1.1.5 a comparative study of individual variable insurance ... comparative... · 07/05/1999 ·...

TRANSCRIPT

1.1.5 A Comparative Study of Individual VariableInsurance Contracts (Segregated Funds)and Mutual Funds

A COMPARATIVE STUDY OF INDIVIDUAL VARIABLEINSURANCE CONTRACTS (Segregated Funds) and

Mutual Funds

Prepared for the Canadian Securities Administrators and the

Canadian Council of Insurance Regulators

May 7, 1999

A. Executive Summary

The Canadian Securities Administrators (CSA) and theCanadian Council of Insurance Regulators (CCIR) are of theview that it is important for both regulators to understand theinvestment products they each regulate and their respectiveregimes of regulation. The CSA regulate mutual funds and theCCIR regulate individual variable insurance contracts (IVICs) andthe segregated funds which determine the value of an IVIC.Mutual funds and IVICs/segregated funds are forms of collectiveinvestment or asset accumulation and, as such, offer investorssimilar investment opportunities.

Due to the increased popularity of both forms of investmentvehicle, the CSA and the CCIR wish to ensure that theirrespective regimes of regulation are harmonized and give similarprotections to investors in these different, yet functionally similarproducts.

As a first step towards ensuring this goal is met, both groups ofregulators embarked on a joint project to compare the productsand their regulation. A joint regulatory/industry working groupcompared the legal structure and nature of the products andtheir regulation. A Comparative Table was developed thatcompares specified features for both products and theirregulation.

This Report constitutes the report of the working group to theCSA and the CCIR and incorporates the Comparative Table.The Report is designed to briefly and concisely describe theproducts and their regulation and the Comparative Table isintended to provide complete details about the findings of theworking group.

B. The Mandate

The CSA and the CCIR agreed to undertake a joint project tocompare the regulatory frameworks governing mutual funds andsegregated funds offered under an IVIC. Given the importanceof IVICs/segregated funds and mutual funds to the assetaccumulation objectives of consumers, the CSA and the CCIRsaw the need to better understand both the similarities anddifferences between these products and their regulation.

The CSA and the CCIR share a common goal in the regulationof asset accumulation products under their respectivejurisdictions. Such regulation must be effective and responsiveto consumer needs and trends in the applicable industry. Thereis also an objective to coordinate and harmonize the treatmentof asset accumulation products under the respective regulatoryregimes, where they have similar features.

Before further discussions can occur between the CSA and theCCIR with respect to the need, if any, for further coordinationand harmonization of regulation of mutual funds and IVICs, acrucial first step is to understand:

• the entities that offer and manage the products;

• the nature and structure of the products and how theydiffer;

• the regulation applicable to the products, theiroperation and their sale to consumers; and

• the regulatory rationale or philosophy behind theapplicable regulation.

The regulation of IVICs and mutual funds cited in this Report andin the Comparative Table is that in force as of the date of theirpreparation. Proposed changes to that regulation, wherepotentially significant, are indicated either in the ComparativeTable or below.

The changes to the regulatory landscape currently beingimplemented for Quebec by Bill 188, which addresses financialservices intermediaries, are not described in this Report or theComparative Table. It is noteworthy, however, that the Quebecreform of financial services distribution is very comprehensive.Under Bill 188, IVICs are treated as insurance products andmutual funds as securities. Where appropriate, consumerprotection measures and market conduct rules will apply equallyto both products.

As this Report and the Comparative Table were being finalized,Industry Canada released the report of Glorianne Strombergprepared for the Office of Consumer Affairs. The working group1

notes that Ms Stromberg raises consumer protection issues thatare relevant to the work of both the CSA and the CCIR and areworthy of further study, although the working group did notpurport to deal with issues raised in Ms Stromberg’s report in thisReport and the Comparative Table. The Comparative Tablefocuses on regulation currently in place and does not consideralternative regulatory structures and rules.

Investment Funds in Canada and Consumer Protection -1

Strategies for the Millennium. A review by GlorianneStromberg prepared for Office of Consumer Affairs, IndustryCanada, October 1998.

C. The Comparative Table

The CSA and the CCIR organized a working group consisting ofstaff of their respective organizations and industry members toprovide them with the necessary information to enable them tomake the first step referred to above. The working groupdeveloped the attached Comparative Table.

The Comparative Table covers, for mutual funds and segregatedfunds offered under IVICs, a comparison of:

• their legal form and structure, their operators andservice providers;

• their governing regulation and their central regulators,as well as the governing regulation and the centralregulators of their operators and service providers;

• the rights of purchasers;

• their method of marketing and disclosure topurchasers; and

• the manner in which they are distributed to purchasers.

The working group believes that the Comparative Table outlinesthe material items of comparison of the above topics and is acomprehensive analysis of both the structure and organizationalforms of the products and their regulation.

Terminology used in the Comparative Table has been madegeneric. For example, the term “operator” has been used torefer to the management company in the mutual fund contextand to the life insurance company in the IVIC context. “Productstructure” and “product” is used to refer to the mutual fund andalso to the IVIC. “Purchaser” is used to refer to investors in amutual fund and to contractholders in the IVIC context.Abbreviations used in the Comparative Table are defined in theGlossary preceding the Comparative Table.

D. Individual Variable Insurance Contracts

The Comparative Table covers IVICs commonly made availableto the public by life insurance companies that include aninvestment element that is valued with reference to one or moresegregated funds. The CCIR and the CSA believe that thisproduct and mutual funds have important similarities anddifferences. The primary regulatory goal should be to ensurethat consumer protection remains the focal point of bothregulatory models.

Two distinct terms are used in the Comparative Table to refer totwo legally distinct matters:

• An “IVIC” is the individual variable insurance contractentered into between a contractholder and the lifeinsurance company. Maturity and death benefitsguarantees are provided to contractholders andbeneficiaries pursuant to an IVIC. Purchasers of anIVIC hold an insurance contract that gives them certainspecified benefits based on the value of one or morespecified segregated funds (or groups of assets).

• A “segregated fund” is a pool of assets owned by thelife insurance company and held by the life companyseparate and apart from other similar pools and itsgeneral assets. An IVIC gives a purchaser the right tochoose among various segregated funds that will givethe purchaser specified benefits based on the value of

the chosen segregated funds.

The Comparative Table highlights that IVICs and segregatedfunds are regulated by two levels of government for differingregulatory purposes:

• The authority to issue IVICs is given to life insurancecompanies under their incorporating legislation. Atpresent virtually all insurance companies issuing IVICsare incorporated under the Insurance Companies Act(Canada) (ICA). This legislation and the regulations2

and guidelines issued under it regulate the governanceand solvency of federally incorporated life insurancecompanies and fraternal organizations and theCanadian branch operations of foreign life companies. Since segregated funds are assets of the lifeinsurance company, the federal legislation requiresthese assets to be maintained and accounted forseparate and apart from the other assets of the lifeinsurance company. The federal regulators, beingconcerned about the solvency of life insurancecompanies, require that adequate reserves bemaintained by the life insurance company in respect ofthe guarantees provided under an IVIC. The amountof reserves and the standards for maintaining suchreserves have been reviewed by a joint OSFI, industryand actuarial committee (the Committee on LifeInsurance Financial Reporting (CLIFR)). AMemorandum dated November 6, 1998 from theCanadian Institute of Actuaries on the 1998 Valuationof Life Policy Liabilities, and a Research Paper, alsodated November 1998, from a CLIFR sub-committee,provide additional guidance to life companies inassessing adequate reserves for guarantees.

• The regulation of an IVIC as an insurance contract isgoverned by provincial insurance legislation, whichmandate the generally applicable elements of all lifeinsurance contracts. Provincial insurance legislationalso dictates the marketing and disclosure topurchasers of IVICs and the segregated funds offeredas investment options under them. Provincialinsurance regulation incorporate certain standards forthe management of segregated fund assets. Thesestandards were drafted taking into consideration theequivalent regulation applicable to mutual funds.

• Individual variable insurance contracts cannot be soldto the public until an insurance contract, applicationand information folder (including summary factstatements and financial statements) are filed, inapproved form, with the provincial insurance regulators.The IVIC Guidelines (described in the following fullparagraph) require that insurance customers receivean information folder. The IVIC Guidelines mandate aform for information folders and are designed to ensurecontractholders receive full and complete disclosureabout their IVIC/segregated fund.

• Distributors of IVICs are also regulated at the provinciallevel. Life insurance agents and brokers are requiredto be licenced, satisfy certain proficiency requirements

There are currently four Quebec incorporated life companies2

that issue or are in the process of issuing, IVICs, under asimilar regulatory system to that which exists for federal lifecompanies issuing IVICs. For the purposes of theComparative Table, the regulation of segregated fundscontained in the ICA is explained.

and be monitored by the life insurance Disclosure and registration are the two central concepts ofcompanies whose IVICs they sell. In several provincial securities laws which are administered by provincialprovinces, certain regulatory functions have securities regulators. Underpinning much of securities regulationbeen delegated or assigned to self-regulatory is the principle that investors must have access to all materialinsurance councils. information concerning their investment both at the time of

The Comparative Table also highlights the co-operative effort of therefore requires delivery of disclosure documentsindustry trade associations and provincial insurance regulators (prospectuses and financial statements) and public disclosure ofin the development of regulations for IVICs and their related information through filing of mandatory documents with thesegregated funds. The CLHIA Guidelines on Individual Variable securities regulators. All documents filed with the securitiesInsurance Contracts related to Segregated Funds (the IVIC regulators are publicly available. Since March 1997 theseGuidelines) were approved by the CCIR on March 4, 1997 and documents have been accessible via the Internet on the websitebecame effective in July 1997. The IVIC Guidelines are applied of SEDAR . These disclosure and registration requirements areconsistently across Canada by provincial insurance regulators. not unique to mutual funds and their managers.In Ontario, they have the force of law, in part, through theirincorporation by reference in Ontario Regulation 132/97. The However, securities regulators have adopted regulation that is3

