10th annual canadian sponsorship landscape study

TRANSCRIPT

NORM O’REILLY | OHIO UNIVERSITY & T1

FEBRUARY 11, 2016

10th Annual CANADIAN SPONSORSHIP LANDSCAPE STUDYELISA BESELT & ADAM DeGRASSE | T1

Note: This is an interim report for 2016 and data is not final.

Historical SnapshotsAbout, History & Method

Sponsorship in 2015Current Realities

A Decade of Data: 2006-2015Findings & Trends

TODAY’S PRESENTATION

123

What’s NextOur Expectations4

ACKNOWLEDGEMENTS

Historical SnapshotsABOUT, HISTORY & METHOD

AnalysisTrends, Comparative

DesignPerspectives, Industry

OriginsIndustry Need, Share

ProcessOnline, Partners, Streamline

METHOD

124 Respondents2016 To Date

3,430 Respondents2006 to 2015#22.7% Were CEOs2006 to 2015

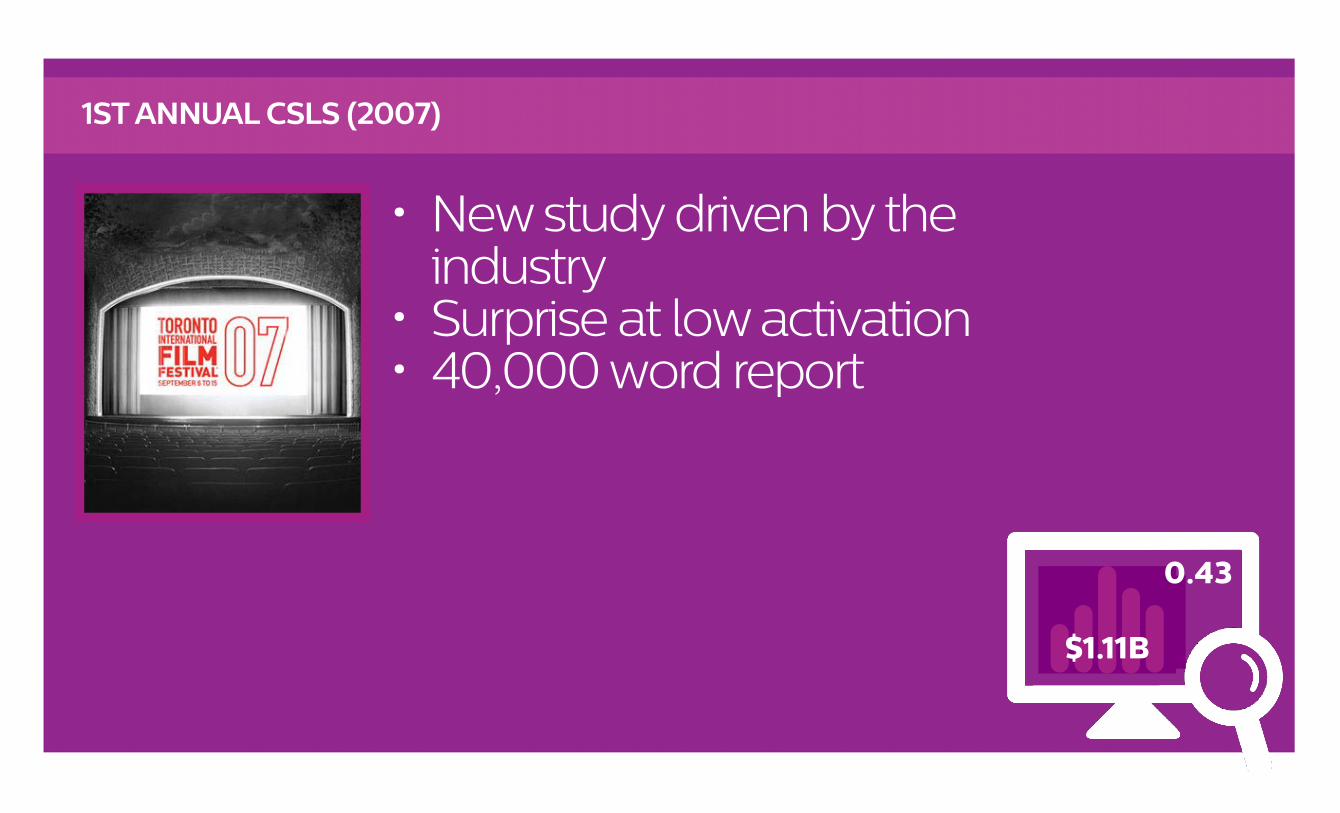

• New study driven by the industry

• Surprise at low activation• 40,000 word report

1ST ANNUAL CSLS (2007)

0.43

$1.11B

• Similar results to 2007• Added qualitative

questions• Demonstrating ROI as

the most important issue in Canadian sponsorship

2ND ANNUAL CSLS (2008)

0.46

$1.22B

• A great year for Canadian sponsorship (recession proof)

• Activation jump• “Festivalization”

3RD ANNUAL CSLS (2009)

0.71

$1.39B

• Strong sponsorship (economic crisis)

• Greatest responses• Collecting online• Industry concerns move

from ROI to digital

4TH ANNUAL CSLS (2010)

0.76

$1.43B

• Less growth in Canadian sponsorship

• Evaluation decline• Gap in service aligns with

emergence of HR needs• SMCC partnership

5TH ANNUAL CSLS (2011)

0.62

$1.55B

• Launched web portal• Evaluation decline• Gap in service expands• Industry concerns move

back to ROI• Uncertain future

6TH ANNUAL CSLS (2012)

0.57

$1.59B

• Activation rebound• Respondent fatigue• Social media moved to

#1 activation investment• Festivals on par with pro

sport

7TH ANNUAL CSLS (2013)

0.72

$1.57B

• Evaluation rebound• Pro sport adapts• Social media activation

tails off

8TH ANNUAL CSLS (2014)

0.62

$1.78B

• Pro sport thrives • All-time low activation

and evaluation • 1 in 4 marketing $ is on

sponsorship

9TH ANNUAL CSLS (2015)

0.41

$1.66B

• What to expect this year?

10TH ANNUAL CSLS (2016)

?

?

Sponsorship in 2015CURRENT REALITIES

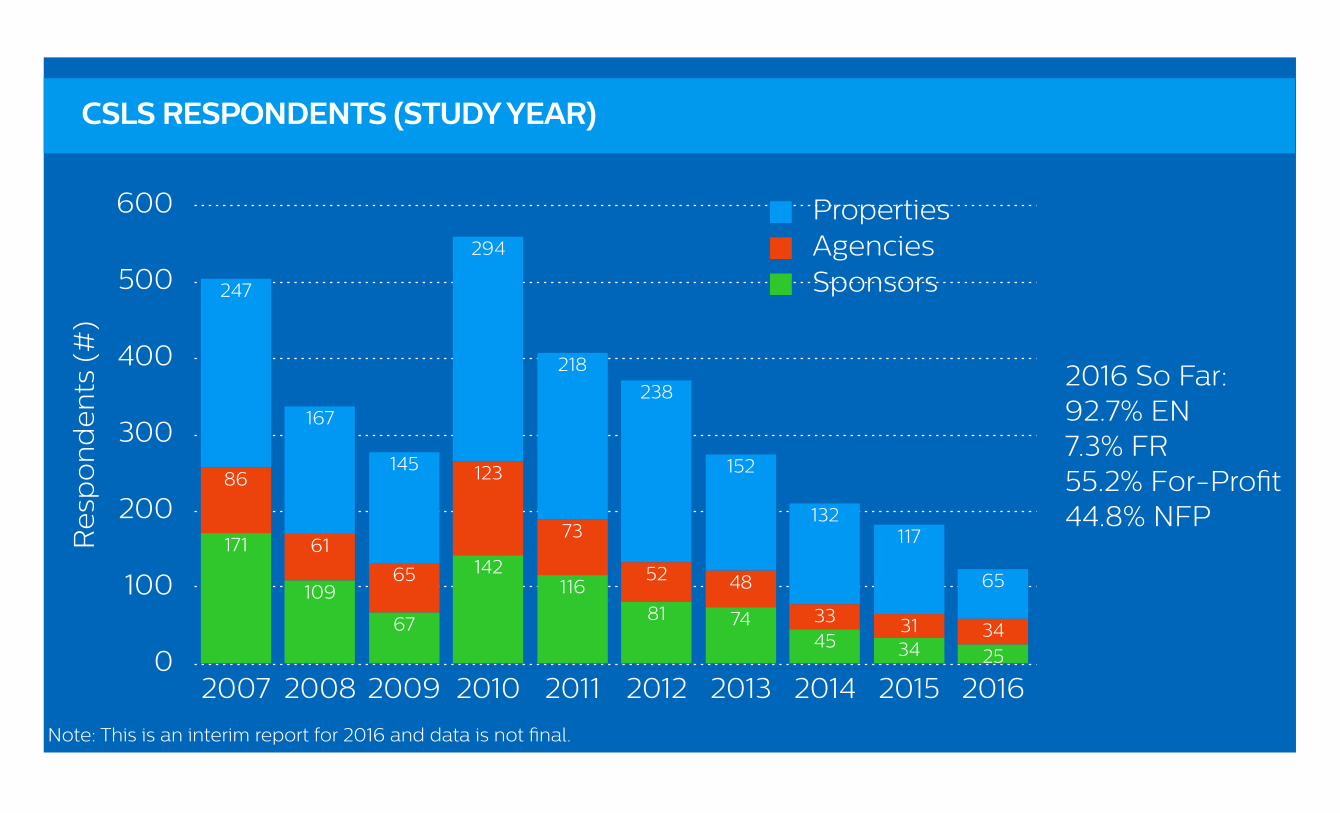

CSLS RESPONDENTS (STUDY YEAR)

0

100

200

300

400

500

600

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

65

117132

152

238218

294

145

167

247

343133

4852

73

123

65

61

86

2534457481

116142

67

109

171Re

spo

nd

en

ts (

#)

SponsorsAgenciesProperties

2016 So Far: 92.7% EN7.3% FR55.2% For-Profit44.8% NFP

Note: This is an interim report for 2016 and data is not final.

Survey is open until April 15, 2016. Visit www.sponsorshiplandscape.ca to enter responses!

SUPPORT THE CSLS

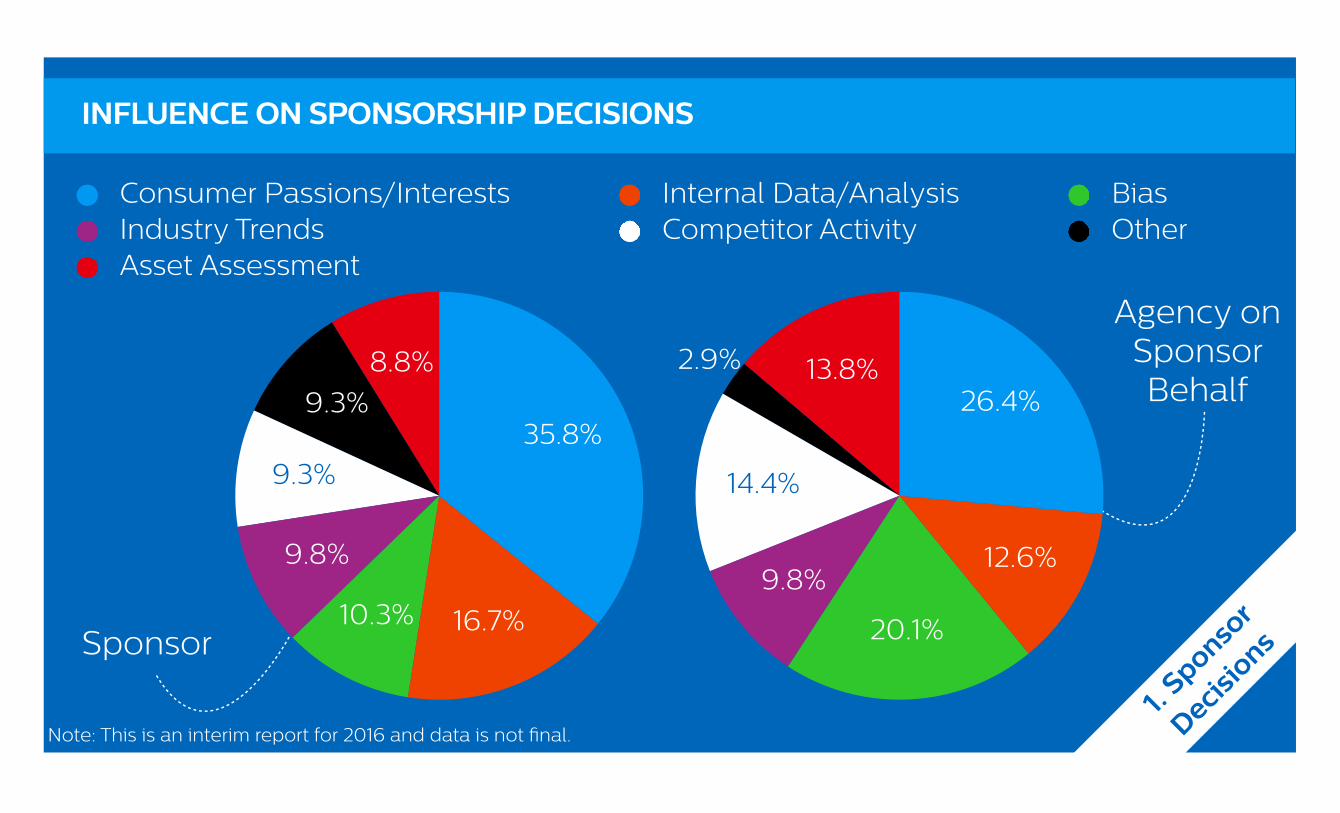

INFLUENCE ON SPONSORSHIP DECISIONS

1. Sponso

r

Decisio

ns

8.8%9.3%

9.3%

9.8%

10.3% 16.7%

35.8%

Consumer Passions/Interests Internal Data/Analysis BiasIndustry Trends Competitor Activity OtherAsset Assessment

Sponsor

Agency on Sponsor Behalf

13.8%2.9%

14.4%

9.8%

20.1%

12.6%

26.4%

Note: This is an interim report for 2016 and data is not final.

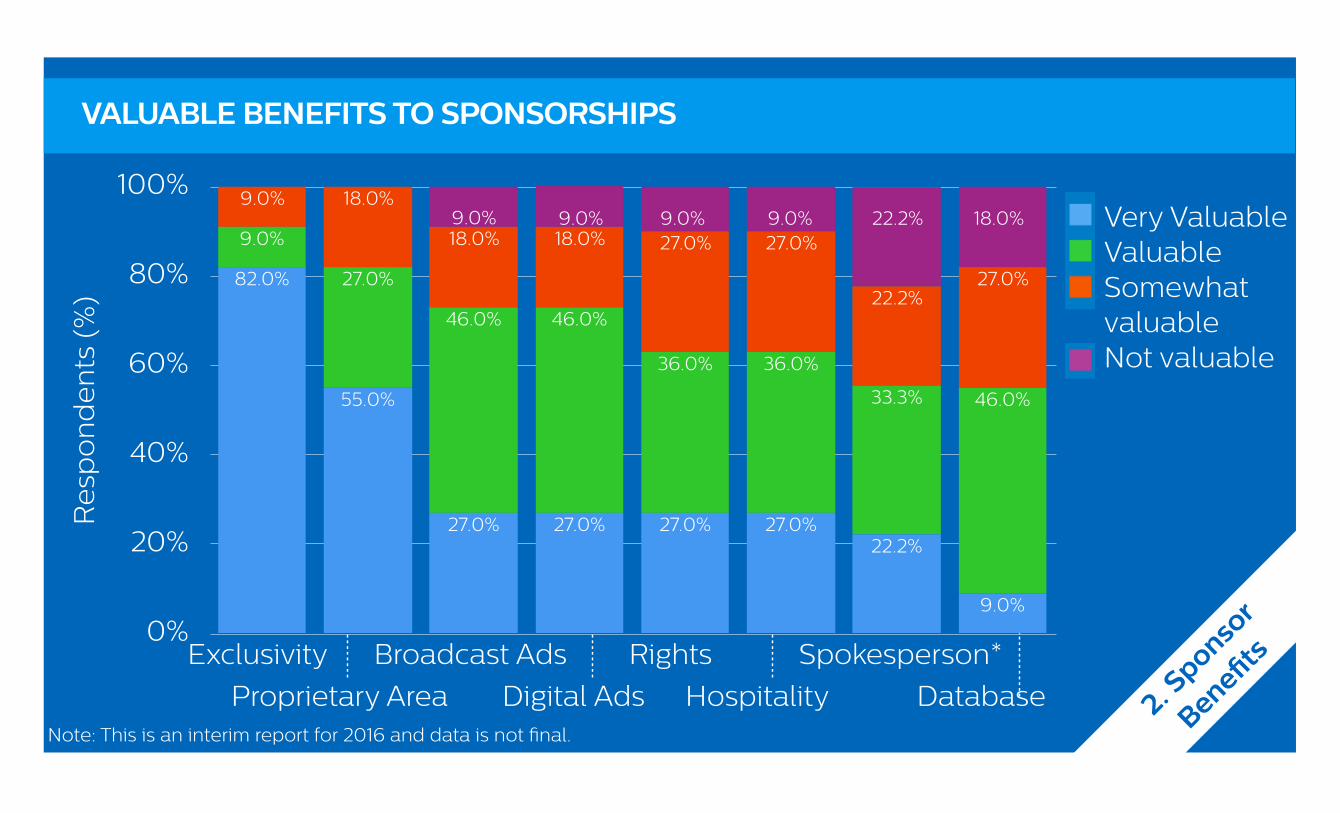

VALUABLE BENEFITS TO SPONSORSHIPS

0%

20%

40%

60%

80%

100%

27.0%22.2%

27.0%27.0%18.0%18.0%

18.0%9.0%

46.0%33.3%

36.0%36.0%

46.0%46.0%

27.0%

9.0%

9.0%

22.2%27.0%27.0%27.0%27.0%

55.0%

82.0%

Re

spo

nd

en

ts (

%)

2. Sponso

r

Benefits

Very ValuableValuableSomewhat valuableNot valuable

9.0% 9.0% 9.0% 9.0% 18.0%

Exclusivity Broadcast Ads Rights Spokesperson*Digital AdsProprietary Area Hospitality Database

22.2%

Note: This is an interim report for 2016 and data is not final.

