2008-2013 - motilal oswal...2008-2013 18th annual wealth creation study . ... management,...

TRANSCRIPT

Uncommon Profits

By Raamdeo Agrawal

13 December 2013

18th Annual Wealth Creation Study

2008-2013

www.motilaloswal.com 18th Annual Wealth Creation Study

Theme Study

Uncommon Profits

www.motilaloswal.com 18th Annual Wealth Creation Study

2

Theme Discussion Points

Uncommon Profits: What & why

Emergence & Endurance: What & why

Framework to identify Emerging Value Creators

Methodology to shortlist Emerging Value Creators

Why Enduring Value Creators?

Methodology to shortlist Enduring Value Creators

www.motilaloswal.com 18th Annual Wealth Creation Study

Uncommon Profits in companies

=

Uncommon Wealth Creation in markets

A simple mantra for Wealth Creation …

www.motilaloswal.com 18th Annual Wealth Creation Study

Uncommon Wealth Creation #1

0

50

100

150

200

250 1

98

8

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Ambuja Cement Sensex - Rebased

Ambuja up 420x in 25 years; 27% CAGR

Sensex up 45x; 16% CAGR

www.motilaloswal.com 18th Annual Wealth Creation Study

Uncommon Wealth Creation #2

0

150

300

450

600

750

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

HDFC Bank Sensex - Re-based

HDFC Bank up 64x in 15 years; 32% CAGR

Sensex up 7x; 14% CAGR

www.motilaloswal.com 18th Annual Wealth Creation Study

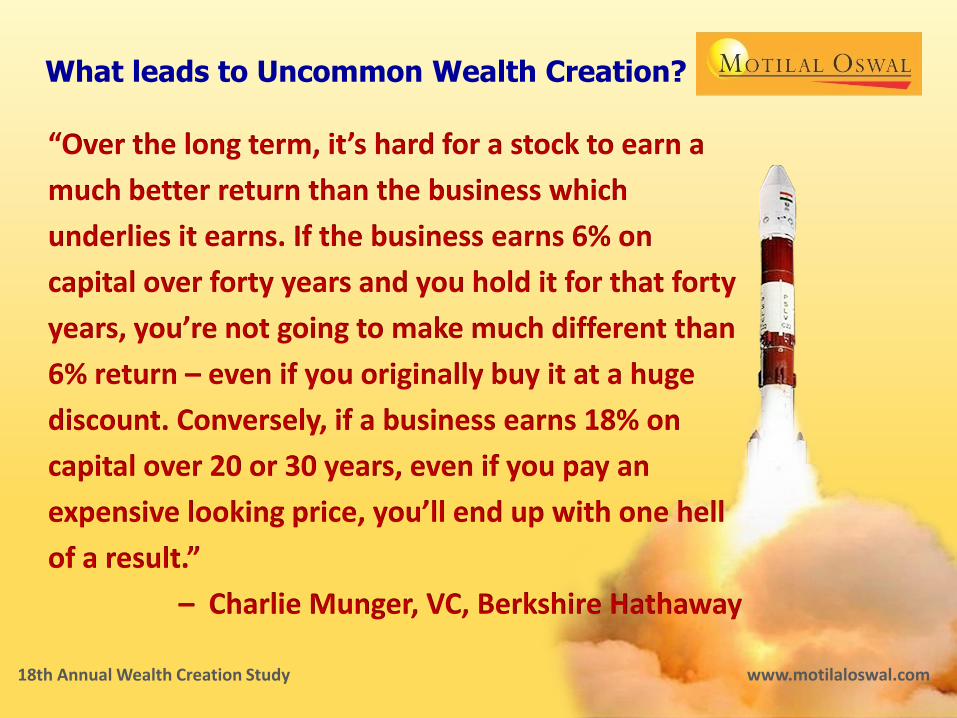

“Over the long term, it’s hard for a stock to earn a

much better return than the business which

underlies it earns. If the business earns 6% on

capital over forty years and you hold it for that forty

years, you’re not going to make much different than

6% return – even if you originally buy it at a huge

discount. Conversely, if a business earns 18% on

capital over 20 or 30 years, even if you pay an

expensive looking price, you’ll end up with one hell

of a result.”

