2011/12 - cse

TRANSCRIPT

2011/12A dynamicyear ofachievementCommercial Leasing & Finance Ltd Annual Report 2011/12

Commercial Leasing & Finance Ltd

Commercial Leasing & Finance LtdRegistration No : PQ 131 PB

P.O. BOX 690,No. 68, Bauddhaloka Mawatha,

Bambalapitiya, Colombo 04, Sri Lanka.Phone (Hunting) : (011) 4 526526,

Fax : (011) 2559510, 4526517, 4526559E-mail : [email protected] Web : www.clc.lk

Commercial Leasing & Finance Ltd. is rated A-(lka) by Fitch Ratings Lanka Ltd., licensed by Monetary Board of the Central Bank of Sri Lanka under the Finance Business Act No. 42 of 2011. Date of incorporation 22/04/1988.

23% G

rowth in Asset Ba

se.

Through the partnership with

Associated Motorways PLC, executed

over 1,300 leases for Suzuki Maruti

branded vehicles within 5 months.

2.8% NPL Ratio.

Rs. 3.2 Bn Profit Before Tax.

Com

mer

cia

l Lea

sing

con

verte

d to

a

Fina

nce

Com

pa

ny.

Com

ple

ted

a d

yna

mic

yea

r of

bus

ines

s.

50th

Bran

ch w

as o

pene

d in

Kilino

chch

i.

Fixed and Savings deposit products

were launched.

Rs. 6.6 Bn Shareholders' Funds.

Total foreign funding lines

exceeding Rs. 3 Bn.

54% G

rowth in Incom

e.

Co

mm

erc

ial Le

asing

& Fina

nce

Ltd | Annua

l Rep

ort 2011/12

First

financ

ial instit

ution t

o open a

dedicated Fa

ctorin

g bra

nch o

utside

Colombo,

in Ka

ndy.

To soar into the future, giving wings to the dreams, hopes and aspirations of our people and everyone who has a stake in the success of our enterprise.

To forge ahead to reach new frontiers, to touch new horizons, seeking new challenges and exploring new opportunities.

Together with our people with diverse strengths, committed to achieving personnel excellence and the continuous growth of our enterprise.

Vision

Name of the Company

Commercial Leasing & Finance Ltd

Country of Incorporation

Sri Lanka

Legal Form

A quoted public company with limited liability

Date of Incorporation

22nd April 1988

Company Registration No.

PQ 131 PB

Principal Activities

During the year the principal activities of the

Company comprised provision of leasing, hire

purchase, loans and other lending products,

Having received a finance company license,

the activities expanded to include mobilizing

of fixed and savings deposits.

Company Secretary

Miss Chrishanthi S. Emmanuel, FCIS, FCCS

Auditors

KPMG, Chartered Accountants

Lawyers

Julius & Creasy, Attorneys-at-Law

Nithya Partners

Corporate Information

Registrars

PW Corporate Secretarial (Private) Ltd

Bankers

Bank of Ceylon

Standard Chartered Bank PLC

Citi Bank N A

Hatton National Bank PLC

Hongkong and Shanghai Banking Corporation Ltd

Deutsche Bank

Nation Trust Bank PLC

Commercial Bank of Ceylon

NDB Bank

Seylan Bank PLC

MCB Bank

Pan Asia Bank

Sampath Bank

DFCC Vardhana Bank

Union Bank

People’s Bank

Habib Bank

Registered Office

No. 68, Baudhaloka Mawatha, Colombo 04.

ContentsFinancial Highlights 2

Chairman’s Message 6Director/Chief Executive Officer’s Review 8

Message from the Director 10Board of Directors 12

Board of Directors’ Profiles 13Management Team 17

Management Discussion & Analysis 19Our Outreach 23

Financial Review 24Risk Management 26Corporate Governance Report 30

Financial InformationAudit Committee Report 50Integrated Risk Management Committee 51Remuneration Committee Report 52Directors’ Report 53Directors’ Statement on Internal Controls 58Chief Executive Officer’s and Chief Financial Officer’s Responsibility Statement 60Independent Auditor’s Report 61Income Statement 62Balance Sheet 63Statement of changes in equity 64Cash Flow Statement 65Accounting Policies 67Notes to the Financial Statements 73

Shareholder Information 88Ten Year Summary 89

Sources and Distribution of Income 90Statement of Value Added 91

Notice of the Meeting 92Notes 93

Form of Proxy 95

Produced by Copyline (Pvt) Ltd Printed by Gunaratne Offset Ltd

1Commercial Leasing & Finance Ltd. Annual Report 2011/12

Commercial Leasing & Finance Limited

Now operates as a fully fledged finance company, offering a range of financial services. Our main services are fixed deposits, savings, leasing, factoring, hire purchase, loans and hiring.

A dynamic year of achievement2011/12 A dynamic year of achievement – what better way to celebrate our momentous progress from leasing to finance than completing a year that showed exceptional & unmatched results. And with the years ahead providing opportunities and challenges that will allow us to grow beyond our limits, we are enthused to carry on this growth and transformation as we serve you, our stakeholders, in more ways than before. Our progress is a testament to our resilient and dynamic nature and we will focus on the future with determination and optimism.

2 Commercial Leasing & Finance Ltd. Annual Report 2011/12

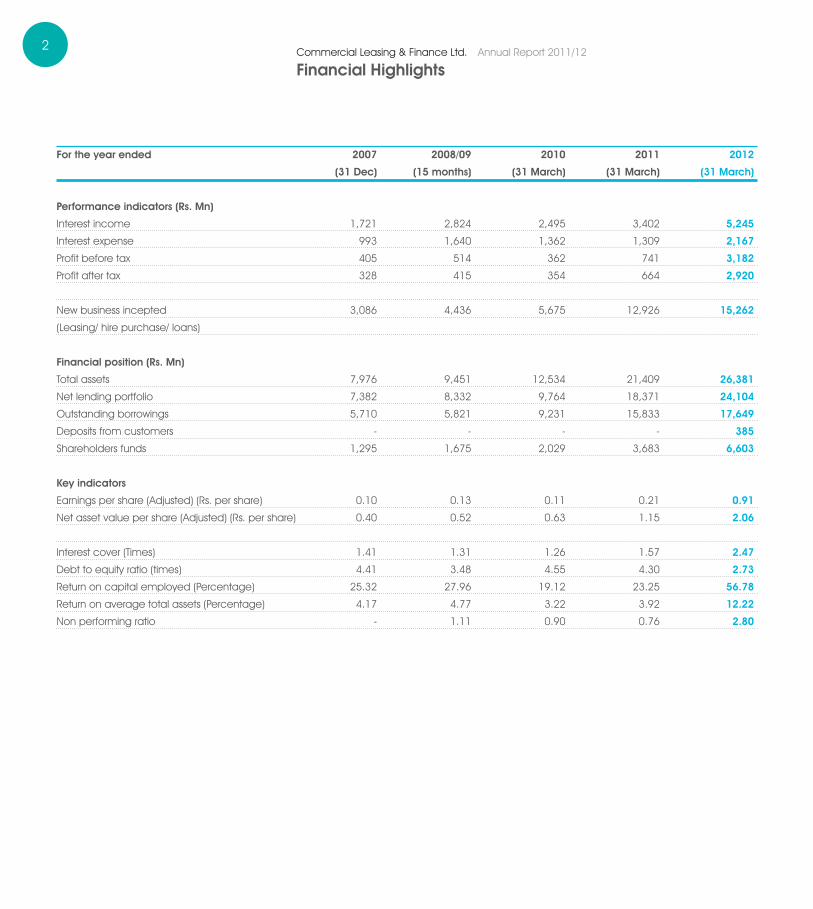

Financial Highlights

For the year ended 2007 2008/09 2010 2011 2012

(31 Dec) (15 months) (31 March) (31 March) (31 March)

Performance indicators (Rs. Mn)

Interest income 1,721 2,824 2,495 3,402 5,245

Interest expense 993 1,640 1,362 1,309 2,167

Profit before tax 405 514 362 741 3,182

Profit after tax 328 415 354 664 2,920

New business incepted 3,086 4,436 5,675 12,926 15,262

(Leasing/ hire purchase/ loans)

Financial position (Rs. Mn)

