1h 2013 1 - toba bara company... · east madura block through subsidiary e&p company pt energi...

TRANSCRIPT

2

Disclaimer

These materials have been prepared by PT Toba Bara Sejahtra (the “Company”).

These materials may contain statements that constitute forward-looking statements. These statements

include descriptions regarding the intent, belief or current expectations of the Company or its officers with

respect to the consolidated results of operations and financial condition of the Company. These statements

can be recognized by the use of words such as “expects,” “plan,” “will,” “estimates,” “projects,” “intends,” or

words of similar meaning. Such forward-looking statements are not guarantees of future performance and

involve risks and uncertainties, and actual results may differ from those in the forward-looking statements

as a result of various factors and assumptions. The Company has no obligation and does not undertake to

revise forward-looking statements to reflect future events or circumstances.

These materials are for information purposes only and do not constitute or form part of an offer, solicitation

or invitation of any offer to buy or subscribe for any securities of the Company, in any jurisdiction, nor

should it or any part of it form the basis of, or be relied upon in any connection with, any contract,

commitment or investment decision whatsoever. Any decision to purchase or subscribe for any securities

of the Company should be made after seeking appropriate professional advice.

3

Content

Financial Highlights

2

5

Corporate Profile & Updates

4

Investment Highlights & Growth Strategies

3 Business Overview & Updates

CSR & Environmental Highlights

1

4

Corporate Profile & Updates 1

5

ABN66.1%

IM15.7%

TMU18.2%

Toba specializes in thermal coal production and comprises three operating subsidiaries: Adimitra

Baratama Nusantara (ABN), Indomining (IM) and Trisensa Mineral Utama (TMU), which hold adjacent

concession areas located in East Kalimantan, Indonesia

Toba in Brief

• Substantial and diversified thermal coal

reserves and resources

oJORC-compliant proved and probable reserves of

147 MM tons and measured, indicated and

inferred resources of 236 MM tons

oCoal brands with calorific values ranging from

4,700 - 5,800 Kcal / kg GAR

ABN79.6%

IM15.0%

TMU5.4%

Reserves

%

• Strong growth profile

oProduced 5.2 MM tons of coal in 2011 and grew to

produce around 5.6 MM tons of coal in 2012

o Prime location provides the operational cost edge to

grow as a logistical & operational center for the area

oContinued exploration effort to increase our Reserves and

Resources. Current reserves only account for 52% of our

total area has been explored

Revenue (1)

%

EBITDA(1)

%

Resources %

Total: 147 MM Tonnes Total: US$ 425 MM Total: US$ 30 MM Total: 236 MM Tonnes

Note: (1) Last Twelve Month analysis ~ Revenue and EBITDA

ABN 73.7%

IM 21.8%

TMU 4.5%

ABN 76.0%

IM 19.6%

TMU 4.4%

6

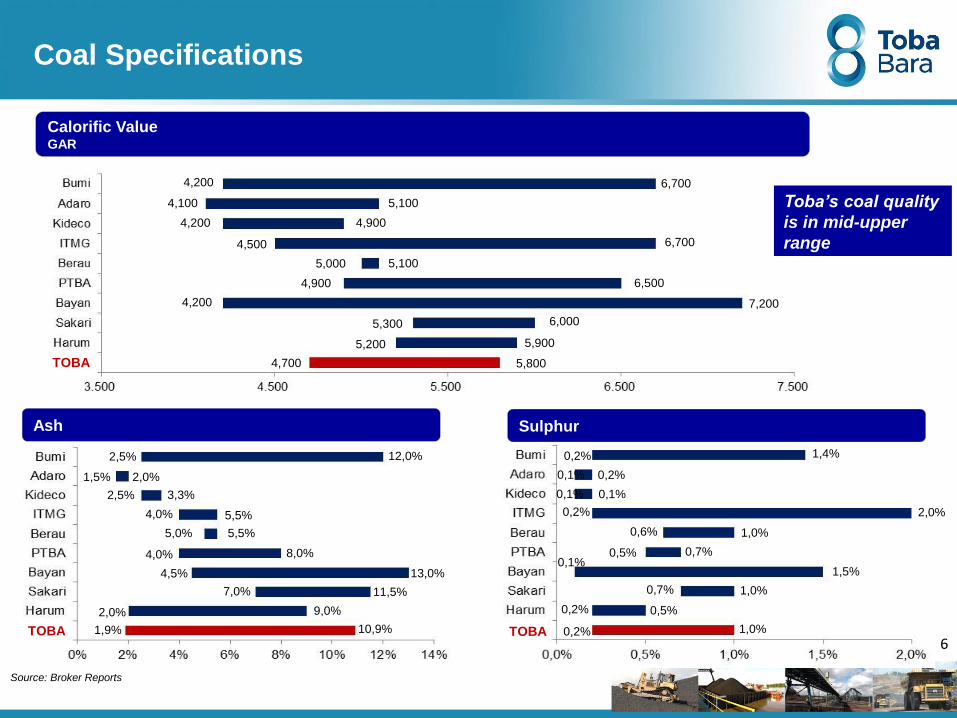

Toba’s coal quality

is in mid-upper

range

Coal Specifications

Calorific Value GAR

Ash Sulphur

4,700 5,800

5,200 5,900

6,000 5,300

4,200 7,200

4,900 6,500

5,000 5,100

4,500 6,700

4,900 4,200

4,100 5,100

6,700 4,200

2,5% 12,0%

1,5% 2,0%

2,5% 3,3%

4,0% 5,5%

5,0% 5,5%

4,0% 8,0%

4,5% 13,0%

7,0% 11,5%

9,0% 2,0%

1,9% 10,9%

0,2% 1,4%

0,1% 0,2%

0,1% 0,1%

0,2% 2,0%

1,0% 0,6%

0,7% 0,5% 0,1%

1,5%

1,0% 0,7%

0,2% 0,5%

0,2% 1,0%

TOBA

TOBA TOBA

Source: Broker Reports

7

Notes:

1. Son of TS founder, Luhut B. Pandjaitan

2. Figures are rounded off

Ownership Structure

• 20-year Production

Operation Mining Permit

(“IUPOP”) expiring in

December 2029

• IUPOP was converted from

Kuasa Pertambangan

(“KP”) in 2009

• IUPOP expires in June 2013

• IUPOP was converted from KP in

2010

• IUPOP extension was completed

in March 2013 (First out of 2

extensions: in 2023, with tenor of

10 years each)

• 13-year IUPOP expires in December

2023

• IUPOP was converted from a KP in

2010

• Plantation permit expires in 2036

• 2,990 ha • 683 ha • 3,414 ha • 8,633 ha (Right to Use Land)

• Reserves: 117MT- JORC

• Resources: 156MT- JORC

• Reserve: 22 MT- JORC

• Resources: 37MT- JORC

• Reserves : 8 MT - JORC and

additional 7 MT of internal estimate

• Resources: 43 MT- JORC

• Planted Area: 2,896 ha

License

Area

Davit Togar Pandjaitan (1) PT Bara Makmur Abadi PT Toba Sejahtra (“TS”) Roby Budi Prakoso PT Sinergi Sukses Utama

71.8% 0.8% 6.2% 5.1%

PT Toba Bumi Energi (“TBE”)

99.99% (2)

99.99% (2)

3.6%

ABN Minorities

49.0%

51.00% 99.99% (2)

Public

12.5%

Reserve

90.00%

8

Majority Shareholder

Toba believes it benefits from Toba Sejahtra’s experience in the Indonesian coal sector as well as its

leadership and experience

Controlling Shareholder with Established Track Record… … Helmed by an Experienced Leader

