2010 bio business forum partnering results - final

TRANSCRIPT

8/6/2019 2010 BIO Business Forum Partnering Results - Final

http://slidepdf.com/reader/full/2010-bio-business-forum-partnering-results-final 1/14

resen a on o uper ess on

May 2010

This report contains information obtained from publicly available sources and is presented as a fair use of the material, or alternatively, contains

information from sources that BIO has obtained permission to use the information. At the time of the presentation or publication, the information is

believed to be accurate and reliable. BIO disclaims responsibility or any damages resulting from anyone’s use or reliance on the information provided.

Any further distribution or use of the contents without appropriate attribution and reference to BIO and the source(s) is prohibited.

8/6/2019 2010 BIO Business Forum Partnering Results - Final

http://slidepdf.com/reader/full/2010-bio-business-forum-partnering-results-final 2/14

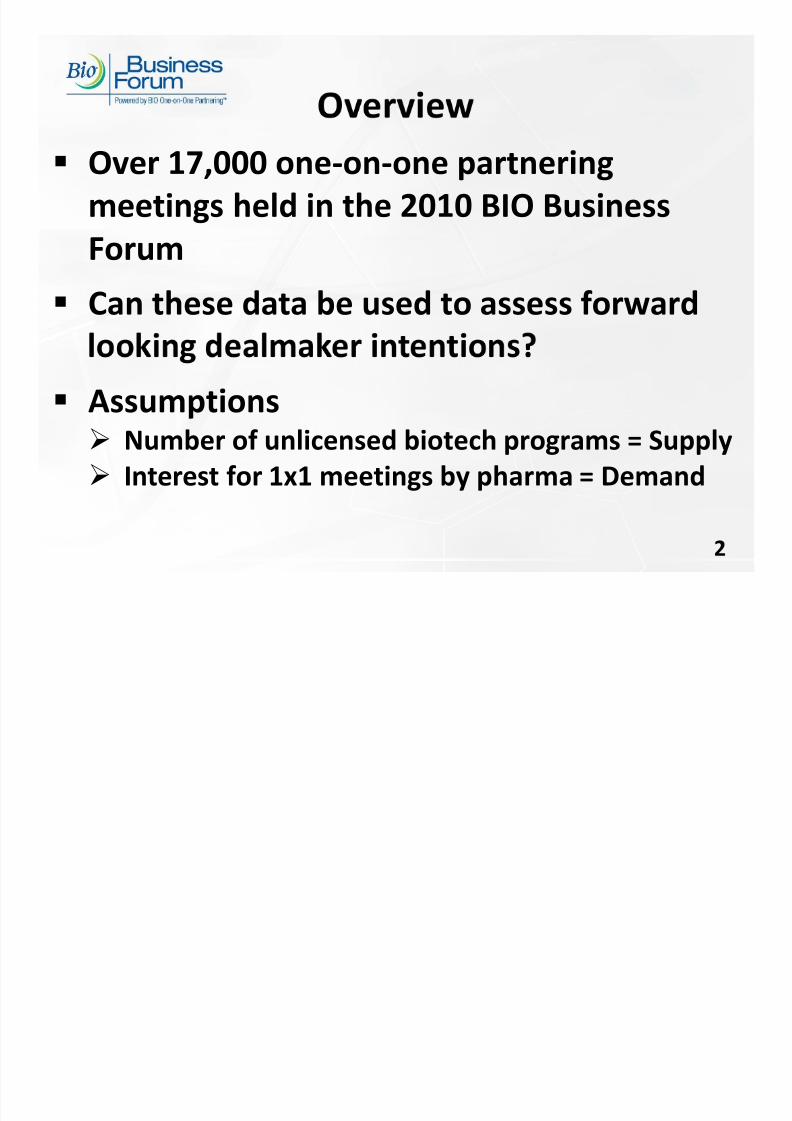

Over 17,000 one‐on‐one partnering

meetings held in the 2010 BIO Business

Forum

Can

these

data

be

used

to

assess

forward

Assumptions Number of unlicensed biotech programs = Supply

Interest for 1x1 meetings by pharma = Demand

2

8/6/2019 2010 BIO Business Forum Partnering Results - Final

http://slidepdf.com/reader/full/2010-bio-business-forum-partnering-results-final 3/14

Partnering Meeting Growth

17,143

CAGR

3

8/6/2019 2010 BIO Business Forum Partnering Results - Final

http://slidepdf.com/reader/full/2010-bio-business-forum-partnering-results-final 4/14

