18 may 2018 - irishfunds-secure.s3.amazonaws.com · irishfunds.ie objectives •develop an irish...

TRANSCRIPT

2

irishfunds.ie

18 May 2018

Irish Funds Distribution Workshop

irishfunds.ie

Kindly hosted by:

irishfunds.ie

Username: Guest

Password: mathesonwifi

Wi-Fi Internet Access

www.slido.com #IFDist18

Sli.do Audience Interaction

irishfunds.ie

Tara Doyle, Matheson

Welcome Address

irishfunds.ie

Len Sutton, JP Morgan

Introduction

irishfunds.ie

Distribution Steering Committee

• Len Sutton - JP Morgan (Global) - Chairperson

• Audrey Behan - InterTrust Group (PRIIPS)

• Chris Christian - Dechert (USA)

• Liam Collins - Matheson (Latin America)

• Vincent Coyne - William Fry (UK)

• Jim Firn – Consultant (Global)

• Kieran Fox - Irish Funds (Global)

• Killian Lonergan - BBH (Switzerland)

• Conor Owens - Mediolanum (Europe)

• Tom Ryan - Blackrock (Asia)

• Tom McGrath - Blackrock (IF Council)

irishfunds.ie

Objectives

• Develop an Irish Funds strategy for local markets in coordination with the Marketing

Steering Group

• Assist in developing the IF profile and network in local markets by attending events,

inviting contacts to local Irish Funds events and profiling Irish Funds when interacting

with industry stakeholders

• Gather local market and distribution intelligence for Irish Funds and prepare distribution

information/ marketing material

• Identify and advise on distribution challenges and opportunities in the local markets

• Work closely with the Events Group to assist in the preparation and planning for Irish

Funds events in the local markets

• Arrange to meet with local distributors when attending overseas events

Moderator:

Panellists:

irishfunds.ie

Panel Discussion: MiFID II &

PRIIPs

Conor Clune, BBH

Manuel Brieske, State Street

Chuck Bohner, SSGA

Marlyn Cooney, Pinsent Masons

Darragh Murphy, McCann Fitzgerald

irishfunds.ie

Mark McFee, MacKay Williams

Update Session: Taking the

Funds Industry’s Temperature

irishfunds.ie

2018 – Hangover or keep partying?

Source: Broadridge FundFile data at March 2018, excluding money market funds and funds of funds.

Cross-border flows data from Broadridge Data Digest 2018, excluding money market funds, funds of funds and ETFs.

0

100

200

300

400

500

600

700

800

2017 YTD Q1 2018

Net flows – All Europe (€bn)

Equity Bond Mixed Assets Other0 20 40 60 80

Austria

Sweden

Neth

Bel

France

UK

Germany

Switz

Spain

Italy

Cross-border flows by market, 2017 (€bn)

irishfunds.ie

2018 – Expectations

Positive estimate: €314bn

Negative estimate: €17bn

Assumptions for positive scenario include:

▷ Contracting flows into fixed income funds:

€75bn – a quarter of 2017 volumes;

▷ Marginally lower volumes for mixed asset

and equity: ~ €100bn each.

Negative scenario includes:

▷ Equity redemptions of €70bn;

▷ Severe contraction in sales of all other

sectors: <€50bn.

Source: MackayWilliams analysis based on Broadridge FundFile data, excluding money market funds and funds of funds.

irishfunds.ie

Secular product shifts: Out of equity

-200

0

200

400

600

800

1,000

Jan

Ap

r

Jul

Oct

Jan

Ap

r

Jul

Oct

Jan

Ap

r

Jul

Oct

Jan

Ap

r

Jul

Oct

Jan

Ap

r

Jul

Oct

2003 2004 2005 2006 2007

Bond Equity Mixed

Cumulative net sales: 2003 - 2007 (€bn)

Source: MackayWilliams analysis based on Broadridge FundFile data – data include active and passive funds.