• A privately owned group founded in 2004 with interests in energy

and plantations

• Its business segments are as follow:

– Energy: Owns 5 coal mining concessions through Toba and PT

Kutai Energi. All of TS' mines are characterized by low production

costs and favorable proximity to ports

– Oil & Gas: In the exploration phase of the 4,567 sq miles South

East Madura Block through subsidiary E&P company PT Energi

Mineral Langgeng

– Power Plant: Operates a 30 MW coal-fired power plant in Palu,

Central Sulawesi and is developing a 120 MW greenfield power

plant in Senipah, East Kalimantan

– Agribusiness: A 25% stake in a 12,000 ha palm oil plantation in

East Kalimantan

• General (Ret.) Luhut B. Pandjaitan is the key shareholder and

founder of Toba Sejahtra group. He is currently the chairman of TS

• Mr. Luhut had a long and illustrious career in the civic service

before turning to the commercial sector. Over the course of thirty

years in the Army Special Forces, Mr. Luhut rose to become a four-

star general

– In 1999, Mr. Luhut retired from the military service to serve as

Ambassador for the Republic of Indonesia to Singapore

– In 2000, he was appointed Minister of Industry and Trade of the

Republic of Indonesia

• Thereafter, Mr. Luhut applied his knowledge and leadership skills to

establish TS in 2004, building it from the ground up into a major

business group with interests in energy oil and gas, power and

agribusiness

9

Initial Public Offering

Listed on IDX 06 July 2012

Number of Shares Offered 210,681,000 shares or 10.47%

IPO Proceed IDR 400,293,900,000

Anchor Investor Baring Private Equity Asia (8% at IPO)

Ticker Code TOBA

10

Ticker Code: Toba In full amount IDR

IPO (6th Jul 2012)

IDR 1900 28 Jun 2013

IDR 860

Historical Share Price

Sources: Bloomberg

• Decline in TOBA’s share price reflects lack of liquidity and lack of stock coverage

• Going forward, we are considering various options to increase liquidity and coverage

2012 2013

-

500.0

1000.0

1500.0

2000.0

2500.0

11

2007

• IM commenced

production

2011

• TMU commenced

production

• Toba production

hit 5m tons

2008

• ABN commenced

production

• Operational

adjustment due to

drop in coal

market

2010

• TS acquired the remaining share

for IM from minority shareholder

• Toba acquired 51.0% of ABN,

52.5% of TBE (IM’s shareholding

company) and 51.0% of TMU

• Toba production hit 4m tons

Key Milestones

Strong track record of acquisitions, development of greenfield mines, rapid production ramp-up and

experience to adjust operation in a down-market

2007 2008 2009 2010 2011 2012 2013

2012

• Toba acquired the minorities’ shares in TBE and TMU

• IPO/Listed on IDX, 6th July

2012

• Eliminated overlapping issues

with plantation company (PKU)

2009

• ABN & IM production

reached 2m tons

2013

• IM successfully

extended IUPOP

until 2023

12

Investment Highlights and Growth Strategies

Source: Company data

0.1

1.1

3.1 3.8

4.4

~ 6,5

0.7

0.9

0.9

1.4

1.0 0.0

0.3

0

1

2

3

4

5

6

7

2007 2008 2009 2010 2011 2012 2013

TMU Indomining ABN

13

Solid Operating Track Record (i)

0,8

2,0

3,9

5,3

5,6

Production Growth MT = Million Tons

0,2

~5,8 – 6,4

Fo

recast

• Toba started exploration at ABN & IM in 2006 and at TMU in 2008

• Production grew at 65% CAGR from initial size of 800k in 2008 to 5.6 MT in 2012

• Toba focuses on Continuous Production Growth and this is supported by available infrastructure

capacity of 13 MT of coal

• Additional 3 MT of capacity is expected to be realized in 3-4Q13 to become total of 16 MT

• Production growth will be driven by TMU and Additional CAPEX will help it fuel growth

ABN

IM TMU

Toba is transitioning from Greenfield into growing major player

Fo

recast

0.3

14

Toba’s production growth is among the highest in the industry over the

last 4 years

Production Growth Comparison 2009 - 2012

CAGR %

Solid Operating Track Record (ii)

15

Prime Location Gives Significant Advantage in Cost (i)

Samarinda

Mahakam River

Muara Jawa

Muara

Berau

Makassar Strait

Major City

Jetty

Transhipment Point

~55 km

(total ~120 km)

~65 km

kilometers

0 12 24 36 48

ABN

Kutai Energy

Adjacent

locations for all

3 mines

TMU ABN

IM

1

17km

ABN Jetty

IM Jetty

~ 5 km

Furthest pit to

jetty 25km | with

closest one ~5km

3 Major city is

less than 50

km

4

Close proximity

transhipment

point & jetty

2

Toba owns all infrastructures (coal processing plants, overland conveyors, and jetties),

giving significant operating leverage vs other concessions in surrounding areas

Prime Location

TMU - IM Hauling Road

Balikpapan

Jetty

16

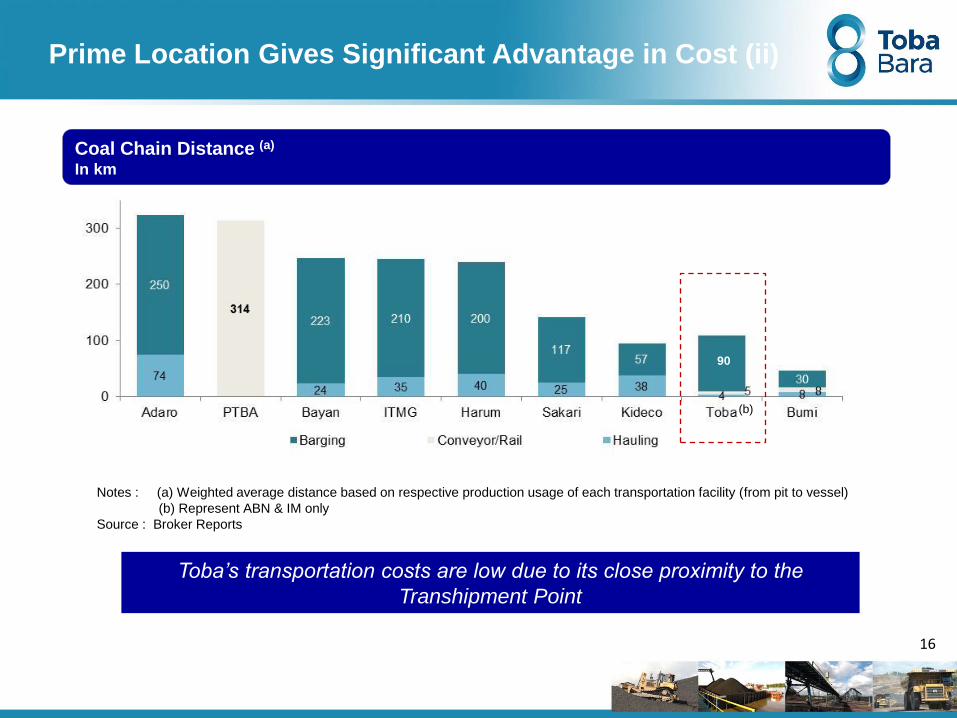

Prime Location Gives Significant Advantage in Cost (ii)

Coal Chain Distance (a)

In km

Toba’s transportation costs are low due to its close proximity to the

Transhipment Point

Notes : (a) Weighted average distance based on respective production usage of each transportation facility (from pit to vessel)

(b) Represent ABN & IM only

Source : Broker Reports

(b)

90

29

47 45 39

71 67

0

10

20

30

40

50

60

70

80

2009 2012

Global Cash Cost Environment & Indonesia’s Position

Average cash cost prices have moved up by close to 50%...