One‐on‐One Partnering Meetings

cago

2010*

t anta

2009

cago

2006

Companies 2,125

(up 20% y‐o‐y)

1,770 1,476

Scheduled 17,143

u 21 ‐o‐

14,202 11,018

Requested 107,324 80,861

‐ ‐

*Final as of Friday, May 7th, 2010 4

8/6/2019 2010 BIO Business Forum Partnering Results - Final

http://slidepdf.com/reader/full/2010-bio-business-forum-partnering-results-final 5/14

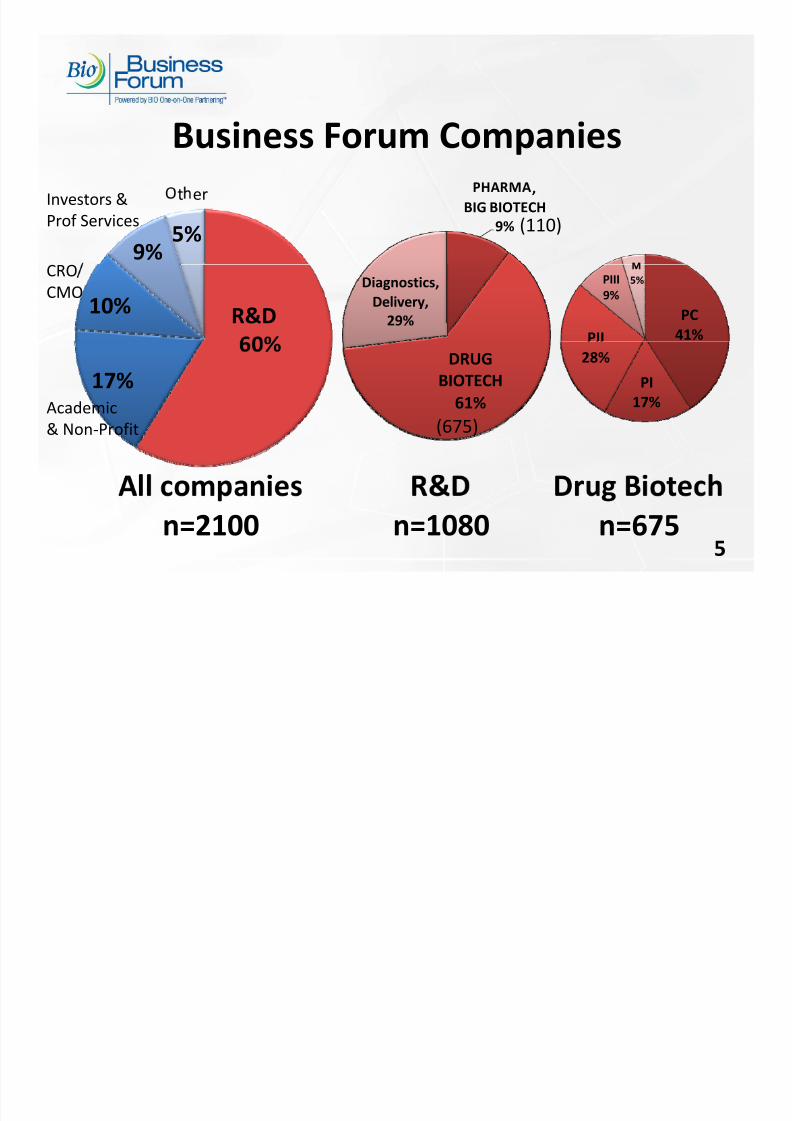

Business Forum Companies

, BIG

BIOTECH

9% (110)

9%5%

t erInvestors &

Prof Services

PC41%PII

PIII

9%

5%Diagnostics, Delivery,

29%

10%

CRO

CMO

R&D

PI

17%

28%DRUG BIOTECH

61%

17%Academic

(675)& Non‐Profit

n=1080

n=675

n=2100 5

8/6/2019 2010 BIO Business Forum Partnering Results - Final

http://slidepdf.com/reader/full/2010-bio-business-forum-partnering-results-final 6/14

