1q12 disclosure and results

TRANSCRIPT

1

Earnings Release | Conference Call – 1Q12 May 15th 2012

2

Agenda

Ricardo Ribeiro

Vice President

Carlos Wollenweber

CFO | IR

1Q12 and Operating

Highlights

Financial Highlights

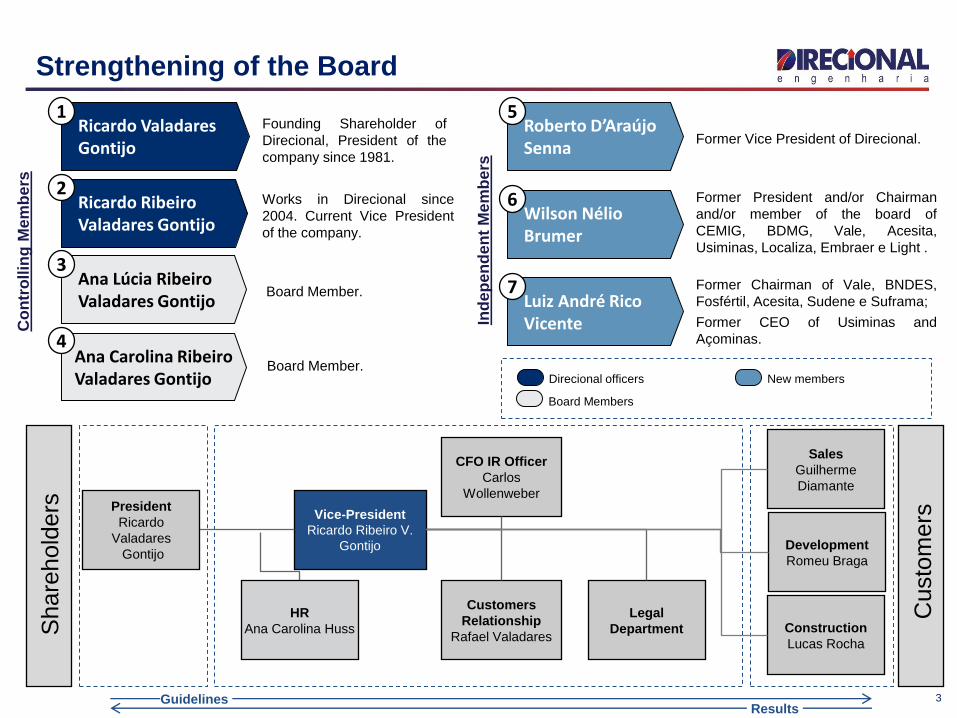

Strengthening of the Board

3

Co

ntr

ollin

g M

em

be

rs

Ind

ep

en

de

nt

Me

mb

ers

Ricardo Valadares Gontijo

Founding Shareholder of

Direcional, President of the

company since 1981.

Works in Direcional since

2004. Current Vice President

of the company.

Former Vice President of Direcional.

Former President and/or Chairman

and/or member of the board of

CEMIG, BDMG, Vale, Acesita,

Usiminas, Localiza, Embraer e Light .

Former Chairman of Vale, BNDES,

Fosfértil, Acesita, Sudene e Suframa;

Former CEO of Usiminas and

Açominas.

Vice-President

Ricardo Ribeiro V.

Gontijo

Guidelines

Share

hold

ers

Custo

mers

CFO IR Officer

Carlos

Wollenweber

Legal

Department

HR

Ana Carolina Huss

Customers

Relationship

Rafael Valadares Construction

Lucas Rocha

President

Ricardo

Valadares

Gontijo

Sales

Guilherme

Diamante

Development

Romeu Braga

Board Member.

Board Member.