Cumulative net sales: 2013 - Q1 2018 (€bn)

-200

0

200

400

600

800

1,000

Jan

Ap

r

Jul

Oct

Jan

Ap

r

Jul

Oct

Jan

Ap

r

Jul

Oct

Jan

Ap

r

Jul

Oct

Jan

Ap

r

Jul

Oct

Jan

2013 2014 2015 2016 2017 2018

irishfunds.ie

Demand drivers

Rank Sector Net sales Assets

1 Asset Allocation 13,358 341,349

2 Equities Global 11,828 645,372

3 Mixed Assets Income 8,545 159,702

4Bonds Emerging

Markets8,079 165,137

5Fund of Funds

Balanced7,690 242,015

Rank Sector Net sales Assets

1Bonds USD Corp.

High Yield-4,988 56,081

2Bonds EUR Corp.

Inv. Grade-4,214 136,988

3Bonds Global High

Yield-3,607 111,725

4 Equities UK Income -3,357 93,224

5 Bonds Target Maturity -2,495 70,609

Top/bottom five sectors by net sales, Q1 2018 (€m)1

Sector April ‘18

Alternative 17%

European equities 17%

Mixed/Flexible 15%

Emerging markets 12%

Japan equity 12%

Global bonds -7%

Bonds North America -7%

Equity North America -9%

Bond High Yield -12%

European bonds -14%

Top/bottom five sectors by net allocation

intentions2

Source 1: Broadridge FundFile data, excluding money market funds and funds of funds.

Source 2: MackayWilliams’ net investment allocation scores based on 81 interviews with third-party fund selectors in April 2018.

irishfunds.ie

Selector themes

1. Revenues are under

pressure

2. Time is under pressure

3. Risk-averse client base

and a low-yield

environment

Shrinking buy lists

Using more passive funds

Funds of funds/sub-advisory

Demanding greater transparency

Service/value-for-money proposition

Share-class options with flexible access

Solutions-type funds

irishfunds.ie

Passive use is still rising

16%17% 18%

20% 20%

22%

0%

5%

10%

15%

20%

25%

2012 2013 2014 2015 2016 2017

Average passive use % – Pan Europe

24%

29%

24%

16%

40%

19%

23%

14%

20%

22%

0% 10% 20% 30% 40% 50%

UK

Switzerland

Sweden

Spain

Netherlands

Italy

Germany

France

BeLux

Austria

Average use of passive funds by market

Source: MackayWilliams, based on 937 interviews with third-party fund selectors in 2017.

irishfunds.ie

Winner takes all?

Source: Broadridge FundFile data at December 2017, excluding money market funds and funds of funds. Val point calculation at

each year end.

29%24%

51%

78%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Top 10 groups as share of AUM

Passive

Active

irishfunds.ie

Little evidence size matters in active, yet

Source: Broadridge FundFile data at December 2017, excluding money market funds and funds of funds. Active funds only.

Top 20 groups Outside top 20 & 30+

funds

Fewer than 30 funds

AUM (end 16) €2.5tn €2.7tn €1.2tn

Flows 2017 €160bn €253bn €87bn

Flows/Assets 6% 9% 7%

irishfunds.ie

Stand out

“They should be more prepared to

stand out from the crowd. For

example, I have just been on a trip to

see US fund managers and barely

did a meeting start without the

clichéd introductory claim of ‘We're

different!’ Most of what you then

heard, however, was anything but

different!”

UK, Fund of Funds Manager

irishfunds.ie

Survival tactics

1. Be an elephant or…

2. Differentiate:

• Product innovation

• Service

• Brand

irishfunds.ie

Innovation demands

Top 10 innovation requests from fund selectors

Source: Product Innovation Perspectives, MackayWilliams. Data from ~1000 selector interviews over the two six-month periods.

Oct ‘16 – Mar ‘17 Oct ‘17 – Mar ‘18

1 Alternatives / Uncorrelated Alternatives / Uncorrelated

2 Transparency / Simplicity ESG / SRI

3 Theme Niche

4 ESG / SRI Theme

5 Risk control / Vol management Transparency / Simplicity

6 Niche True active

7 Absolute return Absolute return

8 Flexible Flexible

9 Passive Multi asset

10 Conservative fixed income / cash

alternative

Smart beta / factor / AI

irishfunds.ie

Into SRI

Definitional complexity makes measurement

difficult although EU currently promising

guidance.

