$12,045,000 aspen valley hospital district … · sherman & howard l.l.c. also has acted as...

TRANSCRIPT

NEW ISSUE RATING: Moody’s: “Aa2” BOOK-ENTRY ONLY See “RATINGS” BANK QUALIFIED-2010A BONDS

In the opinion of Sherman & Howard L.L.C., Bond Counsel, assuming continuous compliance with certain covenants described herein, interest on the 2010A Bonds is excluded from gross income under federal income tax laws pursuant to Section 103 of the Internal Revenue Code of 1986, as amended to the date of delivery of the 2010A Bonds (the “Tax Code”), interest on the 2010A Bonds is excluded from alternative minimum taxable income as defined in Section 55(b)(2) of the Tax Code, and interest on the 2010A Bonds is excluded from Colorado taxable income and Colorado alternative minimum taxable income under Colorado income tax laws in effect on the date of delivery of the 2010A Bonds as described herein. See “TAX MATTERS – 2010A Bonds.”

In the opinion of Bond Counsel, interest on the 2010B Bonds is included in gross income pursuant to the Tax Code. The owners of the 2010B Bonds will not receive a tax credit as a result of holding the 2010B Bonds. In the opinion of Bond Counsel, assuming continuous compliance with certain covenants described herein, interest on and income from the 2010B Bonds is exempt from all taxation and assessments in the State of Colorado. See “TAX MATTERS—2010B Bonds.”

The District has designated the 2010A Bonds as “qualified tax-exempt obligations” for purposes of Section 265(b)(3) of the Tax Code. See “FINANCIAL INSTITUTION INTEREST DEDUCTION.”

$12,045,000 ASPEN VALLEY HOSPITAL DISTRICT

(PITKIN COUNTY, COLORADO) TAX-EXEMPT GENERAL OBLIGATION BONDS

SERIES 2010A

$37,955,000 ASPEN VALLEY HOSPITAL DISTRICT

(PITKIN COUNTY, COLORADO) TAXABLE GENERAL OBLIGATION BONDS

(DIRECT PAY BUILD AMERICA BONDS) SERIES 2010B

Dated: Date of Delivery Due: December 1, as shown herein

The Aspen Valley Hospital District, Pitkin County, Colorado (the “District”) Tax-Exempt General Obligation Bonds, Series 2010A (the “2010A Bonds”) and Taxable General Obligation Bonds (Direct Pay Build America Bonds), Series 2010B (the “2010B Bonds” and together with the 2010A Bonds, the “Bonds”) are issued as fully registered bonds in denominations of $5,000, or any integral multiple thereof. The Bonds initially will be registered in the name of Cede & Co., as nominee of The Depository Trust Company, New York, New York (“DTC”), securities depository for the Bonds. Purchases of the Bonds are to be made in book-entry form only. Purchasers will not receive certificates representing their beneficial ownership interest in the Bonds. See “THE BONDS--Book-Entry Only System.” The Bonds bear interest at the rates set forth on the inside cover hereof, payable to the registered owner of the Bonds (initially Cede & Co.) semiannually on June 1 and December 1 of each year, commencing June 1, 2011, to and including the maturity dates shown below, unless the Bonds are redeemed earlier. The principal of the Bonds will be payable upon presentation and surrender at the principal corporate trust office of UMB Bank, n.a., or its successor as the Paying Agent for the Bonds. See “THE BONDS.”

The maturity schedule for each series of the Bonds appears on the inside cover page of this Official Statement.

The 2010A Bonds are not subject to redemption prior to maturity. The 2010B Bonds are subject to redemption prior to maturity at the option of the District, are subject to extraordinary optional redemption, and also are subject to mandatory sinking fund redemption as described herein. See “THE BONDS--Redemption Provisions.”

Proceeds of the Bonds will be used to: (i) finance a portion of the costs of acquiring, improving, constructing, equipping and furnishing hospital facilities and (ii) paying the costs of issuing the Bonds. See “SOURCES AND USES OF FUNDS.”

The Bonds constitute general obligations of the District. All of the taxable property in the District is subject to the levy of an ad valorem tax to pay the principal of, interest, and premium, if any, on the Bonds without limitation as to rate and in an amount sufficient to pay the Bonds when due. See “SECURITY FOR THE BONDS” and “LEGAL MATTERS--Certain Constitutional Limitations.” The Bonds do not and never shall constitute general obligations of the City of Aspen, Colorado or Pitkin County, Colorado.

This cover page contains certain information for quick reference only. It is not a summary of the issue. Investors must read the entire Official Statement to obtain information essential to making an informed investment decision.

The Bonds are offered when, as, and if issued by the District and accepted by the initial purchaser, subject to the approval of legality of the Bonds by Sherman & Howard L.L.C., Denver, Colorado, Bond Counsel, and the satisfaction of certain other conditions. Sherman & Howard L.L.C. also has acted as special counsel to the District in connection with this Official Statement. Certain legal matters will be passed upon for the District by Elaine Gerson, Esq., General Counsel. It is expected that the Bonds will be available for delivery through the facilities of DTC, on or about December 15, 2010.

This Official Statement is dated December 9, 2010.

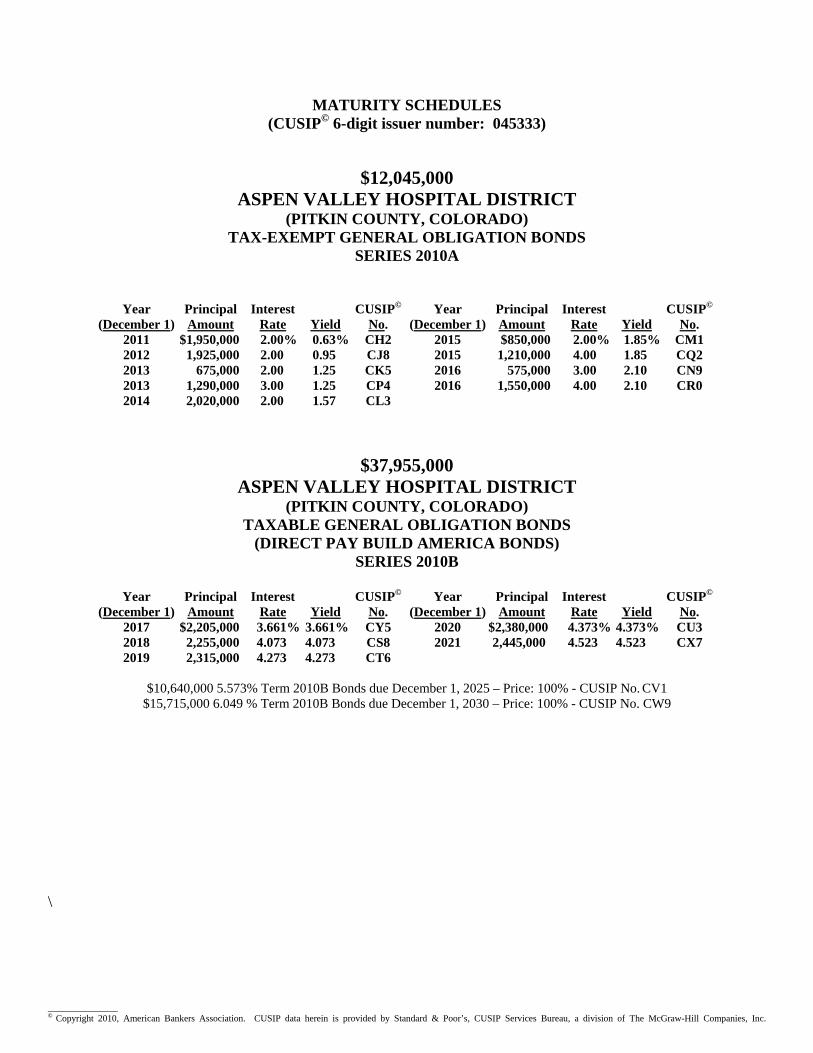

MATURITY SCHEDULES (CUSIP© 6-digit issuer number: 045333)

$12,045,000 ASPEN VALLEY HOSPITAL DISTRICT

(PITKIN COUNTY, COLORADO) TAX-EXEMPT GENERAL OBLIGATION BONDS

SERIES 2010A

Year (December 1)

Principal Amount

Interest Rate

Yield

CUSIP©

No. Year

(December 1)Principal Amount

Interest Rate

Yield

CUSIP©

No. 2011 $1,950,000 2.00% 0.63% CH2 2015 $850,000 2.00% 1.85% CM1 2012 1,925,000 2.00 0.95 CJ8 2015 1,210,000 4.00 1.85 CQ2 2013 675,000 2.00 1.25 CK5 2016 575,000 3.00 2.10 CN9 2013 1,290,000 3.00 1.25 CP4 2016 1,550,000 4.00 2.10 CR0 2014 2,020,000 2.00 1.57 CL3

$37,955,000 ASPEN VALLEY HOSPITAL DISTRICT

(PITKIN COUNTY, COLORADO) TAXABLE GENERAL OBLIGATION BONDS

(DIRECT PAY BUILD AMERICA BONDS) SERIES 2010B

Year

(December 1) Principal Amount

Interest Rate

Yield

CUSIP©

No. Year

(December 1)Principal Amount

Interest Rate

Yield

CUSIP©

No. 2017 $2,205,000 3.661% 3.661% CY5 2020 $2,380,000 4.373% 4.373% CU3 2018 2,255,000 4.073 4.073 CS8 2021 2,445,000 4.523 4.523 CX7 2019 2,315,000 4.273 4.273 CT6

$10,640,000 5.573% Term 2010B Bonds due December 1, 2025 – Price: 100% - CUSIP No. CV1

$15,715,000 6.049 % Term 2010B Bonds due December 1, 2030 – Price: 100% - CUSIP No. CW9

\ _______________ © Copyright 2010, American Bankers Association. CUSIP data herein is provided by Standard & Poor’s, CUSIP Services Bureau, a division of The McGraw-Hill Companies, Inc.