IVIC Guidelines provide a comprehensive code for, among other specific to mutual funds. Securities regulators consider mutualthings, the conduct of the sponsoring life company, the funds to be sufficiently different from other issuers of securities,management of the segregated funds, product and financial such as business corporations, to warrant this specificdisclosure, including advertising and distribution. Industry trade regulation. The primary features that securities regulators haveassociations also play a large role ensuring compliance with taken into account are:these standards and guidelines and in the education, proficiencyand licencing of the distributors of these products. The CCIR • The essential feature of a mutual fund is that itsand the CLHIA are dedicated to updating and reforming, where securityholders are entitled to redeem their securitiesappropriate, the regulation of IVICs on an ongoing basis. on demand and receive for such securities their pro

The introduction of the ‘wrap’ product (a segregated fund which (the “net asset value”). Accordingly, securitiesinvests exclusively in specified mutual funds) with its particular regulators have set regulations governing the types offeatures has created a need to supplement the current rules. In investments and practices that can be made orthis regard, the CCIR and the CLHIA are reviewing the IVIC followed by mutual funds to ensure that theGuidelines to determine where they should be updated. In investments made by the funds are diversified andaddition, insurance regulators are examining the proficiency reasonably liquid;requirements for agents with a view to determining what, if any,changes should be made. • Mutual funds are marketed to the investing public and

E. Mutual Funds

The Comparative Table compares IVICs (and segregated funds)with mutual funds that are distributed to the public under aprospectus filed with the provincial securities commissions andare governed by National Policy Statement No. 39 Mutual Funds(NP39). NP39 is the main instrument of the provincial securitiesregulators governing so-called “conventional” mutual funds.

The Comparative Table highlights that each mutual fund isregulated by the provincial securities regulators as an issuer ofsecurities. As such, mutual fund securities cannot be sold to thepublic without a prospectus being filed with, and accepted by,the securities regulators and delivered to purchasers, andwithout the seller of such securities being registered with thesecurities regulators as a dealer or a sales representative of adealer. In this context, mutual funds are no different from anyother issuer of securities to the retail public. Securitiesregulations also require that the entity making the investmentdecisions regarding the assets of the mutual fund be registered(or be exempt from registration) with the provincial securitiesregulators as an adviser.

purchase and on a continuous basis. Securities regulation

4

rata share of the overall portfolio’s current market value

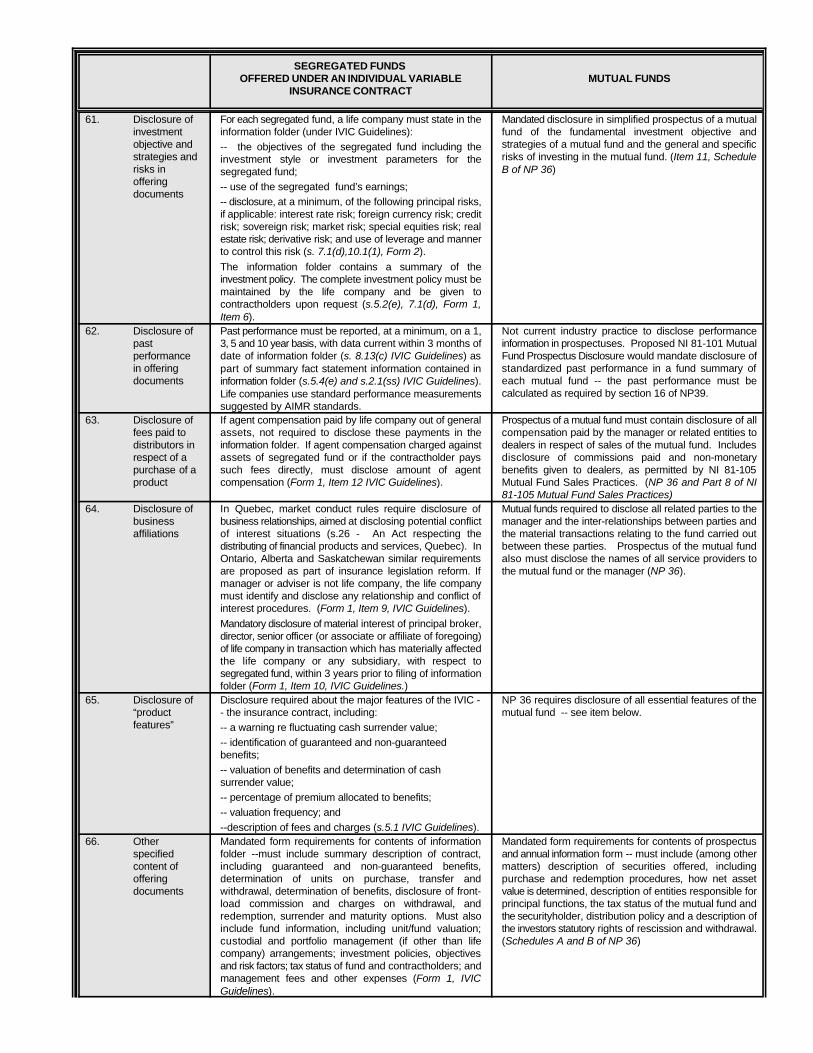

are sold at a retail level to non-institutional investors,who often base their decisions on advertising and thepast performance of such investment vehicles.Accordingly, securities regulators administer a body ofregulations stipulating the disclosure to be given toinvestors both at the point of sale and on a continuousbasis, the content of advertising and other salescommunications, how performance information formutual funds is to be calculated, and theaccountabilities for such disclosure;

• While all mutual funds have a trustee or a board ofdirectors, virtually all the operations and functions ofmutual funds are carried out by a sponsor or promoter(a “manager”) without any involvement of, or oversightby, independent third parties. The manager may wellbe the trustee of the fund. Accordingly, securitiesregulators are of the view that it is important to imposelimits on the transactions that can be carried outbetween related parties. The rules also impose anobjective standard of care upon managers of mutualfunds and custodians of the assets held by mutualfunds. Assets of the mutual fund are required to beheld by a separate qualified custodian who is not themanager;

C Mutual fund securities have common characteristicsthat distinguish them from securities issued by, forexample, an operating business corporation.Accordingly, securities regulators have a specialcategory of registration for dealers selling mutual fund

The current IVIC Guidelines replaced the “Superintendents’3

Guidelines applicable to Variable Insurance Contracts” andthe CLHIA’s Variable Insurance Contract (VIC) Guidelineswhich were developed in the late 1960’s to regulate productdisclosure and distribution. Under the former Guidelines, lifeinsurance companies were required to file long form folderswith some of the provincial insurance regulators. The formerGuidelines also mandated delivery of summary folders tocontractholders. These were adopted in part by regulation inOntario (Reg. 677, R.O. 1990).

The System for Electronic Document Analysis and Retrieval -4

www.sedar.com.

securities. The “mutual fund dealer” category adopted as a rule or policy of each of the securities regulators,of registration has its own proficiency and subject to receipt of the necessary governmental approvals incapital requirements tailored to take account 1999. When adopted, NI 81-101 will replace NP36. of the differences in the business of suchdealers and the nature of the investment NI 81-102 is designed to rewrite and, where necessary, updatevehicle; NP 39. It also will introduce some new rules, for example, those

C Investors in mutual funds acquire them based on their designed to reflect changes in the mutual fund industry since theunderstanding of the reputation of managers of the last compilation of NP39 in 1988.mutual funds, the funds’ investment objectives andother similar fundamental features of their investment. NI 81-101 proposes a new disclosure regime for mutual funds,Most mutual funds are trusts and therefore not subject although still based on the concepts of NP36. The aim is toto corporate legislation that gives shareholders certain ensure that all investors receive a short, concise, readablerights. Accordingly, securities regulators consider it disclosure document that gives all essential informationimportant that investors be given rights to decide necessary for informed decision making and have access to awhether or not fundamental changes will be made to more extensive information disclosure document if they wishtheir mutual fund. Subject to certain limited exceptions, more information.a securityholder meeting must be held andsecurityholder approval given, before certain specified The CSA are addressing the major recommendations made byfundamental changes can be made to a mutual fund. Glorianne Stromberg in her 1995 report on regulatory reform forSecurities regulators also must approve certain mutual funds. Among other matters, the CSA support thefundamental changes before they are made. establishment of the Mutual Fund Dealers Association of

Although Canadian securities regulation of mutual funds is by the CSA and to which all mutual fund dealers would belong.carried out by each of the twelve separate provincial and In Québec, Bill 188 must be taken into account. The Financialterritorial securities regulators, the CSA ensure that mutual fund Services Bureau, concurrently with the Commission des valeursregulation is consistent, and consistently applied, across mobilières du Québec, will be responsible for the application ofCanada. The main rules governing mutual funds (NP39, the some of the rules that govern mutual fund dealers, not thesimplified prospectus regime embodied in National Policy MFDA.Statement No. 36 and National Instrument 81-105 Mutual FundSales Practices) are rules or policies of each of the securities The CSA also have agreed that mutual fund governance reformregulators. The regulation of mutual funds contained in is an important issue for securities regulators to address.provincial securities legislation is also largely consistent. For the5

purposes of the Comparative Table the regulation of mutualfunds contained in the Securities Act of Ontario and theregulation made thereunder has been taken as representative.For information about the specific regulation of mutual funds ina particular province or territory, reference should be made tothat province’s or territory’s securities act and regulations.

The CSA are dedicated to updating and reforming, whereappropriate, the regulation of mutual funds. NP39 is in theprocess of being rewritten as proposed National Instrument 81-102 Mutual Funds ; it is expected to be adopted as a rule or6

policy of each of the securities regulators, subject to receipt ofthe necessary governmental approvals in 1999. When adopted,NI 81-102 will replace NP39. Similarly, NP36 is in the processof being rewritten as proposed National Instrument 81-101Mutual Fund Prospectus Disclosure ; it is also expected to be7

regulating mergers and reorganizations of mutual funds,

8

Canada (the MFDA) as a self regulatory organization overseen

9

F. Conclusion

The CSA and the CCIR have advanced their respectiveunderstandings about mutual funds and IVIC/segregated fundsthrough the preparation of this Report and the ComparativeTable. This Report and the Comparative Table highlight thatalthough there are differences in the legal nature of the product,there exist many similarities in the regulation of the products -- inessence the goals of both regulation are similar -- the protectionof investors. Differences in the regimes reflect:

C the different legal nature of the products; and

C a historically different approach to regulatorysupervision of the products.