Ricardo Ribeiro Valadares Gontijo

Ana Lúcia Ribeiro Valadares Gontijo

Ana Carolina Ribeiro Valadares Gontijo

1

2

3

4

Wilson Nélio Brumer

Luiz André Rico Vicente

Roberto D’Araújo Senna

5

6

7

Direcional officers New members

Board Members

Results

Main Figures

4

1. Adjusted by non-cash expenses (Stock-Options Program).

1Q12 4Q11

Launched PSV% Direcional

R$ million 143 428

Contracted PSV% Direcional

R$ million 133 367

Sales Over Supply (VSO) % PSV 16.1% 31.8%

Net Revenues R$ million 327 296

Adjusted Net Income¹ R$ million 54 48

Adjusted Net Margin¹ % 16.6% 16.2%

5

Operating Highlights

Launches

Sales

Delivered Units

Land Bank

Inventory

Operating Highlights Ricardo Ribeiro

Vice President

6

Launches

Launched PSV

(BRL million)

Launched PSV – Track Record

(BRL million)

143223

1,447

1Q12 1Q11 2011

793

522

131

2010

1,067

686

380

-36%

+36%

143

783710

176

CAGR +69%

1Q12 2011

1,447

1,316

131

2010

1,067

2009 2008 2007

Development

MCMV 1st Layer

Project Acquisition Launched PSV

Project Acquisition

Total

(BRL'000)

% Direcional

(BRL'000)

1 One Hotels By Caesar Business January Belo Horizonte - MG 45,918 45,872 211 211 Commercial

2 Total Ville Manaus - Liberdade March Manaus - AM 37,700 37,662 464 3,848 RET1

3 Setor Total Ville - 8th Phase March Santa Maria - DF 59,720 59,714 416 4,672 Low-Income

Total 143,338 143,248 1,091 8,731

# of Units

Launched

Total Units

(All Phases)Segment1Q12 Projects Date City - State

PSV

MG

Launches Breakdown

7

DF

AM

30%29%

63%

32%

7%8%1%

1Q11

29%

2011

16%

2010

5%

40%

7%

36%

28%

1Q12

68%

Launches by Segment

(% PSV)

Launches by Region

(% PSV)

21% 22%42%

9%

1Q12

26%

32%

1Q11

44%

34%

2011

61%

30%

2010

49%

30%

North Southeast Midwest

MCMV 1st Layer

Low-Income

Medium

Upper-Midde

Commercial

Setor Total Ville – 8ª Etapa

Total Ville Manaus – Liberdade

One Hotels By Caesar Business

Sales

Sales by Segment

(BRL million)

Sales Track Record

(BRL million)

133175 -24%

1,230 +19%

1Q12 1Q11 2011

619

522

89

2010

1,037

657

380

Development

MCMV 1st Layer

Project Acquisition

133

1,037

661

441

127

CAGR +76%

1Q12 2011

1,230

1,141

89

2010 2009 2008 2007

PSV Launched

Project Acquisition

8

20% 26%

52% 41%

13%10%

1Q12

42%

7%

1Q11

36%

9% 3%

2011

46%

18%

6% 4%

2010

37%

30%

MCMV 1st Layer

Low-Income

Medium

Upper-Midde

Commercial

Sales by Economic Segment

(% PSV)

Sales by Region

(% PSV)

19% 24%

52%

42%

7%

1Q11

32%

44%

2011

66%

26%

9%

2010

46%

34%

1Q12

North

Southest

Midwest

9

Sales Speed

1Q12

16.1%

16.1%

4Q11

31.8%

18.5%

3Q11

16.0%

2Q11

18.5%

1Q11

22.1%

22.1%

36.7%

With MCMV 1st Layer projects

Without MCMV 1st Layer projects

Sales-Over-Supply Ratio (VSO)

(In total PSV - %)

1Q11 83% 48% 21% 9%

3%

2%

2Q11 74% 20% 20% 18% 16%

3Q11 94% 90%

2%

2% 4Q11 91% 85% 6%

1Q12 10%

3M 6M 9M 12M 15M

10%

9%

19%

1Q12

4Q11 28%

3Q11

6%

2Q11

25% 1Q11

2% 2010

<2010

Sales by Period of Launching 1Q12

(% PSV – Ex MCMV 1st Layer)

Sales Speed

(% Units)

62% of sales in the 1Q12 refer to sales of units launched

over the last 6 months;

19% of sold PSV refers to units launched before 2010.