Total assets 7,976 9,451 12,534 21,409 26,381

Net lending portfolio 7,382 8,332 9,764 18,371 24,104

Outstanding borrowings 5,710 5,821 9,231 15,833 17,649

Deposits from customers - - - - 385

Shareholders funds 1,295 1,675 2,029 3,683 6,603

Key indicators

Earnings per share (Adjusted) (Rs. per share) 0.10 0.13 0.11 0.21 0.91

Net asset value per share (Adjusted) (Rs. per share) 0.40 0.52 0.63 1.15 2.06

Interest cover (Times) 1.41 1.31 1.26 1.57 2.47

Debt to equity ratio (times) 4.41 3.48 4.55 4.30 2.73

Return on capital employed (Percentage) 25.32 27.96 19.12 23.25 56.78

Return on average total assets (Percentage) 4.17 4.77 3.22 3.92 12.22

Non performing ratio - 1.11 0.90 0.76 2.80

3Commercial Leasing & Finance Ltd. Annual Report 2011/12

2007

0

6,000

5,000

3,000

2,000

4,000

1,000

Rs. Mn

2008

/09

2009

/10

2010

/11

2011

/12

Interest Income to Interest expense

Interest income

Interest expense

2007

0 0

7,000

6,000

60

5,000

50

3,00030

2,00020

4,000

40

1,000 10

Rs. Mn %

2008

/09

2009

/10

2010

/11

2011

/12

Shareholders' Funds and ROCE

Shareholders funds

Return on capital employed

2007

0

20,000

15,000

5,000

10,000

Rs. Mn

2008

/09

2009

/10

2010

/11

2011

/12

New Business Incepted

2007

0

3,500

2,500

3,000

500

1,000

1,500

2,000

Rs. Mn

2008

/09

2009

/10

2010

/11

2011

/12

Net Profit After Tax

Beginning our journey in 1988, we are proud to celebrate the addition of another facet to our gamut of financial solutions.As we progressed from leasing to become a fully fledged financial institution, we look forward to continuing our reputation as a flexible, dynamic entity that is prepared to serve a whole new range of consumers who trust our brand of financing options. 24 years have culminated in this outstanding milestone and we remain hopeful for the years ahead as we expand and grow to accommodate the growing needs of a rapidly developing nation.

6 Commercial Leasing & Finance Ltd. Annual Report 2011/12

Dear Shareholder,It gives me great pleasure to welcome you to the first Annual General Meeting of Commercial Leasing & Finance Ltd as a public listed company, and to share with you the best ever result achieved by the company.

Economic EnvironmentThe buoyancy of Sri Lanka’s post war economy in 2011 provided an ideal environment for the growth achieved by the financial sector. Sri Lanka’s economy sustained its high growth momentum surpassing last year’s record high to grow by 8.3 % in 2011. This was amidst several political and economic challenges in the world economy. Improved consumer and investor confidence in Sri Lanka; favourable macroeconomic conditions, increased capacity utilisation, expansion of infrastructure facilities and renewed economic activity in the Northern and Eastern provinces underpinned this growth. Subdued inflation, at mid single digit levels; and low interest rates, during the year were particularly beneficial to the Licensed Finance Companies (LFC) sector.

Sri Lanka’s Per Capita income increased to US Dollars 2,836 from previous year’s 2,400; whilst a further decline in the unemployment level, to reach the lowest ever rate of 4.2 % was another positive indicator of Sri Lanka’s high growth trajectory. These factors saw Sri Lanka advance from the “low income” category to be placed amongst “middle income economies” in the world.

PerformanceIn such a high growth environment which was most conducive to business, your company achieved a Profit After Tax of Rs. 2.9 Bn, which is a remarkable 339% growth over the previous year; whilst Profit Before Tax reached Rs. 3.2 Bn. This was once again a performance which surpassed that of the industry. The total portfolio grew by 31% to reach Rs. 24 Bn. A strong branch network, a unique operating model, and the dedication and commitment of our entire team of employees were the most significant contributors to this performance.

The company’s Non Performing Loan (NPL) Ratio at 2.8% is amongst the lowest in the industry, facilitated by the collection efficiency of our team. Commercial Leasing Company, became a member of the LOLC Group four years ago, and has since then, evolved from a medium sized leasing company to be amongst the top five players in the industry with results that continue to be above industry performance. Post-acquisition, with the synergies of LOLC, your company grew in leaps and bounds. The disbursements, which we coin as ‘executions’ has grown from Rs. 3 Bn to Rs. 15 Bn within four years and the corresponding asset base has grown from Rs. 8 Bn to Rs. 26.3 Bn making Commercial Leasing one of the rapidly growing, leading leasing player, particularly in the lower end of SME and urban micro sectors. And it is also noteworthy that this level of growth has been achieved organically.

ChairmanCommercial Leasing & Finance Ltd.

Chairman’s Message

PAT of Rs. 2.9 Bn, a remarkable growth of 339%

7Commercial Leasing & Finance Ltd. Annual Report 2011/12

AchievementsThe year under review also saw your company surpass two other milestones. It broadened its sphere of business to become a Registered Finance Company; and Commercial Leasing Company was hence renamed Commercial Leasing & Finance Ltd (CLC). We now look to the year ahead with added vigour to harness the numerous new opportunities that this progression springs up.

The other landmark reached was the listing of 10% of CLC’s shareholding in the Colombo Stock Exchange, converting it to a Public Listed Company in June 2012. On behalf of the Board of Directors and all our members of staff I would like to take this opportunity to express my sincere appreciation to the Central Bank of Sri Lanka and other regulatory authorities for granting approval for CLC to make the transition, to a public listed company, and to a licensed deposit taking enterprise, - which is also an endorsement of the strength and stability of your company.

These significant strides made by CLC during the past four years in particular, have enabled a performance which better reflects its true potential. These achievements would not have been possible without the dedication, enthusiasm and initiative of the entire team at CLC, which I would like to note with much gratitude.

The year 2009 saw a significant achievement as CLC became one of the few Sri Lankan finance companies to be funded by couple of leading international funding agencies, namely FMO, Triodos and the Asian Development Bank (ADB). This has enabled your company to strike a healthy balance in the funding mix with more than 25% accounting for foreign funding at competitive rates. This is also a valuable recognition of the role we play in Sri Lanka’s economic progress and an endorsement of the high standards of governance and management at CLC. We also appreciate the opportunity these relationships offer us to continuously raise the bar for ourselves- whether it be in technical know how or by being abreast of latest in best practices in corporate governance and risk management.

Strategy and Future DirectionOur core area of business has been in lending to Micro and Small and Medium scale Enterprises (SME sector) of the country. This has given us an opportunity to make a valuable contribution in

achieving some of the nation’s macro economic goals, such as reducing the geographical disparity of income distribution, and empowering those who otherwise have no access to formal channels of credit. This contribution we can make to the country’s economic growth is one which we hold high, and is intrinsic to the long term approach to enterprise that we have adopted. It springs from our belief that sustainability of an entity’s profits ultimately depend on the sustainability of the community and environment that it is part of. Our island wide branch network has also helped in employment generation and enabled us to become an integral part of empowering and enriching many rural communities across the country.

Our strategies for the future will see us intensify our focus on micro finance, rural and agri lending, and thereby play an enhanced role in the country’s high growth trajectory.

A key sector in CLC’s SME portfolio has been the Agricultural sector, a thrust area of economic growth identified by the government. We are also particularly proud to have been an active player in the post war resurgence of the North & East, where by providing credit facilities we have been able to help rebuild lives and livelihoods; and build hitherto dormant skills and the entrepreneurial spirits of a people. CLC will continue to strengthen its presence in the North & East and to contribute to uplift living standards across the country.

CLC’s model of “Business Introducers” is one which is unique, and has been a key element of the company’s rapid growth and remarkable performance. The company will hence expand this island wide network whilst continuing to build on the confidence and commitment of its existing network of over 2,500 “Business Introducers”.

The initiative of opening window offices in the local post office is another which has served the company well in its integration into the rural communities.

Your company will continue to harness the synergies of CLC and LOLC. The customer trust and confidence that the brand CLC has earned over the past 24 years, combined with the operational excellence and the management expertise of LOLC Group, find CLC well poised to capitalize on the many opportunities that I foresee. This is particularly so as the potential in micro and SME sectors of the economy is still largely untapped.

Macro economic imbalances in the economy necessitated several new policy measures by the government at the beginning of year 2012. The resulting environment of a weaker currency, higher interest rates and import taxes and an expected rise in cost of living, has necessitated that we review some of our strategies to respond as appropriate to these changing dynamics.

AcknowledgementsI wish to express my sincere appreciation to my colleagues on the Board for their invaluable support and encouragement and for the confidence placed in me. My most sincere appreciation also to our entire team that makes up CLC, whose focused approach, passion and commitment have been indispensable to achieving an excellent financial performance. I also extend my gratitude to our shareholders, customers and business partners and other stakeholders for their confidence which continues to inspire us to reach greater heights.

Ishara NanayakkaraChairman

8 Commercial Leasing & Finance Ltd. Annual Report 2011/12

It is my pleasure to present to you the review of a record performance and an year of several milestones.

Surpassing MilestonesThe year under review was a landmark year for Commercial Leasing Company (CLC) for many reasons. Most significantly, CLC, which has been a leasing company since its inception 24 years ago, was able to obtain Central Bank approval to become a Finance Company. CLC was thus renamed Commercial Leasing & Finance Ltd during the year. This enhanced role has presented us with many new opportunities; and we look to the year ahead with much enthusiasm to offer a broader portfolio to our customers and to capitalize on these opportunities. The transition also brought with it several challenges; such as the need for a change in outlook and employee orientation and training; the need for new policy and procedural manuals and to create market awareness of our enhanced scope. It was a noteworthy achievement that CLC was able to launch into deposit taking within one month of being registered as a finance company, and I would like to note with gratitude the effort by our entire team at CLC, that made it possible.