– Charlie Munger, VC, Berkshire Hathaway

What leads to Uncommon Wealth Creation?

www.motilaloswal.com 18th Annual Wealth Creation Study

Uncommon Profits in companies

=

Uncommon Wealth Creation in markets

In simple words …

8

• Uncommon Profitability (%) = RoE > Cost of Equity

• Uncommon Profit (abs) = (RoE – CoE) x Equity employed where RoE = Return on Equity Cost of equity = Opportunity cost of equity or Risk free rate + Equity risk premium

• In Indian context, Cost of Equity = 15%

• Consistent Uncommon Profit earning companies

are Value Creators

What is Uncommon Profit?

9

What is Emergence & Endurance?

• Emergence is first entry of a company into the Uncommon Profit zone i.e. RoE > 15%

• The next challenge is Endurance i.e. sustaining RoE > 15% for several years ahead

10

Uncommon Profit & Company Lifecycle

Pre-Emergence struggle for survival

Time

PAT

POINT OF EMERGENCE

Post-Emergence struggle for Endurance

Introduction Growth Maturity

(b) Decline

(a) Renewal

11

Uncommon Profit Case Study #1

Titan Industries (YoE: 2003)

… Uncommon Wealth Creation

26x in 5 years (85% CAGR),

130x in 10 years (59% CAGR)

Uncommon Profit generation …

12

Uncommon Profit Case Study #2

Gruh Finance (YoE: 2003)

… Uncommon Wealth Creation

10x in 5 years (60% CAGR),

70x in 10 years (54% CAGR)

Uncommon Profit generation …

13

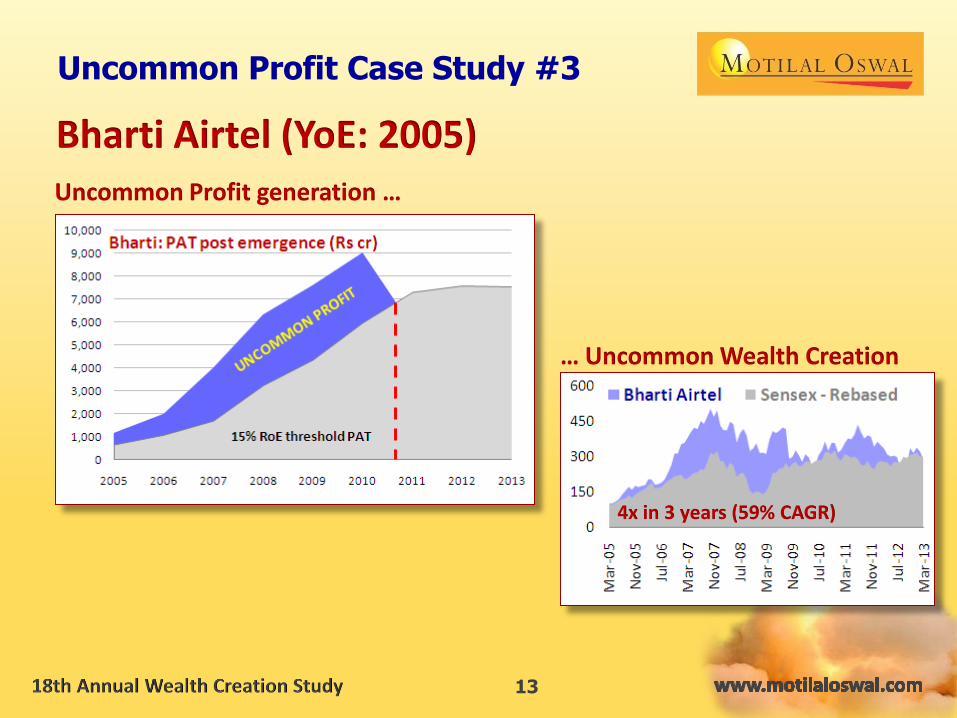

Uncommon Profit Case Study #3

Bharti Airtel (YoE: 2005)

… Uncommon Wealth Creation

4x in 3 years (59% CAGR)

