16th annual mexican energy conference nov, 13-14 2012 · 16th annual mexican energy conference nov,...

TRANSCRIPT

16th Annual Mexican Energy

Conference Nov, 13-14 2012

Alfredo Santillan

Representative

SMBC - Mexico Representative Office

“Electric Power Supply and

Generation in Mexico”

Copyright © 2012 Sumitomo Mitsui Banking Corporation. All Rights Reserved. 1

Industry Overview:

The Mexican electricity market is the exclusive responsibility of Comisión

Federal de Electricidad (“CFE”), which is wholly-owned by the Federal

Government.

CFE is a vertically-integrated electric utility and also the largest electric utility

in Latin America.

Its budget and borrowing program is included in the Mexican Government

Budget and approved by the Mexican Congress.

CFE (BBB/BAA1/Stable) has the responsibility for the strategic development,

construction, operation and maintenance of the country’s electricity system.

In 1992, there were some modifications to the Mexican Electricity Law to

allow private investment in the industry: Mainly through Self-Supply/Co-

generation & Independent Power Producers (“IPPs”).

IPP program Allows private companies to build and operate power plants

in Mexico, but limit their sale of power to CFE under long-term contracts.

Electricity Industry

Copyright © 2012 Sumitomo Mitsui Banking Corporation. All Rights Reserved. 2

Industry Overview:

CFE accounts for nearly 77% of Mexico’s total installed capacity and

electricity production.

Total installed generation capacity in 2010 was 52.9 GW (41 GW and 11.9

GW of independent power producer capacity).

CFE operates Mexico’s national transmission grid and its sub-transmission

and distribution network covers 833,081 km.

Market Demand:

The electricity market consists of the sale of electricity to industrial,

commercial, residential, transportation and other end-users including

agricultural sector.

Demand growth in the power sector is a reflection of population expansion,

increased economic activity and changing energy intensity/efficiency.

In the next 15 years Mexican estimated consumption of electricity will

increase at an average annual rate of 3.5%.

Market Supply

Mexico’s electricty generation is dominated by natural gas, oil, hydro and

coal which make up roughly 39%, 24%, 10% and 22% of the installed

capacity, respectively.

CFE’s plans to increase its installed capacity by 37.7 GW between 2012 –

2026. This represents a 71% increase over current capacity.

The power sector in Mexico is an important element and a key factor for the

The Mexican constitution states that generation, transmission, distribution

and supply of electricity are the exclusive responsibility of the Federal

Government. By law, CFE is entrusted with the overall planning,

development and operation of the national electricity system.

There used to be another company called Luz y Fuerza Centro (“LFC),

which was in charge of planning and providing electricity to Mexico City and

surrounding areas, but was dissolved by Presidential Decree on October 11,

2009. Operations and activities formerly performed by LFC have been

undertaken by CFE since the date of the mentioned dissolution.

The exception to the above is the power generated under the independent

power producer (“IPP”) program.

Generation:

Of this capacity, as the figures below show, 46% is capacity provided by

thermoelectric plants, 23% is provided by independent generators (IPP),

22% is generated by hydroelectric plants and the remaining 9% is distributed

among coal, nuclear and others. The system’s high reliance on thermal

generation exposes it to the supply of fuels.

Electricity Industry

Copyright © 2012 Sumitomo Mitsui Banking Corporation. All Rights Reserved. 3

Market Supply/Generation

Mexico’s electricity generation is dominated by natural gas, oil, hydro and

coal which make up roughly 39%, 24%, 10% and 22% of the installed

capacity, respectively.

Of this capacity, as the figures below show, 46% is capacity provided by

thermoelectric plants, 23% is provided by IPPs, 22% is generated by

hydroelectric plants and the remaining 9% is distributed among coal, nuclear

and others. The system’s high reliance on thermal generation exposes

it to the supply of fuels.

Installed capacity by type (aug-2010)

Hydro, 22%

Nuclear, 3% Eolic, 0%

Geothermal,

2%

Thermal,

46%

Coal, 5%

IPP, 23%

Electricity Industry

Copyright © 2012 Sumitomo Mitsui Banking Corporation. All Rights Reserved. 4

4

Overview of the Mexican Wind Power Market (Continued)

Independent Power Producers (IPPs):

With the opening of Norte Durango with a Net Capacity of 450 MW, the IPP’s generation capacity increased to 11.9GW

PRIVATE & CONFIDENTIAL

Electricity Industry

Copyright © 2012 Sumitomo Mitsui Banking Corporation. All Rights Reserved. 5

Main regulatory entities in the Mexican Energy Industry:

Energy Regulatory Commission (CRE): Is in charge of elaborating

clear rules for independent power production, sales and reserve

purchase contracts between private generators and the public utilities,

wheeling charges, and overseeing the power generation and natural gas

concessions being awarded.

