer’s Net Profit Benchmark leading to downward adjustment for full year

• Solid cash flow half year 2003

• 29% decrease in net debt from EUR 2,993 mln to EUR 2,122 mln

• Key financial ratios improved

• Limited acquisition spending

• Buy-back of shares

• Strategy Update on October 30th will outline medium to long term plans

22

HY 03 ResultsHY 03 %HY 02 Constant

currencies %

EUR mln

RevenuesEBITAEBITA margin %

Amortization of intangibles

Financing results

Taxation on operating incomeNon-consolidated and minority interestResults on divestments (after taxation)

Net income

1,609230

14.3

(291)(58)

(10)(4)

18

(115)*

1,917347

18.1

(174)(74)

(67)(2)

2

32

(16)(34)

(6)(24)

* Impairment effect (EUR 155 mln)

23

HY 03 Results (cont)

Net income Amortization of intangiblesTaxation on amortizationResults on divestments (after taxation)

Ordinary BM net income

Ordinary EPS before amortization of intangibles, and exceptionals (fully diluted)

(115)*

291(38)

(18)

120

0.42

32174(10)

(2)

194

0.66

HY 03 %HY 02 Constant currencies %

EUR mln

(38) (26)

* Impairment effect (EUR 155 mln)

24

Consolidated Balance SheetHY 03EUR mln HY 02

Total fixed assets

Total current assets

Total current liabilities

Working capital

Capital Employed

Shareholders equity

Perpetual subordinated bond

Convertible bond

Minority interests

Provisions

Long term loans

Total Financing

3,578

1,991

(1,257)

734

4,312

1,050

225

700

5

346

1,986

4,312

4,732

1,264

(1,340)

(76)

4,656

1,297

225

700

3

254

2,177

4,656

25

Wolters Kluwer complies with Dutch GAAP RJ 270 and RJ 271

• Wolters Kluwer has implemented RJ 270 and RJ 271 as per 1 January

2003, bringing it closer to IAS/IFRS

RJ 270 / IAS 18 – Revenue Recognition

RJ 271 / IAS 19 – Pensions/Employee Benefits

• Estimated impact;

• Year-end 2003 results will include these accounting changes

Equity opening

balance 2003 Revenue 2003

EBITA 2003

RJ 270 (80) 75 pm RJ 271 (50) - pm Total (130) 75 pm

EUR mln (after tax)

26

Improving Key Financial Ratios

2.32.0Net interest bearing debt to shareholders equity

3.22.8Net debt to EBITDA(Rolling 12 months)

4.95.6

2,993

5.36.2

2,122

Net interest coverage- EBITA- EBITDA(Rolling 12 months)

Net debt (29% improvement)

HY 03EUR mln HY 02

27

Cash flow statement

EBITADepreciation

23053

34761

(34)

EBITDA 283 408 (31)

Movement in working capitalCash flow from operationsFinancing costs

(42) (116)(17)241

(71)292(77)

Paid corporate income tax (39) (79)

Other (2) (15)

Cash flow from operating activities 129 121 7

(49)(6)

(63)(16)

Net expenditure fixed assetsAppropriation acquisition provisions

Acquisition spendingDivestment of activitiesCash flow investments

(56)502

(203)0

391 (282)

Cash flow surplus/(deficit) 520 (161)

HY 03EUR mln HY 02 %

28

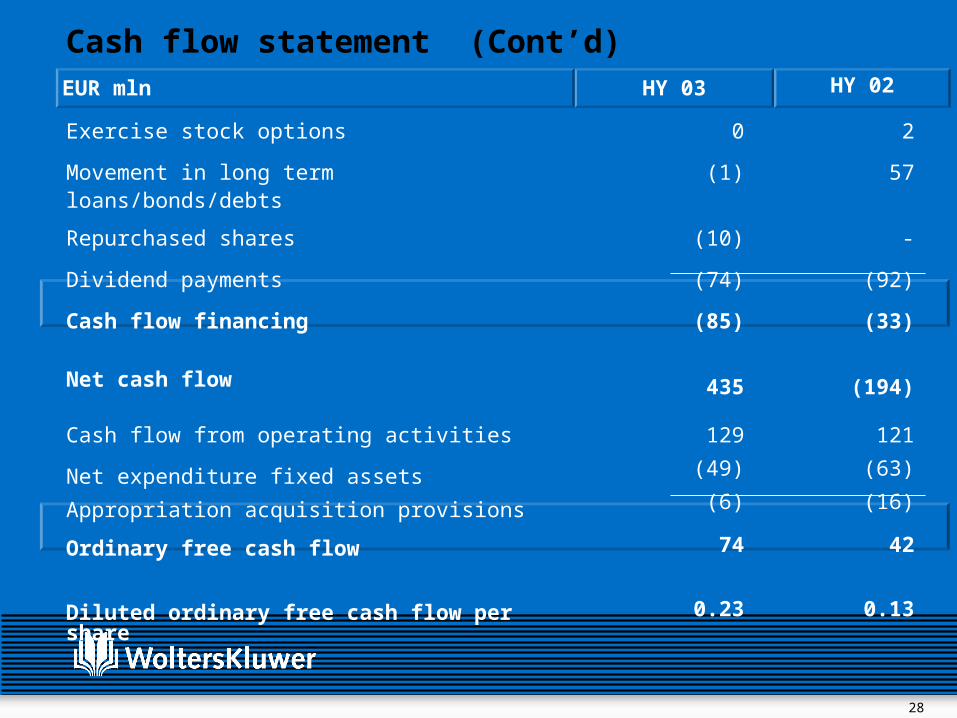

Cash flow statement (Cont’d)

