©2011 cengage learning part iv: the secondary money market

TRANSCRIPT

©2011 Cengage Learning

PART IV:

The Secondary Money Market

©2011 Cengage Learning

Chapter 12: Shipping and Servicing

By Dr. D. Grogan

M.C. “Buzz” Chambers

©2011 Cengage Learning

PREVIEW The loan broker is prohibited from servicing the loan after the loan has funded. The

borrower may believe that the monthly payments are made payable to the loan broker.

The secondary money market is designed to match borrowers with available lending funds. Demand is often not matched with the money supply within the same area.

Government regulates funds that move from international investments, across state lines and between banks. This chapter discusses protecting the funds of the investor by explaining how the secondary money market works. The flow of capital funds moves from the initial investor through the primary market, in which the lender makes the original loan, to a consumer-borrower. The borrower makes payments to a loan servicer, who, in turn, forwards the collected funds to the investor. Loan servicing has a national code of behavior for the industry.

Discuss alternatives and trends in the markets. Real estate loans are traded as securities, similar to money for bonds and stocks.

Real estate economics knowledge to better predict trends. To aid in understanding markets, long-term interest rates, consumer confidence, employment changes, housing affordability, and numbers of loan originations are reviewed.

©2011 Cengage Learning

Student Learning Outcomes1. Outline the components of loan shipping and servicing.

2. Identify Department of Corporation (DOC) and Department of Real Estate (DRE) securities dealer transactions and regulations.

3. Explain how the general real estate economic market affects loans.

4. Diagram the flow of funds from investor to borrower and from borrower to investor.

5. Describe discounts and yields used by lenders’ and investors’ property loans.

6. Discuss the DRE regulations concerning loan types.

7. Explain the national code of behavior for the loan servicing industry.

©2011 Cengage Learning

12.1 Shipping The lender receives the closing documents from

escrow prior to recordation. The loan servicing department of the lender

assimilates the exact stacking order for the final documents adding: Title insurance policy Hazard insurance, assignment & endorsements Final HUD settlement closing statement

The file is ready to be presented to the investor.

©2011 Cengage Learning

Loan Originator

The initial lender who approved and funded the loan.

Must disclose the intent to transfer the loan for loan servicing.

Borrower must sign loan servicing agreement with original loan documents.

Makes loans in the primary market.

©2011 Cengage Learning

Originator: Mortgage Company Not regulated on loan term or L-T-V ratio. Must comply with Real Property Loan Law. Specialize in specific types of loans:

Junior liens Mini-warehouse storage Medical office building Condominiums

©2011 Cengage Learning

12.2 Loan Servicing Loan servicing collects the payments from the

borrower. Loan servicing divided the payment for the

various disbursements. Loan servicing verifies insurance coverage and

property tax payments. Loan servicing notifies parties of default. Loan servicing coordinates foreclosure

proceedings.

©2011 Cengage Learning

Payment to Loan Servicing

1. Monthly billing – lender mails payment notice (computer printout); borrower mails payment with stub.

2. Coupon – lender sends borrower 12 coupons, once a year.

3. Direct deposit – lender automatically deducts payment from borrower’s account.

4. On-line debit – borrower dials in and accesses on-line account to make bill payment.

©2011 Cengage Learning

Monthly PaymentIt’s “A PITI” to have to make the payment!

rincipal

nterest on the loan

axes on the property

nsurance

ssociation dues

©2011 Cengage Learning

Loan Servicer collects:

A PITI Impounds for property taxes Impounds for insurance reserve

Hazard, fire, disaster (earthquake/flood) insurance Late fees Advance fees are not allowed in California

©2011 Cengage Learning

Collections Within 10 days for receipt of payment, the

loan servicer must give written notice to the mortgagee, beneficiary or owner of: Date the payment was received Total amount of the payment Name of the person who made the payment Source of the funds Reason for making the payment

©2011 Cengage Learning

Loan Servicer

Compensated for performing services Collecting payments for borrower, lender, owner

Loans secured by real property or a business opportunity

Real property sales contracts RMLA (1/1/1996)-servicer license thru DOC

©2011 Cengage Learning

Loan Servicer (continued) Services Instruct trustee to proceed with:

NOD – Notice of Default NOS – Notice of trustee’s Sale

Borrower Dispute: Borrower to document, in writing, payment and

servicer notification of problem/error If no satisfactory response within 30-60 days, file

a complaint with DRE or DOC.

©2011 Cengage Learning

Loan Servicer (continued) The loan administration that maintains the

loan terms during the life of the loan. Involves instructions from the lender on:

Monitoring the loan Assuring faithful compliance of borrower duties Adhering to covenants outlined in loan terms

©2011 Cengage Learning

Loan Servicer (continued)

Who may act as the loan servicer? Mortgage loan banker Mortgage loan correspondent :

Represents a single entity Originates the loan May service loans for some lenders

Private lender May make loans directly to borrower Term usually: short; maximum interest rate

©2011 Cengage Learning

Loan Servicer (continued) Who may NOT act as the loan servicer?