Our measure – based on funds explicitly

marketed as responsible investments via stated

SRI terminology in fund names.

Demand drivers coming from end-consumer, but

so far fail to translate into noticeable sales uplift.

‘Green washing’ likely to be viewed negatively.

Long-term, though, EU Commission favour

implementing a regulatory kicker.

Source: MackayWilliams analysis of Broadridge FundFile data at February 2018. Data exclude money market funds and funds of

funds.

SRI/ESG Other

AUM (€bn) 170 8,529

3yr AUM Growth 92% 31%

3yr Net sales (€bn) 63 1,132

# Funds 807 27,643

Ave fund size (€m) 211 309

Passive share of AUM 21% 16%

Top 10 funds as % AUM 14% 3%

SRI/ESG – Key fund industry metrics

irishfunds.ie

Andreas Pfunder, instiHub Analytics

Update Session: Sub-advisory

trends overview

irishfunds.ie

Andreas Pfunder, Founder & CEO

European sub-advisory

The hidden dimension of asset

gathering

21/05/2018 Content inc lud ing propr ie tary data i s the proper ty o f inst iHub Analyt i cs L imi ted. Reproduc t ion sub jec t to perm iss ion.

irishfunds.ie

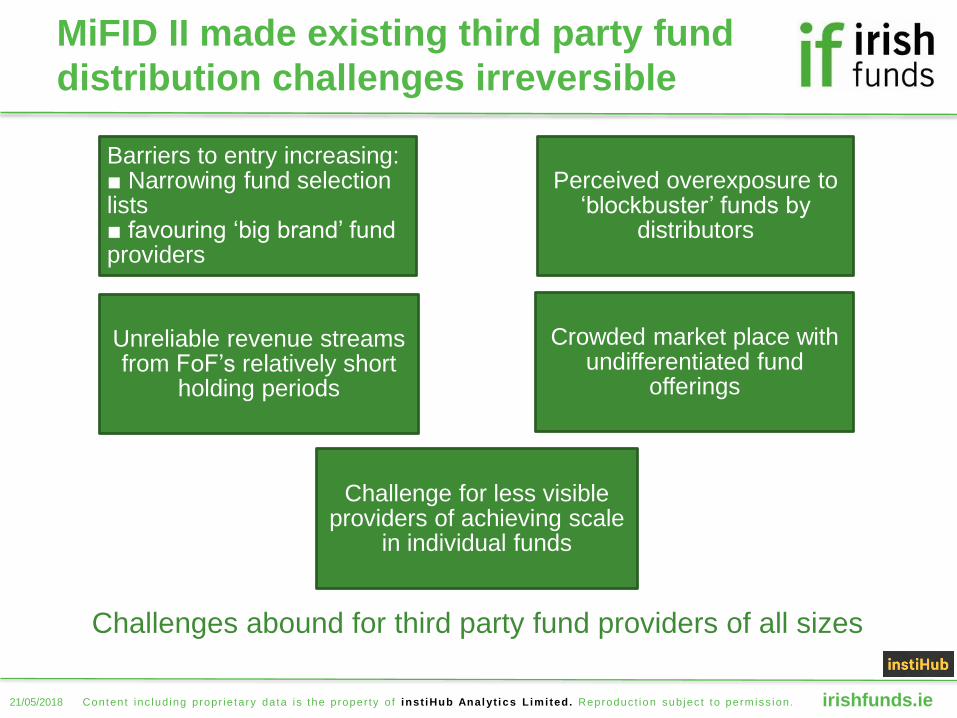

MiFID II made existing third party fund

distribution challenges irreversible

Challenges abound for third party fund providers of all sizes

21/05/2018 Content inc lud ing propr ie tary data i s the proper ty o f inst iHub Analyt i cs L imi ted. Reproduc t ion sub jec t to perm iss ion.