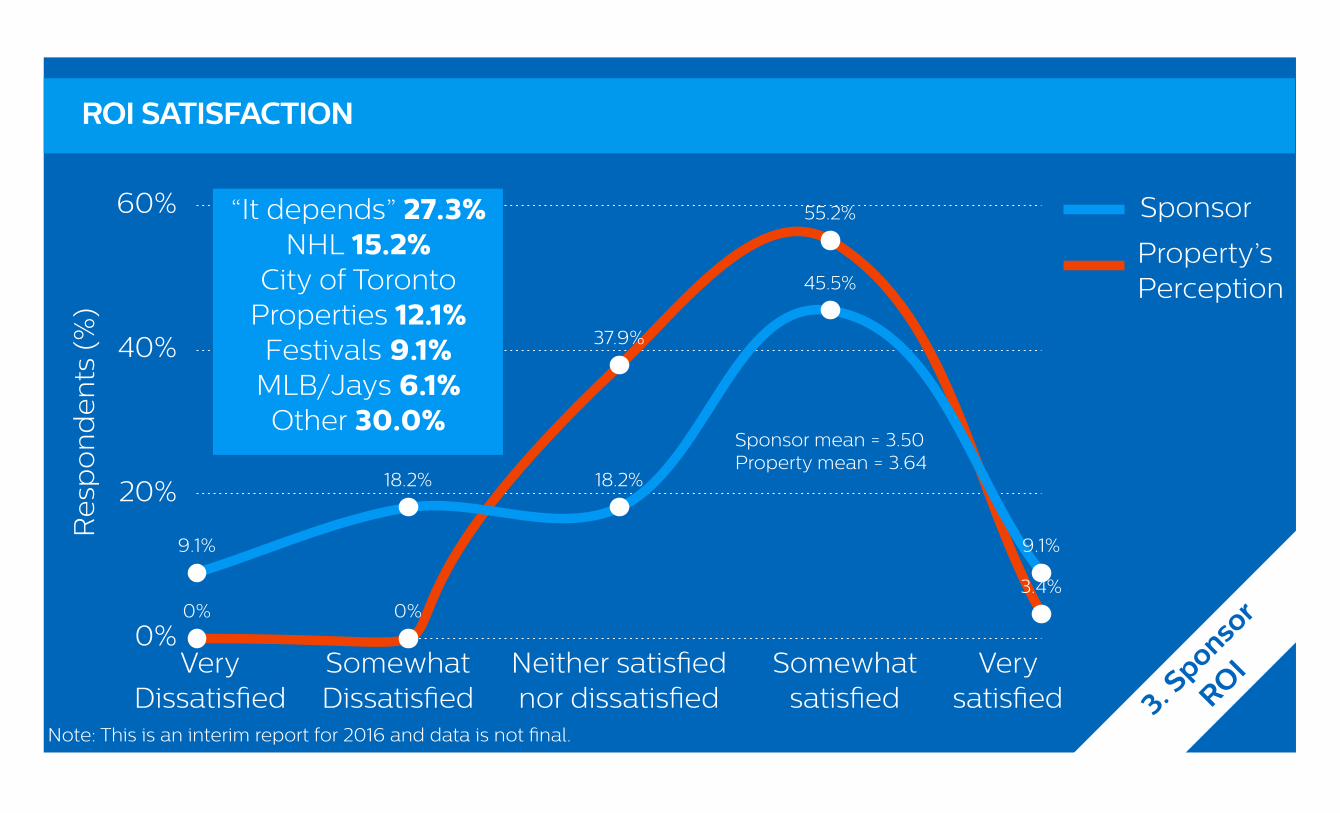

ROI SATISFACTION

0%

20%

40%

60%

0% 0%

37.9%

55.2%

3.4%

9.1%

18.2% 18.2%

45.5%

9.1%

Re

spo

nd

en

ts (

%)

Sponsor mean = 3.50Property mean = 3.64

3. Sponso

r

ROISomewhatDissatisfied

Neither satisfied nor dissatisfied

Somewhat satisfied

Very satisfied

VeryDissatisfied

Sponsor

Property’s Perception

“It depends” 27.3%NHL 15.2%

City of Toronto Properties 12.1%Festivals 9.1%

MLB/Jays 6.1%Other 30.0%

Note: This is an interim report for 2016 and data is not final.

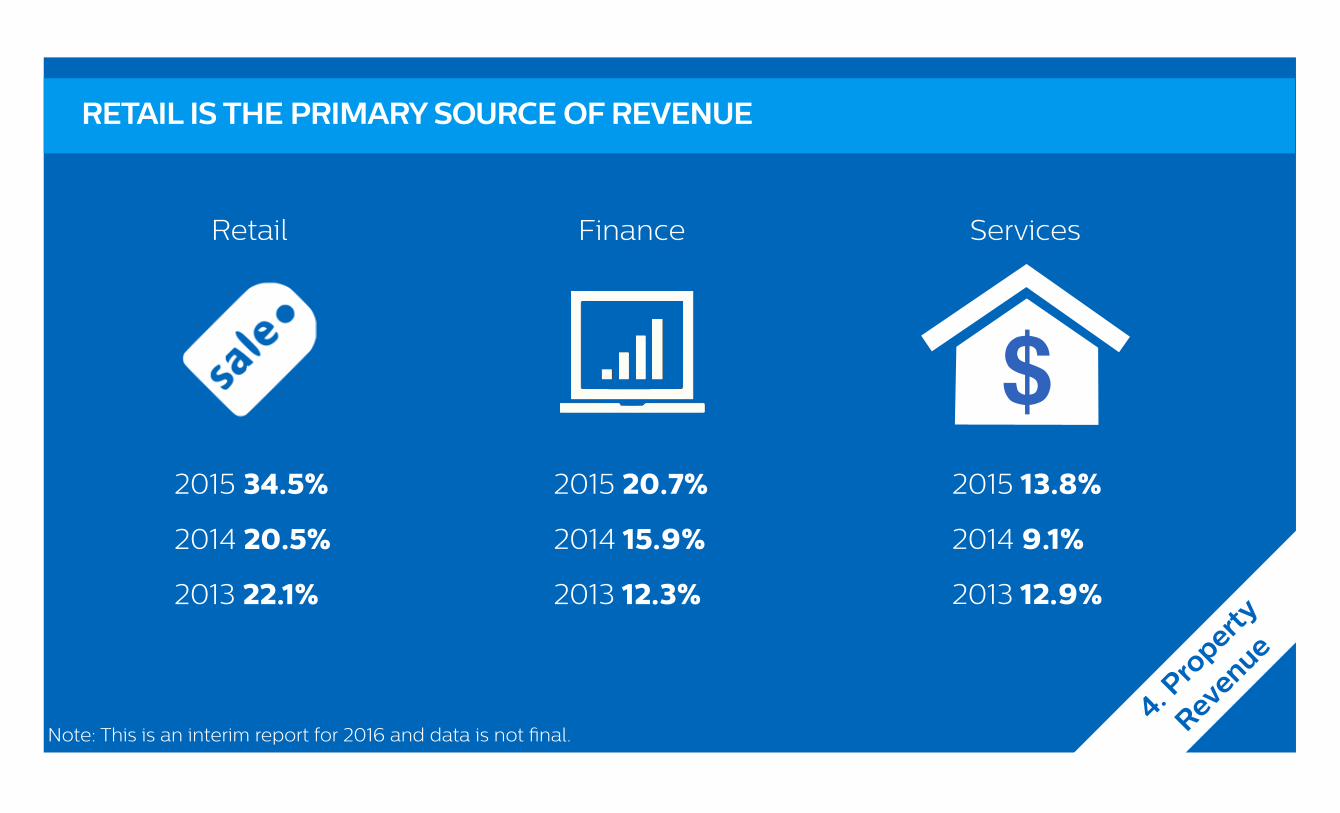

RETAIL IS THE PRIMARY SOURCE OF REVENUE

4. Pro

perty

Revenue

$2015 34.5%

Retail Finance Services

2014 20.5%

2013 22.1%

2015 20.7%

2014 15.9%

2013 12.3%

2015 13.8%

2014 9.1%

2013 12.9%

Note: This is an interim report for 2016 and data is not final.

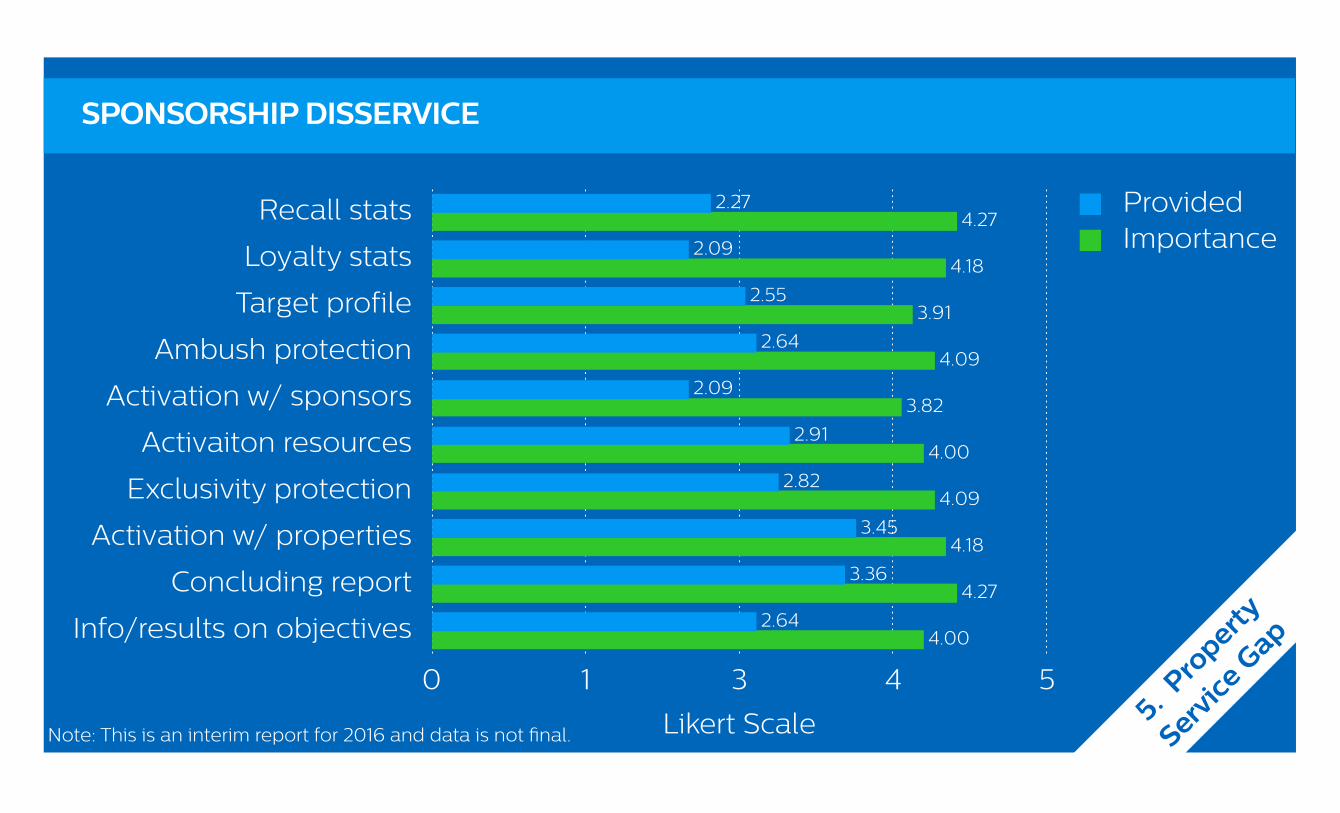

SPONSORSHIP DISSERVICE

Recall stats

Loyalty stats

Target profile

Ambush protection

Activation w/ sponsors

Activaiton resources

Exclusivity protection

Activation w/ properties

Concluding report

Info/results on objectives

0 1 3 4 5

4.00

4.27

4.18

4.09

4.00

3.82

4.09

3.91

4.18

4.27

2.64

3.36

3.45

2.82

2.91

2.09

2.64

2.55

2.09

2.27

Likert Scale 5. Pro

perty

Service

Gap

ProvidedImportance

Note: This is an interim report for 2016 and data is not final.

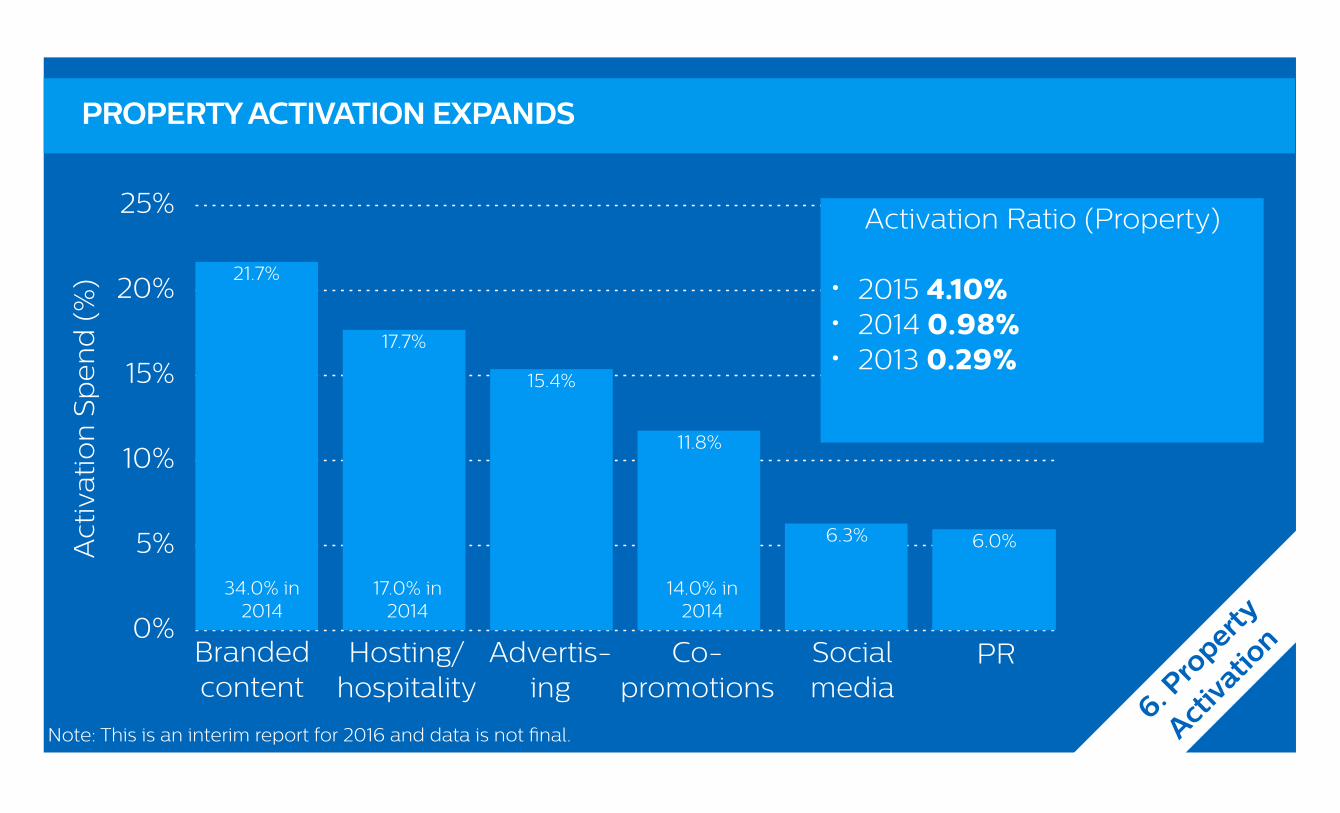

PROPERTY ACTIVATION EXPANDS

0%

5%

10%

15%

20%

25%

6.0%6.3%

11.8%

15.4%

17.7%

21.7%

Act

ivat

ion

Sp

en

d (

%)

6. Pro

perty

Activa

tion

34.0% in 2014

17.0% in 2014

14.0% in 2014

Activation Ratio (Property)

• 2015 4.10%• 2014 0.98%• 2013 0.29%

Branded content

Hosting/hospitality

Advertis-ing

Co-promotions

Socialmedia

PR

Note: This is an interim report for 2016 and data is not final.

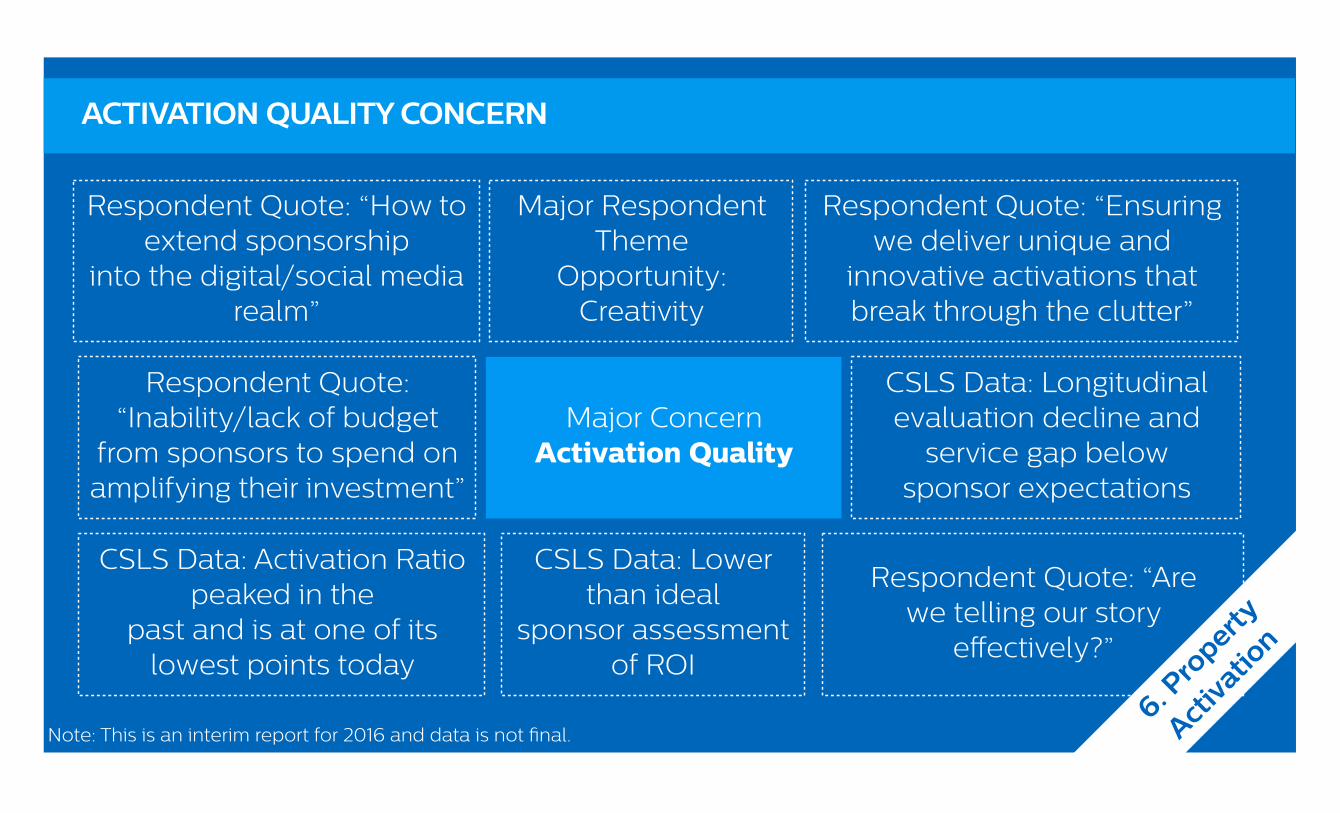

Respondent Quote: “Inability/lack of budget

from sponsors to spend on amplifying their investment”

ACTIVATION QUALITY CONCERN

Respondent Quote: “How to extend sponsorship

into the digital/social media realm”

Major Concern Activation Quality

Major Respondent Theme

Opportunity: Creativity

Respondent Quote: “Ensuring we deliver unique and

innovative activations that break through the clutter”

CSLS Data: Longitudinal evaluation decline and

service gap belowsponsor expectations

CSLS Data: Lower than ideal

sponsor assessment of ROI

CSLS Data: Activation Ratio peaked in the

past and is at one of its lowest points today

Respondent Quote: “Are we telling our story

effectively?”

6. Pro

perty

Activa

tion

Note: This is an interim report for 2016 and data is not final.