Mortgage loan broker

Companies chartered out-of-state

©2011 Cengage Learning

Loan Administration Duties Adhere to terms of the note and trust deed:

Administer monthly loan payment records Post payment of funds received Issuance of statements or coupon book Bill for late fees Maintain impound account for insurance and taxes

Interest required on impound account 2% per annum for impound funds held

Enforce property maintenance requirements Notify parties in case of default

©2011 Cengage Learning

Loan Administration Duties (continued)

Handle loan pay off request Surrender loan document to borrower Obtain Reconveyance Deed for the lien Distribute funds to the beneficiary

Adhere to loan assumption provisions Administer property tax collection and payment Impound account required for DVA or FHA loan

©2011 Cengage Learning

California Usury Law Maximum rate of 10% for consumer loans Maximum rate for real estate loans:

10% or 5% above 11th District San Francisco Federal Reserve Bank discount rate

Exempt from Usury Law: Loans arranged or made by Real estate broker Loans made by a bank or savings & loan

©2011 Cengage Learning

Termination of Loan Servicing

Loan payoff: Furnishes information on: Unpaid loan balance Accrued late fees, penalties and charges Impound account shortage Beneficiary Demand Statement

Foreclosure: Beneficiary notifies trustee to begin foreclosure proceedings

Transfer of loan servicing to another entity Assignment: Beneficiary assigned loan to another Assumption: New trustor takes over existing loan

©2011 Cengage Learning

12.5 Security Dealer Pledge: Something deposited or given as assurance for

the fulfillment of an obligation. Securities dealer: one who undertakes to fulfill the

obligation of another, and to transact business on behalf of another. A person with information on stocks, bonds, T-bills &

money market investments. Article 6 of Real Estate Law covers real property

securities dealers by DRE licensees.

©2011 Cengage Learning

DRE Real Property Security

Code, Part 1: An agreement made in connection with: arranging a loan loan has a promissory note on real property note is secured directly or collaterally as a lien on real

property Includes the sale of a promissory note secured

by real property.

©2011 Cengage Learning

Guaranteed Note Guarantee the note or contract against loss of any kind at any time. Guarantee that payments of principal or interest will be paid in

conformity with that terms of the note or contract. Assume any payments necessary to protect the security of the note

or contract. Accept partial payment for funding the loan or purchasing the note or

contract. Guarantee a specific yield or return on the note or contract. Pay with his or her own funds any interest or premium for a period

prior to actual purchase and delivery of the note or contract. Repurchase the note or contract.

©2011 Cengage Learning

DRE Real Property Security

Code, Part 2: The real estate broker who: arranges the loan negotiates the sale of the note is servicing the note secured by real property

Payments made to the owner by a broker must be made from the funds of the obligor.

Exempt: Seller carry-back, Land sale contract

©2011 Cengage Learning

DRE Real Property Security Code, Part 3: Promotional note:

used with liens on or sale of real property in a subdivision.

the provision does not include a note more than 3 years before being offered for sale, or

secured by a first trust deed. See Corporate Securities Law (CSL) of 1968 and

as amended: http://www.legisinfo.ca.gov

©2011 Cengage Learning

12.4 Types of Securities

80% of loan originations go through the secondary money market as securities: GNMA-(Ginnie Mae) Government National Mortgage Association FNMA-(Fannie Mae) Federal National Mortgage Association FHLMC-(Freddie Mac) Federal Home Loan Bank Corporation

Mortgage-Backed Securities Program increases funds in the secondary mortgage market to attract new sources of financing for real estate loans.

©2011 Cengage Learning

12.5 Secondary Market Promotes Real Estate Investments, Provides Stability

$Mtg.

Note

NoteMtg.