Barriers to entry increasing:■ Narrowing fund selection lists■ favouring ‘big brand’ fund providers

Perceived overexposure to ‘blockbuster’ funds by

distributors

Unreliable revenue streams from FoF’s relatively short

holding periods

Crowded market place with undifferentiated fund

offerings

Challenge for less visible providers of achieving scale

in individual funds

irishfunds.ie

Distributors’ reaction and mindset drive

sub-advisory growth

Across Europe, distributors are seeking

Higher margins to offset increased costs of distribution burden under MiFID II

Greater control over the products they sell, achieved through in-house funds

Lower cost, higher performance = ‘better value’ solutions for investors

Differentiation through customised or exclusive solutions

Risk diversification away from reliance on blockbuster third party funds

Emergence of a ‘private equity’ mindset amongst distributors

“My business is worth more as an asset manager than as a distributor”

The sub-advisory model offers distributors an optimal solution,

creating valuable growth opportunities for sub-advisers

21/05/2018 Content inc lud ing propr ie tary data i s the proper ty o f inst iHub Analyt i cs L imi ted. Reproduc t ion sub jec t to perm iss ion.

irishfunds.ie

instiHub’s definition of sub-advisory

The sub-advisory industry comprises

Any fund

whose sponsor / initiator

formally delegates

investment management / advisory responsibilities

to a third party

Industry coverage within above definition on which the following data

content is based: > 90% (estimate)

21/05/2018 Content inc lud ing propr ie tary data i s the proper ty o f inst iHub Analyt i cs L imi ted. Reproduc t ion sub jec t to perm iss ion.

irishfunds.ie

Key statistics of the EMEA sub-

advisory industry in Q1 2018

€526bn AUM on 31st Mar 2018 with YoY annual growth of 10%

Wide spread of geographies to grow sub-advised business opportunities

15 markets where selection decisions are made

132 sponsors (buyers/grantors of sub-advisory mandates)

Potential exists among a range of channel segments

Top 5 sponsors own 37% AUM

Top 35 (28%) own 83% of AUM (29 have > €5bn AUM each)

527 sub-advisers in 30 countries manage over 2,220 mandates

Specialist boutiques manage or advise on 37% of AUM

Average holding period of 3 years and 9 months

varies by …

Channel & country

Multi-manager vs single manager implementation

21/05/2018 Content inc lud ing propr ie tary data i s the proper ty o f inst iHub Analyt i cs L imi ted. Reproduc t ion sub jec t to perm iss ion.

Source: instiHub, iPsa (public sub-advisory insights), 31/03/2018.

irishfunds.ie

Latest trends: markets

Largest markets by AUM (€bn)

21/05/2018 Content inc lud ing propr ie tary data i s the proper ty o f inst iHub Analyt i cs L imi ted. Reproduc t ion sub jec t to perm iss ion.

Source: instiHub, iPsa (public sub-advisory insights), 31/03/2018.

Country Uplift Jan-Dec 2017

Italy 23%

United Kingdom 15%

Ireland 14%

France 12%

Europe Average 10%

*Annualised growth rate

Country Uplift Dec 2017-Mar 2018

Switzerland 13%

United Kingdom 12%

Italy 7%

France 2%

Europe Average 1%

*Annualised growth rate

Fastest growing markets – Q1 2018 vs 2017

Clear rankings for market size

Top 3 likely to retain rankings as smaller

markets show differential expansion

Four hot sponsor countries

2017 - Italy, UK, Ireland, France

2018 – Switzerland, UK, Italy, France

Seasonal flows volatile – true pattern

will emerge as year progresses

irishfunds.ie

YoY trends: investment strategies

21/05/2018 Content inc lud ing propr ie tary data i s the proper ty o f inst iHub Analyt i cs L imi ted. Reproduc t ion sub jec t to perm iss ion.

Source: instiHub, iPsa (public sub-advisory insights), 31/03/2018.

0%

2%

4%

6%

8%

10%

12%

14%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Equity Fixed Income Multi Asset Alternative

% G

row

th

20

17

AU

M G

row

th (€

m)

Investment sector

Strongest growth from FI & EquitiesBreakdown of AUM by sector

Equity49%

Fixed Income29%

Multi Asset18%

Alternative3%

Money Market1%

Equity remains largest asset class (49% AUM) but with below average growth

(7%)

Fixed income (29%) grows most, i.e. 13% / €17.4bn

Multi asset (18%) is also increasing above average - 12% / €10.3bn

Alternatives (illiquid) are small – appeal more to institutional sponsors

irishfunds.ie

Expected growth dynamics

21/05/2018 Content inc lud ing propr ie tary data i s the proper ty o f inst iHub Analyt i cs L imi ted. Reproduc t ion sub jec t to perm iss ion.