In Québec, the short form prospectus regime for mutual funds5

is not part of National Policy No. 36 (C-36) but is covered bythe Québec Securities Act (S.A.) and its regulations(Regulation). This regime is equivalent to the one provided inC-36. Some sections of National Policy Statement No. 39 arealso included in sections 277 to 293 of the Regulation.

A Notice of Proposed National Instrument 81-102 Mutual6

Funds and its Companion Policy and the proposed NationalInstrument and Companion Policy were published for a 120- Canadian Securities Administrators by the Investment Fundsday comment period on June 27, 1997. In Ontario, these Steering Group, November 1996.documents were published as a special supplement edition ofthe OSCB at (1997) 20 OSCB (Supp2). A revised version of On May 15, 1997, the CSA released the Report of the CSANI 81-102 and its Companion Policy was published for a Investment Funds Implementation Group, a high-level CSAfurther 60-day comment period on March 19, 1999. committee established to consider how the CSA could

A Notice of Proposed National Instrument 81-101 Mutual Fund the Investment Funds Steering Group. The Report of the CSA7

Prospectus Disclosure and its Companion Policy and the Investment Funds Implementation Group was published inproposed National Instrument and Companion Policy were Ontario on May 16, 1997 (1997) 20 OSCB 559. published for a 90-day comment period on July 31, 1998 -- in

Ontario at (1998) 21 OSCB 4793.

Regulatory Strategies for the Mid-90's--Recommendation for8

Regulating Investment Funds in Canada” prepared byGlorianne Stromberg for the Canadian SecuritiesAdministrators, January 1995. The recommendationscontained in the Stromberg Report were considered by a jointindustry and regulatory steering group, the Investment FundsSteering Group. Their report was released in 1996. “TheStromberg Report: An Industry Perspective” prepared for the

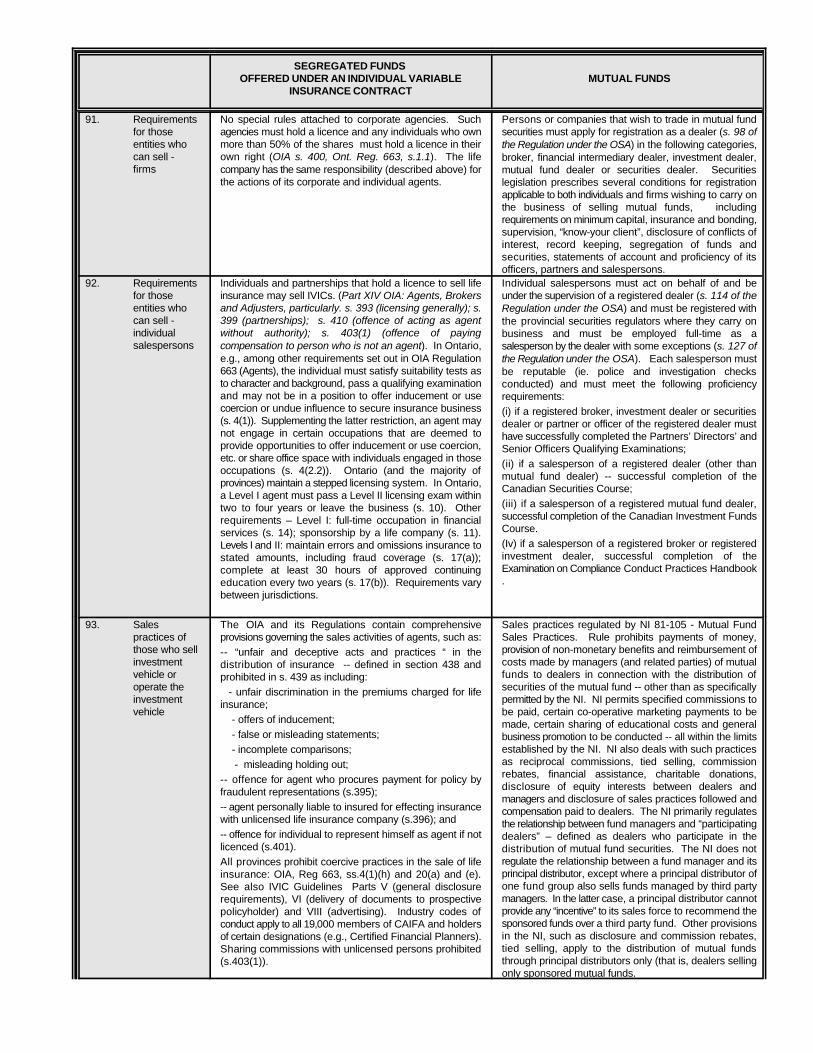

9

implement the Stromberg Report and the subsequent report of

This Report and the Comparative Table are expected to providean opportunity for further examination to determine whereadditional harmonization for regulation is warranted.

G. The Members of the Working Group

The following individuals from the organizations notedparticipated on the working group that prepared this Report,including the Comparative Table:

British Columbia Securities Commission:Robert Hudson

Canadian Association of Insurance and FinancialAdvisors:Edward Rothberg

Canadian Life and Health Insurance Association Inc.:Jean-Pierre BernierSheldon Meyers

Financial Services Commission of Ontario:Rahim DharssiMaureen SimpsonGrant Swanson

The Great-West Life Assurance Company:Gary Senft

The Investment Funds Institute of Canada:John KaszelJohn Mountain

Ontario Securities Commission:Rebecca CowderyTanis MacLarenTracey Stern

Sun Life Assurance Company of Canada:Hugh Kerr

Transamerica Life Insurance Company:Gerald Badali

Trimark Investment Management Inc.:Kathryn Ash

1.1.6 Individual Variable Insurance Contracts (Segregated Funds) and Mutual Funds: Comparative Table

Individual Variable Insurance Contracts (Segregated Funds) and

Mutual Funds:

Comparative Table

Prepared for the Canadian Securities Administrators and the

Canadian Council of Insurance Regulators

May 7, 1999

GLOSSARY TO THE COMPARATIVE TABLE

AIMR Association for Investment Management and Research

CAIFA Canadian Association of Insurance and Financial Advisors

CCIR Canadian Council of Insurance Regulators

CISRO Canadian Insurance Self-Regulatory Organization

CLHIA Canadian Life and Health Insurance Association

CompCorp Canadian Life and Health Insurance Compensation Corporation

CSA Canadian Securities Administrators

ICA Insurance Companies Act (Canada)

IDA Investment Dealers Association of Canada

IFIC The Investment Funds Institute of Canada

ITA Income Tax Act (Canada)

IVIC Individual Variable Insurance Contract

IVIC Guidelines The CLHIA Guidelines on Individual Variable Insurance Contracts related to Segregated Funds,established by the Canadian Council of Insurance Regulators dated March 4, 1997 and effective July 1,1997 and referred to in Ontario Regulation 132/97 and published in the Ontario Gazette May 3, 1997.

MFDA Mutual Fund Dealers Association of Canada

NP 29 National Policy No. 29 - Mortgage Mutual Funds

NP 36 National Policy Statement No. 36 - Simplified Prospectus System

NP 39 National Policy Statement No. 39 - Mutual Funds

OIA Insurance Act (Ontario)

OSA Securities Act (Ontario)

OSC Ontario Securities Commission

OSFI Office of the Superintendent of Financial Institutions (federal)

Page numbers referred to original document

Index toComparative Table

A. Legal Form and Structure

1. Legal nature of product2. Standard operating structure for product3. Nature of “investment” -- from perspective of purchaser4. Requirement for regulatory approval of product before public can purchase5. Who operates the product structure?

B. Governing Regulation and Regulatory Body

6. Rules governing the product7. Central regulators of product8. National uniformity of regulation9. Rules governing the operators of or service providers to the product structure10. Central regulators of operators of, or service providers to the product structure11. Fundamental purpose and goals of the regulation of product and operators and service providers to product

structure 12. Role of self-regulatory organizations and trade associations

C. Operators of and Service Providers to Product Structure

13. Independence required?14. Capital requirements15. Proficiency requirements16. Other qualifying requirements17. Codes of conduct18. Resources19. Duties of service providers mandated?20. Ability to sub-contract and sub-delegate21. Regulatory oversight of operators of or service providers to product structure22. Regulatory sanctions against operators of or service providers to product structure23. Any requirements for operators/service providers to put seed money into product structure?