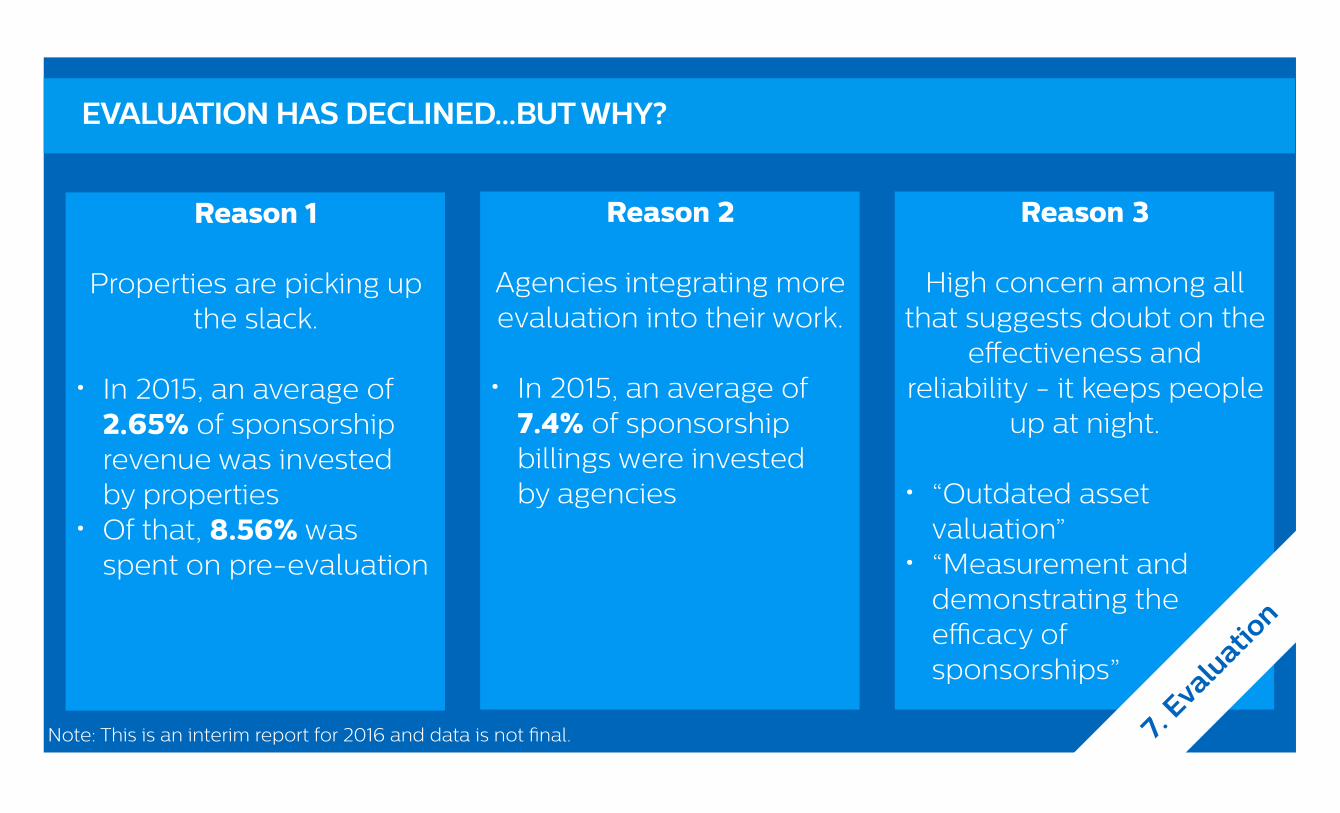

EVALUATION HAS DECLINED...BUT WHY?

Reason 1

Properties are picking up the slack.

• In 2015, an average of 2.65% of sponsorship revenue was invested by properties

• Of that, 8.56% was spent on pre-evaluation

Reason 2

Agencies integrating more evaluation into their work.

• In 2015, an average of 7.4% of sponsorship billings were invested by agencies

Reason 3

High concern among all that suggests doubt on the

effectiveness and reliability - it keeps people

up at night.

• “Outdated asset valuation”

• “Measurement and demonstrating the efficacy of sponsorships”

7. Eva

luatio

n

Note: This is an interim report for 2016 and data is not final.

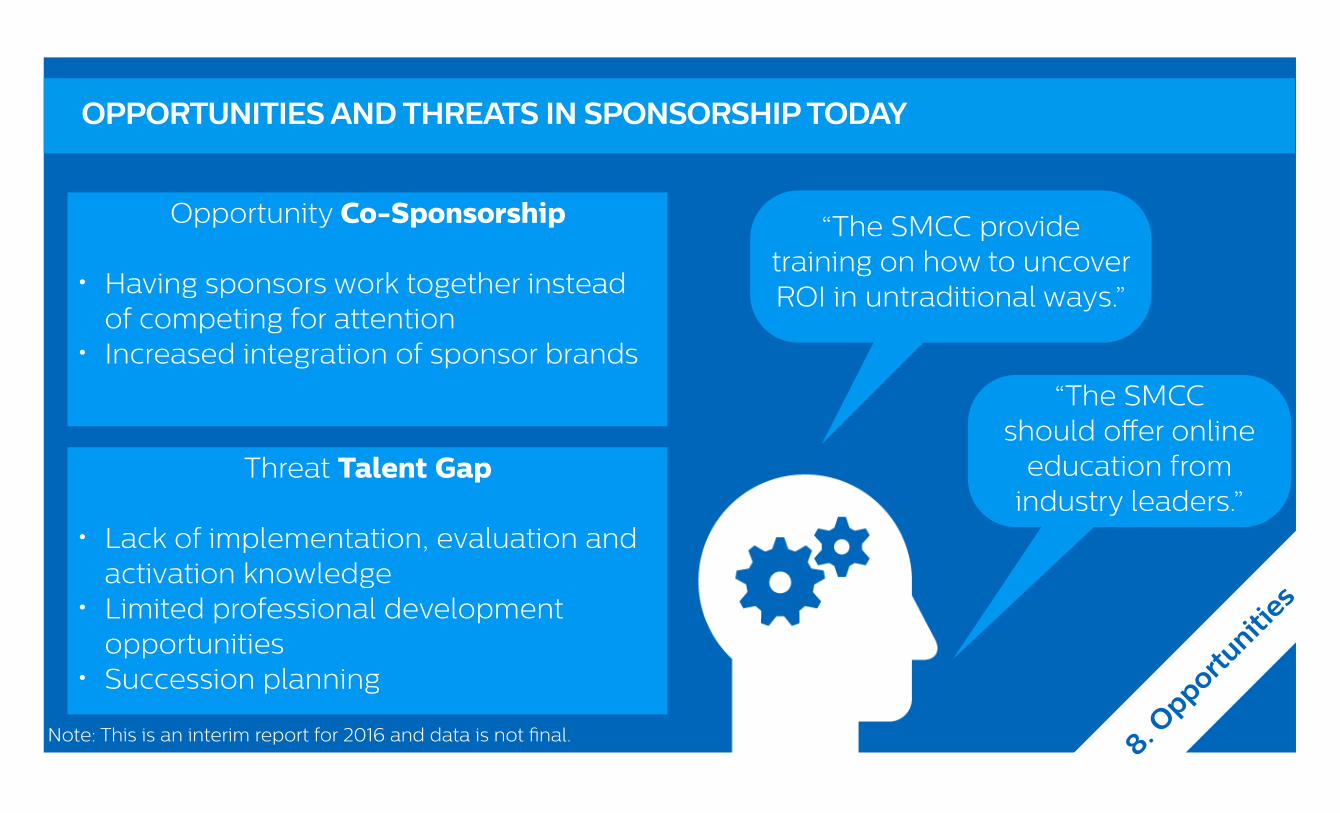

OPPORTUNITIES AND THREATS IN SPONSORSHIP TODAY

Opportunity Co-Sponsorship

• Having sponsors work together instead of competing for attention

• Increased integration of sponsor brands

Threat Talent Gap

• Lack of implementation, evaluation and activation knowledge

• Limited professional development opportunities

• Succession planning

8. Opportu

nities

“The SMCC provide training on how to uncover ROI in untraditional ways.”

“The SMCC should offer online

education from industry leaders.”

Note: This is an interim report for 2016 and data is not final.

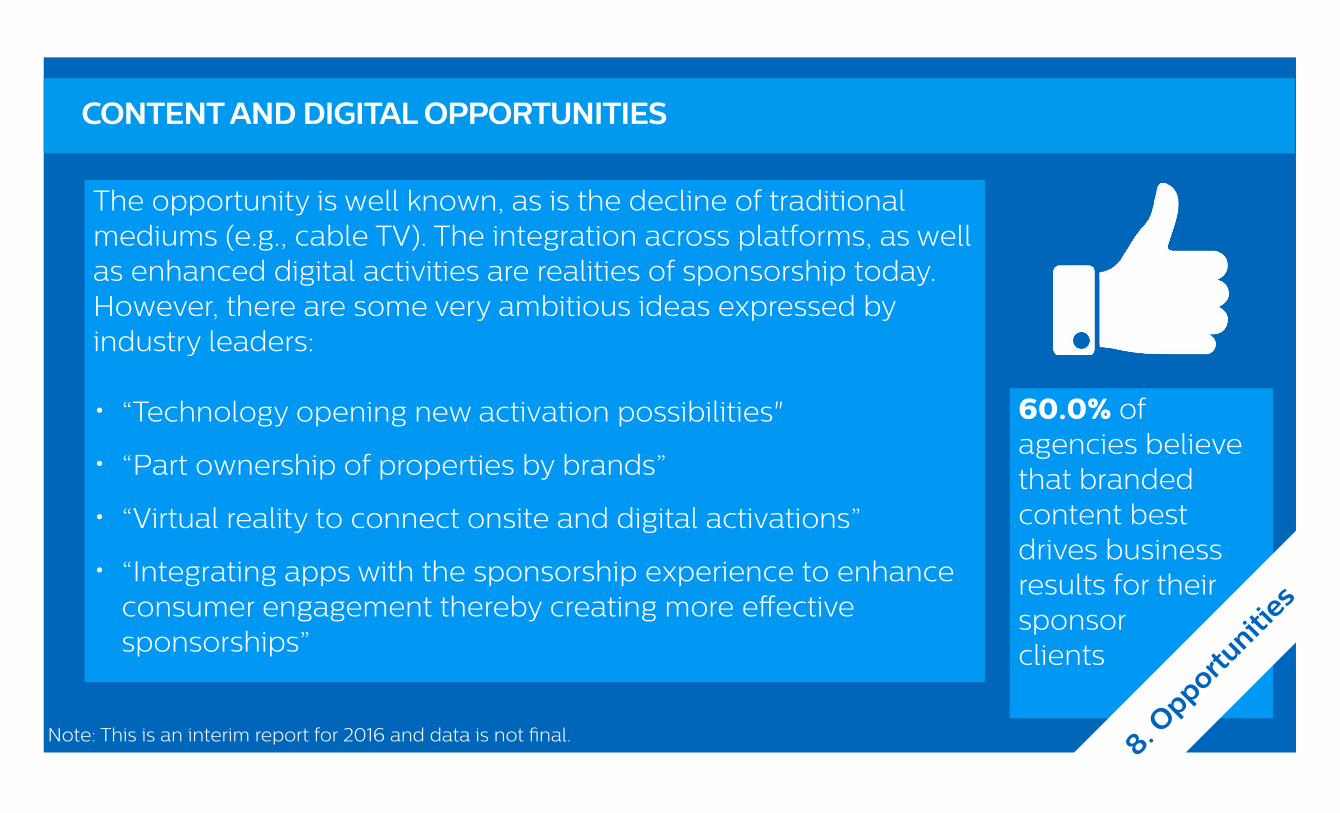

CONTENT AND DIGITAL OPPORTUNITIES

60.0% of agencies believe that branded content best drives business results for their sponsor clients

8. Opportu

nities

The opportunity is well known, as is the decline of traditional mediums (e.g., cable TV). The integration across platforms, as well as enhanced digital activities are realities of sponsorship today. However, there are some very ambitious ideas expressed by industry leaders:

• “Technology opening new activation possibilities"

• “Part ownership of properties by brands”

• “Virtual reality to connect onsite and digital activations”

• “Integrating apps with the sponsorship experience to enhance consumer engagement thereby creating more effective sponsorships”

Note: This is an interim report for 2016 and data is not final.

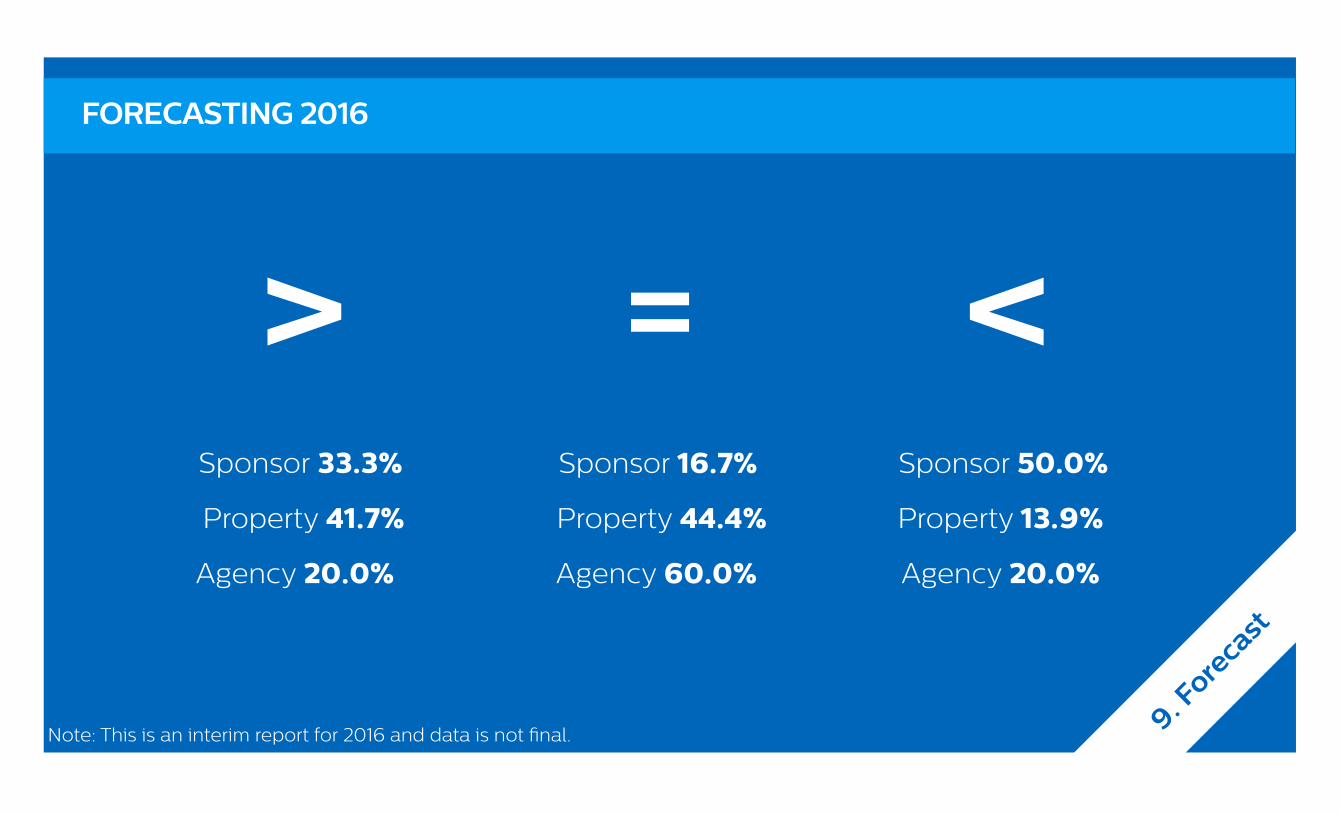

FORECASTING 2016

Sponsor 33.3%

Property 41.7%

Agency 20.0%

>Sponsor 16.7%

Property 44.4%

Agency 60.0%

=Sponsor 50.0%

Property 13.9%

Agency 20.0%

<

9. Fore

cast

Note: This is an interim report for 2016 and data is not final.

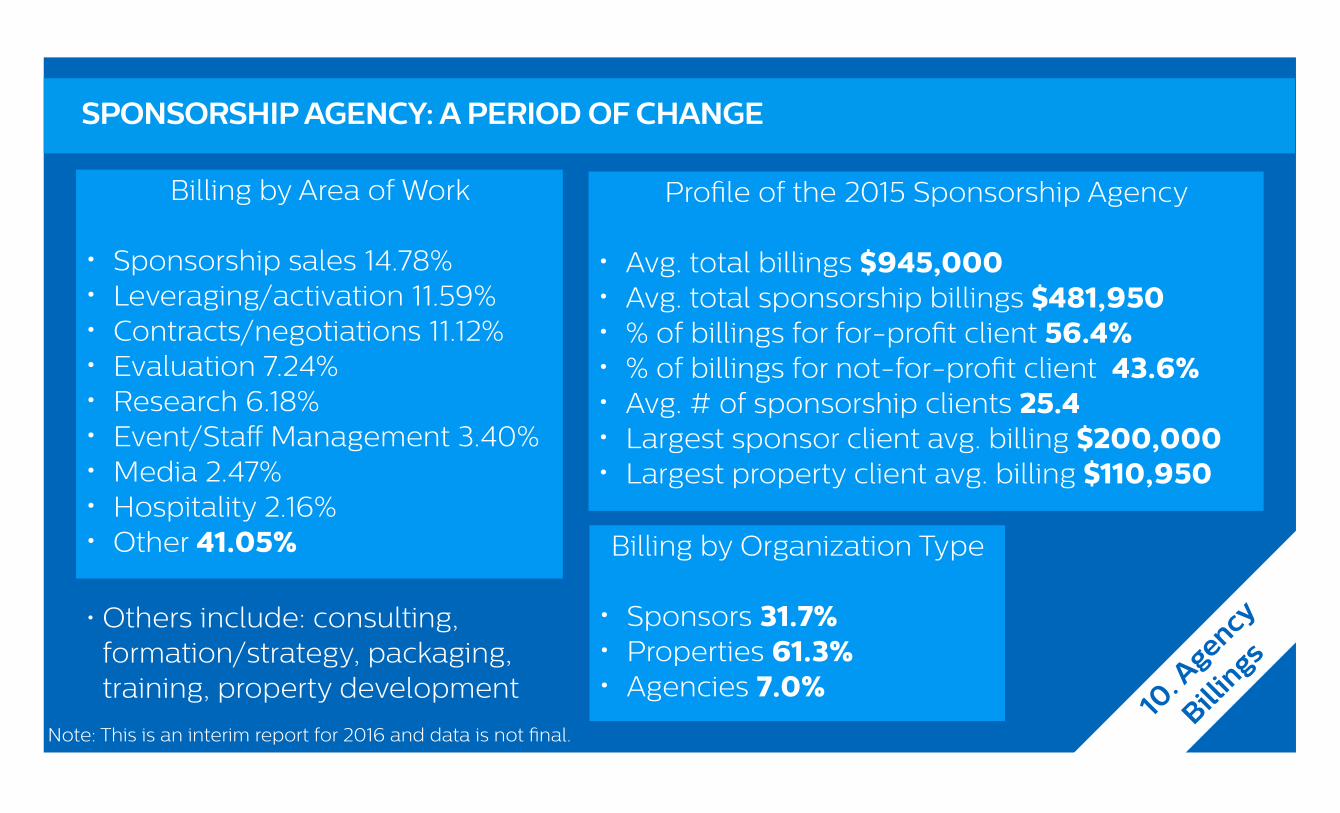

SPONSORSHIP AGENCY: A PERIOD OF CHANGE

10. A

gency

Billin

gs

Profile of the 2015 Sponsorship Agency

• Avg. total billings $945,000• Avg. total sponsorship billings $481,950• % of billings for for-profit client 56.4%• % of billings for not-for-profit client 43.6%• Avg. # of sponsorship clients 25.4• Largest sponsor client avg. billing $200,000• Largest property client avg. billing $110,950

Billing by Area of Work

• Sponsorship sales 14.78%• Leveraging/activation 11.59%• Contracts/negotiations 11.12%• Evaluation 7.24%• Research 6.18%• Event/Staff Management 3.40%• Media 2.47%• Hospitality 2.16%• Other 41.05% Billing by Organization Type

• Sponsors 31.7%• Properties 61.3%• Agencies 7.0%

• Others include: consulting, formation/strategy, packaging, training, property development

Note: This is an interim report for 2016 and data is not final.