CH, IRL, IT, UK - New sponsors emerging, e.g. bank distributors, wealth managers

CH, DE, ES, FR, IRL, IT - Sponsors favouring sub-advised structures to improve margins & deliver better value to investors

CH, IT, Nordics - Sponsors with in-house or institutional clients seeking to scale up through broader, external distribution

CH, UK, IT, DE, FR - Large wealth managers, private banks with discretionary mandates transitioning to sub-advisory for greater operational efficiencies and lower cost-to-investors

Individual territories responding in different ways, driven by existing

distribution landscape and needs for solutions

Net effect creates sizeable growth opportunities for sub-advisers of all kinds

irishfunds.ie

How fast will growth be impactful?

instiHub’s ongoing engagement with both sponsors and sub-

advisers provides crucial intelligence on likely milestones

21/05/2018 Content inc lud ing propr ie tary data i s the proper ty o f inst iHub Analyt i cs L imi ted. Reproduc t ion sub jec t to perm iss ion.

Starting in H1 2018 until 2020 - Wave of new sponsor entrants from all channels

Starting in H1 2018 until 2019 - Expansion of exclusive product partnerships

Wealth managers & private banks with sub-advised fund platforms scale up to address Discretionary Portfolio Management (DPM) challenges

Existing sponsors with captive reach scale up and broaden 3rd party distribution

First wave of FoF managers setting up sub-advised structures

Where are you positioned in this timeline?

H2 2018 – H2 2019

From H2 2018

From H1 2019

irishfunds.ie

instiHub growth forecast:

€1tn industry by 2022

10-year AUM growth expectation to €1.5tn with 10.5% CAGR

402

428

458

103

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

-

200

400

600

800

1,000

1,200

1,400

1,600

2017 Act 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E 2026E 2027E

Asset Manager (incl. consultants) Wealth Manager Bank Distributor

Private Bank Insurance (Unit-Linked) Pension

Growth p.a. (%, rhs)

Anticipating 18% uplift over 12m with €1tn AUM reached by 2022

Thereafter, reversion back to recent levels (10%) or just below (8%) if capital return

remain low

21/05/2018 Content inc lud ing propr ie tary data i s the proper ty o f inst iHub Analyt i cs L imi ted. Reproduc t ion sub jec t to perm iss ion.

Source: instiHub, iPsa (public sub-advisory insights), 31/03/2018.

irishfunds.ie

Early adopter ‘winners’ in sub-

advisory have clear vision

21/05/2018 Content inc lud ing propr ie tary data i s the proper ty o f inst iHub Analyt i cs L imi ted. Reproduc t ion sub jec t to perm iss ion.

‘Expand the pie’ versus ‘zero sum’ game mindset

No fear of cannibalising existing book of business

Confidently manage ‘renegotiation’ of legacy assets pricing

Seek new clients in new sectors and markets

See sub-advisory as ‘low friction/ high profit business’

Use contextual business vocabulary

Provide ‘investment strategies’ – not products

Promote brand through high-value ‘content’ – not high cost communications

Initial traction generated, now building momentum

Putting ‘blue water’ between themselves and rival sub-advisers

Intuitive grasp of revenue ‘bounce’ from growing share in an expanding market

Not addicted to high bps (fund distribution) business

Range of pricing strategies in place across multiple client segments & channels

Possess process expertise to engineer business operations for pricing point

irishfunds.ie

instiHub has developed a unique data

analytics tool

21/05/2018 Content inc lud ing propr ie tary data i s the proper ty o f inst iHub Analyt i cs L imi ted. Reproduc t ion sub jec t to perm iss ion.

Rank individual sponsors

Scope size &growth of individual markets

Part 1: ‘Top down’Analyse appeal of addressable opportunities

Channels, e.g.