Uncommon Profit generation …

14

Framework to identify Value Creators

Contribution of various factors to abnormal profits

Contributing factor High Performers Low Performers

Emergence Sustainability Emergence Sustainability

Year 2% 3% -7% -5%

Industry 37% 44% 12% 13%

Corporate-parent 18% 19% -4% 2%

Segment-specific 43% 34% 99% 90% Source: Paper by Anita McGahan & Michael Porter

Year – Economic cycle

Industry – Industry-level factors like size of profit pool,

competition, stability, strategic opportunity, etc

Corporate Parent – Promoter or majority owner

Segment-specific – Company-specific factors like quality of

management, strategy/unique value proposition, etc

15

Value Creators: Industry-level factors

#1 Size of profit pool

10 highest PAT sectors (2013)

Sector Rs crores % share

Financials - Banks 84,154 21

Energy - Oil & Natural Gas 39,963 10

Technology - Software 34,702 9

Financials - NBFCs 32,376 8

Mining & Minerals 27,261 7

Energy - Refineries 22,774 6

Utilities 22,349 6

Automobiles 21,931 6

Healthcare 16,518 4

Metals - Non-Ferrous 10,520 3

Total of above 312,547 79

Grand Total 394,786 100

16

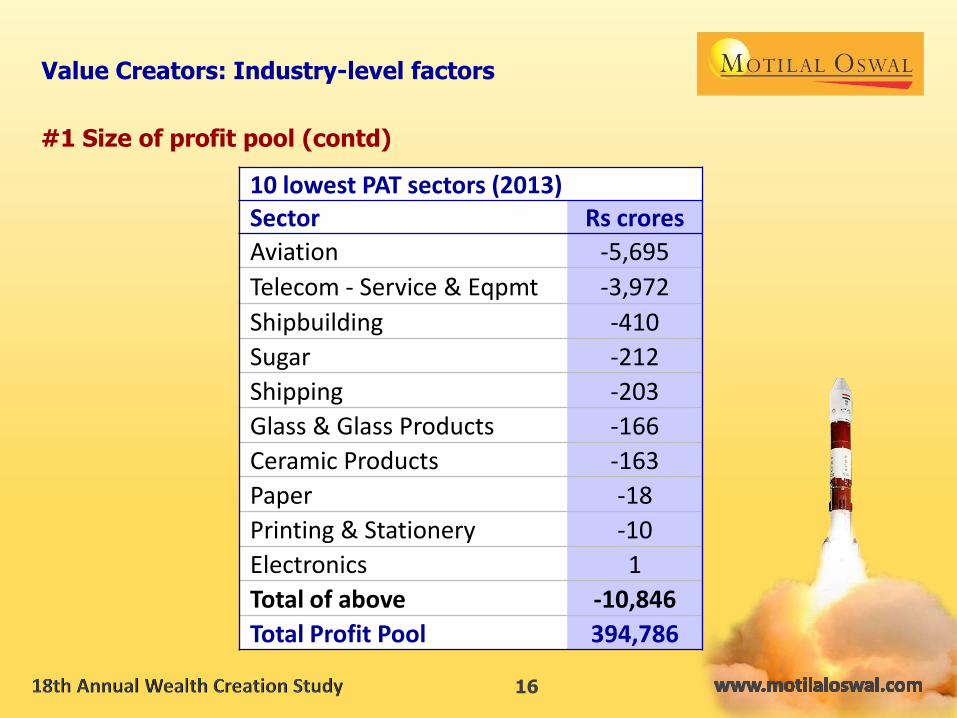

Value Creators: Industry-level factors

#1 Size of profit pool (contd)

10 lowest PAT sectors (2013) Sector Rs crores

Aviation -5,695

Telecom - Service & Eqpmt -3,972

Shipbuilding -410

Sugar -212

Shipping -203

Glass & Glass Products -166

Ceramic Products -163

Paper -18

Printing & Stationery -10

Electronics 1

Total of above -10,846

Total Profit Pool 394,786

17

Value Creators: Industry-level factors

#1 Size of profit pool (contd)