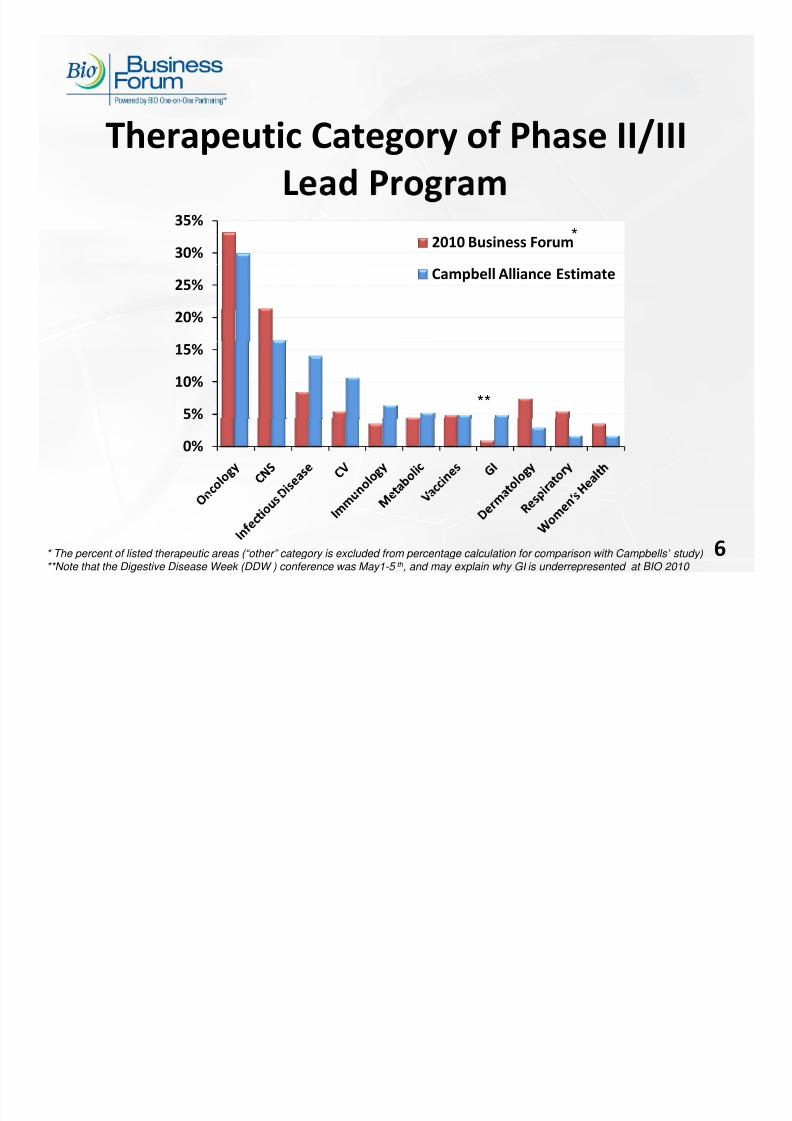

Therapeutic Category of Phase II/III

30%

35%

2010 Business Forum

*

20%

25%Campbell Alliance Estimate

5%

10%

15%

**

0%

* The percent of listed therapeutic areas (“other” category is excluded from percentage calculation for comparison with Campbells’ study)**Note that the Digestive Disease Week (DDW ) conference was May1-5 th , and may explain why GI is underrepresented at BIO 2010

6

8/6/2019 2010 BIO Business Forum Partnering Results - Final

http://slidepdf.com/reader/full/2010-bio-business-forum-partnering-results-final 7/14

