11.1 © 2006 by prentice hall welcome. 11.2 © 2006 by prentice hall title of the thesis...

TRANSCRIPT

11.1 © 2006 by Prentice Hall

WelcomeWelcome

11.2 © 2006 by Prentice Hall

Title of the ThesisTitle of the Thesis

Productivity Improvement of a Sewing Line in a Selected Company of Ready

Made Garment Industry by Using Assembly Line Balancing Technique

Presented By

Md. Anwar HossenReg. No. 2003334049

Md. Shakil KhanReg. No. 2003334034

11.3 © 2006 by Prentice Hall

Now the business world is very dynamic and competitive.

This competitive situation can only be managed by applying operations management tools.

As example, for repetitive production system Assembly Line Balancing is very effective tool.

Line balancing can ensure the improvement of: efficiency production rate productivity and

Reduction of: idle time resource utilization production cost etc.

IntroductionIntroduction

11.4 © 2006 by Prentice Hall

ObjectivesObjectives

To evaluate the existing assembly line for finding the current status

To reduce idle time, if any

To improve productivity, if possible

11.5 © 2006 by Prentice Hall

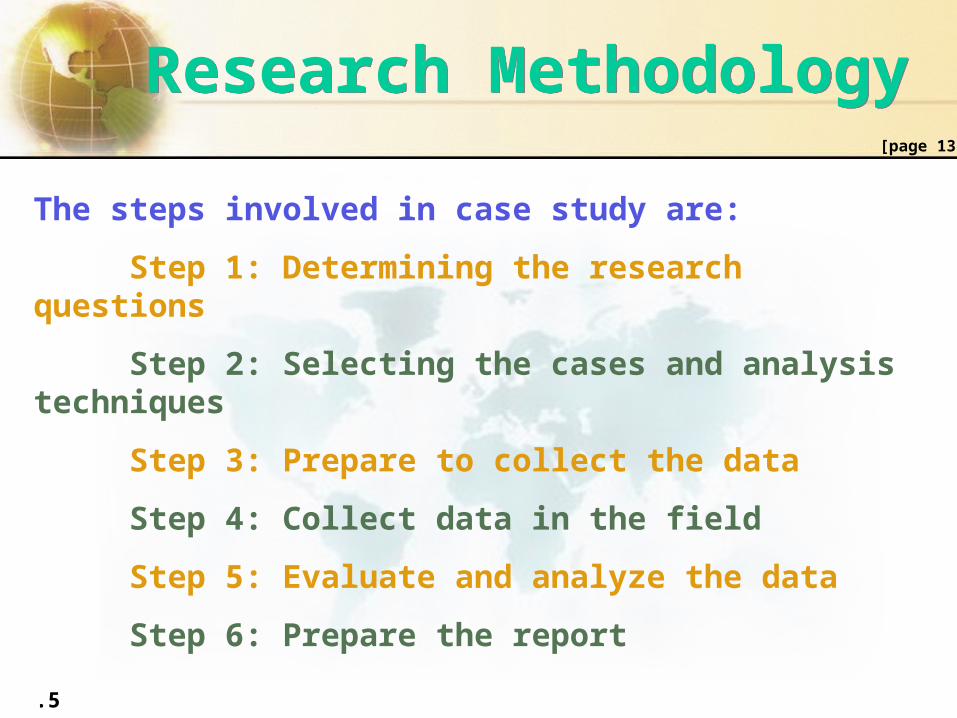

Research MethodologyResearch Methodology

The steps involved in case study are:

Step 1: Determining the research questions

Step 2: Selecting the cases and analysis techniques

Step 3: Prepare to collect the data

Step 4: Collect data in the field

Step 5: Evaluate and analyze the data

Step 6: Prepare the report

[page 13]