Lowest

Median

Weighted average

US$/ton

Prod. Cash Cost by Country (Thermal Coal)

Cash Cost Curve in 2009

Cash Cost Curve in 2012

Global Cash Cost in 2012

18

Co

st

Red

ucti

on

Cost Reduction Initiatives

ABN

IM

TMU

SR (x)

Dump

Distance

(m)

2012A 2013F

SR

Dump

Distance

(m)

SR

Instrastruc

ture

(US$/ton)

15.3x

13.0x

14.9x

US$13/ton US$4 – 6 /ton

2,365

2,174

12 – 14x

1500 - 1800

9 – 11x

1800- 2100

9 – 10x

Potential Cost Saving

Up to US$8/ton

US$15 - 20 /ton

Up to US$8 /ton

19

ABN66.1%

IM15.7%

TMU18.2%

Coal Reserves Coal Resources

(MM Tons) Proved Probable

Total

Reserves Measured Indicated Inferred

Total

Resources

ABN 70 47 117 73 70 13 156

IM 11 10 22 24 10 4 37

TMU 5 4 8 9 8 26 43

Total 86 61 147 106 88 43 236

Reserves and resources upside from conversion of resources to reserves and further exploration of

concession areas

Notes:

1. Differences in totals are due to rounding off

2. The Runge Report for ABN was as of 31 December 2011, the PT SMG Consulting Report for IM was as of 1 January 2012 and the Marston Report for TMU

was as of 31 October 2011

Total: 147 MM Tons Total: 236 MM Tons

Substantial Reserves and Resources

Support Production Expansion

Coal Reserves and Resources (1) (2) (JORC) Reserves (1)

MM Tons

Resources (1)

MM Tons

ABN79.6%

IM15.0%

TMU5.4%

Note: Areas already explored

20

Substantial Reserves and Resources due to Vast

Unexplored Areas & Relatively Long Reserve Life

• Explored 3,704 of 7,087 hectares of concession areas

(52% of total concession area) and drilled 3,512

boreholes as of 31 December 2011

• Additional JORC coal reserves and resources

expected to be discovered, especially at TMU where

only 680 hectares out of 3,414 hectares of

concession (20% of TMU concession area) have

only been explored

TMU

Source : Broker report

Toba’s reserve life of over 20 years compares

favorably with other listed peers

Toba’s Concessions Reserve life ~ Industry Comparison

ABN

IM

TMU

21

Coal Market Update

Range-bound US$77 -95/ton

• Coal Prices have bounced back from high 70’s in 2Q 2013 and now on decline trend within

US$ 77-83/ton

• Going forward, prices are expected to trade within range-bound of US77-95/ton

Source: Newcastle Index

70

80

90

100

2012 2013

Changes in Forward Curve Newc Global Coal Index

Source: Global Coal

81.7 83.2 86.6 90.3 93.6

95.4 96.7 100.6

105.9 110.2

0

50

100

150

200

250

Q3'13 Q4'13 Cal-14 Cal-15 Cal-16

19-Jun-13 2-Jan-13

Coal Price Trend

22

Strong Relationships with Multinational Customers

Major Customers

DRAGON ENERGY GROUP

Major customers provide the stable

business support for Toba’s marketing…

… minimum marketing fees because Toba

handles our own marketing internally

Toba’s Marketing Operations

Central Marketing Operations of all 3

subsidiaries

Internally developed customer base

that allows Toba to have low marketing

costs

Balance mix of long term contracts,

short term and spot

Active participation in reputable

conference and trade shows to promote

Toba brand

Enhance marketing strategy to sell

directly to end-users

23

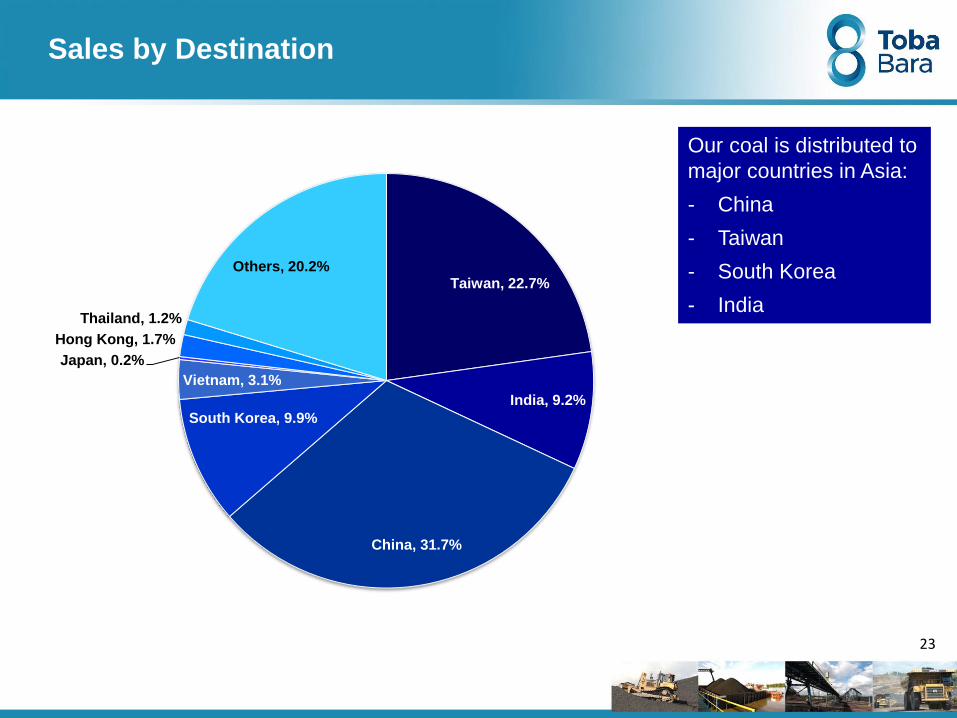

Sales by Destination

Our coal is distributed to

major countries in Asia:

- China

- Taiwan

- South Korea

- India Taiwan, 22.7%

India, 9.2%

China, 31.7%

South Korea, 9.9%

Vietnam, 3.1%

Japan, 0.2%

Hong Kong, 1.7%

Thailand, 1.2%

Others, 20.2%

24

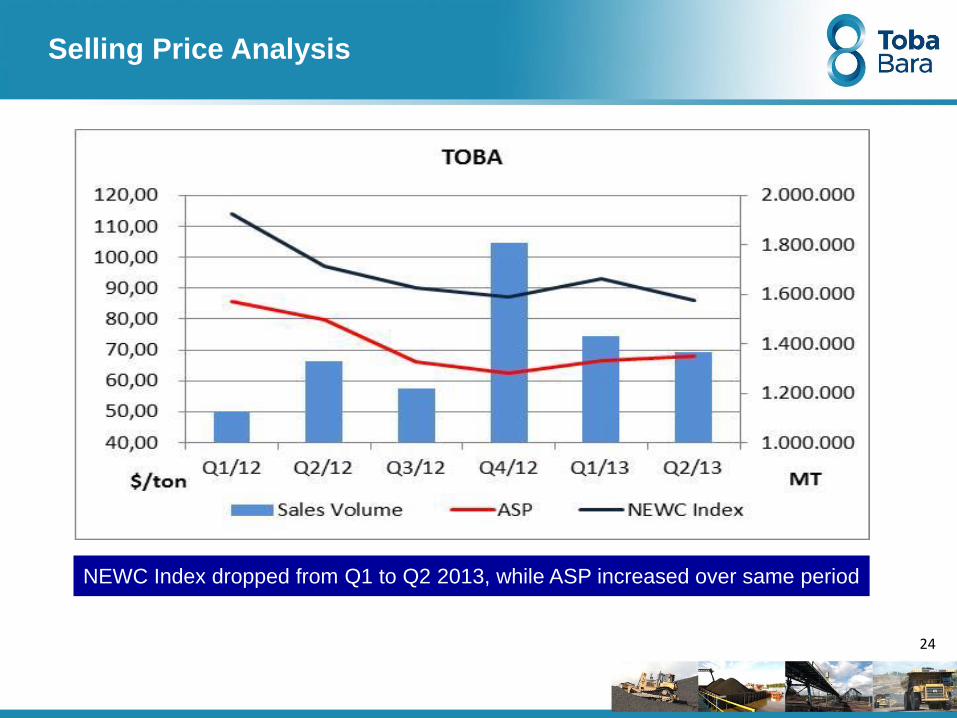

Selling Price Analysis

NEWC Index dropped from Q1 to Q2 2013, while ASP increased over same period

25

Business Overview 3

26

Manage cash costs: Lower SR,

Shorten Dump Distance

Construct hauling road from

TMU to IM

Share current infrastructures :

CPP & Jetty & lower costs

Centralize fuel supply

Optimize sales through hedging

activities

Increase our reserves through

acquisition and exploration

Strategic Initiatives to Manage Changing Environment

Returning future

Profitability

Level

Strategic Initiatives / Response to Changing Coal Prices

1

2

3

4

5

6

27

Executions and Achievements so far… (I)

Manage Cash Cost: lower SR &

dump distance

OPERATION

Achievement Execution Initiative

Construct Hauling Road from

TMU to IM

Share Existing Infrastructure

Adjusted mine plan in 3Q12 and

lowered dump distance despite pre-

stripping in 1Q13 at ABN

Construction commenced end-2012

and was scheduled for completion in

2Q13

TMU commenced infra-sharing using

ABN’s road and IM’s CPP & Jetty

Provide Financing to IM

FINANCIAL

Optimize Sales through Hedging

Centralize Fuel Supply

Maximized current ideal capital structure

by using loan to finance new CPP

construction and land compensation

Made available hedging line with

notable financial institutions

Sourced constant bulk supply from

major fuel supplier to allow for good

monitoring of effective fuel usage

Secured 3-year US$ 15 mn term loan

from SCB at competitive lending rate

of LIBOR+3.6%

No hedging has been utilized. Sold

~70% of 2013 sales volume using fixed

pricing, and securing cash

prepayments

Cash cost is on track to be

lowered ~US$8/t by FY13

Hauling road was completed in

May 2013, ahead of schedule

TMU’s underwent significant

production ramp-up from 25K tons

in April 2013 to 72K in June 2013

Sourced supply at competitive

price, while continuing to seek

other sources with better pricing

In

Progress

In

Progress

In

Progress

Conduct Joint Mine Plan Maximizing extraction of ~2 MT of

high quality coal reserve with low SR

ABN & IM commenced joint-

border mining end-2012

In

Progress

Achievement Execution Initiative

Executions and Achievements so far… (II)

Secure Sales Volume and

Maintain this Activity

continuously

COMMERCIAL

Achievement Execution Initiative

TOBA successfully sold and secured

~ 50-90% of targeted sales volume for

2013

Develop and Implement Corporate

Social Responsibility

CORPORATE SOCIAL RESPONSIBILITY / ENVIRONMENT

Achievement Execution Initiative

• Created Educational Program for

local Communities

• Provided health services to local

communities

• Created local employment

Proper Mining award in East

Kalimantan for ABN and IM

• ABN secured ~ 80-90% of 2013

targeted sales

• IM secured one-year contract

with one of its major customers

at competitive price

• TMU secured ~50%

prepayment from one of buyers

Enhance Marketing Expertise

TOBA negotiates directly with

logistics providers

Internal marketing team currently

handles sales activities

Maximize Cost Efficiency Lower logistics cost (barging

costs) by 18% from 1Q13 to 2Q13

TOBA does not depend on third

party marketing agent

In

Progress

28

…Next: Objectives in 2H 2013

COMMERCIAL

Execution Initiative

Develop and Implement Corporate

Social Responsibility

CORPORATE SOCIAL RESPONSIBILITY / ENVIRONMENT

Execution Initiative

Aiming to be eligible for “Proper” mining

awards for all three mines

Maximize Cost Efficiency Aiming to continue lowering logistics

cost i.e. by another 10-15%, resulting in

overall cost savings for full year of US$1/

ton, equivalent to 25% cost savings

Increase Cooperation and Internal

integration with Suppliers

Working together with contractors on

fleet management and supply parts

management with end-providers

Status

Still in negotiation. Expected to be

completed in 2H 2013

Expected to be completed in 2H 2013

Status

Expected to be achieved in 1Q14

29

30

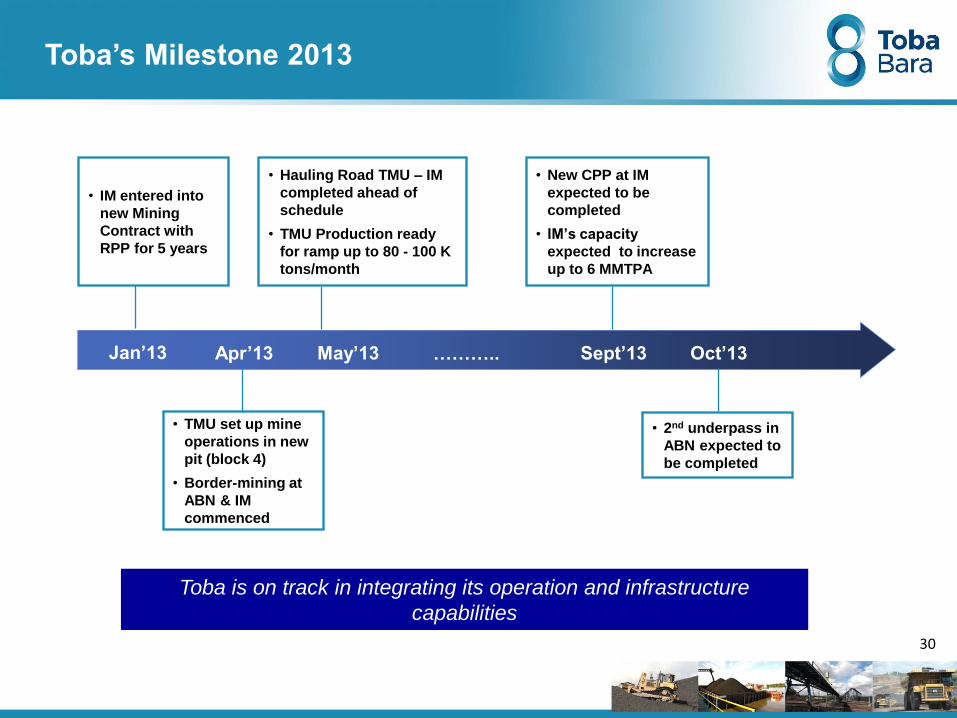

Toba’s Milestone 2013

2007 2008 2009 2010 2011 2012

• Hauling Road TMU – IM

completed ahead of

schedule

• TMU Production ready

for ramp up to 80 - 100 K

tons/month

May’13 Sept’13

• New CPP at IM

expected to be

completed

• IM’s capacity

expected to increase

up to 6 MMTPA

Oct’13

• 2nd underpass in

ABN expected to

be completed

Apr’13

• TMU set up mine

operations in new

pit (block 4)

• Border-mining at

ABN & IM

commenced

Jan’13

• IM entered into

new Mining

Contract with

RPP for 5 years

Toba is on track in integrating its operation and infrastructure

capabilities

………..