USE OF INFORMATION IN THIS OFFICIAL STATEMENT This Official Statement, which includes the cover page and the Appendices, does not constitute an offer to sell or

the solicitation of an offer to buy any of the Bonds in any jurisdiction in which it is unlawful to make such offer, solicitation, or sale. No dealer, salesperson, or other person has been authorized to give any information or to make any representations other than those contained in this Official Statement in connection with the offering of the Bonds, and if given or made, such information or representations must not be relied upon as having been authorized by the District or the Underwriter. The District maintains an internet website; however, the information presented there is not a part of this Official Statement and should not be relied upon in making an investment decision with respect to the Bonds.

The information set forth in this Official Statement has been obtained from the District, from the sources referenced throughout this Official Statement and from other sources believed to be reliable. No representation or warranty is made, however, as to the accuracy or completeness of information received from parties other than the District.

The Underwriter has provided the following sentence for inclusion in this Official Statement. The Underwriter has reviewed the information in this Official Statement pursuant to its responsibilities to investors under the federal securities laws, but the Underwriter does not guarantee the accuracy or completeness of such information.

This Official Statement contains, in part, estimates and matters of opinion which are not intended as statements of fact, and no representation or warranty is made as to the correctness of such estimates and opinions, or that they will be realized.

The information, estimates, and expressions of opinion contained in this Official Statement are subject to change without notice, and neither the delivery of this Official Statement nor any sale of the Bonds shall, under any circumstances, create any implication that there has been no change in the affairs of the District, or in the information, estimates, or opinions set forth herein, since the date of this Official Statement.

This Official Statement has been prepared only in connection with the original offering of the Bonds and may not be reproduced or used in whole or in part for any other purpose.

The Bonds have not been registered with the Securities and Exchange Commission due to certain exemptions contained in the Securities Act of 1933, as amended. In making an investment decision investors must rely on their own examination of the District, the Bonds and the terms of the offering, including the merits and risks involved. The Bonds have not been recommended by any federal or state securities commission or regulatory authority, and the foregoing authorities have neither reviewed nor confirmed the accuracy of this document.

THE PRICES AT WHICH THE BONDS ARE OFFERED TO THE PUBLIC BY THE UNDERWRITER (AND THE YIELDS RESULTING THEREFROM) MAY VARY FROM THE INITIAL PUBLIC OFFERING PRICES OR YIELDS APPEARING ON THE INSIDE COVER PAGE HEREOF. IN ADDITION, THE UNDERWRITER MAY ALLOW CONCESSIONS OR DISCOUNTS FROM SUCH INITIAL PUBLIC OFFERING PRICES TO DEALERS AND OTHERS. IN ORDER TO FACILITATE DISTRIBUTION OF THE BONDS, THE UNDERWRITER MAY ENGAGE IN TRANSACTIONS INTENDED TO STABILIZE THE PRICE OF THE BONDS AT A LEVEL ABOVE THAT WHICH MIGHT OTHERWISE PREVAIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME.

i

ASPEN VALLEY HOSPITAL DISTRICT PITKIN COUNTY, COLORADO

Board Of Directors John Sarpa, President

Barry Mink, M.D., Vice President Chuck Frias, Treasurer

Melinda Nagle, M.D., Director Lee Schumacher, Director

Administrative Officials

David Ressler, Chief Executive Officer Terry Collins, Chief Financial Officer

Elaine Gerson, Internal Legal Counsel

Nell Strijbos-Arthur – Secretary to the Board of Directors

Bond and Special Counsel

Sherman & Howard L.L.C.

Denver, Colorado

Registrar and Paying Agent

UMB Bank, n.a. Denver, Colorado

UNDERWRITER

RBC Capital Markets, LLC Denver, Colorado

ii

TABLE OF CONTENTS

PAGE INTRODUCTORY STATEMENT .................................................................................................1

General .........................................................................................................................................1 The District ..................................................................................................................................1 Security ........................................................................................................................................2 Purpose of the Bonds ...................................................................................................................3 The Bonds; Redemption Provisions.............................................................................................3 Taxable Build America Bonds.....................................................................................................3 Authority for Issuance..................................................................................................................4 Professionals ................................................................................................................................4 Tax Status of Interest on Bonds ...................................................................................................4 Continuing Disclosure Information Concerning the District.......................................................5 Certain Risks................................................................................................................................5 Additional Information ................................................................................................................6

SOURCES AND USES OF FUNDS...............................................................................................7 Sources and Uses of Funds ..........................................................................................................7 The Project ...................................................................................................................................7

THE BONDS ...................................................................................................................................8 General .........................................................................................................................................8 Designation of the 2010B Bonds as “Build America Bonds” .....................................................8 Payment Provisions......................................................................................................................8 Redemption Provisions ................................................................................................................9 Tax Covenants ...........................................................................................................................12 Defeasance .................................................................................................................................13 Bond Resolution Irrepealable ....................................................................................................14 Amendment of Bond Resolution ...............................................................................................14 Book-Entry Only System...........................................................................................................15

SECURITY FOR THE BONDS....................................................................................................16 General Ad Valorem Property Tax Pledge ................................................................................16 Pledge of Revenues; Priority .....................................................................................................17 Limitations on Remedies Available to Owners of Bonds..........................................................17

DEBT SERVICE SCHEDULE......................................................................................................19 THE DISTRICT.............................................................................................................................20

General .......................................................................................................................................20 Inclusion, Exclusion, Consolidation and Dissolution ................................................................20 District Powers...........................................................................................................................21 Governing Board........................................................................................................................22 Conflicts of Interest....................................................................................................................22 Administration ...........................................................................................................................23 Employees and Benefits.............................................................................................................23 District Insurance Coverage.......................................................................................................24 Existing Facilities.......................................................................................................................24

iii

Future Capital Expenditures ......................................................................................................25 Services Provided.......................................................................................................................26 Medical Staff..............................................................................................................................26 Service Area and Competition ...................................................................................................29 Aspen Valley Medical Foundation ............................................................................................29

DISTRICT FINANCIAL INFORMATION..................................................................................31 Sources of District Revenues .....................................................................................................31 Budget Process...........................................................................................................................31 Financial Statements ..................................................................................................................31 History of District Revenues and Expenses...............................................................................32 Budget Summary and Comparison ............................................................................................34 Management’s Discussion and Analysis of Recent Financial and Operational Performance ...35

PROPERTY TAXATION, ASSESSED VALUATION AND OVERLAPPING DEBT .............36 Ad Valorem Property Taxes ......................................................................................................36 Ad Valorem Property Tax Data .................................................................................................41 Mill Levies Affecting Property Owners Within the District .....................................................42 Estimated Overlapping General Obligation Debt ......................................................................43

DISTRICT DEBT STRUCTURE..................................................................................................45 Required Elections .....................................................................................................................45 General Obligation Debt ............................................................................................................45 Revenue and Other Financial Obligations .................................................................................45 Selected Debt Ratios ..................................................................................................................47

ECONOMIC AND DEMOGRAPHIC INFORMATION .............................................................48 Population and Age Distribution ...............................................................................................48 Income........................................................................................................................................49 Employment...............................................................................................................................50 Major Employers .......................................................................................................................52 Retail Sales.................................................................................................................................53 Building Permit Activity............................................................................................................53 Foreclosure Activity...................................................................................................................54 Recreation and Tourism.............................................................................................................55

TAX MATTERS............................................................................................................................58 2010A Bonds .............................................................................................................................58 2010B Bonds..............................................................................................................................59

FINANCIAL INSTITUTION INTEREST DEDUCTION............................................................61 LEGAL MATTERS.......................................................................................................................62