11.6 © 2006 by Prentice Hall

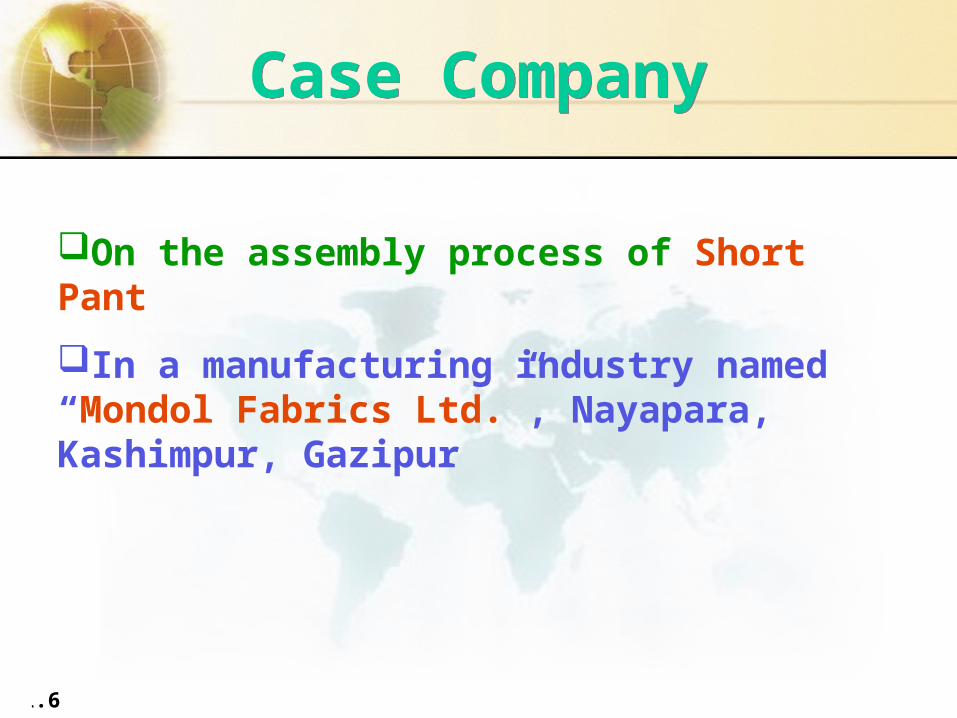

Case CompanyCase Company

On the assembly process of Short Pant

In a manufacturing industry named “Mondol Fabrics Ltd.”, Nayapara, Kashimpur, Gazipur

11.7 © 2006 by Prentice Hall

Tools & TechniquesTools & TechniquesEvaluation parameters of existing assembly process:

efficiency

idle time

production time

production rate

production cost &

productivity

Scientific technique “Six-Step Assembly Line Balancing”

Improvement analysis “Sequential Improvement Technique”

11.8 © 2006 by Prentice Hall

Evaluation Evaluation

11.9 © 2006 by Prentice Hall

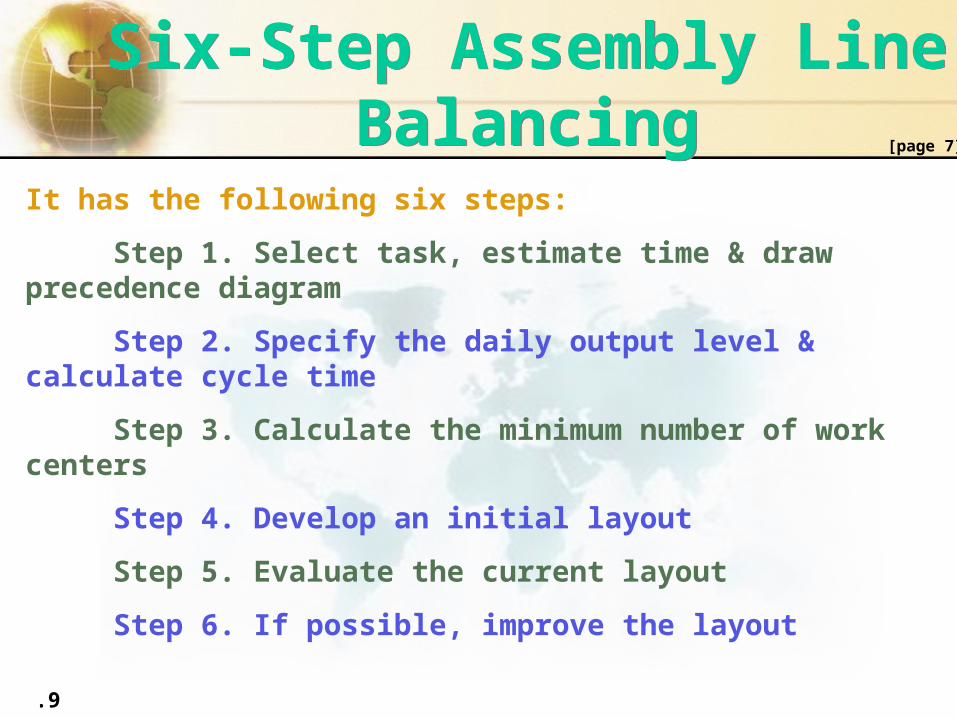

Six-Step Assembly Line Balancing

Six-Step Assembly Line Balancing

It has the following six steps:

Step 1. Select task, estimate time & draw precedence diagram

Step 2. Specify the daily output level & calculate cycle time

Step 3. Calculate the minimum number of work centers

Step 4. Develop an initial layout

Step 5. Evaluate the current layout

Step 6. If possible, improve the layout

[page 7]

11.10 © 2006 by Prentice Hall

Time StudyTime Study

Time study is the combination of a series of activities as follows:

Step 1: Define the Task

Step 2: Breaking the Job into Elements

Step 3: Estimate the Required Number of Observation

Step 4: Record the Times and Ratings of Performance

Step 5: Average Observed Time

Step 6: Normal Time

Step 7: Allowance

Step 8: Standard Time

[page 3]