A Decade of Data: 2006-2015FINDINGS & TRENDS

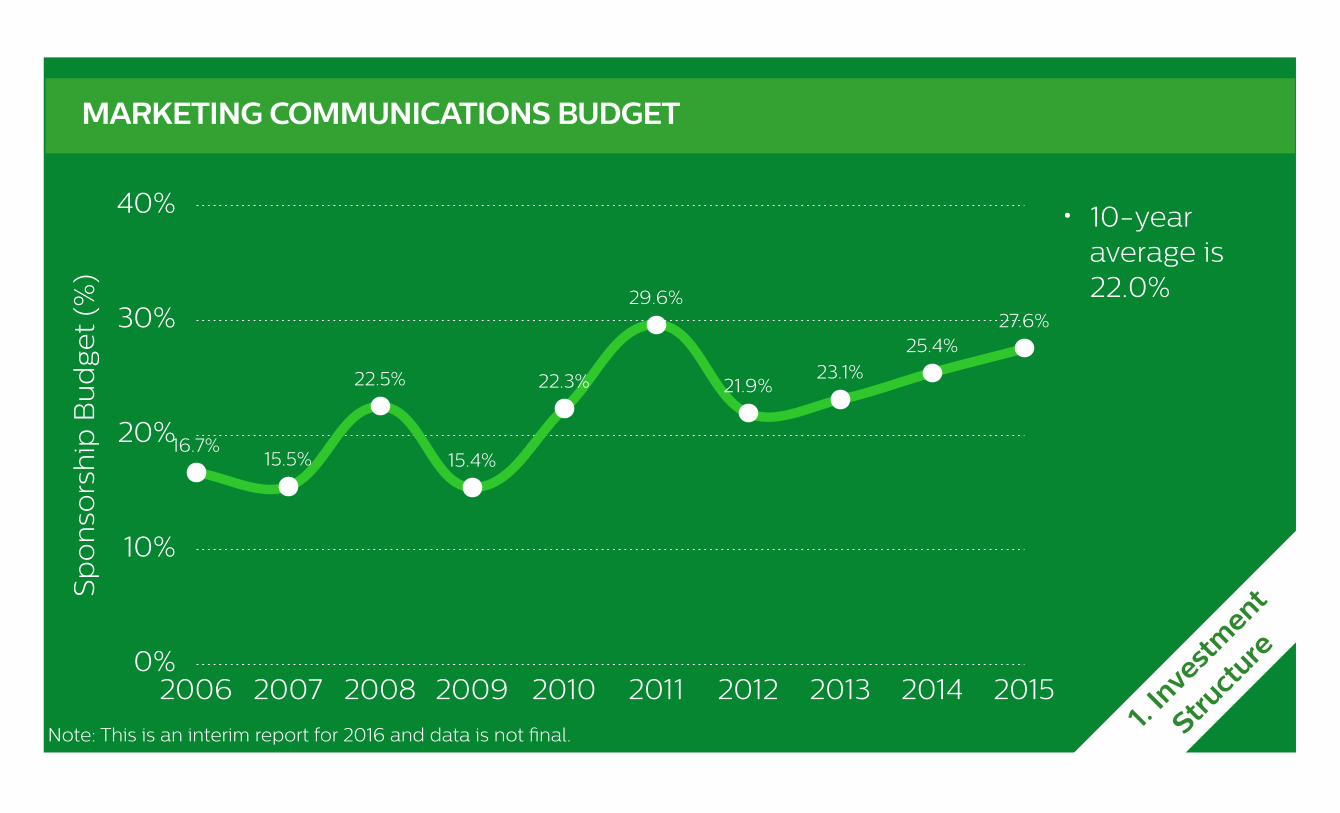

MARKETING COMMUNICATIONS BUDGET

0%

10%

20%

30%

40%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

16.7%15.5%

22.5%

15.4%

22.3%

29.6%

21.9%23.1%

25.4%27.6%

Sp

on

sors

hip

Bu

dge

t (%

)

• 10-year average is 22.0%

1. In

vest

ment

Struct

ure

Note: This is an interim report for 2016 and data is not final.

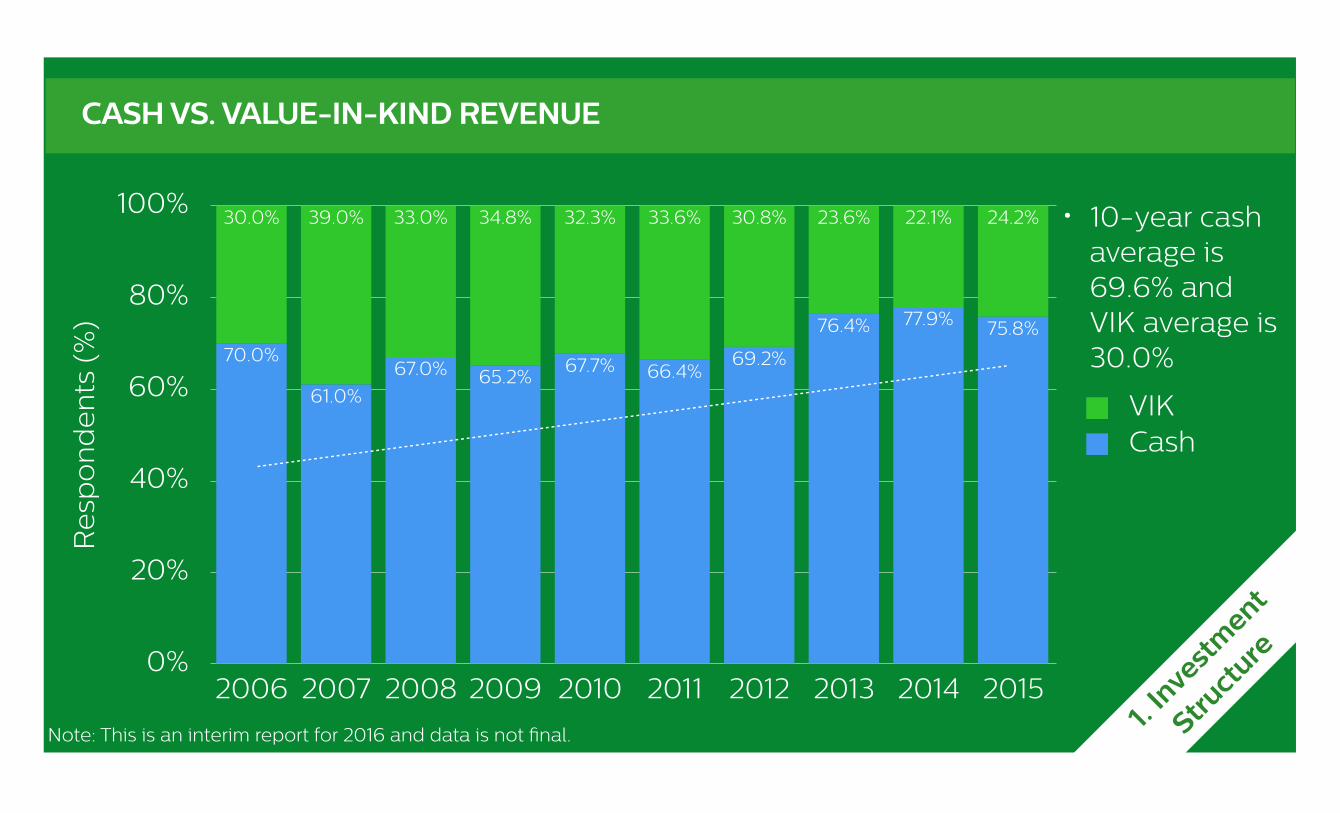

• 10-year cash average is 69.6% and VIK average is 30.0%

CASH VS. VALUE-IN-KIND REVENUE

0%

20%

40%

60%

80%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

24.2%22.1%23.6%30.8%33.6%32.3%34.8%33.0%39.0%30.0%

75.8%77.9%76.4%

69.2%66.4%67.7%

65.2%67.0%61.0%

70.0%

Re

spo

nd

en

ts (

%)

CashVIK

1. In

vest

ment

Struct

ure

Note: This is an interim report for 2016 and data is not final.

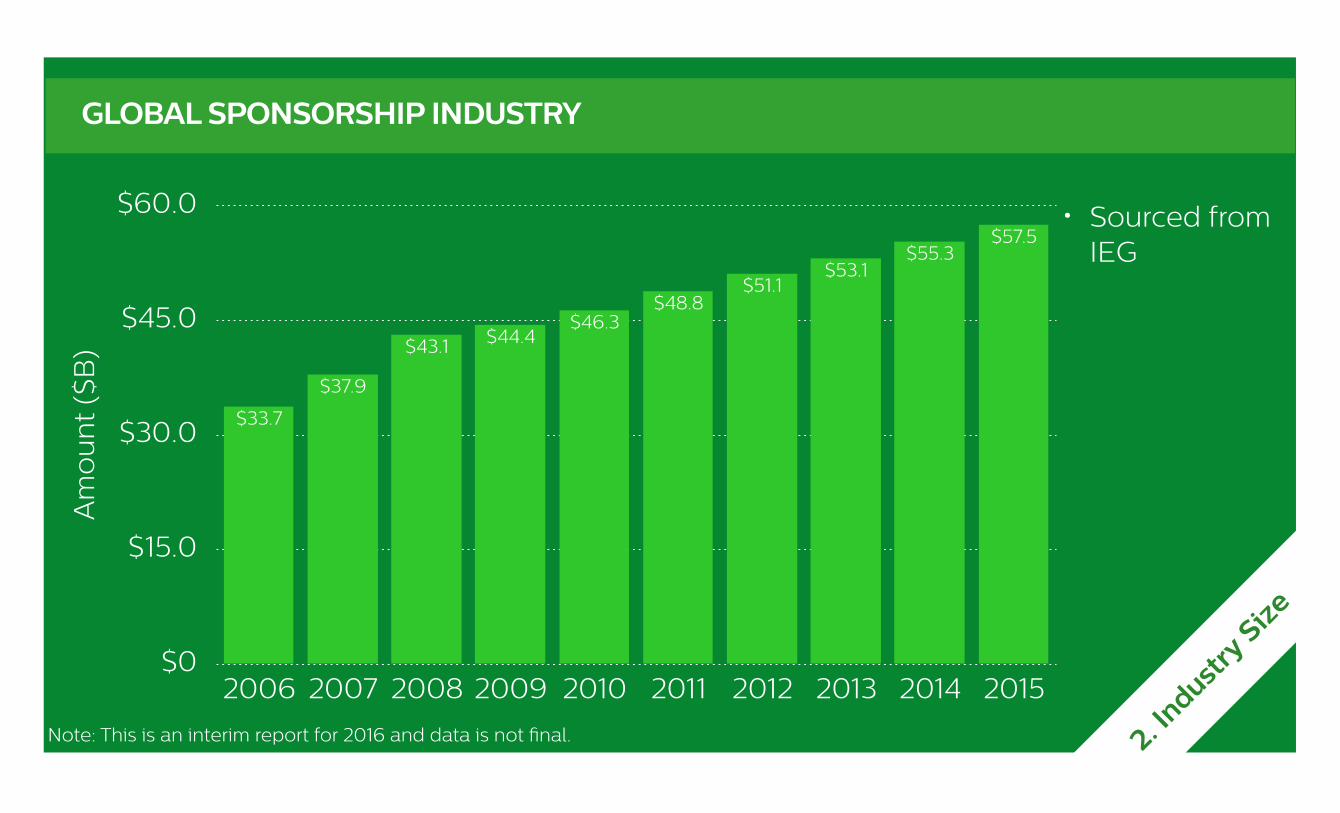

GLOBAL SPONSORSHIP INDUSTRY

$0

$15.0

$30.0

$45.0

$60.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$57.5$55.3

$53.1$51.1

$48.8$46.3

$44.4$43.1

$37.9

$33.7

Am

ou

nt

($B

)

2. Indust

ry S

ize

• Sourced from IEG

Note: This is an interim report for 2016 and data is not final.

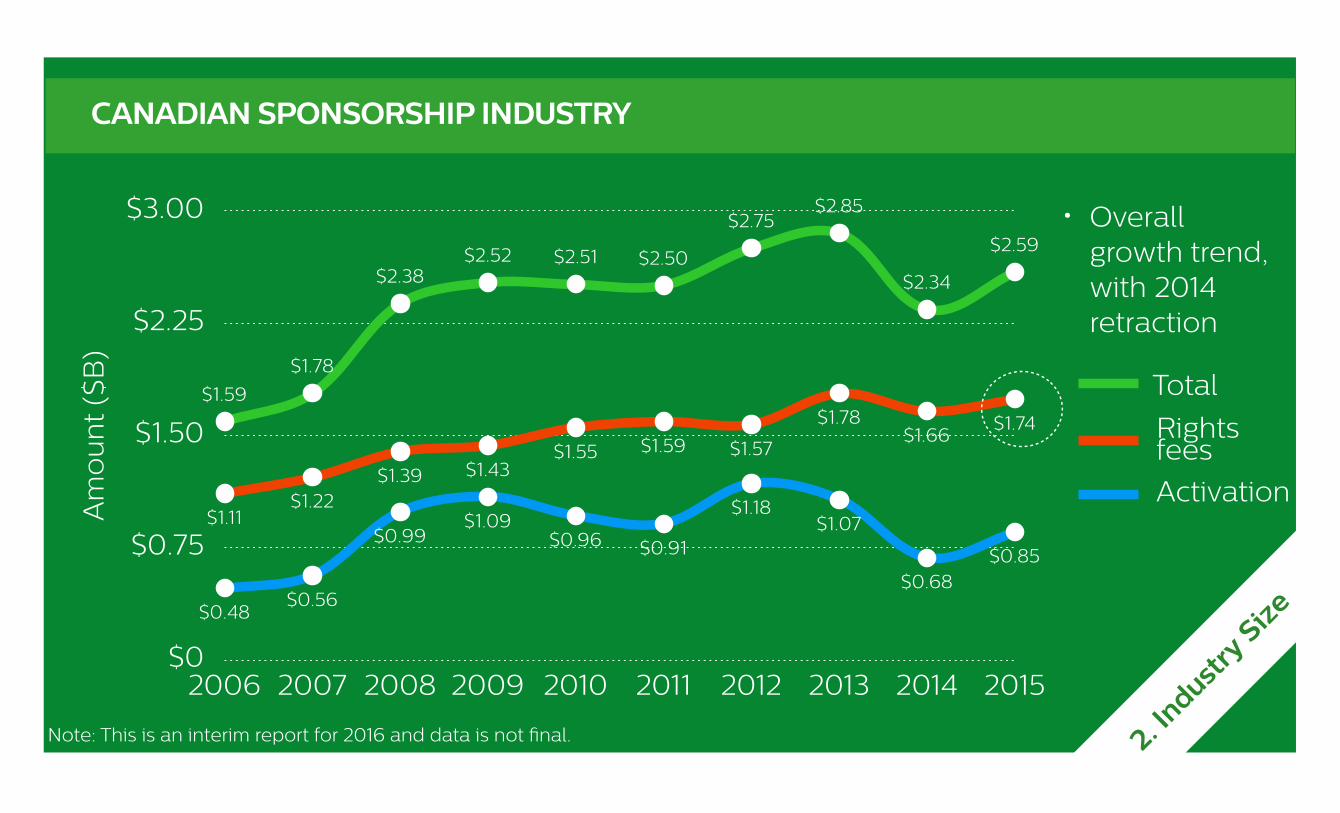

CANADIAN SPONSORSHIP INDUSTRY

$0

$0.75

$1.50

$2.25

$3.00

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$1.59

$1.78

$2.38$2.52 $2.51 $2.50

$2.75$2.85

$2.34

$2.59

$0.48$0.56

$0.99$1.09

$0.96 $0.91

$1.18$1.07

$0.68$0.85

$1.11$1.22

$1.39 $1.43$1.55 $1.59 $1.57

$1.78$1.66

$1.74

Am

ou

nt

($B

)

2. Indust

ry S

ize

• Overall growth trend, with 2014 retraction

Activation

Rights fees

Total

Note: This is an interim report for 2016 and data is not final.

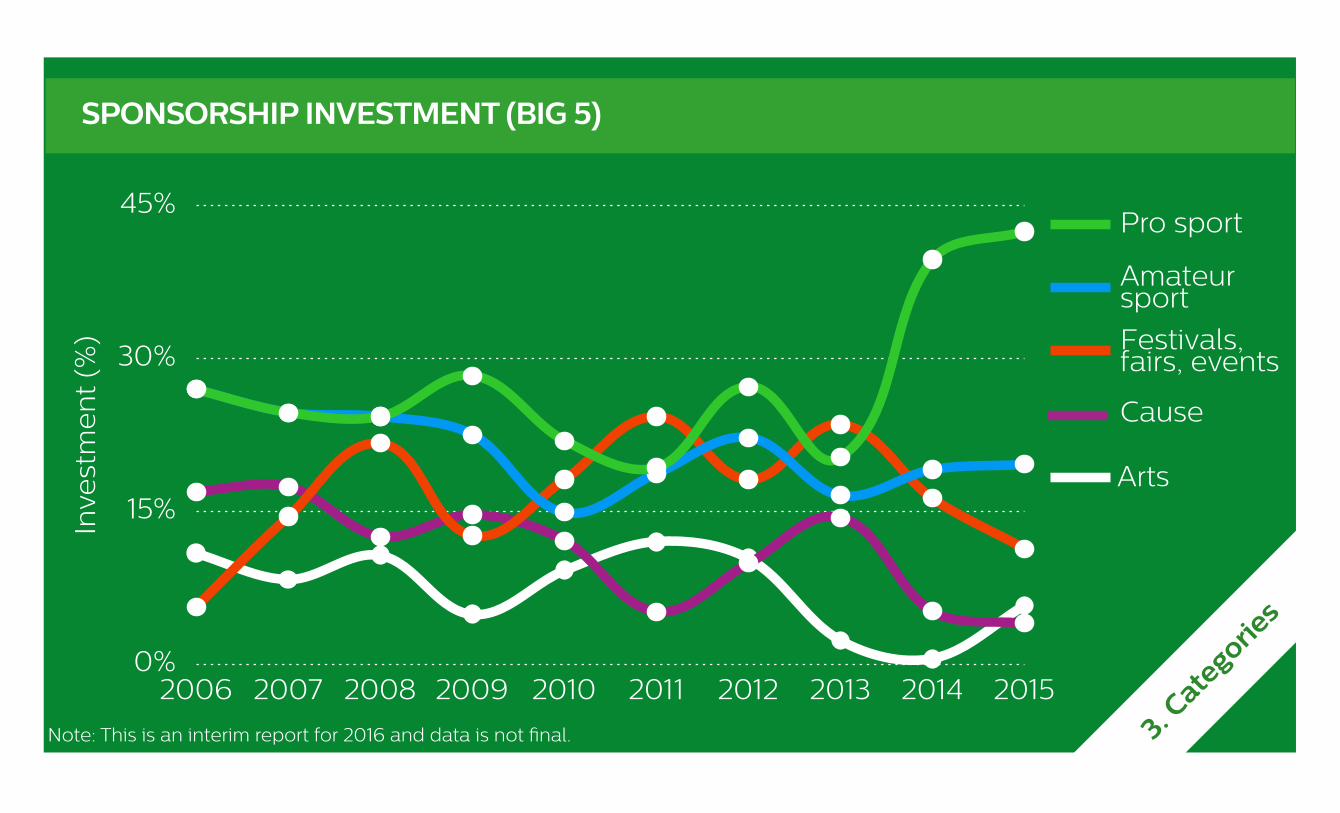

SPONSORSHIP INVESTMENT (BIG 5)

0%

15%

30%

45%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Inve

stm

en

t (%

) Festivals, fairs, events

Cause

Amateur sport

Pro sport

Arts

3. Cate

gories

Note: This is an interim report for 2016 and data is not final.