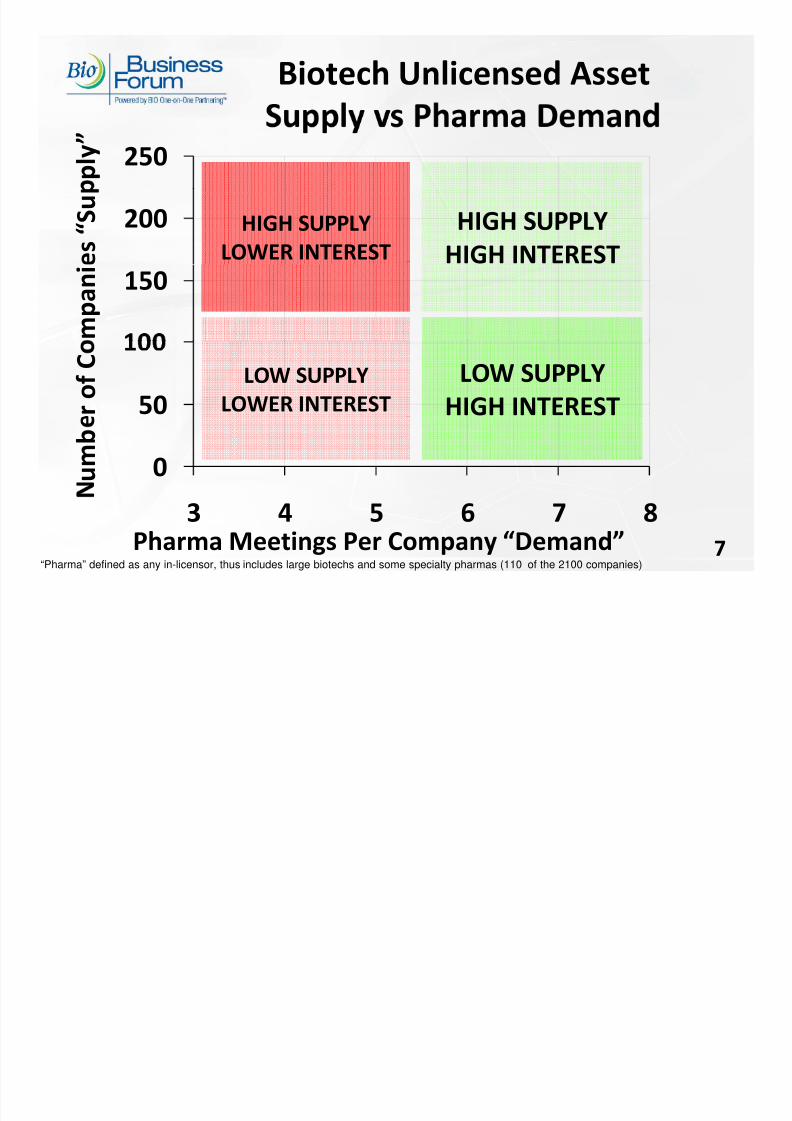

Biotech Unlicensed Asset

p l y ”

250

HIGH SUPPLY

LOWER INTERESTHIGH SUPPLY

HIGH INTEREST e s “ S u

200

m p a n i

150

LOW SUPPLY

LOWER INTEREST

LOW SUPPLY

HIGH INTEREST r o f C

50

u m b

0

Pharma Meetings Per Company “Demand”

3 4 5 6 7 8

“Pharma” defined as any in-licensor, thus includes large biotechs and some specialty pharmas (110 of the 2100 companies)7

8/6/2019 2010 BIO Business Forum Partnering Results - Final

http://slidepdf.com/reader/full/2010-bio-business-forum-partnering-results-final 8/14