11.11 © 2006 by Prentice Hall

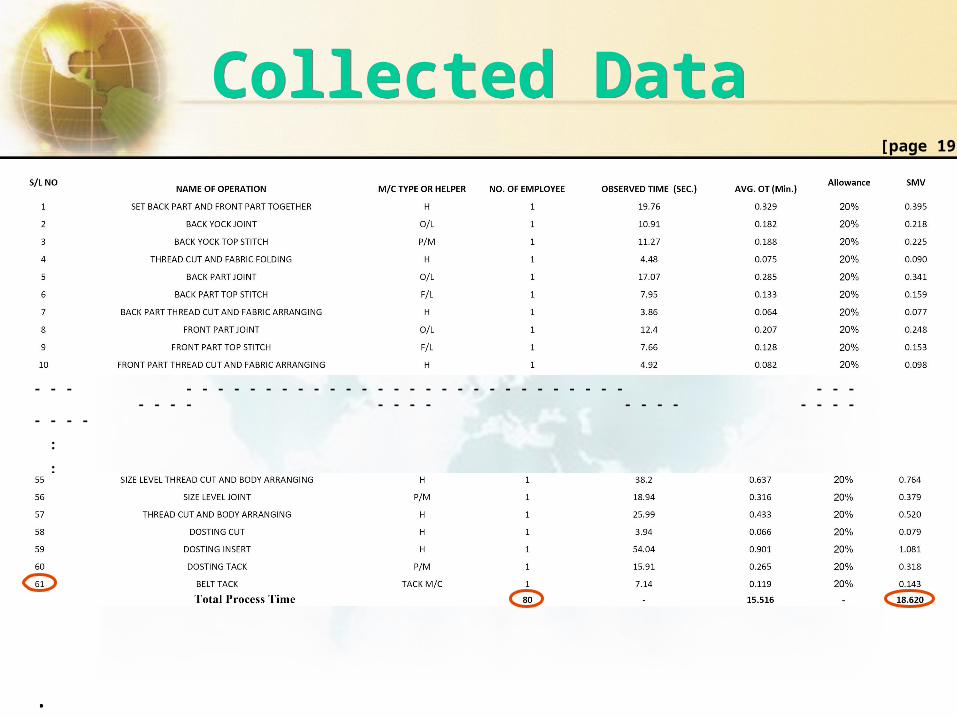

Collected DataCollected Data

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

:

:

:

[page 19]

11.12 © 2006 by Prentice Hall

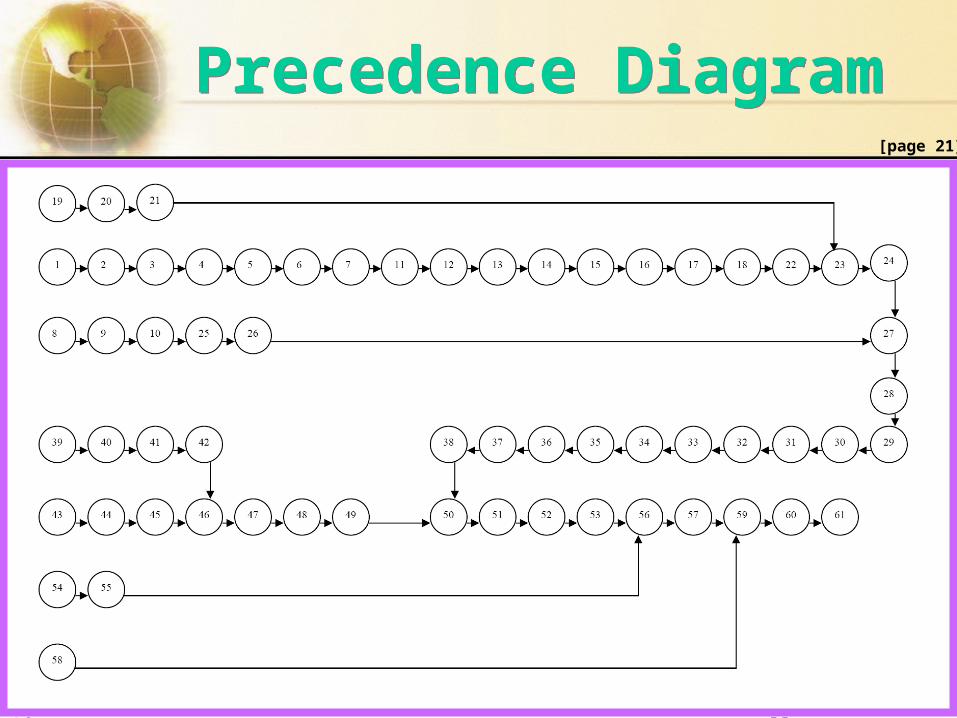

Precedence DiagramPrecedence Diagram[page 21]