D. Investment and Borrowing Limitations (for mutual funds or segregated funds)

24. Investment objective/strategies25. Changing investment objective/strategies26. Eligible instruments--publicly traded, transferable, liquid securities27. Eligible Investments--money market instruments28. Eligible investments--other investment vehicles (that is, other segregated funds or mutual funds or closed end funds)29. Eligible Investments--derivatives30. Eligible Investments--bank deposits or other liquid assets31. Eligible Investments--other financial instruments32. Investment limitations--on publicly traded, transferable, liquid securities33. Investment limitations--on going voting rights34. Investment limitations--on derivatives35. Other limitations36. Borrowing and Lending Limitations37. Regulatory oversight - compliance with investment limitations/restrictions

E. Conflicts of Interest

38. General standards concerning conflicts of interest39. Soft dollar transactions 40. Purchase by product structure of underwritten securities (related underwriter to operators of product structure)41. Purchase of securities of operator or related parties of operators of product structure42. Principal transactions with affiliates43. Borrowing and lending to affiliates

F. Asset Valuation and Pricing

44. Principles for valuation and pricing interests in the product45. Regulation of redemption rights/purchase of interests by purchasers

G. Structural requirements for product

46. Where and how must assets of the product structure be held?47. Regulation of fees charged to product structure48. Record-keeping49. Privacy and Confidentiality50. Governance of product and/or operators of product

H. Purchaser Rights

51. Principal rights of purchasers52. Consumer inquiries/complaints53. Change in operators of investment vehicle54. Ability to change auditor of investment vehicle55. Mergers and terminations of investment vehicle56. Meetings of purchasers

I. Marketing and Disclosure

57. Principal obligation58. Summary of reporting/disclosure requirements to new purchasers59. Standards applicable to disclosure in offering documents60. Disclosure of fees paid by investment vehicle and by investors in offering documents61. Disclosure of investment objective and strategies and risks in offering documents62. Disclosure of past performance in offering documents63. Disclosure of fees paid to distributors in respect of a purchase of a product 64. Disclosure of business affiliations 65. Disclosure of product features66. Other specified content of offering documents67. Other documents to accompany offering documents (financial statements or otherwise)68. When offering documents may be distributed and interests issued69. Who may purchase product? -- individuals/corporations --investment in a trust70. When must a purchaser receive offering documents71. Documents issued following purchase of product72. Procedural matters73. Notification of material changes from offering documents74. Accountability of investment vehicle and/or operators of investment vehicle for information contained in offering

documents 75. Rights of purchasers in connection with offering documents or purchase of interest in product76. Initial filing and review process77. Annual filing and review process78. Powers to reject offering documents79. Powers of regulator to take action during course of distribution or sale of product 80. On-going reporting requirements - continuous disclosure (reports, standards,contents, filing and delivery

requirements)81. Advertising restrictions82. Contents of advertising83. Role of regulator in reviewing advertising84. Requirements relating to coercion or tied selling85. Electronic distribution86. Other marketing restrictions

J. Selling Interests in the Product

87. The sales process and industry relationships

88. Dual registration/multiple licensing 89. Direct sales by unregistered personnel (head office or otherwise)90. Responsibility for sales activity91. Requirements for those entities who can sell - firms92. Requirements for those entities who can sell - individual salespersons 93. Sales practices of those who sell investment vehicle or operate the investment vehicle94. “Know your client” rules95. Who regulates those who sell product?96. Proceeds of Crime (Money Laundering Regulations)

K. Guarantees

97. Any government guarantees?98. Any industry compensation fund?99. Does operator of investment vehicle guarantee performance?100. Who monitors the ability of the operator of the investment vehicle to complete any contractual guarantees?

SEGREGATED FUNDS

OFFERED UNDER AN INDIVIDUAL VARIABLE MUTUAL FUNDSINSURANCE CONTRACT

Legal Form andStructure:

1. Legal nature IVICs are most commonly [“non-participating”] life Each separate mutual fund is a separate legal entity andof product insurance contracts offered by life insurance companies. issuer of securities. A mutual fund is defined in securities

Most life companies offering IVICs, provide segregated regulation of each province (s. 1.1 of the OSA). Thefunds as an investment option, although some lifecompanies may offer other investment options under anIVIC, such as fixed term guaranteed rate or daily interestaccounts (both backed by the general assets of the lifecompany). If a contractholder chooses a segregated fundas an investment option, the liabilities of the life company tothe holder of the IVIC vary in amount depending on themarket value of a specified group of assets held in asegregated account. (Definition of IVIC in s.2.1(y) IVICGuidelines). Companies licensed to carry on the business of the mutual fund (generally fees and expenses payableof life insurance under the ICA are authorized to issueIVICs pursuant to s. 450. The assets in segregated fundsare owned by the life company but must be segregatedfrom the other assets of the life company (s. 451 ICA). Thelife company must maintain separate accounts (from itsgeneral funds accounts) in respect of IVICs (s. 451 ICA).Contractholder has statutory priority over other claimantsagainst assets of segregated fund (s.454 ICA). Acontractholder may seek damages against the generalassets of a life company to the extent a segregated fundhas insufficient assets to satisfy a claim under theguarantees (s.455 ICA). Claims against the general assetsof a life company rank after secured creditors and claims ofparticipating policyholders. A life company offering IVICsmust maintain reserves in respect of the guaranteesgranted under the IVIC.

essential nature of a mutual fund is that its value is basedon the current value of its assets less the current value ofits liabilities and investors in a mutual fund have the rightto redeem their interest “on demand” at the net asset valueof their interest. The assets of a mutual fund are ownedby the mutual fund and investors are entitled to a pro ratashare of those assets by holding units or shares of themutual fund. Investors are given limited liability (under theconstating documents of the mutual fund). Any liabilities

to the manager of the fund, brokerage commissions andtaxes) are generally accrued daily.

2. Standard IVICs are contracts between a contractholder and a life Both open-ended investment trusts (mutual fund trusts)operating company. Each IVIC has an annuitant who consents to be and corporations (mutual fund corporations) are permitted,structure for the “measuring life” for the purposes of the death although open-ended investment trusts are more common,product guarantee. This annuitant must be the contractholder in a due to the more favourable flow-through tax treatment

registered IVIC; in a non-registered IVIC the annuitant need under the ITA for mutual fund trusts. The structure of anot be the contractholder. A contractholder is entitled to mutual fund trust is largely determined by a declaration ofname beneficiaries. Segregated funds are assets owned trust or trust deed (subject to restrictions andand held by the life company separate from its general requirements imposed by securities regulations governingassets -- their operation is governed by federal insurance mutual funds). These trust documents dictate the affairslaws. and operations of the mutual fund trust and also appoint

a trustee for the mutual fund (who agrees to act as trusteeon the terms set out in the trust document). Mutual fundcorporations are governed similar to any other businesscorporation (via articles, by-laws, corporate law) -- againsubject to the restrictions and requirements imposed bysecurities regulations governing mutual funds.

3. Nature of Through the payment of premiums, a contractholder Investors in a mutual fund purchase and hold securities“investment” -- purchases an IVIC and is allocated notional units in issued by the mutual fund. Investors pay for thesefrom specified segregated funds at the net asset value per securities at the net asset value per security nextperspective of segregated fund next determined after the premium is paid. determined by the mutual fund after their order is placed.purchaser These units have no independent legal existence and serve The money so invested becomes the property of the

only to determine the value of the benefits to the mutual fund and is invested according to its investmentcontractholder based on the proportional interest of the objectives. Mutual fund trusts are divided into units ofcontractholder in the assets of the segregated fund (s.2.1 equal value and rights; corporations into shares of equal(uu) IVIC Guidelines). value and rights. Each security has equal voting rights and

entitlements to distributions and proceeds upon wind-upof the mutual fund. As securities, mutual fund units orshares are personal property and securityholders areentitled to a pro rata share of the assets of the mutualfund.

SEGREGATED FUNDS

OFFERED UNDER AN INDIVIDUAL VARIABLE MUTUAL FUNDSINSURANCE CONTRACT

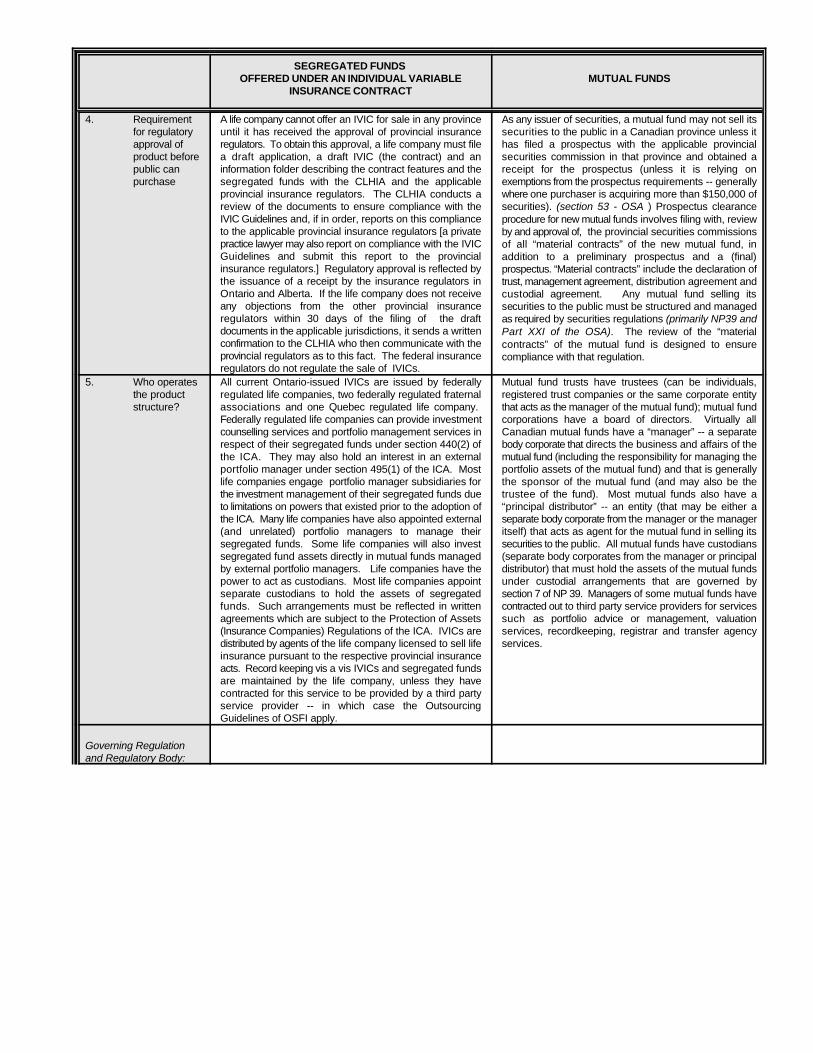

4. Requirement A life company cannot offer an IVIC for sale in any province As any issuer of securities, a mutual fund may not sell itsfor regulatory until it has received the approval of provincial insurance securities to the public in a Canadian province unless itapproval of regulators. To obtain this approval, a life company must file has filed a prospectus with the applicable provincialproduct before a draft application, a draft IVIC (the contract) and an securities commission in that province and obtained apublic can information folder describing the contract features and the receipt for the prospectus (unless it is relying onpurchase segregated funds with the CLHIA and the applicable exemptions from the prospectus requirements -- generally

provincial insurance regulators. The CLHIA conducts a where one purchaser is acquiring more than $150,000 ofreview of the documents to ensure compliance with the securities). (section 53 - OSA ) Prospectus clearanceIVIC Guidelines and, if in order, reports on this complianceto the applicable provincial insurance regulators [a privatepractice lawyer may also report on compliance with the IVICGuidelines and submit this report to the provincialinsurance regulators.] Regulatory approval is reflected bythe issuance of a receipt by the insurance regulators inOntario and Alberta. If the life company does not receiveany objections from the other provincial insuranceregulators within 30 days of the filing of the draftdocuments in the applicable jurisdictions, it sends a writtenconfirmation to the CLHIA who then communicate with theprovincial regulators as to this fact. The federal insuranceregulators do not regulate the sale of IVICs.

procedure for new mutual funds involves filing with, reviewby and approval of, the provincial securities commissionsof all “material contracts” of the new mutual fund, inaddition to a preliminary prospectus and a (final)prospectus. “Material contracts” include the declaration oftrust, management agreement, distribution agreement andcustodial agreement. Any mutual fund selling itssecurities to the public must be structured and managedas required by securities regulations (primarily NP39 andPart XXI of the OSA). The review of the “materialcontracts” of the mutual fund is designed to ensurecompliance with that regulation.