Highest PAT CAGR (03-13) with minimum PAT of Rs 2,000 crores in 2013

Sector 03-13 PAT PAT Sector 03-13 PAT PAT

CAGR (%) Delta CAGR (%) Delta

Textiles L to P 5,653 Infra Developers 28 6,233

Realty L to P 3,799 Metals - Steel 28 3,006

Fertilizers L to P 2,821 Metals - Non-ferrous 27 9,556

Cement 57 7,825 Healthcare 20 13,843

Tech - Software 54 34,239 Capital Goods 19 5,413

Gems & Jewelry 46 3,176 Tobacco Products 18 6,275

Financials - NBFC 46 31,647 Banks 18 67,998

Mining & Minerals 46 26,627 Auto Ancillaries 17 2,917

Automobiles 39 21,101

Chemicals 29 3,115 TOTAL CORP. SECTOR 20 331,719

18

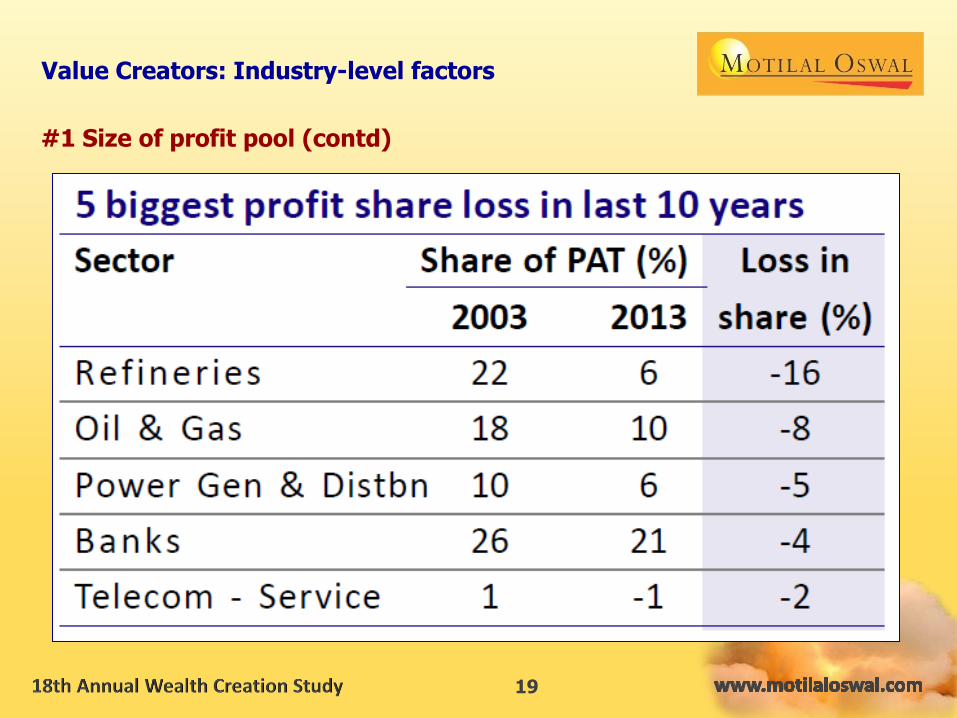

Value Creators: Industry-level factors

#1 Size of profit pool (contd)

19

Value Creators: Industry-level factors

#1 Size of profit pool (contd)