11.13 © 2006 by Prentice Hall

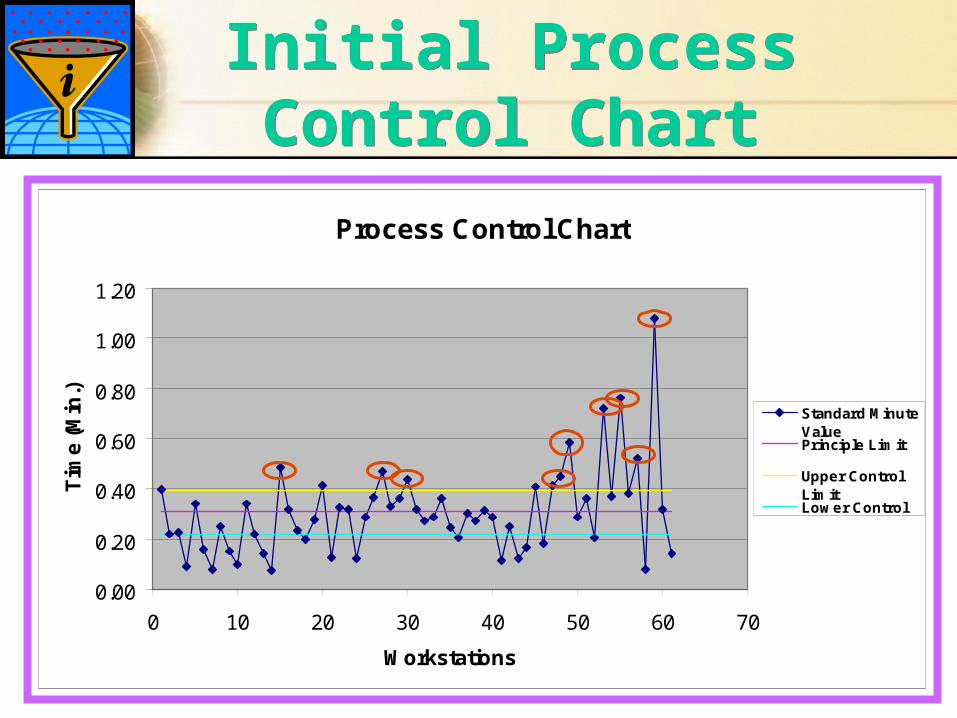

Initial Process Control Chart

Initial Process Control Chart

Process Control Chart

0.00

0.20

0.40

0.60

0.80

1.00

1.20

0 10 20 30 40 50 60 70

Workstations

Tim

e (

Min

.)

Standard MinuteValuePrinciple Limit

Upper ControlLimitLower ControlLimit

11.14 © 2006 by Prentice Hall

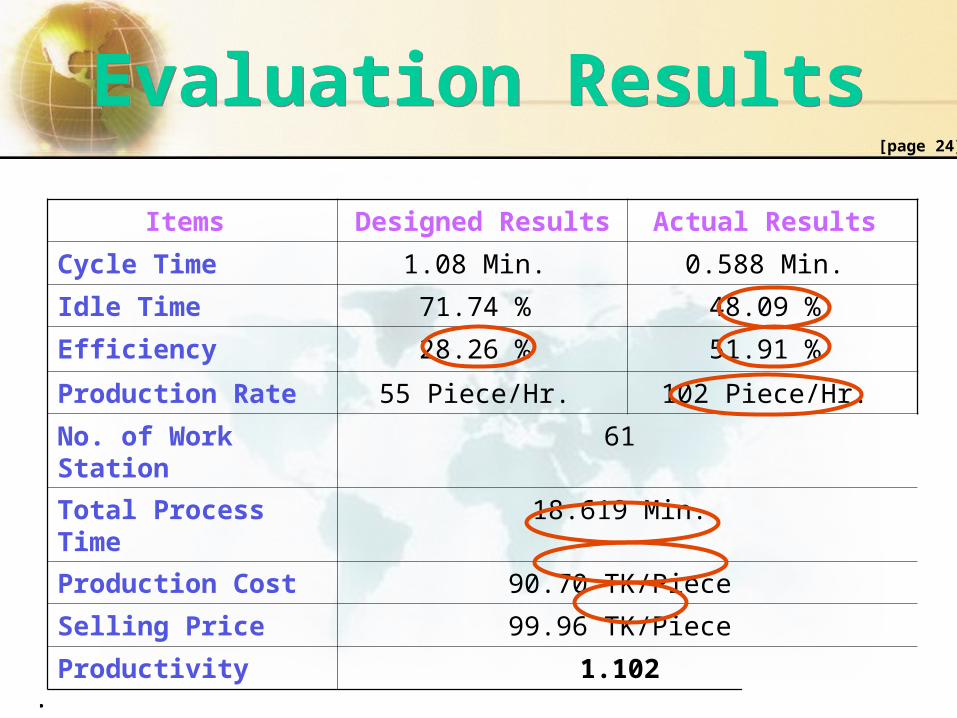

Evaluation ResultsEvaluation Results

Items Designed Results Actual Results

Cycle Time 1.08 Min. 0.588 Min.

Idle Time 71.74 % 48.09 %

Efficiency 28.26 % 51.91 %

Production Rate 55 Piece/Hr. 102 Piece/Hr.

No. of Work Station 61

Total Process Time 18.619 Min.

Production Cost 90.70 TK/Piece

Selling Price 99.96 TK/Piece

Productivity 1.102

[page 24]