Subsequent to the year under review also saw another milestone as CLC made a transition to become a public listed company, meeting the regulations of the new Finance Business Act No. 42 of 2011; by listing 10% of the company’s shareholding in the Colombo Stock Exchange.

CLC opened its 50th branch in February 2012, in Killinochchi. This became our 8th branch in the North & East of the country, and is a reflection of our commitment to support the socio-economic revival in these areas.

PerformanceSupported by an environment of high economic growth and low interest rates in 2011 which was most conducive to business, CLC recorded significant growth and achieved its best performance to date.

Profits Before Tax grew by a significant 329% to reach Rs. 3.2 Bn compared with Rs. 741 Mn the previous year, whilst Profit After Tax reached Rs. 2.9 Bn. The growth in profits stemmed mainly from the increase in interest income which grew by 54%. A very successful marketing strategy, operational excellence, an effective, balanced credit policy and guidelines were factors which drove this performance.

Director/Chief Executive OfficerCommercial Leasing & Finance Ltd.

Director/Chief Executive Officer’s Review

Broader solutions to customers

9Commercial Leasing & Finance Ltd. Annual Report 2011/12

The portfolio recorded steady growth over the previous year, increasing by 31% to Rs. 24 Bn. Reflecting this growth in the portfolio, Revenue also increased to Rs. 5.2 Bn compared with Rs. 3.4 Bn the previous year.

The Non Performing Loan (NPL) ratio during the year was amongst the industry best, at 2.8%. And this achievement is made all the more significant in the context of the high portfolio growth during the period; thus reflecting the fact that the quantum increase in the portfolio came without a compromise on quality. It is also a reflection of the commitment and dedication of our recovery staff.

Our pioneering decision to introduce factoring into rural areas has proven to be a wise one, and has also enabled Commercial Factors to enjoy first mover advantage in this niche market. The factoring business which constitutes 11% of our total portfolio contributed 15% to revenue during the year under review. Factoring also contributed to the increase in interest income, with a 73% growth over the previous year, to reach Rs. 795 Mn.

The Company also made a structural change of divesting its investment in Diriya Investments, thereby making a capital gain of Rs. 2 Bn during the year under review with a capital base of Rs. 6.6 Bn. The Company is one of the most capitalized Finance companies in Sri Lanka with a debt to equity ratio of 1:2.7. The opportunity to mobilise deposits as a finance company would further strengthen our funding base in the year ahead. CLC is one of the few Sri Lankan finance companies whose funding base extends to credit lines from international agencies, which include FMO, Triodos and the Asian Development Bank (ADB). The company thus stands well poised to meet the challenges of tomorrow and further accelerate the growth recorded over the past few years. Our association with these leading international funding institutions provides us with a valuable advantage which underscores the potential of the company.

Future GrowthThe strength of our Business Introducer model continued to be a key element of CLC’s performance, and contributed around 60% of total business volumes once again. In addition to a lean management style that this model facilitates due to its cost efficacy, the strength of these partnerships also inspires us to reach higher, and extend our island wide reach.

Our financial products mainly benefit the micro sector of the economy and the small to medium scale entrepreneurs. And brand CLC has become a household name in the multitude of rural and semi urban locations we operate in. This has enabled CLC to become an integral part of the empowerment and enrichment of these communities. We will intensify our focus in these micro and SME sectors in the next few years and capitalize on the numerous opportunities that still remain untapped. Our branch network and the “Business Introducer” channel would continue to be a key conduit for this strategy in the next few years.

We also plan to expand products such as factoring facilities for working capital into markets which are yet to have seen these products.

The synergies that we enjoy from the combination of being a member of the LOLC Group and the value of the CLC brand as a trusted and preferred brand in the micro and SME market, will continue to be a key strength which we will leverage on.

AppreciationI would like to convey my sincere appreciation to the Chairman and the Board of Directors, and my colleagues on the management team for their vision, unstinted support and guidance, and for the confidence placed in me.

My sincere appreciation to our entire team of employees, for demonstrating that the dedication, commitment and loyalty of a company’s human resource is the greatest asset that it can have. Surpassing the many milestones as we did this year, would not have been possible without the passion and initiative of this team of over 500 individuals. The challenges that came with these transitions were met successfully and swiftly enabling a seamless transition; and the team is now geared to capitalize on the numerous opportunities that we foresee.

The confidence and trust amongst our customers, business partners and other stakeholders, in our dependability and stability have been significant factors that have contributed to our performance, and the strength of the CLC brand during its 24 years in business. I would like to extend my sincere appreciation to them. And the enhanced scope of our company in the year ahead will help further strengthen these relationships.

Krishan ThilakaratneDirector/Chief Executive Officer

10 Commercial Leasing & Finance Ltd. Annual Report 2011/12

Dear Shareholder,Commercial Leasing & Finance Ltd (CLC) reports yet another remarkable performance in an year in which it also surpassed several other milestones.

The company’s performance is adequately discussed in the Chairman’s and CEO’s Reviews. In my message I would like to emphasise on the key performance s the Company achieved during the reported period.

The year under review saw another record performance with the highest ever profits in the company’s history. The vibrant growth it has achieved in its portfolio in the year under review is a result of many factors. Amongst the most significant is the success of CLC’s “Business Introducer” model, which has been able to reach areas and people which probably financial institutions have been unable to, spanning the many rural and semi urban localities of the country. Since the company’s inception 24 years ago, it has recorded steady growth built on a brand name which has earned the loyalty and trust of a customer base of over 40,000; and the growth achieved since 2008 has been particularly significant with 227% increase in net lending portfolio.

The company has added a reason to feel rewarded, as its consistently high performance stands as testimony to its approach to business and to the values it holds high; that a sustainability of a business must go hand in hand with the sustainability of the larger communities which it is part of. This value is fundamental to CLC’s business strategy which focuses on the micro and lower end of SME sectors of the economy who otherwise have limited access to formal sources of credit. The company will continue to focus on these sectors in which it sees much untapped potential. It will also further strengthen its focus on the Northern and Eastern provinces of the country where an economic revival since the dawn of peace, offers much potential for growth, not just for your company but for the collective benefit of the country.

Message from the Director

DirectorCommercial Leasing & Finance Ltd.

The success of CLC is its people, who with their own unique sense of passion have contributed to its performance

11Commercial Leasing & Finance Ltd. Annual Report 2011/12

The need for good governance in a financial enterprise can never be overstated. Whilst CLC’s association with leading international funding agencies is an endorsement of its stability and good governance, these relationships also provide opportunities for CLC to frequently enhance and adopt the state of the art best practices. Some of the measures practiced at CLC to ensure collective instead of individual decision making and facilitate greater transparency and accountability include the several committees such as the Audit Committee, the Assets & Liabilities Management Committee, the Internal Risk Management Committee and the IT Steering Committee, all of which meet regularly and play an active role. Senior management meetings are held frequently.

Risk management has been a priority area in the company’s strategy and this is reflected in an excellent Non Performing Loan (NPL) ratio of 2.8%,achieved during the year, and which is well above the industry average.

Strengthened by its past successes and re-energised by the broadened scope as a finance company, CLC is well poised for sustainable growth by capitalising on the many opportunities in the micro and SME market in the years ahead. Sound management and a visionary strategy will continue to be key factors in its future performance.

AcknowledgementsI would like to convey my sincere thanks to our Chairman for his leadership and unstinted support and to my colleagues on the Board for their constant guidance and support. My sincere appreciation also extends to all employees of CLC whose commitment and work ethic has made the many significant achievements possible. My gratitude also extends to the regulatory authorities, customers, business partners and all other stakeholders of the company for their vital contribution to CLC’s success.

Kapila JayawardenaDirector

12 Commercial Leasing & Finance Ltd. Annual Report 2011/12

Board of Directors

1. Mr. I C Nanayakkara Chairman/Non-Executive Director

2. Mr. W D K Jayawardena Non-Executive Director

3. Mrs. K U Amarasinghe Non-Executive Director

4. Mr. P D J Fernando Senior Independent Non-Executive Director

5. Dr. H Cabral, PC Independent Non-Executive Director

6. Mr. D M D K Thilakratne Director/Chief Executive Officer

7. Miss. C S Emmanuel Company Secretary

1

3

5

7

2

6

4

13Commercial Leasing & Finance Ltd. Annual Report 2011/12

Board of Directors’ Profiles

Mr. I C NanayakkaraMr. Ishara Nanayakkara is an astute businessman who holds directorial positions in many corporates and conglomerates in Sri Lanka.

He ventured into the arena of financial services with the strategic investment in Lanka ORIX Leasing Company PLC. He was appointed to the Board of CLC in June 2008 and was appointed as Chairman in January 2012. Today, as Deputy Chairman of LOLC Group, he straddles a conglomerate that encompasses financial services, agriculture and plantation, leisure, renewable energy, construction, manufacturing and trading.

Mr. Nanayakkara has extensive exposure in both banking and non-banking financial sectors through his involvement in Lanka ORIX Leasing Company PLC, Lanka ORIX Finance PLC and Seylan Bank.