10

Delivered Projects – 1Q12

Delivered Projects

Total

(BRL'000)

% Direcional

(BRL'000)

1 Weekend Club Ponta Negra February Manaus - AM 90,960 72,768 427 Medium

2 Total Ville Manaus - Harmonia February Manaus - AM 50,050 50,000 512 Low-Income

3 Riviera Residencial Clube February Porto Velho - RO 31,800 25,440 82 Upper-Middle

4 Total Ville Bella Città - Salinas March Marituba - PA 61,875 61,869 598 Low-Income

Total 234,685 210,077 1,619

Delivered Projects - 1Q12 Date City - State

PSV# of Units

DeliveredSegment

Total Ville Manaus – Harmonia – AM (PSV R$ 50.0 MN) Total Ville Bella Città – Salinas – PA (PSV R$ 61.9 MN)Riviera Residencial Clube – RO (PSV R$ 25.4 MN)Weekend Club Ponta Negra – AM (PSV R$ 72.8 MN)

11

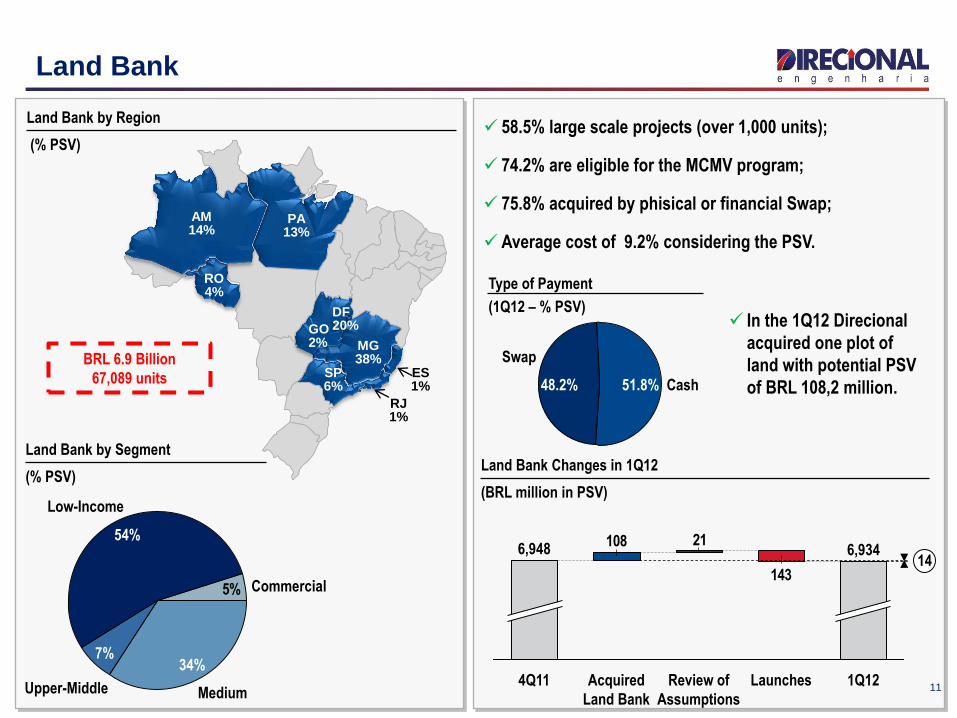

Land Bank

58.5% large scale projects (over 1,000 units);

74.2% are eligible for the MCMV program;

75.8% acquired by phisical or financial Swap;

Average cost of 9.2% considering the PSV.

BRL 6.9 Billion

67,089 units

Land Bank by Segment

(% PSV) Land Bank Changes in 1Q12

(BRL million in PSV)

143

211086,934

1Q12 Launches Review of

Assumptions

Acquired

Land Bank

4Q11

6,948 14

Land Bank by Region

(% PSV)

In the 1Q12 Direcional

acquired one plot of

land with potential PSV

of BRL 108,2 million.

Type of Payment

(1Q12 – % PSV)