5. Who operates All current Ontario-issued IVICs are issued by federally Mutual fund trusts have trustees (can be individuals,the product regulated life companies, two federally regulated fraternal registered trust companies or the same corporate entitystructure? associations and one Quebec regulated life company. that acts as the manager of the mutual fund); mutual fund

Federally regulated life companies can provide investment corporations have a board of directors. Virtually allcounselling services and portfolio management services in Canadian mutual funds have a “manager” -- a separaterespect of their segregated funds under section 440(2) of body corporate that directs the business and affairs of thethe ICA. They may also hold an interest in an external mutual fund (including the responsibility for managing theportfolio manager under section 495(1) of the ICA. Most portfolio assets of the mutual fund) and that is generallylife companies engage portfolio manager subsidiaries for the sponsor of the mutual fund (and may also be thethe investment management of their segregated funds due trustee of the fund). Most mutual funds also have ato limitations on powers that existed prior to the adoption of “principal distributor” -- an entity (that may be either athe ICA. Many life companies have also appointed external separate body corporate from the manager or the manager(and unrelated) portfolio managers to manage their itself) that acts as agent for the mutual fund in selling itssegregated funds. Some life companies will also invest securities to the public. All mutual funds have custodianssegregated fund assets directly in mutual funds managed (separate body corporates from the manager or principalby external portfolio managers. Life companies have the distributor) that must hold the assets of the mutual fundspower to act as custodians. Most life companies appoint under custodial arrangements that are governed byseparate custodians to hold the assets of segregated section 7 of NP 39. Managers of some mutual funds havefunds. Such arrangements must be reflected in written contracted out to third party service providers for servicesagreements which are subject to the Protection of Assets such as portfolio advice or management, valuation(Insurance Companies) Regulations of the ICA. IVICs are services, recordkeeping, registrar and transfer agencydistributed by agents of the life company licensed to sell life services.insurance pursuant to the respective provincial insuranceacts. Record keeping vis a vis IVICs and segregated fundsare maintained by the life company, unless they havecontracted for this service to be provided by a third partyservice provider -- in which case the OutsourcingGuidelines of OSFI apply.

Governing Regulationand Regulatory Body:

SEGREGATED FUNDS

OFFERED UNDER AN INDIVIDUAL VARIABLE MUTUAL FUNDSINSURANCE CONTRACT

6. Rules The ICA provides for the creation and operation of Provincial securities regulations regulate mutual funds asgoverning the segregated funds offered by life companies under IVICs. issuers of securities (primarily NP39, NP36 and NI 81-product The OSFI Equity Linked Insurance Contract Guidelines 105 and provincial securities legislation). If a mutual fund

(currently under review by the CLIFR Committee) deal with is established as a corporation, applicable provincial orthe nature of IVICs and the applicable reserve requirements federal corporate legislation applies. To the extent ain respect of the guarantees provided by IVICs. IVICs are mutual fund wishes certain tax treatment (both for itselfalso governed by provincial insurance regulation which and for investors) its structure is governed by the ITA.mandates the minimum features of an insurance contract Manager-sponsors of mutual funds may offer registeredincluding basic provisions and the ability of insured to tax plans through which investors may invest in mutualdesignate beneficiaries. In Ontario, IVICs are governed by funds. These registered tax plans are governed by thethe OIA and Ont. Reg. 131/97 made under the OIA. Ont. ITA and may have locking-in features by which pensionReg. 131/97 refers to the IVIC Guidelines and requires any proceeds may be invested in mutual funds in accordanceIVICs sold in Ontario to comply with certain of the IVIC with provincial pension benefits legislation. In Quebec,Guidelines. The tax treatment afforded IVICs and the short form prospectus regime for mutual funds iscontractholders is governed by the ITA. A segregated fund provided in sections 64 and 108 of the Securities Actis deemed to be an inter vivos trust under s.138(1)(a) of the (Quebec) and section 170 of the Regulation.ITA. IVICs are qualified investments for registered taxplans on specified conditions, but without requirements forany minimum number of participants in segregated fundsor purchasers of IVICs. If a life company wishes an IVICto be an eligible investment for pension proceeds, provincialpension regulators review the contract’s locking-inprovisions for compliance with provincial pension benefitslegislation, prior to issue and upon any material change.IVICs which provide payment at maturity of an amount notless than three-quarters of the premiums paid by purchaserfor a benefit on maturity are exempt from the definition of“security” contained in the OSA (section 1.1 OSA).Securities regulators have no jurisdiction over IVICs andseg funds (other than in BC - see Bill 9 - not in force yet )

7. Central Provincial insurance regulators; OSFI, as the federal Provincial securities commissions; provincial businessregulators of regulator of life companies; Revenue Canada; provincial corporation regulators; Revenue Canada.product pension regulators.

8. National A high degree of uniformity in the regulation of the product The CSA strive to make uniform rules that are applicableuniformity of occurs at both the provincial and federal levels, although to all mutual funds offered for sale in Canada; for exampleregulation each province has its own insurance legislation. The IVIC NP 39 and 36 are national policy statements and their

Guidelines have regulatory standing only in Ontario, replacement national instruments will be adopted by eachhowever practically speaking, the other Canadian provinces province and territory. Similarly, the CSA regulation ofwill not allow IVICs to be sold in their jurisdictions unless mutual funds’ service providers (including distributors) isthe IVIC Guidelines are complied with. Uniformity is generally uniform. The main rules governing mutual fundsaccomplished at the federal level as all Ontario issuers of are national rules adopted by each provincial and territorialIVICs, except one, are federally regulated life companies securities commission. Some differences in theand fraternal organizations under the ICA. Certain features registration requirements for mutual fund dealers andof IVICs are regulated by the ITA and pension benefits advisers exist between the provinces (this regulation islegislation. Life insurance agents are regulated and provided for by statute); for example, capital requirementssupervised either directly by insurance regulators or by differ between certain provinces. Mutual funds must fileinsurance councils (self-regulatory organizations acting prospectuses in each province where their securities willunder delegated authority from the provincial insurance be sold, but such filings are made, and reviewed, in aregulators). Although regional differences exist, concurrent and coordinated fashion.harmonization is sought through meetings and initiatives ofthe Superintendents (through the CCIR) and insurancecouncils (through CISRO).

SEGREGATED FUNDS

OFFERED UNDER AN INDIVIDUAL VARIABLE MUTUAL FUNDSINSURANCE CONTRACT

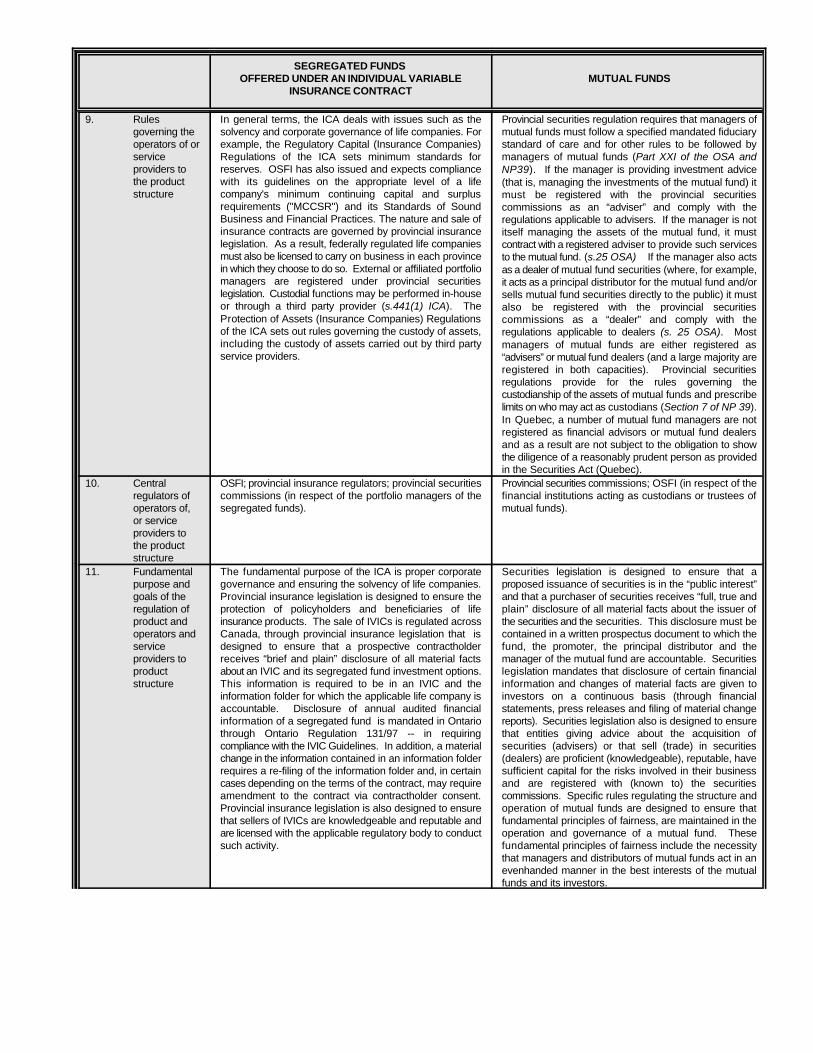

9. Rules In general terms, the ICA deals with issues such as the Provincial securities regulation requires that managers ofgoverning the solvency and corporate governance of life companies. For mutual funds must follow a specified mandated fiduciaryoperators of or example, the Regulatory Capital (Insurance Companies) standard of care and for other rules to be followed byservice Regulations of the ICA sets minimum standards for managers of mutual funds (Part XXI of the OSA andproviders to reserves. OSFI has also issued and expects compliancethe product with its guidelines on the appropriate level of a lifestructure company's minimum continuing capital and surplus

requirements ("MCCSR") and its Standards of SoundBusiness and Financial Practices. The nature and sale ofinsurance contracts are governed by provincial insurancelegislation. As a result, federally regulated life companiesmust also be licensed to carry on business in each provincein which they choose to do so. External or affiliated portfoliomanagers are registered under provincial securitieslegislation. Custodial functions may be performed in-houseor through a third party provider (s.441(1) ICA). TheProtection of Assets (Insurance Companies) Regulationsof the ICA sets out rules governing the custody of assets,including the custody of assets carried out by third partyservice providers.