His interest in microfinance is evident through his recurrent contribution to PRASAC – the largest microfinance Company in Cambodia and in his own initiative, LOLC Micro Credit Ltd - the only regulated private sector microfinance institution with foreign equity in Sri Lanka.

His passion for renewable energy is reflected through the green portfolio of the LOLC Group - comprising hydro power, solar power, agri waste and bio-mass – a promising source of alternate energy. The green investments of the LOLC Group companies are poised to offer their share to the environment.

Mr. Nanayakkara is also conversant in sustainable forestry and plantation through group companies - Maturata, Pussellawa and Gal Oya Plantations. The addition of Agstar Fertilisers Ltd, a leading agri input provider in the country, have further enhanced the Group’s contribution to the agriculture and plantation sectors.

The participation in Sierra Constructions (Pvt) Ltd, one of the largest construction companies in the country, is timely, considering the contribution of the construction sector to the post war development.

Mr. Nanayakkara is focused on the opportunities presented by the leisure sector. With the recent acquisitions of some of the leading hotels in the Southern Coast alongside key properties in the North and East, development plans are underway for the leisure subsidiaries of LOLC Group – Eden Hotel Lanka PLC, Riverina Hotels PLC, Palm Garden Hotels PLC, Tropical Villas (Pvt) Ltd and Dickwella Resorts (Pvt) Ltd.

He is also involved at strategic level in Browns Group of Companies, a conglomerate with leading market position in trade, leisure, manufacturing, consumer appliances and agriculture equipment.

He holds a Diploma in Business Accounting from Australia.

14 Commercial Leasing & Finance Ltd. Annual Report 2011/12

Mr. W D K JayawardenaMr. Kapila Jayawardena was appointed as a Director of the Company in June 2008. He holds a MBA in Financial Management, is an Associate of the Institute of Cost and Executive Accountants and was awarded Fellowship of the Institute of Bankers (IBSL) in 2006.

He has varied experience in the fields of Banking, Audit, Relationship Management, Corporate Finance, Corporate Banking, Investment Banking and Treasury Management.

Mr. Jayawardena was appointed as the Chairman of the Sri Lanka Banks Association (SLBA) in 2003/04 and served as President of the American Chamber of Commerce in Sri Lanka in 2006/2007.

He served as a Director of Lanka Clear, National Institute of Business Management (NIBM) and The Institute of Bankers (IBSL).

Mr. Jayawardena was appointed to the Financial Sector Reforms Committee (FSRC) by the Prime Minister and was a member of the Finance Sector and Capital markets cluster of the National Council of Economic Development (NCED). He was a key member of the inaugural sovereign rating team and sovereign debt for Sri Lanka appointed by the Governor of the Central Bank.

He was presented with the prestigious Combined Support Group Award by the US Navy for services rendered after the Tsunami in 2005. The Government of Sri Lanka appointed him to the Board of the Sri Lanka Fulbright Commission in 2010.

Mr. Jayawardena was appointed to the Council of the National Chamber of Commerce of Sri Lanka on 27th January 2011.

Mr. Jayawardena has over 27 years experience in all areas of banking, out of which 9 years in the capacity of CEO/Country Head Citibank Sri Lanka and Maldives. He was the first Sri Lankan to be appointed as a Senior Credit Officer (SCO) by Citi Bank in Sri Lanka. During his leadership Citi Bank in Sri Lanka was rated AAA by Fitch Rating in Sri Lanka. Citi Bank Sri Lanka was the first foreign Bank to obtain an AAA rating.

Mr. Jayawardena is also the Chairman of Lanka ORIX Finance PLC, LOLC Insurance Co Ltd, LOLC General Insurance Ltd, LOLC Life Insurance Ltd, LOLC Leisure Ltd, LOLC Motors Ltd, LOLC Securities Ltd, Speed Italia (Pvt) Ltd, United Dendro Energy (Pvt) Ltd, Palm Garden Hotels PLC, Riverina Hotels PLC and Eden Hotel Lanka PLC.

He is the Group Managing Director/ CEO of Lanka ORIX Leasing Company PLC and serves on the Board of LOLC Micro Credit Ltd. Mr. Jayawardena is also a Director of HDFC Bank and Brown & Company PLC.

Board of Directors Profiles contd.

15Commercial Leasing & Finance Ltd. Annual Report 2011/12

Mrs. K U AmarasingheMrs. Kalsha Amarasinghe was appointed to the Board of Directors in June 2008. She holds an Honours Degree in Economics.

She serves on the Boards of Lanka ORIX Finance PLC, LOLC Insurance Co Ltd, LOLC General Insurance Ltd, LOLC Life Insurance Ltd, LOLC Leisure Ltd, LOLC Securities Ltd, Speed Italia (Pvt) Ltd, United Dendro Energy (Pvt) Ltd, Palm Garden Hotels PLC, Riverina Hotels PLC and Eden Hotel Lanka PLC.

Mr. Priyantha FernandoMr. Priyantha Fernando was appointed to the Board of CLC on 30th March 2012.

Mr. Fernando has more than 35 years of experience at the Central Bank where he rose to the position of the Deputy Governor. He was the Deputy Governor of the Central Bank in 2010-2011, in charge of Financial System Stability and the Corporate Services clusters. Mr. Fernando has extensive experience and expertise in the fields of Banking and Financial Sector particularly at the policy making levels in financial regulation and supervision, information technology, national accounting, macro-economic analysis and statistics and finance and fund management. At the Central Bank he was the Chairman of the Financial Stability Committee, member of the Monetary Policy Committee, member of the Risk Management Committee, Chairman of the National Payment Council. He also functioned as the Secretary to the Monetary Board during 2009/2010.

He was an ex-officio board member in several regulatory organisations, namely the Securities & Exchange Commission, the Insurance Board of Sri Lanka, the Chairman of the Credit Information Bureau, Institute of Bankers - Sri Lanka and have also served as a Board Member at Employers Trust Fund, Lanka Clear (Pvt) Ltd and Lanka Financial Services Bureau.

During his career he has initiated and spearheaded several key projects of national importance, especially in the area of developing the infrastructure for the national payments and settlement system.

Mr. Fernando has served a number of committees at national level covering a range of subjects representing the Central Bank.

Currently he serves on the Boards of Union Bank PLC, Taprobane Holdings Ltd and Hambana Petrochemicals Ltd., as an Independent Non-Executive Director.

Dr. Harsha Cabral, PCDr. Harsha Cabral was appointed to the Board as an independent Director in December 2011. He is a President’s Counsel and holds a PhD in Corporate Law (University of Canberra) Australia. Dr. Cabral is a Senior Counsel in Corporate Law with twenty four years experience, specialising in Company Law, Intellectual Property Law, Commercial Law, International Trade Law & Commercial Arbitration.

16 Commercial Leasing & Finance Ltd. Annual Report 2011/12

Board of Directors Profiles contd.

He serves as a Commissioner, Law Commission of Sri Lanka. He is a Member of the Advisory Commission in Company Law, Sri Lanka (key member in drafting the new Companies Act No. 07 of 2007), NCED (National Council for Economic Development –Legal Cluster) Sri Lanka, Ministerial Committee appointed to reform the Law on Commercial Arbitration. He is a Council member of the University of Colombo, member of the Board of Studies - the Council of Legal Education in Sri Lanka, member of the Academic Board of Studies of the Institute of Chartered Accountants of Sri Lanka and a member of the Corporate Governance Committee of the Institute of Chartered Accountants of Sri Lanka.

He is currently serving on the boards of Diesel & Motor Engineering PLC (DIMO), Union Bank of Colombo PLC, Richard Pieris & Co. Distributors Ltd., Tokyo Cement Company (Lanka) PLC, Tokyo Super Cement Co (Private) Ltd., Fuji Cement Co (Lanka) Ltd, Tokyo Cement Power (Lanka) Ltd, Hayleys PLC, Hambana Petrochemicals Ltd, and Lanka ORIX Finance PLC.

Dr. Cabral is the Course Director of University of Wales – IALS – LLM Programme, a lecturer & examiner of University of Wales-UK, University of Colombo & Sri Lanka Law College, Council member/faculty member of Institute for the Development of Commercial Law & Practice, a lecturer & examiner, Post Graduate Diploma in Advanced Corporate Law, Institute of Advanced Legal Studies, Sri Lanka Law College and the Vice President of Business Recovery & Insolvency Practitioners Association of Sri Lanka.

He is the author of several books on Company Law & Intellectual Property Law.

Mr. Krishan ThilakaratneMr. Krishan Thilakaratne was appointed to the Board on 6th March 2012. He is an Associate Member of the Institute of Bankers of Sri Lanka (AIB) and joined the LOLC Group in 1995. He counts over nineteen years of experience in Banking, Credit, Leasing, Factoring and Branch Management.

He is the CEO of the Islamic Business Unit of Lanka ORIX Finance PLC. He has held the position of CEO of Lanka ORIX Factors Limited and CEO of Auto Finance of Lanka ORIX Leasing Company PLC previously.