11.15 © 2006 by Prentice Hall

Improvement Improvement

11.16 © 2006 by Prentice Hall

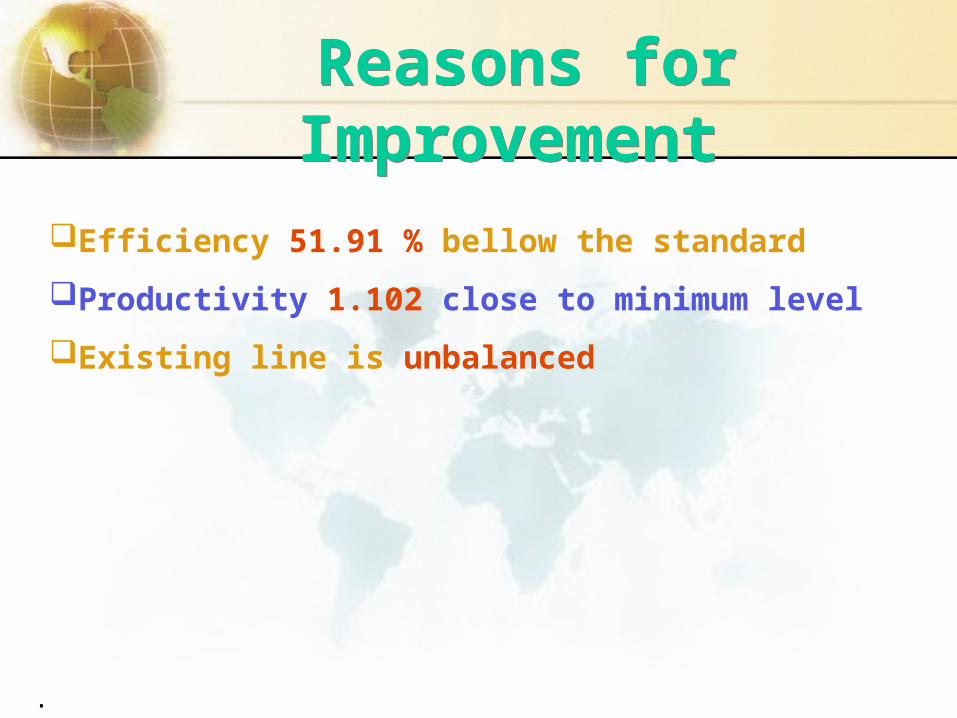

Reasons for Improvement Reasons for

Improvement Efficiency 51.91 % bellow the standard

Productivity 1.102 close to minimum level

Existing line is unbalanced

11.17 © 2006 by Prentice Hall

Sequential Improvement

Technique

Sequential Improvement

TechniqueIt has three sequential steps:

Step 1: Withdrawal of Idle Resources

Step 2: Redistribution of Tasks

Step 3: Bottleneck Reduction

a. By Existing Resources &

b. By Additional Resources

[page 9]

11.18 © 2006 by Prentice Hall

Summary after Withdrawal of Idle

Resources

Summary after Withdrawal of Idle

Resources Items Before Improvement After Improvement

Cycle Time 1.08 Min. 1.08 Min.

Idle Time 71.74 % 70.86 %

Efficiency 28.26 % 29.14 %

Production Rate 55 Piece/Hr. 55 Piece/Hr.

No. of Work Station 61

Total Process Time 18.619 Min. 19.217 Min.

No. of M/C & Operator 46 41

No. of Helper 34 33

[page 28]

11.19 © 2006 by Prentice Hall

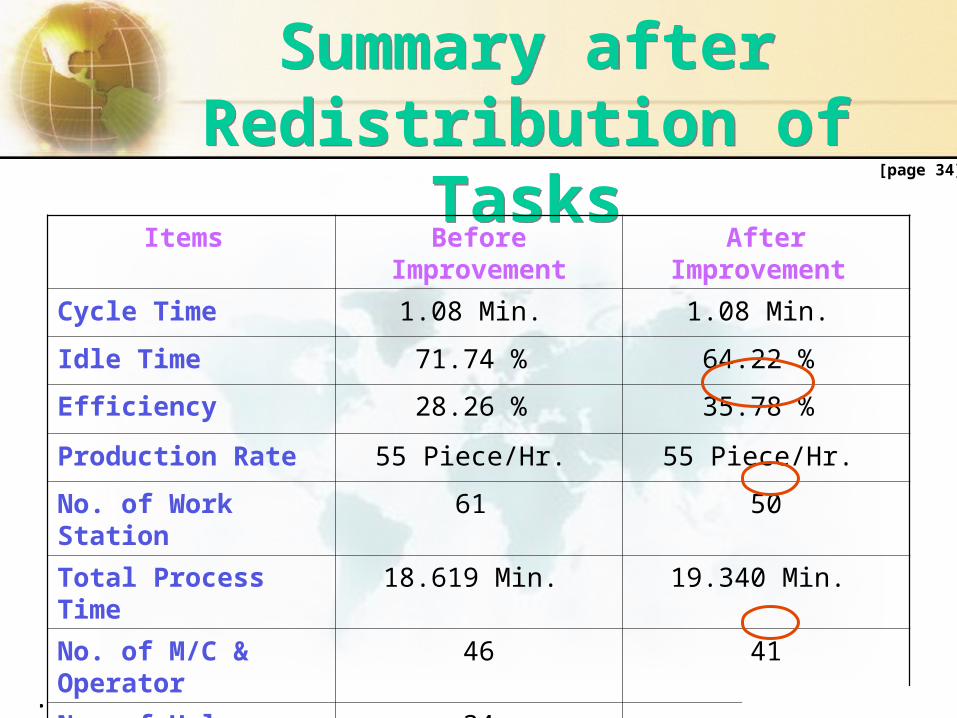

Summary afterRedistribution of Tasks

Summary afterRedistribution of Tasks

Items Before Improvement After Improvement

Cycle Time 1.08 Min. 1.08 Min.

Idle Time 71.74 % 64.22 %

Efficiency 28.26 % 35.78 %

Production Rate 55 Piece/Hr. 55 Piece/Hr.

No. of Work Station 61 50

Total Process Time 18.619 Min. 19.340 Min.