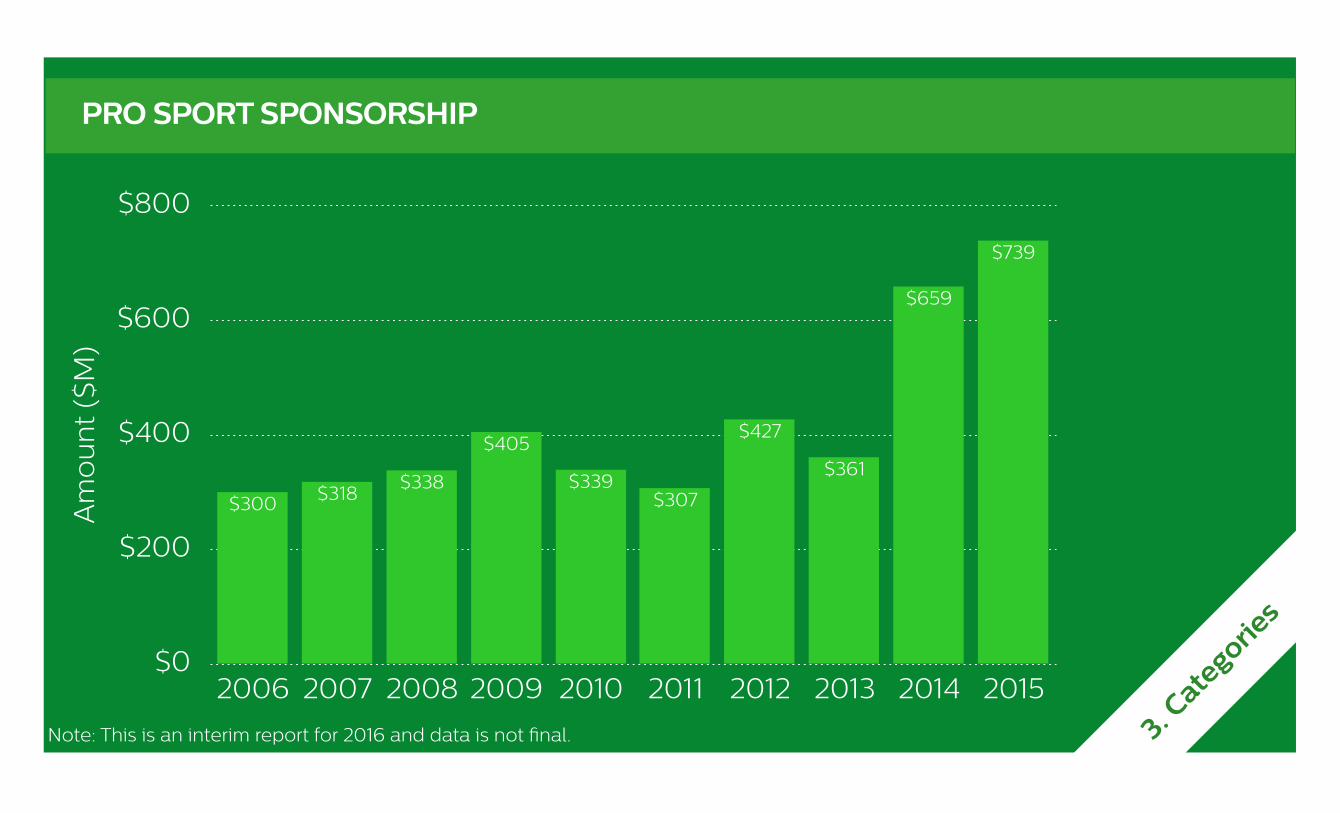

PRO SPORT SPONSORSHIP

$0

$200

$400

$600

$800

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$739

$659

$361

$427

$307$339

$405

$338$318$300A

mo

un

t ($

M)

3. Cate

gories

Note: This is an interim report for 2016 and data is not final.

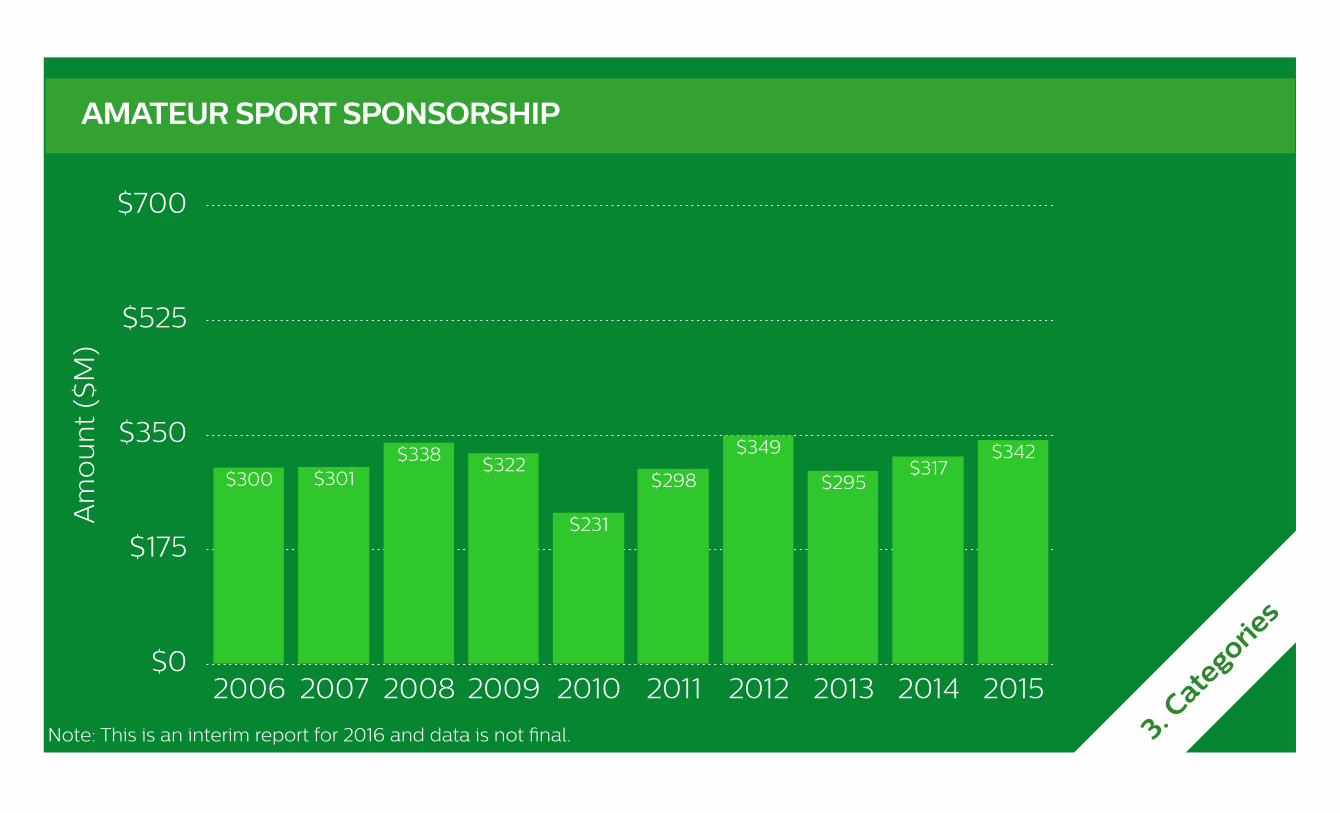

AMATEUR SPORT SPONSORSHIP

$0

$175

$350

$525

$700

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$342$317

$295

$349

$298

$231

$322$338$301$300

Am

ou

nt

($M

)

3. Cate

gories

Note: This is an interim report for 2016 and data is not final.

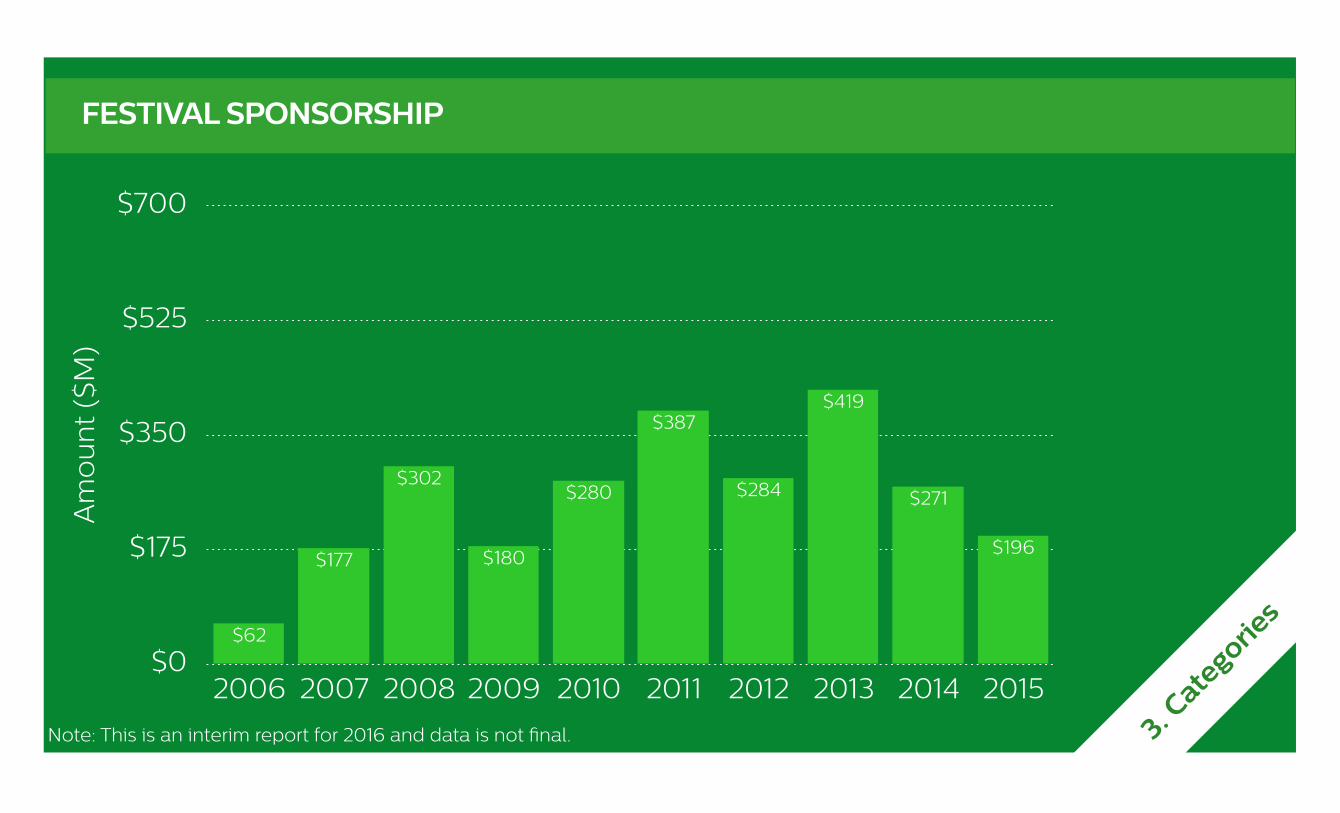

FESTIVAL SPONSORSHIP

$0

$175

$350

$525

$700

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$196

$271

$419

$284

$387

$280

$180

$302

$177

$62

Am

ou

nt

($M

)

3. Cate

gories

Note: This is an interim report for 2016 and data is not final.

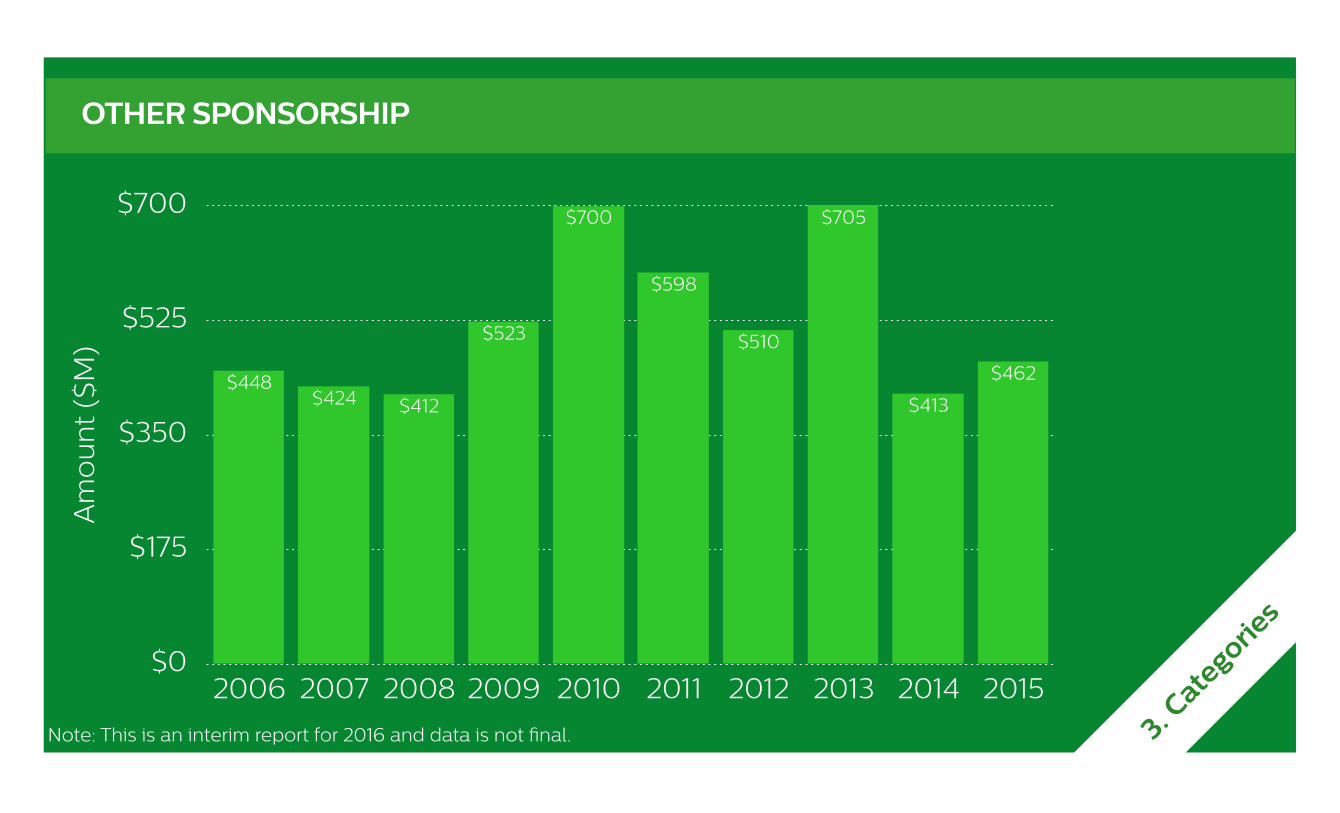

OTHER SPONSORSHIP

$0

$175

$350

$525

$700

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$462

$413

$705

$510

$598

$700

$523

$412$424$448

Am

ou

nt

($M

)

3. Cate

gories

Note: This is an interim report for 2016 and data is not final.

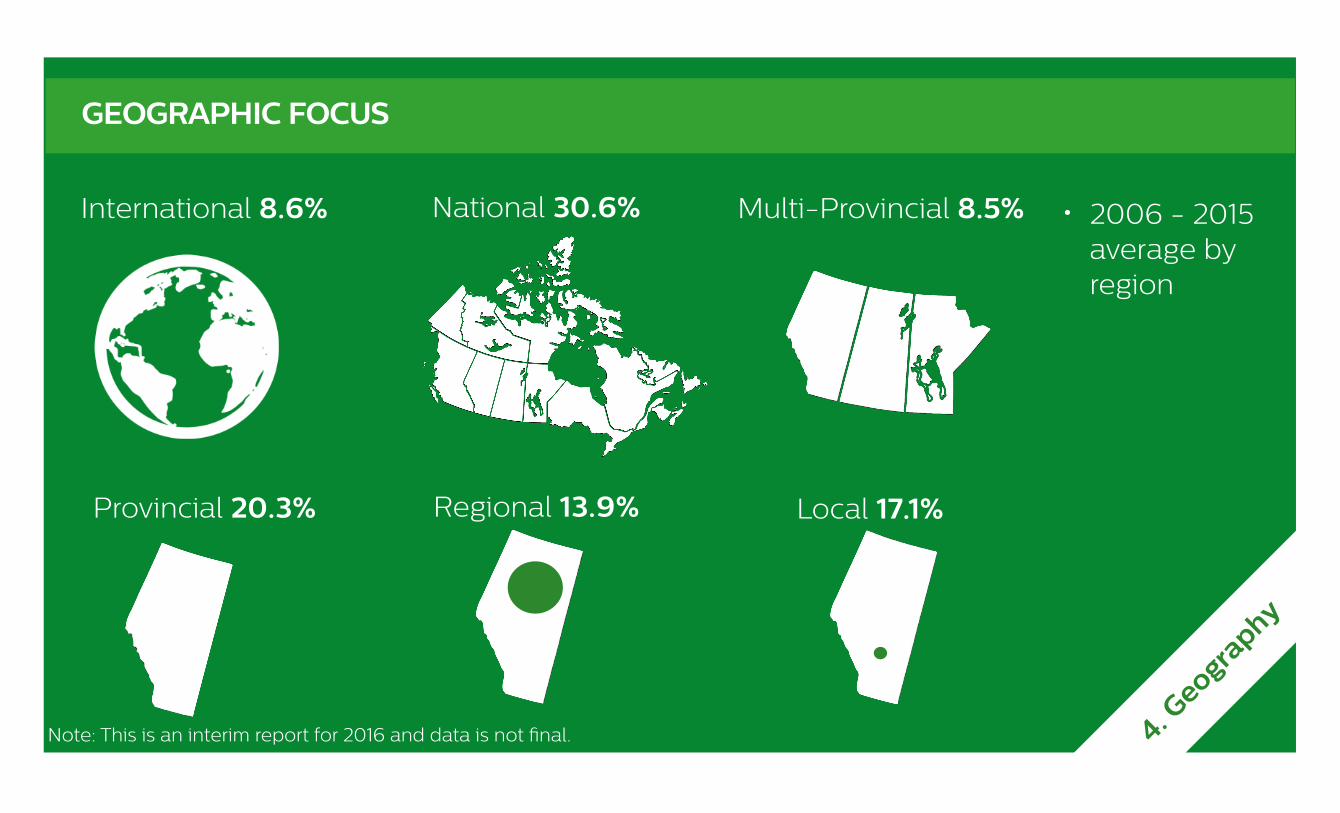

GEOGRAPHIC FOCUS

International 8.6% National 30.6% Multi-Provincial 8.5%

Provincial 20.3% Regional 13.9% Local 17.1%

4. Geogra

phy

• 2006 - 2015 average by region

Note: This is an interim report for 2016 and data is not final.

