18/05/10 securitisation in renewable energy: hercules or hydra jason langley beng aca amimeche a...

TRANSCRIPT

18/05/10

Securitisation in Renewable Energy: Hercules or Hydra

Jason Langley BEng ACA AMIMechE

A Presentation for

The London Accord Spring Conference – Structuring Cleantech Investment

2

Renewable Energy European Subsidies – Predictable Income

Debt, the most senior & lowest risk ownership of a renewable energy plant should be suitable for institutional investors (Pension funds and Insurance companies)

One reason for this is the subsidy systems in place: Feed in Tariff ROC system or similar

These systems give renewable energy assets a predictable yearly income stream for over a decade (especially the Feed in Tariff).

Mature technologies (wind & solar) are quite simple and together with predictable income produce a low risk real asset.

3

Renewable Energy Assets have a Suitable Cost Profile for Debt Finance

Renewable Energy

Nuclear Power

Natural Gas (Thermal Power)

Lifetime cost profile illustrations for 3 types of power plants

Time

Cost High upfront cost Very low variable cost (maintenance only)

High upfront cost Low variable cost (fuel & maintenance) Unknown final cost

Low upfront cost High variable Cost (fuel & maintenance) Fuel price inflation assumed in chart

Time

Time

Cost

Cost

Wind is free

Fuel is not free Risk of cost inflation

?

This combination of predictable income and low variable costs means significant levels of debt can be used to finance the high upfront costs of the renewable energy plant

4

Renewable Energy Project Debt Profile and Plant Value Over Time

Developers equity

Time 15 yearsLoa

n to

Val

ue

(£ o

r €

) of

Ren

ewab

le E

nerg

y A

sset

Time in years

Proof of asset 1 year

Banks project development finance

Institutional investors Long term debt profile matches long term liabilities of Institutional Investors

Bui

ld O

ut

Pla

nnin

g

War

ehou

se

Long term stable period of ownership

Sec

uri

tis

atio

n

Banks capital free for new project lending

However one project is too small to create a liquid bond suitable for fixed income institutional investors

5

The Housing Finance Corporation (THFC) – An Old and Stable Model

Equity

Tot

al V

alue

of a

sset

sAggregated loans to

Housing Associations secured by property

Incr

easi

ng S

enio

rity

Bonds to

market

This Simple Aggregation Structure can be Replicated for Renewable Energy Debt

Debt assets

in

Alignment of interestsAll bonds are the same

seniority

Vertical structureof notes

Bonds tranches

equal

Term bonds of different maturities sold into the bond market

Aggregation will allow large bond issuances that are listed on global benchmarks and are therefore liquid enough for Fixed Income Investors

6

Credit Ratings Inflation – The Perception of AAA

Premier League

Championship

League One

League Two

Aggregateddebt assets

To

tal V

alue

AAA

A

SuperSenior

Securitised debt trances League names changed

to make the lower leagues more attractive

TranchesCreated

Debt Assets

In

AA

If the underlying assets are partially devalued the AAA is put underwater quite quickly by the presence of the Super Senior.

Key principle should be AAA always means most senior

7

Untangling the Hydra – If things go wrong resolving issues is hampered by conflicting interests of note holders

D

C

EA

A

Incr

easi

ng S

enio

rity

B

Impa

ired

Val

ue o

f A

sset

s

Investors A to E invest in notes

of different seniority

Underlying debt assets impaired

Investor A is conflicted as it has taken a position in Junior and

Senior notes

The most senior note holders may want to close the structure and sell

the assets

The most junior notes want to hold the assets until maturity in case

values recover

In any restructuring negotiation there are many lawyers with conflicting briefs.

Very significant time and legal expense to restructure the debt

8

Simple aggregation structure would work for a Green Investment Bank.

The Housing Finance Corporation (THFC) creates a secondary market for debt. This increases supply of money available for new lending.

Freddie Mac is the same simple structure as THFC and demonstrates the importance of robust rules for the input debt assets.

Equity

Tot

al V

alue

of a

sset

s

1. Pass through bonds2. Bullet and Call bonds of

various maturities• Large bond issuances

listed on Fixed Income Benchmarks

Aggregateddebt assets

Structureof notes

Bonds to

Market

Debt Assets

In

Alignment of interestsAll bonds are the same

seniority

Robust rules for the underlying debt assets produce robust bonds

9

Green Investment Bank (GIB) Template Rules – Transparency Leads to Measurable Risk

Template Rules

1. Min debt service coverage ratios2. Max starting LTV’s3. Proven technology list 4. Robust agency agreement

Only debt within

parameters

Transparent bonds

measurable risk

These template rules would be clearly understood by Fixed Income Investors allowing them to more accurately measure the risk profile of the bonds

A standardised template would give transparency through a clear and strictly enforced set of rules for a bank to be able to place its debt into the aggregation vehicle or (GIB)

10

Applications of this simple aggregation structure – Mature Technologies

Horns-Rev Denmark 80 2MW wind turbines

Debt funding to large scale wind farms

Beneixama Spain 20MW of Solar PhotoVoltaic

Debt funding to large scale solar plants

11

Applications of this simple aggregation structure – Regulated Assets and Loans Secured Against Property

www.calfinder.com

National Grid Proposal for HVDC Cable Rebuilding Security, Conservative Energy Policy Paper