He also serves on the Boards of Commercial Insurance Brokers (Pvt) Ltd and Commercial Factors Limited .

Miss. C S Emmanuel (Company Secretary)Miss. Chrishanthi Emmanuel is a Fellow of the Institute of Chartered Secretaries and Administrators - UK and a Fellow of the Institute of Chartered Corporate Secretaries (Sri Lanka).

She is Company Secretary of most subsidiaries within the LOLC Group. She is also Secretary of the Leasing Association of Sri Lanka.

17Commercial Leasing & Finance Ltd. Annual Report 2011/12

Management Team

1. Jude Anthony - Assistant General Manager - Branch Network2. Nihal Weerapana - Deputy General Manager - Recoveries3. Nishanthi Kariyawasam - Assistant General Manager - Finance4. Lasantha Peiris - Chief Manager - IT Operations5. Dharsha Abeyawardena - Manager - Savings & Fixed Deposits6. Dishan Obeysinghe - Manager - Asset Backed Finance7. Upul Samarasinghe - Chief Manager - Credit8. Prasanna Dayaratne - Chief Manager - Customer Service9. Deepamalie Abhayawardane - Assistant General Manager - Factoring10. Pradeep Uluwaduge - Head of Human Resources and Administration11. Tharanga Indrapala - Chief Manager - Operations

1

6 7 8 9 10 11

2 3 4 5

18 Commercial Leasing & Finance Ltd. Annual Report 2011/12

3.2BnProfit Before Tax

26Bn

Ass

et

Base

6.6BnShareholders Funds

19Commercial Leasing & Finance Ltd. Annual Report 2011/12

The EnvironmentSri Lanka’s economy sustained its high growth momentum surpassing last year’s record high to grow by 8.3% in 2011. This high pace of economic growth combined with subdued inflation, at mid single digit levels and low interest rates in 2011 provided an ideal environment for business. The rapid pace of expansion resulting in high demand for credit, fuelled significant growth in the Listed Finance Companies (LFC) sector during the year. The country’s financial stability continued to be strengthened, thereby supporting the growth momentum despite the uncertainties in global prospects and turbulence in international financial markets. In the low interest regime, credit growth accelerated during the year and the performance of financial institutions improved with enhanced growth in assets, healthy profitability, higher capitalization and lower risk levels.

The regulatory and prudential framework governing the financial system was strengthened, facilitating greater investor confidence and safeguards. The key reform during the year was the new “Finance Business Act” which aims at further strengthening the regulation of finance companies by enhancing powers to combat unauthorized deposit-taking and finance business activities. It also introduced new requirements for capital adequacy and liquidity for finance companies. In order to comply with the requirements of this new regulatory regime, CLC listed 10% of its shareholding in the Colombo Stock Exchange thereby becoming a Public Listed Company in June 2012.

Key ContributorsThe most significant landmark during the year was the enhancement of the company’s business scope from a specialized leasing company to become a full fledged finance company. Thus, Commercial Leasing was renamed as Commercial Leasing & Finance during the year. And it is a noteworthy achievement that CLC was able to launch into deposit taking within a month of being registered as a finance company.

The credit team’s role in the company’s performance is a vital one, and more so in the case of CLC which focuses on the micro and SME sectors in the country. In addition to developing an appropriate and a balanced credit policy, the team also played a key role in training marketing personnel across the company, thus facilitating a higher portfolio quality and credit standards at CLC.

MD

&A

Management Discussion & Analysis

A customer centric approach permeates our culture

20 Commercial Leasing & Finance Ltd. Annual Report 2011/12

The performance of CLC’s recoveries has also been a key element of the company’s performance. The Non Performing Loan (NPL) ratio during the year was amongst the industry best, at 2.8%. And this achievement is made all the more significant in the context of the high portfolio growth during the period; indicating that the quantum increase in the portfolio was without compromise on quality. This achievement also reflects the sound credit policies, operational excellence, and the commitment, dedication and market knowledge of our staff across all departments.

The company continually reviews and enhances its operations, and is guided by the principle that achieving operational excellence must be without compromise on the quality of customer service. We are in fact ever mindful that our operations must be geared to providing an excellent service to our customers. Towards this end, the Operational Manual is regularly reviewed and adapted to meet changing needs and trends.

Information Technology (IT) is a vital cog that moves our enterprise in today’s market. We have invested in world class IT infrastructure and systems that support our business model. The co-banking system in use supports assets and liabilities of our business and is well integrated.

With a customer centric approach that permeates our corporate culture, the company’s marketing strategy is designed to develop brand CLC and to support our business channels. The marketing communication team played a particularly significant role during the year just ended, in creating market awareness of the transition to a finance company, and more specifically, in the launch of savings and fixed deposits. The seamless transition that we were able to make into this new role of a finance company and the wide market acceptance received within a very short span, stand as testimony to the success of our marketing strategy and effort.

The Factoring BusinessSri Lanka’s Factoring industry, in line with other sectors of the economy, continued on the high growth trend of the previous year, recording a 76% growth during the year just ended.

Commercial Factors, which has been a pioneer in the factoring industry, during the year under review was amongst the two best performers in the sector. Along with the significant growth of the factoring portfolio CLC managed to secure more clients during the year. The increase in active clientele by 32% reflected the high demand for working capital and related solutions, in an environment of high growth and low interest rates. Our strategy and service standards were key factors in this performance. Trading and Manufacturing sectors accounted for a majority of the business and the Services sector contributed the remainder.

CLC, which pioneered the offer of Factoring services outside the traditional urban and semi urban areas of Western Province, will continue to strengthen its presence and expand further into rural markets. During the year under review, two branches dedicated for factoring and working capital products were opened in Kandy and Matara to offer an enhanced service to our clients in the Central and Southern Provinces respectively.

We continued to innovate by structuring customized facilities to meet the different working capital needs of clients. The product mix offered by CLC included Domestic Recourse Factoring, Invoice Discounting, Sales Ledger Administration, Debt Collection and Cheque Discounting,- to enhance factoring services in the SME sector in particular.

We see factoring as a sound alternative to bank overdrafts, and combined with its added feature of portfolio management, the potential for the factoring industry in Sri Lanka is immense.

Management Discussion & Analysis contd.

21Commercial Leasing & Finance Ltd. Annual Report 2011/12

StrategyThe key focus area of our financial products continued to be the micro and SME sectors of the economy. We will continue to intensify our focus on these sectors, which have tremendous potential still to be tapped.

CLC’s "Business Introducer" model continued to be a significant conduit for its strategy, accounting for over 60% of the business. The company will continue to build on the strength of this model for future expansion and growth. In addition to the cost effectiveness of this model, the lean management structure it facilitates also supports CLC’s ability to be nimble in responding to market changes.

The synergies we enjoy, from being a member of the LOLC Group since 2008,combined with the customer loyalty and trust that brand CLC has earned during its 24 years in the leasing market, will continue to be key advantages in capitalising on the many opportunities we foresee.

Our ReachCLC continued its strategy of volume growth, and expanded its distribution channel, opening 8 new branches and 2 post office window counters during the year. This brings the total number of island wide branches to 50. The milestone 50th branch was opened in Killinochchi bringing the total number of CLC’s branches in the North and East of the country to eight, reflecting our commitment to contribute to the post war socio economic resurgence in these areas by fulfilling a need for financial solutions.

Our PeopleThe year under review saw your company surpass several significant milestones, for which kudos must go to our team of 511 employees. The success we achieved during the year reflects our belief that a company’s most valuable asset is the commitment, ability, passion and the dedication of its human resource. A belief made more real by the fact that our company is in the service sector where the intangibles of service provides a vital competitive edge.

Our training and development initiatives include continuous training as well as need based training. Continuous training involves providing training programmes regularly to motivate individuals, create the appropriate culture, build leadership skills and enhance knowledge and skills. Training programmes carried out during the year under review included several “Induction & Orientation” programmes which enabled new recruits to adapt easily to the culture of CLC.

As an enterprise engaged in providing Financial Services, the quality of service delivery is also an area of emphasis in our training and development, and more so because of the excellence we strive for at CLC. And combined with the technical know how of our people, our service quality has been a key factor in the strong relationships we have built; and the trust and confidence we have earned amongst all our stakeholders. Building relationships with rural customers requires a paradigm shift in modern customer relationship management, requiring our staff to grasp the hopes and aspirations of the economically disadvantaged and the cultural nuances of each locale and community, whilst being cognizant of their inherent pride and dignity. Our staff have hence developed the ability to empathize and speak the same language as our customers who hail from different socio economic backgrounds.

A culture sans hierarchy is actively promoted within the company. We believe that employees must be provided an environment in which they can give their best to the organization whilst reaching towards their own potential. A merit based work place ensures professionalism and

34

177

300

Staff Grade Wise

Managerial

Executive

Clerical

22 Commercial Leasing & Finance Ltd. Annual Report 2011/12

has also served to engender a new mind set. A clear career path, succession planning and performance based remuneration are key elements which has enabled CLC to become a preferred employee, as reflected in the high staff retention ratio of 87%. This is a noteworthy achievement, in a highly competitive industry which has seen many new entrants into the business over the past few years.