No Litigation..............................................................................................................................62 Sovereign Immunity...................................................................................................................62 Approval of Certain Legal Proceedings.....................................................................................63 Certain Constitutional Limitations.............................................................................................63 Police Power ..............................................................................................................................64

iv

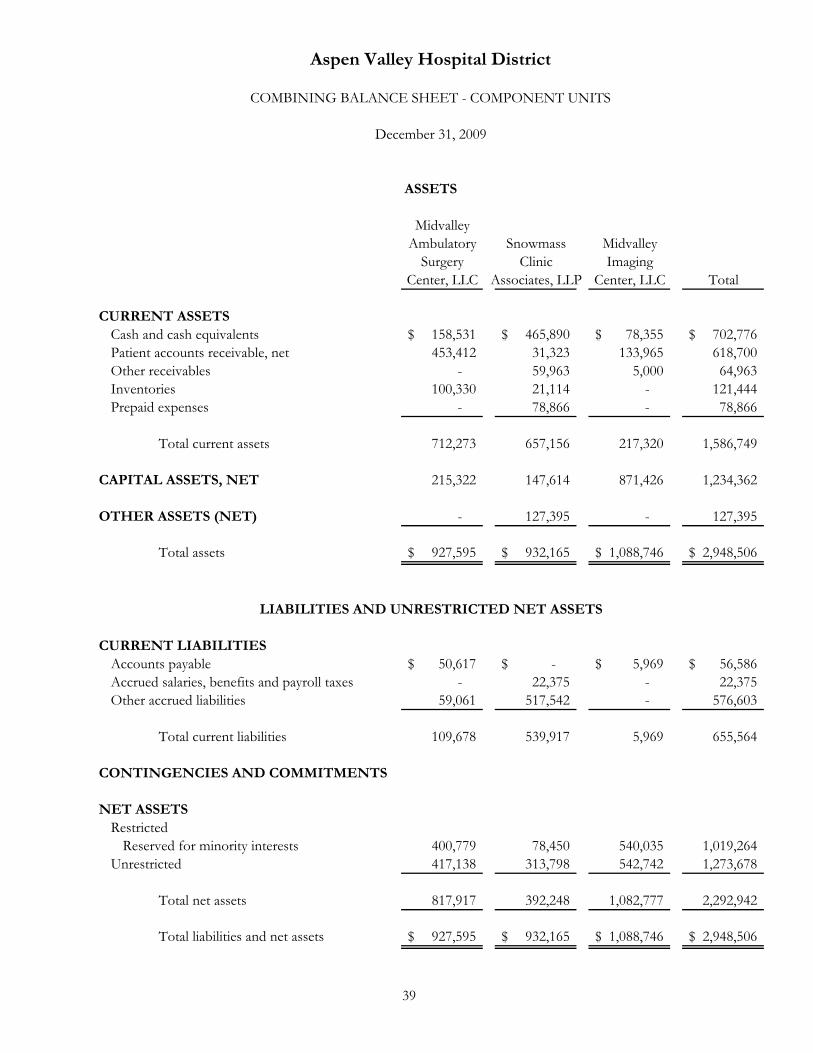

RATING ........................................................................................................................................64 INDEPENDENT AUDITORS.......................................................................................................65 UNDERWRITING ........................................................................................................................65 OFFICIAL STATEMENT CERTIFICATION..............................................................................65 APPENDIX A - Audited Basic Financial Statements for the years ended December 31, 2009

and 2008........................................................................................................ A-1 APPENDIX B - Book-Entry Only System...............................................................................B-1

APPENDIX C - Form of Continuing Disclosure Certificate....................................................C-1 APPENDIX D - Form of Opinion of Bond Counsel ............................................................... D-1

v

INDEX OF TABLES

NOTE: Tables marked with an (*) indicate Annual Financial Information to be updated pursuant to SEC Rule 15c2-12, as amended. See Appendix C.

Table Page

Sources and Uses of Funds ............................................................................................................. 7 Debt Service Requirements........................................................................................................... 19 Active, Provisional, Consulting, Affiliate and Honorary Medical Staff Profile June 30, 2010 ... 27 Active, Provisional, Consulting and Emeritus Medical Staff Profile June 30, 2010.................... 28 Top 20 Physicians Rated by Discharge Volume (Year Ended December 31, 2009) ................... 29 *Statement of Revenues, Expenses and Changes in Net Assets for 2005-2009........................... 33 *General Fund Budget Summary and Comparison (1)(2)............................................................ 34 *History of Assessed Valuations and Mill Levies for the District ............................................... 41 *Property Tax Collections in the District ..................................................................................... 41 *2010 Assessed Valuation of Classes of Property in the District................................................. 42 *Ten Largest Taxpayers in the District for 2010 .......................................................................... 42 Sample Mill Levies Affecting Property Owners Within the District - 2009 ................................ 43 Estimated Overlapping General Obligation Indebtedness............................................................ 44 Selected Debt Ratios of the District as of the Date of the Issuance of the Bonds ........................ 47 Population ..................................................................................................................................... 48 Age Distribution............................................................................................................................ 49 Annual Per Capita Personal Income ............................................................................................. 49 Median Household Effective Buying Income............................................................................... 50 Percent of Households by Effective Buying Income Group - 2010 ............................................. 50 Labor Force and Employment ...................................................................................................... 51 Average Number of Employees Within Selected Industries – Pitkin County.............................. 52 Selected Major Employers in the City of Aspen .......................................................................... 53 Retail Sales (in thousands)............................................................................................................ 53 Building Permit Issuances in the City of Aspen ........................................................................... 54 Building Permits Issued in Pitkin County..................................................................................... 54 History of Foreclosures - Pitkin County ....................................................................................... 55 Historical Skier Visits ................................................................................................................... 56 Mountain Statistics – Aspen/Snowmass ....................................................................................... 57

1

OFFICIAL STATEMENT

$12,045,000

ASPEN VALLEY HOSPITAL DISTRICT (PITKIN COUNTY, COLORADO)

TAX-EXEMPT GENERAL OBLIGATION BONDS SERIES 2010A

$37,955,000

ASPEN VALLEY HOSPITAL DISTRICT (PITKIN COUNTY, COLORADO)

TAXABLE GENERAL OBLIGATION BONDS (DIRECT PAY BUILD AMERICA BONDS)

SERIES 2010B

INTRODUCTORY STATEMENT

General

This Official Statement, including the cover page and appendices, is furnished by the Aspen Valley Hospital District, Pitkin County, Colorado (the “District”), a quasi-municipal corporation and political subdivision of the State of Colorado (the “State”), to provide information about the District and its $50,000,000 General Obligation Bonds, Series 2010, consisting of $12,045,000 Tax-Exempt General Obligation Bonds, Series 2010A (the “2010A Bonds”) and $37,955,000 Taxable General Obligation Bonds (Direct Pay Build America Bonds), Series 2010B (the “2010B Bonds” and, together with the 2010A Bonds, the “Bonds”). The Bonds will be issued pursuant to a resolution adopted by the Board of Directors of the District (the “Board”) prior to the issuance of the Bonds (the “Bond Resolution”).

The offering of the Bonds is made only by way of this Official Statement, which supersedes any other information or materials used in connection with the offer or sale of the Bonds. The following introductory material is only a brief description of and is qualified by the more complete information contained throughout this Official Statement. A full review should be made of the entire Official Statement and the documents summarized or described herein. Detachment or other use of this “INTRODUCTION” without the entire Official Statement, including the cover page and appendices, is unauthorized.

The District

Aspen Valley Hospital District (the “District”), located in the City of Aspen (the “City”) and Pitkin County, Colorado (the “County”) has been in existence under various governance since 1890. The District was formed and approved by the Board of County Commissioners of the County on August 5, 1974. On January 1, 1977, the District assumed the operations of Aspen Valley Hospital. The District is a quasi-municipal corporation and political subdivision of the State of Colorado organized pursuant to the laws of the State, particularly Article 1 of Title 32, Colorado Revised Statutes, as amended, and presently owns and operates an

2

acute care hospital which is known as Aspen Valley Hospital (the “Hospital Facility” or “Hospital Facilities”), located in the City. The Hospital Facility was constructed in 1977 and was originally licensed to accommodate 49 beds. The Hospital Facility as presently configured has 25 licensed beds. The geographic boundaries of the District include substantially all residential and commercial property in Pitkin County, including, the City, the Town of Snowmass Village, Woody Creek, Old Snowmass and parts of the Town of Basalt. The geographic boundaries of the District define the real property in Pitkin County which is subject to ad valorem taxation by the District and which residents and property owners within Pitkin County are allowed to participate in District elections. The geographic boundaries of the District do not define its service area. The District’s current population is estimated to be approximately 14,384. The District’s 2010 preliminary certified assessed valuation is $3,649,568,110 (subject to change on or before December 10, 2010). See “THE DISTRICT.”

Security

General. The Bonds constitute general obligations of the District. All of the taxable property in the District is subject to the levy of an ad valorem tax to pay the principal of and interest on the Bonds without limitation as to rate and in an amount sufficient to pay the Bonds when due, subject to the limitations contained in the authorizing question adopted at an election held on November 2, 2010 (the “Election”). The District will covenant in the Bond Resolution to levy such taxes in an amount which, together with other legally available funds of the District, if any, is sufficient to pay debt service on the Bonds. See “SECURITY FOR THE BONDS” and “LEGAL MATTERS--Certain Constitutional Limitations.”