No. of M/C & Operator 46 41

No. of Helper 34 22

[page 34]

11.20 © 2006 by Prentice Hall

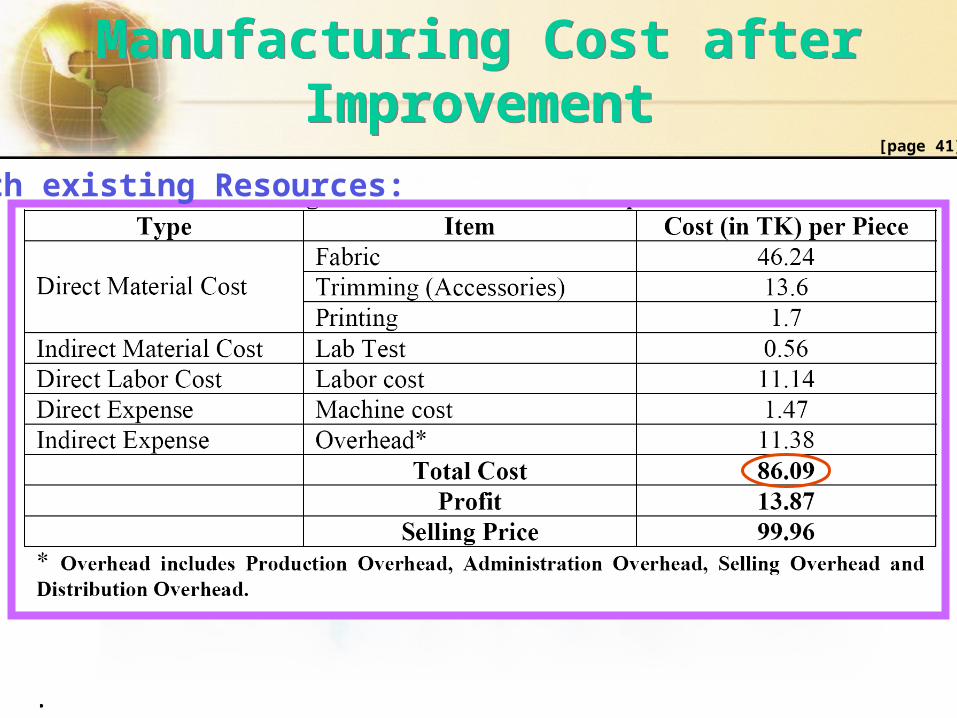

Manufacturing Cost after Improvement

Manufacturing Cost after Improvement

With existing Resources:[page 41]

11.21 © 2006 by Prentice Hall

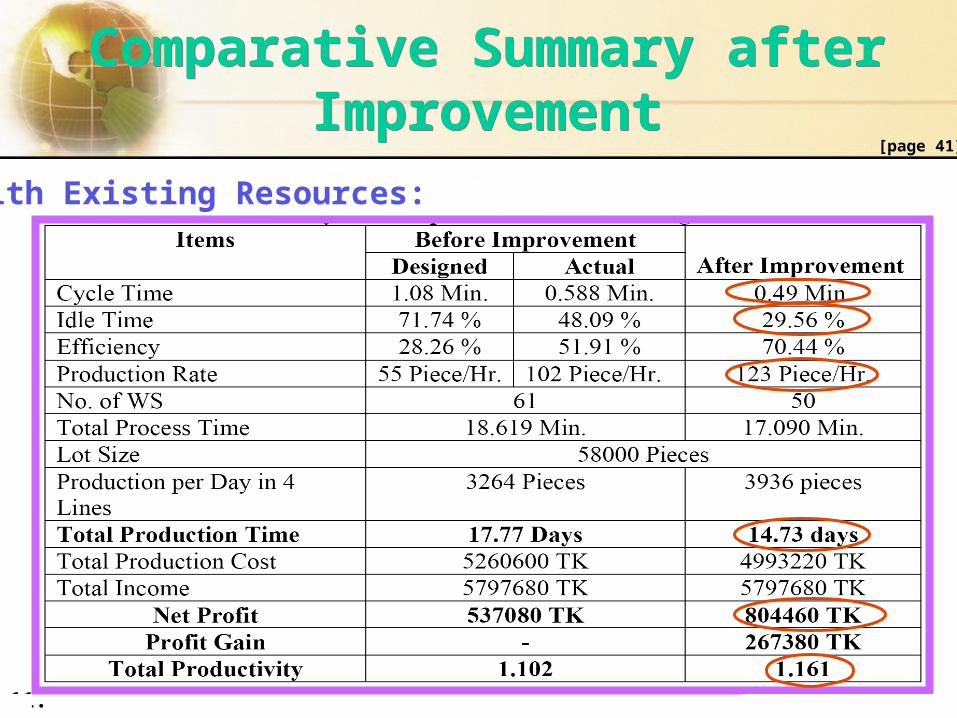

Comparative Summary after Improvement

Comparative Summary after Improvement

With Existing Resources:

[page 41]

11.22 © 2006 by Prentice Hall

Manufacturing Cost after Improvement

Manufacturing Cost after Improvement

With Additional Resources:[page 42]

