1.what factors influence your credit score? 2.what are the advantages and disadvantages of credit?...

TRANSCRIPT

1. What factors influence your credit score?2. What are the advantages and disadvantages of credit?3. As a borrower how are you legally protected?4. How do the C’s of credit effect your ability to get a loan?

(Credit , open/revolving credit, closed-end/installment credit, cosign, capacity, character, collateral, conditions, loan term, grace period, APR, finance charges, annual fee, credit limit, credit report, credit score, credit bureaus,

FICO score, Bankruptcy, chapter 7 & 13, ID theft, Truth in Lending Act)

Understanding Credit

Credit: arrangement to receive cash, goods, or services now and pay for them in the future

68% of teens have never discussed credit responsibility

84% of college students have at least 1

17% of college students pay there credit card off in full each month

Credit Benefits

• Emergencies• Safety & Convenience• Bonus & Rewards• Buyer Protection• Build Credit• Immediate

Gratification

• Interest

• Overspending

• Debt

• Identity Theft

Credit Risks

Building Good Credit

Paying bills on time Responsibly using credit Having limited-no debt Limited lines of credit Responsible spending Correct credit mistakes

Paying bills late Criminal record Lots of debt Too many lines of credit (cards/loans)

Bankruptcy Defaulting on a loan Exceeding credit limits

Hurting your Credit

http://www.investopedia.com/video/play/5-Easy-Ways-To-Improve-Your-Credit#axzz1cCDFWuQy

Types of CreditCharacteristics Closed-Ended

Installment CreditOpen-ended credit (Revolving credit)

Definition A one-time loan Credit is extended in advance

Purpose of the loan Specified in application

May be used for a variety of purposes

Payments Specified number of equal payments

Vary depending upon amount charged

Loan amount Agreed upon during the application process

May be increased for responsible consumers

Examples Mortgage, Automobile Loan

Credit Card

The C’s of Credit:

Capacity- Ability to Repay the Debt? Current income vs. expenses/debt- Cash flow

Collateral- Assets of value to secure a loan Home or car that will help you secure a loan

Character- Previous record of credit use Credit score & previous credit history Past default or bankruptcies?

Conditions- Principal & Interest How much are you borrowing, for what, & at what interest rate

Closed-end Credit

Term: Length of time you will repay a loan (Loan)

Debt: The entire amount of money you owe to lenders

APR: (Annual Percentage Rate)

Origination Fee: Cost to set up a loan

*The quicker you pay it off the higher the monthly payments, but the less overall you will pay.

Car http://www.bankrate.com/calculators/auto/early-payment-payoff-calculator.aspx

Home: http://www.mortgage-calc.com/mortgage/simple.html

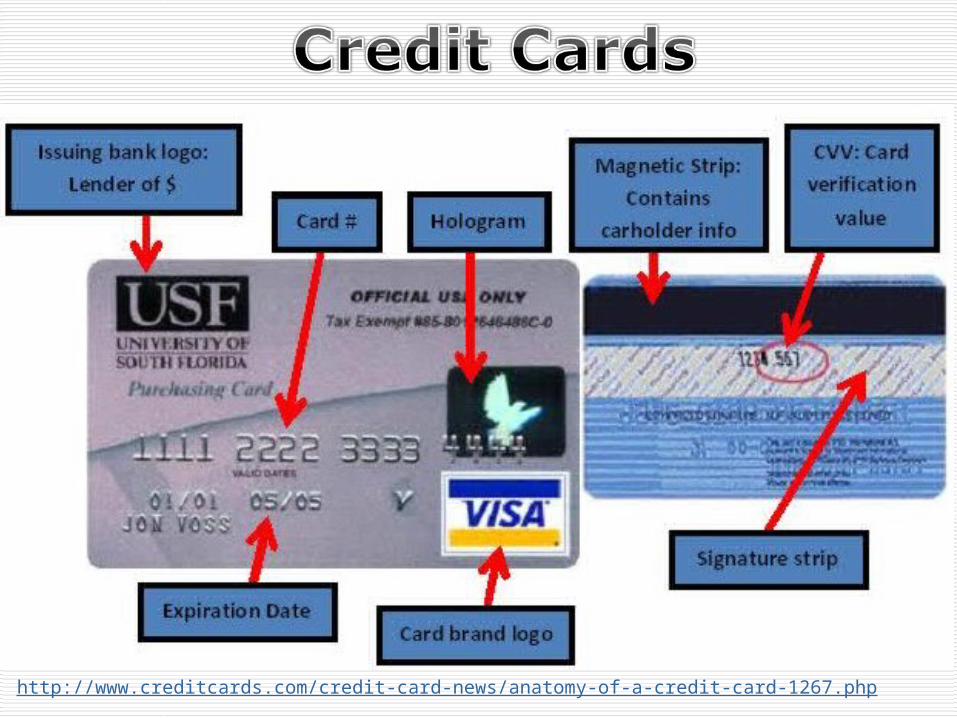

http://www.creditcards.com/credit-card-news/anatomy-of-a-credit-card-1267.php

Credit Cards

Credit Limit: Maximum amount of credit a lender will extend to a customer

Grace Period: Length of time you have to pay a line of credit before you start

accumulating finance charges.

Annual Fee: Yearly charge for privilege of using credit

Finance Charge: Total dollar cost to use credit

Pay in full each month within grace period and it costs you nothing.

Cash Advance: A loan taken out on a line of credit or a credit card • May cost a flat rate ($10) or %, whichever is greater• Don’t forget ATM fees, no grace period, & higher interest rateBalance Transfer: Move unpaid credit card debt from one card to another• May charge cost or fee for transfer• Typically has higher APR than purchases

Credit Cards

ExistingVISA$2,00024% APR

NewDiscover$2,00014% Intro APR

Interest Rates and Interest Charges

Annual Percentage Rate (APR) for

Purchases

0% introductory APR for 18 monthsAfter that, your APR will be 11.99%, 16.99%, or 21.99%, based

on your creditworthiness.

APR for Balance Transfers

0% introductory APR for 18 months After that, your APR will be 11.99%, 16.99%, or 21.99%, based on your creditworthiness.

APR for Cash Advances

25.24%

Penalty APR and When it Applies

Up to 29.99%, based on your creditworthiness. This APR may be applied to your account if you:

(1) Make a late payment or (2) Make a payment that is returned

Paying Interest Your due date is at least 23 days after the close of each billing cycle. We will begin charging interest on cash advances and

balance transfers on the transaction date.

Minimum Interest Charge

If you are charged interest, the charge will be no less than 50 cents.

Fees

Annual Fee None

Transaction Fees -----

Balance Transfer Either $5 or 3% of the amount of each transfer,

whichever is greater.

Cash Advance Either $10 or 5% of the amount of each cash advance,

whichever is greater.

Foreign Purchase Transaction

3% of each purchase transaction in US dollars.

Penalty Fees

Late Payment Up to $35

Returned Payment

Up to $35

FEES

G6

Due Date: The day by which the company requires at least the minimum payment

Payments / credits: Amount applied toward balance (amount paid off)

Total Credit Limit: Total amt. you have to spend on your credit card

Total Credit Available: Amt. still available on card (Total credit limit- purchases)

Minimum Payment Due: The minimum amount that must be paid to avoid

defaulthttp://www.bankrate.com/calculators/managing-debt/minimum-payment-calculator.aspx

Understanding the Bill

MINIMUM PAYMENT PAYOFF (18% APR)

ITEM COST MIN PAYMENTTIME TO PAYOFF

TOTAL AMOUNT

PAID

TOTAL INTEREST

PAID

Bedroom Set

$3,500 $87.5019 yrs. & 10 months

$8,173.24 $4,673.24

TV $1,000 $259 yrs. & 5 months

$1,923.12 $923.12

New Balance: The total amount currently owed on a credit card

Example Statement

https://www.citicards.com/cards/wv/html/cm/know-the-rules/how-credit-cards-work/how-to-read-your-statement.html

4-C-44-C-4

• Transactions taking you over credit limit will be denied unless

• Late payment fees limited to under $25 (unless 2nd time in 6 months)

• No inactivity fees

• If under 21 must show ability to pay or have cosigner

• Credit card companies cannot solicit within 1,000 ft of college campus

• Statements must include length of time it would take to pay of balance

if paying min. amount.

New Regulations

4-C-24-C-2

Credit History: Record of borrowing and repaying loans.

Credit Report: Detailed record of credit and financial transactions.

Credit Score: Rating used by credit reporting companies to help lenders decide whether and/or how

much credit can be extended to a borrower.

The Language of Credit

http://www.investopedia.com/video/play/what-is-a-credit-score#axzz1cCDFWuQy

Credit Reports

Who can see your credit report?

Potential Creditors

Government agencies

Landlords

Insurance companies*Employers (only with written permission)

Teens – Lesson 7 - Slide 7-D

Over 50% of credit reports have errors. Most common are

1.Mistaken identity2.Fraud

If incorrect, notify in writingEXAMPLE

Your Credit

Can check once a year free from each agency

Equifax (www.equifax.com) Experian (www.experian.com) Trans Union (www.transunion.com)

Should check your credit report at least once per year to make sure there are no errors

Credit Bureau: An agency that collects information on how promptly people and businesses pay their bills.

Credit Inquiries

Not all credit inquiries are the same!Type of inquiry Soft check Hard check

Do they impact your credit score?

Not usually Yes

Examples•Individuals checking their free reports

Permission given when seeking credit•Automobile loan

Individuals should avoid too many hard credit checks at one time!

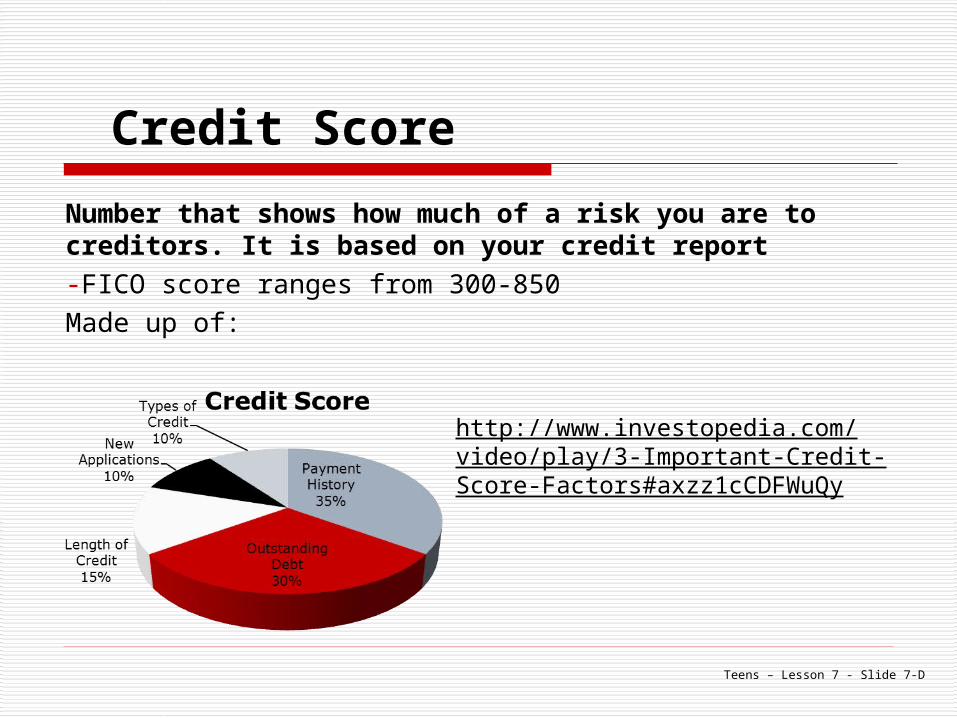

Credit Score

Number that shows how much of a risk you are to creditors. It is based on your credit report-FICO score ranges from 300-850Made up of:

Teens – Lesson 7 - Slide 7-D

http://www.investopedia.com/video/play/3-Important-Credit-Score-Factors#axzz1cCDFWuQy

Credit Score

720-850Lenders rest easier when they extend credit to people in this category. They see you as a moderate to low risk and are more likely to give you a competitive interest rate on the loans they provide.

620-719In this range, lenders still consider you a fair to good risk, but interest rates on loans provided will probably be higher. You should work to improve your score by paying your bills on time and reducing your outstanding debt.

350-619Lenders may be very wary about extending loans or credit to you if you fall into this high-risk range, so improving your score should be a priority.

Teens – Lesson 7 - Slide 7-D

Payday Loan

User writes a check to lender for amount + fee Payday loans usually for between $50 and $1000 Fees between $10 and $30 per $100 borrowed

Fees translate to an APR of 391% - 443%4

Short-term loans for small amounts. Use for emergencies only• 10 years ago almost non-existent • In 2005 loans equaled $40 Billion and $6 Billion in fees• Today there are more payday loan stores than McDonalds and Burger King restaurants in California5

How to get out of debt…. Spend less than you earn!