Election. At the Election, the electors of the District approved the issuance of general obligation bonds in an amount not to exceed $50,000,000 with a total repayment cost not to exceed $86,850,000 and a maximum annual repayment cost not to exceed $4,363,000. The electors also approved increased ad valorem property taxes to pay debt service on such bonds, provided that the annual amount of such taxes cannot exceed $4,363,000. The District may not exceed these limitations for any reason. See “SECURITY FOR THE BONDS” and “LEGAL MATTERS--Certain Constitutional Limitations.”

Additional Bonds. After issuance of the Bonds, the District will have outstanding $50,000,000 in general obligation debt, consisting of the Bonds. After issuance of the Bonds, the District will have no remaining voter authorization from the Election. However, the District may seek voter authorization to issue additional general obligation bonds at any time in compliance with existing law.

In addition to the Bonds, the District has two series of revenue bonds outstanding, which bonds are payable solely from hospital revenues. In 2003, the District issued its Aspen Valley Hospital District Variable Rate Demand Revenue Bonds, Series 2003 (the “Series 2003 Bonds”) and in 2007, the District issued its Aspen Valley Hospital District Refunding Revenue Bonds, Series 2007 (the “Series 2007 Bonds”), which were issued on a parity with the Series 2003 Bonds. The District’s revenue bonds are payable solely from the “net revenues” of the District and are not payable from general ad valorem property taxes imposed for the payment of the Bonds. See “DISTRICT DEBT STRUCTURE--Revenue and Other Financial Obligations.”

3

Purpose of the Bonds

The proceeds of the Bonds will be used (i) finance the acquisition, improvement, construction, equipping and furnishing of certain improvements to the Hospital Facility (the “Project”), and (ii) to pay the costs of issuance of the Bonds. See “SOURCES AND USES OF FUNDS.”

The Bonds; Redemption Provisions

The Bonds are issued solely as fully registered certificates in the denomination of $5,000, or any integral multiple thereof. The Bonds initially will be registered in the name of Cede & Co., as nominee of The Depository Trust Company, New York, New York (“DTC”), the securities depository for the Bonds. Purchases of the Bonds are to be made in book-entry form only. Purchasers will not receive certificates representing their beneficial ownership interest in the Bonds. See “THE BONDS--Book-Entry Only System.” The Bonds mature and bear interest (calculated based on a 360-day year consisting of twelve 30-day months) as set forth on the inside cover page of this Official Statement. The payment of principal and interest on the Bonds is described in “THE BONDS--Payment Provisions.”

The 2010A Bonds are not subject to redemption prior to maturity. The 2010B Bonds are subject to redemption prior to maturity at the option of the District, are subject to mandatory sinking fund redemption, and are also subject to extraordinary optional redemption. See “THE BONDS--Redemption Provisions.”

Taxable Build America Bonds

The 2010B Bonds are expected to be issued as Direct Pay Build America Bonds. See “THE BONDS--Tax Covenants.” Accordingly, the District expects to receive revenue from the United States Treasury related to the interest payable on the 2010B Bonds.

Build America Bonds Generally. In February 2009, as part of the American Recovery and Reinvestment Act of 2009 (the “Recovery Act”), Congress added Sections 54AA and 6431 to the Tax Code, which permit state or local governments to obtain certain tax advantages when issuing taxable obligations that meet certain requirements of the Tax Code and the related Treasury regulations. Such bonds are referred to as “Build America Bonds.” A Build America Bond is a qualified bond under Section 54AA(g) of the Tax Code (a “Qualified Build America Bond”) if it meets certain requirements of the Tax Code and the related Treasury Regulations and the issuer has made an irrevocable election to have the special rule for qualified bonds apply. Interest on Qualified Build America Bonds is included in gross income for federal income tax purposes, and owners of Qualified Build America Bonds will not receive any tax credits as a result of ownership of such Qualified Build America Bonds when an issuer has elected to receive the BAB Credit, as defined in “THE BONDS--Designation of the 2010B Bonds as Build America Bonds.”

The 2010B Bonds as Qualified Build America Bonds. In the Bond Resolution, the District has made an irrevocable election to treat the 2010B Bonds as Qualified Build America Bonds. As a result of this election, interest on the 2010B Bonds will be includable in gross income of the holders thereof for federal income tax purposes and the holders of the 2010B

4

Bonds will not be entitled to any tax credits as a result of either ownership of the 2010B Bonds or receipt of any interest payments on the 2010B Bonds. See “TAX MATTERS--2010B Bonds.”

Authority for Issuance

The Bonds will be issued pursuant to the Constitution and laws of the State, particularly Title 32, Article 1, Part 1, Colorado Revised Statutes (“C.R.S.”), the Supplemental Public Securities Act (Title 11, Article 57, Part 2, C.R.S.) and the Bond Resolution. The 2010B Bonds also will be issued pursuant to Article 59.7 of Title 11, C.R.S., as amended.

Professionals

Sherman & Howard L.L.C., Denver, Colorado, has acted as Bond Counsel in connection with the execution and delivery of the Bonds and also has acted as special counsel to the District in connection with this Official Statement. The fees of Sherman & Howard L.L.C. will be paid only at closing from the proceeds of the Bonds. Certain legal matters will be passed on for the District by the District’s general counsel, Elaine Gerson, Esq. Grant Thornton LLP, independent certified public accountants, Wichita, Kansas, have audited the District’s basic financial statements which are attached hereto as Appendix A. See “INDEPENDENT AUDITORS.” UMB Bank, n.a., will act as the paying agent and registrar for the Bonds (the “Paying Agent” and “Registrar”). RBC Capital Markets, LLC, will act as the underwriter for the Bonds (the “Underwriter”). See “UNDERWRITING.”

Tax Status of Interest on Bonds

2010A Bonds. In the opinion of Sherman & Howard L.L.C., Bond Counsel, assuming continuous compliance with certain covenants described herein, interest on the 2010A Bonds is excluded from gross income under federal income tax laws pursuant to Section 103 of the Internal Revenue Code of 1986, as amended to the date of delivery of the 2010A Bonds (the “Tax Code”), interest on the 2010A Bonds is excluded from alternative minimum taxable income as defined in Section 55(b)(2) of the Tax Code, and interest on the 2010A Bonds is excluded from Colorado taxable income and Colorado alternative minimum taxable income under Colorado income tax laws in effect on the date of delivery of the 2010A Bonds as described herein. See “TAX MATTERS.”

The District has designated the 2010A Bonds as “qualified tax-exempt obligations” for purposes of Section 265(b)(3) of the Tax Code. See “FINANCIAL INSTITUTION INTEREST DEDUCTION.”

2010B Bonds. In the opinion of Sherman & Howard L.L.C., Bond Counsel interest on the 2010B Bonds is included in gross income under current federal income tax laws and the owners of the 2010B Bonds will not receive a tax credit as a result of owning the 2010B Bonds. In the opinion of Bond Counsel, interest on and income from the 2010B Bonds is exempt from all taxation and assessments in the State of Colorado. Bond Counsel’s opinion regarding the status of the 2010B Bonds under Colorado law specifically assumes that the District will comply with the covenants described under the heading “TAX MATTERS” and the failure to comply with these covenants could result in the interest on and income from the 2010B

5

Bonds becoming subject to taxation and assessments in the State of Colorado. See “TAX MATTERS.”