Moreover, CLC also has one of the youngest set of employees in the industry with more than 50% of staff under thirty years of age. A formal succession planning for the company enables the grooming and developing of employees, whilst career planning at individual level encourages employees to reach their potential. Performance evaluation methods are carried out in a transparent manner and the best performing employees are recognized and rewarded fittingly.

The cadre at CLC grew by 18.84% to 511 during the year under review, mainly due to an increased demand at branches. This comparatively slower rate of growth vis a vis the previous year’s of 87%; reflects the company’s increased focus on quality and a search for the “right attitude” when recruiting.

We firmly believe that the sustainability of our human resource is not merely about the monetary rewards which are commensurate with performance; but it also has much to do with satisfaction levels which are linked to the corporate culture, spirit of camaraderie, opportunities for recognition, personal development and fellowship. Some of the informal channels at CLC that facilitate a team spirit include the annual CLC sports day – a much looked forward to event which brings together employees from head office and the fifty branches. CLC’s Sports Club sponsored by the company, plays an active role in employee recreation, and also participates in mercantile cricket, football, rugby, badminton and athletics. CLC is also a popular participant at the Annual Mercantile Quiz contests organized by the Banking and Finance sector institutes. Our people philosophy supported by new systems and processes will continue to attract, develop and build a pool of talented, dynamic and a motivated human resource base with the right competencies that will be a key driver of the company’s sustainable growth in the years ahead.

1043

275183

Age Analysis

20-30

30-40

40-50

Above 50

Management Discussion & Analysis contd.

23Commercial Leasing & Finance Ltd. Annual Report 2011/12

Our Outreach

CLC BranchesPost Office Service CentersSpecialised Factoring Branches

Matara

Galle

Ambalangoda

Pitigala

Udugama

Embilipitiya Tissamaharama

Kalawana

Ratnapura

Welimada Monaragala

BadullaNuwara Eliya

Ampara

Baduraliya

Kalutara

NugegodaMaharagama

AvissawellaKaduwela

Gampaha

WarakapolaKandy

Kalmunai

Batticaloa

Bakamoona

Dambulla

Polonnaruwa

Nochchiyagama

TrincomaleeKebitigollewa

Anuradhapura

Medawachchiya

Vavuniya

Parakramapura

Nelliady

Jaffna

Kilinochchi

Kurunegala

Puttalam

Matale

Wennappuwa

Kelaniya

Negombo

Kuliyapitiya

PettahBambalapitiya

24 Commercial Leasing & Finance Ltd. Annual Report 2011/12

Financial Review

OverviewThe Company concluded an extremely successful year in achieving both objectives of top line and bottom line contribution results. Main strategic contributory factors for better performance were the rapid expansion in the island wide reach, concentrated efforts on improving the service delivery to the different customer segments of the Company and maintaining and strengthening the brand of the Company.

The name of the Company was changed to Commercial Leasing and Finance Ltd. after obtaining approval from the Central Bank of Sri Lanka (CBSL) to function as a Finance Company. Keeping in line with the CBSL requirements to list the Company, an application was made with the Colombo Stock Exchange for listing which was accepted and the Company shares were traded after the financial year end.

RevenueTotal revenue of the Company reached Rs.5,245 Mn compared to Rs.3,402Mn last year. Revenue includes interest income from leasing, hire purchase, loans, factoring income and operational income such as interest on overdue rentals, profit on contracts terminated etc.

The growth in profits was a direct result of the increase in interest and operational income which grew by 54% to reach Rs. 5,245Mn. The factoring business of the Company, ComFactors too contributed to the increase in interest income with 73% growth over the last year to end at Rs. 795 Mn. Other operating income increased by 1155% mainly due to the profit on sale of subsidiary.

Interest expenseIncrease in borrowings to fund the additional volume growth together with rising market interest rates have caused an increase in interest expenses for the year to Rs. 2,167Mn from Rs.1309 Mn, an increase of 66% over the previous year.

Operating expensesThe operating expenses of the Company increased supporting the growth in the business and expansion of the footprint throughout the island. The resultant increase in total overheads by 37% from Rs.1,530Mn to 2,093Mn. However, these increases in expenses did not negatively affect the

The Company concluded an excellent year of financial performance and further strengthening of the balance sheet

Lea

sing

0

2,000

250

500

1,000

1,500

Rs. Mn

Hire

pur

cha

se

Fac

torin

g

Oth

er l

oa

n

Inte

rest

on

ove

rdue

rent

als

Hire

rent

al

Interest Income

2011

2012

25Commercial Leasing & Finance Ltd. Annual Report 2011/12

performance of the Company, clearly demonstrating the low cost model of the Company with a superior cost to income ratio of 20%. The Company made additional provisions over and above the CBSL requirement, providing an additional Rs. 96Mn on account of bad and doubtful debts.

TaxationThe Company paid Rs.85Mn as VAT on financial services and provided Rs.205Mn as income taxation. The deferred taxation provision made in the financials amounts to Rs. 57Mn.

ProfitabilityThe Company recorded an impressive growth in profit before tax of Rs. 3,182Mn for FY 2011/12 up from Rs. 741 Mn in the previous year. Company’s profit after tax Rs. 2,920 Mn. These profits were achieved by strategic expansion of its core business of lending and effective management of the borrowing costs and operating expenses.

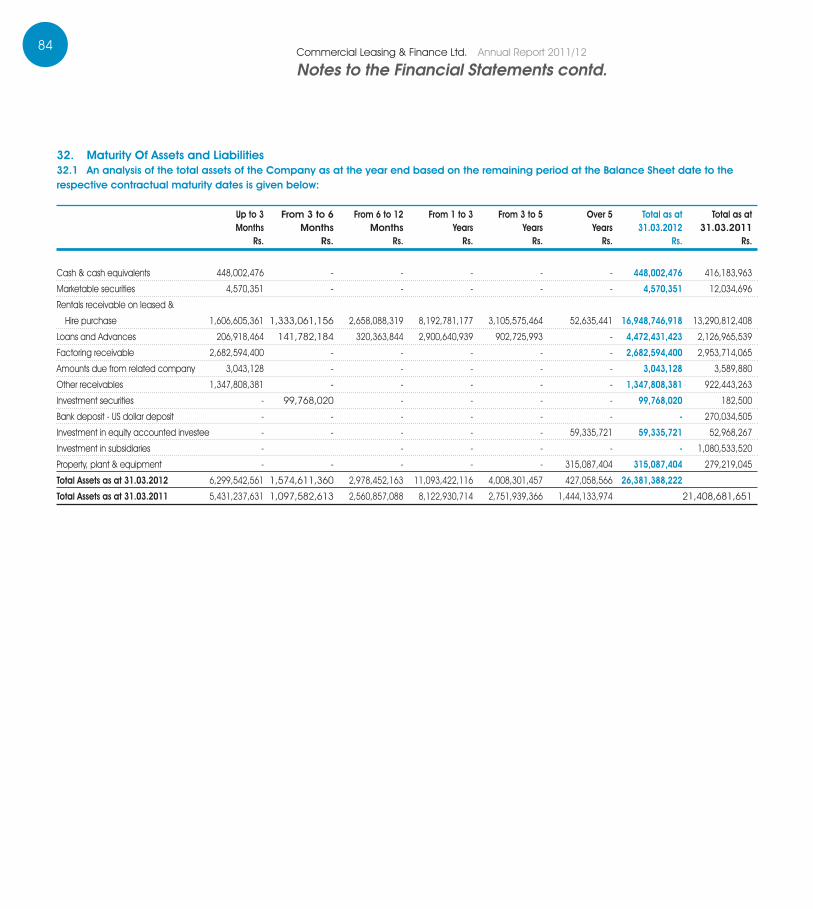

Asset growthThe total assets reached Rs. 26,381 Mn from Rs. 21,408 Mn last year which is an increase of 23%. The lending portfolio including factoring recorded steady growth over the year increasing the portfolio from Rs. 18,371Mn to Rs. 24,104 Mn. This was a growth of 31%.

BorrowingsTotal borrowings of the Company increased to Rs.17,649Mn from 15,833Mn supporting the portfolio growth and business expansion. The Company enjoys a rare benefit of having a wide range of multilateral and bilateral funding agencies as a result of the parent company’s long standing relationship with these institutions. During the year, the Company secured US$ 17Mn new foreign borrowing from foreign funding partners. These funding comes at attractive long term rates which helps the Company to maintain a healthy level of cost of borrowings. The Company policy is to have a zero foreign exchange risk with 100% hedging on all foreign borrowings which safeguards the Company against the foreign exchange fluctuations prevailed during the year. This policy is aligned to the mandate given by the CBSL of zero exposure to exchange risks on foreign borrowings.

Non performing loans and advancesThe Company’s collection efforts provided a strong backing to achieve this superior financial performance with the non-performing loans being contained at a ratio of 2.8%, which is one of the best NPL ratios in the industry. The provisions made on account of bad and doubtful debts were strengthened with additional provisions of Rs. 96 Mn being made over and above the Central Bank of Sri Lanka (CBSL) requirements.