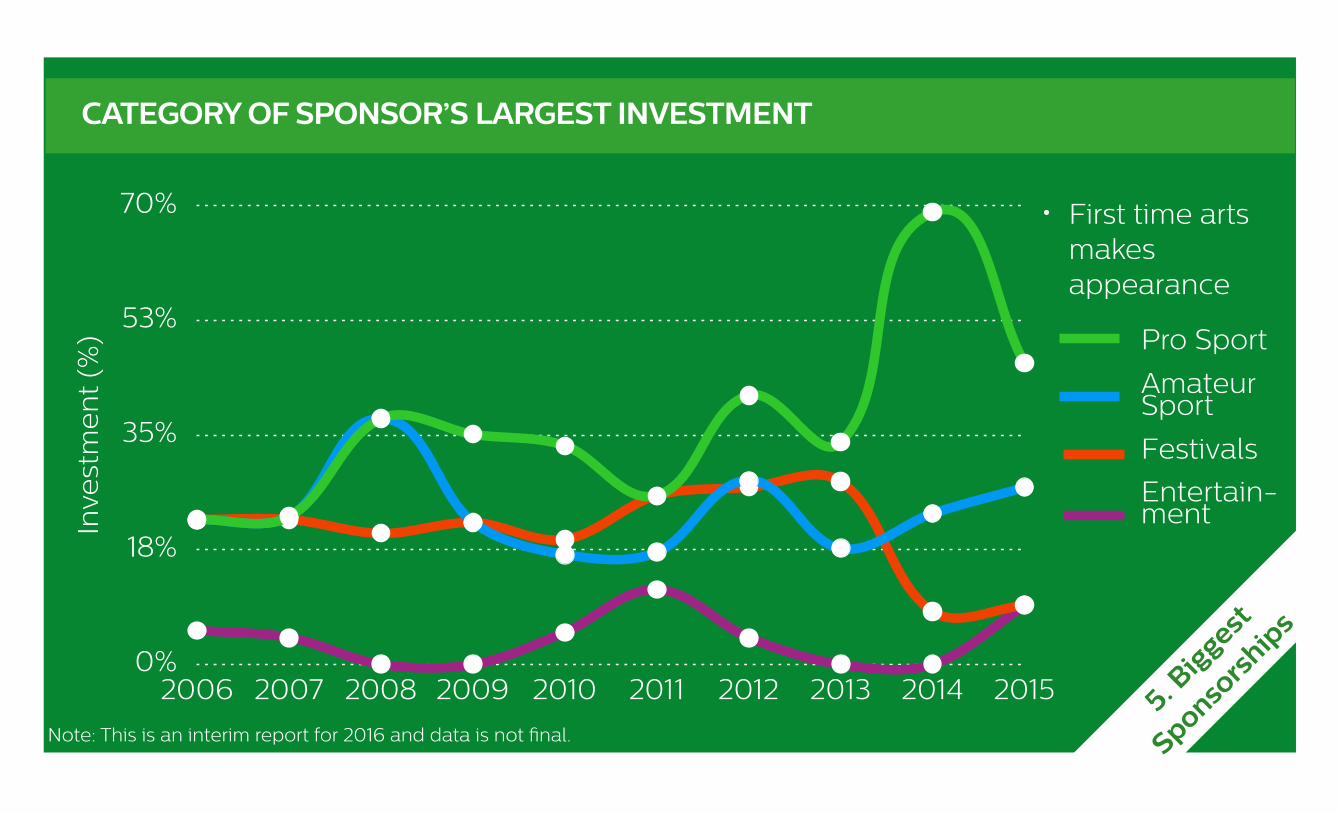

CATEGORY OF SPONSOR’S LARGEST INVESTMENT

0%

18%

35%

53%

70%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Inve

stm

en

t (%

) Pro Sport

Amateur Sport

Festivals

Entertain-ment

5. Big

gest

Sponsors

hips

• First time arts makes appearance

Note: This is an interim report for 2016 and data is not final.

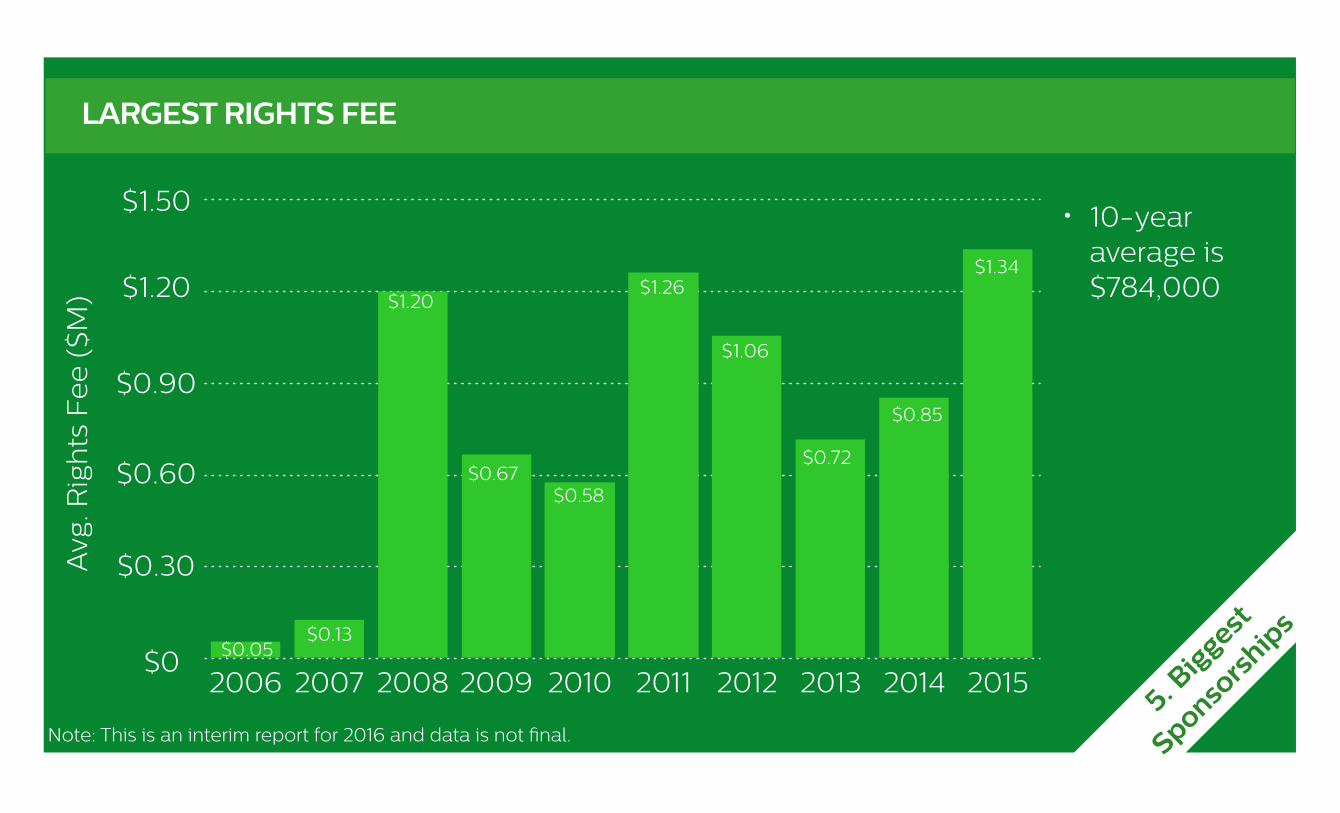

LARGEST RIGHTS FEE

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Avg

. Rig

hts

Fe

e (

$M)

$1.50

$1.20

$0.90

$0.60

$0.30

$0 $0.05$0.13

$1.20

$0.67$0.58

$1.26

$1.06

$0.72

$0.85

5. Big

gest

Sponsors

hips

$1.34

• 10-year average is $784,000

Note: This is an interim report for 2016 and data is not final.

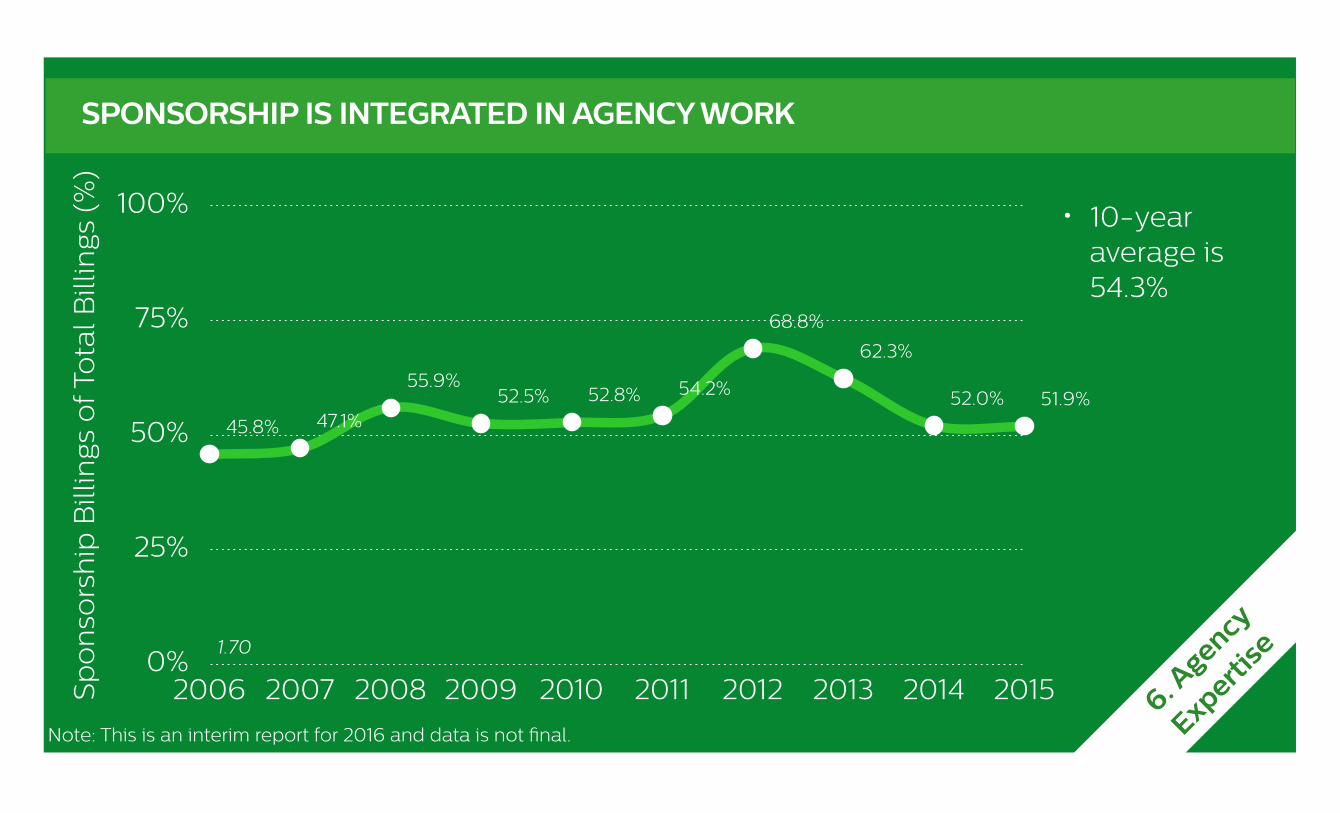

SPONSORSHIP IS INTEGRATED IN AGENCY WORK

0%

25%

50%

75%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

45.8% 47.1%

55.9%52.5% 52.8% 54.2%

68.8%

62.3%

52.0% 51.9%

Sp

on

sors

hip

Bill

ings

of T

ota

l Bill

ings

(%

)

1.70

6. Agency

Expertise

• 10-year average is 54.3%

Note: This is an interim report for 2016 and data is not final.

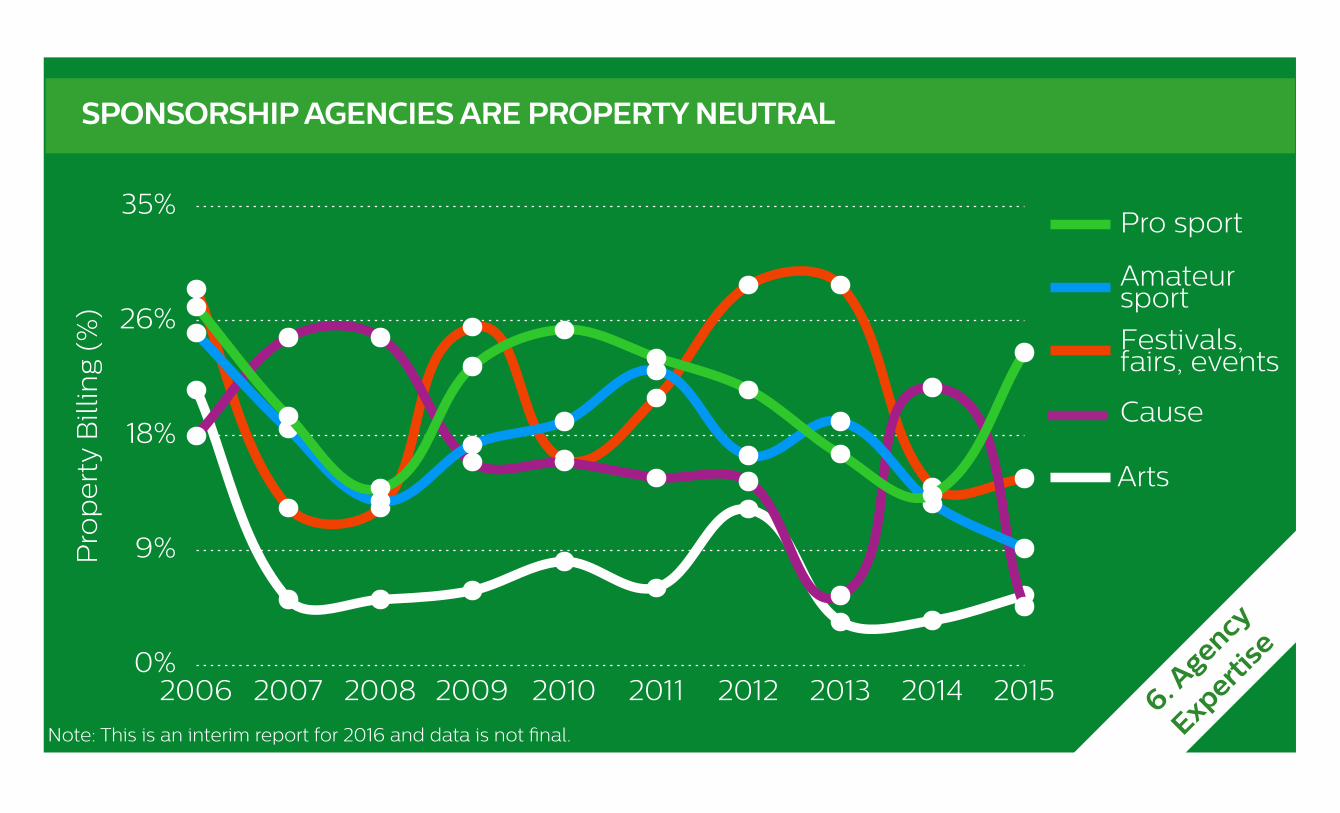

SPONSORSHIP AGENCIES ARE PROPERTY NEUTRAL

0%

9%

18%

26%

35%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Pro

pe

rty

Bill

ing

(%)

Festivals, fairs, events

Cause

Amateur sport

Pro sport

Arts

6. Agency

Expertise

Note: This is an interim report for 2016 and data is not final.

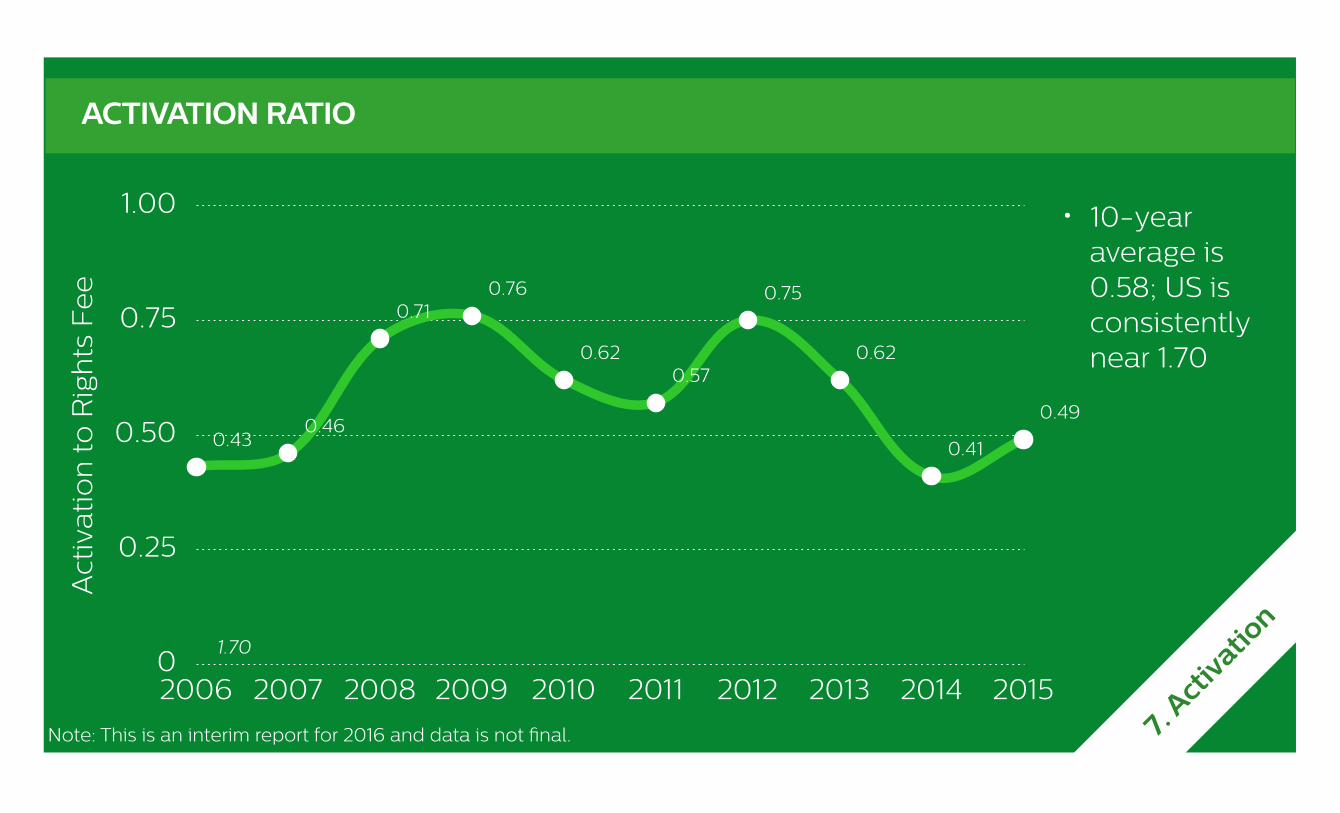

ACTIVATION RATIO

0

0.25

0.50

0.75

1.00

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

0.430.46

0.710.76

0.620.57

0.75

0.62

0.41

0.49

Act

ivat

ion

to

Rig

hts

Fe

e

1.70

7. Act

ivatio

n

• 10-year average is 0.58; US is consistently near 1.70

Note: This is an interim report for 2016 and data is not final.