Exercise stock options 0 2

Movement in long term loans/bonds/debts (1) 57

Repurchased shares (10) -

Dividend payments (74) (92)

Cash flow financing

Net cash flow

(85) (33)

435

(194)

Cash flow from operating activities 129

(49)

(6)

121

(63)

(16)Net expenditure fixed assets

Appropriation acquisition provisions

Ordinary free cash flow

Diluted ordinary free cash flow per share

74

0.23

42

0.13

HY 03EUR mln HY 02

29

Working Capital Development(Organic Trend)

Analysis of contribution (+) absorption of (-) Cash Flow

HY 03EUR mln HY 02

Inventories

Trade debtors

Other debtors

Trade creditors

Deferred income

Other short-term liabilities

Increase/(Decrease)

(4)

2

1

(53)

89

(77)

(42)

(20)

(35)

(14)

(62)

86

(71)

(116)

30

Acquisitions HY 2003Stricter acquisition policy and focus on core markets in Europe and US

1.9

7.3

162

300

32

2.2

6.8

211

458

37

2.6

11.1

Revenues multiplier

EBITA multiplier

204Acquired annual revenues

533Total investment

29# of transactions

(incl. minority stakes)

2.2

8.3

618

1,361

104

2002 20002001 Total 00-03

EUR mln

1.7

10.6

41

70

6

HY03

31

Summary & Outlook• Trading conditions will remain challenging for the rest of 2003

• Inevitable impact on revenues and income

• Benchmark ordinary net income at constant currency rates will be

significantly below that of last year and lower than indicated in

May

• Second half of the year expected to be stronger than the first half,

also showing benefits of accelerated cost cutting and

restructuring

• Improvement in financial controls and strong focus on cash

generation

• Further capitalizing on valuable market positions

• Sound medium and long-term prospects, - further details in the

Strategy Update, October 30th

32

• Strategy Update – October 30th, London

• Q3 Results – November 12th, conference call

• Education Cluster Day – November 25th, Amsterdam

33

Appendix

34

Revenues by Media

ElectronicInternetOther

538234304

341519

579240339

331419

(8)(3)

(11)

Print 811 52 939 53 (13)

Services 212 14 249 14 (15)

Continuing business 1,561 1,767 (12)

Non Core 48 3 150 8 (68)

Total 1,609 100 1,917 100 (16)

%EUR mln HY 03 %HY 02%

35

Overview Electronic sales per cluster

LTB Europe 174 28 168 27

LTB North America 245 51 294 47

LTB Asia Pacific 9 27 9 28

Health 101 33 102 28

Education 9 8 6 5

Total 538 34 579 32

EUR mln HY 03 HY 02 % of cluster sales

HY 02HY 03 % of cluster sales

36

Print Revenues

Loose leavesInfo PackagingJournals & NewslettersBooks

200104237270

137

1517

25567

307310

144

1817

(22)55

(23)(13)

Print 811 52 939 53 (13)

%EUR mln HY 03 %HY 02%

37

Print and services Revenues in local currency

100

99

112

60

83

454

118

43

141

58

93

453

Loose-leaves

Info Packaging

Journals/news.

Books

Document services

Total

97

4

15

59

117

292

85

4

10

48

113

260

Loose-leaves

Info Packaging

Journals/news.

Books

Document services

Total

LTB North America (USD mln) HY 03 HY 02

LTB Europe (EUR mln) HY 03 HY 02

38

LTB Asia Pacific (AUD mln)

Health (USD mln)

Print and services Revenues in local currency

25

3

1

9

5

43

25

3

1

9

2

40

Loose-leaves

Info Packaging

Journals/news.

Books

Document services

Total

9

0

127

67

19

222

11

15

131

67

19

243

Loose-leaves

Info Packaging

Journals/news.

Books

Document services

Total

HY 03 HY 02

HY 03 HY 02

39

Print Revenues in local currency

0

0

102

6

108

0

0

108

6

114

Loose-leaves

Journals/news.

Books

Other

Total

Education (EUR) HY 03 HY 02

40

32759

18.2

Revenues (EUR) EBITA (EUR)EBITA margin %

32467

20.8

Million Q2 02Q2 03

LTB Europe

Revenues (USD)(EUR)

EBITA (USD)(EUR)

EBITA margin %

2592275346

20.5

2773047279

25.9

Million Q2 02Q2 03

LTB North America

Q2 03 results per cluster

41

Revenues (USD)(EUR)

EBITA (USD)(EUR)

EBITA margin %

1801593027

16.7

1821993134

17.0

Million Q2 02Q2 03

Health

Q2 03 results per cluster

Revenues (AUD)(EUR)

EBITA (AUD)(EUR)

EBITA margin %

27151.60.95.8

26152.41.49.2

Million Q2 02Q2 03

LTB Asia Pacific

42

7815

20.0

Revenues (EUR) EBITA (EUR)EBITA margin %

7716

20.6

Million Q2 02Q2 03

Education

Q2 03 results per cluster

43

WoltersKluwer

August 12, 2003 - Amsterdam

First Half Year Results 2003