31

Integration of three (3) mines

• Benchmarking and

sharing between

departments and

functions

• Optimize and

coordinate mine

planning and logistics

• Centrally coordinate

and streamline

corporate finance,

legal, human resource

and CSR functions

• Joint mine plan and

infrastructure sharing

1 Increase coal reserve

and resource

• Continue exploration

activities to increase

proven and probable

reserves as only 52%

has been explored to

JORC standard

• Consider opportunities

to acquire coal

concessions with

significant reserves

3 Strengthen existing

and develop new customer

relationships

• Supply a higher

proportion of sales

volume to end users,

while maintaining

relationships with

existing coal traders

• Target customers in

Japan, Taiwan, South

Korea, China, Vietnam

and Hong Kong, South

East Asia and India

4 Continue to focus on

health and safety, environmental track

record and commitment to CSR

• Maintain and enhance

high international

operating standards,

utilize automated

mining methods to

minimize accidents and

enhance safety

• Foster community ties

through development

programs as well as job

creation

5 Organically increase

coal production levels

• Expand coal production

through increased

production and mine

development activities

• Strengthen

relationships with third

party mining

contractors and work

closely with them to

improve their

productivity

2

Toba’s Business Strategies

Growing Reserves and Maintain Profitability at Different Cycles

Toba’s Operational Performance in 2Q 2013

Quarterly Production & Stripping Ratio (SR) Thousand Tons

Production Summary

1Q13 2Q13 Change Comment

Production

(Mn tons)

SR (x)

1.29 1.50

15.1 13.6

1.44 1.37 Sales volume in 1Q13 was slightly higher than in 2Q13

mainly due to inventory clearance accumulated from

4Q12

-4.9%

16.6%

-9.9%

Q-o-Q production in 2Q13 increased by 16.6%

resulting from completion of pre-stripping at ABN and

TMU

SR fell due to completion of pre-stripping at ABN

Sales

(Mn tons)

1,097 1,373 1,574 1,587 1,287 1,501

17.6x

16.6x

14.2x

12.1x

15.1x 13.6x

5x

10x

15x

20x

500

1,000

1,500

2,000

1Q 2012 2Q 2012 3Q 2012 4Q 2012 1Q2013 2Q2013

Production volume Stripping Ratio (SR)• Production volume of 2.8

MMT in 1H 2013 was 44%

of our FY 2013 production

target

• To achieve FY target of

5.8MT-6.4MT, TMU is

expected to be

instrumental in boosting

overall growth via

continued ramp-up

33

ABN Operational Performance

Production & Stripping Ratio Thousand Tons

Despite higher than anticipated rainfall delayed operational activities in 1H13,

ABN still managed to increase production by 7.6% from 1Q13 to 2Q13

ABN’s 2nd underpass is currently under construction and expected to be

completed by 4Q13 with aim to lower OB dump distance

At 14.2x SR, for every 100 meter-decrease in dump distance is expected to

reduce cost by~US$0.73/ton, contributing to ~US$ 4.3/ton in FOB cash cost

saving

Operational Advantage & Focus

Short coal hauling distance 4km

High Built Crusher Cap 10 mm ton/year

Barge Loading Jetty Loading Speed of up to

1,800 ton/hour

Under-pass:

Capitalizing on Infra Strength

1 2 3 4

ABN

Key Highlights

TMU

IM

PT Kutai Energi

884 1,078 1,224 1,225 925 995

17.6x 17.1x

14.7x

12.6x

16.6x 14.2x

5x

10x

15x

20x

500

1,000

1,500

1Q 2012 2Q 2012 3Q 2012 4Q 2012 1Q2013 2Q 2013

Production volume (mt) Stripping ratio

Dump

distance (m)2,492 2,461 1,978 1,723 1,719 1,864

34

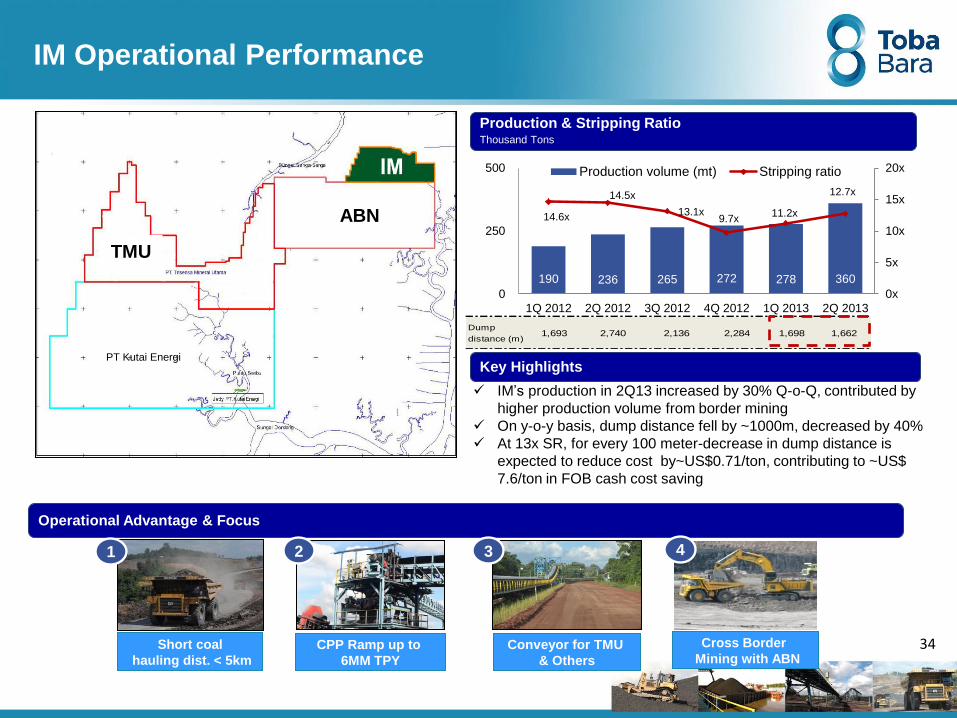

IM Operational Performance

IM’s production in 2Q13 increased by 30% Q-o-Q, contributed by

higher production volume from border mining

On y-o-y basis, dump distance fell by ~1000m, decreased by 40%

At 13x SR, for every 100 meter-decrease in dump distance is

expected to reduce cost by~US$0.71/ton, contributing to ~US$

7.6/ton in FOB cash cost saving

Key Highlights

Production & Stripping Ratio Thousand Tons

Operational Advantage & Focus

Short coal

hauling dist. < 5km

CPP Ramp up to

6MM TPY

Conveyor for TMU

& Others

Cross Border

Mining with ABN

1 2 3 4

TMU

ABN

PT Kutai Energi

190 236 265 272 278 360

14.6x

14.5x

13.1x 9.7x

11.2x

12.7x

0x

5x

10x

15x

20x

0

250

500

1Q 2012 2Q 2012 3Q 2012 4Q 2012 1Q 2013 2Q 2013

Production volume (mt) Stripping ratio

Dump

distance (m)1,693 2,740 2,136 2,284 1,698 1,662

35

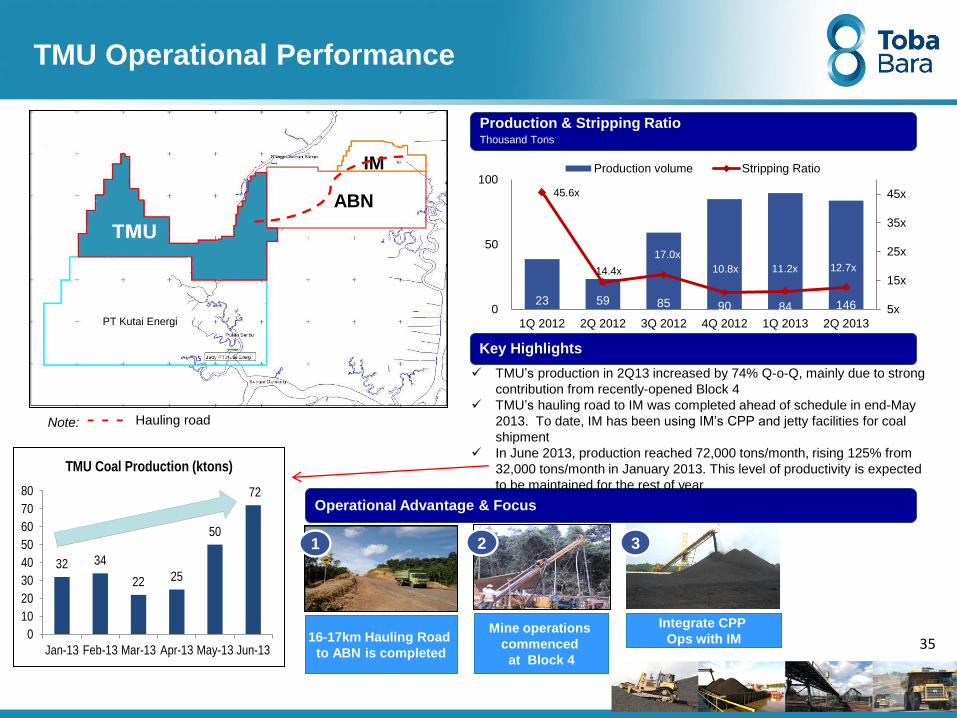

TMU Operational Performance

Key Highlights

Production & Stripping Ratio Thousand Tons

Operational Advantage & Focus

TMU’s production in 2Q13 increased by 74% Q-o-Q, mainly due to strong

contribution from recently-opened Block 4

TMU’s hauling road to IM was completed ahead of schedule in end-May

2013. To date, IM has been using IM’s CPP and jetty facilities for coal

shipment

In June 2013, production reached 72,000 tons/month, rising 125% from

32,000 tons/month in January 2013. This level of productivity is expected

to be maintained for the rest of year

16-17km Hauling Road

to ABN is completed

Integrate CPP

Ops with IM Mine operations

commenced

at Block 4

1 2 3

ABN

IM

PT Kutai Energi

Note: - - - Hauling road

23 59 85 90 84 146

45.6x

14.4x

17.0x

10.8x 11.2x 12.7x

5x

15x

25x

35x

45x

0

50

100

1Q 2012 2Q 2012 3Q 2012 4Q 2012 1Q 2013 2Q 2013

Production volume Stripping Ratio

32 34

22 25

50

72

0

10

20

30

40

50

60

70

80

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13

TMU Coal Production (ktons)

36

Financial Highlights 4

37

Financial Performance YTD 2013

• In 2Q13, SR was

lowered by 10%, while

production increased

by 17%...

• …resulting in 6%

decline in adj FOB

Vessel cash cost

• ASP slightly rose by 3%

despite 8% Q-o-Q fall

in NEWC Index…

Notes (a) FOB vessel cash costs: COGS, Selling Expenses, Royalty,excluding depreciation fixed assets and amortization of exploration

and development

(b) Adj. FOB vessel cash costs: COGS, Selling Expenses, Royalty excluding depreciation fixed asset and amortization of

exploration and development asset & without accounting for component of deferred striping cost

• … EBITDA and Net

Income increased by

32% and 11%

respectively

1

2

3

TOBA 1Q 2013 2Q 2013 YTD 2013 Change %

Operation

Sales Volume kton 1.435 1.367 2.802 -5%

Coal production kton 1.287 1.500 2.787 17%

Stripping Ratio x 15.1 13.6 14.3 -10%

NEWC Index US$/ton 93.0 85.9 89.5 -8%

Per Ton Basis

ASP US$/ton 66.4 68.1 67.2 3%

FOB Vessel Cash Cost US$/ton 55.4 54.9 55.2 -1%

Adj. FOB Vessel Cash Cost US$/ton 59.3 56.0 57.7 -6%

EBITDA US$/ton 6.6 9.1 7.8 39%

Financial

Sales US$'000 94,942 93,138 188,079 -2%

Gross Profit US$'000 14,392 16,692 31,084 16%

Operating Profit US$'000 7,745 10,655 18,400 38%

EBITDA US$'000 9,448 12,486 21,934 32%

Net Income before Minority

InterestUS$'000 5,975 6,616 12,591 11%

Ratio

Gross Profit Margin % 15.2% 17.9% 16.5% 18%

EBITDA Margin % 10.0% 13.4% 11.7% 35%

Net Profit Margin % 6.3% 7.1% 6.7% 13%

38

Financial Performance – 1H 2013 vs 1H 2012

Note (a) FOB vessel cash costs: COGS, Royalty, Selling Expenses excluding depreciation and

amortization

Coal production grew 13% (yoy)

driven by TMU and border mining

at IM

(a)

1H 2012 1H 2013 Change %

Operation

Sales Volume million ton 2.45 2.80 14.1

Coal Production million ton 2.47 2.79 13.0

Striping Ratio x 17.1 14.3 (16.4)

NEWC Index US$/ton 105.3 89.5 (15.0)

Financials

Sales US$ Million 202.86 188.10 (7.3%)

Gross Profit US$ Million 35.90 31.10 (13.4%)

Operating Profit US$ Million 25.11 17.82 (29.0%)

EBITDA US$ Million 27.63 21.92 (20.7%)

Net Income US$ Million 18.15 12.65 (30.3%)

Net Income after Minority US$ Million 9.73 6.61 (32.1%)

Interest

Ratio

Gross Profit Margin % 0.18 0.17 (6.6%)

EBITDA Margin % 0.14 0.12 (14.4%)

Net Profit Margin % 8.95 6.73 (24.8%)

Per Ton Basis

ASP US$/ton 82.6 67.2 (18.6%)

FOB Vessel Cash Cost US$/ton 67.6 55.0 (18.6%)

EBITDA declined 20.7%

attributable to 18.6% drop in ASP,

but compensated by lower

COGS and increased sales

volume

Toba’s 1H13 production achieved

44% of 2013 highest production

target of 6.4 million tons

FOB vessel cash cost slashed by

18.6% yoy mainly due to lower

SR and shortened dump

distance

39

Evolution of FOB Vessel Cash Cost

on Quarterly Basis

ABN

IM

1Q 2012 2Q 2012 3Q 2012 4Q 2012 2Q 2013

Adj. FOB vessel

cash cost (b) US$74/ton US$73/ton US$64/ton

US$66/ton US$64/ton US$49/ton

SR 17,6x 17,1x 14,7x 12,6x

14,6x 14,5x 13,1x 10,5x

14,2x

12,9x

US$56/ton

US$53/ton

US$51/ton

US$61/ton

Notes (a) FOB vessel cash costs: COGS, Selling Expenses, Royalty,excluding depreciation fixed assets and amortization of exploration and development