NP39). If the manager is providing investment advice(that is, managing the investments of the mutual fund) itmust be registered with the provincial securitiescommissions as an “adviser” and comply with theregulations applicable to advisers. If the manager is notitself managing the assets of the mutual fund, it mustcontract with a registered adviser to provide such servicesto the mutual fund. (s.25 OSA) If the manager also actsas a dealer of mutual fund securities (where, for example,it acts as a principal distributor for the mutual fund and/orsells mutual fund securities directly to the public) it mustalso be registered with the provincial securitiescommissions as a “dealer” and comply with theregulations applicable to dealers (s. 25 OSA). Mostmanagers of mutual funds are either registered as“advisers” or mutual fund dealers (and a large majority areregistered in both capacities). Provincial securitiesregulations provide for the rules governing thecustodianship of the assets of mutual funds and prescribelimits on who may act as custodians (Section 7 of NP 39).In Quebec, a number of mutual fund managers are notregistered as financial advisors or mutual fund dealersand as a result are not subject to the obligation to showthe diligence of a reasonably prudent person as providedin the Securities Act (Quebec).

10. Central OSFI; provincial insurance regulators; provincial securities Provincial securities commissions; OSFI (in respect of theregulators of commissions (in respect of the portfolio managers of the financial institutions acting as custodians or trustees ofoperators of, segregated funds). mutual funds).or serviceproviders tothe productstructure

11. Fundamental The fundamental purpose of the ICA is proper corporate Securities legislation is designed to ensure that apurpose and governance and ensuring the solvency of life companies. proposed issuance of securities is in the “public interest”goals of the Provincial insurance legislation is designed to ensure the and that a purchaser of securities receives “full, true andregulation of protection of policyholders and beneficiaries of life plain” disclosure of all material facts about the issuer ofproduct and insurance products. The sale of IVICs is regulated across the securities and the securities. This disclosure must beoperators and Canada, through provincial insurance legislation that is contained in a written prospectus document to which theservice designed to ensure that a prospective contractholder fund, the promoter, the principal distributor and theproviders to receives “brief and plain” disclosure of all material facts manager of the mutual fund are accountable. Securitiesproduct about an IVIC and its segregated fund investment options. legislation mandates that disclosure of certain financialstructure This information is required to be in an IVIC and the information and changes of material facts are given to

information folder for which the applicable life company is investors on a continuous basis (through financialaccountable. Disclosure of annual audited financial statements, press releases and filing of material changeinformation of a segregated fund is mandated in Ontario reports). Securities legislation also is designed to ensurethrough Ontario Regulation 131/97 -- in requiring that entities giving advice about the acquisition ofcompliance with the IVIC Guidelines. In addition, a material securities (advisers) or that sell (trade) in securitieschange in the information contained in an information folder (dealers) are proficient (knowledgeable), reputable, haverequires a re-filing of the information folder and, in certain sufficient capital for the risks involved in their businesscases depending on the terms of the contract, may require and are registered with (known to) the securitiesamendment to the contract via contractholder consent. commissions. Specific rules regulating the structure andProvincial insurance legislation is also designed to ensure operation of mutual funds are designed to ensure thatthat sellers of IVICs are knowledgeable and reputable and fundamental principles of fairness, are maintained in theare licensed with the applicable regulatory body to conduct operation and governance of a mutual fund. Thesesuch activity. fundamental principles of fairness include the necessity

that managers and distributors of mutual funds act in anevenhanded manner in the best interests of the mutualfunds and its investors.

SEGREGATED FUNDS

OFFERED UNDER AN INDIVIDUAL VARIABLE MUTUAL FUNDSINSURANCE CONTRACT

12. Role of self- CLHIA, an industry trade association, acts as the initial IFIC is the industry trade association -- managers of 97%regulatory reviewer of all IVICs, disclosure documents and policy (by assets) of mutual funds are members of IFIC. Its roleorganizations forms. Once those contracts meet with CLHIA approval, is to set voluntary standards of conduct for the industry,and trade they are then filed with the various provincial insurance better serve investor education and act as a lobby groupassociations regulators for approval. The CLHIA also promulgates its for regulatory changes favourable to the industry (in

Consumer Code of Ethics and various guidelines to be securities regulation, corporate legislation and income taxfollowed by life companies on a wide variety of subjects legislation). IFIC members also include distributorsincluding privacy of information, advertising and criteria for (dealers) of, and service providers to, mutual funds. Anassessing the suitability of agents. CLHIA also operates a affiliate of IFIC is a course provider -- offering standardnationwide policyholder information and complaint hot line. courses for salespersons and officers and directors ofSee item #51 for more detail. CAIFA, an industry trade mutual fund dealers. The IDA is the recognized SRO forassociation, provides agents with continuing education the broker-dealers; these firms sell mutual funds, alongprograms including one dealing specifically with IVICs. In with carrying on their other activities. The IDA alsowestern Canada and in Quebec, insurance councils (being performs a trade association function for its members.self-regulatory organizations acting under delegated The proposed MFDA will be the SRO for mutual fundauthority from the provincial insurance regulators) have the dealers (firms that sell only mutual funds). Both the IDAauthority to licence and discipline agents. and the MFDA will regulate the distribution side of the

mutual fund industry, under the supervision of theprovincial securities commissions. In Quebec, with Bill188, the Financial Services Bureau, concurrently with theCVMQ, will be responsible for the application of some ofthe rules concerning mutual fund dealers.

Operators of andService Providers toProduct Structure:

13. Independence The ICA prescribes a minimum number of directors for life No requirement for independence for trustees/board ofrequired? companies and otherwise deals with their corporate directors of mutual fund (other than under corporate

governance. At least one-third of directors must not be legislation for mutual fund corporations) -- no requirementaffiliated with the life company. The ICA also limits the that a board of directors of a manager of a mutual fundnumber of employee-directors and prohibits insurance have independent directors. NP 39 requires each mutualagents and brokers from being directors (s. 167, 168 and fund to appoint a custodian for its assets -- a custodian of171 ICA). In addition, the ICA requires that conduct review a fund is a separate body corporate from the manager ofand audit committees of boards of life companies be the fund, although it need not be a non-affiliated entity. established, the majority of whom must be unaffiliated. TheICA defines affiliation (s.171). An appointed actuary foreach life company must review and report to the board and,in certain circumstances, to OSFI, actuarial and other policyliabilities in accordance with generally accepted actuarialpractices, with such changes as may be determined byOSFI (s.365-369 ICA).

14. Capital Federally-incorporated life companies must have at least Capital required for managers of mutual funds registeredrequirements $10 million of capital upon incorporation. The average as “advisers” or “dealers”; minimum net free capital

capital of life companies issuing IVICs is $617 million. Life requirements for advisers - amount deductible undercompanies are required to maintain adequate capital and requisite insurance/bonding plus $5,000 [BC $25,000];adequate and appropriate forms of liquidity (s. 515 ICA). and for mutual fund dealers - amount deductible underAccording to OSFI, the average MCCSR for the industrywas 236% at December 31, 1997. The required regulatory 108 of the Regulation under the OSA) [BC $75,000 ifcapital is a ratio of 100%. A life company’s appointedactuary must certify on an annual basis that the lifecompany meets the capital adequacy requirements andexceeds the MCCSR. A life company bears the ultimateresponsibility for its liabilities under an IVIC.

requisite insurance/bonding plus $25,000 (ss. 107 and

dealer holds client funds or securities]. Entities eligible toact as custodians for mutual funds must be eitherCanadian chartered banks, registered provincial trustcompanies with shareholders equity of at least $10 millionor wholly owned subsidiaries of such entities havingshareholders equity of $10 million (s. 7 of NP39). Otherthan a requirement to have at least $150,000 of seedcapital or $500,000 of invested money (through a bestefforts offering) (section 3 NP39) no requirements forminimum level of assets for mutual funds. In Quebec, afinancial adviser must have working capital at least equalto $25,000 and the deductible required under section 209of the Regulation.A mutual fund dealer in Quebec, with a restricted practicemust have net free capital of $50,000 and the deductibleunder section 208 of the Regulation.