Wealth Manager

Private Bank

Investment strategies

Asset Managers/

Consultants

and

irishfunds.ie

Build prospect list by identifying specific opportunities

New product ideas for

presentation to sponsors

Replacement switches

from incumbent

peers

Multi manager blending

opportunities

… that delivers the identification of

potential sales opportunities

21/05/2018 Content inc lud ing propr ie tary data i s the proper ty o f inst iHub Analyt i cs L imi ted. Reproduc t ion sub jec t to perm iss ion.

Fully transparent

analytics tool built

from mandate

components

Profile individual

sponsors to match

engagement model

and probability of

success

irishfunds.ie

Continuing the journey …

If you are any of the following :

An existing advocate for sub-advisory

A C-suite executive excited by the potential of this channel

An inquisitive Head of Business ‘spooling up’ for growth in sub-advisory

- then please contact me directly:

for a confidential discussion

OR

to arrange a demonstration of instiHub iPsa - the only EMEA-transparent,

actionable, sub-advisory data analytics tool

Andreas Pfunder

Mobile: +44 7500 060 171

www.instihub.com

21/05/2018 Content inc lud ing propr ie tary data i s the proper ty o f inst iHub Analyt i cs L imi ted. Reproduc t ion sub jec t to perm iss ion.

Disclaimer: The material contained in this document is for marketing, general information and reference purposes only

and is not intended to provide legal, tax, accounting, investment, financial or other professional advice on any matter,

and is not to be used as such. Further, this document is not intended to be, and should not be taken as, a definitive

statement of either industry views or operational practice.

The contents of this document may not be comprehensive or up-to-date, and neither Irish Funds, nor any of its member

firms, shall be responsible for updating any information contained within this document.

irishfunds.ie

Moderator:

Panellists:

irishfunds.ie

Panel Discussion- Guide to setting

up/distributing from Ireland

Conor Owens, Mediolanum

Conor MacGuinness, DMS

Kieran Fox, Irish Funds

Sarah Murphy, PwC

Marion Mellett, BlackRock

irishfunds.ie

Net Sales into Irish Funds from UK

investors

irishfunds.ie

Net Sales into Irish Funds from UK

investors

irishfunds.ie

Liam Collins, Matheson

Update Session – Opportunites

for Irish Funds Distributing in

Latin America

irishfunds.ie

Introduction

• Post 2008 – investors move from unregulated to

regulated product

• Local regulatory changes

• Managers seeking increased regional and sector

diversification

• Underperforming economy

irishfunds.ie

Expected AUM growth in Latin America

irishfunds.ie

Mexico

• New Investment Regulations – January 2018

• AFOREs – investment in mutual funds

• Exposure limited to 20%

• US$160 billion to invest

irishfunds.ie

Colombia

• Decree 1756 of 2017 – October 2017

• Distribution of foreign funds in Colombia

• Inter-regulator agreement required

irishfunds.ie

Chile

• Over 200 Irish funds registered for sale

• AFPs – US$210 billion to invest

• New Rules in November 2017 / April 2018

• Prohibition on investment in hedge funds

• Opening to alternative asset classes – private equity,

private debt, real estate

irishfunds.ie

Brazil

• CVM Resolution 555 - relaxes rules on foreign

investment

• Facilitates investment in UCITS

• Qualified or Professional investor funds – investment

without limit in foreign investment funds

• Invested vehicles must be subject to extensive

regulation and supervision by recognised foreign

authority

• Retail Funds – Increase from 10% to 20% in

investment in foreign assets

irishfunds.ie

Christopher D. Christian

Dechert LLP

Janice Y. Barnwell

DTCC

Accessing the US Non-Resident

Alien Customer Distribution

Channel with Irish Funds

irishfunds.ie

Introduction: General Structural

Overview

Class A (USD)

Retail (Load)

Class C (USD)

Finder Fee

Retail

Class I (USD)

Institutional

Class X (USD)

Separate

Account

Class F (USD)

Fee-based

Retail

Independent

Director

Independent

DirectorDirectorDirectorDirector

Investment Manager

Irish Fund Administrator

$ $$

$

Class N (USD)

Clean

$

Sub-Fund

2

Sub-Fund

3

Sub-Fund

4Sub-Fund

5

Sub-Fund

6

Sub-Fund

7

Sub-Fund

8Sub-Fund

9Sub-Fund

10

Sub-Fund

1

Board of Directors

UCITS ICAV Umbrella Fund

$

Service

s

Service

s

$

U.S. Sub-Distributor (e.g., Merrill

Lynch)

U.S. Distributor

$Service

s

Service

s$

Irish DepositaryService

s

$

$

irishfunds.ie

What is the Opportunity?