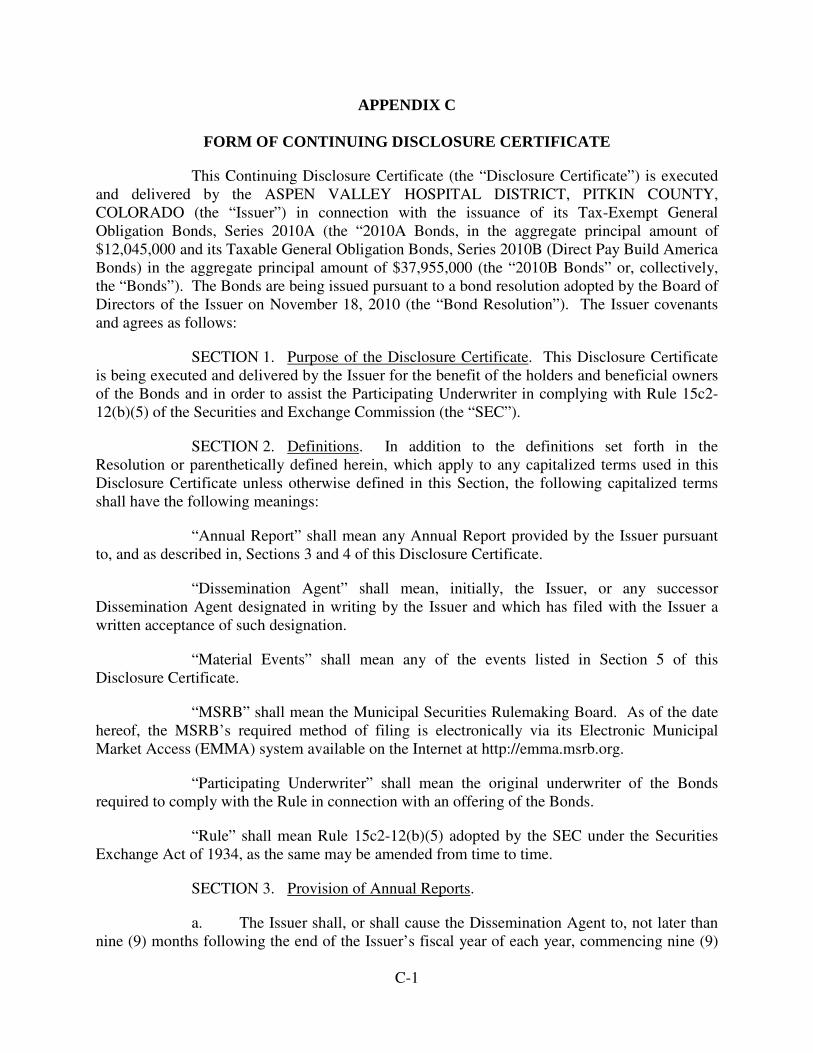

Continuing Disclosure Information Concerning the District

The District will execute a continuing disclosure certificate (the “Disclosure Certificate”) at the time of the closing for the Bonds. The Disclosure Certificate will be executed for the benefit of the beneficial owners of the Bonds and the District will covenant in the Bond Resolution to comply with its terms. The Disclosure Certificate will provide that so long as the Bonds remain outstanding, the District will provide the following information to the Municipal Securities Rulemaking Board, acting through its Electronic Municipal Market Access (“EMMA”) system: (i) certain annual financial information and operating data; and (ii) notice of certain material events. The form of the Disclosure Certificate is attached hereto as Appendix C.

The District made similar undertakings when it issued prior revenue obligations. For the past five fiscal years, the District reports that it has complied in a timely fashion with the terms of the Continuing Disclosure Certificate.

Certain Risks

The purchase of the Bonds involves certain investment risks that are discussed throughout this Official Statement. Accordingly, each prospective purchaser of the Bonds should make an independent evaluation of all of the information presented in this Official Statement in order to make an informed investment decision. Certain risks with respect to the payment of debt service on the Bonds are discussed in the sections entitled “SECURITY FOR THE BONDS--General Ad Valorem Property Tax Pledge,” “SECURITY FOR THE BONDS--Limitations on Remedies Available to Owners” and “PROPERTY TAXATION, ASSESSED VALUATION AND OVERLAPPING DEBT--Property Tax Data;” however, the discussion of risks associated with the Bonds is not limited to those sections. Risks associated with the District’s operations also are discussed throughout this Official Statement. Investors must review the entire Official Statement in order to make an informed investment decision.

6

Additional Information

This Introduction is only a brief summary of the provisions of the Project, the Bonds and the Bond Resolution and other documents described in this Official Statement; a full review of the entire Official Statement should be made by potential investors. Summary descriptions of the Bonds, the Bond Resolution and other documents described in this Official Statement are qualified by reference to such documents. This Official Statement speaks only as of its date and the information contained herein is subject to change. Additional information is available from the District or the Underwriter as follows:

The District Underwriter Aspen Valley Hospital District RBC Capital Markets, LLC 0401 Castle Creek Road 1200 17th Street, Suite 2150 Aspen, Colorado 81611 Denver, Colorado 80202 Attention: Chief Financial Officer Attention: Terry Casey Telephone: (970) 544-1261 Telephone: (303) 595-1204

7

SOURCES AND USES OF FUNDS

Sources and Uses of Funds

The proceeds from the sale of the Bonds are expected to be applied as shown in the following table.

Sources and Uses of Funds

Sources 2010A Bonds 2010B Bonds Par amount of Bonds....................................................... $12,045,000.00 $37,955,000.00 Plus: Net reoffering premium ........................................ 499,826.55 0.00 Less: Net original issue discount ................................... $12,544,826.55 $37,955,000.00

Total Uses The Project ...................................................................... $12,442,025.12 $37,631,062.43 Costs of issuance (including underwriting discount) ...... 102,801.43 323,937.57

Total............................................................................ $12,544,826.55 37,955,000.00 Source: The Underwriter. The Project

A portion of the proceeds of the Bonds will be utilized to acquire, improve, construct, equip and furnish Hospital Facilities as approved by the voters of the District at the Election (the “Project”). Such improvements include, but are not limited to, (i) modernizing and expanding the Hospital Facilities to meet contemporary standards for treatment and technology, (ii) enhancing the quality, safety and privacy of patient care; and (iii) rightsizing and reconfiguring of Hospital Facilities to meet the present and future healthcare needs of the community.

On July 12, 2010, the City of Aspen approved the District’s Master Facility Plan Phase II Expansion and Renovation Project. The start date of construction of the Project is expected to be on or about December 1, 2010, with an estimated 28 month construction period. The estimated cost of the Project is approximately $75,137,000, with a portion of the Project to be funded with the proceeds of the Bonds and the remainder with District funds or private contributions. Specifically, the Project is expected to: expand the Hospital Facility by 62,200 square feet, while also renovating another 26,330 square feet, create an additional 15,500 square feet in employee housing units to provide an additional 18 units and to create a new three level parking garage providing 235 parking spaces. Finally, the scope of Project includes: (i) expansion and renovation of the Patient Care Unit (PCU) to total 27 new patient rooms and the Intensive Care Unit (ICU) to total four beds; (ii) creation of new Cardiac Rehabilitation (Cardiac Rehab) and Physical Therapy (PT) departments, Medical Office Space and cafeteria and kitchen, as well as clinical spaces and gift shop and volunteer areas; and (iii) relocation and expansion of Cardiopulmonary and Same Day Surgery departments, chemo therapy, nuclear medicine and stress test areas, as well as Administration, Finance, Human Resources and mail room. Other

8

enhancements include: improved storm drainage, multiple road and transportation improvements and the attainment of a LEED (green energy) rating.

THE BONDS

General

The Bonds will be dated as of their date of delivery and will mature on the dates and in the amounts as set forth on the inside cover page of this Official Statement. The Bonds will be issued as fully registered bonds in denominations of $5,000 or integral multiples thereof and will initially be registered in the name of “Cede & Co.,” as nominee for DTC. Purchases by beneficial owners of the Bonds (“Beneficial Owners”) are to be made in book-entry only form in the principal amount of $5,000 or any integral multiple thereof. Payments to Beneficial Owners are to be made as described below in “Book-Entry Only System.”

Designation of the 2010B Bonds as “Build America Bonds”

The District intends to designate the 2010B Bonds as Build America Bonds for purposes of the federal Recovery Act and to receive BAB Credit payments (defined in the Bond Resolution as the credit provided in Section 6431 of the Tax Code in lieu of any credit otherwise available to the owners of the 2010B Bonds under Section 54AA(a) of the Code) from the United States Treasury equal to 35% of the interest payable on the 2010B Bonds. See “TAX MATTERS--2010B Bonds.” Under current State law, BAB Credits may be used by the District for any lawful purpose for which the District may spend money. The BAB Credits are not pledged to pay debt service on the Bonds or any other District bonds. See “SECURITY FOR THE BONDS” for a description of the security and sources of payment of the Bonds.

Payment Provisions

Interest on the Bonds (calculated based on a 360-day year consisting of twelve 30-day months) is payable semiannually on June 1 and December 1, commencing June 1, 2011. The principal of and premium, if any, on any Bond shall be payable to the registered owner thereof as shown on the registration records kept by the Registrar, upon maturity or prior redemption of the Bonds and upon presentation and surrender at the principal office of the Paying Agent. If any Bond shall not be paid upon such presentation and surrender at maturity, it shall continue to draw interest at the same interest rate borne by said Bond until the principal thereof is paid in full. Payment of interest on any Bond shall be made to the registered owner thereof by the Paying Agent, on or before each interest payment date (or, if such interest payment date is not a Business Day, on or before the next succeeding Business Day), to the registered owner thereof at his or her address as it last appears on the registration books kept by the Registrar on the fifteenth day (whether or not a business day) of the calendar month immediately preceding such interest payment date (the “Record Date”); but any such interest not so timely paid or duly provided for shall cease to be payable to the person who is the registered owner thereof at the close of business on the Record Date and shall be payable to the person who is the registered owner thereof at the close of business on a Special Record Date for the payment of any such defaulted interest. The Special Record Date and the date for payment of defaulted interest shall be fixed by the Registrar whenever moneys become available for payment of the

9

defaulted interest. Notice of the Special Record Date and the date for payment of defaulted interest shall be given to the registered owners of the Bonds not less than ten days prior thereto by first-class mail to each such registered owner as shown on the Registrar’s registration books on a date selected by the Registrar. The Paying Agent may make payments of interest on any Bond by such alternative means as may be mutually agreed to between the Owner of such Bond and the Paying Agent. All such payments shall be made in lawful money of the United States of America without deduction for the services of the Paying Agent or Registrar.