Stick to budget

Pay all loans- even if it is minimum

Prioritize- highest interest rate first

Look for ways to cut costs

Truth-in-Lending Act1. Lenders must disclose all costs of credit

2. Limits liability of credit card holder to $50 for unauthorized use

Fair Debt Collection Practices Act 3. Lenders may not add extra costs or harass consumers

Consumer Credit Protection Act

Handling Credit Problems

Consumer Credit Counselor Nonprofit organization that provides debt counseling services

for families and individuals with serious financial problems.

Debt Repayment Plan Reorganizes debt and sometimes includes renegotiating

terms Creditors will often accept such arrangements for partial

payment, rather than not be repaid.

Results of Overuse1. Garnishment of Wages: Money deducted from wages for money owed.

2. Repossession: Loss of property from failure to repay loan.

3. Bankruptcy: Legal process in which some or all of the assets of a debtor are distributed among the creditors because the debtor is unable to pay his or her debts. (legal process of getting out of debt)

Chapter 7: allows to erase debt, must be unemployed or low income. Must seek counseling. Keeps only exempt propertyChapter 13: allows pay back of debt with more time, court oversees repayment plan.

Top Questions To Ask Before Signing on Dotted Line……

1. Do I really need it or can it wait?2. Can I qualify for credit?3. What is the interest rate (APR)?4. Additional Fees?5. How much is the monthly payment?6. Can you afford the payment?7. What happens if payments are late?8. Is there a penalty for paying off early?9. Is it worth it?

© Family Economics & Financial Education – Revised October 2004 – Consumer Protection Unit – Identity TheftFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of

Arizona

IDENTITY THEFT occurs when someone wrongfully acquires and uses a consumer’s personal identification, credit, or account information.

Identity Theft

• The dollar loss suffered because of identity theft and consumer fraud was $1.8 billion in 2008. -- Federal Trade Commission

• 9-10 million people a year are victims of ID Theft.—FTC

• Approximately 7% of identity theft victims in 2008 were under 20 years of age. -- United States Department of Commerce

© Family Economics & Financial Education – Revised October 2004 – Consumer Protection Unit – Identity TheftFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

Name Address and Telephone Number Social Security number Driver’s license number Bank account numbers Credit card numbers Passwords Bills

Personal Identification Information Includes

© Family Economics & Financial Education – Revised October 2004 – Consumer Protection Unit – Identity TheftFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

Wallet/Purse Loss or Theft - Taken from a lost or stolen wallet/purse (most common method).

Mail and Phone - Info. is taken from mailboxes, a change of address form is completed, or personal info. is solicited by phone.

“Dumpster Diving” - Personal info. is discarded carelessly either at home or by businesses and thieves remove it from the trash.

“Insider Access” - Dishonest employees steal info. & sell it Credit Reports – A credit report containing personal information may be

obtained fraudulently.

Internet - Personal data taken off the Internet.• Phishing• Spyware• Malware

Ways Identity Thieves Acquire Information

© Family Economics & Financial Education – Revised October 2004 – Consumer Protection Unit – Identity TheftFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

Safety Tips for Shopping Online

1. Know the real deal: Get all details before buying including prices, delivery time, warranty information, and return policies.

2. Look for clues about security: Make sure the browser states “https” or “shttp”

3. Use a credit card: Credit cards are the safest way

4. Use an escrow service: An escrow service will hold a person’s money until confirmation of the product or services has been received.

5. Keep proof handy: Print and file all information in case needed later.

© Family Economics & Financial Education – Revised October 2004 – Consumer Protection Unit – Identity TheftFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

If You Are A VictimAct immediately!Keep a detailed record of correspondence and phone records.1.Contact the three major credit bureaus and request a “fraud alert.” in writing and over phone2.Close all accounts which have been tampered with or opened fraudulently.3.File a police report.4.File a complaint with the Federal Trade Commission.

© Family Economics & Financial Education – Revised October 2004 – Consumer Protection Unit – Identity TheftFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

ATM & Debit Cards, Electronic Transfers

Liability depends upon how quickly the loss is reported (Consumer Credit Protection Act). Within two days is a maximum of $50.00. Within sixty days is a maximum of $500.00. After sixty days a person may be liable for

everything. To report a loss call the financial institution and follow up in

writing. Get new bank numbers, personal identification numbers, and

passwords.

Card Liability