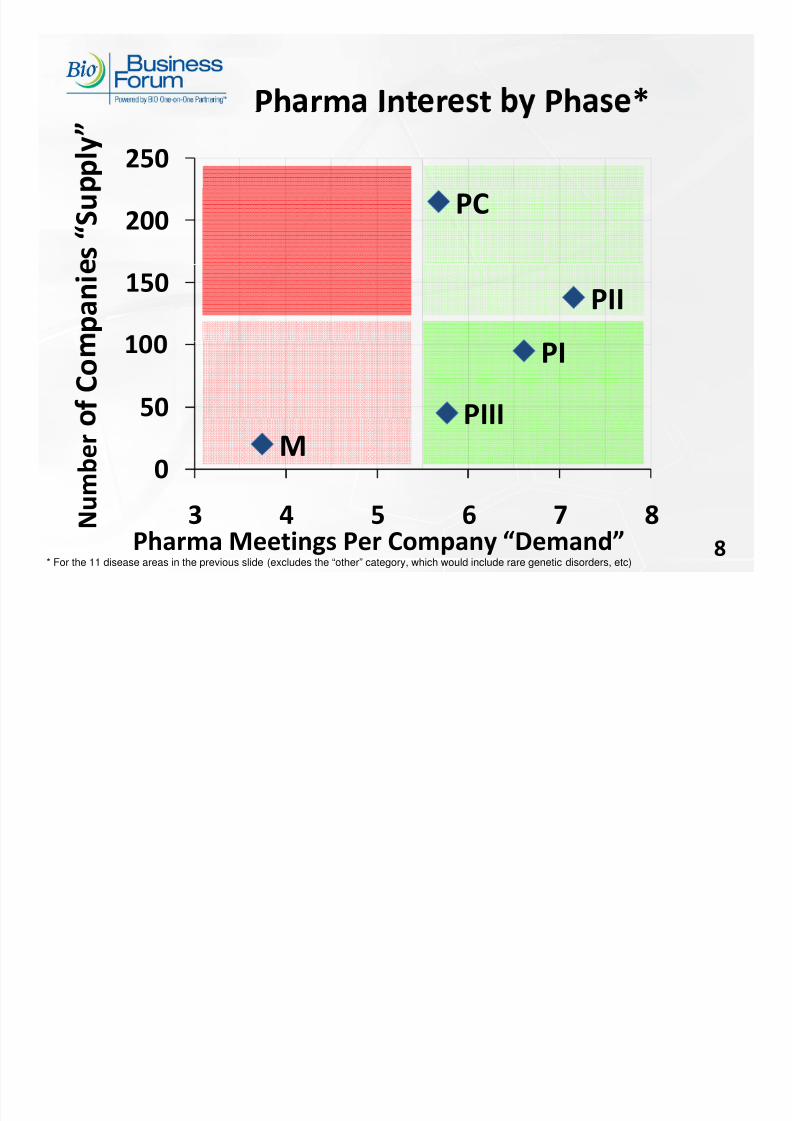

Ph rm Int r t Ph *250 p

l y ”

PC200 s “ S u

PII150

p a n i

PI

50 f C o

M0

m b e r

3 4 5 6 7 8

Pharma Meetings Per Company “Demand” N u

* For the 11 disease areas in the previous slide (excludes the “other” category, which would include rare genetic disorders, etc)8

8/6/2019 2010 BIO Business Forum Partnering Results - Final

http://slidepdf.com/reader/full/2010-bio-business-forum-partnering-results-final 9/14

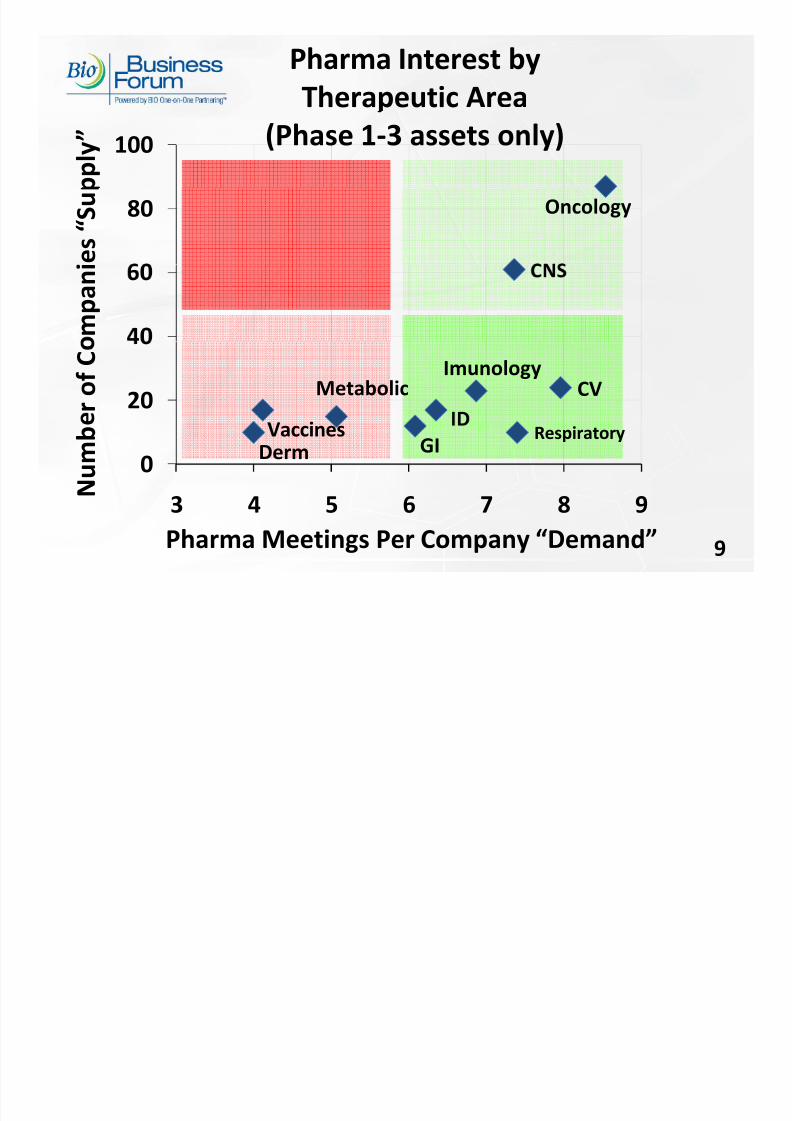

Pharma Interest by

Therapeutic

Area

100

p p l y ” (Phase 1‐3 assets only)