$

Borrower

LenderInvestor

PrivateFNMAGNMAFHLMC

Primary Market

Secondary Market

©2011 Cengage Learning

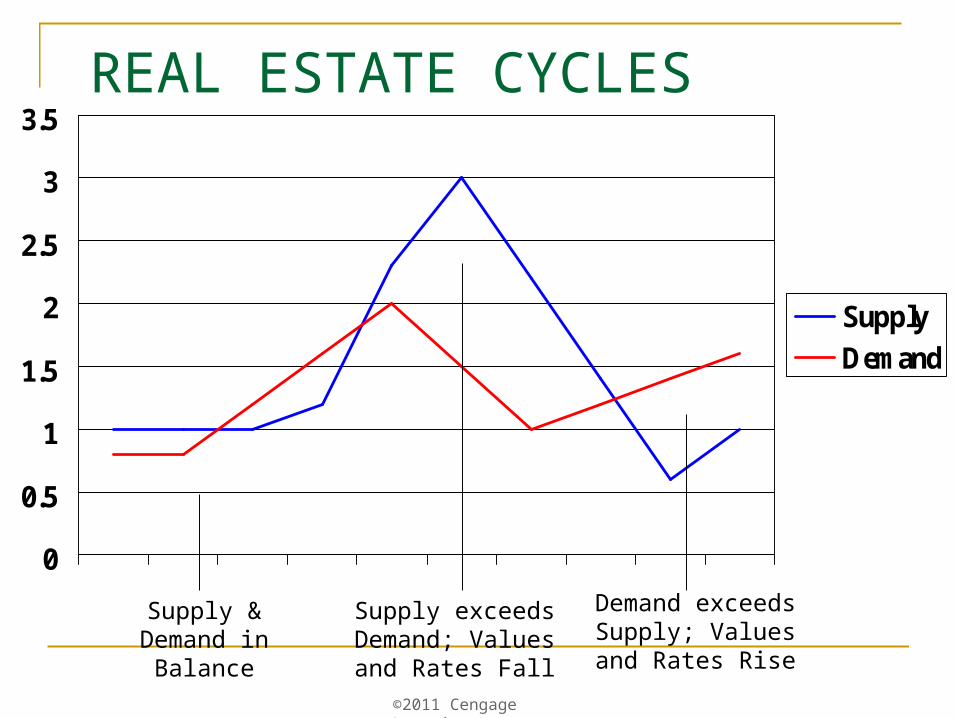

REAL ESTATE CYCLES

0

0.5

1

1.5

2

2.5

3

3.5

Supply

Demand

Supply & Demand in

Balance

Supply exceeds Demand; Values and

Rates Fall

Demand exceeds Supply; Values and

Rates Rise

©2011 Cengage Learning

Real Estate Economics: 30-year Fixed-rate contract rate1971-2009

©2011 Cengage Learning

Real Estate Economics: Consumer Confidence 1967-2007

©2011 Cengage Learning

Real Estate Economics: Unemployment (1965-2010)

©2011 Cengage Learning

Real Estate Economics: Affordability (1992 – 2009)

©2011 Cengage Learning

Real Estate Economics: Consumer Price Index 1913-2009

©2011 Cengage Learning

Real Estate Economics: Federal Deficit (1900-2007)

©2011 Cengage Learning

Real Estate Economics:Institutional Money Funds (1974-2009)

©2011 Cengage Learning

Real Estate Economics: Discount Window Borrowings of Depository Institutions from the Federal Reserve (1959-2009)

©2011 Cengage Learning

12.6 Secondary Money Market: Investor Protection Article 5 – loan fee disclosure Article 6 – Multi-lender (fractionalized) loans Article 7 – loan origination and servicing

©2011 Cengage Learning

Secondary Money Market Function to the originating lender:

Generates loans directly to borrowers Termed the Primary Money Market

Secondary Money Market: Involves the sale of existing notes that were

originally made in the primary market. Investors purchase notes secured by real

property. Investor tends to hold the loan over a longer

period of time to generate income revenue.

©2011 Cengage Learning

Loan Servicer Relationship Assignment agreement in the loan note

Mortgage bankers usually service loans they generate

Mortgage brokers cannot service loans they generate

©2011 Cengage Learning

12.7 Packaging & Selling Loans

Institutional lenders making less direct loans. Large investors include:

Pension funds Endowment funds Insurance company investments Foreign investors Mutual funds Real estate investment trusts (REITs)

©2011 Cengage Learning

12.8 Yield Spread Premium (YSP)

The points, charges and fees paid by lenders for high-rate loans. Points: An upfront charge (a %) of the loan). The points

increase the loan yield, or return. Loan broker receives fees as reasonable compensation for services

actually rendered. Loan broker may report the value over par for the loan, with a

premium rate as a YSP paid to the loan broker and reported in the “200” series line item on the GFE and HUD-1.

©2011 Cengage Learning

12.9 National Code of Real Estate Loan Servicing Industry Prohibits predatory practices and include:

Loan servicing firms must follow detailed requirements designed to properly credit on-time loan payments.

Loan servicers cannot force high cost hazard insurance policies on borrowers.

Loan companies cannot impose fees on borrowers for services not specifically sanctioned in the loan documents.

©2011 Cengage Learning

Federal code of conduct prohibits

Unfair, misleading or deceptive debt collection techniques on real estate loans.

Using negative monthly reports about false delinquencies to squeeze funds from borrowers.

Knowingly providing false credit report data. Failing to respond to a customer inquiry & complaint within 20 days after

inquiry receipt & resolution within 60 days. Failing to maintain adequate toll-free call center operations for handling

complaints & questions. Taking quick foreclosure action before verifying the consumer failed to

make full payments for three months.