Notwithstanding the foregoing, payments of the principal of and interest on the Bonds will be made directly to DTC or its nominee, Cede & Co., by the Paying Agent, so long as DTC or Cede & Co. is the registered owner of the Bonds. Disbursement of such payments to DTC’s Participants is the responsibility of DTC, and disbursements of such payments to the Beneficial Owners is the responsibility of DTC’s Participants and the Indirect Participants, as more fully described herein. See “Book-Entry Only System” below.

Redemption Provisions

No Redemption of the 2010A Bonds. The 2010A Bonds are not subject to redemption prior to maturity.

Optional Redemption - 2010B Bonds. The 2010B Bonds maturing on or before December 1, 2020 are not subject to redemption prior to maturity at the option of the District. The 2010B Bonds maturing on and after December 1, 2021, shall be subject to redemption prior to their respective maturities at the option of the District, in whole or in part, in integral multiples of $5,000, from such maturities as are selected by the District and by lot within a maturity and interest rate (giving proportionate weight to Bonds in denominations larger than $5,000), in such a manner as the District may determine, on December 1, 2020, or on any date thereafter at a redemption price equal to the principal amount so redeemed plus accrued interest to the redemption date without a redemption premium.

Mandatory Sinking Fund Redemption. The 2010B Bonds maturing on December 1, 2025 and December 1, 2030 (the “Term Bonds”), are subject to mandatory sinking fund redemption at a price equal to the principal amount thereof plus accrued interest thereon to the redemption date. Term Bonds subject to mandatory sinking fund redemption shall be selected by lot in such manner as the Registrar shall determine (giving proportionate weight to 2010B Bonds in denominations larger than $5,000).

As and for a sinking fund for the redemption of the 2010B Bonds maturing December 1, 2025, the District will deposit into the Bond Fund (as defined in the Resolution) on or before December 1, 2022 and on or before each December 1 through and including December 1, 2024, a sum, which together with other moneys available in the Bond Fund is sufficient to redeem (after credit as provided in the Resolution) the following principal amounts of the Bonds maturing December 1, 2025:

10

Sinking Fund Redemption(December 1)

Principal Amount

2022 $2,520,000 2023 2,610,000 2024 2,705,000

The remaining $2,805,000 of the 2010B Bonds maturing on December 1, 2025,

shall be paid upon presentation and surrender at maturity unless redeemed pursuant to optional redemption prior to maturity.

As and for a sinking fund for the redemption of the 2010B Bonds maturing

December 1, 2030, the District will deposit into the Bond Fund (as defined in the Resolution) on or before December 1, 2026 and on or before each December 1 through and including December 1, 2029, a sum, which together with other moneys available in the Bond Fund is sufficient to redeem (after credit as provided in the Resolution) the following principal amounts of the Bonds maturing December 1, 2030:

Sinking Fund Redemption(December 1)

Principal Amount

2026 $2,905,000 2027 3,020,000 2028 3,140,000 2029 3,260,000

The remaining $3,390,000 of the 2010B Bonds maturing on December 1, 2030,

shall be paid upon presentation and surrender at maturity unless redeemed pursuant to optional redemption prior to maturity.

At its option, to be exercised on or before the sixtieth day next preceding each

sinking fund redemption date, the District may (a) deliver to the Registrar for cancellation Term Bonds subject to mandatory sinking fund redemption on such date in an aggregate principal amount desired or (b) receive a credit in respect of its sinking fund redemption obligation for any Term Bonds subject to mandatory sinking fund redemption on such date, which prior to said date have been redeemed (otherwise than through the operation of the sinking fund) and canceled by the Registrar and not theretofore applied as a credit against any sinking fund redemption obligation. Each Term Bond so delivered or previously redeemed will be credited by the Registrar at the principal amount thereof on the obligation of the District on such sinking fund redemption date and the principal amount of Term Bonds to be redeemed by operation of such sinking fund on such date will be accordingly reduced.

Extraordinary Optional Redemption. The 2010B Bonds are subject to extraordinary redemption prior to their respective maturities, at the option of the District, upon the occurrence of an Extraordinary Event (defined below), as a whole or in part, on any date, at a redemption price equal to the greater of (a) the principal amount thereof plus accrued interest to

11

the redemption date on the 2010B Bonds to be redeemed, or (b) the sum of the present value of the remaining scheduled payments of principal and interest to the maturity date of the 2010B Bonds to be redeemed, not including any portion of those payments of interest accrued and unpaid as of the date on which the 2010B Bonds are to be redeemed, discounted to the date on which the 2010B Bonds are to be redeemed on a semiannual basis, assuming a 360-day year consisting of twelve 30-day months, at the “Treasury Rate” plus 100 basis points provided that the redemption price shall not exceed 103%, plus, in each case, accrued and unpaid interest on the 2010B Bonds to be redeemed to the redemption date.

For purposes of the preceding paragraph, “Treasury Rate” means, with respect to any redemption date for a particular 2010B Bond, the yield to maturity as of such redemption date of United State Treasury securities with a constant maturity (as compiled and published in the most recent Federal Reserve Statistical Release H.15 (519) that has become publicly available at least two Business Days prior to the redemption date (excluding inflation-indexed securities) or, if such Statistical Release is no longer published, any publicly available source of similar market data) most nearly equal to the period from the redemption date to the maturity date of the 2010B Bonds to be redeemed; provided, however that if the period from the redemption date to the maturity date is less than one year, the weekly average yield on actually traded United States Treasury securities adjusted to a constant maturity of one year shall be used.

The Paying Agent shall have the right to retain, at the expense of the District, an independent accounting firm, investment banking firm or financial advisor subject to the District’s approval to determine the redemption price and perform all actions and make all calculations required to determine the redemption price. The Paying Agent and the District may conclusively rely on such accounting firm’s, investment banking firm’s or financial advisor’s calculations in connection with, and determination of, the redemption price, and shall bear no liability for such reliance.

The Bond Resolution defines “Extraordinary Event” as: (i) a material adverse change has occurred to Section 54AA or 6431 of the Code, (ii) there is any guidance published by the Internal Revenue Service or the United States Treasury with respect to such Sections, or (iii) any other determination by the Internal Revenue Service or the United States Treasury, which determination is not the result of a failure of the District to satisfy the requirements of Section 830(B) of the Tax Code, and as a result thereof, the BAB Credit expected to be received with respect to the 2010B Bonds is eliminated or reduced, as reasonably determined by the President, Chief Executive Officer or the Chief Financial Officer, which determination shall be conclusive.

Notice of Redemption. Notice of any redemption shall be given by the Paying Agent in the name of the District by sending a copy of such notice by first-class, postage prepaid mail, not more than 60 days and not less than 30 days prior to the redemption date to the initial purchaser of the Bonds (the “Initial Purchaser” or the “Purchaser”) and to each Registered Owner of any Bond all or a portion of which is called for redemption at his or her address as it last appears on the registration books kept by the Registrar. Failure to give such notice by mailing to the Registered Owner of any Bond or to the Purchaser, or any defect therein, shall not affect the validity of the proceedings for the redemption of any other Bonds. Except as described below, prior to any redemption date, the District shall deposit with the Paying Agent an amount

12

of money sufficient to pay the redemption price of all the Bonds or portions of Bonds which are to be redeemed on that date. In addition to the foregoing notice, further notice may be given by the Paying Agent in order to comply with the requirements of any depository holding the Bonds but no defect in said further notice nor any failure to give all or any portion of such further notice shall in any manner defeat the effectiveness of a call for redemption if notice thereof is given as above prescribed.

Official notice of redemption having been given as described above, the Bonds or portions of Bonds so to be redeemed shall, on the redemption date, become due and payable at the redemption price therein specified, and from and after such date (unless the District shall default in the payment of the redemption price) such Bonds or portions of Bonds shall cease to bear interest.

Notwithstanding the foregoing provisions, any notice of optional redemption may contain a statement that the redemption is conditioned upon the receipt by the Paying Agent of funds on or before the date fixed for redemption sufficient to pay the redemption price of the Bonds so called for redemption, and that if such funds are not available, such redemption shall be cancelled by written notice to the Owners of the Bonds called for redemption in the same manner as the original redemption notice was mailed.

Tax Covenants

In the Bond Resolution, the District covenants for the benefit of the registered owners of the 2010A Bonds (the “Owners” or “Registered Owners”) that it will not take any action or omit to take any action with respect to the 2010A Bonds, the proceeds thereof, any other funds of the District or any facilities financed or refinanced with the proceeds of the 2010A Bonds, if such action of omission (i) would cause the interest on the 2010A Bonds to lose its exclusion from gross income for federal income tax purposes under Section 103 of the Tax Code, (ii) would cause interest on the 2010A Bonds to lose its exclusion from alternative minimum taxable income as defined in Section 55(b)(2) of the Tax Code, or (iii) would cause interest on the 2010A Bonds to lose its exclusion from Colorado taxable income and Colorado alternative minimum taxable income under present State law. The foregoing covenant shall remain in full force and effect notwithstanding the payment in full or defeasance of the 2010A Bonds until the date on which all obligations of the District in fulfilling the covenant under the Tax Code have been met.