(b) Adj. FOB vessel cash costs: COGS, Selling Expenses, Royalty excluding depreciation fixed asset and amortization of exploration and development asset &

without accounting for component of deferred striping cost

FOB vessel

cash cost (a) US$65/ton US$68/ton US$61/ton US$57/ton US$56/ton

US$74/ton US$71/ton US$57/ton US$57/ton US$57/ton Adj. FOB vessel

cash cost (b)

SR

FOB vessel

cash cost (a)

TMU

Adj. FOB vessel

cash cost (b)

SR

FOB vessel

cash cost (a) US$76/ton US$69/ton US$64/ton

45,6x 14,4x 10,9x 10,8x 12,7x

US$42/ton US$66/ton

US$128/ton US$56/ton US$41/ton US$52/ton US$64/ton

1Q 2013

16,6x

11,3x

US$62/ton

US$57/ton

US$56/ton

US$55/ton

11,2x

US$44/ton

US$49/ton

ABN Petrosea 34 40 ABN internal

Indomining RCI 58 57 Indomining internal

TMU STA 45 30 TMU internal

Kideco Jaya Agung Petrosea 41 44 PTRO Financial Statement

Santan Batubara Petrosea 82 117 PTRO Financial Statement

Gunung Bayan Pratama Petrosea 114 95 PTRO Financial Statement

Berau Coal BUMA 159 113 DOID Financial Statement

Gunung Bayan Pratama BUMA 140 112 DOID Financial Statement

Adaro Indonesia BUMA 130 73 DOID Financial Statement

Arutmin Indonesia Darma Henwa 138 109 DEWA Financial Statement

Berau Coal Darma Henwa 169 152 DEWA Financial Statement

Kaltim Prima Coal Darma Henwa 44 52 DEWA Financial Statement

Arutmin Indonesia ABM 46 78 ABM Financial Statement

Total 103 92

SourceAP Days

30 Jun Customer Contractor

AP Days

31 Mar

40

Toba Commands Strong Bargaining Power

with Contractor(s)

Toba is a quality partner, consistent in fulfilling its liabilities with business partners even

during worst of times. This enables it to demand excellent services and top quality

heavy equipment to perform its mining activities

41 Note (a) FOB Vessel Cash Costs exclude G&A, royalty, marketing fee, depreciation of fixed asset, and

amortization of exploration asset, while including deferred striping cost

Toba’s Cash Costs Comparisons

• ABN can operate in higher SR

relative to peers mainly due to

lower transportations costs from

location advantages

SR 16,6x 11,3x 7,2x 11,7x

FOB Vessel Cash Cost (a)

US$/ton

• The FOB Vessel Cash Cost

calculation excludes marketing

fees, in which HRUM and ITMG

paid significant amount

• ABN’s cash cost and SR was

high in 1Q 2013 mainly due to

pre-stripping activities in Pit 1

1Q 2013 Figures

42

Balance Sheet

• Total Assets as of June 2013

increased by 13% from December

2012

• Cash and cash equivalent rose by

47% compared to December 2012

• Shareholders Equity surged by 4%

from December 2012 to June 2013,

reflecting positive growth return

Balance Sheet US$’000

Despite decreasing trend in Coal index

price, we have successfully grown total

assets through stronger equity base

Dec-12 Mar-13 Jun-13 Movement

(Jun'13 - Dec'12)

Cash and cash equivalents 36,307 60,348 53,289 47%

Fixed Assets 34,053 35,678 41,337 21%

Others 191,166 187,232 199,681 4%

Total Assets 261,526 283,258 294,307 13%

Debt 49,033 43,352 55,804 14%

Other Liabilities 101,549 122,991 123,395 22%

Total Liabilities 150,582 166,343 179,199 19%

Shareholders Equity 110,944 116,915 115,108 4%

Total Net debt/Equity 44% 37% 48%

114

97

90

87

93

86

80

85

90

95

100

105

110

115

120

1Q 2012 2Q 2012 3Q 2012 4Q 2012 1 Q 2013 2Q 2013

NEWC Index Price (US$/tons)

34

16

39 36

60

53

35 35

44

49

43

56

0

10

20

30

40

50

60

70

1Q 2012 2Q 2012 3Q 2012 4Q 2012 1Q 2013 2Q 2013

Cash

Debt

43

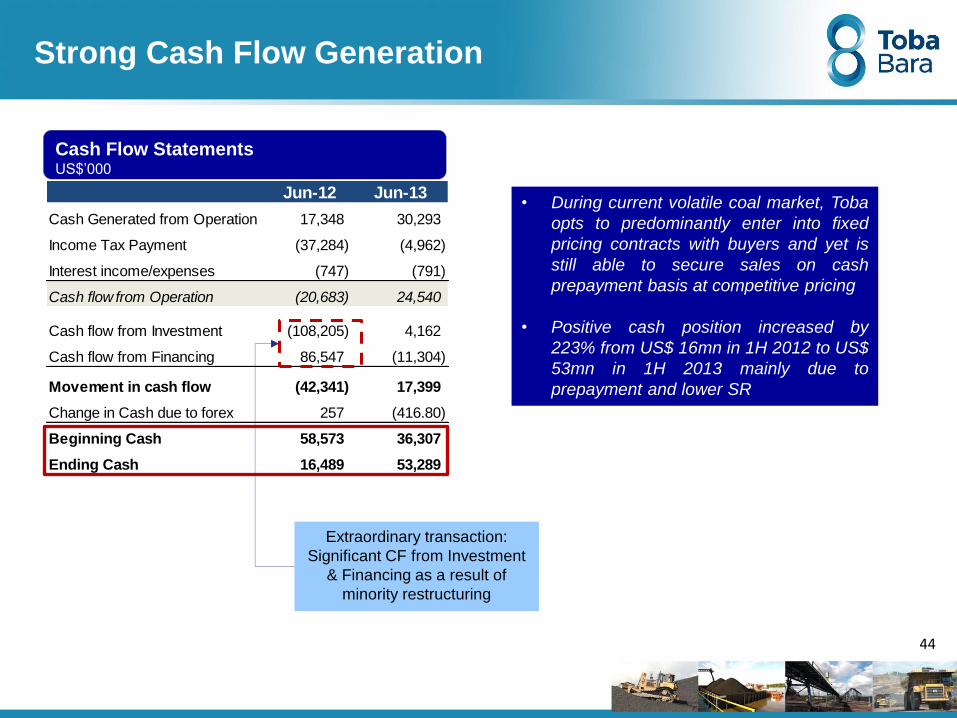

Debt and Cash Position

Net Debt Position US$ Mn

2% 34% 6% 11% Net Cash 3% Net Debt to

Equity

Cash balance rose from US$16.5 mn in 2Q12 to US$53.3mn in 2Q13, causing net debt

position to improve from US$18.5mn in 2Q12 to US$3.0mn in 2Q13

Jun-12 Jun-13

Cash Generated from Operation 17,348 30,293

Income Tax Payment (37,284) (4,962)

Interest income/expenses (747) (791)

Cash flow from Operation (20,683) 24,540

Cash flow from Investment (108,205) 4,162

Cash flow from Financing 86,547 (11,304)