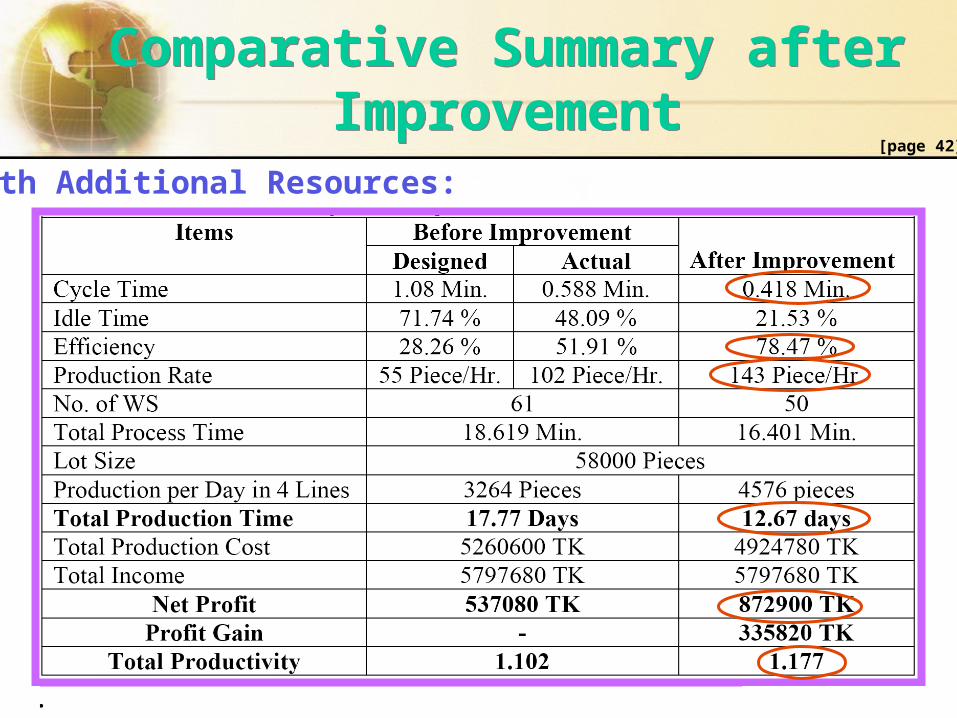

11.23 © 2006 by Prentice Hall

Comparative Summary after Improvement

Comparative Summary after Improvement

With Additional Resources:[page 42]

11.24 © 2006 by Prentice Hall

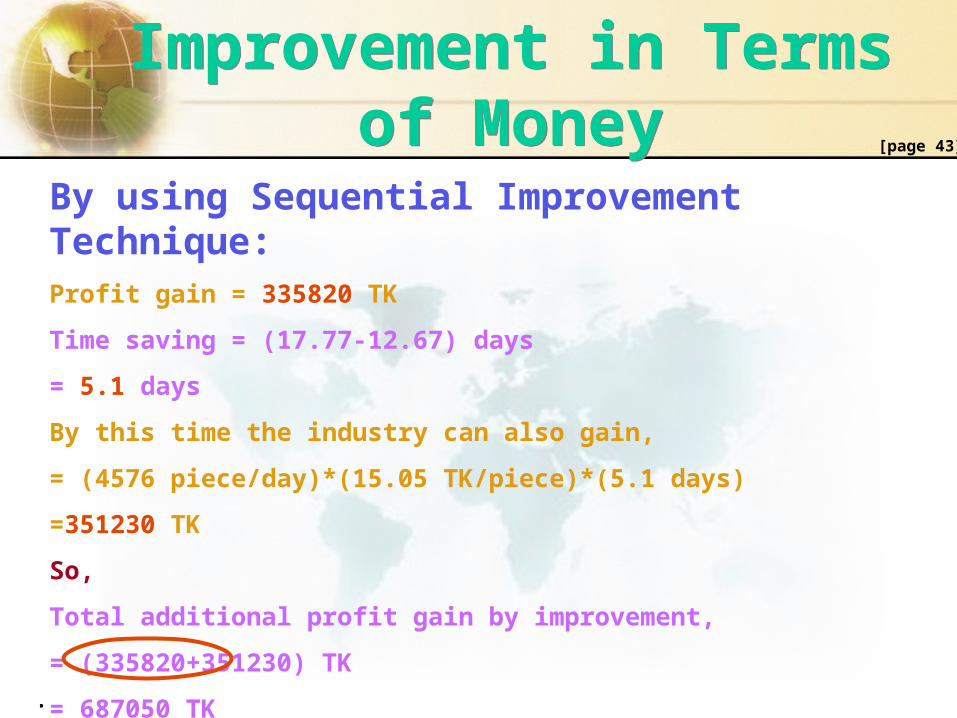

Improvement in Terms of Money

Improvement in Terms of Money

By using Sequential Improvement Technique:Profit gain = 335820 TK

Time saving = (17.77-12.67) days

= 5.1 days

By this time the industry can also gain,

= (4576 piece/day)*(15.05 TK/piece)*(5.1 days)

=351230 TK

So,

Total additional profit gain by improvement,

= (335820+351230) TK

= 687050 TK

[page 43]