SEGREGATED FUNDS

OFFERED UNDER AN INDIVIDUAL VARIABLE MUTUAL FUNDSINSURANCE CONTRACT

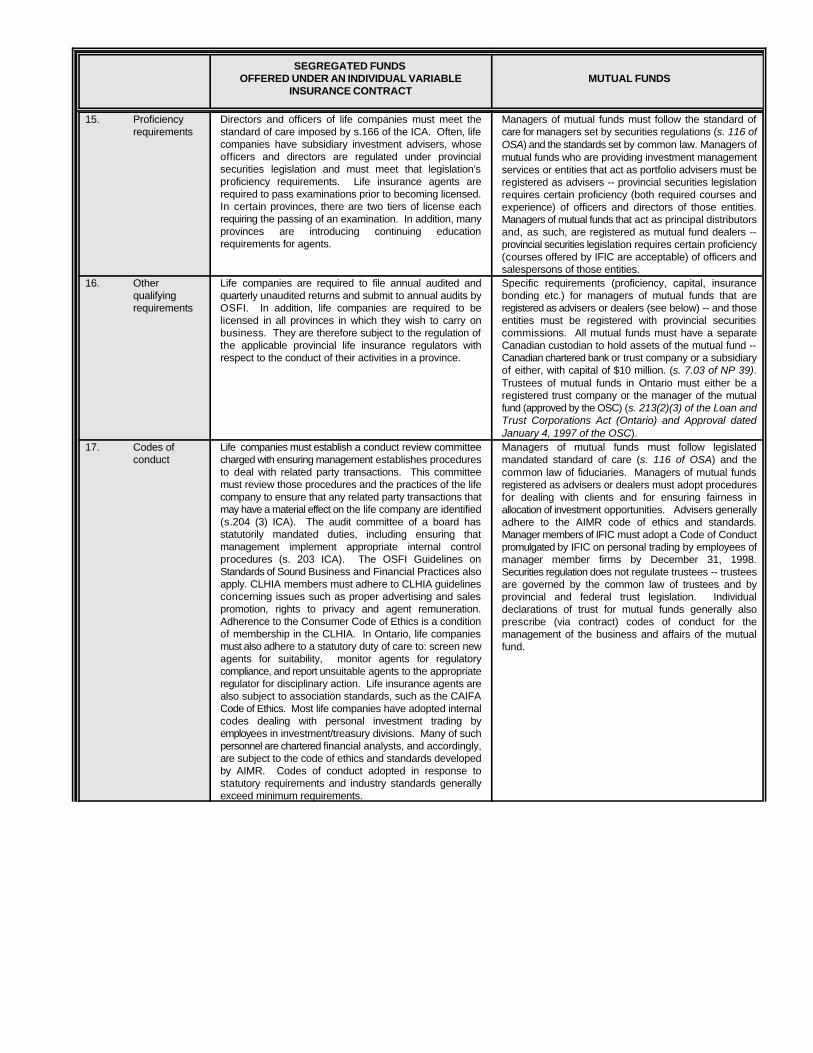

15. Proficiency Directors and officers of life companies must meet the Managers of mutual funds must follow the standard ofrequirements standard of care imposed by s.166 of the ICA. Often, life care for managers set by securities regulations (s. 116 of

companies have subsidiary investment advisers, whoseofficers and directors are regulated under provincialsecurities legislation and must meet that legislation’sproficiency requirements. Life insurance agents arerequired to pass examinations prior to becoming licensed.In certain provinces, there are two tiers of license eachrequiring the passing of an examination. In addition, manyprovinces are introducing continuing educationrequirements for agents.

OSA) and the standards set by common law. Managers ofmutual funds who are providing investment managementservices or entities that act as portfolio advisers must beregistered as advisers -- provincial securities legislationrequires certain proficiency (both required courses andexperience) of officers and directors of those entities.Managers of mutual funds that act as principal distributorsand, as such, are registered as mutual fund dealers --provincial securities legislation requires certain proficiency(courses offered by IFIC are acceptable) of officers andsalespersons of those entities.

16. Other Life companies are required to file annual audited and Specific requirements (proficiency, capital, insurancequalifying quarterly unaudited returns and submit to annual audits by bonding etc.) for managers of mutual funds that arerequirements OSFI. In addition, life companies are required to be registered as advisers or dealers (see below) -- and those

licensed in all provinces in which they wish to carry on entities must be registered with provincial securitiesbusiness. They are therefore subject to the regulation of commissions. All mutual funds must have a separatethe applicable provincial life insurance regulators with Canadian custodian to hold assets of the mutual fund --respect to the conduct of their activities in a province. Canadian chartered bank or trust company or a subsidiary

of either, with capital of $10 million. (s. 7.03 of NP 39).Trustees of mutual funds in Ontario must either be aregistered trust company or the manager of the mutualfund (approved by the OSC) (s. 213(2)(3) of the Loan andTrust Corporations Act (Ontario) and Approval datedJanuary 4, 1997 of the OSC).

17. Codes of Life companies must establish a conduct review committee Managers of mutual funds must follow legislatedconduct charged with ensuring management establishes procedures mandated standard of care (s. 116 of OSA) and the

to deal with related party transactions. This committeemust review those procedures and the practices of the lifecompany to ensure that any related party transactions thatmay have a material effect on the life company are identified(s.204 (3) ICA). The audit committee of a board hasstatutorily mandated duties, including ensuring thatmanagement implement appropriate internal controlprocedures (s. 203 ICA). The OSFI Guidelines onStandards of Sound Business and Financial Practices alsoapply. CLHIA members must adhere to CLHIA guidelinesconcerning issues such as proper advertising and salespromotion, rights to privacy and agent remuneration.Adherence to the Consumer Code of Ethics is a conditionof membership in the CLHIA. In Ontario, life companiesmust also adhere to a statutory duty of care to: screen newagents for suitability, monitor agents for regulatorycompliance, and report unsuitable agents to the appropriateregulator for disciplinary action. Life insurance agents arealso subject to association standards, such as the CAIFACode of Ethics. Most life companies have adopted internalcodes dealing with personal investment trading byemployees in investment/treasury divisions. Many of suchpersonnel are chartered financial analysts, and accordingly,are subject to the code of ethics and standards developedby AIMR. Codes of conduct adopted in response tostatutory requirements and industry standards generallyexceed minimum requirements.

common law of fiduciaries. Managers of mutual fundsregistered as advisers or dealers must adopt proceduresfor dealing with clients and for ensuring fairness inallocation of investment opportunities. Advisers generallyadhere to the AIMR code of ethics and standards.Manager members of IFIC must adopt a Code of Conductpromulgated by IFIC on personal trading by employees ofmanager member firms by December 31, 1998.Securities regulation does not regulate trustees -- trusteesare governed by the common law of trustees and byprovincial and federal trust legislation. Individualdeclarations of trust for mutual funds generally alsoprescribe (via contract) codes of conduct for themanagement of the business and affairs of the mutualfund.

SEGREGATED FUNDS

OFFERED UNDER AN INDIVIDUAL VARIABLE MUTUAL FUNDSINSURANCE CONTRACT

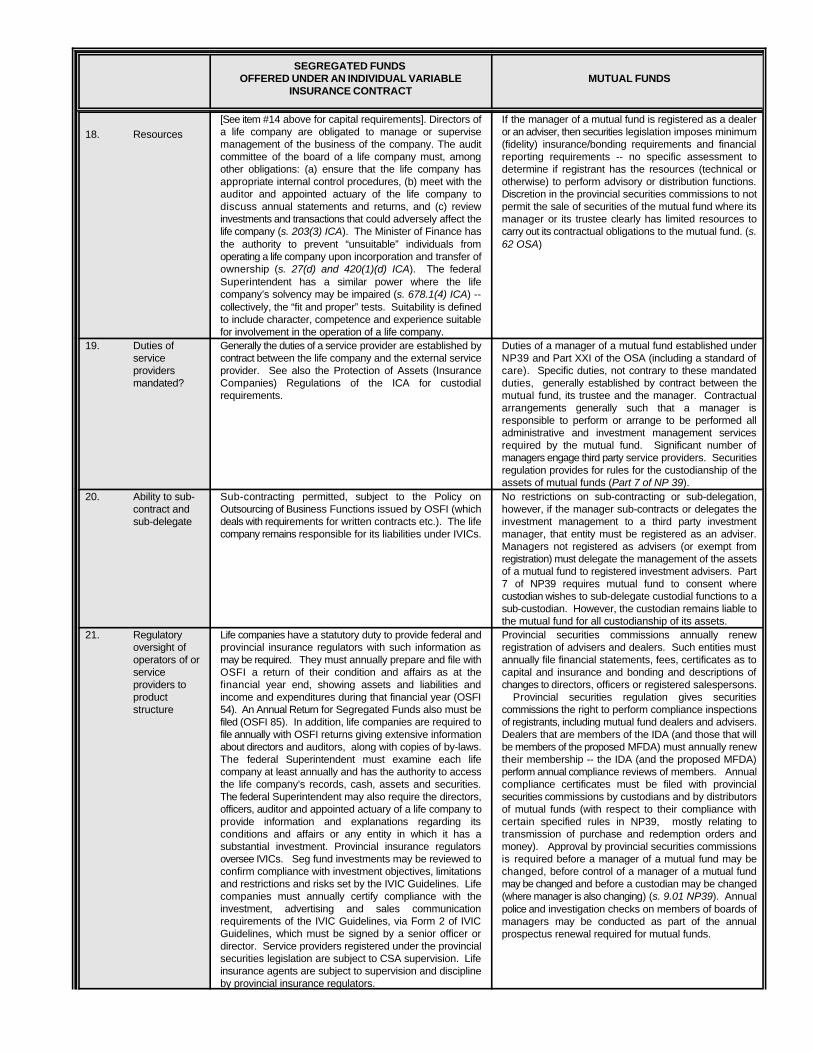

18. Resources[See item #14 above for capital requirements]. Directors of If the manager of a mutual fund is registered as a dealera life company are obligated to manage or supervise or an adviser, then securities legislation imposes minimummanagement of the business of the company. The audit (fidelity) insurance/bonding requirements and financialcommittee of the board of a life company must, among reporting requirements -- no specific assessment toother obligations: (a) ensure that the life company has determine if registrant has the resources (technical orappropriate internal control procedures, (b) meet with the otherwise) to perform advisory or distribution functions.auditor and appointed actuary of the life company to Discretion in the provincial securities commissions to notdiscuss annual statements and returns, and (c) review permit the sale of securities of the mutual fund where itsinvestments and transactions that could adversely affect the manager or its trustee clearly has limited resources tolife company (s. 203(3) ICA). The Minister of Finance has carry out its contractual obligations to the mutual fund. (s.the authority to prevent “unsuitable” individuals from 62 OSA)operating a life company upon incorporation and transfer ofownership (s. 27(d) and 420(1)(d) ICA). The federalSuperintendent has a similar power where the lifecompany’s solvency may be impaired (s. 678.1(4) ICA) --collectively, the “fit and proper” tests. Suitability is definedto include character, competence and experience suitablefor involvement in the operation of a life company.