Oncology80

e s “ S

u

m

p a n i

CVImunology

Metabolic20 r

o f C

Vaccines GIDermRespiratory

0 N u m b

3 4 5 6 7 8 9

Pharma Meetings Per Company “Demand” 9

8/6/2019 2010 BIO Business Forum Partnering Results - Final

http://slidepdf.com/reader/full/2010-bio-business-forum-partnering-results-final 10/14

Pharma Interest by

Phase 1‐3 & Thera eutic Area

THERAPEUTIC AREAS (11) PHASE

# COMPANIES

PHARMA MEETINGS PER COMPANY

GI PII 4 9.5

Oncology PII 46 8.9

CV PI 9 8.8

CV PII 7 8.7

CNS PII 30 8.5

Oncology PI 28 8.2

Oncology PIII 13 8.0

Immunology PII 15 7.7

CNS PIII 9 7.6

CV PIII 8 6.4

6 of the top 10 are Phase I or II**Table excludes pre-clinical

10

8/6/2019 2010 BIO Business Forum Partnering Results - Final

http://slidepdf.com/reader/full/2010-bio-business-forum-partnering-results-final 11/14

Take Home Messages

One‐on‐one partnering meetings can e use to

assess forward looking dealmaker intentions

Phase II assets are in high demand

Oncology & CNS have high supply & high

interest

CV Res irator & Immunolo have hi h

interest and lower supply

11

8/6/2019 2010 BIO Business Forum Partnering Results - Final

http://slidepdf.com/reader/full/2010-bio-business-forum-partnering-results-final 12/14

Campbell Alliance 2010 Dealmakers’

Intentions Panel Discussion

Chair: Ben Bonifant, Vice President and Head, Business Development Practice, Campbell Alliance

Chair: John Craighead, Ph.D., Managing Director, Investor Relations &

Business Development, Biotechnology Industry Organization

BJ Bormann Ph.D. Senior Vice President & Global Head Business

Development, Boehringer Ingelheim

Shaun Grady, Vice President, Strategic Partnering & Business

eve opmen ,

s ra enecaPaul J. Hastings, President and Chief Executive Officer, OncoMed

Pharmaceuticals

James Sabry, M.D., Ph.D., Vice President, Genentech Partnering,

Genentech 12

8/6/2019 2010 BIO Business Forum Partnering Results - Final

http://slidepdf.com/reader/full/2010-bio-business-forum-partnering-results-final 13/14

Alan F. Eisenberg Amy Finan

t a es a age…

,

Companies & Business Development

,

Development & Marketing

John Craighead, PhD

Managing Director, Investor Relations

John Sloan

Managing Director, External

Jason Rupp

Managing Director,

& Business Development Relations & Development Membership

Cartier Esham, PhD

Director, Emerging Companies

Health & Re ulator Affairs

Susanna Ling

Director, Sponsorship,

Cor orate Dev & Marketin

Shelly Mui‐Lipnik

Director, Capital Formation &

Financial Services Polic

David Thomas

Director, Industry

Research & Anal sis

Wesley Triplett

Director, BD Marketing

Jen Welch, CMP

Director, Meetings &

Operations

Fred Zeldow

Director, Business Development &

Strategic Alliances

Bernadette Blake

Manager, Registration

& Customer Service

Joe Colangelo

Manager, Business

Development

Celia Economides, MPH

Manager, IR & Corporate

Strategy

Tamy Dalal

Manager, BD &

Strategic Alliances

Elizabeth Gaskins

Manager, Membership

Rena’e Grant

Manager,

Partnering Programs

Tom Heebink

Manager, BD &

Strategic Alliances

Amy Nguyen

Manager, IR & BD

Event Programs

Beth Rosenkoetter

Manager,

Sponsorship

Tooshar Swain

Manager, Policy

& Research 13

8/6/2019 2010 BIO Business Forum Partnering Results - Final

http://slidepdf.com/reader/full/2010-bio-business-forum-partnering-results-final 14/14

Visit us online at insidebioia.com

14