ES 1%

AM 14%

MG 38%

RO 4%

SP 6%

PA 13%

DF 20%

RJ 1%

GO 2%

Swap

48.2% Cash 51.8%

5%

Low-Income

54%

Upper-Middle

7%

Medium

34%

Commercial

12

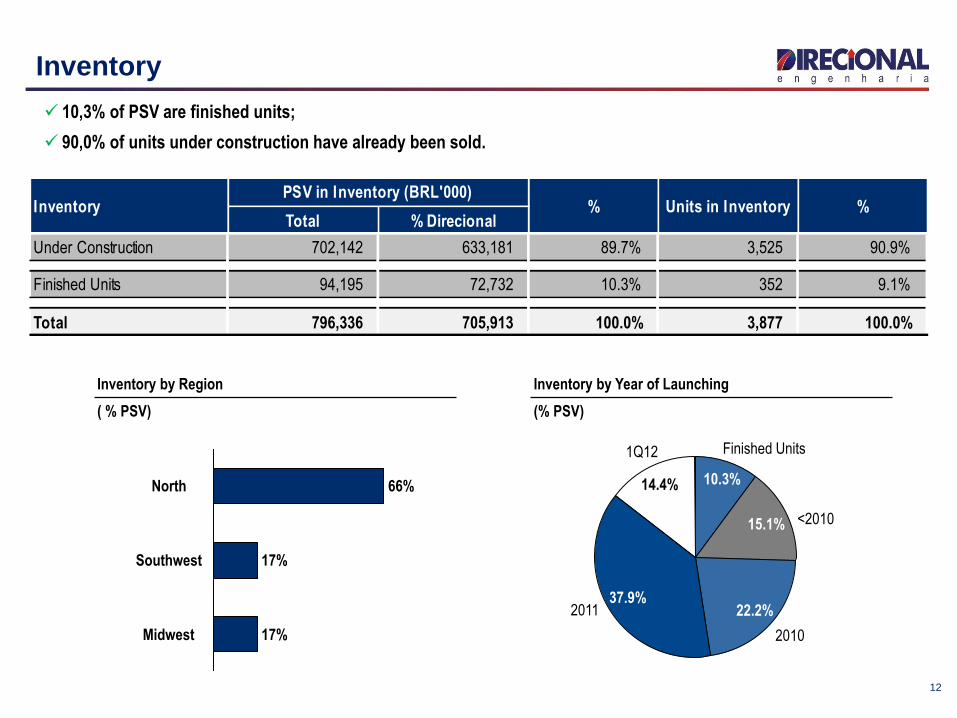

Inventory

10,3% of PSV are finished units;

90,0% of units under construction have already been sold.

15.1%

2011

<2010

14.4%

1Q12

37.9%

10.3%

Finished Units

22.2%

2010 Midwest 17%

Southwest 17%

66% North

Inventory by Region

( % PSV)

Inventory by Year of Launching

(% PSV)

Total % Direcional

Under Construction 702,142 633,181 89.7% 3,525 90.9%

Finished Units 94,195 72,732 10.3% 352 9.1%

Total 796,336 705,913 100.0% 3,877 100.0%

%InventoryPSV in Inventory (BRL'000)

% Units in Inventory

13

Financial Highlights

Financial Highlights

Capital Structure

Cash Burn

Deferred Results

DIRR3 Stock Analysis

Financial Highlights Carlos Wollenweber

CFO | IR

14

Financial Highlights

782

327296234

+40%

+11%

1,072

+37%

2011 2010 1Q12 4Q11 1Q11

CAGR +80%

1Q12

327

2011

1,072

2010

782

2009

378

2008

263

2007

102

Net Revenue

(BRL million)

Net Revenue – Track Record

(BRL million)

2115

+130%

2011

269

25%

+19% 117

15%

1Q12 2010

98

29%

4Q11

82

27%

3Q11

72

24%

2Q11

58

23%

1Q11

57

24%

4Q10

48

18%

3Q10

33

15%

2Q10

12%

1Q10

10%

Revenue from Services – Track Record

(BRL million)

MCMV 1st Layer

97.2% Brokerage Fee

1,4%

Management

1.3%

Breakdown of Revenue from Services

(in 1Q12 - %)

Service Revenue % of Net Revenue

1Q11 1Q12 D %

Gross Revenue 239 339 42%

Development 182 241 32%

Services 57 98 73%

15

Gross Revenue – Track Record

(BRL million)

1Q12

339

Development

Growth

59

Services

Growth

41

1Q11

239

71% 67%55% 51% 49%

1Q12

51%

4Q11

49%

3Q11

45%

2Q11

33%

1Q11

29%

Industrial Construction Method²

Traditional Construction Method

Units Under Construction by Construction Method

(% of Units)

+37%

+9%

332

+27%

2011

301

32

31.0%

2010

261

248

13

33.4%

1Q12

99

88

30.2%

4Q11

90

83

30.5%

1Q11

72

66

30.8%

11 8 6

Gross Profit

Interest Capitalised in costs

Adjusted Gross Margin

Gross Profit and Gross Margin

(BRL million) Adjusted EBITDA¹

(BRL million)

Financial Highlights

1. Gross Margin Ex-SFH: excluding interest expenses; 2. Aluminum mold and concrete walls method

41% of the

total Gross

Revenue

Growth

243202

716458

+23%

+11%

+21%

2011

22.7%

2010

25.8%

1Q12

21.6%

4Q11

21.6%

1Q11

24.7%

Adjusted EBITDA Adjusted EBITDA Margin

16

Financial Highlights

199176

544851+14%

+13%

2011

18.5%

2010

22.6%

1Q12

16.6%

4Q11

16.2%

1Q11

21.7%

+7%

CAGR +74%

1Q12

54

16.6%

2011

199

18.5%

2010

176

22.6%

2009

85

22.5%

2008

64

24.5%

2007

22

21.1%

Adjusted Net Income¹

(BRL million)

Adjusted Net Income - Track Record

(BRL million)

Adjusted Net Income¹ Adjusted Net Margin¹ Adjusted Net Income¹ Adjusted Net Margin¹

Adjusted¹ G&A

(BRL million)

Sales Expenses

(BRL million)

2423

171617

7.3%6.5%7.8%7.1%6.9%6.6%

1Q12 4Q11

19

16

3

3Q11 2Q11 1Q11 4Q10

99

67

56

2.6%3.1%2.0%3.1%2.1%2.3%

1Q12 4Q11 3Q11 2Q11 1Q11 4Q10

Sales Expenses % Net Revenue

Accounting adjustments

Adjusted¹ G&A % Net Revenue

1. Adjusted by non-cash expenses (Stock-Options Program).

Cash and Debt 1Q12 4Q11 1Q11 D % D %

(BRL'000) (a) (b) (c) (a/b) (a/c)

Loans and Financing 556,575 473,152 348,307 17.6% 59.8%

SFH 492,754 407,563 282,674 20.9% 74.3%

Receivables Securitization 30,080 31,847 36,429 -5.5% -17.4%

FINAME and others 13,707 13,076 8,611 4.8% 59.2%

Working Capital 20,034 20,666 20,593 -3.1% -2.7%

Cash and Cash Equivalents 364,088 351,112 355,410 3.7% 2.4%

Net debt 192,487 122,040 -7,103 57.7% n/a

Net debt / Equity 14.8% 9.9% -0.6%

17

Capital Structure

Net Debt

192

Cash and Cash

Equivalent

364

Net Debt

Without SFH

-300

Gross Debt

557

SFH

493

64

Indebtedness

(BRL million)

SFH

93.6%

FINAME and others

2.6%

Working Capital

3.8%

Loans and Financing Ex-Securitization

(% Loans and Financing)

1. Cash Burn: measured by the variation of the net debt, less capital increases, dividends and share repurchase plan.

18

Cash Burn

+12%

1Q12

70

4Q11 4Q09

33

3Q09

22

2Q09

25

1Q09

15

86

2Q10

55

1Q10

41 28

3Q11

52

2Q11

34

1Q11

63

4Q10

101

3Q10

Cash Burn¹

(BRL million)

D Accounts

receivable from

concluded units

-6

Cash Burn

176

Cash Burn

70

-33

Adjusted

Cash Burn

103

D Accounts

receivable from

concluded units

Cash Burn vs D Accounts receivable from concluded units

(BRL million)

2011 1Q12

-38%

2011

176

2010

283

19

Deferred Results

Schedule of Deferred Results

(%)

1%

34%

65%

2014 2013 2012

Deferred Results

(BRL million)

-1%

553 560

334

226

1Q11

382

+45%

1Q12

343

210

4Q11

326

57

Development

MCMV 1st Layer projects

Consolidated Deferred Results (BRL'000) 1Q12 4Q11 1Q11 D % D %

(a) (b) (c) (a/b) (a/c)

Consolidated Deferred results (1+2) 552,655 560,382 382,339 -1.4% 44.5%

Deferred revenues 1,434,378 1,482,460 967,047 -3.2% 48.3%

Deferred results - Margin 38.5% 37.8% 39.5% 0.7 p.p. -1.0 p.p.

Deferred results - Development (1) 342,617 334,100 325,687 2.5% 5.2%

Deferred revenues 815,321 775,531 762,873 5.1% 6.9%

Deferred results - Margin 42.0% 43.1% 42.7% -1.1 p.p. -0.7 p.p.

Deferred results - MCMV 1st Layer projects (2) 210,038 226,282 56,652 -7.2% 270.8%

Deferred revenues 619,058 706,928 204,174 -12.4% 203.2%

Deferred results - Margin 33.9% 32.0% 27.7% 1.9 p.p. 6.2 p.p.

20

Shares Performance Since IPO

0

20

40

60

80

100

120

140

160

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

19

-no

v-0

9

9-d

ez-0

9

30

-dez

-09

20

-jan

-10

9-f

ev-

10

2-m

ar-1

0

19

-mar

-10

8-a

br-

10

28

-ab

r-1

0

17

-mai

-10

7-j

un

-10

25

-ju

n-1

0

15

-ju

l-1

0

5-a

go-1

0

27

-ago

-10

24

-set

-10

15

-ou

t-1

0

4-n

ov-

10

26

-no

v-1

0

17

-dez

-10

7-j

an-1

1

27

-jan

-11

15

-fe

v-1

1

4-m

ar-1

1

25

-mar

-11

13

-ab

r-1

1

4-m

ai-1

1

23

-mai

-11

9-j

un

-11

29

-ju

n-1

1

18

-ju

l-1

1

4-a

go-1

1

23

-ago

-11

12

-set

-11

29

-set

-11

19

-ou

t-1

1

8-n

ov-

11

28

-no

v-1

1

15

-dez

-11

4-j

an-1

2

23

-jan

-12

10

-fe

v-1

2

2-m

ar-1

2

3/2

1/2

01

2

4/1

0/2

01

2

4/2

7/2

01

2

Pre

ço d

a A

ção

Vo

lum

e (

R$

mil)

Volume (BRL '000)

0

20

40

60

80

100

120

140

160

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

18

-No

v-0

9

8-D

ec-0

9

29

-De

c-0

9

19

-Jan

-10

8-F

eb

-10

1-M

ar-1

0

18

-Mar

-10

7-A

pr-

10

27

-Ap

r-1

0

14

-May

-10

4-J

un

-10

24

-Ju

n-1

0

14

-Ju

l-1

0

4-A

ug-

10

25

-Au

g-1

0

23

-Se

p-1

0

14

-Oct

-10

3-N

ov-

10

25

-No

v-1

0

16

-De

c-1

0

6-J

an-1

1

26

-Jan

-11

14

-Fe

b-1

1

3-M

ar-1

1

24

-Mar

-11

12

-Ap

r-1

1

3-M

ay-1

1

20

-May

-11

8-J

un

-11

28

-Ju

n-1

1

15

-Ju

l-1

1

3-A

ug-

11

22

-Au

g-1

1

9-S

ep

-11

28

-Se

p-1

1

18

-Oct

-11

7-N

ov-

11

25

-No

v-1

1

14

-De

c-1

1

3-J

an-1

2

20

-Jan

-12

9-F

eb

-12

1-M

ar-1

2

20

-Mar

-12

9-A

pr-

12

26

-Ap

r-1

2

Sto

ck P

erfo

rman

ce

Vo

lum

e (B

RL

'00

0)

Average Volume (21 days) Ibovespa IMOB Direcional

21

Disclosure

This presentation contains certain forward-looking statements concerning the business prospects,

projections of operating and financial results and growth potential of the Company, which are based on

management’s current expectations and estimates of the future performance of the Company. Although the

Company believes such forward-looking statements are based on reasonable assumptions, it can give no

assurance that its expectations will be achieved. Expectations and estimates that are based on the future

prospects of the Company are highly dependent upon market behavior, Brazil’s political and economic

situation, existing and future regulations of the industry and international markets and, therefore, are

subject to changes outside the Company’s and management’s control. The Company undertakes no

obligation to update any information contained herein or to revise any forward-looking statement as a result

of new information, future events or other information.

22

Contacts

Carlos Wollenweber CFO | IR Officer

Paulo Sousa IR Analyst

www.direcional.com.b/ri

(55 31) 3214-6200

(55 31) 3214-6450