Deposit baseSubsequent to receiving the approval of the CBSL to canvass public deposits, the Company launched its deposit mobilising campaign towards the latter part of the year and within three months of savings and fixed deposits operations, the Company was able to mobilise Rs.385Mn as deposits.

The Company concluded an excellent year of financial performance and further strengthening of the balance sheet. The Company’s strategies are well defined and carefully executed to further strengthen the financial position of the Company, which will enhance overall value to all the stakeholders.

2007

0

30,000

25,000

5,000

10,000

15,000

20,000

Rs. Mn

2008

/09

2009

/10

2010

/11

2011

/12

Total Assets to Net Lending Portfolio

Net portfolio

Total assets

26 Commercial Leasing & Finance Ltd. Annual Report 2011/12

Risk Management

Enterprise Risk Management at LOLC group is a centralised operation and the Group level mechanisms, models are replicated for Commercial Leasing & Finance PLC as in the case of other subsidiaries. The following is an extract of the Enterprise Risk Management Review for the LOLC Group which was published in the Group Annual Report. The Risk Profile has been amended to depict the entity level position of CLC.

Risk Management with a VisionWith the vision of creating an organisational culture where protection, assurance, reliability, accountability, transparency and confidentiality are treasured as lasting values, We consider all employees, including the Board of Directors, as risk managers within the scope of their respective functions.

We define risk as any circumstance or event that might hinder the achievement of stated corporate objectives. This definition helps all members of the CLC team to focus on identifying material, minor or even isolated process level risks. It also allows us to identify potential issues at source, enabling us to formulate controls and strategies to align risk with our risk appetite.

The Risk Management FrameworkThe LOLC Group risk management framework permits active synergies between risk management, compliance, internal audit and information systems audit functions under the umbrella of the Group Enterprise Risk Management (ERM) Division, ensuring that risk is a consideration with respect to all operational functions.

Action is guided by the Group risk management policy. Dedicated officers are appointed within the risk management function for each subsidiary in which the Parent Company has a material stake. These officers report to the Chief Risk Officer (CRO). The ERM process retains total independence from other business functions, with the CRO reporting to the Chairperson of the Board through the Integrated Risk Management Committees (IRMC) of every major Group company. These Committees are constituted from an appropriate mix of Independent Directors, Executive Directors and Management Personnel.

Each IRMC evaluates the identified risks that are relevant to it. Group level risks are escalated to the Parent Company IRMC and the Board. The process is simplified by adopting common risk policies across the Group, retaining uniformity and avoiding policy conflict. Risk information is held centrally at Group level, with reporting lines to Group ERM from each subsidiary. Additionally,

LOLC takes a defence-in-depth approach in responding to risk

27Commercial Leasing & Finance Ltd. Annual Report 2011/12

every regulated subsidiary has its own appointed compliance officer for better focus on the diverse regulatory compliance requirements of each. The Group ERM Division enjoys unrestricted access and auditing rights over all major subsidiaries of the Group.

Despite our broad presence at grass roots level across Sri Lanka, support services of the Group are managed centrally. In order to capture vital risk information, reporting lines run to Group ERM from every business unit and branch. Tactical level operations are governed by well-defined policies and procedures, which once approved by the Board, are owned and protected by Group ERM. Any changes to operating policy or procedures are reviewed for adequacy with respect to internal controls. Internal Audit reviews compliance and the currency of rules when a function is audited.

Accountability and a focus on supervisory functions are maintained by the annual issue, by the heads of each business unit, of certificates testifying compliance with internal controls, with all material exceptions reported. Internal audit also conducts an annual compliance test on key and material controls relating to financial reporting.

Propagating Awareness and Understanding of RiskAll Group employees undergo training on risk management at induction, while training programmes on risks relating to specific functions are conducted periodically by Group ERM. Should internal audit report a lack of awareness or increased frequency of non-compliance in a certain function or business unit, Group ERM mandates awareness building and training sessions, which are conducted in collaboration with the respective unit and the Human Resources Division.

How We Identify RiskThe inherent risk of risk management lies in not identifying a particular risk. LOLC Group practises a three-tier risk identification methodology to help minimise this danger. The three tiers consist of separate assessments by the risk owner, by stakeholders and finally an independent assessment by LOLC Group ERM. This process is augmented by a “whistle-blowers’ hot line” whose users enjoy full privacy and confidentiality.

Customers are often the first to detect irregular practices or process efficiency bottlenecks, and they are encouraged to report them to Group ERM using our customer feedback line. Information received is acted upon and followed up until resolution. This practice has greatly helped us in streamlining our processes and procedures, increasing both effectiveness and control.

Supplementing the operational monitoring mechanisms established by business and service units of the Group are compulsory reporting requirements on risk for each unit, as well as field audits by the Group’s Internal Auditors. Anti-money laundering precautions and ‘know your customer’ rules are embedded in all contract and transaction processes, with centralised monitoring by Group compliance officers.

28 Commercial Leasing & Finance Ltd. Annual Report 2011/12

Defence-in-DepthLOLC takes a defence-in-depth approach in responding to risk. Within the policy and procedural frame work, the first line of defence relies on the risk awareness, skills and knowledge of line staff with respect to their particular functions. The second line of defence is formed by management supervision, embedded information systems and application controls. Risk detection and response may also result from reviews conducted by the internal monitoring functions of each business unit as well as from periodic internal and IT audits. Finally, Group ERM has the mandate and capacity to conduct forensic audits and investigations, including the integrity of our IT platform, if the need arises.

Internal audit adopts a four-step follow-up process on action to mitigate risk. It consists of:1. Confirmation by the risk owner that the weakness identified by internal audit has been

rectified.2. Follow up review on the effectiveness of rectification by internal audit.3. Control self-assessment by the risk owner, under the guidance of Group ERM.4. Follow-up by internal audit based on this self-assessment.

Capacity Building and Quality Management for ERM StaffERM staff possess a diverse array of knowledge and skills covering the entire gamut of operations of the LOLC Group. They are kept updated through continuous training and education. A broad and comprehensive educational resource base, managed by Group ERM, is in frequent use by risk officers as well as Internal Auditors.

Reaching for ExcellenceIn this uncertain world, the complete elimination of risk is impossible. However, we believe there is no limit to continuous improvement in effective risk management. All our risk management processes are continually reviewed and, wherever possible, improved. Internal quality management is strengthened by a rating system adopted to monitor the quality of assignments handled by department staff, and feedback received from supervisors drives further improvement.

Risk Profile of LOLCThis is a high level categorisation based on perceived risk. The table below assigns risk values based on a numerical scale:

Risk Rating ScoreVery Low 1Low 2Medium 3High 4Very High 5

Financial Risks

Asset & Liability Risk

Profitability & Income structure Risk

Capital Adquacy

Risk

Credit Risk

Liquidity Risk

Interest rate Risk

Market Risk

Currency Risk

5

4

3

2

1

0

Business Risks

Legal Risk

Systemic Risk

5

4

3

2

1

0

Industry Risk

Image RiskFinancial InfrastructureRisk

Policy Risk

Risk Management contd.

29Commercial Leasing & Finance Ltd. Annual Report 2011/12

Future ChallengesThe volatile global business environment, a variable macroeconomic outlook and the Group’s exposure to multiple industry sectors call for aggressive and effective risk mitigation strategies. This has necessitated changes in our risk management approach and the adjustment of mitigation mechanisms to meet various regulatory and business requirements. It has also created a need for robust automation to strengthen our processes.

Global RecognitionLOLC Group’s institutionalisation of good governance, risk management and compliance Practices were recognised in the year under review with a global achievement award from the Open Compliance and Ethics Group (OCEG), USA. LOLC is the first Asian business entity to receive this award.

In her congratulatory message to LOLC, Ms. Carole Switzer, President of OCEG observes: “I am writing to extend my personal congratulations to LOLC, as a recipient of the 2012 GRC Achievement Award from OCEG. The award recognises the great strides that companies, Government agencies and other organisations have made in improving and integrating their approaches to governance, risk management and compliance, to achieve principled performance”.

Although elated, we will not rest on our laurels. We are already moving to further improve and consolidate our internationally-acclaimed risk management practices.

Political Risk

Disaster Management & Business Continuity Risk

Event Risks

5

4

3

2

1

0Contagion RiskExogenous Risk

Business Strategy Risk

Operational Risks

4

3

2

1

0

5

MIS Management

&FraudRisk

InternalSystems

&Operational

risk

Technology Risk

30 Commercial Leasing & Finance Ltd. Annual Report 2011/12

Corporate Governance Report

Commercial Leasing & Finance Limited comes within the purview of the Central Bank of Sri Lanka (CBSL), as it is a licensed finance company (LFC) and also a company licensed to engage in leasing. Consequent to its listing on 5th June 2012, the Company also complies with the Listing Rules of the Colombo Stock Exchange (CSE).