20

#2 Competitive landscape & bargaining power

Value Creators: Industry-level factors

Porter’s 5 forces

framework to

assess competition

& bargaining power

21

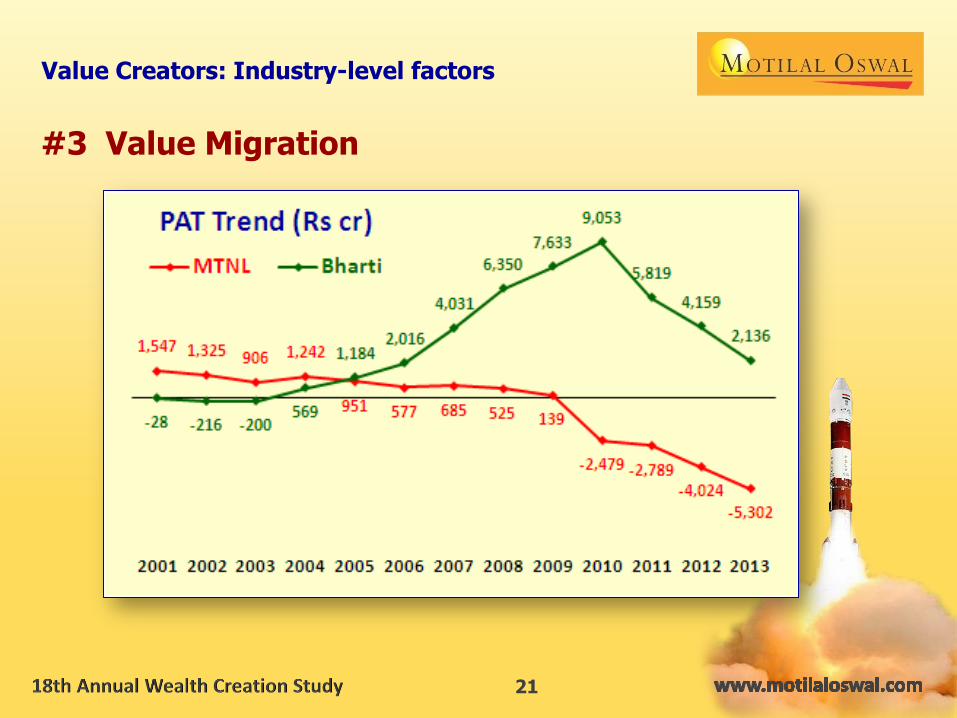

#3 Value Migration

Value Creators: Industry-level factors

22

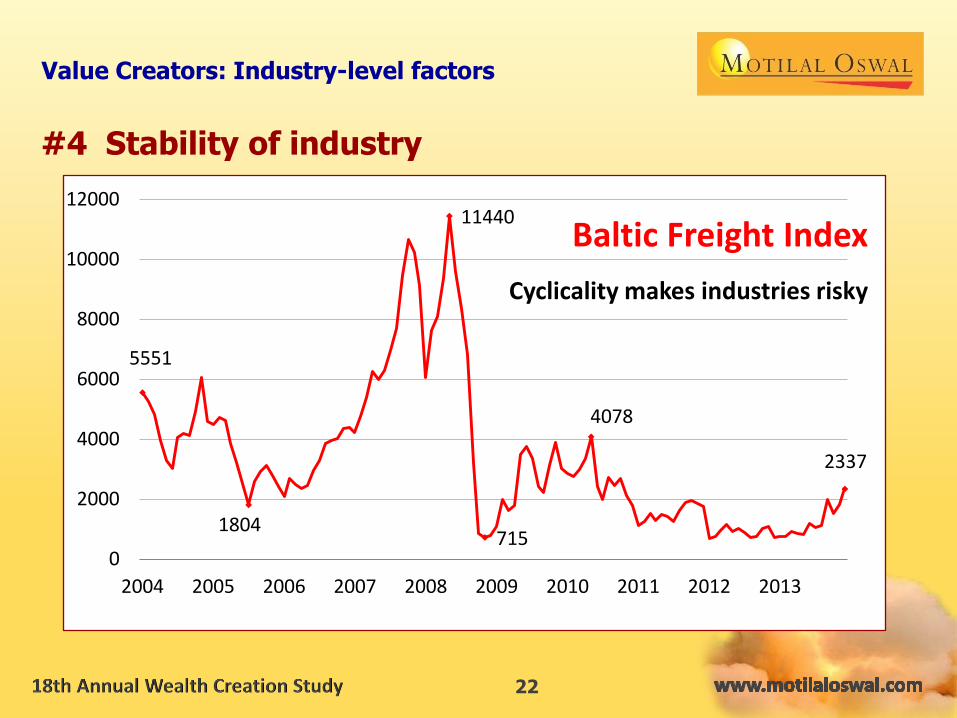

#4 Stability of industry

Value Creators: Industry-level factors

5551

1804

11440

715

4078

2337

0

2000

4000

6000

8000

10000

12000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Baltic Freight Index

Cyclicality makes industries risky

23

#5 Emergence of new industry /strategic opportunity

Value Creators: Industry-level factors

0

300

600

900

1,200

1,500

Feb

-10

May

-10

Au

g-1

0

No

v-1

0

Feb

-11

May

-11

Au

g-1

1

No

v-1

1

Feb

-12

May

-12

Au

g-1

2

No

v-1

2

Feb

-13

May

-13

Au

g-1

3

No

v-1

3

Jubilant Foodworks Sensex - Rebased

Jubilant up 6x in under 4 years; CAGR of 65% v/s 7% for Sensex

Uncommon Wealth Creation

24

Value Creators: Corporate-parent factors

3Is – Integrity + Intelligence + Initiative

#1 Value system

#2 Processes

#3 Capital allocation

#4 Management skill v/s Luck

25

Value Creators: Company-specific factors

#1 Unique value proposition / Strategy

#2 Nature of business: Consumer Adv v/s Production Adv

#3 Market leadership or pioneering

26

Pitfalls to avoid in Emergence

#1 Pre-empting emergence

#2 Emergence during peak of good times

“…the risk of paying too high a price for good-quality

stocks – while a real one – is not the chief hazard

confronting the average buyer of securities.