11.25 © 2006 by Prentice Hall

Achievement of Objectives

Achievement of Objectives

11.26 © 2006 by Prentice Hall

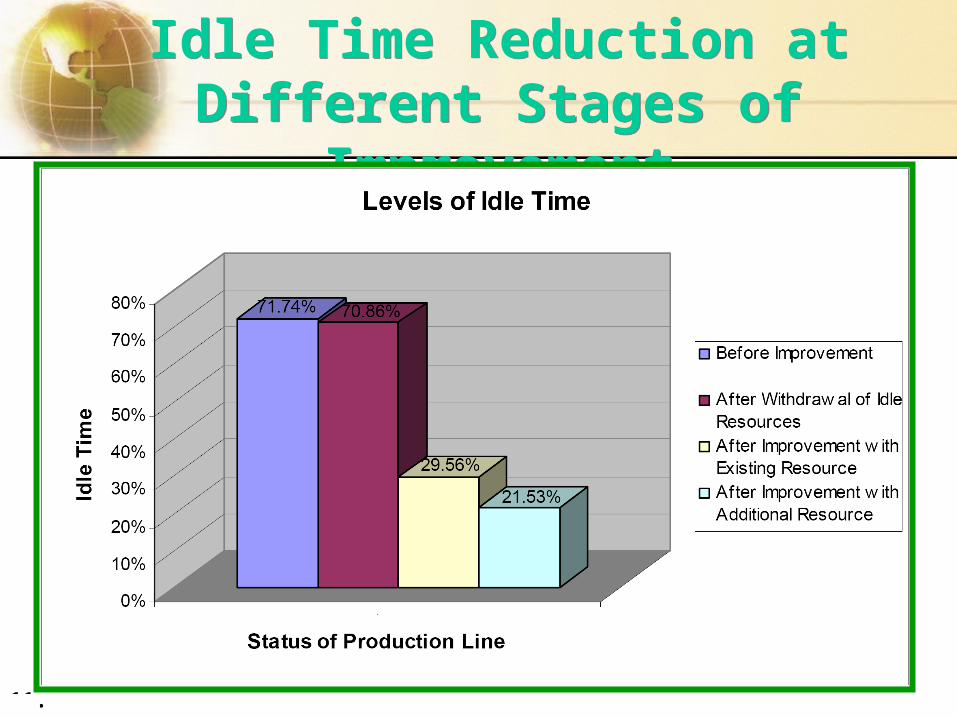

Idle Time Reduction at Different Stages of

Improvement

Idle Time Reduction at Different Stages of

Improvement

11.27 © 2006 by Prentice Hall

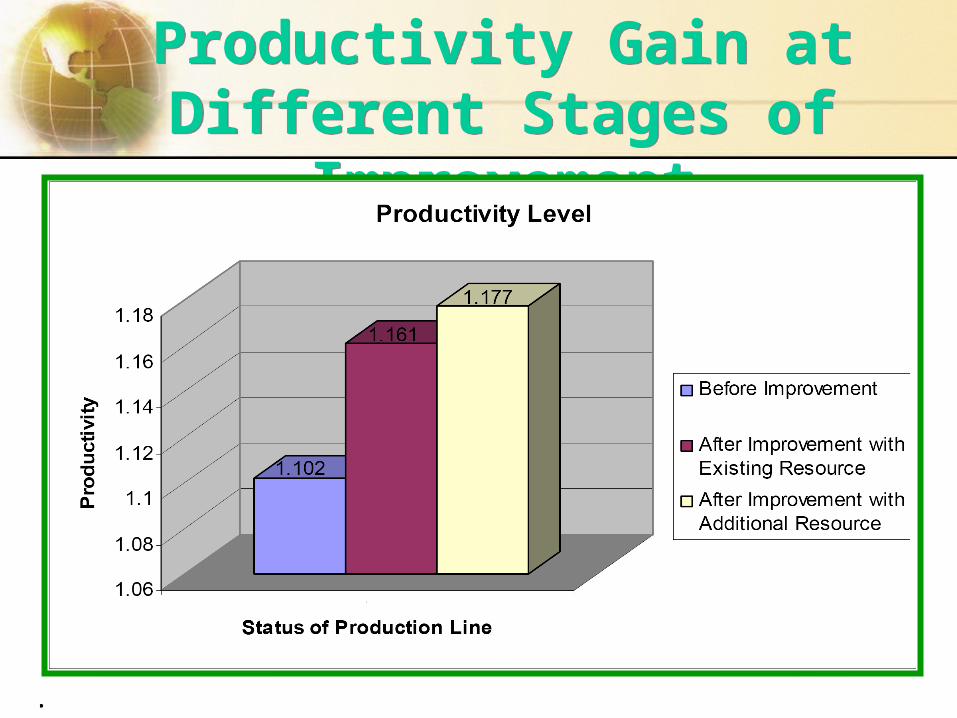

Productivity Gain at Different Stages of

Improvement

Productivity Gain at Different Stages of

Improvement

11.28 © 2006 by Prentice Hall

Analytical Results Considering Different

Allowance

Analytical Results Considering Different

Allowance

11.29 © 2006 by Prentice Hall

Productivity Gain for Different Allowance Productivity Gain for Different Allowance

11.30 © 2006 by Prentice Hall

Efficiency Gain for Different Allowance

Efficiency Gain for Different Allowance

11.31 © 2006 by Prentice Hall

Errors/Mistakes in Our Report

Errors/Mistakes in Our Report

11.32 © 2006 by Prentice Hall

Major MistakesMajor MistakesIn page 1: A world dominating business sector can fall down suddenly. (organization)

In page 4: Average observed valve. (value)

In page 15: After Introduction we have used STEP: ONE. (before STEP: ONE will be 4.2 Six-Step Assembly Line Balancing & after STEP: ONE will be 4.2.1 Time Study)

In page 25 & 28: The given control charts are wrong.

In page 34: We have used 39.3 % allowance. (20 %).

In page 37: Typing mistake for value of SSV & SMV.

11.33 © 2006 by Prentice Hall

Limitations of this Thesis

Limitations of this Thesis

11.34 © 2006 by Prentice Hall

Limitations Limitations

Assumption about the current method.

Omission of performance rating.

Omission of cross study for different product.

Lack of our experience.

11.35 © 2006 by Prentice Hall

Thank YouThank You

11.36 © 2006 by Prentice Hall

Questions ???Questions ???