As a LFC, CLC is regulated and monitored by the CBSL, which conducts periodic inspections of the Company’s records and operations. The ensuing dialogue between the Directors of the Company and the CBSL officials ensures focus and compliance on a continuing basis. The Company also reports regularly to the CBSL on various aspects of operations, including liquidity and other ratios. This facilitates transparency and accountability.

In accordance with CBSL directions, sub committees of the Board have been appointed, to facilitate a more detailed study of relevant issues, including controls.

The Audit Committee is governed by the Audit Charter establishing its duties and responsibilities in financial reporting, business risk management, internal controls, compliance with laws and Company policies, monitor performance and independence of external and internal auditors. The Committee has acted within the parameters set by its terms of reference. During the year under review the Committee reviewed the scope of internal and external audits, and the internal control mechanisms established to provide the assurance that the assets and integrity of financial reporting have been safeguarded.

The Integrated Risk Management Committee reviews credit, market, liquidity, operational and strategic risks. These risks were reviewed monthly by the Chief Risk Officer and summarised reports were submitted quarterly to the Committee for concurrence and/or specific directions in order to ensure that the risks were managed appropriately.

Relevant senior management personnel are also invited to the meetings of these board sub committees, so that the gravity of the issues and the need for swift and appropriate action are understood by all. The Minutes of all sub committee meetings are also submitted to the Board, so that all directors are aware of the discussions and decisions of these sub committees.

To the best of the knowledge of the Directors, the Company has been in compliance with all prudential requirements, regulations and laws

31Commercial Leasing & Finance Ltd. Annual Report 2011/12

In compliance with the listing rules of the Colombo Stock Exchange, a Remuneration Committee was formed to determine the broad policy framework of the remuneration of the Executive and Non-Executive Directors.

A whistle blowing policy has been introduced and the number of the related “hot line” has been publicised to all Company (and LOLC group) employees. This had been done in order to encourage employees/ customers to inform the management of deliberate deviations from controls and / or processes and procedures so that preventive/ corrective actions could be promptly taken.

The Company’s 20th Annual General Meeting of the shareholders will be held on 18th September 2012, where, as with every other AGM the shareholders are provided an opportunity to dialogue with the Board and senior management, on any aspect of the Company’s operations.

In accordance with best practices, the offices of Chairperson and Chief Executive Officer are separate, and the Chairperson is a Non-Executive Director. This ensures a balance of power and enhances accountability. To bring in a greater element of independence the Board appointed Mr. P D J Fernando as the Senior Independent Director.

The agenda of the monthly Board meetings includes reports on performance and on compliance with relevant regulations. This enables the Board to ensure that, the Company performs at an optimal level, while being fully compliant.

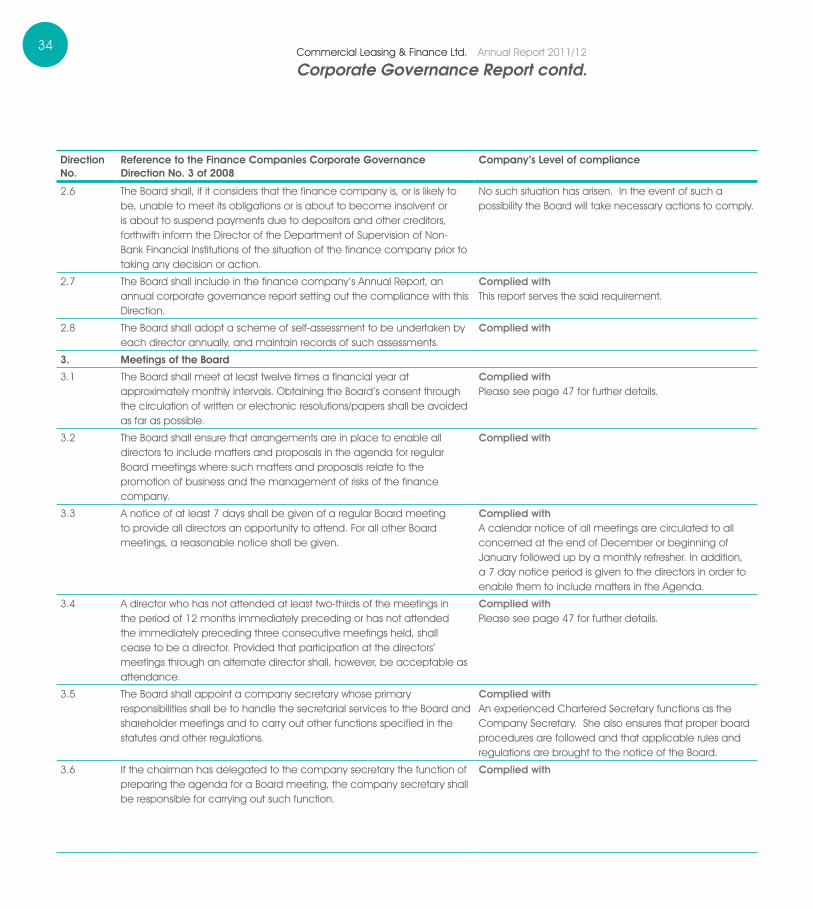

Mr. W D K Jayawardena retires by rotation and offers himself for re-election. The Board recommends his re-election. Dr. H Cabral, PC, Mr. P D J Fernando, and Mr. D M D K Thilakaratne were appointed during the year. They retire and offer themselves for re-election. The Board recommends their re-election.

In compliance with the Corporate Governance direction of the Central Bank of Sri Lanka, having reached the age limit, and at the conclusion of the transitional period, Mrs. R L Nanayakkara stepped down as Chairperson on 31st December 2011. The Board places on record its deep appreciation of her valued contribution.

There is no financial, business, family or other relationship between the Chairman and the CEO. Mr. I C Nanayakkara and Mrs. K U Amarasinghe share a family relationship. There is no financial, business, family or other material relationship between any other members of the Board.

The Directors believe that the Company is in a position to continue its operations in the foreseeable future. Accordingly the financial statements are prepared on the basis that the Company is a going concern.

The Company has obtained a certification from its external auditors, M/s KPMG, Chartered Accountants on compliance with the Corporate Governance Direction issued by the Monetary Board.

The Directors confirm that no significant deviations have been observed by the external auditors and that the Company has not engaged in any activity that contravenes any applicable law or regulation. To the best of the knowledge of the Directors, the Company has been in compliance with all prudential requirements, regulations and laws.

32 Commercial Leasing & Finance Ltd. Annual Report 2011/12

Direction No.

Reference to the Finance Companies Corporate Governance Direction No. 3 of 2008

Company’s Level of compliance

2. The Responsibilities of the Board of Directors

2.1 The Board of Directors shall strengthen the safety and soundness of the finance company by:

a. approving and overseeing the finance company’s strategic objectives and corporate values and ensuring that such objectives and values are communicated throughout the finance company;

Complied with

b. approving the overall business strategy of the finance company, including the overall risk policy and risk management procedures and mechanisms with measurable goals, for at least immediate next three years;

In view of the volatile market environment the Company has to review its strategies constantly to compensate for negative market influences. However we are now in the process of drafting a medium to long term strategy factoring in the above challenges while allowing the Company to remain flexible enough to take remedial action and also seize opportunities.

c. identifying risks and ensuring implementation of appropriate systems to manage the risks prudently;

Complied with

d. approving a policy of communication with all stakeholders, including depositors, creditors, shareholders and borrowers;

Complied with

e. reviewing the adequacy and the integrity of the finance company’s internal control systems and management information systems;

Complied with

f. identifying and designating key management personnel, who are in a position to: (i) influence policy; (ii) direct activities; and (iii) exercise control over business activities, operations and risk

management;

Complied with

g. defining the areas of authority and key responsibilities for the Board and for the key management personnel;

Complied with

h. ensuring that there is appropriate oversight of the affairs of the finance company by key management personnel, that is consistent with the finance company’s policy;

Complied with

i. periodically assessing the effectiveness of its governance practices, including: (i) the selection, nomination and election of directors and appointment

of key management personnel;

Complied withDirectors are selected and nominated to the Board for skills and experience in order to bring about an objective judgment on issues of strategy, performance and resources. Election of directors are effected in accordance with the requirements of the Companies Act No. 7 of 2007. Effectiveness of this process is ascertained by their contribution at board meetings in their respective fields. In addition a Board approved procedure for the appointment of Directors is also in place.

Corporate Governance Report contd.

33Commercial Leasing & Finance Ltd. Annual Report 2011/12

Direction No.

Reference to the Finance Companies Corporate Governance Direction No. 3 of 2008

Company’s Level of compliance

i. (contd.) (ii) the management of conflicts of interests; and (iii) the determination of weaknesses and implementation of changes

where necessary;

KMPs are selected and recruited in terms of the HR policy of the Company. KMPs directly report to the Managing Director or the Group CEO and performance appraisals are completed at least twice a year by the above Directors.

Conflicts of interest are managed on a monthly basis where directors disclose their directorships in other companies. KMPs declare any interest annually.

Weaknesses are identified from the above processes and changes may be implemented where necessary.