Ministry of Energy (SENER): In charge of conducting energy policies

with the aim of guaranteeing a competitive, efficient, high-quality,

economically viable and environmentally sustainable energy supply.

Federal Electricity Commission (CFE): Is a decentralized, vertically

integrated electric energy service company wholly owned by the Mexican

federal government. CFE is in charge of generation, transmission,

transformation, distribution and commercialization of electricity for all of

Mexico.

Main Players (Independent Power Producers)

Iberdrola

4,239 MW

Mitsui

2,510 MW

Gas Natural

1,941 MW

Mitsubishi

990 MW

Intergen

754 MW

AES

484 MW

Note: The following Japanese companies are minority partners in some power plants: Kyushu, Chubu, Tokyo Gas and Tohoku.

Main Players

Copyright © 2012 Sumitomo Mitsui Banking Corporation. All Rights Reserved. 6

Main Players

EPC Contract participants (last 5 years)

EPC Contractor Project Fuel

KepCo / Samsung

C&T / Techint

•Norte II (433MW) •Gas Combined Cycle

Iberinco •Phase I - Salamanca

(430MW)

•Cogeneration

Abengoa / Abener •Nuevo Pemex (300MW) •Cogeneration

Iberdrola •Laguna Verde (1,365MW) •Nuclear

Mitsubishi •Carboeléctrica del Pacífico

(651MW)

•Coal

ICA •La Yesca (750MW) •Hydro

Cobra •Oaxaca I (102MW) •Eolic

Acciona •Oaxaca II, III and IV (102

MW each)

•Eolic

Mitsui / Samsung /

Kogas / TOA

•Manzanillo LNG •LNG

Copyright © 2012 Sumitomo Mitsui Banking Corporation. All Rights Reserved. 7

In the next 15 years (2012-2026), CFE plans to increase its installed

capacity by 37.7 GW.

This represents a % = 71% increase over current capacity.

Capital investment of MXP$ 1,264 millions (US$ 97.2 bn).

The private sector represents a key player in the future investments for

the Sector IPPs & OPF.

Investments/Outlook

Transmission

18%

Distribution

23%

Generation

58%

Maintenance

1%

OPF

30%

CFE's Budget

40%

IPP

30%

Copyright © 2012 Sumitomo Mitsui Banking Corporation. All Rights Reserved. 8

Additional Capacity Requirements 2012 – 2019 period:

Investments/Outlook

Copyright © 2012 Sumitomo Mitsui Banking Corporation. All Rights Reserved. 9

In order to achieve the projected additional capacity, CFE is promoting an

integrated approach.

Including the development of a new natural gas supply system. There is a

significant focus on natural gas due to:

Increasing price differentials between natural gas and fuel oil.

Expected supply restrictions of fuel oil in the mid and long terms, planned

by SENER.

Pipeline system in Mexico

SENER together with Pemex, CFE and CRE have launched a strategy to

improve the gas pipeline in Mexico.

Multiple large-scale projects to expand Mexico’s gas pipeline network have

been announced, most to be developed by private investors.

Over US$10 Bn in new investment in the gas pipeline system is anticipated

over the next 5-10 years.