Observation over many years has taught us that the

chief losses to investors come from the purchase of

low-quality securities at times of favorable business conditions.”

– Benjamin Graham in his book The Intelligent Investor

27

Methodology for Emerging Value Creators

#1 Age criterion

Select listed companies below 25 years of age

#2 Meaningful Emergence

15% RoE for first time with minimum PAT size, say, Rs 10 crores

#3 View on corporate-parent/management

based on group performance, Annual Reports, payout policy, etc

#4 Avoid cyclicals

Incorporating stability of industry

#5 Valuation check considering risk of non-Endurance

P/E typically not exceeding 20x

28

Backtesting during 2001 to 2008

Emerging Value Creators’ financial & stock market performance

Company Year of P/E (x) 5-year post emergence (%) Emerg. in YoE PAT CAGR Price CAGR Rel Perf. Shriram Transport 2001 1 56 85 60 Accelya Kale 2008 3 36 60 56 Shriram City Union 2004 3 45 70 58 GRUH Finance 2003 4 33 60 22 Plastiblends (I) 2004 4 1 4 -8 Manappuram Finance 2007 4 123 70 64 Havells India 2004 7 P to L 39 27 Cera Sanitaryware 2008 7 36 29 17 KPIT Tech 2004 8 36 4 -7 Blue Dart Express 2001 9 22 45 20 Titan Industries 2003 12 53 85 46 Hitachi Home 2006 12 14 22 11 Tata Elxsi 2001 16 20 23 -3 Emami 2007 18 31 33 27 Suprajit Engg. 2006 18 21 0 -12 IL&FS Invt Managers 2007 18 32 9 3 Asahi India Glass 2002 19 25 51 21 AVERAGE 10 24 41 24

29

Backtesting during 2001 to 2008

Applying Value Creator checklist items (“amplifiers”)

Industry Profit pool size

Nature of business

Leadership

Amplifier No. of cos.

5 years post-emergence (%) PAT CAGR Avg RoE Price CAGR Rel. Perf.

Industry Profit Pool High 10 26 29 55 37 Low 7 21 37 20 4

Nature of business advantage Consumer 9 21 34 46 31 Production 8 27 30 34 16

Leadership i.e. among top 3 players Yes 10 19 32 45 28 No 7 31 32 34 18

Portfolio avg 17 24 32 41 24

30

Backtesting during 2001 to 2008

Optimized portfolio with Amplifiers

Company P/E (x) 5-year post emergence (%)

in YoE PAT CAGR Price CAGR Rel. Perf.