Movement in cash flow (42,341) 17,399

Change in Cash due to forex 257 (416.80)

Beginning Cash 58,573 36,307

Ending Cash 16,489 53,289

44

Strong Cash Flow Generation

• During current volatile coal market, Toba

opts to predominantly enter into fixed

pricing contracts with buyers and yet is

still able to secure sales on cash

prepayment basis at competitive pricing

• Positive cash position increased by

223% from US$ 16mn in 1H 2012 to US$

53mn in 1H 2013 mainly due to

prepayment and lower SR

Cash Flow Statements US$’000

Extraordinary transaction:

Significant CF from Investment

& Financing as a result of

minority restructuring

45

CSR & Environmental Highlights 5

46

• Toba is continuously developing and implementing its corporate social responsibility programs

– Creating educational opportunities for local communities including renovating schools, training teachers,

providing post-graduate educational assistance and creating a literacy program for adults and a scholarship

program for school-aged children

– Providing health services to the local communities

– Helping groups of farmers plant crops of vegetables and bamboo and assisting with land rehabilitation

– Creating local employment opportunities by sourcing some of the Company’s site workforce from the

neighboring areas

Helping Farmers Plant Crops Creating Educational Opportunities Providing Health Services

Toba is Committed to Being a Responsible

Corporate Citizen

2007 2008 2009 2010

2

0

1

1

Target

PROPER Mining Award in

ABN, IM, & TMU

47

Award and Recognition

ABN

East Kalimantan PROPER Green

Mining Award

2012 2014 2011

Ernst and Young

Social

Entrepreneur of

the Year 2011

2013

Indomining

East Kalimantan PROPER Blue

Mining Award

PT Toba Bara Sejahtra Ranks as one of Indonesia’s

Top 50 companies

!

48

Appendix

49

• Current production capacity (31 December 2012):

– Crusher: 10 MM tonnes p.a.

– Conveyor: 10 MM tonnes p.a.

• Produces two varieties of blended thermal coal

– ABN 52: Marketed CV(1) of 5,200 kcal / kg GAR

– ABN 55: Marketed CV of 5,500 kcal / kg GAR

– ABN 58 : Marketed CV of 5,800 kcal / kg GAR

• Substantially all of the owners of the land within ABN’s

concession area have been compensated and ABN has been

granted the exclusive right to mine those areas

• Area: 2,990 ha

• Location: Sanga-Sanga, Kutai Kartanegara, East Kalimantan

• Type of license: IUPOP

• Expiry date: 1 December 2029

• Commencement of production: September 2008

• 2012 production: 4.4 MM tonnes

• Mining consultant: PT Runge Indonesia

ABN: Coal Concession Overview

IM

TMU

ABN

Jetty ABN

Overview

Operations

Marketing

• Historically sold between 50%-100% of its annual production through

long-term (longer than 1 year) with coal trading companies

– The remainder were sold on the spot market

• Currently, IM sells coal to buyers based on fixed priced contracts up

to one year, backed with pre-determined cash prepayments

Note:

1. Calorific value

50

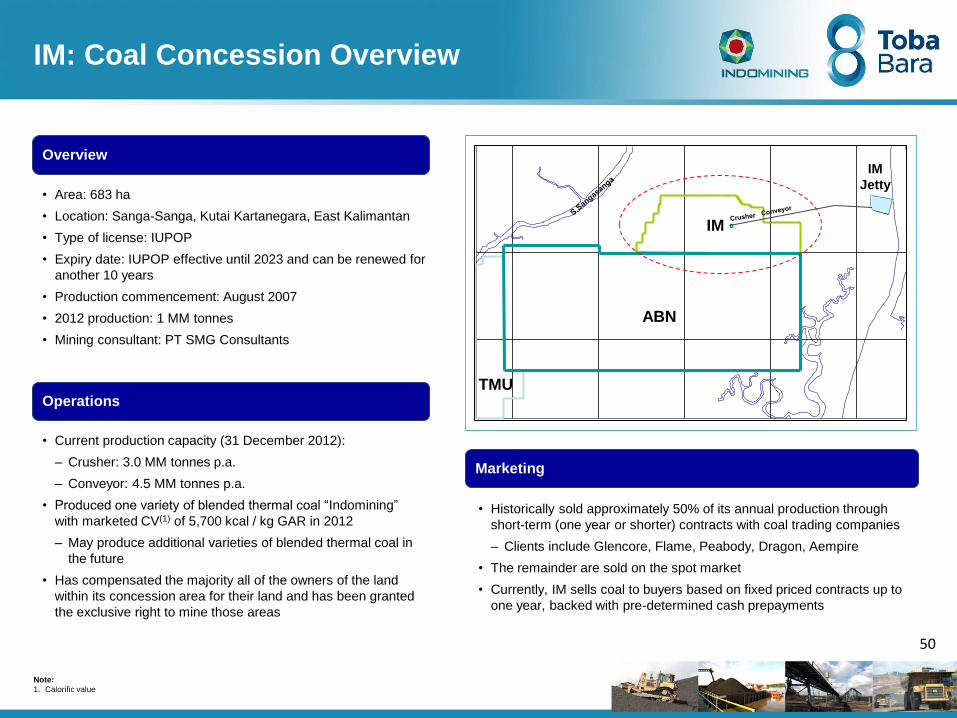

• Current production capacity (31 December 2012):

– Crusher: 3.0 MM tonnes p.a.

– Conveyor: 4.5 MM tonnes p.a.

• Produced one variety of blended thermal coal “Indomining”

with marketed CV(1) of 5,700 kcal / kg GAR in 2012

– May produce additional varieties of blended thermal coal in

the future

• Has compensated the majority all of the owners of the land

within its concession area for their land and has been granted

the exclusive right to mine those areas

• Area: 683 ha

• Location: Sanga-Sanga, Kutai Kartanegara, East Kalimantan

• Type of license: IUPOP

• Expiry date: IUPOP effective until 2023 and can be renewed for

another 10 years

• Production commencement: August 2007

• 2012 production: 1 MM tonnes

• Mining consultant: PT SMG Consultants

IM: Coal Concession Overview

IM

TMU

Overview

Operations

Marketing

• Historically sold approximately 50% of its annual production through

short-term (one year or shorter) contracts with coal trading companies

– Clients include Glencore, Flame, Peabody, Dragon, Aempire

• The remainder are sold on the spot market

• Currently, IM sells coal to buyers based on fixed priced contracts up to

one year, backed with pre-determined cash prepayments

IM

Jetty

Note:

1. Calorific value

ABN

51

• Current production capacity (31 December 2012):

– Crusher: 1.4 MM tons p.a.

• Produces one variety of blended thermal coal “Trisensa-

47”, with marketed CV(1) of 4,700 kcal / kg GAR

– May produce additional varieties of blended thermal

coal in the future

• Area: 3,414 ha

• Location: Loa Janan, Muara Jawa and Sanga-Sanga,

Kutai Kartanegara, East Kalimantan

• Type of license: IUPOP

• Expiry date: 14 December 2023

• Commencement of production: October 2011

• 2012 coal production: ~257,000 tons

• Mining consultant: Marston & Marston

TMU: Coal Concession Overview

Overview

Operations & Marketing

Note:

1. Calorific value

Kutai Energi haul

road and jetty

(17 km)

IM

ABN

TMU

Sungai Sangasanga

Sungai Dondang

Pulau Seribu

Jetty KE

Completed haul road

to ABN and IM (25 km)