Expansion Project / Supply Challenges

Copyright © 2012 Sumitomo Mitsui Banking Corporation. All Rights Reserved. 10

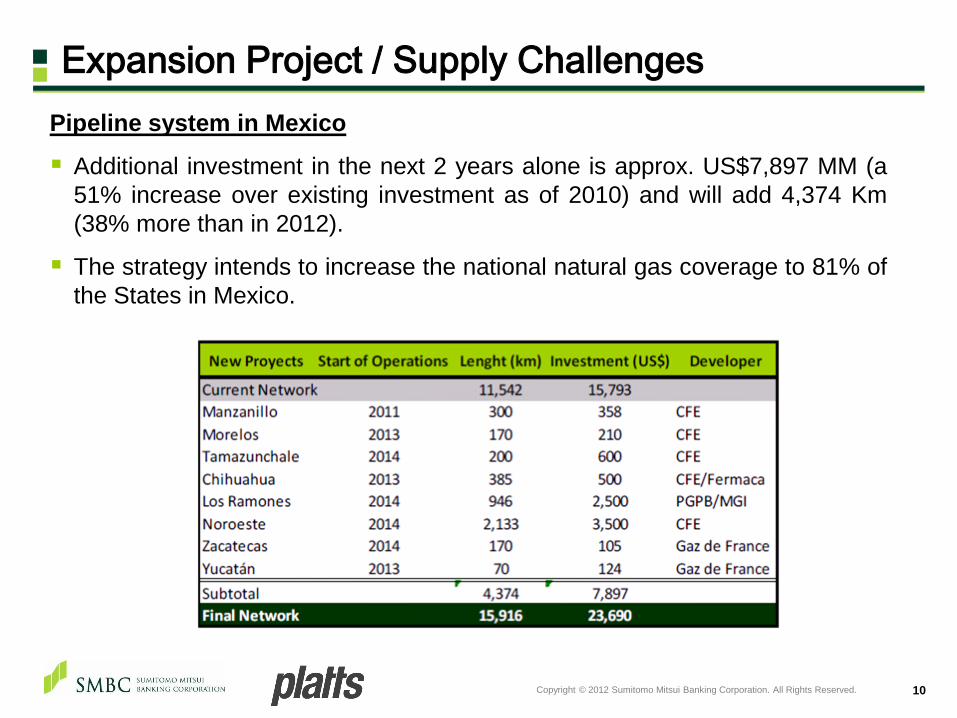

Pipeline system in Mexico

Additional investment in the next 2 years alone is approx. US$7,897 MM (a

51% increase over existing investment as of 2010) and will add 4,374 Km

(38% more than in 2012).

The strategy intends to increase the national natural gas coverage to 81% of

the States in Mexico.

Expansion Project / Supply Challenges

Copyright © 2012 Sumitomo Mitsui Banking Corporation. All Rights Reserved. 11

Mexican Gas Market

The shale gas revolution in the U.S., based on the exploitation of hydro-

fracking and horizontal drilling, has led to a significant increase in the overall

supply of gas production and reserves in the US and Canada.

The U.S. is expected to become a significant net exporter of natural gas.

Mexico is a traditional market for U.S. gas.

The dramatic increase in production and reserves in the US has resulted in a

sharp downward movement in natural gas prices for the North America

region.

The price differential between gas delivered at Reynosa, on the US-Mexican

border, with a common European gas index, Italy PSV, now stands at

US$9.25.

The case for increasing gas imports from the U.S. has become very strong.

Expansion Project / Supply Challenges

Copyright © 2012 Sumitomo Mitsui Banking Corporation. All Rights Reserved. 12

Independent Power Producers (IPPs). Public Works Contracts (OPF)

• Scheme utilized in generation projects,

excluding hydroelectric plants.

• Normally used in transmission lines,

substations, hydroelectric plants, re-

vamping, etc.

• Projects awarded through international

tenders Most competitive KW/h.

• Projects awarded through international

tenders Most competitive turn-key

price.

• Companies are responsible for the

financing during construction.

• Companies are responsible for the

financing during construction.

• CFE signs a power purchase

agreement (25 years) At COD.

• “Turnkey” projects allow CFE to

operate the plants at COD.

• The company remains as the owner of

the assets and operates the facilities

Acquisition option by CFE.

• Upon completion, assets (and all

operational risks) are transferred to

CFE Companies get the total

contract value paid.

Main Schemes for Private Investment

Copyright © 2012 Sumitomo Mitsui Banking Corporation. All Rights Reserved. 13

How to Structure a Bankable Project

Equipment

& Technology

Providers

Offtakers

and/or

Marketers

Utility

Providers

Feedstock

Supplier

(i.e. PEMEX)

EPC

Contractor

Project

Key Elements for a Successful Financing

Experienced EPC Contractor

Proven Technology

Lump Sum Turn Key approach is

preferred

Adequate liquidated damages

Clear strategy to sell the Project’s output

(offtakers and marketers)

Reliable suppliers

Experienced operator

Environmental and social risks properly

mitigated – Equator Principles Construction phase Operating phase

Thank You!

Alfredo Santillan

Representative

SMBC - Mexico Representative Office

Q&A