19. Duties of Generally the duties of a service provider are established by Duties of a manager of a mutual fund established underservice contract between the life company and the external service NP39 and Part XXI of the OSA (including a standard ofproviders provider. See also the Protection of Assets (Insurance care). Specific duties, not contrary to these mandatedmandated? Companies) Regulations of the ICA for custodial duties, generally established by contract between the

requirements. mutual fund, its trustee and the manager. Contractualarrangements generally such that a manager isresponsible to perform or arrange to be performed alladministrative and investment management servicesrequired by the mutual fund. Significant number ofmanagers engage third party service providers. Securitiesregulation provides for rules for the custodianship of theassets of mutual funds (Part 7 of NP 39).

20. Ability to sub- Sub-contracting permitted, subject to the Policy on No restrictions on sub-contracting or sub-delegation,contract and Outsourcing of Business Functions issued by OSFI (which however, if the manager sub-contracts or delegates thesub-delegate deals with requirements for written contracts etc.). The life investment management to a third party investment

company remains responsible for its liabilities under IVICs. manager, that entity must be registered as an adviser.Managers not registered as advisers (or exempt fromregistration) must delegate the management of the assetsof a mutual fund to registered investment advisers. Part7 of NP39 requires mutual fund to consent wherecustodian wishes to sub-delegate custodial functions to asub-custodian. However, the custodian remains liable tothe mutual fund for all custodianship of its assets.

21. Regulatory Life companies have a statutory duty to provide federal and Provincial securities commissions annually renewoversight of provincial insurance regulators with such information as registration of advisers and dealers. Such entities mustoperators of or may be required. They must annually prepare and file with annually file financial statements, fees, certificates as toservice OSFI a return of their condition and affairs as at the capital and insurance and bonding and descriptions ofproviders to financial year end, showing assets and liabilities and changes to directors, officers or registered salespersons.product income and expenditures during that financial year (OSFI Provincial securities regulation gives securitiesstructure 54). An Annual Return for Segregated Funds also must be commissions the right to perform compliance inspections

filed (OSFI 85). In addition, life companies are required to of registrants, including mutual fund dealers and advisers.file annually with OSFI returns giving extensive information Dealers that are members of the IDA (and those that willabout directors and auditors, along with copies of by-laws. be members of the proposed MFDA) must annually renewThe federal Superintendent must examine each life their membership -- the IDA (and the proposed MFDA)company at least annually and has the authority to access perform annual compliance reviews of members. Annualthe life company's records, cash, assets and securities. compliance certificates must be filed with provincialThe federal Superintendent may also require the directors, securities commissions by custodians and by distributorsofficers, auditor and appointed actuary of a life company to of mutual funds (with respect to their compliance withprovide information and explanations regarding its certain specified rules in NP39, mostly relating toconditions and affairs or any entity in which it has a transmission of purchase and redemption orders andsubstantial investment. Provincial insurance regulators money). Approval by provincial securities commissionsoversee IVICs. Seg fund investments may be reviewed to is required before a manager of a mutual fund may beconfirm compliance with investment objectives, limitations changed, before control of a manager of a mutual fundand restrictions and risks set by the IVIC Guidelines. Life may be changed and before a custodian may be changedcompanies must annually certify compliance with the (where manager is also changing) (s. 9.01 NP39). Annualinvestment, advertising and sales communicationrequirements of the IVIC Guidelines, via Form 2 of IVICGuidelines, which must be signed by a senior officer ordirector. Service providers registered under the provincialsecurities legislation are subject to CSA supervision. Lifeinsurance agents are subject to supervision and disciplineby provincial insurance regulators.

police and investigation checks on members of boards ofmanagers may be conducted as part of the annualprospectus renewal required for mutual funds.

SEGREGATED FUNDS

OFFERED UNDER AN INDIVIDUAL VARIABLE MUTUAL FUNDSINSURANCE CONTRACT

22. Regulatory Federal regulatory sanctions include cease and desist In Ontario, the OSC can make various orders if it is “in thesanctions orders requiring a life company to cease any action or to public interest” to do so. Such orders include suspendingagainst take measures necessary to remedy a situation. OSFI is or restricting registration, cease trading an issueroperators of or authorized to take temporary control of the assets (including (including a mutual fund) permanently or temporarily,service segregated fund assets) of a life company and to manage prohibiting the availability of any exemption under theproviders to its affairs where assets are not accounted for, liabilities are OSA, ordering a review of the practices and proceduresproduct not being paid or a practice or state of affairs exists that is of a “market participant”, ordering the production orstructure materially prejudicial to the contractholders or creditors of amendment of a prospectus or financial statements

the life company. Life companies and their officers and (among other documents) or ordering a reprimand of adirectors may be subject to fines and jail terms, in the case person or company (s. 127 OSA). In addition to theof officers and directors. Provincial regulatory sanctionsinclude revocation or suspension of a life company'slicense, cease and desist orders and fines levied against alife company and/or its officers and directors. Provincialinsurance regulators can refuse to issue a certificate topermit the issuance of new IVICs. Federal and provincialregulators are also authorized to examine and investigatethe affairs of life companies at any time (s.440, OIA.; s.674ICA). securities, power to prohibit voting rights or exercise of

powers given to the OSC, the OSC can apply to theOntario Court (General Division) for a declaration that aperson has not complied with securities laws. The courtis given the power to make orders, in addition to thoseimposed upon the party by the OSC. The court’s powersinclude the power to rescind transactions, power to requirethe issuance, cancellation, purchase, exchange,disposition or purchase of or repayment of money paid for

other rights, power to appoint directors or officers, powerto prohibit a person from acting as a director or officer andthe power to order general or punitive damages (s.128OSA).

23. Any There is no minimum amount mandated for the creation of Before a new mutual fund may be offered to the public,requirements a segregated fund underlying an IVIC. OSFI approval is the manager of the mutual fund (or its affiliates) mustfor required for the return of seed money when deposited by either invest $150,000 in the mutual fund, which cannotoperators/serv the applicable life company (s.453 ICA). be redeemed until an additional $500,000 has beenice providers invested or it must arrange for the mutual fund to be soldto put seed on a best efforts offering where a minimum of $500,000money into must be invested by outside investors. (s. 3.01 NP 39)productstructure?

Investment andBorrowing Limitations(for mutual funds orsegregated funds):

24. Investmentobjective /strategies

Life companies are required under the IVIC Guidelines (s. A mutual fund must have a “fundamental investment10.1(1)) to ensure that an information folder contains aninvestment policy for each segregated fund brieflyaddressing each of the following matters: (a) the objectiveof the segregated fund including the investment style orparameters of the investment portfolio; (b) use of thesegregated fund’s earnings and (c) disclosure of theprincipal risks. More detailed description of eachsegregated fund’s investment policy (if one exists) must beavailable upon request and the information folder mustdisclose how a contractholder can access this moredetailed policy (s. 5.2(3) IVIC Guidelines).

objective” that must be described in its prospectus, alongwith the investment strategies pursuant to which suchinvestment objective will be achieved. The prospectus ofa mutual fund must disclose how income of the fund willbe distributed and what risks are applicable to aninvestment in the fund. ( s. 2.01 NP39 and Appendix A toNP36)

25. Changing A change in the investment objective, including the A mutual fund cannot change its “fundamental investmentinvestment investment style or parameters of the portfolio, would objective” without obtaining securityholder approval (via aobjective/strat constitute a material change of facts described in the meeting of securityholders). The prospectus for theegies information folder and the information folder would be mutual fund must also be amended to disclose the

required to be re-filed (s. 2.1(gg), 4.2 IVIC Guidelines). prospective change (before a meeting) and the changeContractholders rights in this regard determined bycontract. Some contracts require that contractholders benotified in advance of a material change in investmentpolicy.

(after the meeting). Investment strategies followed toachieve a fundamental investment objective may bechanged as needed, provided appropriate prospectusdisclosure made (via amendments to current prospectus).(s.6.01 NP39)

26. Eligible No specific restrictions on investments in publicly traded No specific restrictions on the investments eligible to beinstruments securities eligible to be made for a segregated fund. made by a mutual fund, although they must be consistent-- publiclytraded,transferable,liquid securities

Investments must be consistent with investment objectives with the fundamental investment objective of the fund,of the segregated fund as described in its information folder which must be described in the prospectus of the mutualand investment policy statement. No more than 10% of net fund. No more than 10% of net assets of the mutual fundassets of a segregated fund may be invested in “illiquid can be invested in “illiquid” or “restricted” securities, asassets” as defined in IVIC Guidelines (s. 10.4 IVIC defined in NP39. Guidelines).

SEGREGATED FUNDS

OFFERED UNDER AN INDIVIDUAL VARIABLE MUTUAL FUNDSINSURANCE CONTRACT

27. Eligible If the segregated fund is a money market fund, it is If the mutual fund is a money market fund, it is restrictedInvestments restricted to investing in money market instruments with a to investing in money market instruments with term to--moneymarketinstruments

term of less than 13 months (25 months for government maturity of less than 13 months (25 months forsecurities) and is subject to other specified restrictions government securities) and is subject to other specified(s.2.1 IVIC Guidelines). Other segregated funds have no restrictions, including that the fund’s average term torestrictions in investing in money market instruments(provided consistent with investment policy) mutual funds have no restrictions in investing in money

maturity must not exceed 180 days. (s. 16 NP39). Other

market instruments (provided consistent with investmentobjectives).

28. Eligible If the segregated fund is to invest in other segregated funds A mutual fund may invest only in other mutual fundsInvestments or mutual funds, there must be adequate disclosure of this qualified for sale in Canada or where an investment in a--otherinvestmentvehicles (thatis, othersegregatedfunds ormutual fundsor closed endfunds)