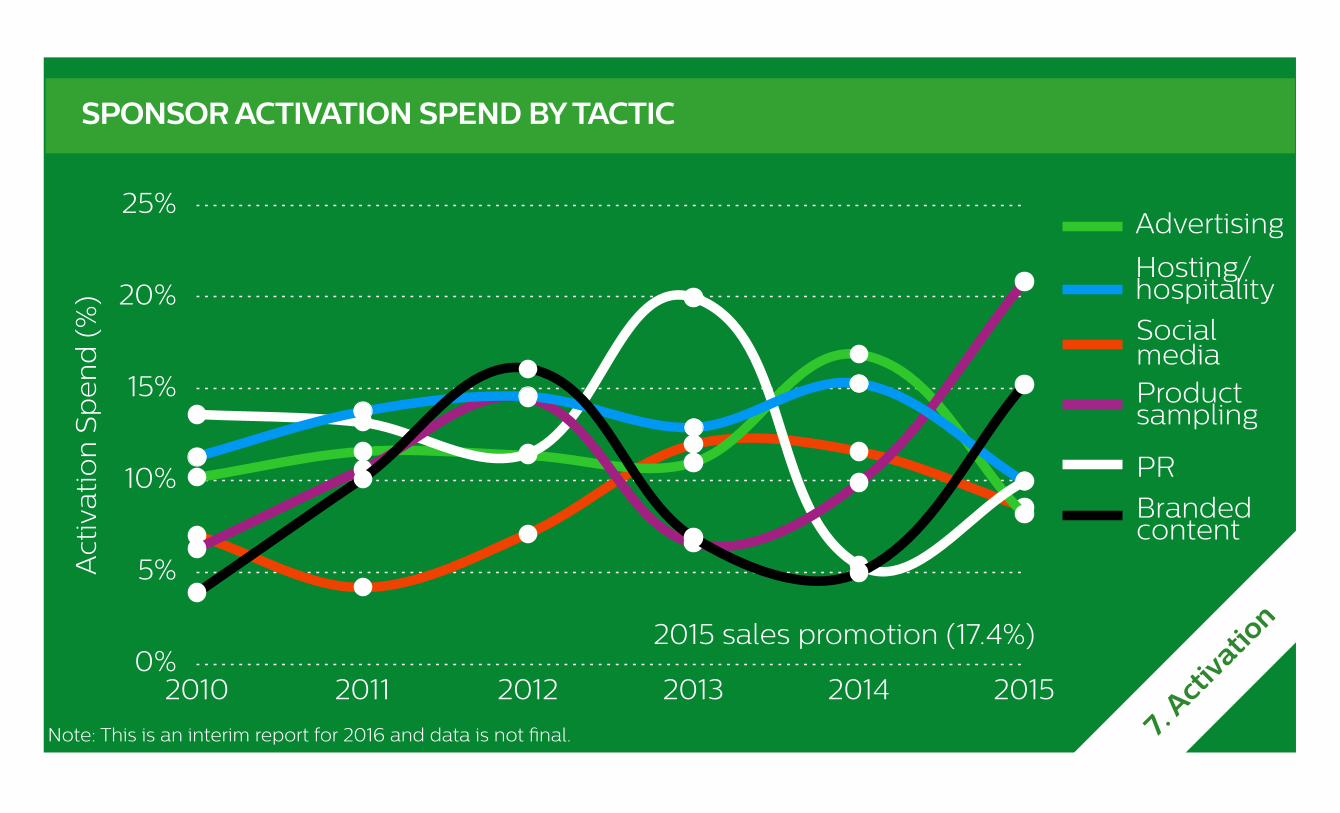

SPONSOR ACTIVATION SPEND BY TACTIC

0%

5%

10%

15%

20%

25%

2010 2011 2012 2013 2014 2015

Act

ivat

ion

Sp

en

d (

%)

Advertising

Social mediaProduct sampling

PR

Hosting/hospitality

Branded content

7. Act

ivatio

n2015 sales promotion (17.4%)

Note: This is an interim report for 2016 and data is not final.

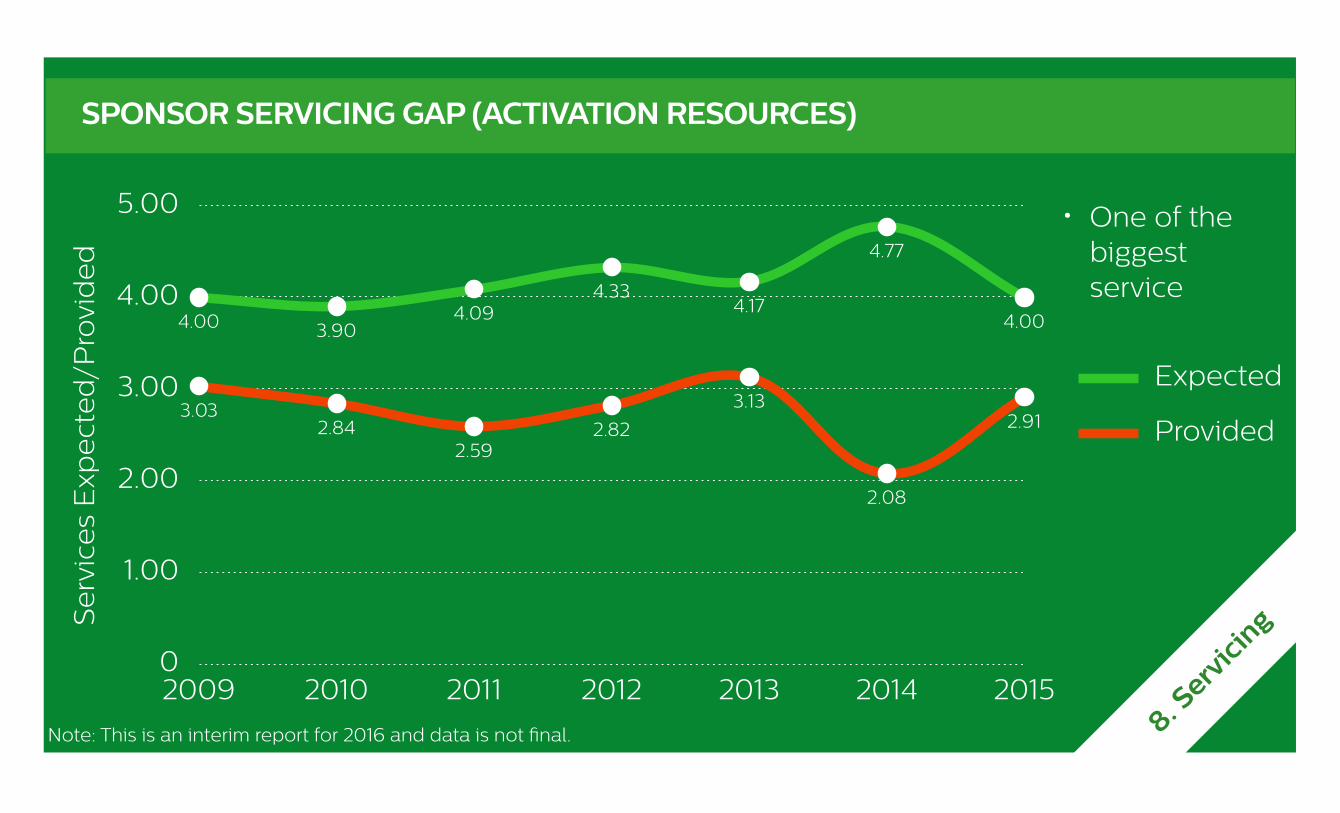

SPONSOR SERVICING GAP (ACTIVATION RESOURCES)

0

1.00

2.00

3.00

4.00

5.00

2009 2010 2011 2012 2013 2014 2015

3.032.84

2.592.82

3.13

2.08

2.91

4.00 3.904.09

4.334.17

4.77

4.00

Se

rvic

es

Exp

ect

ed

/Pro

vid

ed

Expected

Provided

8. Serv

icing

• One of the biggest service

Note: This is an interim report for 2016 and data is not final.

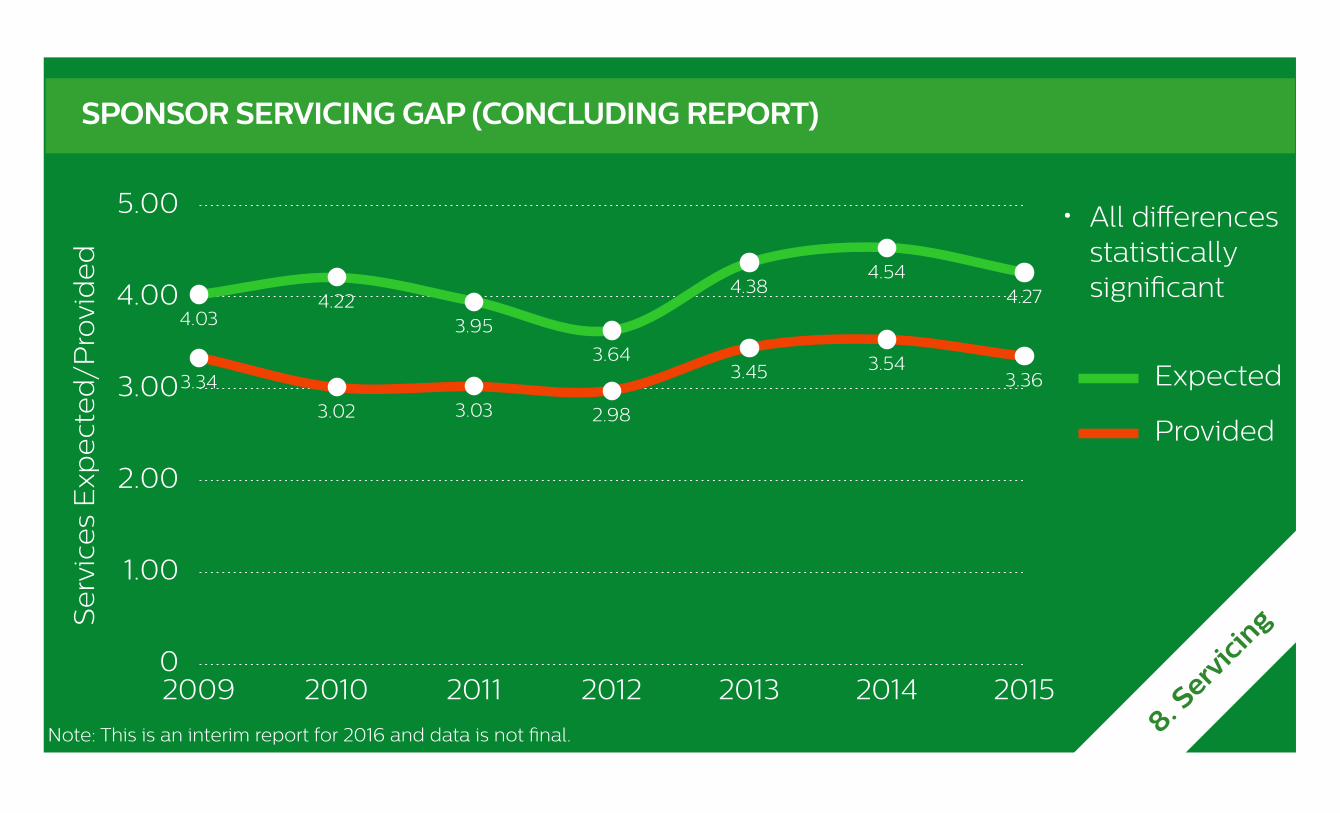

SPONSOR SERVICING GAP (CONCLUDING REPORT)

0

1.00

2.00

3.00

4.00

5.00

2009 2010 2011 2012 2013 2014 2015

3.34

3.02 3.03 2.98

3.45 3.543.36

4.034.22

3.95

3.64

4.384.54

4.27

Se

rvic

es

Exp

ect

ed

/Pro

vid

ed

8. Serv

icing

Expected

Provided

• All differences statistically significant

Note: This is an interim report for 2016 and data is not final.

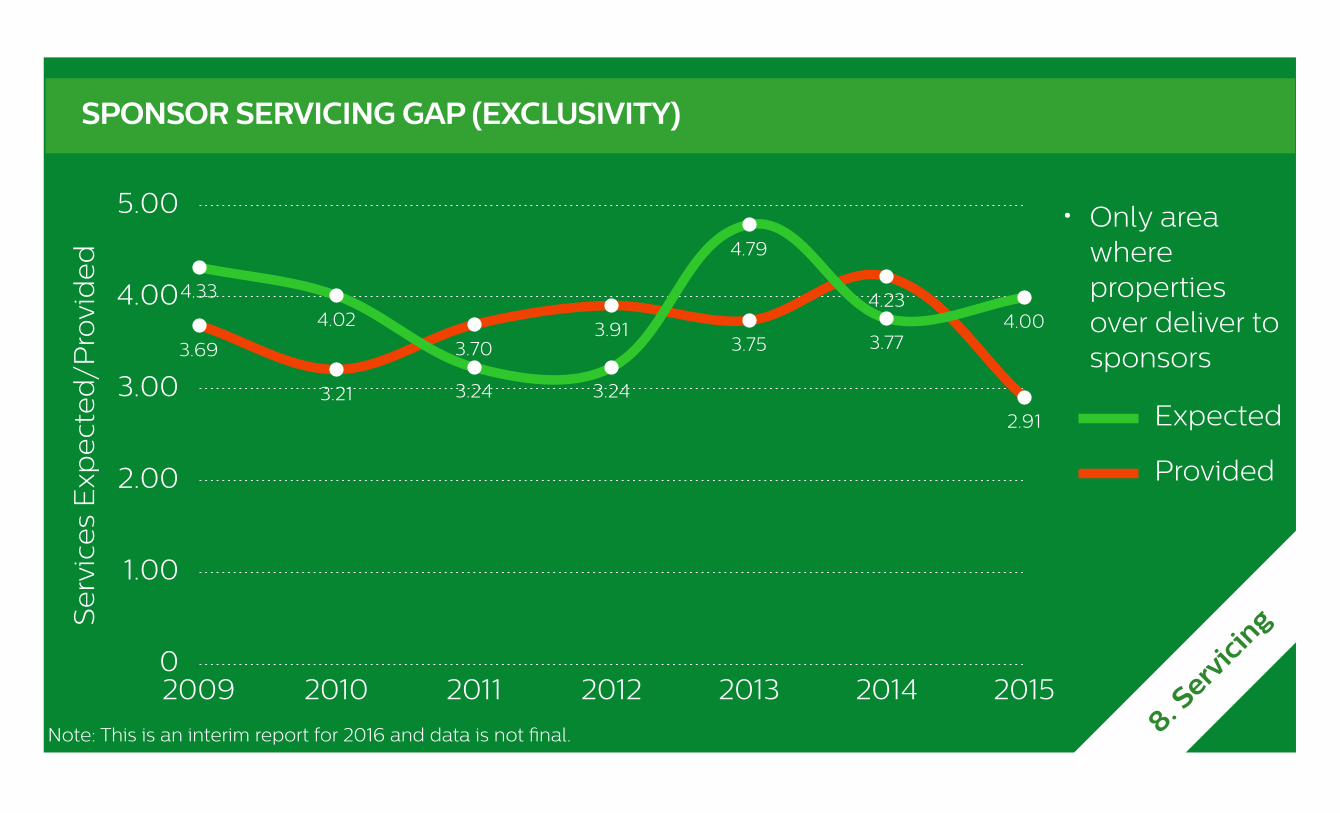

SPONSOR SERVICING GAP (EXCLUSIVITY)

0

1.00

2.00

3.00

4.00

5.00

2009 2010 2011 2012 2013 2014 2015

3.69

3.21

3.703.91

3.75

4.23

2.91

4.33

4.02

3.24 3.24

4.79

3.774.00

Se

rvic

es

Exp

ect

ed

/Pro

vid

ed

8. Serv

icing

Expected

Provided

• Only area where properties over deliver to sponsors

Note: This is an interim report for 2016 and data is not final.

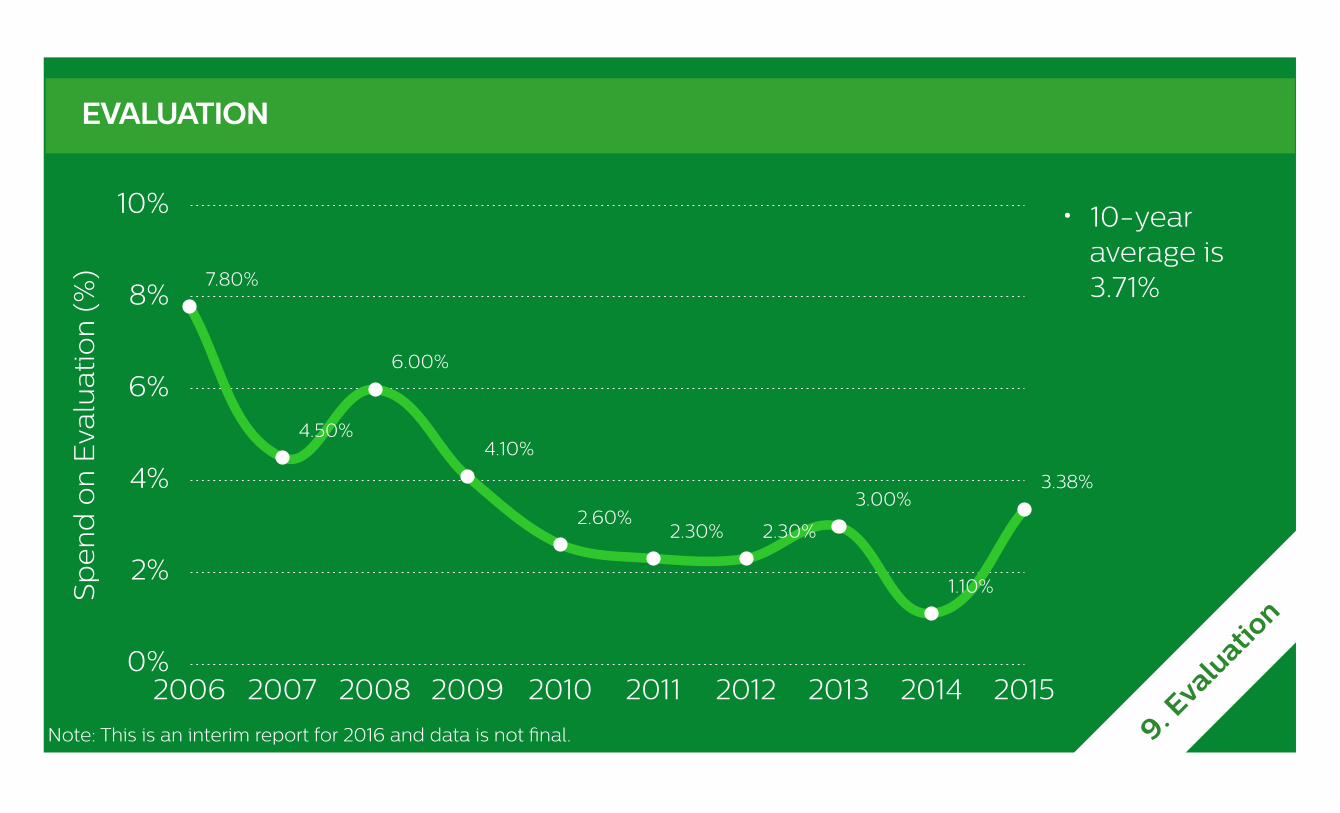

EVALUATION

0%

2%

4%

6%

8%

10%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

7.80%

4.50%

6.00%

4.10%

2.60%2.30% 2.30%

3.00%

1.10%

3.38%

Sp

en

d o

n E

valu

atio

n (

%)

9. Eva

luatio

n

• 10-year average is 3.71%

Note: This is an interim report for 2016 and data is not final.