• Non-Resident Customer (NRC) Market

o Continues to grow in size as economies in

Latin America grow and investors look for safe

places for brokerage

o NSCC and wholesale coverage required

o U.S. Financial Intermediaries

- U.S. Broker-Dealers / Wire-House Channel

- U.S. Wealth Management / Financial Advisers

- Clearing Platforms for U.S. Advisers (e.g., Pershing)

- New York, Miami, Houston, San Diego Major Coverage

Markets

irishfunds.ie

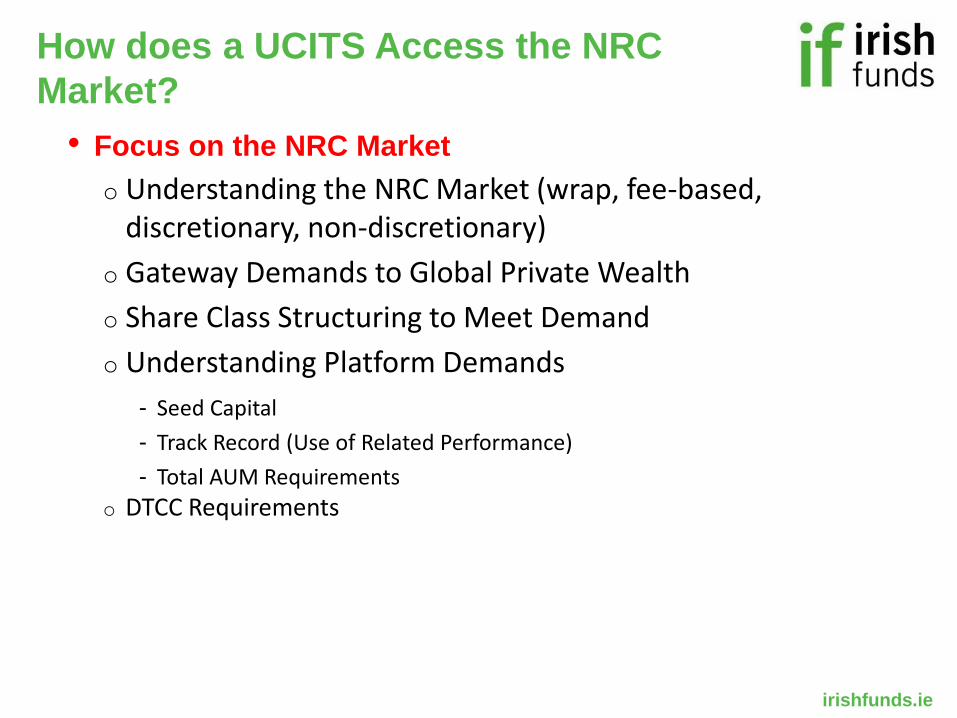

How does a UCITS Access the NRC

Market?

• Focus on the NRC Market

o Understanding the NRC Market (wrap, fee-based, discretionary, non-discretionary)

o Gateway Demands to Global Private Wealth

o Share Class Structuring to Meet Demand

o Understanding Platform Demands

- Seed Capital

- Track Record (Use of Related Performance)

- Total AUM Requirements

o DTCC Requirements

irishfunds.ie

DTCC REQUIREMENTS

o NSCC* Fund Membership

- Connectivity

- Transfer Agent

- Settling Bank

*NSCC is a subsidiary of DTCC

irishfunds.ie

Kieran Fox, Irish Funds

Closing Address

irishfunds.ie

Lunch kindly sponsored by: