#20 - ethical considerations

TRANSCRIPT

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 1/36

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 2/36

Topic list1. A framework of rules

2. Management accountability

3. The ethical environment4. Ethics in organisations

5. Accountants and ethics

6. A code of ethics for accountants

7. Ethics in business

8. Ethical dilemmas

9. Resolution of ethical conflicts

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 3/36

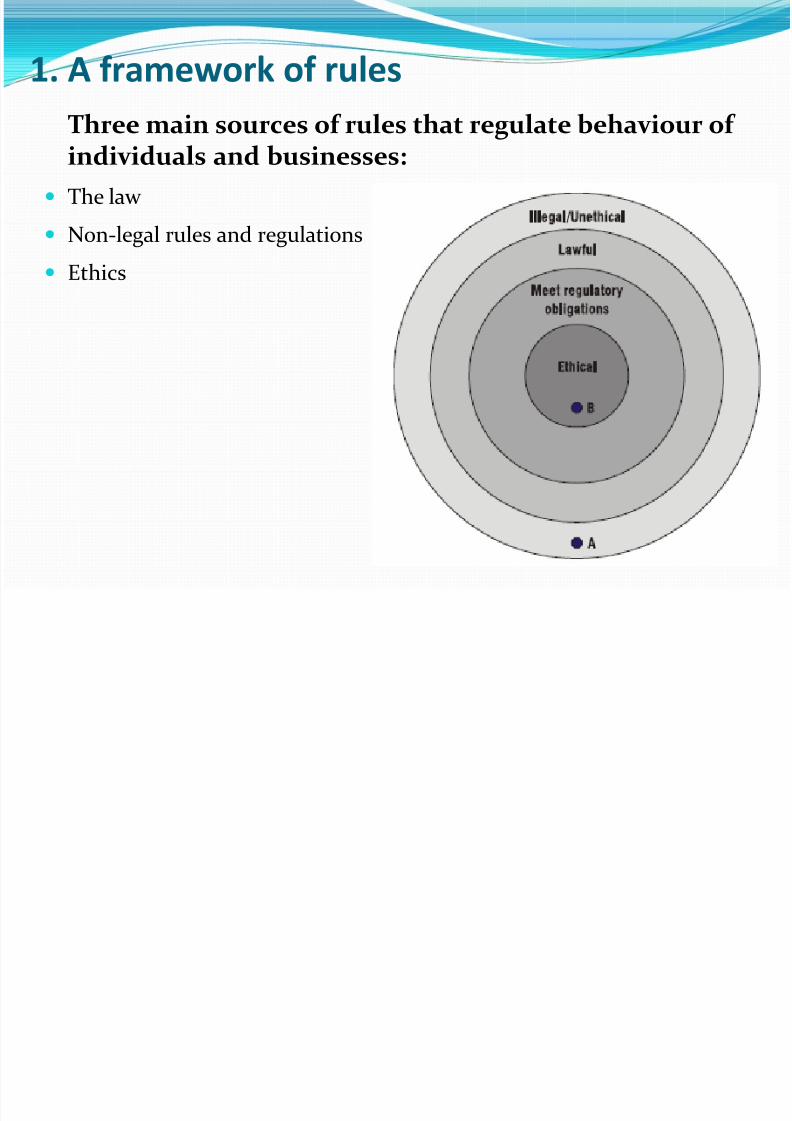

1. A framework of rules

Three main sources of rules that regulate behaviour ofindividuals and businesses:

The law

Non-legal rules and regulations

Ethics

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 4/36

1. A framework of rules

Corporate governance concepts: Fairness

Openness/ transparency

Probity/ honesty

Responsibility

Accountability

Reputation

Judgment

Integrity

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 5/36

2. Management accountability

Fiduciary responsibility Business objectives and management discretion

The stakeholder view of company objectives

The consensus theory of company objectives

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 6/36

3. The ethical environment

Ethics: a set of moral principles to guide behaviourEthical principles

The certainty of legal rules does not exist in ethical theory. Different ideasapply in different cultures

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 7/36

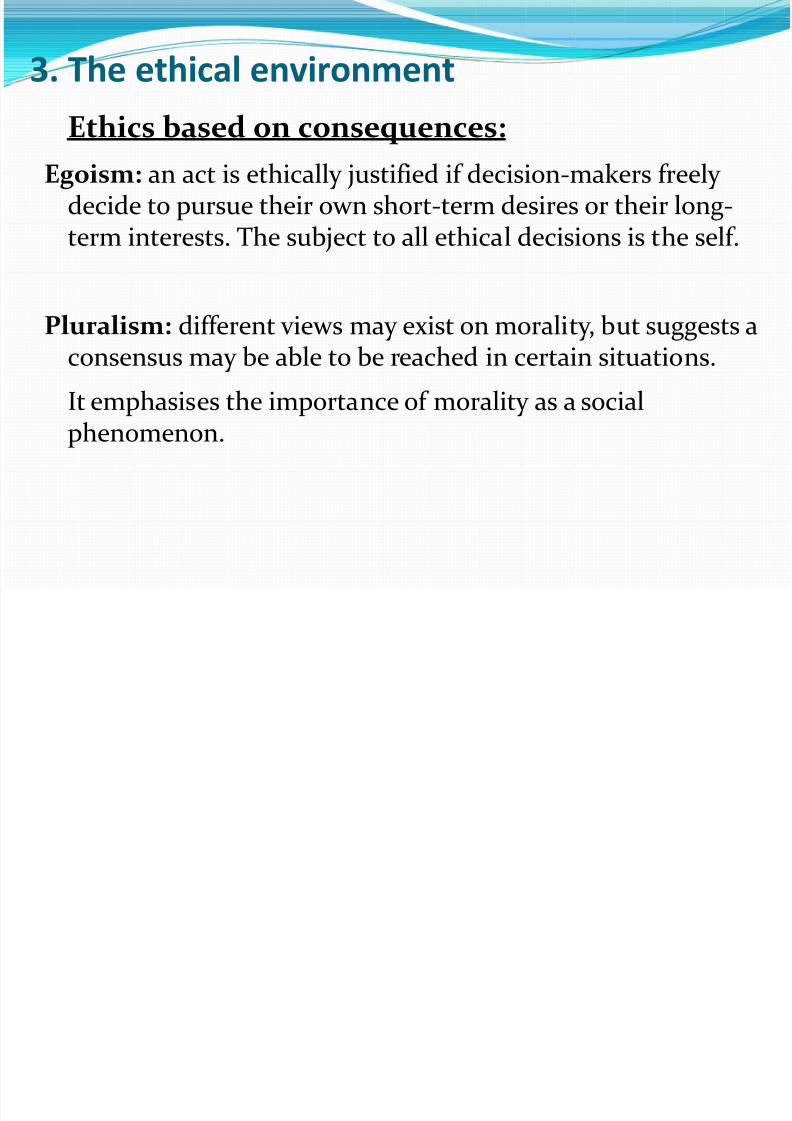

3. The ethical environment

Ethics based on consequences:Egoism: an act is ethically justified if decision-makers freely

decide to pursue their own short-term desires or their long-term interests. The subject to all ethical decisions is the self.

Pluralism: different views may exist on morality, but suggests aconsensus may be able to be reached in certain situations.

It emphasises the importance of morality as a socialphenomenon.

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 8/36

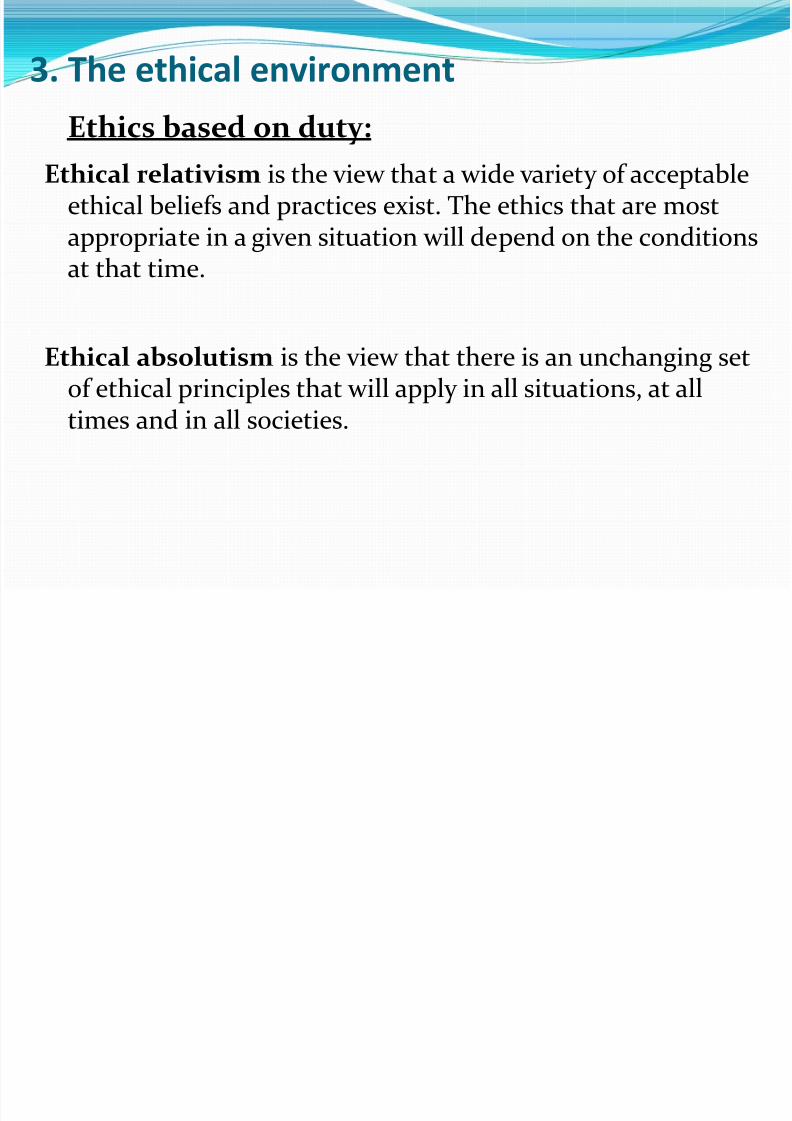

3. The ethical environment

Ethics based on duty:Ethical relativism is the view that a wide variety of acceptable

ethical beliefs and practices exist. The ethics that are mostappropriate in a given situation will depend on the conditions

at that time.

Ethical absolutism is the view that there is an unchanging setof ethical principles that will apply in all situations, at all

times and in all societies.

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 9/36

3. The ethical environment

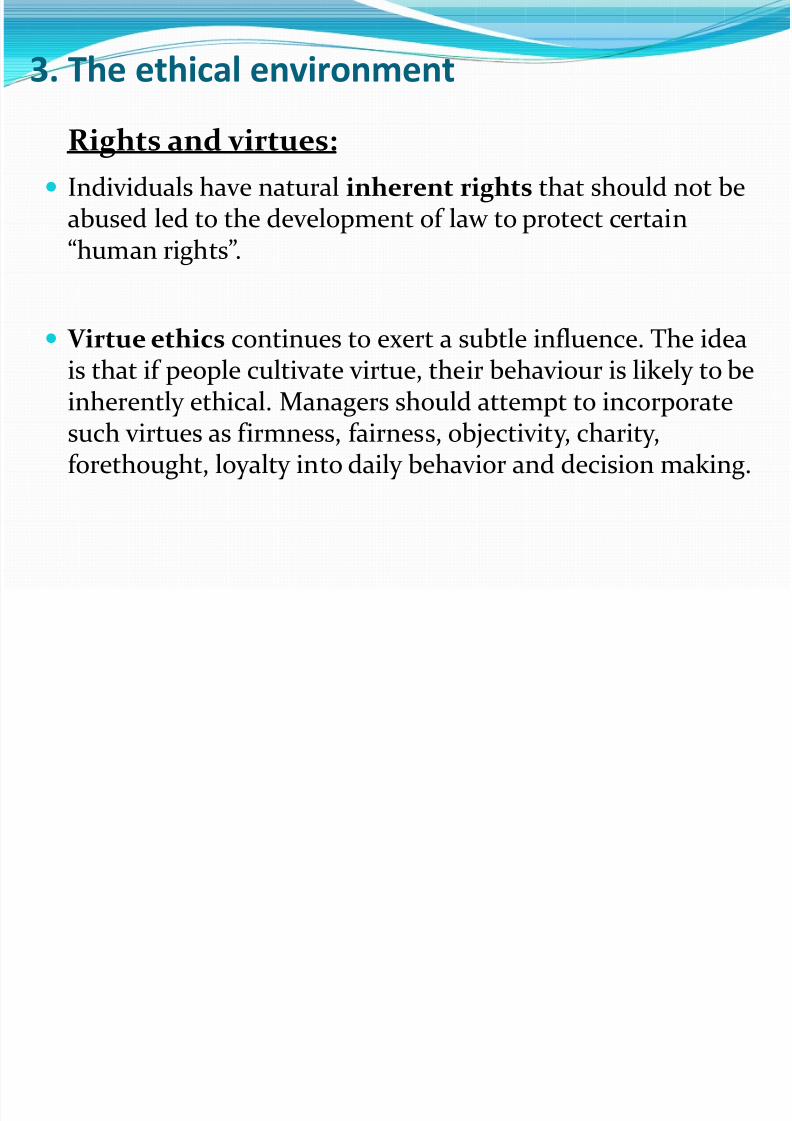

Rights and virtues: Individuals have natural inherent rights that should not be

abused led to the development of law to protect certain“human rights”.

Virtue ethics continues to exert a subtle influence. The ideais that if people cultivate virtue, their behaviour is likely to be

inherently ethical. Managers should attempt to incorporatesuch virtues as firmness, fairness, objectivity, charity,forethought, loyalty into daily behavior and decision making.

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 10/36

3. The ethical environment

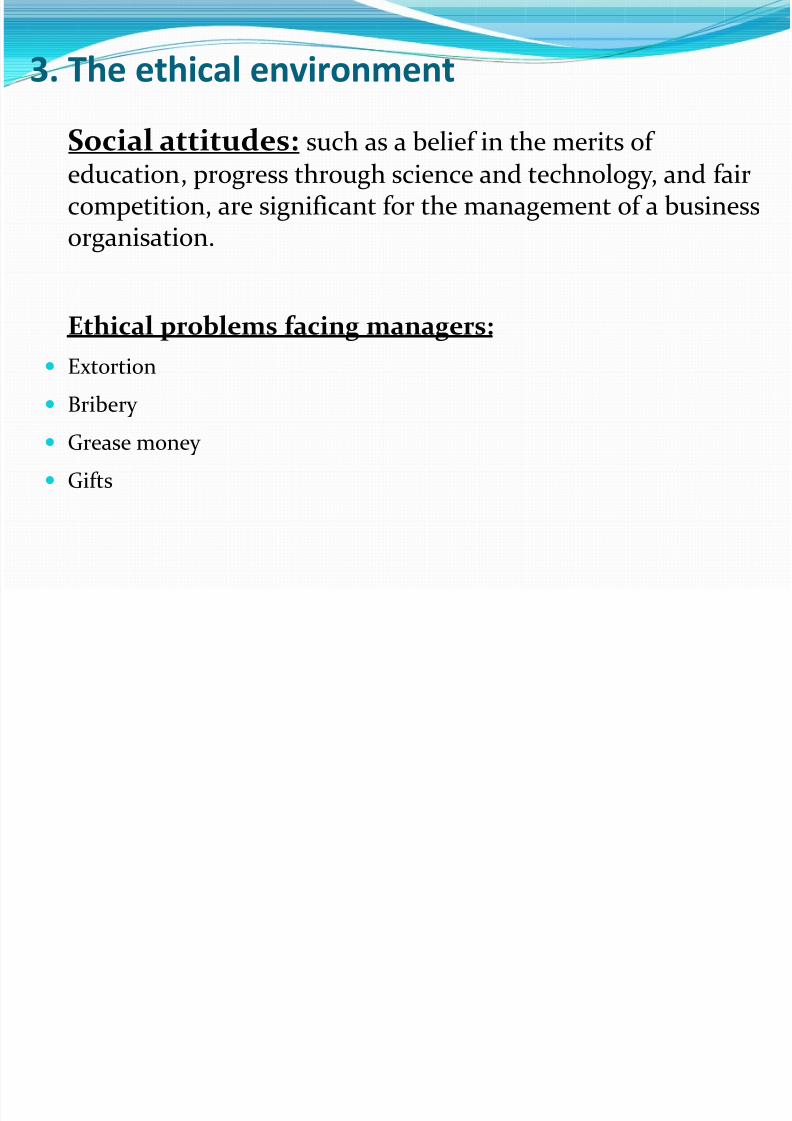

Social attitudes: such as a belief in the merits ofeducation, progress through science and technology, and faircompetition, are significant for the management of a businessorganisation.

Ethical problems facing managers:

Extortion

Bribery Grease money

Gifts

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 11/36

3. The ethical environment

Social responsibility and businesses:Social responsibility action is likely to have an adverse effect onshareholders' interests.

Additional costs such as those of environmental monitoring

Reduced revenues as a result of refusing to supply certain customers

Diversion of employee effort away from profitable activities

Diversion of funds into social projects

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 12/36

3. The ethical environment

Specific environmental responsibilities:Businesses are widely regarded as having a duty to safeguard the naturalenvironment. There are six areas for action

Environmental auditing

Economic action: charges for environmental damage should be made internally togive managers an incentive to avoid it.

Accounting action: a separate set of accounts incorporating shadow prices torepresent environmental costs is prepared.

Ecological approach: aspects of the business such as a product or a location are

selected for examination to ascertain their environmental impact.

Production is managed to minimise inputs of materials and energy.

Quality management is applied using the principle of continuous improvementin environmental performance.

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 13/36

4. Ethics in organisations

Ethics in organisations: Personal ethics

Professional ethics

Organisation cultures

Organisation systems

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 14/36

4. Ethics in organisations

Leadership practices and ethics: Openness

Trust

Honesty

Respect

Empowerment

Accountability

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 15/36

4. Ethics in organisations

The seven principles of Public life: individualsemployed in the public sector must follow:

Selflessness

Integrity

Objectivity

Accountability

Openness

Honesty Leadership

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 16/36

4. Ethics in organisations

Two approaches to managing ethics: Compliance-based approach: ensure that the company acts within the

letter of the law

Integrity-based programmes:

combines a concern for the law with an emphasis on managerialresponsibility for ethical behaviour

Whistleblowing is the disclosure by an employee of illegal, immoral orillegitimate practices on the part of the organisation

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 17/36

5. Accountants and ethics

As an accountant, your values and attitudes flow througheverything you do professionally.

They contribute to the trust the wider community puts in theprofession and the perception it has of it.

Guidance is usually known as a ‘Code of ethics’ or ‘Code ofconduct’

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 18/36

6. A code of ethics for accountants

IFAC and the ACCA: To enable the development of high standards, IFAC’s ethics

committee established a code of ethics.

The code indicates a minimum level of conduct that allaccountants must adhere.

As a member of IFAC, ACCA released its own code of ethics,designed to align to the IFAC code.

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 19/36

6. A code of ethics for accountants

Fundamental principles of the ACCA Code of Ethics andConduct:

Integrity

Confidentiality

Objectivity

Professional behaviour

Professional competence and due care

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 20/36

6. A code of ethics for accountants

Personal qualities expected of an accountant: Personal qualities

Professional qualities

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 21/36

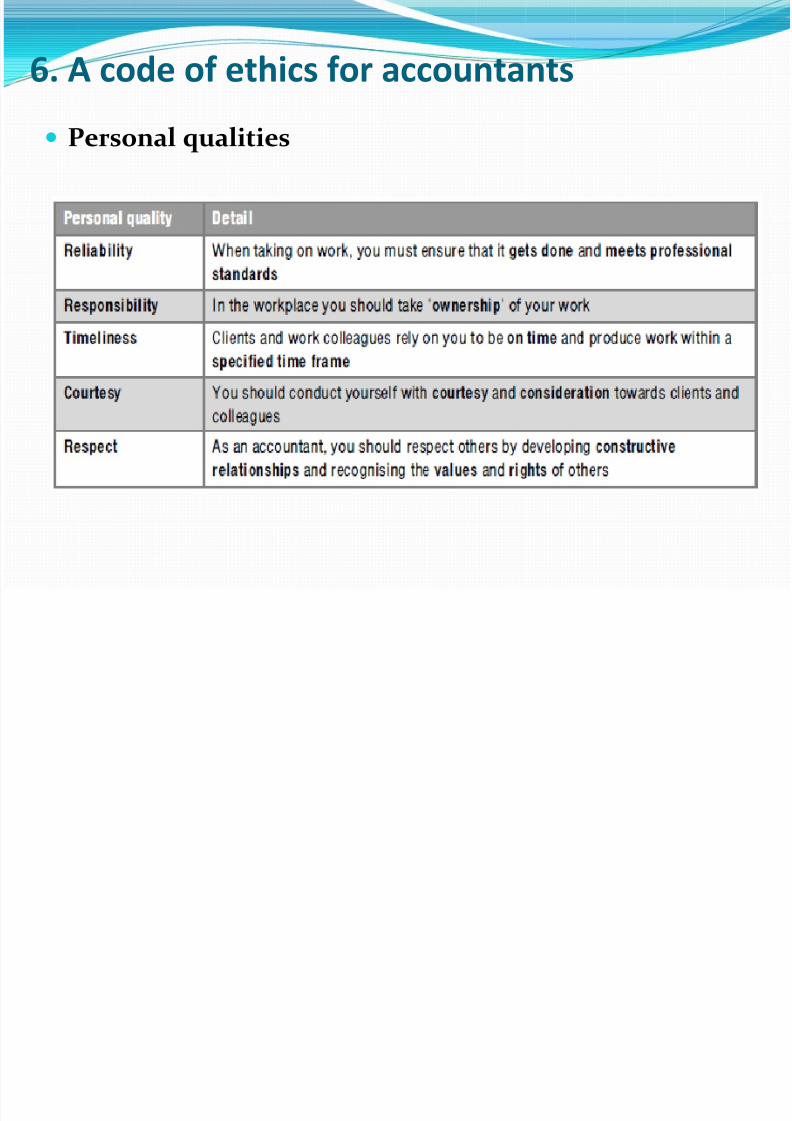

6. A code of ethics for accountants

Personal qualities

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 22/36

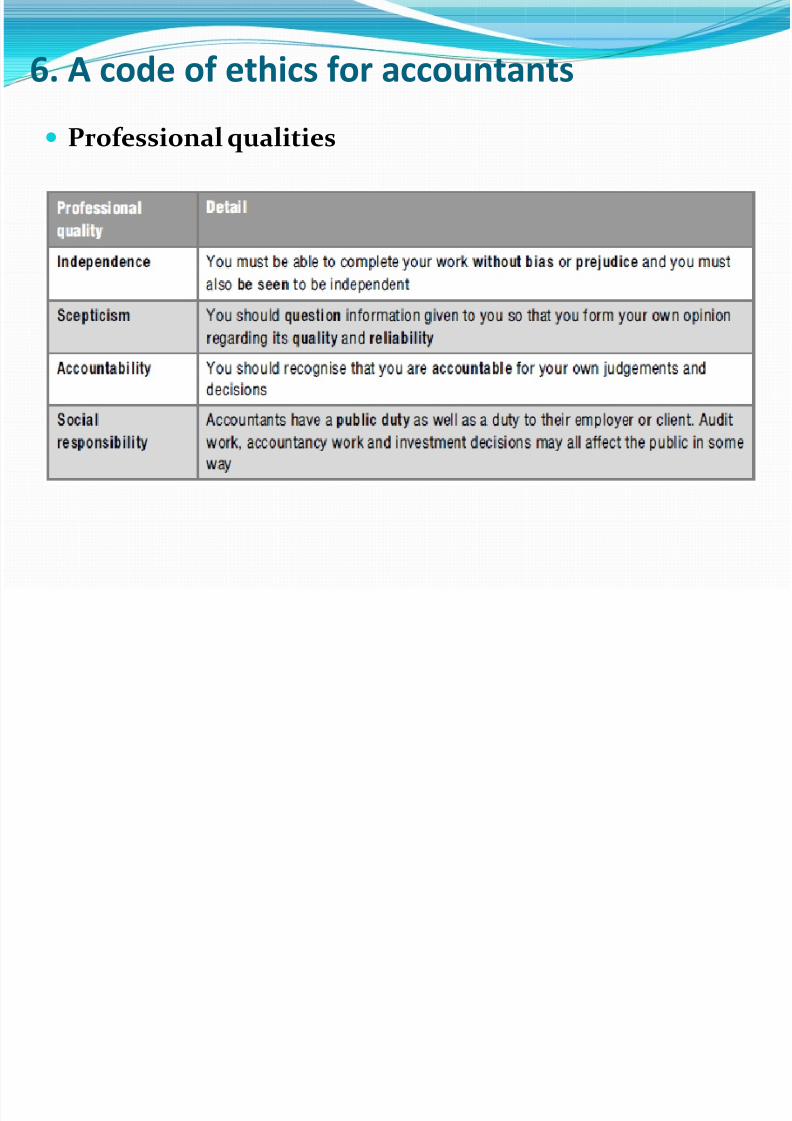

6. A code of ethics for accountants

Professional qualities

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 23/36

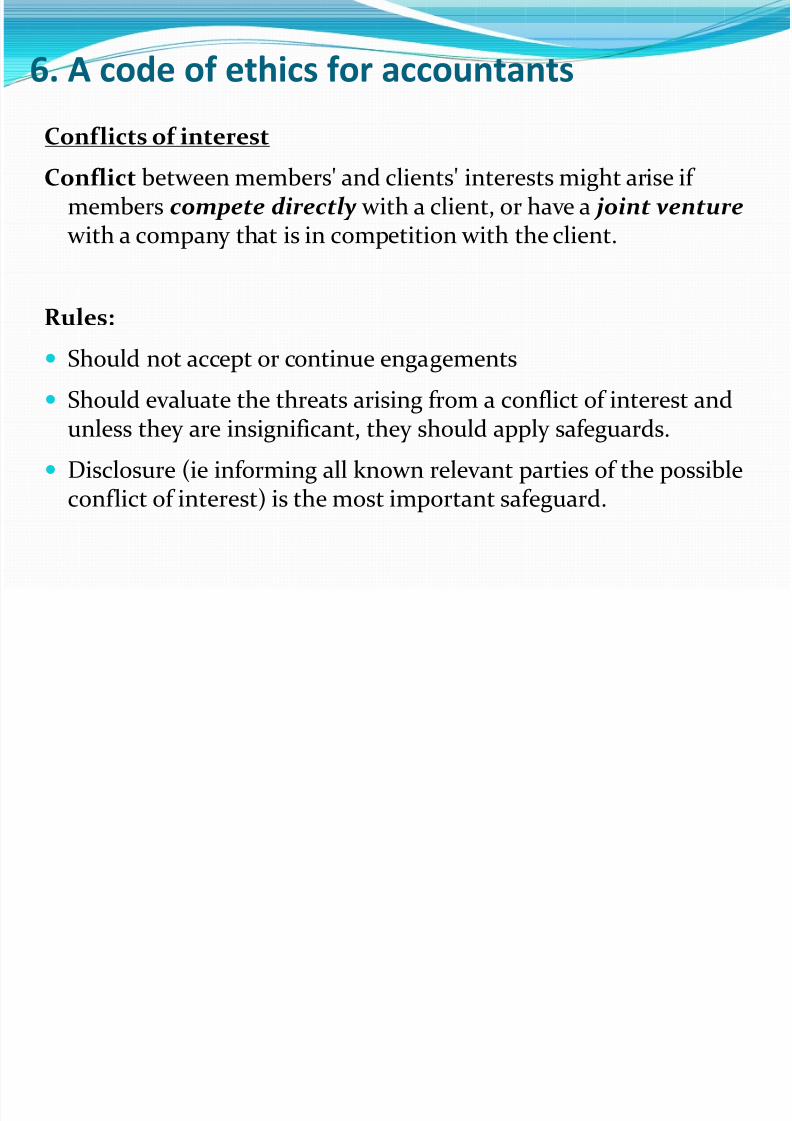

6. A code of ethics for accountants