In the Bond Resolution, the District makes an irrevocable election that Section 54AA of the Tax Code shall apply to the 2010B Bonds and that subsection (g) of Section 54AA will also apply to the 2010B Bonds so that the District will receive the credit provided in Section 6431 of the Tax Code in lieu of any BAB Credit otherwise available to the bondholders of the 2010B Bonds under Section 54AA(a) of the Tax Code. None of the Owners of the 2010B Bonds shall be entitled to any credit under Section 54AA of the Tax Code. The District covenants that it will not take any action or omit to take any action with respect to the 2010B Bonds, the proceeds thereof, any other funds of the District or the Project if such action or omission would cause the District to not be entitled to the BAB Credit. In furtherance of this covenant, the District agrees to comply with the procedures set forth in the Tax Compliance Certificate to be executed with respect to the 2010B Bonds. The foregoing covenant shall remain in full force

13

and effect notwithstanding the payment in full or defeasance of the 2010B Bonds until the date on which all obligations of the District in fulfilling the covenant have been met. The District also covenants that it will timely file any document required by the Internal Revenue Service to be filed in order to claim the BAB Credit.

Defeasance

When the Bonds shall be paid in accordance with their terms (or payment of the Bonds has been provided for in the manner described below), then the Bond Resolution and all rights granted thereunder shall thereupon cease, terminate and become void and be discharged and satisfied.

Payment of any Outstanding Bond shall, prior to the maturity or redemption date thereof, be deemed to have been provided for within the meaning and with the effect expressed described in this paragraph if: (a) in case the Bond is to be redeemed on any date prior to its maturity, the District shall have given to the Paying Agent irrevocable instructions to give notice of redemption of such Bond on said redemption date in accordance with the provisions described in “Redemption Provisions - Notice of Redemption” above, (b) there shall have been deposited with the Paying Agent or a commercial bank exercising trust powers either moneys in an amount which shall be sufficient, or Federal Securities (defined below) which shall not contain provisions permitting the redemption thereof at the option of the issuer, the principal of and the interest on which when due, and without any reinvestment thereof, will provide moneys which, together with the moneys, if any, deposited with or held by the Paying Agent or other commercial bank exercising trust powers at the same time, shall be sufficient to pay when due the principal of and interest due and to become due on the Bond on and prior to the redemption date or maturity date thereof, as the case may be, and (c) in the event the Bond is not by its terms subject to redemption within the next sixty days, the District shall have given the Paying Agent irrevocable instructions to give, as soon as practicable in the same manner as the notice of redemption is given pursuant to the Bond Resolution, a notice to the Owner of such Bond that the deposit required by (b) above has been made with the Paying Agent or other a commercial bank exercising trust powers and that payment of the Bond has been provided for as described in this paragraph and stating such maturity or redemption date upon which moneys are to be available for the payment of the principal of and interest of the Bond. Neither such securities nor moneys deposited with the Paying Agent or other commercial bank exercising trust powers as described above or principal or interest payments on any such Federal Securities shall be withdrawn or used for any purpose other than, and shall be held in trust for, the payment of the principal of and interest on the Bond; provided any cash received from such principal or interest payments on such Federal Securities deposited with the Paying Agent or other commercial bank exercising trust power, if not then needed for such purpose, shall, to the extent practicable, be reinvested in securities of the type described in (b) of this paragraph maturing at times and in amounts sufficient to pay when due the principal of and interest to become due on the Bond on or prior to such redemption date or maturity date thereof, as the case may be. At such time as payment of a Bond has been provided for as aforesaid, such Bond shall no longer be secured by or entitled to the benefits of the Bond Resolution, except for the purpose of any payment from such moneys or securities deposited with the Paying Agent or other commercial bank exercising trust powers.

14

Upon compliance with the provisions described above with respect to all Bonds then Outstanding, the Bond Resolution may be discharged in accordance with the provisions described above, but the liability of the District in respect of the Bonds shall continue; provided that the Owners thereof shall thereafter be entitled to payment only out of the moneys or Federal Securities deposited with the Paying Agent or other commercial bank exercising trust powers as described above.

The Bond Resolution defines “Federal Securities” to mean only direct obligations of, or obligations the principal of and interest on which are unconditionally guaranteed by, the United States (or ownership interests in any of the foregoing) and which are not callable prior to their scheduled maturities by the issuer thereof.

Bond Resolution Irrepealable

In accordance with Article XI, Section 6 of the Constitution of the State, the Bond Resolution provides that after any of the Bonds are issued, the Bond Resolution shall be and remain irrepealable until the Bonds and the interest accrued thereon shall have been fully paid, satisfied or discharged.

Amendment of Bond Resolution

The District may, without the consent of or notice to the Owners, adopt one or more resolutions supplemental to the Bond Resolution, which supplemental resolutions shall thereafter form a part of the Bond Resolution, for any one or more of the following purposes: (1) to cure any ambiguity, or to cure, correct or supplement any formal defect or omission or inconsistent provision contained in the Bond Resolution, to make any provision necessary or desirable due to a change in law, to make any provisions with respect to matters arising under the Bond Resolution, or to make any provisions for any other purpose if, in each case, such provisions are necessary or desirable and do not adversely affect the interests of the Registered Owners; (2) to pledge additional revenues, properties or collateral as security for the Bonds; (3) to grant or confer upon the Registrar for the benefit of the Registered Owners any additional rights, remedies, powers or authorities that may lawfully be granted to or conferred upon the Registered Owners; (4) to qualify the Bond Resolution under the Trust Indenture Act of 1939; (5) to preserve or protect the excludability from gross income for federal income tax purposes of the interest allocable to the 2010A Bonds; or (6) to maintain the status of the 2010B Bonds as qualified Build America Bonds under Section 54AA of the Tax Code.

Except for amendatory or supplemental resolutions adopted pursuant to the prior paragraph, the Owners of not less than two-thirds (2/3) in aggregate principal amount of the Bonds then Outstanding shall have the right, from time to time, to consent to and approve the adoption by the District of such resolutions amendatory or supplemental hereto as shall be deemed necessary or desirable by the District for the purpose of modifying, altering, amending, adding to, or rescinding, in any particular, any of the terms or provisions contained in the Bond Resolution; provided however, that without the consent of the Owners of all the Bonds affected thereby, nothing herein contained shall permit, or be construed as permitting: (1) a change in the terms of the maturity of any Bond, in the principal amount of any Bond or the rate of interest thereon, the dates of payment of principal and interest, or in the terms of prior redemption of any

15

Bond; (2) an impairment of the right of the Owners to institute suit for the enforcement of any payment of the principal of or interest on the Bonds when due; (3) a privilege or priority of any Bond or any interest payment over any other Bond or interest payment; or (4) a reduction in the percentage in principal amount of the Bonds the consent of whose Owners is required for any such amendatory or supplemental resolution.

If, at any time, the District shall desire to adopt an amendatory or supplemental resolution for any of the purposes of the above paragraph, the District shall cause notice of the proposed adoption of such amendatory or supplemental resolution to be given by mailing such notice by certified or registered first-class mail to the Underwriter and to each Owner at the address shown on the registration books of the Registrar, at least thirty days prior to the proposed date of adoption of any such amendatory or supplemental resolution. Such notice shall briefly set forth the nature of the proposed amendatory or supplemental resolution and shall state that copies thereof are on file at the offices of the District or some other suitable location for inspection by all Owners. If, within sixty days or such longer period as shall be prescribed by the District following the giving of such notice, the Owners of not less than the required percentage in aggregate principal amount of the Bonds then outstanding at the time of the execution of any such amendatory or supplemental resolution shall have consented to and approved the execution thereof as herein provided, no Owner shall have any right to object to any of the terms and provisions contained therein, or the operation thereof, or in any manner to question the propriety of the adoption and effectiveness thereof, or to enjoin or restrain the District from adopting the same or from taking any action pursuant to the provisions thereof.

Book-Entry Only System

The Bonds will be available only in book-entry form in the principal amount of $5,000 or any integral multiple thereof. DTC will act as the initial securities depository for the Bonds. The ownership of one fully registered Bond for each maturity in each series, as set forth on the inside cover page of this Official Statement, in the aggregate principal amount of such maturity coming due thereon, will be registered in the name of Cede & Co., as nominee for DTC. See Appendix B - Book-Entry Only System.

SO LONG AS CEDE & CO, AS NOMINEE OF DTC, IS THE REGISTERED OWNER OF THE BONDS, REFERENCES IN THIS OFFICIAL STATEMENT TO THE OWNERS WILL MEAN CEDE & CO. AND WILL NOT MEAN THE BENEFICIAL OWNERS.

None of the District, the Registrar or the Paying Agent will have any responsibility or obligation to DTC’s Direct Participants or Indirect Participants (each as defined in Appendix B), or the persons for whom they act as nominees, with respect to the payments to or the providing of notice for the Direct Participants, the Indirect Participants or the beneficial owners of the Bonds as further described in Appendix B to this Official Statement.