Manappuram Finance 4 123 70 64

Shriram Transport 1 56 85 60

Titan Industries 12 53 85 46

Havells India 7 P to L 39 27

Blue Dart Express 9 22 45 20

AVERAGE 7 – 65 43

31

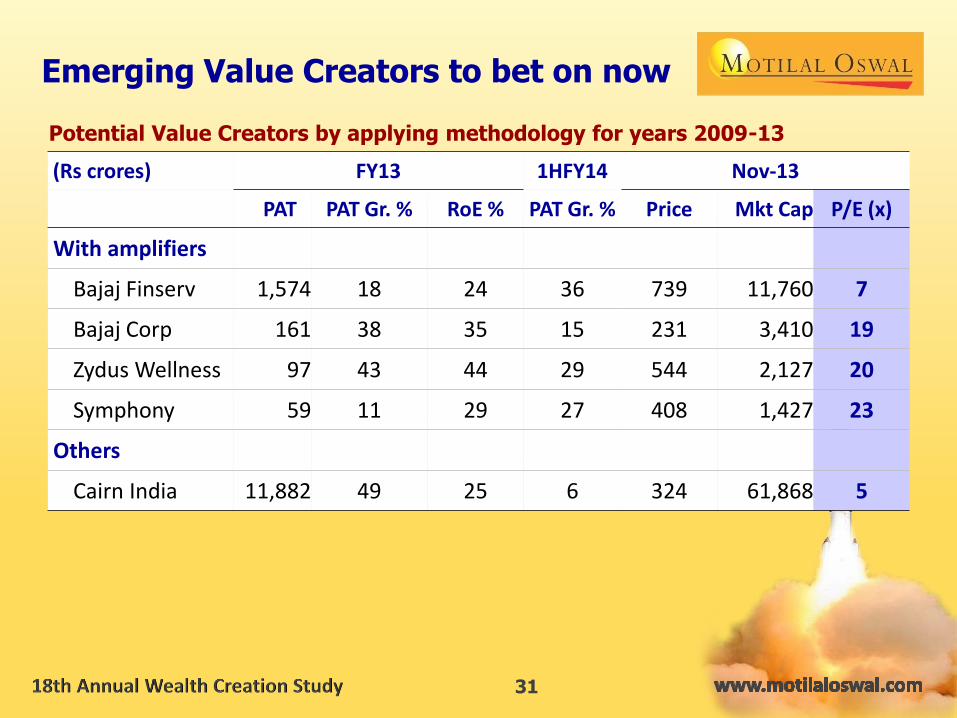

Emerging Value Creators to bet on now

Potential Value Creators by applying methodology for years 2009-13

(Rs crores) FY13 1HFY14 Nov-13

PAT PAT Gr. % RoE % PAT Gr. % Price Mkt Cap P/E (x)

With amplifiers

Bajaj Finserv 1,574 18 24 36 739 11,760 7

Bajaj Corp 161 38 35 15 231 3,410 19

Zydus Wellness 97 43 44 29 544 2,127 20

Symphony 59 11 29 27 408 1,427 23

Others

Cairn India 11,882 49 25 6 324 61,868 5

32

Why Enduring Value Creators

Emerging Value Creators are rare

(we could get only 17 in 8 years 2001-08)

Enduring Value Creators too

outperform despite being fully discovered

and fairly discounted

A suitable methodology may help

to shortlist Enduring Value Creators

33

Methodology for Enduring Value Creators

#1 Quality & Longevity criteria

RoE >= 15% for each of the last 10 consecutive years

#2 View on corporate-parent/management

based on group performance, Annual Reports, payout policy, etc

#3 Growth

Last 3-year CAGR of at least 15%

#4 Value-enhancing growth

Postive delta RoE over the last 5 years

#5 Reasonable valuation

Not more than 50% premium to market

i.e. P/E typically not exceeding 30x

34

Backtesting during 1999 to 2008

2008 Enduring Value Creators’ financial & stock market performance

Company 2008-13 P/E

PAT

CAGR Price CAGR

Rel. Perf.

2008 2013

Berger Paints 19 40 36 12 31

Torrent Pharma 28 38 34 9 13

Asian Paints 22 33 29 28 43

Castrol India 15 27 23 20 33

Colgate-Palmolive 16 27 23 22 34

Marico 18 26 22 26 37

City Union Bank 26 25 21 7 8

H D F C 20 12 8 25 19

Wipro 13 11 7 19 18

Glenmark Pharma -1 -1 -5 19 20

AVERAGE 16 24 20 21 20

35

Enduring Value Creators to bet on now

Applying methodology for years 2004 to 2013; preferred bets highlighted

Company 2010-13 2003-13 P/E Price Return CAGR

PAT CAGR % Avg RoE % (x) (INR) 08-13 (%)

City Union Bank 28 23 7 49 25

Axis Bank 28 20 10 1,155 11

Suprajit Engg 24 31 11 39 34

Torrent Pharma 27 26 15 462 38

HCL Technologies 47 26 16 1,087 25

M & M Financial 36 22 17 296 28

Zydus Wellness 28 37 20 544 38

VST Industries 25 31 20 1,664 37

HDFC Bank 32 18 23 661 19

Astral Poly Technik 29 30 24 250 35

GRUH Finance 28 27 26 233 47

ITC 21 29 34 320 25

Hindustan Unilever 16 77 40 594 17

Page Industries 42 62 44 5,265 51

Thank You !

&

Happy Investing For

Uncommon Profits