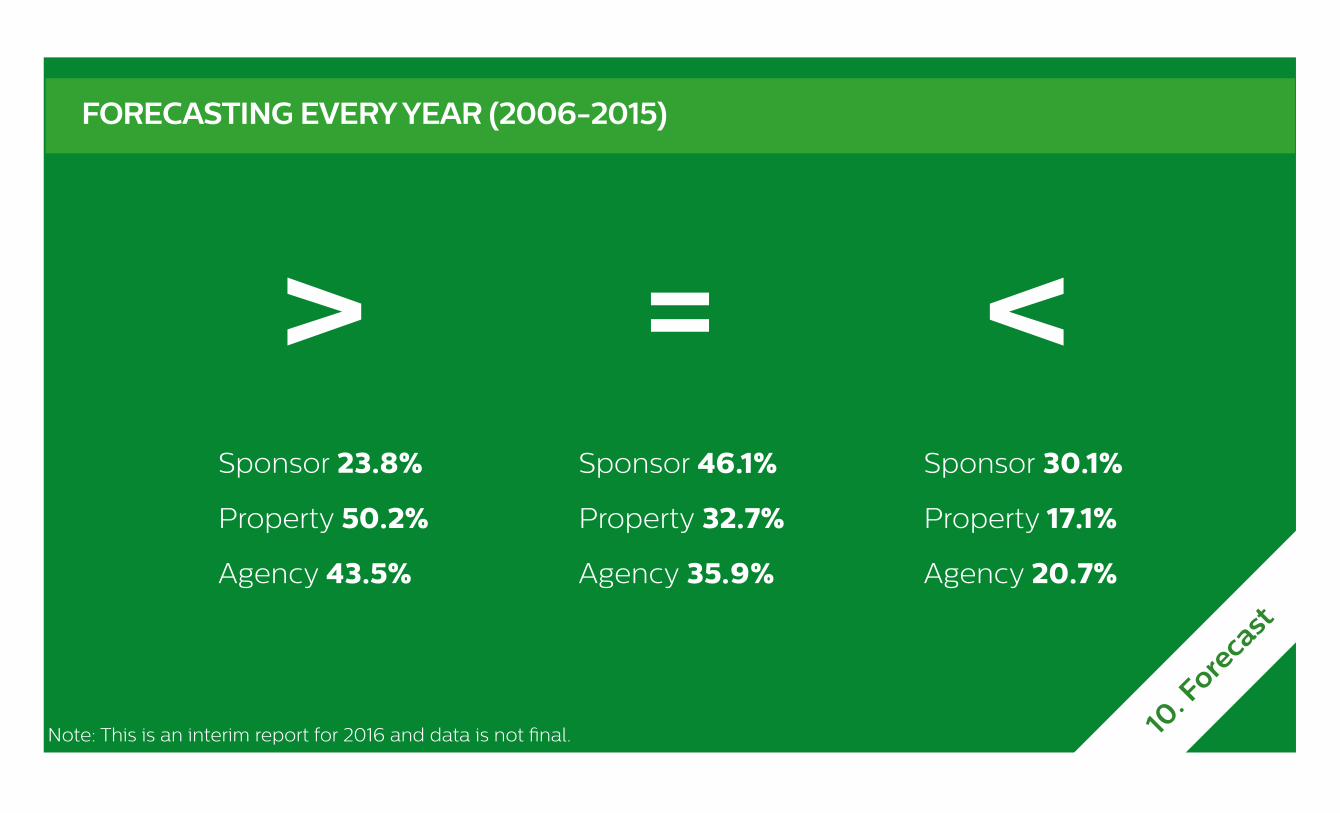

FORECASTING EVERY YEAR (2006-2015)

Sponsor 23.8%

Property 50.2%

Agency 43.5%

>Sponsor 46.1%

Property 32.7%

Agency 35.9%

=Sponsor 30.1%

Property 17.1%

Agency 20.7%

<

10. F

oreca

st

Note: This is an interim report for 2016 and data is not final.

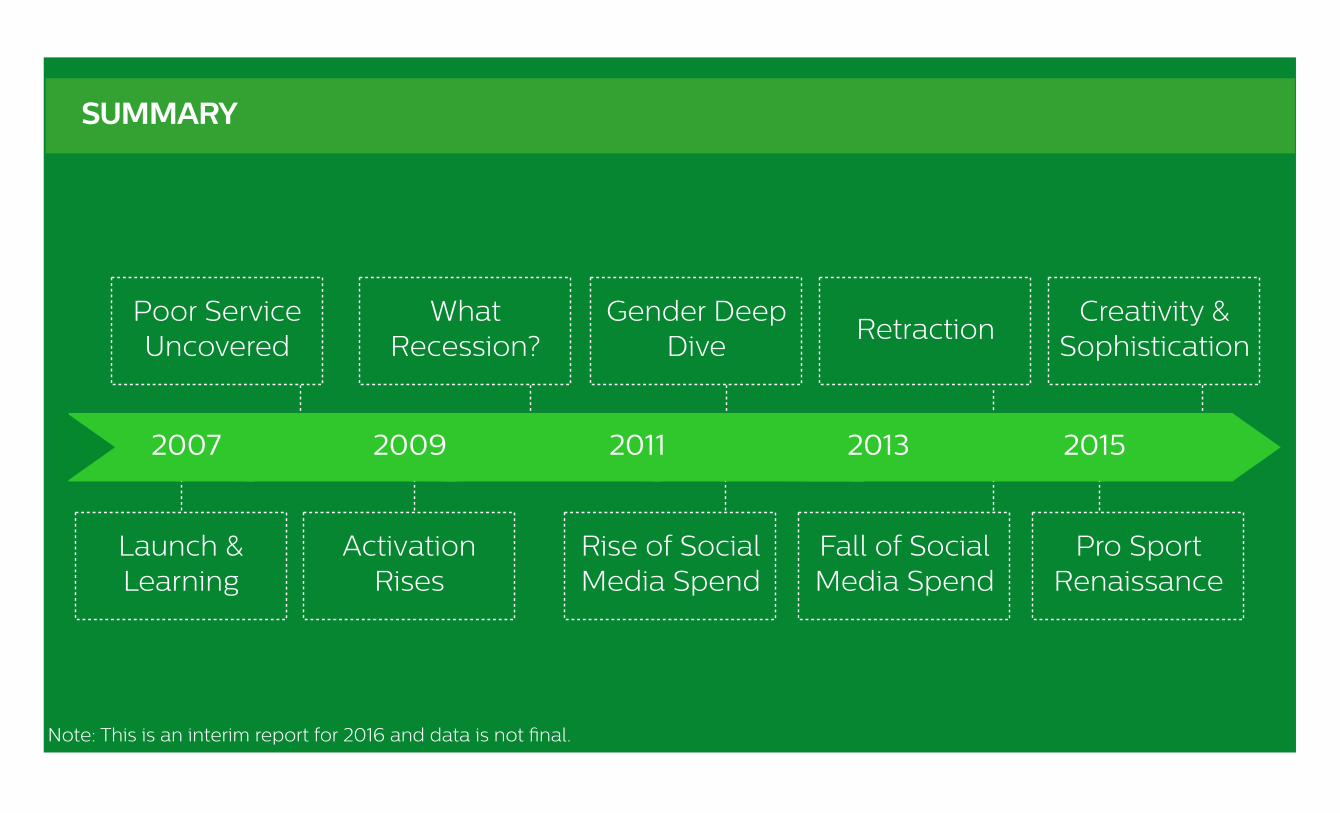

SUMMARY

Launch & Learning

Activation Rises

What Recession?

RetractionCreativity &

Sophistication

Rise of Social Media Spend

Fall of Social Media Spend

Poor Service Uncovered

20152013201120092007

Gender Deep Dive

Pro Sport Renaissance

Note: This is an interim report for 2016 and data is not final.

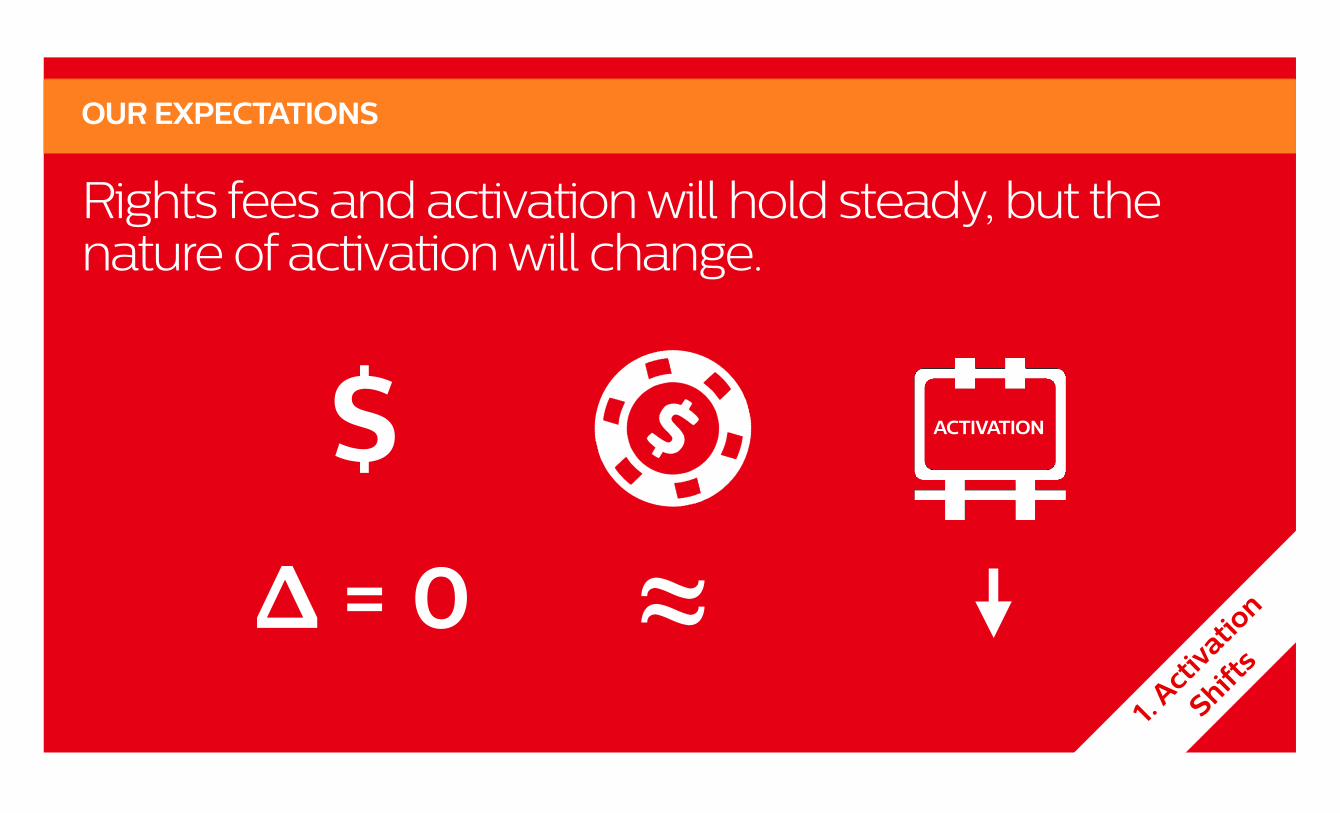

What’s Next?OUR EXPECTATIONS

Rights fees and activation will hold steady, but the nature of activation will change.

$ ACTIVATION

OUR EXPECTATIONS

1. Act

ivatio

n

Shifts

≈Δ = 0

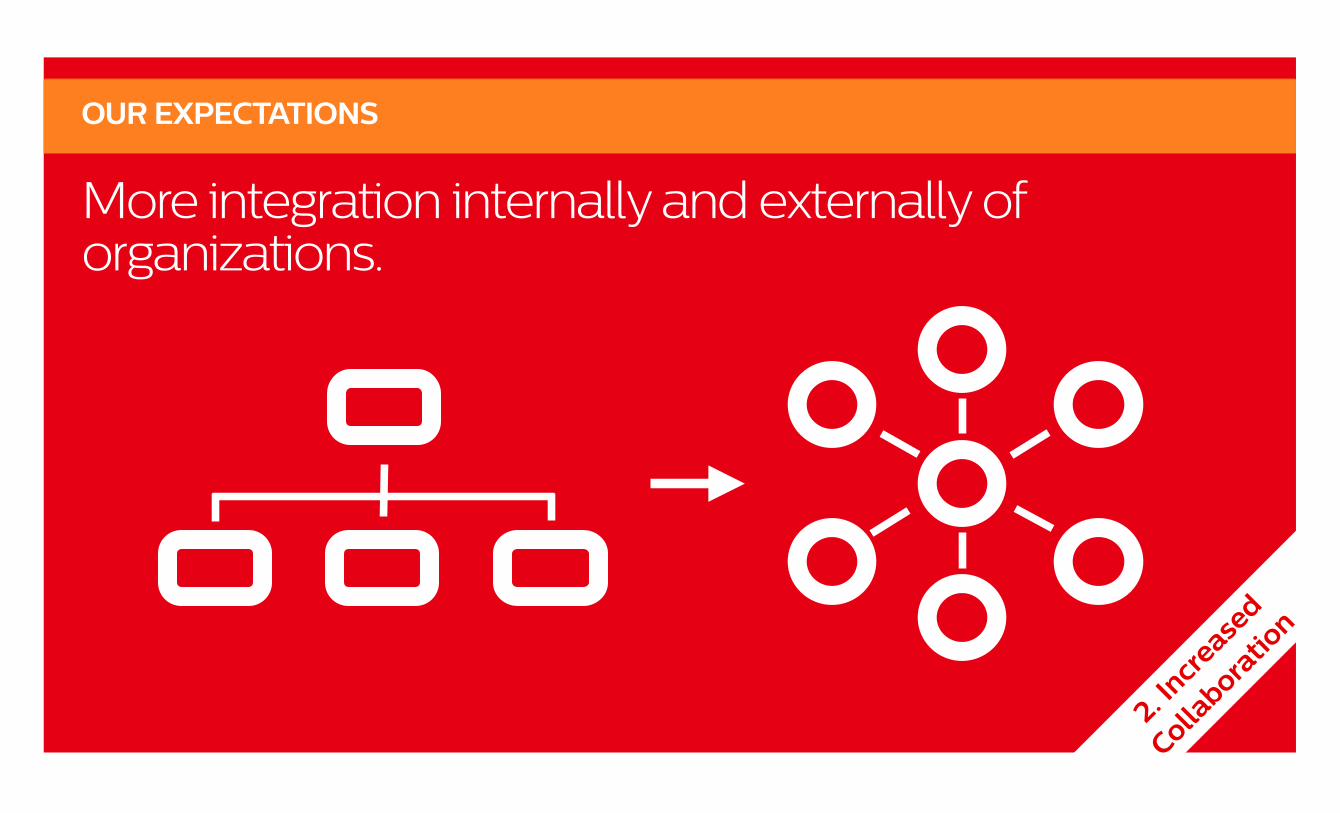

More integration internally and externally of organizations.

OUR EXPECTATIONS

2. Incr

eased

Collabora

tion

Social media will fall as a target of activation investment.

OUR EXPECTATIONS

3. Socia

l Media

Integrating across traditional and new platforms.

OUR EXPECTATIONS

4. Dig

itiza

tion

Live content will continue its reign as a driver of sponsorship investment.

OUR EXPECTATIONS

5. Conte

nt

Partners

hips

Festivalization is a fundamental activation platform.

OUR EXPECTATIONS

6. Fest

ivals

Cause will need to be an integral component of all great sponsorships.

=+

OUR EXPECTATIONS

7. Gre

ater C

ause

Sponsorship marketers will be come more strategic about who they want to interact with.

OUR EXPECTATIONS

8. Targ

et

Mark

ets

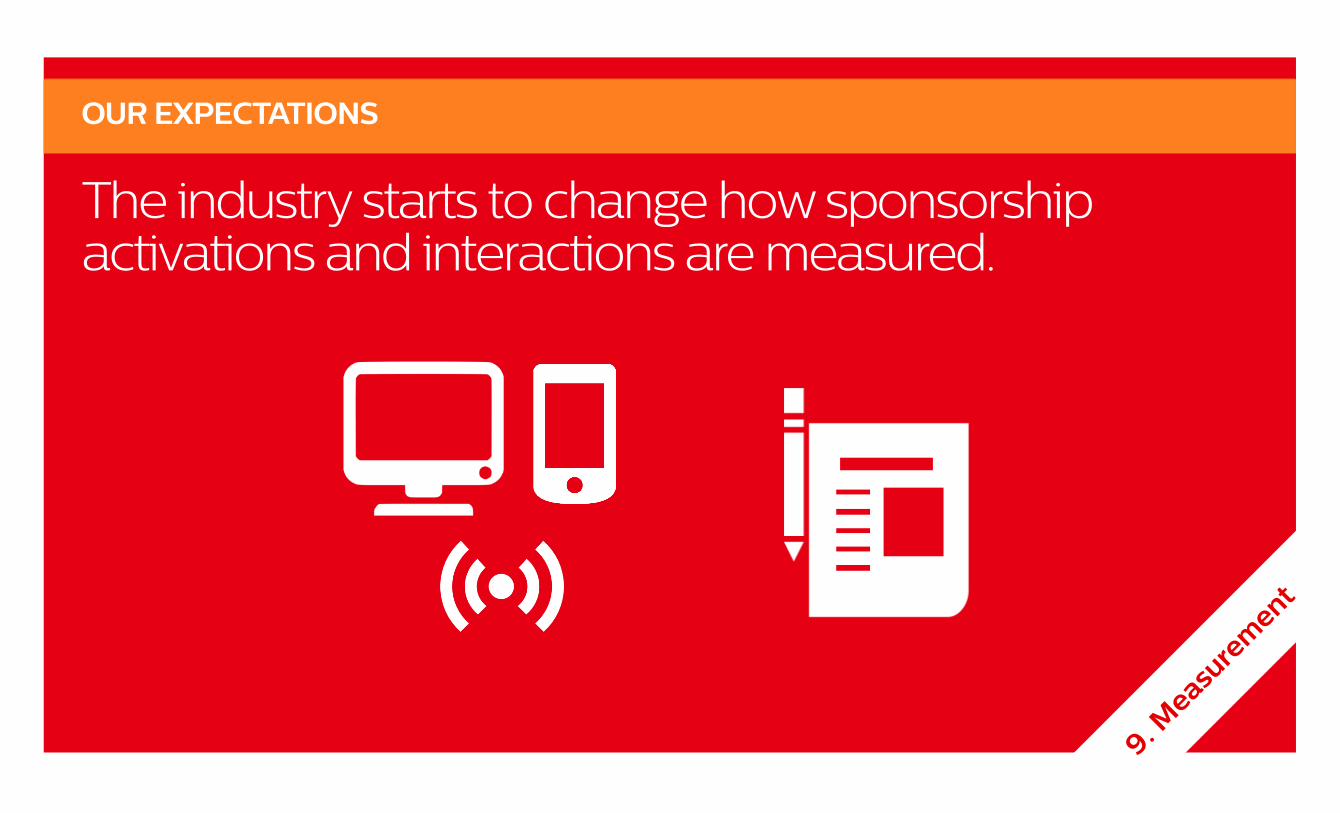

The industry starts to change how sponsorship activations and interactions are measured.

OUR EXPECTATIONS

9. Measu

rem

ent

More formalized training, education, resources and experiences.

OUR EXPECTATIONS

10. T

alent

Survey is open until April 15, 2016.

Visit www.sponsorshiplandscape.ca to enter responses!

THANK YOU!