16

SECURITY FOR THE BONDS

General Ad Valorem Property Tax Pledge

The Bonds are general obligations of the District payable from ad valorem taxes which may be levied against all taxable property within the District without limitation of rate and in an amount sufficient to pay the Bonds when due. See “INTRODUCTION--Security,” “Limitations on Remedies Available to Owners of Bonds” below and “LEGAL MATTERS--Certain Constitutional Limitations.” The Bonds are not secured by property within the District, but rather by the District’s obligation to certify to the board of county commissioners of the County (the “Commissioners”) a rate of levy sufficient, together with other legally available revenues, to meet the debt service requirements on the Bonds. Such annual levy for debt service creates a statutory tax lien. Neither the State nor the County has any responsibility to pay the debt service on the Bonds.

The District anticipates that the major source of revenues for repayment of the Bonds will be the ad valorem taxes levied against property within the District and collected by the county treasurer (the “County Treasurer”). The District’s ability to retire the indebtedness created by the issuance of the Bonds is dependent, in part, upon the maintenance of an adequate tax base against which the District may levy and collect property tax revenues. The amount of ad valorem property taxes collected will be dependent upon the assessed valuation of property within the District and the rate of levy certified by the Board. See “LEGAL MATTERS--Certain Constitutional Limitations” and “PROPERTY TAXATION, ASSESSED VALUATION AND OVERLAPPING DEBT--Ad Valorem Property Taxes.”

The payment of property taxes does not constitute a personal obligation of the property owners within the District. Instead, these obligations are tied to the properties taxed, and if timely payment is not made, the obligations constitute a lien against the specific properties. The District will not have recourse to any assets of any property owners for the payment of property taxes. To enforce the liens, the County Treasurer has the power to cause the sale of the property that is subject to the delinquent taxes, as provided by law. However, selling property at a tax sale is a time-consuming remedy and proceeds realized from the sale, if any, may not be sufficient to cover the delinquent taxes. Because property taxes do not constitute personal obligations of the owners of taxable property in the District, in the event of a tax sale in which less than the amount of the delinquent taxes is realized, no deficiency judgment could be taken against the property owner who failed to pay taxes.

Foreclosure activity in the County has been increasing in recent years. See “ECONOMIC AND DEMOGRAPHIC INFORMATION--Foreclosure Activity.” It is not possible to predict whether foreclosure rates will continue to rise or whether any increase in foreclosures will cause significant delinquencies in property tax payments and the realization of property tax revenues by the District. Further, the country currently is in the midst of a recession; it is not possible to predict what effect the economic downturn will have on property values, foreclosures or delinquencies in property tax payments. See “PROPERTY TAXATION, ASSESSED VALUATION AND OVERLAPPING DEBT—Ad Valorem Property Tax Data.”

17

The remedies available to the owners of the Bonds upon an event of default under the Bond Resolution are in many respects dependent upon judicial actions which are often subject to discretion and delay under existing constitutional and statutory law and judicial decisions, including specifically the United States Bankruptcy Code. The various legal opinions to be delivered concurrently with delivery of the Bonds will be qualified as to enforceability of the various legal instruments by limitations imposed by bankruptcy, insolvency, reorganization, moratorium and other similar laws affecting the rights of creditors generally and by equitable principles, whether considered at law or in equity. See “Limitations on Remedies Available to Owners of Bonds” below.

Various State laws and constitutional provisions apply to the assessment and collection of ad valorem property taxes. There is no assurance that there will not be any change in, interpretation of, or addition to the applicable laws, provisions, and regulations which would have a material effect, directly or indirectly, on the affairs of the District. See “PROPERTY TAXATION, ASSESSED VALUATION AND OVERLAPPING DEBT” and “LEGAL MATTERS--Certain Constitutional Limitations.”

Pledge of Revenues; Priority

The creation, perfection, enforcement, and priority of the pledge of revenues to secure or pay the Bonds as provided in the Bond Resolution shall be governed by the Supplemental Act and the Bond Resolution. The revenues pledged for the payment of the Bonds, as received by or otherwise credited to the District, shall immediately be subject to the lien of such pledge without any physical delivery, filing, or further act. The lien of such pledge on the revenues pledged for payment of the Bonds and the obligation to perform the contractual provisions made in the Bond Resolution shall have priority over any or all other obligations and liabilities of the District, except for any general obligation indebtedness of the District currently outstanding or any general obligation indebtedness issued on a parity with the Bonds. The lien of such pledge shall be valid, binding, and enforceable as against all persons having claims of any kind in tort, contract, or otherwise against the District irrespective of whether such persons have notice of such liens.

Limitations on Remedies Available to Owners of Bonds

No Acceleration. There is no provision for acceleration of maturity of the principal of the Bonds in the event of a default in the payment of principal of or interest on the Bonds. Consequently, remedies available to the Owners of the Bonds may have to be enforced from year to year.

Limitations Generally. The enforceability of the rights and remedies of the Owners of the Bonds and the obligations incurred by the District in issuing the Bonds are subject to the federal bankruptcy code and applicable bankruptcy, insolvency, reorganization, moratorium, or similar laws relating to or affecting the enforcement of creditors’ rights generally, now or hereafter in effect; usual equity principles which may limit the specific enforcement under State law of certain remedies; the exercise by the United States of America of the powers delegated to it by the federal Constitution; and the reasonable and necessary exercise, in certain exceptional situations, of the police power inherent in the sovereignty of the State and

18

its governmental bodies in the interest of serving a significant and legitimate public purpose. Bankruptcy proceedings or the exercise of powers by the federal or State government, if initiated, could subject the Owners of the Bonds to judicial discretion and interpretation of their rights in bankruptcy or otherwise, and consequently may entail risks of delay, limitation or modification of their rights.

Limitations on Debt Service. At the Election, District voters approved the issuance of bonds in an amount not to exceed $50,000,000 with a total repayment cost not to exceed $86,850,000 and a maximum annual repayment cost not to exceed $4,363,000. The voters also approved increased ad valorem property taxes to pay debt service on such bonds, provided that the annual amount of such taxes cannot exceed $4,363,000. The District may not exceed these limitations with respect to the payment of debt service for any reason. See “LEGAL MATTERS--Certain Constitutional Limitations.”

19

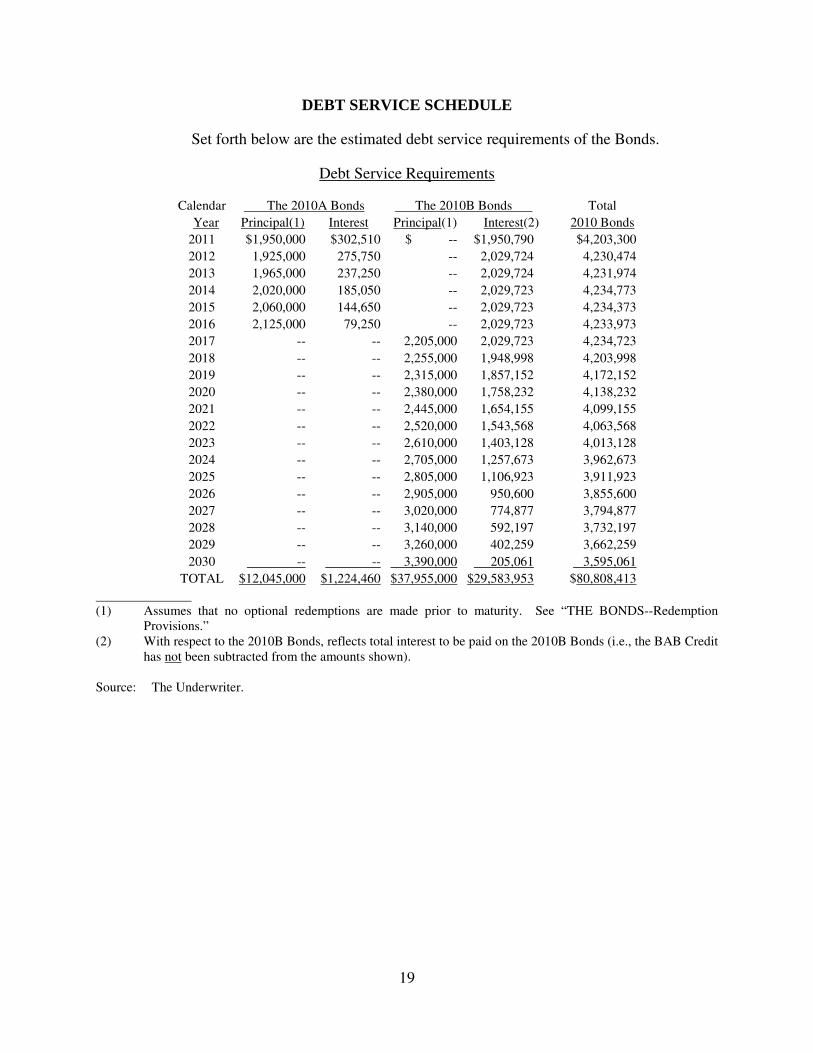

DEBT SERVICE SCHEDULE