Conflicts of interestConflict between members' and clients' interests might arise if

members compete directly with a client, or have a joint venture with a company that is in competition with the client.

Rules:

Should not accept or continue engagements

Should evaluate the threats arising from a conflict of interest andunless they are insignificant, they should apply safeguards.

Disclosure (ie informing all known relevant parties of the possibleconflict of interest) is the most important safeguard.

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 24/36

6. A code of ethics for accountants

Threats to independence: Self-interest threat

Self-review threat

Advocacy threat Familiarity threat

Intimidation threat

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 25/36

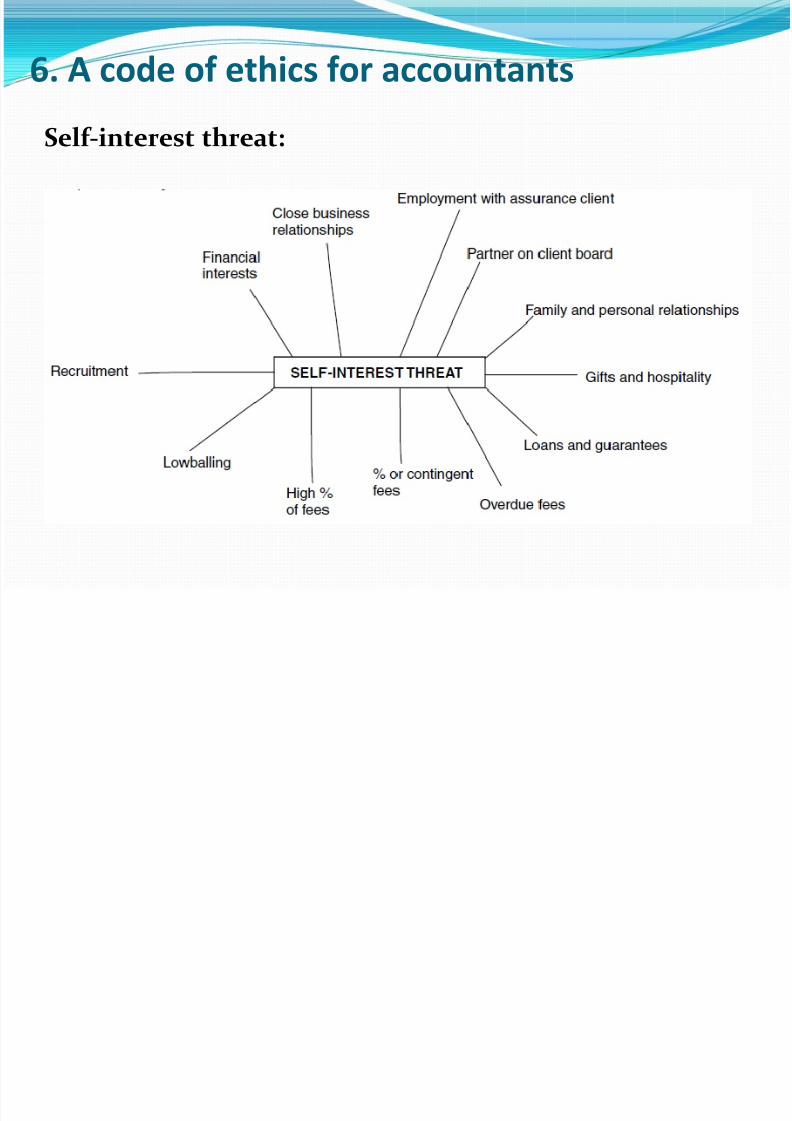

6. A code of ethics for accountants

Self-interest threat:

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 26/36

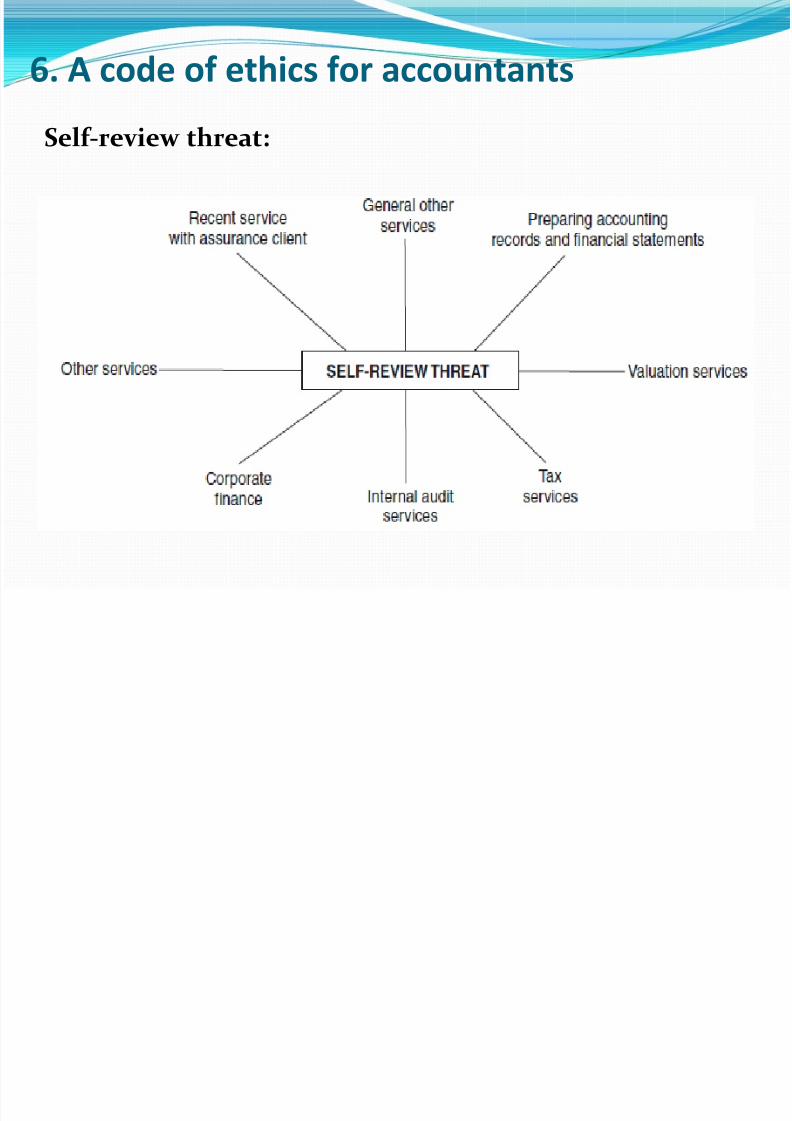

6. A code of ethics for accountants

Self-review threat:

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 27/36

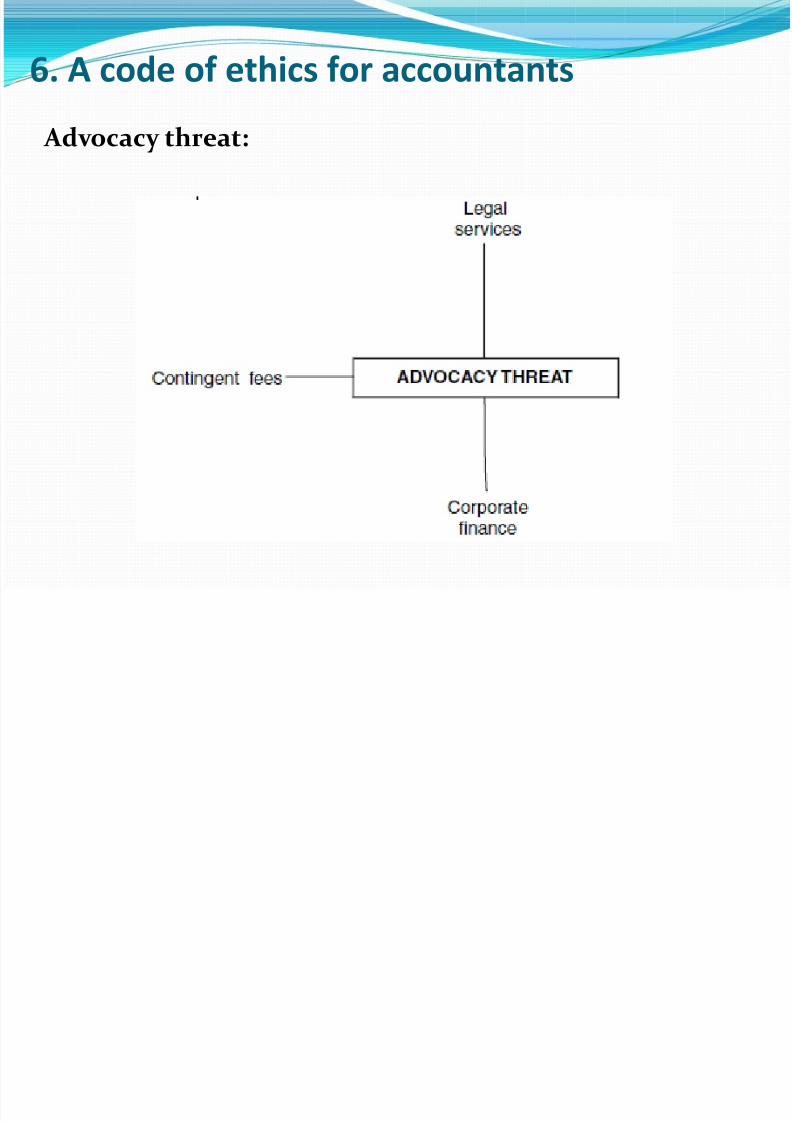

6. A code of ethics for accountants

Advocacy threat:

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 28/36

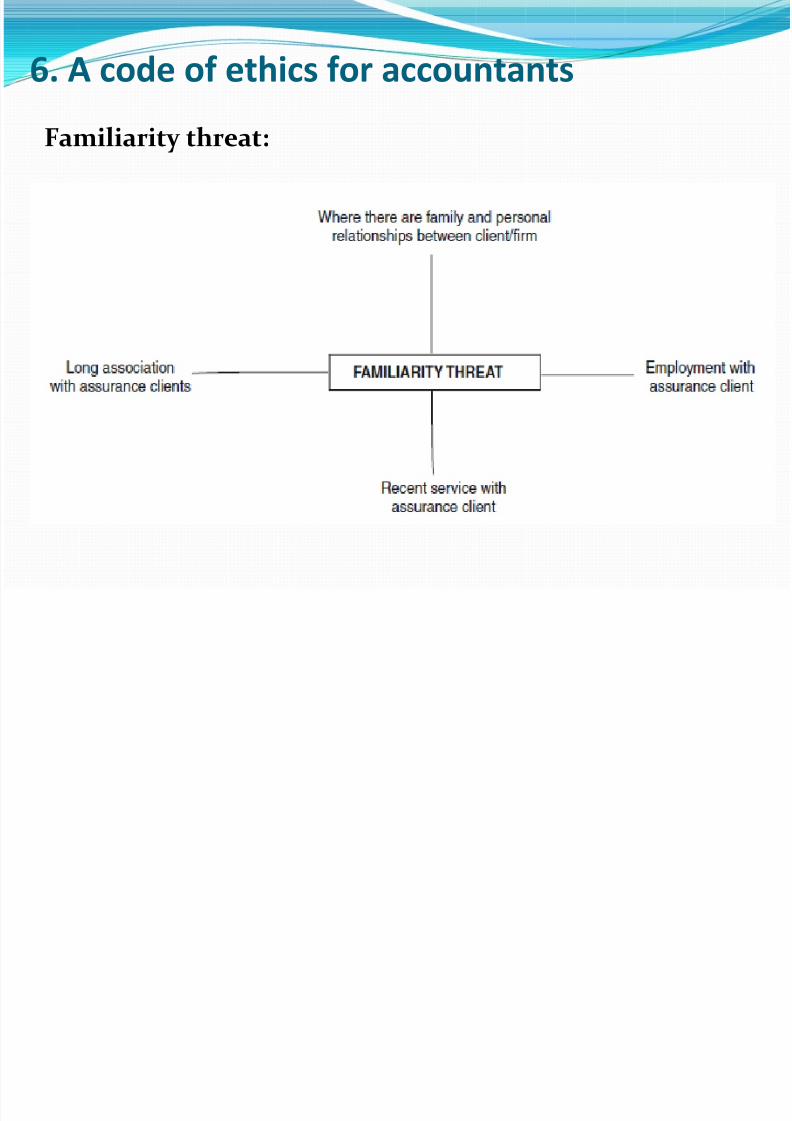

6. A code of ethics for accountants

Familiarity threat:

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 29/36

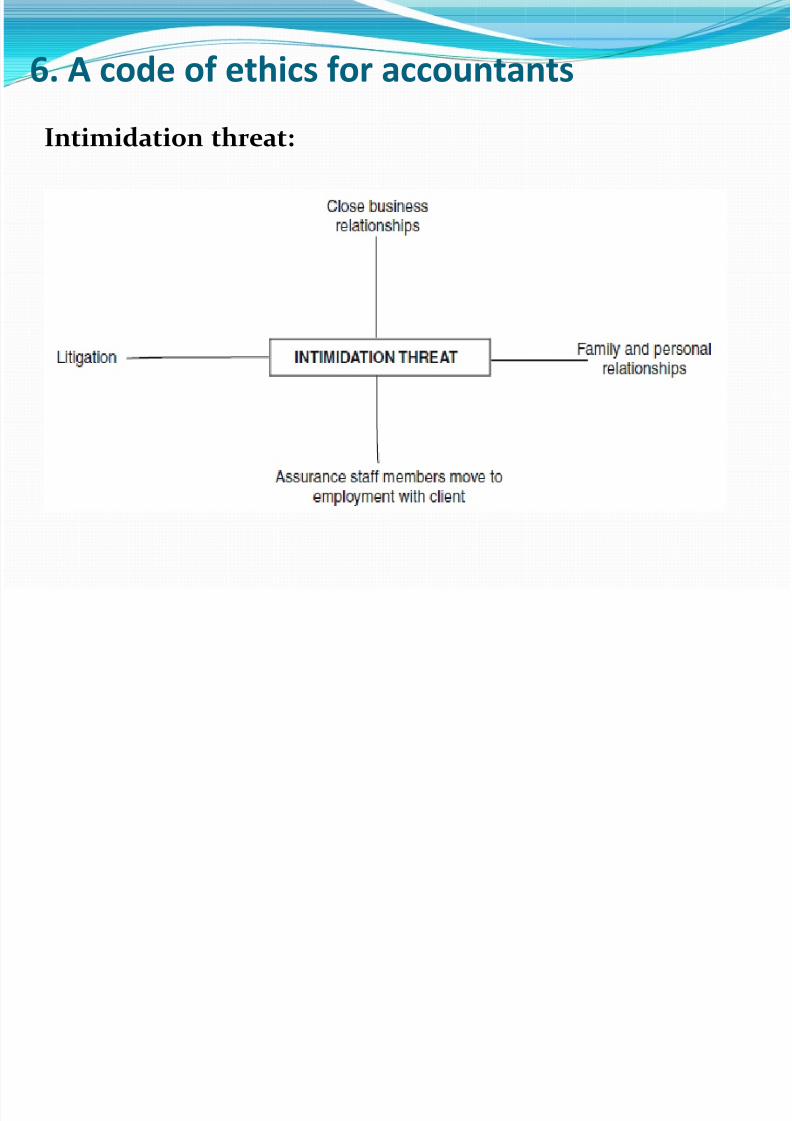

6. A code of ethics for accountants

Intimidation threat:

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 30/36

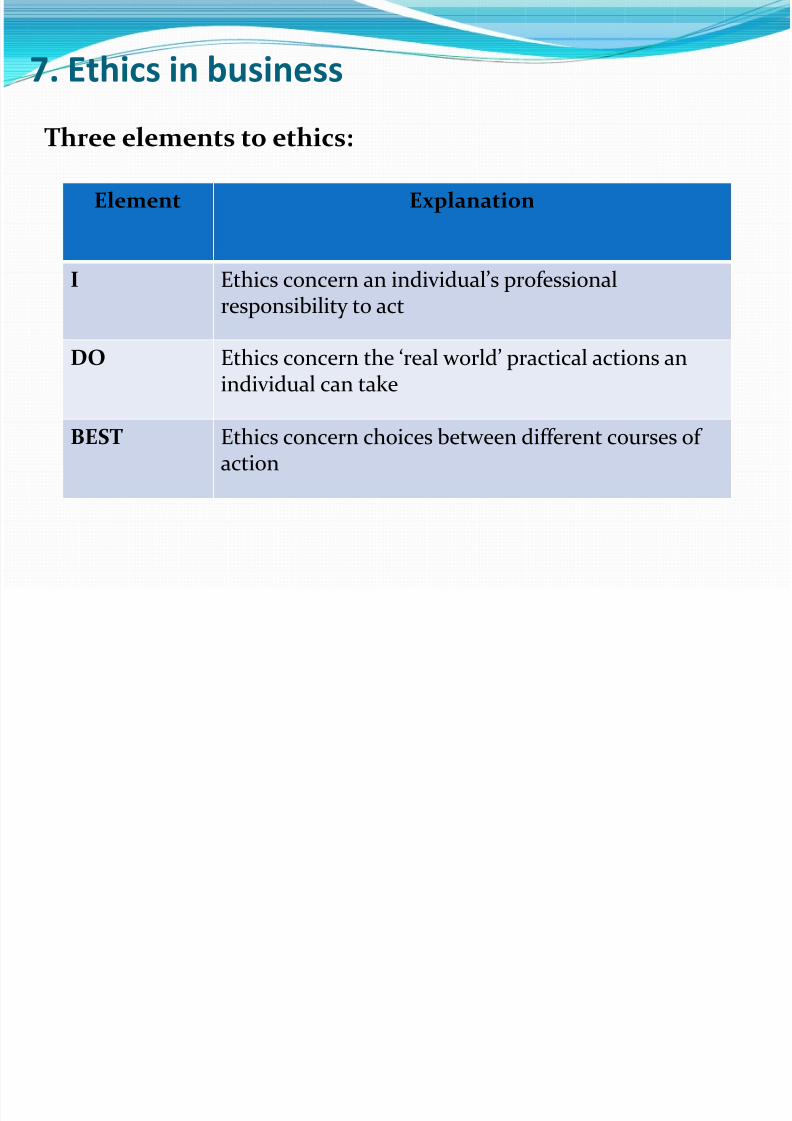

7. Ethics in business

Three elements to ethics:

Element Explanation

I Ethics concern an individual’s professionalresponsibility to act

DO Ethics concern the ‘real world’ practical actions anindividual can take

BEST Ethics concern choices between different courses ofaction

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 31/36

8. Ethical dilemmas

Ethical dilemmas and conflicts of interest:Ethical dilemmas are situations where two ethical values or requirements

seem to be incompatible. They can also arise where two conflictingdemands or obligations are placed on an individual.

A conflict of interest arises where an individual has a duty to two or moreparties.

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 32/36

8. Ethical dilemmas

Ethical dilemmas occur as a result of tensions between 4sets of values:

Societal values – the law

Personal values – values and principles held by the individual

Corporate values – the values and principles of org where theindividual works, often laid down in ethical codes.

Professional values – the values and principles of the professionalbody that the individual is a member of, often laid down in ethical

codes.

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 33/36

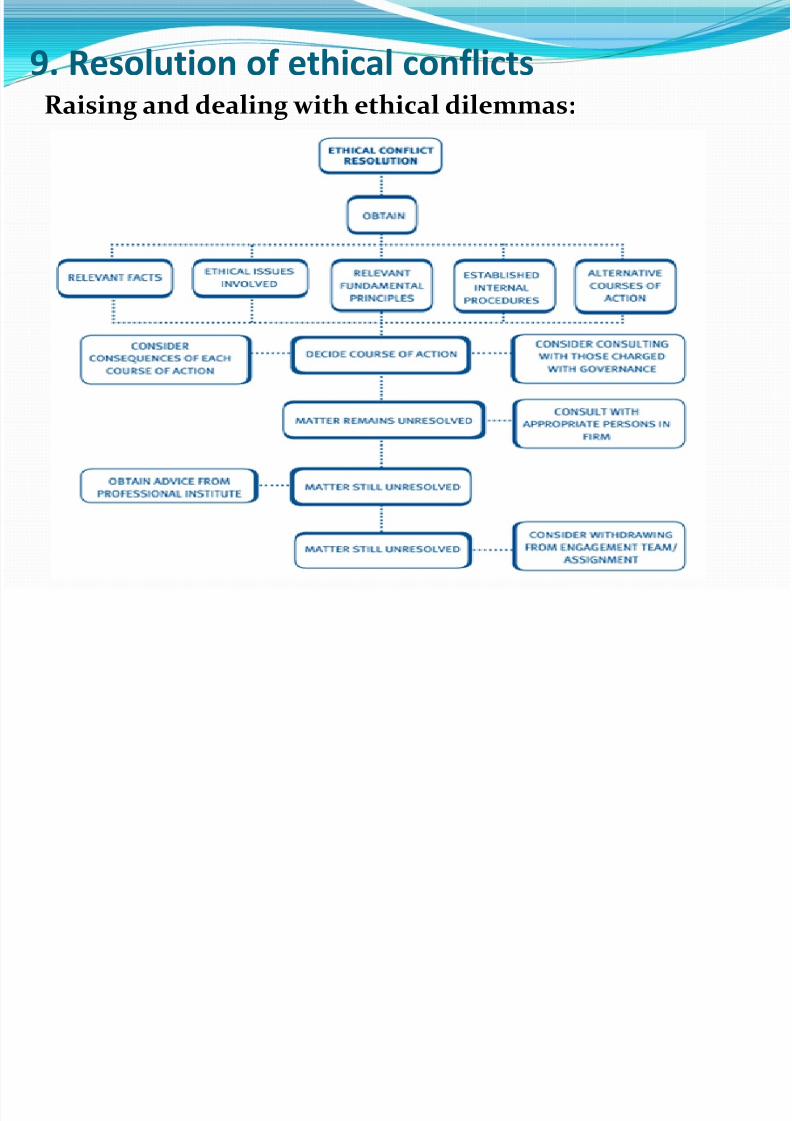

9. Resolution of ethical conflicts

Ethical conflicts may arise from: Pressure form an overbearing colleague/ family

Members asked to act contrary to technical/ professionalstandards

Publication of misleading information

Personal relationship with clients

Gift and hospitality being offered

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 34/36

9. Resolution of ethical conflicts

Individual should ask themselves: Transparency

Effect

Fairness

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 35/36

9. Resolution of ethical conflictsRaising and dealing with ethical dilemmas:

8/12/2019 #20 - Ethical Considerations

http://slidepdf.com/reader/full/20-ethical-considerations 36/36

Q&A