Offshore high voltage direct current (HVDC) electricity cables

North sea supper grid

Home energy efficiency loans secured against residential property via your electricity supplier

12

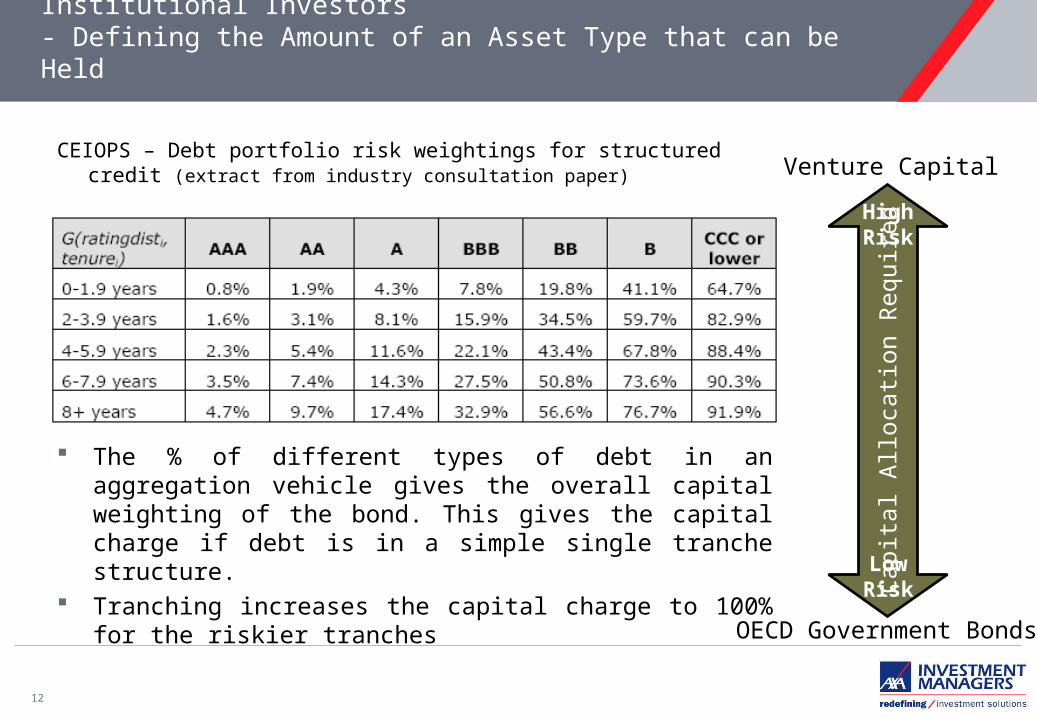

Solvency 2 – Regulated Capital Charge for Institutional Investors- Defining the Amount of an Asset Type that can be Held

CEIOPS – Debt portfolio risk weightings for structured credit (extract from industry consultation paper)

Cap

ital A

lloca

tion

Req

uire

d

HighRisk

LowRisk

OECD Government Bonds

Venture Capital

The % of different types of debt in an aggregation vehicle gives the overall capital weighting of the bond. This gives the capital charge if debt is in a simple single tranche structure.

Tranching increases the capital charge to 100% for the riskier tranches

13

Conclusion – Key Principles if Securitisation is to Become a Hercules for Renewable Energy

Simplicity – Fewer tranches – Ideally 1

– No tranche should be more senior than AAA

Transparency – Clear & robust template for debt to be input and bonds to be output

Large Size – Aggregation to allow large bond issuances that are listed on global benchmarks and are therefore liquid enough for mainstream Fixed Income investors

BACK TO BASICS

14

Important Information

This presentation is for information purposes only and does not in anyway constitute an offer, solicitation or specific recommendation with respect to the purchase or sale of securities issued by any fund which is promoted or managed by AXA Investment Managers. Any information contained in this presentation, including but not limited to examples related to turnover, leverage, allocation or diversification is based upon certain assumptions on our part and does not in any way intended to relate to any fund which is promoted or managed by AXA Investment Managers.

This presentation is not an advertisement and may not be copied or circulated, in whole or in part, to any person without the prior written consent of AXA Investment Managers. It shall not be deemed to constitute investment advice and should not be relied upon as the basis for a decision to enter into a transaction or as the basis for an investment decision. Investments should only be made on the basis of suitable investment, legal and taxation advice. Subscriptions to any fund managed or promoted by AXA Investment Managers are accepted only from eligible investors on the basis of the then current prospectus and related offering documentation. AXA Investment Managers does not offer legal, investment, tax or other advice on the suitability of these funds or services for investors, who should take appropriate professional advice and make their own assessment of the merits, risks and tax consequences prior to investing. The value of the investments may fall as well as rise. Past performance is not necessarily indicative of future returns. Target returns and volatility are not guaranteed. Investment returns may be subject to foreign currency exchange risks.

This document is not for private client use.